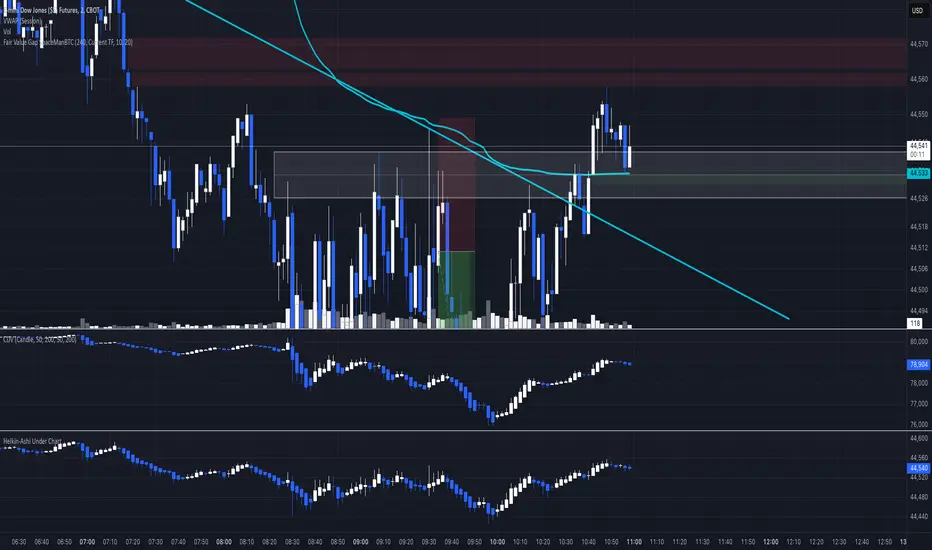

Ultimate Heiken-AshiWhy ultimate?

It's very configurable (you can select to see the candles or a line, pick the colors, switch between Heiken-Ashi and normal candles, etc.).

In addition to standard Heiken-Ashi candles, it offers the option of a new, modified calculation of the candles different than the standard Heiken-Ashi calculation.

It can work based off the existing candles of the chart or it can force working based off normal candles regardless of any non-standard candles loaded in the current chart.

It can add the Heiken-Ashi calculation (or the modified one) twice, thus intensifying the effect.

FYI, you can disable the regular bars (so that they don't overlap with this indicator) by click on the eye icon next to the ticker on the very top left of the chart.

Manage risk and enjoy!

Pine Script®指标