EMA 20+50 + MACD Strateji ( omerprıme)EASY BUY-SELL basitçe al -sat yapabileceğiniz macd indikatörü ve ema kullanılmış bir indikatördür unutmayın ki ne kadar basit o kadar verimli.

Moving Averages) to generate trading signals and trend confirmation.

Trend Identification with EMA

Two EMAs are used to determine the overall market trend (commonly a short-term EMA and a long-term EMA).

When the short EMA crosses above the long EMA, it indicates an uptrend.

When the short EMA crosses below the long EMA, it signals a downtrend.

Signal Confirmation with MACD

The MACD line and Signal line are analyzed to detect momentum shifts.

A bullish signal occurs when the MACD line crosses above the Signal line, especially if the EMAs confirm an uptrend.

A bearish signal occurs when the MACD line crosses below the Signal line, especially if the EMAs confirm a downtrend.

Trading Logic

Buy signals appear only when both the EMA trend is bullish and the MACD confirms momentum to the upside.

Sell signals appear only when both the EMA trend is bearish and the MACD confirms momentum to the downside.

Forecasting

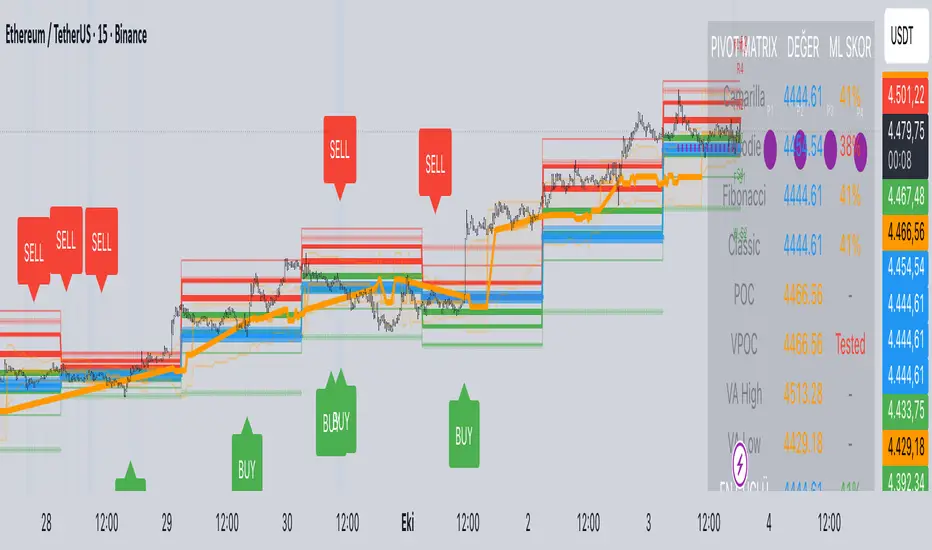

Predictive Pivot Matrix OHLC data, integrates volume profile for POC/Value Area tracking (including virgin POC), applies rule-based "ML" scoring to evaluate pivot strength via factors like proximity, volume, touches, trend, and confluence, monitors adaptive success rates, projects 5-day future pivots using trend/volatility, detects overlapping confluence zones, and generates visuals (lines, labels, table), alerts, and buy/sell signals on key crossings.

Brownian Motion Probabilistic Forecasting (Time Adaptive)Probabilistic Price Forecast Indicator

Overview

The Probabilistic Price Forecast is an advanced technical analysis tool designed for the TradingView platform. Instead of predicting a single future price, this indicator uses a Monte Carlo simulation to model thousands of potential future price paths, generating a cone of possibilities and calculating the probability of specific outcomes.

This allows traders to move beyond simple price targets and ask more sophisticated questions, such as: "What is the probability that this stock will increase by 5% over the next 24 hours?"

Core Concept: Geometric Brownian Motion

The indicator's forecasting model is built on the principles of Geometric Brownian Motion (GBM) , a widely accepted mathematical model for describing the random movements of financial asset prices. The core idea is that the next price step is a function of the asset's historical trend (drift), its volatility, and a random "shock."

The formula used to project each price step in the simulation is:

next_price = current_price * exp( (μ - (σ²/2))Δt + σZ√(Δt) )

Where:

μ (mu) represents the drift , which is the average historical return.

σ (sigma) represents the volatility , measured by the standard deviation of historical returns.

Z is a random variable from a standard normal distribution, representing the random "shock" or new information affecting the price.

Δt (delta t) is the time step for each projection.

How It Works

The indicator performs a comprehensive analysis on the most recent bar of the chart:

**Historical Analysis**: It first analyzes a user-defined historical period (e.g., the last 240 hours of price data) to calculate the asset's historical drift (μ) and volatility (σ) from its logarithmic returns.

**Monte Carlo Simulation**: It then runs thousands of simulations (e.g., 2000) of future price paths over a specified forecast period (e.g., the next 24 hours). Each path is unique due to the random shock (Z) applied at every step.

**Probability Distribution**: After all simulations are complete, it collects the final price of each path and sorts them to build a probability distribution of potential outcomes.

**Visualization and Signaling**: Finally, it visualizes this distribution on the chart and generates signals based on the user's criteria.

Key Features & Configuration

The indicator is highly configurable, allowing you to tailor its analysis to your specific needs.

Time-Adaptive Periods

The lookback and forecast periods are defined in hours , not bars. The script automatically converts these hour-based inputs into the correct number of bars based on the chart's current timeframe, ensuring the analysis remains consistent across different chart resolutions.

Forecast Quartiles

You can visualize the forecast as a "cone of probability" on the chart. The indicator draws lines and a shaded area representing the price levels for different quartiles (percentiles) of the simulation results. By default, this shows the range between the 25th and 95th percentiles.

Independent Bullish and Bearish Signals

The indicator allows you to set independent criteria for bullish and bearish signals, providing greater flexibility. You can configure:

A bullish signal for an X% confidence of a Y% price increase.

A bearish signal for a W% confidence of a Z% price decrease.

For example, you can set it to alert you for a 90% chance of a 2% drop, while simultaneously looking for a 60% chance of a 10% rally.

How to Interpret the Indicator

The Forecast Cone : The blue shaded area on the chart represents the probable range of future prices. The width of the cone indicates the expected volatility; a wider cone means higher uncertainty. The price labels on the right side of the cone show the calculated percentile levels at the end of the forecast period.

Green Signal Label : A green "UP signal" label appears when the probability of the price increasing by your target percentage exceeds your defined confidence level.

Red Signal Label : A red "DOWN signal" label appears when the probability of the price decreasing by your target percentage exceeds your confidence level.

This tool provides a statistical edge for understanding future possibilities but should be used in conjunction with other analysis techniques.

Volume Based Sampling [BackQuant]Volume Based Sampling

What this does

This indicator converts the usual time-based stream of candles into an event-based stream of “synthetic” bars that are created only when enough trading activity has occurred . You choose the activity definition:

Volume bars : create a new synthetic bar whenever the cumulative number of shares/contracts traded reaches a threshold.

Dollar bars : create a new synthetic bar whenever the cumulative traded dollar value (price × volume) reaches a threshold.

The script then keeps an internal ledger of these synthetic opens, highs, lows, closes, and volumes, and can display them as candles, plot a moving average calculated over the synthetic closes, mark each time a new sample is formed, and optionally overlay the native time-bars for comparison.

Why event-based sampling matters

Markets do not release information on a clock: activity clusters during news, opens/closes, and liquidity shocks. Event-based bars normalize for that heteroskedastic arrival of information: during active periods you get more bars (finer resolution); during quiet periods you get fewer bars (coarser resolution). Research shows this can reduce microstructure pathologies and produce series that are closer to i.i.d. and more suitable for statistical modeling and ML. In particular:

Volume and dollar bars are a common event-time alternative to time bars in quantitative research and are discussed extensively in Advances in Financial Machine Learning (AFML). These bars aim to homogenize information flow by sampling on traded size or value rather than elapsed seconds.

The Volume Clock perspective models market activity in “volume time,” showing that many intraday phenomena (volatility, liquidity shocks) are better explained when time is measured by traded volume instead of seconds.

Related market microstructure work on flow toxicity and liquidity highlights that the risk dealers face is tied to information intensity of order flow, again arguing for activity-based clocks.

How the indicator works (plain English)

Choose your bucket type

Volume : accumulate volume until it meets a threshold.

Dollar Bars : accumulate close × volume until it meets a dollar threshold.

Pick the threshold rule

Dynamic threshold : by default, the script computes a rolling statistic (mean or median) of recent activity to set the next bucket size. This adapts bar size to changing conditions (e.g., busier sessions produce more frequent synthetic bars).

Fixed threshold : optionally override with a constant target (e.g., exactly 100,000 contracts per synthetic bar, or $5,000,000 per dollar bar).

Build the synthetic bar

While a bucket fills, the script tracks:

o_s: first price of the bucket (synthetic open)

h_s: running maximum price (synthetic high)

l_s: running minimum price (synthetic low)

c_s: last price seen (synthetic close)

v_s: cumulative native volume inside the bucket

d_samples: number of native bars consumed to complete the bucket (a proxy for “how fast” the threshold filled)

Emit a new sample

Once the bucket meets/exceeds the threshold, a new synthetic bar is finalized and stored. If overflow occurs (e.g., a single native bar pushes you past the threshold by a lot), the code will emit multiple synthetic samples to account for the extra activity.

Maintain a rolling history efficiently

A ring buffer can overwrite the oldest samples when you hit your Max Stored Samples cap, keeping memory usage stable.

Compute synthetic-space statistics

The script computes an SMA over the last N synthetic closes and basic descriptors like average bars per synthetic sample, mean and standard deviation of synthetic returns, and more. These are all in event time , not clock time.

Inputs and options you will actually use

Data Settings

Sampling Method : Volume or Dollar Bars.

Rolling Lookback : window used to estimate the dynamic threshold from recent activity.

Filter : Mean or Median for the dynamic threshold. Median is more robust to spikes.

Use Fixed? / Fixed Threshold : override dynamic sizing with a constant target.

Max Stored Samples : cap on synthetic history to keep performance snappy.

Use Ring Buffer : turn on to recycle storage when at capacity.

Indicator Settings

SMA over last N samples : moving average in synthetic space . Because its index is sample count, not minutes, it adapts naturally: more updates in busy regimes, fewer in quiet regimes.

Visuals

Show Synthetic Bars : plot the synthetic OHLC candles.

Candle Color Mode :

Green/Red: directional close vs open

Volume Intensity: opacity scales with synthetic size

Neutral: single color

Adaptive: graded by how large the bucket was relative to threshold

Mark new samples : drop a small marker whenever a new synthetic bar prints.

Comparison & Research

Show Time Bars : overlay the native time-based candles to visually compare how the two sampling schemes differ.

How to read it, step by step

Turn on “Synthetic Bars” and optionally overlay “Time Bars.” You will see that during high-activity bursts, synthetic bars print much faster than time bars.

Watch the synthetic SMA . Crosses in synthetic space can be more meaningful because each update represents a roughly comparable amount of traded information.

Use the “Avg Bars per Sample” in the info table as a regime signal. Falling average bars per sample means activity is clustering, often coincident with higher realized volatility.

Try Dollar Bars when price varies a lot but share count does not; they normalize by dollar risk taken in each sample. Volume Bars are ideal when share count is a better proxy for information flow in your instrument.

Quant finance background and citations

Event time vs. clock time : Easley, López de Prado, and O’Hara advocate measuring intraday phenomena on a volume clock to better align sampling with information arrival. This framing helps explain volatility bursts and liquidity droughts and motivates volume-based bars.

Flow toxicity and dealer risk : The same authors show how adverse selection risk changes with the intensity and informativeness of order flow, further supporting activity-based clocks for modeling and risk management.

AFML framework : In Advances in Financial Machine Learning , event-driven bars such as volume, dollar, and imbalance bars are presented as superior sampling units for many ML tasks, yielding more stationary features and fewer microstructure distortions than fixed time bars. ( Alpaca )

Practical use cases

1) Regime-aware moving averages

The synthetic SMA in event time is not fooled by quiet periods: if nothing of consequence trades, it barely updates. This can make trend filters less sensitive to calendar drift and more sensitive to true participation.

2) Breakout logic on “equal-information” samples

The script exposes simple alerts such as breakout above/below the synthetic SMA . Because each bar approximates a constant amount of activity, breakouts are conditioned on comparable informational mass, not arbitrary time buckets.

3) Volatility-adaptive backtests

If you use synthetic bars as your base data stream, most signal rules become self-paced : entry and exit opportunities accelerate in fast markets and slow down in quiet regimes, which often improves the realism of slippage and fill modeling in research pipelines (pair this indicator with strategy code downstream).

4) Regime diagnostics

Avg Bars per Sample trending down: activity is dense; expect larger realized ranges.

Return StdDev (synthetic) rising: noise or trend acceleration in event time; re-tune risk.

Interpreting the info panel

Method : your sampling choice and current threshold.

Total Samples : how many synthetic bars have been formed.

Current Vol/Dollar : how much of the next bucket is already filled.

Bars in Bucket : native bars consumed so far in the current bucket.

Avg Bars/Sample : lower means higher trading intensity.

Avg Return / Return StdDev : return stats computed over synthetic closes .

Research directions you can build from here

Imbalance and run bars

Extend beyond pure volume or dollar thresholds to imbalance bars that trigger on directional order flow imbalance (e.g., buy volume minus sell volume), as discussed in the AFML ecosystem. These often further homogenize distributional properties used in ML. alpaca.markets

Volume-time indicators

Re-compute classical indicators (RSI, MACD, Bollinger) on the synthetic stream. The premise is that signals are updated by traded information , not seconds, which may stabilize indicator behavior in heteroskedastic regimes.

Liquidity and toxicity overlays

Combine synthetic bars with proxies of flow toxicity to anticipate spread widening or volatility clustering. For instance, tag synthetic bars that surpass multiples of the threshold and test whether subsequent realized volatility is elevated.

Dollar-risk parity sampling for portfolios

Use dollar bars to align samples across assets by notional risk, enabling cleaner cross-asset features and comparability in multi-asset models (e.g., correlation studies, regime clustering). AFML discusses the benefits of event-driven sampling for cross-sectional ML feature engineering.

Microstructure feature set

Compute duration in native bars per synthetic sample , range per sample , and volume multiple of threshold as inputs to state classifiers or regime HMMs . These features are inherently activity-aware and often predictive of short-horizon volatility and trend persistence per the event-time literature. ( Alpaca )

Tips for clean usage

Start with dynamic thresholds using Median over a sensible lookback to avoid outlier distortion, then move to Fixed thresholds when you know your instrument’s typical activity scale.

Compare time bars vs synthetic bars side by side to develop intuition for how your market “breathes” in activity time.

Keep Max Stored Samples reasonable for performance; the ring buffer avoids memory creep while preserving a rolling window of research-grade data.

Portfolio Simulator & BacktesterMulti-asset portfolio simulator with different metrics and ratios, DCA modeling, and rebalancing strategies.

Core Features

Portfolio Construction

Up to 5 assets with customizable weights (must total 100%)

Support for any tradable symbol: stocks, ETFs, crypto, indices, commodities

Real-time validation of allocations

Dollar Cost Averaging

Monthly or Quarterly contributions

Applies to both portfolio and benchmark for fair comparison

Model real-world investing behavior

Rebalancing

Four strategies: None, Monthly, Quarterly, Yearly

Automatic rebalancing to target weights

Transaction cost modeling (customizable fee %)

Key Metrics Table

CAGR: Annualized compound return (S&P 500 avg: ~10%)

Alpha: Excess return vs. benchmark (positive = outperformance)

Sharpe Ratio: Return per unit of risk (>1.0 is good, >2.0 excellent)

Sortino Ratio: Like Sharpe but only penalizes downside (better metric)

Calmar Ratio: CAGR / Max Drawdown (>1.0 good, >2.0 excellent)

Max Drawdown: Largest peak-to-trough decline

Win Rate: % of positive days (doesn't indicate profitability)

Visualization

Dual-chart comparison - Portfolio vs. Benchmark

Dollar or percentage view toggle

Customizable colors and line width

Two tables: Statistics + Asset Allocation

Adjustable table position and text size

🚀 Quick Start Guide

Enter 1-5 ticker symbols (e.g., SPY, QQQ, TLT, GLD, BTCUSD)

Make sure percentage weights total 100%

Choose date range (ensure chart shows full period - zoom out!)

Configure DCA and rebalancing (optional)

Select benchmark (default: SPX)

Analyze results in statistics table

💡 Pro Tips

Chart data matters: Load SPY or your longest-history asset as main chart

If you select an asset that was not available for the selected period, the chart will not show up! E.g. BTCUSD data: Only available from ~2017 onwards.

Transaction fees: 0.1% default (adjust to match your broker)

⚠️ Important Notes

Requires visible chart data (zoom out to show full date range)

Limited by each asset's historical data availability

Transaction fees and costs are modeled, but taxes/slippage are not

Past performance ≠ future results

Use for research and education only, not financial advice

Let me know if you have any suggestions to improve this simulator.

Hummingbird Probability Mapping IndicatorHummingbird Probability Mapping Indicator - A nature inspired indicator that utilizes combinations of the following trend patterns and projects a probability mapping with greater than 70% accuracy based on real-time analysis.

EMA Trend

MACD

RSI

VWAP Spread

Burst

Squeeze

Volatility (ATRp)

Qi Dass

Foxbrady D/G CrossFoxbrady D/G Cross - Golden Cross & Death Cross Indicator**

A clean and simple indicator that identifies Golden Cross and Death Cross events using the classic 50-day and 200-day simple moving averages.

Features:

- Blue line: 50-day SMA (fast moving average)

- Red line: 200-day SMA (slow moving average)

- Green "GC" label appears at the exact crossover point when a Golden Cross occurs (bullish signal)

- Red "DC" label appears at the exact crossover point when a Death Cross occurs (bearish signal)

- Built-in alert conditions for both events

- Customizable MA periods to suit your trading style

How to Use:

The Golden Cross (50 MA crossing above 200 MA) is traditionally viewed as a bullish long-term signal, while the Death Cross (50 MA crossing below 200 MA) is considered a bearish indicator. This indicator makes it easy to spot these events historically and receive alerts when they occur in real-time.

Perfect for swing traders and long-term investors looking to identify major trend changes.

Advanced Directional Stoch RSIAdvanced Directional Stochastic RSI

Overview

The Advanced Directional Stochastic RSI (Adv Stoch RSI Dir) is a powerful oscillator that combines the classic Stochastic RSI with John Ehlers' SuperSmoother filter for ultra-smooth signals and reduced noise. Unlike traditional Stoch RSI, this indicator incorporates directional coloring based on price action relative to a smoothed trend line, helping traders quickly spot bullish or bearish momentum. It's designed for swing traders and scalpers looking for clearer overbought/oversold conditions in volatile markets.

Key Features

Directional Coloring: %K line turns green when price is above the trend MA (bullish) and red when below (bearish), providing instant visual bias.

Multi-Pass SuperSmoothing: Apply Ehlers' SuperSmoother filter up to 5 times for customizable noise reduction—dial in passes (default: 2) to balance responsiveness and smoothness.

Trend-Aware Baseline: Uses a cascaded smoothed moving average (default length: 20) to gauge overall direction, making the oscillator more context-aware.

Classic Stoch RSI Core: Built on RSI (default: 14) and Stochastic (default: 14), with SMA smoothing for %K (3) and %D (3).

Visual Aids: Includes overbought (80), oversold (20), and midline (50) levels, plus a subtle blue fill between OB/OS zones for easy reference.

How It Works

Source Smoothing: The input source (default: close) is passed through the SuperSmoother filter multiple times to create a trend MA.

Stoch RSI Calculation: Computes RSI on the source, then applies Stochastic to the RSI values, followed by SMA smoothing for base %K and %D.

Advanced Smoothing: Extra SuperSmoother layers are applied to %K and %D based on your chosen passes, minimizing whipsaws.

Directional Logic: Compares current close to the trend MA to color %K dynamically.

Plotting: %K (thick line, colored) and %D (thin orange) oscillate between 0-100, highlighting crossovers and divergences.

Usage Tips

Buy Signal: Green %K crosses above %D below 50, or bounces off oversold (20) in uptrends.

Sell Signal: Red %K crosses below %D above 50, or rejects overbought (80) in downtrends.

Customization: Increase smoothing passes (3-5) for choppy markets; reduce for faster signals. Pair with volume or support/resistance for confirmation.

Timeframes: Best on 1H-4H charts for stocks/crypto; adjust lengths for forex.

This open-source script is licensed under Mozilla Public License 2.0. Backtest thoroughly—past performance isn't indicative of future results. Enjoy trading smarter with less noise! 🚀

© HighlanderOne

Seasonal Pattern DecoderSeasonal Pattern Decoder

The Seasonal Pattern Decoder is a powerful tool designed for traders and analysts who want to uncover and leverage seasonal tendencies in financial markets. Instead of cluttering your chart with complex visuals, this indicator presents a clean, intuitive table that summarizes historical monthly performance, allowing you to spot recurring patterns at a glance.

How It Works

The indicator fetches historical monthly data for any symbol and calculates the percentage return for each month over a specified number of years. It then organizes this data into a comprehensive table, providing a clear, year-by-year and month-by-month breakdown of performance.

Key Features

Historical Performance Table: Displays monthly returns for up to a user-defined number of years, making it easy to compare performance across different periods.

Color-Coded Heatmap: Each cell is colored based on the performance of the month. Strong positive returns are shaded in green, while strong negative returns are shaded in red, allowing for immediate visual analysis of monthly strength or weakness.

Annual Summary: A "Σ" column shows the total percentage return for each full calendar year.

AVG Row: Calculates and displays the average return for each month across all the years shown in the table.

WR Row: Shows the "Win Rate" for each month, which is the percentage of time that month had a positive return. This is crucial for identifying high-probability seasonal trends.

How to Use

Add the "Seasonal Pattern Decoder" indicator to your chart. Note that it works best on Daily, Weekly, or Monthly timeframes. A warning message will be displayed on intraday charts.

In the indicator settings, adjust the "Lookback Period" to control how many years of historical data you want to analyze.

Use the "Show Years Descending" option to sort the table from the most recent year to the oldest.

The "Heat Range" setting allows you to adjust the sensitivity of the color-coding to fit the volatility of the asset you are analyzing.

This tool is ideal for confirming trading biases, developing seasonal strategies, or simply gaining a deeper understanding of an asset's typical behavior throughout the year.

## Disclaimer

This indicator is designed as a technical analysis tool and should be used in conjunction with other forms of analysis and proper risk management.

Past performance does not guarantee future results, and traders should thoroughly test any strategy before implementing it with real capital.

MACD Forecast [Titans_Invest]MACD Forecast — The Future of MACD in Trading

The MACD has always been one of the most powerful tools in technical analysis.

But what if you could see where it’s going, instead of just reacting to what has already happened?

Introducing MACD Forecast — the natural evolution of the MACD Full , now taken to the next level. It’s the world’s first MACD designed not only to analyze the present but also to predict the future behavior of momentum.

By combining the classic MACD structure with projections powered by Linear Regression, this indicator gives traders an anticipatory, predictive view, redefining what’s possible in technical analysis.

Forget lagging indicators.

This is the smartest, most advanced, and most accurate MACD ever created.

🍟 WHY MACD FORECAST IS REVOLUTIONARY

Unlike the traditional MACD, which only reflects current and past price dynamics, the MACD Forecast uses regression-based projection models to anticipate where the MACD line, signal line, and histogram are heading.

This means traders can:

• See MACD crossovers before they happen.

• Spot trend reversals earlier than most.

• Gain an unprecedented timing advantage in both discretionary and automated trading.

In other words: this indicator lets you trade ahead of time.

🔮 FORECAST ENGINE — POWERED BY LINEAR REGRESSION

At its core, the MACD Forecast integrates Linear Regression (ta.linreg) to project the MACD’s future behavior with exceptional accuracy.

Projection Modes:

• Flat Projection: Assumes trend continuity at the current level.

• LinReg Projection: Applies linear regression across N periods to mathematically forecast momentum shifts.

This dual system offers both a conservative and adaptive view of market direction.

📐 ACCURACY WITH FULL CUSTOMIZATION

Just like the MACD Full, this new version comes with 20 customizable buy-entry conditions and 20 sell-entry conditions — now enhanced with forecast-based rules that anticipate crossovers and trend reversals.

You’re not just reacting — you’re strategizing ahead of time.

⯁ HOW TO USE MACD FORECAST❓

The MACD Forecast is built on the same foundation as the classic MACD, but with predictive capabilities.

Step 1 — Spot Predicted Crossovers:

Watch for forecasted bullish or bearish crossovers. These signals anticipate when the MACD line will cross the signal line in the future, letting you prepare trades before the move.

Step 2 — Confirm with Histogram Projection:

Use the projected histogram to validate momentum direction. A rising histogram signals strengthening bullish momentum, while a falling projection points to weakening or bearish conditions.

Step 3 — Combine with Multi-Timeframe Analysis:

Use forecasts across multiple timeframes to confirm signal strength (e.g., a 1h forecast aligned with a 4h forecast).

Step 4 — Set Entry Conditions & Automation:

Customize your buy/sell rules with the 20 forecast-based conditions and enable automation for bots or alerts.

Step 5 — Trade Ahead of the Market:

By preparing for future momentum shifts instead of reacting to the past, you’ll always stay one step ahead of lagging traders.

🤖 BUILT FOR AUTOMATION AND BOTS 🤖

Whether for manual trading, quantitative strategies, or advanced algorithms, the MACD Forecast was designed to integrate seamlessly with automated systems.

With predictive logic at its core, your strategies can finally react to what’s coming, not just what already happened.

🥇 WHY THIS INDICATOR IS UNIQUE 🥇

• World’s first MACD with Linear Regression Forecasting

• Predictive Crossovers (before they appear on the chart)

• Maximum flexibility with Long & Short combinations — 20+ fully configurable conditions for tailor-made strategies

• Fully automatable for quantitative systems and advanced bots

This isn’t just an update.

It’s the final evolution of the MACD.

______________________________________________________

🔹 CONDITIONS TO BUY 📈

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

🔹 MACD > Signal Smoothing

🔹 MACD < Signal Smoothing

🔹 Histogram > 0

🔹 Histogram < 0

🔹 Histogram Positive

🔹 Histogram Negative

🔹 MACD > 0

🔹 MACD < 0

🔹 Signal > 0

🔹 Signal < 0

🔹 MACD > Histogram

🔹 MACD < Histogram

🔹 Signal > Histogram

🔹 Signal < Histogram

🔹 MACD (Crossover) Signal

🔹 MACD (Crossunder) Signal

🔹 MACD (Crossover) 0

🔹 MACD (Crossunder) 0

🔹 Signal (Crossover) 0

🔹 Signal (Crossunder) 0

🔮 MACD (Crossover) Signal Forecast

🔮 MACD (Crossunder) Signal Forecast

______________________________________________________

______________________________________________________

🔸 CONDITIONS TO SELL 📉

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

🔸 MACD > Signal Smoothing

🔸 MACD < Signal Smoothing

🔸 Histogram > 0

🔸 Histogram < 0

🔸 Histogram Positive

🔸 Histogram Negative

🔸 MACD > 0

🔸 MACD < 0

🔸 Signal > 0

🔸 Signal < 0

🔸 MACD > Histogram

🔸 MACD < Histogram

🔸 Signal > Histogram

🔸 Signal < Histogram

🔸 MACD (Crossover) Signal

🔸 MACD (Crossunder) Signal

🔸 MACD (Crossover) 0

🔸 MACD (Crossunder) 0

🔸 Signal (Crossover) 0

🔸 Signal (Crossunder) 0

🔮 MACD (Crossover) Signal Forecast

🔮 MACD (Crossunder) Signal Forecast

______________________________________________________

______________________________________________________

🔮 Linear Regression Function 🔮

______________________________________________________

• Our indicator includes MACD forecasts powered by linear regression.

Forecast Types:

• Flat: Assumes prices will stay the same.

• Linreg: Makes a 'Linear Regression' forecast for n periods.

Technical Information:

• Function: ta.linreg()

Parameters:

• source: Source price series.

• length: Number of bars (period).

• offset : Offset.

• return: Linear regression curve.

______________________________________________________

______________________________________________________

⯁ UNIQUE FEATURES

______________________________________________________

Linear Regression: (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Table of Conditions: BUY/SELL

Conditions Label: BUY/SELL

Plot Labels in the graph above: BUY/SELL

Automate & Monitor Signals/Alerts: BUY/SELL

Linear Regression (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Table of Conditions: BUY/SELL

Conditions Label: BUY/SELL

Plot Labels in the graph above: BUY/SELL

Automate & Monitor Signals/Alerts: BUY/SELL

______________________________________________________

📜 SCRIPT : MACD Forecast

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy!

______________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

🎗️ In memory of João Guilherme — your light will live on forever.

Gamma Exposure Levels by OMG (Oh My Gamma)OMG (Oh My Gamma) - Daily GEX Levels

An operational framework for Gamma analysis with daily data.

Indicator's Purpose & Demo Data

This indicator plots key strategic levels derived from Gamma Exposure (GEX) analysis. It showcases the operational logic of OhMyGamma analytical engine.

IMPORTANT: The levels plotted by this public script are based on a past date's snapshot for demonstration purposes. They are not valid for live trading and will not update automatically.

The real edge comes from using the fresh data structure provided daily.

How to Read the Levels

This indicator is designed to provide actionable intelligence, not just data. Here's how to read it:

The Levels: Each line represents a key strategic zone (Zero Gamma, Call/Put Walls, etc.) where a market reaction is statistically probable due to dealer hedging flows.

Line Thickness = Strategic Importance: The thickness of each line directly corresponds to its strategic rating. Thicker, solid lines represent higher-conviction zones.

Labels & Tooltips: Hover over a level's label on your chart to see its full description, confluences, and strategic rating.

Pro Tip: The Power of Confluence

This indicator is not a standalone "system". It's an institutional-grade intelligence layer. Its predictive power increases exponentially when used to find confluence with your own analysis.

The highest-probability trades occur when a key Gamma level aligns with:

Price Action: Key support/resistance zones, order blocks, or liquidity pools.

Volumetric Indicators: High/Low Volume Nodes (HVN/LVN) from Volume Profile, VWAP, and Anchored VWAP.

Use these levels to confirm your setups and gain the conviction to act.

How to Get the Daily Updated Script

This indicator requires a new Pine Script code each day to load the current session's data.

To get the daily updated code feel free to visit www.ohmygamma.com

Feedback & Suggestions

This tool is built for the community. Suggestions for improvements and new features are highly welcome and help the project evolve. Feel free to get in touch via the contact form on the website.

Disclaimer: This tool is for informational and educational purposes only. Trading involves significant risk. The authors assume no responsibility for any trading decisions.

DCA vs One-ShotCompare a DCA strategy by choosing the payment frequency (daily, weekly, or monthly), and by choosing whether or not to pay on weekends for cryptocurrency. You can add fees and the reference price (opening, closing, etc.).

MAs+Engulfing O caminho das Criptos

This indicator overlays multiple moving averages (EMAs 20/50/100/200 and SMA 200) and highlights bullish/bearish engulfing candles by dynamically coloring the candle body. When a bullish engulfing is detected, the candle appears as a strong dark green; for bearish engulfing, a more vivid red. Normal candles keep classic lime/red colors. Visual alerts and bar coloring make price-action patterns instantly visible.

Includes built-in alert conditions for both patterns, supporting both trading automation and education. The tool upgrades trend-following setups by combining structure with automatic price action insights.

Este indicador combina médias móveis (EMAs de 20/50/100/200 e SMA 200) com detecção de engolfo de alta/baixa, colorindo o candle automaticamente: engolfo de alta com verde escuro, engolfo de baixa com vermelho destacado. Inclui alertas automáticos para ambos os padrões, perfeito para análise visual, estratégia, ou ensino.

Effort vs Result TRFxThe Effort vs Result (EVR) indicator is designed to identify high-probability reversal signals based on volume and price action dynamics. It highlights points where the market “effort” (high volume) does not correspond to an immediate “result” (price continuation), providing actionable trade setups for both bullish and bearish scenarios.

Features:

Detects bullish EVR signals when a previous high-volume sell candle is followed by a strong bullish candle that sweeps the previous low.

Detects bearish EVR signals when a previous high-volume buy candle is followed by a strong bearish candle that sweeps the previous high.

Sticky arrows plot automatically above or below the candle, ensuring the signal moves with the price bar.

Considers inside bars, wick size, and relative volume to filter low-quality setups.

Fully compatible with multiple timeframes.

Inputs:

Volume Multiplier: Sets how much higher the current candle’s volume should be compared to the previous candle to count as high volume.

Min Wick % of Candle: Minimum wick size relative to the candle body to filter insignificant bars.

Max Inside Bars to Ignore: Number of inside bars between the previous candle and the EVR candle to ignore minor consolidations.

Usage:

(Green Arrow): Enter long when a green arrow appears below the candle. Place stop-loss slightly below the previous swing low.

(Red Arrow): Enter short when a red arrow appears above the candle. Place stop-loss slightly above the previous swing high.

Can be combined with support/resistance levels, trendlines, or other technical indicators for higher accuracy.

Benefits:

Simple and clean visual signals with tiny arrows that move with candles.

Helps traders identify high-probability reversal points based on volume and price action.

Ideal for intraday and swing trading strategies.

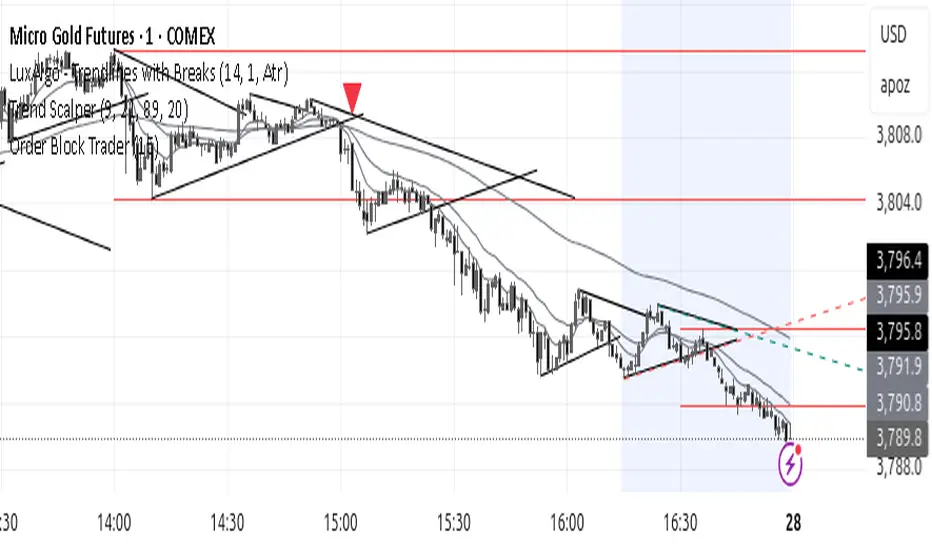

Order Block TraderThe Order Block (HTF) indicator automatically detects and plots higher timeframe order blocks directly onto your chart. Order blocks represent zones of institutional buying or selling pressure that often act as powerful support or resistance levels when revisited. This tool is designed for traders who want to align their lower timeframe entries with higher timeframe structure, helping to filter noise and focus on the most meaningful price levels.

What This Indicator Does

Scans a higher timeframe of your choice to identify potential bullish and bearish order blocks.

Draws the blocks on your current chart, extending them forward in time as reference zones.

Highlights trade signals when price returns to and reacts at these order blocks.

Optionally triggers alerts so that you never miss a potential opportunity.

How It Can Be Used Successfully

Bullish Setup: A bullish order block may serve as a demand zone. When price revisits it, look for bullish confirmation such as a bounce from the block low and a close back above it. This can be used as a long entry point, with stops placed just below the block.

Bearish Setup: A bearish order block may serve as a supply zone. When price revisits it, watch for rejection at the block high followed by a close back below it. This can be used as a short entry point, with stops placed just above the block.

Multi-Timeframe Trading: Use order blocks from larger timeframes (e.g., 4H or Daily) as key zones, then drill down to shorter timeframes (e.g., 5m, 15m) to refine entries.

Confluence with Other Tools: Combine order block signals with your existing strategy—trend indicators, Fibonacci levels, moving averages, or candlestick patterns—for stronger confirmation and improved win probability.

Trade Management: Treat order blocks as zones rather than single price levels. Position sizing, stop placement, and risk-to-reward management remain essential for long-term success.

This indicator is not a standalone trading system but a framework for identifying high-probability supply and demand zones. Traders who apply it consistently—alongside proper risk management and confirmation methods—can improve their ability to catch trend continuations and reversals at structurally important levels.

Opening Range BoxThis indicator, called the "Opening Range Box," is a visual tool that helps you track the start of key trading sessions like London and New York (or whatever session you set).

It does three main things:

Finds the Daily 'First Move': It automatically calculates the High and Low reached during the first 30 minutes (or whatever time you set) of each defined session.

Draws a Box: It immediately draws a colored, transparent box on your chart from the moment the session starts. The top of the box is the OR High, and the bottom is the OR Low. This box acts as a clear reference for the session's initial boundaries.

Extends the Levels: After the initial 30 minutes are over, the box stops growing vertically (it locks in the OR High/Low) but continues to stretch out horizontally for the rest of the trading session. This allows you to easily see how the price reacts to the opening levels throughout the day.

In short: It visually highlights the most important price levels established at the very beginning of the major market sessions.

Pro Momentum Table + Trade Alerts📊 Indicator Name: Pro Momentum Table – ADX + DI + ATR + Astro Timing

🧠 Concept:

This indicator is designed for professional scalpers and intraday traders who want to capture only strong momentum waves — not noise. It combines trend strength, volatility, directional movement, momentum oscillation, vega divergence, and astrological timing into a single compact table on your chart.

⚙️ Components Explained:

Metric Description

ADX (Average Directional Index) Measures the strength of the trend. Values above 20 indicate that a meaningful move is starting.

+DI / -DI (Directional Indicators) Show whether buyers (+DI) or sellers (-DI) are dominating. Increasing +DI with ADX rising = bullish momentum. Increasing -DI with ADX rising = bearish momentum.

ATR (Average True Range) Shows volatility and expected range. Used for setting realistic stop-loss and multi-level targets (1×, 1.5×, 2×, 2.5× ATR).

Price Displays the current price level for quick reference.

CMO (Chande Momentum Oscillator) Measures short-term momentum direction and strength. Helps identify overbought/oversold conditions in trend continuation.

Vega Divergence Shows a synthetic reading of volatility pressure — "Bullish" when volatility expansion supports upward moves, "Bearish" for downward pressure, and "Neutral" otherwise.

Astro Remark Suggests ideal time windows based on planetary cycles for scalping entries. “Bullish Window” often aligns with high-probability long trades; “Bearish Window” favors shorts.

Trade Signal The core momentum condition: “Bullish Momentum” if ADX > 20 and +DI rising, “Bearish Momentum” if ADX > 20 and -DI rising, else “No Clear Momentum.”

📈 How to Use:

Wait for ADX > 20 – This confirms that the market is entering a strong momentum phase.

Check DI direction:

✅ +DI rising: Buyers gaining strength → look for long setups.

✅ -DI rising: Sellers gaining strength → look for short setups.

Use ATR to plan exits:

🎯 TP1 = Entry ± 1 × ATR

🎯 TP2 = Entry ± 1.5 × ATR

🎯 TP3 = Entry ± 2 × ATR

🎯 TP4 = Entry ± 2.5 × ATR

CMO & Vega Divergence: Confirm momentum direction and volatility expansion before committing.

Astro Remark: Align your scalping activity with the planetary support window for higher probability trades.

🪙 Pro Tips for Scalpers:

Only trade when ADX > 20 and DI is consistently rising. Ignore signals in choppy or sideways phases.

Avoid trades if Vega is neutral and CMO is flat – these usually indicate fake breakouts.

If targets aren’t hit within expected ATR-based time, treat the move as false and exit early.

Combine with 9 EMA and 20 EMA (hidden) for wave structure confirmation without cluttering the chart.

💡 Summary:

This indicator acts as a real-time trade decision dashboard. It removes clutter from the chart and delivers everything a professional scalper needs — strength, direction, volatility, momentum, timing, and actionable trade bias — all in one elegant table.

Pattern Match & Forward Projection – Weekly (EN)

Overview

This indicator searches for recurring price patterns in weekly data and projects their average forward performance.

The logic is based on historical pattern repetition: it scans past price sequences similar to the most recent one, then aggregates their forward returns to estimate potential outcomes.

⚠️ Important: The indicator is designed for weekly timeframe only. Using it on daily or intraday charts will trigger an error message.

Settings (Inputs)

Pattern Settings

Pattern length (weeks): Number of weeks used to define the reference pattern.

Forward length (weeks): Number of weeks into the future to evaluate after each pattern match.

Lookback (weeks): Historical window to scan for past pattern matches.

Normalize by shape (z-score): If enabled, patterns are normalized by z-score, focusing on shape similarity rather than absolute values.

Distance threshold (Euclidean): Maximum allowed Euclidean distance between the reference pattern and historical candidates. Smaller values = stricter matching.

Min. required matches: Minimum number of valid matches needed for analysis.

Quality Filters

Min required Hit%: Minimum percentage of positive outcomes (upside forward returns) required for the pattern to be considered valid.

Return filter mode:

Either: absolute average return ≥ threshold

Long only: average return ≥ threshold

Short only: average return ≤ -threshold

Min avg return (%): Minimum average forward return threshold for validation.

Visual Options

Highlight historical matches (labels): Marks where in history similar patterns occurred.

Max match labels to draw: Caps the number of match markers shown to avoid clutter.

Draw average projection: Displays the average projected forward curve if conditions are met.

Show summary panel: Enables/disables the information panel.

Show weekly avg curve in panel: Adds a breakdown of average returns week by week.

Projection color: Choose the color of the projected forward curve.

What the Screen Shows

Summary Panel (top-left by default)

Total matches found in history

Matches with valid forward data

Average, minimum, and maximum distance (similarity measure)

Average forward return and Hit%

Distance threshold and normalization setting

Weekly average forward curve (if enabled)

Quality filter results (pass/fail)

Projection Curve (dotted line on price chart)

Drawn only if enough valid matches are found and filters are satisfied

Represents the average forward performance of historical matches, anchored at the current bar

Historical Match Labels (▲ markers)

Small arrows below past bars where similar patterns occurred

Tooltip: “Historical match”

Forecast Logic

The indicator does not predict the future in a deterministic way.

Instead, it relies on a pattern-matching algorithm:

The most recent N weeks (defined by Pattern length) are taken as the reference.

The algorithm scans the last Lookback (weeks) for segments with similar shape and magnitude.

Similarity is measured using Euclidean distance (optionally z-score normalized).

For each valid match, the subsequent Forward length weeks are collected.

These forward paths are averaged to generate a composite forward projection.

The summary panel reports whether the current setup passes the quality filters (Hit% and minimum average return).

Usage Notes

Best used as a contextual tool, not a standalone trading system.

Works only on weekly timeframe.

Quality filters help distinguish between noisy and statistically meaningful patterns.

A higher number of matches usually improves reliability, but very strict thresholds may reduce sample size.

📊 This tool is useful for traders who want to evaluate how similar historical setups have behaved and to visualize potential forward paths in a statistically aggregated way.

WASDE DatesOverview

WASDE Dates — a small, focused event indicator that displays confirmed USDA WASDE release dates for 2025 on the chart and marks each release day. The indicator is designed to be a lightweight timing tool for traders who want clean visual reminders and optional alerts around USDA WASDE publications.

Features

• Shows official WASDE release dates for 2025 in a compact chart table.

• Draws on-chart markers and a dotted vertical line on WASDE release days.

• Two alert conditions you can enable in TradingView: "WASDE Day Alert" and "WASDE 24h Reminder".

• Simple table position control (Top/Bottom, Left/Right) in the indicator settings.

• Minimal, self-contained code — no external data feeds or permissions required.

How to use

1. Apply the indicator to any chart and timeframe.

2. Use the indicator settings to choose table position.

3. Enable Alerts (if desired) via TradingView Alerts → choose “WASDE Day Alert” or “WASDE 24h Reminder”.

4. This version contains 2025 confirmed dates only — verify dates for live trading and enable alerts as needed.

Design & rationale

This indicator is intentionally not a technical trading signal. It is an event scheduler focused on clarity and low overhead: combine it with your existing setup to avoid being surprised by WASDE publications and to quickly inspect price action around these event dates.

Limitations & disclaimer

• This script shows **confirmed 2025** WASDE dates only. It does not provide trading advice or entry/exit signals. Use at your own risk.

• Double-check official USDA publishing times before executing trades.

• No external links or contact information are included in this description to comply with TradingView publishing rules.

Feature outlook (V2)

Planned V2 (future release): enhanced countdown (days → hours/minutes), optional inclusion of estimated 2026 dates marked as (TBC), and an invite-only/protected advanced version with reaction overlays (T+1/T+3) and extended alert options. V2 will be announced on this script page when ready.

Changelog

v1 — public release: 2025 confirmed dates, release markers, alerts, table position control.

Smart Money Support/Resistance - LiteSmart Money Support/Resistance — Lite

Overview & Methodology

This indicator identifies support and resistance as zones derived from concentrated buying and selling pressure, rather than relying solely on traditional swing highs/lows. Its design focuses on transparency: how data is sourced, how zones are computed, and how the on‑chart display should be interpreted.

Lower‑Timeframe (LTF) Data

The script requests Up Volume, Down Volume, and Volume Delta from a lower timeframe to expose intrabar order‑flow structure that the chart’s native timeframe cannot show. In practical terms, this lets you see where buyers or sellers briefly dominated inside the body of a higher‑timeframe bar.

bool use_custom_tf_input = input.bool(true, title="Use custom lower timeframe", tooltip="Override the automatically chosen lower timeframe for volume calculations.", group=grpVolume)

string custom_tf_input = input. Timeframe("1", title="Lower timeframe", tooltip="Lower timeframe used for up/down volume calculations (default 5 seconds).", group=grpVolume)

import TradingView/ta/10 as tvta

resolve_lower_tf(useCustom, customTF) =>

useCustom ? customTF :

timeframe.isseconds ? "1S" :

timeframe.isintraday ? "1" :

timeframe.isdaily ? "5" : "60"

get_up_down_volume(lowerTf) =>

= tvta.requestUpAndDownVolume(lowerTf)

var float upVolume = na

var float downVolume = na

var float deltaVolume = na

string lower_tf = resolve_lower_tf(use_custom_tf_input, custom_tf_input)

= get_up_down_volume(lower_tf)

upVolume := u_tmp

downVolume := d_tmp

deltaVolume := dl_tmp

• Data source: TradingView’s ta.requestUpAndDownVolume(lowerTf) via the official TA library.

• Plan capabilities: higher‑tier subscriptions unlock seconds‑based charts and allow more historical bars per chart. This expands both the temporal depth of LTF data and the precision of short‑horizon analysis, while base tiers provide minute‑level data suitable for day/short‑swing studies.

• Coverage clarity: a small on‑chart Coverage Panel reports the active lower timeframe, the number of bars covered, and the latest computed support/resistance ranges so you always know the bounds of valid LTF input.

Core Method

1) Data acquisition (LTF)

The script retrieves three series from the chosen lower timeframe:

– Up Volume (buyers)

– Down Volume (sellers)

– Delta (Up – Down)

2) Rolling window & extrema

Over a user‑defined lookback (Global Volume Period), the algorithm builds rolling arrays of completed bars and scans for extrema:

– Buyers_max / Buyers_min from Up Volume

– Sellers_max / Sellers_min from Down Volume

Only completed bars are considered; the current bar is excluded for stability.

3) Price mapping

The extrema are mapped back to their source candles to obtain price bounds:

– For “maximum” roles the algorithm uses the relevant candle highs.

– For “minimum” roles it uses the relevant candle lows.

These pairs define candidate resistance (max‑based) and support (min‑based) zones or vice versa.

4) Zone construction & minimum width

To ensure practicality on all symbols, zones enforce a minimum vertical thickness of two ticks. This prevents visually invisible or overly thin ranges on instruments with tight ticks.

5) Vertical role resolution

When both max‑ and min‑based zones exist, the script compares their midpoints. If, due to local price structure, the min‑based zone sits above the max‑based zone, display roles are swapped so the higher zone is labeled Resistance and the lower zone Support. Colors/widths are updated accordingly to keep the visual legend consistent.

6) Rendering & panel

Two horizontal lines and a filled box represent each active zone. The Coverage Panel (bottom‑right by default) prints:

– Lower‑timeframe in use

– Number of bars covered by LTF data

– Current Support and Resistance ranges

If the two zones overlap, an additional “Range Market” note is shown.

Key Inputs

• Global Volume Period: shared lookback window for the extrema search.

• Lower timeframe: user‑selectable override of the automatically resolved lower timeframe.

• Visualization toggles: independent show/hide controls and colors for maximum (resistance) and minimum (support) zones.

• Coverage Panel: enable/disable the single‑cell table and its readout.

Operational Notes

• The algorithm aligns all lookups to completed bars (no peeking). Price references are shifted appropriately to avoid using the still‑forming bar in calculations.

• Second‑based lower timeframes improve granularity for scalping and very short‑term entries. Minute‑based lower timeframes provide broader coverage for intraday and short‑swing contexts.

• Use the Coverage Panel to confirm the true extent of available LTF history on your symbol/plan before drawing conclusions from very deep lookbacks.

Visual Walkthrough

A step‑by‑step image sequence accompanies this description. Each figure demonstrates how the indicator reads LTF volume, locates extrema, builds price‑mapped zones, and updates labels/colors when vertical order requires it.

Chart Interpretation

This chart illustrates two distinct perspectives of the Smart Money Support/Resistance — Lite indicator, each derived from different lookback horizons and lower-timeframe (LTF) resolutions.

1- Short-term view (43 bars, 10-second LTF)

Using the most recent 43 completed bars with 10-second intrabar data, the algorithm detects that both maximum and minimum volume extrema fall within a narrow range. The result is a clearly identified range market: resistance between 178.15–184.55 and support between 175.02–179.38.

The Coverage Panel (bottom-right) confirms the scope of valid input: the lower timeframe used, number of bars covered, and the resulting zones. This short-term scan highlights how the indicator adapts to limited data depth, flagging sideways structure where neither side dominates.

2 - Long-term view (120 bars, 30-second LTF)

Over a wider 120-bar lookback with higher-granularity 30-second data, broader supply and demand zones emerge.

– The long-term resistance zone captures the concentration of buyers and sellers at the upper boundary of recent price history.

– The long-term support zone anchors to the opposite side of the distribution, derived from maxima and minima of both buying and selling pressure.

These zones reflect deeper structural levels where market participants previously committed significant volume.

Combined Perspective

By aligning the short-term and long-term outputs, the chart shows how the indicator distinguishes immediate consolidation (range market) from more durable support and resistance levels derived from extended history. This dual resolution approach makes clear that support and resistance are not static lines but dynamic zones, dependent on both timeframe depth and the resolution of intrabar volume data.

Momentum Volume Analyzer [CHE] Momentum Volume Analyzer — Adaptive momentum with volume-gated signals and expressive visual cues

Summary

This indicator combines a normalized momentum oscillator with a volume Z-score gate and adaptive gradient visuals. The oscillator centers around a midline and scales between a lower and an upper bound. Intensity is derived from the distance to the midline and is normalized inside a rolling window, which helps keep contrast consistent across regimes. Volume pressure is compressed to a discrete level between one and ten and is used to qualify momentum flips and extremes. Layered “burst” markers and optional background gradients provide immediate visual emphasis without adding new data sources. Pine version is v6. The script runs in a separate pane.

Motivation: Why this design?

Common oscillators flip rapidly during noisy conditions or flatten during calm periods, which obscures actionable shifts. A rolling normalization keeps the visual intensity stable across different regimes, and a volume gate reduces reactions when participation is weak. The goal is clearer momentum shifts that are supported by measurable activity rather than cosmetic smoothing alone.

What’s different vs. standard approaches?

Baseline reference: Classical RSI-style oscillators or simple filtered momentum without volume gating.

Architecture differences:

Local window normalization with gamma control for contrast.

Volume converted to a Z-score and compressed into a discrete level between one and ten with a configurable cap.

Directional color gradients that intensify with distance from the midline.

Layered glow markers with optional trail and an internal label budget to avoid UI overload.

Practical effect: Signals are visually stronger only when both momentum and volume align; background and line colors convey regime strength at a glance.

How it works (technical)

Momentum core: A high-pass path with automatic gain control produces a bounded oscillator centered around a midline. A simple moving average smooths the result over a short window.

Normalization and contrast: The absolute distance from the midline is scaled inside a rolling window and limited between zero and one. Two gamma parameters separately shape contrast for the line and for labels.

Coloring: When the oscillator is above the midline, a green gradient is used; below the midline, a red gradient is used. Intensity increases with normalized distance. Optional area fill to the midline and a background gradient reinforce strength.

Volume levels: Volume is standardized over a lookback window, clipped by a user cap, and mapped to a level between one and ten. Only positive excursions are considered; non-positive values map to zero.

Event markers: When the oscillator reaches extreme zones and the volume level is positive, the script spawns layered circular labels at fixed y-positions. A small trail can extend behind the event. An internal queue discards the oldest labels when a user-defined maximum is exceeded.

Alerts: Alerts fire on overbought and oversold spikes, midline shifts with minimum intensity and volume, and continuation patterns inside strong zones.

Parameter Guide

TFRSI length (default six): Core momentum lookback. Shorter values react faster but are less stable.

Signal SMA (default two): Light smoothing of the oscillator. Larger values reduce jitter.

Gradient window (default one hundred): Normalization window for intensity. Longer values produce steadier contrast but slower adaptation.

Line/marker transparency (default zero): Visual prominence of drawings. Higher values reduce dominance.

Background on and BG transparency (defaults true and eighty-five): Enables and tunes the pane background gradient.

Area fill to fifty and Fill transparency (defaults true and eighty): Fills between the oscillator and the midline.

Gamma bars/labels and Gamma plot (defaults zero point seven and zero point eight): Contrast shapers for markers and line. Higher values compress low intensities.

Bottom marker and Show last N (defaults true and three hundred thirty-three): Optional compact heat markers with a display cap.

Up/Down colors: Dark and neon pairs for positive and negative regimes.

Lookback (default two hundred) and Z cap (default five): Volume standardization window and clipping level before scaling to one through ten.

Enable bursts, Layers, Trail, Trail transparency, Max live labels, Size scale: Control the layered glow effect, trail length, opacity, label budget, and size multiplier. Reducing the size scale lowers visual dominance.

Spike min level, Shift min level, Min intensity, Rise/Fall length: Gates for alerts; adjust to balance sensitivity and false positives.

Reading & Interpretation

Line color and intensity: Green shades above the midline indicate bullish pressure; red shades below indicate bearish pressure. Stronger color corresponds to stronger normalized distance.

Background and fill: Reinforce regime strength; consider reducing transparency when the pane feels too busy.

Bursts and trails: Emphasize volume-backed extremes. Larger bursts reflect stronger volume levels or scaling choices.

Volume level: Internal level between one and ten. Levels near the upper bound signal exceptional activity.

Practical Workflows & Combinations

Trend following: Use midline cross upward with minimum shift level and intensity as a trigger. Confirm with structure such as higher highs and higher lows. For shorts, reverse the conditions.

Exits and risk: Fade exposure when intensity weakens toward the midline or when volume level drops below the shift threshold. Consider disabling bursts when monitoring many symbols.

Multi-asset and multi-timeframe: Defaults are designed to travel across liquid futures, large-cap equities, and major crypto pairs. For higher timeframes, increase the lookback window and consider reducing the Z cap.

Behavior, Constraints & Performance

Repaint and confirmation: Signals are evaluated on the live bar. They can appear and withdraw before bar close. For confirmed signals, require closed-bar alerts or manual confirmation.

Higher-timeframe sources: Not used. No `security` calls.

Resources: `max_bars_back` is two thousand. The script uses arrays and label objects, including loops for trails. The label budget mitigates clutter.

Known limits: Very illiquid symbols with unstable volume can reduce the usefulness of the Z-score. Sharp regime changes can still produce brief flips.

Sensible Defaults & Quick Tuning

Starting point: TFRSI length six, Signal two, Gradient window one hundred, Z cap five, Spike level six, Shift level four, Min intensity zero point four, Rise length three, Size scale zero point five.

Too many flips: Increase Signal, increase Gradient window, or raise Shift level.

Too sluggish: Decrease TFRSI length or reduce Gradient window.

Bursts too dominant: Lower Size scale or reduce Layers; increase Trail transparency or set Trail length to zero.

What this indicator is—and isn’t

This is a visualization and signal layer that couples momentum with a volume gate and adaptive visuals. It is not a complete trading system, optimizer, or predictor. Use it together with market structure, risk controls, and position management.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Best regards and happy trading

Chervolino

NY 14:30 High/Low - 1mThis indicator automatically draws horizontal lines for the High (green) and Low (red) of the 14:30 (Lisbon) candle on the 1-minute chart.

It is designed for traders who want to quickly identify the New York open levels (NY Open), allowing you to:

Visualize the NY market opening zone.

Use these levels as intraday support or resistance.

Plan entries and exits based on breakouts or pullbacks.

Features:

Works on any 1-minute chart.

Lines are drawn immediately after the 14:30 candle closes.

Lines extend automatically to the right.

Simple and lightweight, no complex variables or external dependencies.

Daily reset, always showing the current day’s levels.

Recommended Use:

Combine with support/resistance zones, order blocks, or fair value gaps.

Monitor price behavior during the NY open to identify breakout or rejection patterns.