IU Inside/Harami candlestick patternDESCRIPTION

The IU Inside/Harami Candlestick Pattern indicator is designed to detect bullish and bearish inside bar formations, also known as Harami patterns. This tool gives users flexibility by allowing pattern detection based on candle wicks, bodies, or a combination of both. It highlights detected patterns using colored boxes and optional text labels on the chart, helping traders quickly identify areas of consolidation and potential reversals.

USER INPUTS :

Pattern Recognition Based on =

Choose between "Wicks", "Body", or "Both" to determine how the inside candle pattern is identified.

Show Box =

Toggle the appearance of colored boxes that highlight the pattern zone.

Show Text =

Toggle on-screen labels for "Bullish Inside" or "Bearish Inside" when patterns are detected.

INDICATOR LOGIC :

Bullish Inside Bar (Harami) is detected when:

* The current candle's high is lower and low is higher than the previous candle (wick-based),

* or the current candle’s open and close are inside the previous candle’s body (body-based),

* and the current candle is bullish while the previous is bearish.

Bearish Inside Bar (Harami) is detected when:

* The current candle's high is lower and low is higher than the previous candle (wick-based),

* or the current candle’s open and close are inside the previous candle’s body (body-based),

* and the current candle is bearish while the previous is bullish.

The user can choose wick-based, body-based, or both logics for pattern confirmation.

Boxes are drawn between the highs and lows of the pattern, and alert messages are generated upon confirmation.

Optional labels show the pattern name for quick visual identification.

WHY IT IS UNIQUE :

Offers three different logic modes: wick-based, body-based, or combined.

Highlights patterns visually with customizable boxes and labels.

Includes built-in alerts for immediate notifications.

Uses clean and transparent plotting without repainting.

HOW USER CAN BENEFIT FROM IT :

Receive real-time alerts when Inside/Harami patterns are formed.

Use the boxes and text labels to spot price compression zones and breakout potential.

Combine it with other tools like trendlines or support/resistance for enhanced accuracy.

Suitable for scalpers, swing traders, and price action traders looking to trade inside bar breakouts or reversals.

DISCLAIMER :

This indicator is not financial advice, it's for educational purposes only highlighting the power of coding( pine script) in TradingView, I am not a SEBI-registered advisor. Trading and investing involve risk, and you should consult with a qualified financial advisor before making any trading decisions. I do not guarantee profits or take responsibility for any losses you may incur.

Forecasting

Position Size Calculator with Fees# Position Size Calculator with Portfolio Management - Manual

## Overview

The Position Size Calculator with Portfolio Management is an advanced Pine Script indicator designed to help traders calculate optimal position sizes based on their total portfolio value and risk management strategy. This tool automatically calculates your risk amount based on portfolio allocation percentages and determines the exact position size needed while accounting for trading fees.

## Key Features

- **Portfolio-Based Risk Management**: Calculates risk based on total portfolio value

- **Tiered Risk Allocation**: Separates trading allocation from total portfolio

- **Automatic Trade Direction Detection**: Determines long/short based on entry vs stop loss

- **Fee Integration**: Accounts for trading fees in position size calculations

- **Risk Factor Adjustment**: Allows scaling of position size up or down

- **Visual Display**: Shows all calculations in a clear, color-coded table

- **Automatic Risk Calculation**: No need to manually input risk amount

## Input Parameters

### Total Portfolio ($)

- **Purpose**: The total value of your investment portfolio

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

- **Example**: If your total portfolio is worth $100,000, enter 100000

### Trading Portfolio Allocation (%)

- **Purpose**: The percentage of your total portfolio allocated to active trading

- **Default**: 20.0%

- **Range**: 0.0% to 100.0%

- **Step**: 0.01

- **Example**: If you allocate 20% of your portfolio to trading, enter 20

### Risk from Trading (%)

- **Purpose**: The percentage of your trading allocation you're willing to risk per trade

- **Default**: 0.1%

- **Range**: Any positive value

- **Step**: 0.01

- **Example**: If you risk 0.1% of your trading allocation per trade, enter 0.1

### Entry Price ($)

- **Purpose**: The price at which you plan to enter the trade

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

### Stop Loss ($)

- **Purpose**: The price at which you will exit if the trade goes against you

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

### Risk Factor

- **Purpose**: A multiplier to scale your position size up or down

- **Default**: 1.0 (no scaling)

- **Range**: 0.0 to 10.0

- **Step**: 0.1

- **Examples**:

- 1.0 = Normal position size

- 2.0 = Double the position size

- 0.5 = Half the position size

### Fee (%)

- **Purpose**: The percentage fee charged per transaction

- **Default**: 0.01% (0.01)

- **Range**: 0.0% to 1.0%

- **Step**: 0.001

## How Risk Amount is Calculated

The script automatically calculates your risk amount using this formula:

```

Risk Amount = Total Portfolio × Trading Allocation (%) × Risk % ÷ 10,000

```

### Example Calculation:

- Total Portfolio: $100,000

- Trading Allocation: 20%

- Risk per Trade: 0.1%

**Risk Amount = $100,000 × 20 × 0.1 ÷ 10,000 = $20**

This means you would risk $20 per trade, which is 0.1% of your $20,000 trading allocation.

## Portfolio Structure Example

Let's say you have a $100,000 portfolio:

### Allocation Structure:

- **Total Portfolio**: $100,000

- **Trading Allocation (20%)**: $20,000

- **Long-term Investments (80%)**: $80,000

### Risk Management:

- **Risk per Trade (0.1% of trading)**: $20

- **Maximum trades at risk**: Could theoretically have 1,000 trades before risking entire trading allocation

## How Position Size is Calculated

### Trade Direction Detection

- **Long Trade**: Entry price > Stop loss price

- **Short Trade**: Entry price < Stop loss price

### Position Size Formulas

#### For Long Trades:

```

Position Size = -Risk Factor × Risk Amount / (Stop Loss × (1 - Fee) - Entry Price × (1 + Fee))

```

#### For Short Trades:

```

Position Size = -Risk Factor × Risk Amount / (Entry Price × (1 - Fee) - Stop Loss × (1 + Fee))

```

## Output Display

The indicator displays a comprehensive table with color-coded sections:

### Portfolio Information (Light Blue Background)

- **Portfolio (USD)**: Your total portfolio value

- **Trading Portfolio Allocation (%)**: Percentage allocated to trading

- **Risk as % of Trading**: Risk percentage per trade

### Trade Setup (Gray Background)

- **Entry Price**: Your specified entry price

- **Stop Loss**: Your specified stop loss price

- **Fee (%)**: Trading fee percentage

- **Risk Factor**: Position size multiplier

### Risk Analysis (Red Background)

- **Risk Amount**: Automatically calculated dollar risk

- **Effective Entry**: Actual entry cost including fees

- **Effective Exit**: Actual exit value including fees

- **Expected Loss**: Calculated loss if stop loss is hit

- **Deviation from Risk %**: Accuracy of risk calculation

### Final Result (Blue Background)

- **Position Size**: Number of shares/units to trade

## Usage Examples

### Example 1: Conservative Long Trade

- **Total Portfolio**: $50,000

- **Trading Allocation**: 15%

- **Risk per Trade**: 0.05%

- **Entry Price**: $25.00

- **Stop Loss**: $24.00

- **Risk Factor**: 1.0

- **Fee**: 0.01%

**Calculated Risk Amount**: $50,000 × 15% × 0.05% ÷ 100 = $3.75

### Example 2: Aggressive Short Trade

- **Total Portfolio**: $200,000

- **Trading Allocation**: 30%

- **Risk per Trade**: 0.2%

- **Entry Price**: $150.00

- **Stop Loss**: $155.00

- **Risk Factor**: 2.0

- **Fee**: 0.01%

**Calculated Risk Amount**: $200,000 × 30% × 0.2% ÷ 100 = $120

**Actual Risk**: $120 × 2.0 = $240 (due to risk factor)

## Color Coding System

- **Green/Red Header**: Trade direction (Long/Short)

- **Light Blue**: Portfolio management parameters

- **Gray**: Trade setup parameters

- **Red**: Risk-related calculations and results

- **Blue**: Final position size result

## Best Practices

### Portfolio Management

1. **Keep trading allocation reasonable** (typically 10-30% of total portfolio)

2. **Use conservative risk percentages** (0.05-0.2% per trade)

3. **Don't risk more than you can afford to lose**

### Risk Management

1. **Start with small risk factors** (1.0 or less) until comfortable

2. **Monitor your total exposure** across all open positions

3. **Adjust risk based on market conditions**

### Trade Execution

1. **Always validate calculations** before placing trades

2. **Account for slippage** in volatile markets

3. **Consider position size relative to liquidity**

## Risk Management Guidelines

### Conservative Approach

- Trading Allocation: 10-20%

- Risk per Trade: 0.05-0.1%

- Risk Factor: 0.5-1.0

### Moderate Approach

- Trading Allocation: 20-30%

- Risk per Trade: 0.1-0.15%

- Risk Factor: 1.0-1.5

### Aggressive Approach

- Trading Allocation: 30-40%

- Risk per Trade: 0.15-0.25%

- Risk Factor: 1.5-2.0

## Troubleshooting

### Common Issues

1. **Position Size shows 0**

- Verify all portfolio inputs are greater than 0

- Check that entry price differs from stop loss

- Ensure calculated risk amount is positive

2. **Very small position sizes**

- Increase risk percentage or risk factor

- Check if your risk amount is too small for the price difference

3. **Large risk deviation**

- Normal for very small positions

- Consider adjusting entry/stop loss levels

### Validation Checklist

- Total portfolio value is realistic

- Trading allocation percentage makes sense

- Risk percentage is conservative

- Entry and stop loss prices are valid

- Trade direction matches your intention

## Advanced Features

### Risk Factor Usage

- **Scaling up**: Use risk factors > 1.0 for high-confidence trades

- **Scaling down**: Use risk factors < 1.0 for uncertain trades

- **Never exceed**: Risk factors that would risk more than your comfort level

### Multiple Timeframe Analysis

- Use different risk factors for different timeframes

- Consider correlation between positions

- Adjust trading allocation based on market conditions

## Disclaimer

This tool is for educational and planning purposes only. Always verify calculations manually and consider market conditions, liquidity, and correlation between positions. The automated risk calculation assumes you're comfortable with the mathematical relationship between portfolio allocation and individual trade risk. Past performance doesn't guarantee future results, and all trading involves risk of loss.

Easy Position Size Calculator with Fees# Easy Position Size Calculator with Fees - Manual

## Overview

The Easy Position Size Calculator is a Pine Script indicator designed to help traders calculate the optimal position size for their trades while accounting for trading fees. This tool automatically determines whether you're planning a long or short position and calculates the exact position size needed to risk a specific dollar amount.

## Key Features

- **Automatic Trade Direction Detection**: Determines if you're going long or short based on entry price vs stop loss

- **Fee Integration**: Accounts for trading fees in position size calculations

- **Risk Management**: Calculates position size based on your specified risk amount

- **Risk Factor Adjustment**: Allows you to scale your position size up or down

- **Visual Display**: Shows all calculations in a clear, organized table

## Input Parameters

### Entry Price ($)

- **Purpose**: The price at which you plan to enter the trade

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

### Stop Loss ($)

- **Purpose**: The price at which you will exit the trade if it goes against you

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

### Risk ($)

- **Purpose**: The maximum dollar amount you're willing to lose on this trade

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

### Risk Factor

- **Purpose**: A multiplier to scale your position size up or down

- **Default**: 1.0 (no scaling)

- **Range**: 0.0 to 10.0

- **Step**: 0.1

- **Examples**:

- 1.0 = Normal position size

- 2.0 = Double the position size

- 0.5 = Half the position size

### Fee (%)

- **Purpose**: The percentage fee charged per transaction (buy/sell)

- **Default**: 0.01% (0.01)

- **Range**: 0.0% to 1.0%

- **Step**: 0.001

## How It Works

### Trade Direction Detection

The script automatically determines your trade direction:

- **Long Trade**: Entry price > Stop loss price

- **Short Trade**: Entry price < Stop loss price

### Position Size Calculation

#### For Long Trades:

```

Position Size = -Risk Factor × Risk Amount / (Stop Loss × (1 - Fee) - Entry Price × (1 + Fee))

```

#### For Short Trades:

```

Position Size = -Risk Factor × Risk Amount / (Entry Price × (1 - Fee) - Stop Loss × (1 + Fee))

```

### Fee Adjustment

The script accounts for fees on both entry and exit:

- **Long trades**: You pay fees when buying (entry) and selling (exit)

- **Short trades**: You pay fees when shorting (entry) and covering (exit)

## Output Display

The indicator displays a table with the following information:

### Trade Information

- **Trade Type**: Shows whether it's a LONG, SHORT, or INVALID trade

- **Entry Price**: Your specified entry price

- **Stop Loss**: Your specified stop loss price

- **Fee (%)**: The fee percentage being used

### Risk Parameters

- **Risk Amount**: The dollar amount you're willing to risk

- **Risk Factor**: The multiplier being applied

### Calculated Values

- **Effective Entry**: The actual cost per share including fees

- **Effective Exit**: The actual exit value per share including fees

- **Expected Loss**: The calculated loss if stop loss is hit

- **Deviation from Risk %**: Shows how close the expected loss is to your target risk

- **Position Size**: The number of shares/units to trade

## Usage Examples

### Example 1: Long Trade

- Entry Price: $100.00

- Stop Loss: $95.00

- Risk Amount: $500.00

- Risk Factor: 1.0

- Fee: 0.01%

**Result**: The script will calculate how many shares to buy so that if the stop loss is hit, you lose approximately $500 (accounting for fees). Position Size: 99.61152

### Example 2: Short Trade

- Entry Price: $50.00

- Stop Loss: $55.00

- Risk Amount: $300.00

- Risk Factor: 1.0

- Fee: 0.01%

**Result**: The script will calculate how many shares to short so that if the stop loss is hit, you lose approximately $300 (accounting for fees). Position Size: 59.87426

## Important Notes

### Validation Requirements

For the script to work properly, all of the following must be true:

- Entry price > 0

- Stop loss > 0

- Risk amount > 0

- Entry price ≠ Stop loss (to determine direction)

### Negative Position Sizes

The script may show negative position sizes, which is normal:

- **Negative values for long trades**: Represents shares to buy

- **Negative values for short trades**: Represents shares to short

### Risk Deviation

The "Deviation from Risk %" shows how closely the calculated position size matches your target risk. Small deviations are normal due to:

- Fee calculations

- Rounding

- Market precision

## Color Coding

The table uses color coding for easy identification:

- **Green**: Long trade information

- **Red**: Short trade information

- **Gray**: Invalid trade (when inputs are incorrect)

- **Blue**: Final position size

- **Red background**: Risk-related calculations

## Troubleshooting

### Common Issues

1. **Position Size shows 0**

- Check that all inputs are greater than 0

- Ensure entry price is different from stop loss

2. **Trade Type shows INVALID**

- Verify that entry price and stop loss are both positive

- Make sure entry price ≠ stop loss

3. **Large Risk Deviation**

- This is normal for very small position sizes

- Consider adjusting your risk amount or price levels

## Best Practices

1. **Always validate your inputs** before placing actual trades

2. **Double-check the trade direction** shown in the table

3. **Review the expected loss** to ensure it aligns with your risk management

4. **Consider the effective entry/exit prices** which include fees

5. **Use appropriate risk factors** - avoid extreme values that could lead to overexposure

## Disclaimer

This tool is for educational and planning purposes only. Always verify calculations manually and consider market conditions, liquidity, and other factors before placing actual trades. The script assumes that fees are charged on both entry and exit transactions.

VIX-Price Covariance MonitorThe VIX-Price Covariance Monitor is a statistical tool that measures the evolving relationship between a security's price and volatility indices such as the VIX (or VVIX).

It can give indication of potential market reversal, as typically, volatility and the VIX increase before markets turn red,

This indicator calculates the Pearson correlation coefficient using the formula:

ρ(X,Y) = cov(X,Y) / (σₓ × σᵧ)

Where:

ρ is the correlation coefficient

cov(X,Y) is the covariance between price and the volatility index

σₓ and σᵧ are the standard deviations of price and the volatility index

Enjoy!

Features

Dual Correlation Periods: Analyze both short-term and long-term correlation trends simultaneously

Adaptive Color Coding: Correlation strength is visually represented through color intensity

Market Condition Assessment: Automatic interpretation of correlation values into actionable market insights

Leading/Lagging Analysis: Optional time-shift analysis to detect predictive relationships

Detailed Information Panel: Real-time statistics including current correlation values, historical averages, and trading implications

Interpretation

Positive Correlation (Red): Typically bearish for price, as rising VIX correlates with falling markets. This is what traders should be looking for.

Negative Correlation (Green): Typically bullish for price, as falling VIX correlates with rising markets

How to use it

Apply the indicator to any chart to see its correlation with the default VIX index

Adjust the correlation length to match your trading timeframe (shorter for day trading, longer for swing trading)

Enable the secondary correlation period to compare different timeframes simultaneously

For advanced analysis, enable the Leading/Lagging feature to detect if VIX changes precede or follow price movements

Use the information panel to quickly assess the current market condition and potential trading implications

Smart Directional Fib Zone (Selectable Session)🎯 Overview

This indicator plots a dynamic Fibonacci zone between the 0.5 and 0.618 levels , calculated from the previous day’s price action , and is designed specifically for intraday traders.

It visually highlights key retracement or reaction areas where the market often pauses or reverses.

🔍 How it works

At the start of each day, the script automatically captures:

the previous day’s open (pdo),

high (pdh),

low (pdl),

and close (pdc).

It then determines if the previous day was bullish (Close > Open) or bearish (Close < Open).

Based on that:

If the previous day was bullish, it projects the Fibonacci levels down from the high (typical for expecting retracements).

If bearish, it projects them up from the low.

The two key levels are:

0.5 (50%) retracement / projection

0.618 (61.8%) retracement / projection

A colored zone is plotted between these levels to act as a leading guide for intraday setups.

⏰ Time filtering & session customization

A unique feature is the dynamic session filtering:

By default, the zone is only plotted during active market hours, keeping your chart clean outside trading hours.

The script provides a dropdown selector so you can quickly switch between:

India session (9:15 to 15:30)

Europe session (9:00 to 17:30)

US session (9:30 to 16:00)

Or even define your own custom session times.

This makes it ideal for intraday traders in any region.

🎨 Visual features

The fill zone changes color based on the previous day’s sentiment:

Green zone if the previous day was bullish

Red zone if the previous day was bearish

🚨 Alerts

The script includes an alert condition, so you can easily set up TradingView alerts to notify you when:

Price enters the Fibonacci zone.

This is extremely helpful for catching retracements or reversals without staring at the screen all day.

⚙️ How to use

✅ Works on any intraday timeframe (1 min, 5 min, 15 min, etc.).

✅ Simply add it to your chart, pick your session in the dropdown, and watch the Fibonacci zone automatically adjust to your selected market hours.

Use it as a confluence tool alongside other indicators like VWAP, EMAs, Bollinger Bands, or price action patterns to time entries and exits.

💪 Why this is powerful

This is more than a simple Fib retracement tool:

It dynamically adapts to the previous day’s sentiment, helping you trade in alignment with recent market psychology.

The session filtering ensures your charts are focused only on the periods

Dynamic Gap Probability ToolDynamic Gap Probability Tool measures the percentage gap between price and a chosen moving average, then analyzes your chart history to estimate the likelihood of the next candle moving up or down. It dynamically adjusts its sample size to ensure statistical robustness while focusing on the exact deviation level.

Originality and Value:

• Combines gap-based analysis with dynamic sample aggregation to balance precision and reliability.

• Automatically extends the sample when exact matches are scarce, avoiding misleading signals on rare extreme moves.

• Provides real “next-candle” probabilities based on historical occurrences rather than fixed thresholds or untested heuristics.

• Adds value by giving traders an evidence-based edge: you see how similar past deviations actually played out.

How It Works:

1. Calculate gap = (close – moving average) / moving average * 100.

2. Round the absolute gap to nearest percent (X%).

3. Count historical bars where gap ≥ X% above or ≤ –X% below.

4. If exact X% count is below the minimum occurrences threshold, include gaps at X+1%, X+2%, etc., until threshold is reached.

5. Compute “next-candle” green vs. red probabilities from the aggregated sample.

6. Display current gap, sample size, green probability, and red probability in a table.

Inputs:

• Moving Average Type (SMA, EMA, WMA, VWMA, HMA, SMMA, TMA)

• Moving Average Period (default 200)

• Minimum Occurrences Threshold (default 50)

• Table position and styling options

Examples:

• If price is 3% above the 200-period SMA and 120 occurrences ≥3% are found, with 84 green next candles (70%) and 36 red (30%), the script displays “3% | 120 | 70% green | 30% red.”

• If price is 8% below the SMA but only 20 exact matches exist, the script will include 9% and 10% gaps until it reaches 50 samples, then calculate probabilities from that broader set.

Why It’s Useful:

• Mean-reversion traders see green-probability signals at extreme overbought or oversold levels.

• Trend-followers identify continuation likelihood when red probability is high.

• Risk managers gauge reliability by inspecting sample size before acting on any signal.

Limitations:

• Historical probabilities do not guarantee future performance.

• Results depend on timeframe and symbol, backtest with your data before trading.

• Use realistic slippage and commission when overlaying on strategy scripts.

EVaR Indicator and Position SizingThe Problem:

Financial markets consistently show "fat-tailed" distributions where extreme events occur with higher frequency than predicted by normal distributions (Gaussian or even log-normal). These fat tails manifest in sudden price crashes, volatility spikes, and black swan events that traditional risk measures like volatility can underestimate. Standard deviation and conventional VaR calculations assume normally distributed returns, leaving traders vulnerable to severe drawdowns during market stress.

Cryptocurrencies and volatile instruments display particularly pronounced fat-tailed behavior, with extreme moves occurring 5-10 times more frequently than normal distribution models would predict. This reality demands a more sophisticated approach to risk measurement and position sizing.

The Solution: Entropic Value at Risk (EVAR)

EVaR addresses these limitations by incorporating principles from statistical mechanics and information theory through Tsallis entropy. This advanced approach captures the non-linear dependencies and power-law distributions characteristic of real financial markets.

Entropy is more adaptive than standard deviations and volatility measures.

I was inspired to create this indicator after reading the paper " The End of Mean-Variance? Tsallis Entropy Revolutionises Portfolio Optimisation in Cryptocurrencies " by by Sana Gaied Chortane and Kamel Naoui.

Key advantages of EVAR over traditional risk measures:

Superior tail risk capture: More accurately quantifies the probability of extreme market moves

Adaptability to market regimes: Self-calibrates to changing volatility environments

Non-parametric flexibility: Makes less assumptions about the underlying return distribution

Forward-looking risk assessment: Better anticipates potential market changes (just look at the charts :)

Mathematically, EVAR is defined as:

EVAR_α(X) = inf_{z>0} {z * log(1/α * M_X(1/z))}

Where the moment-generating function is calculated using q-exponentials rather than conventional exponentials, allowing precise modeling of fat-tailed behavior.

Technical Implementation

This indicator implements EVAR through a q-exponential approach from Tsallis statistics:

Returns Calculation: Price returns are calculated over the lookback period

Moment Generating Function: Approximated using q-exponentials to account for fat tails

EVAR Computation: Derived from the MGF and confidence parameter

Normalization: Scaled to for intuitive visualization

Position Sizing: Inversely modulated based on normalized EVAR

The q-parameter controls tail sensitivity—higher values (1.5-2.0) increase the weighting of extreme events in the calculation, making the model more conservative during potentially turbulent conditions.

Indicator Components

1. EVAR Risk Visualization

Dynamic EVAR Plot: Color-coded from red to green normalized risk measurement (0-1)

Risk Thresholds: Reference lines at 0.3, 0.5, and 0.7 delineating risk zones

2. Position Sizing Matrix

Risk Assessment: Current risk level and raw EVAR value

Position Recommendations: Percentage allocation, dollar value, and quantity

Stop Parameters: Mathematically derived stop price with percentage distance

Drawdown Projection: Maximum theoretical loss if stop is triggered

Interpretation and Application

The normalized EVAR reading provides a probabilistic risk assessment:

< 0.3: Low risk environment with minimal tail concerns

0.3-0.5: Moderate risk with standard tail behavior

0.5-0.7: Elevated risk with increased probability of significant moves

> 0.7: High risk environment with substantial tail risk present

Position sizing is automatically calculated using an inverse relationship to EVAR, contracting during high-risk periods and expanding during low-risk conditions. This is a counter-cyclical approach that ensures consistent risk exposure across varying market regimes, especially when the market is hyped or overheated.

Parameter Optimization

For optimal risk assessment across market conditions:

Lookback Period: Determines the historical window for risk calculation

Q Parameter: Controls tail sensitivity (higher values increase conservatism)

Confidence Level: Sets the statistical threshold for risk assessment

For cryptocurrencies and highly volatile instruments, a q-parameter between 1.5-2.0 typically provides the most accurate risk assessment because it helps capturing the fat-tailed behavior characteristic of these markets. You can also increase the q-parameter for more conservative approaches.

Practical Applications

Adaptive Risk Management: Quantify and respond to changing tail risk conditions

Volatility-Normalized Positioning: Maintain consistent exposure across market regimes

Black Swan Detection: Early identification of potential extreme market conditions

Portfolio Construction: Apply consistent risk-based sizing across diverse instruments

This indicator is my own approach to entropy-based risk measures as an alterative to volatility and standard deviations and it helps with fat-tailed markets.

Enjoy!

Enhanced Gann Time-Price SquaresEnhanced Gann Time-Price Squares Indicator

A comprehensive Pine Script indicator that identifies and visualizes W.D. Gann's time-price square formations on your charts. This tool helps traders spot potential market turning points where time and price movements align according to Gann's legendary market theories.

Key Features:

Automatic Square Detection - Identifies completed squares where price movement equals time movement

Future Projections - Shows forming squares with projected completion points

Pivot Integration - Automatically detects pivot highs/lows as square starting points

Visual Clarity - Clean box outlines with customizable colors and styles

Smart Filtering - Prevents overlapping squares and includes minimum move thresholds

Real-time Status - Information table showing current square formations

How to Use:

The indicator draws boxes when price moves from pivot points equal the time elapsed (number of bars). Green squares indicate upward movements, red squares show downward movements. Dashed lines show forming squares, while dotted lines project where they might complete.

Settings:

Adjust pivot sensitivity and minimum price moves

Customize tolerance for time-price matching

Toggle projections, labels, and visual elements

Fine-tune colors and line styles

Perfect for Gann theory practitioners and traders looking for time-based market analysis. The squares often coincide with significant support/resistance levels and potential reversal points.

Compatible with all timeframes and instruments.

More updates to follow

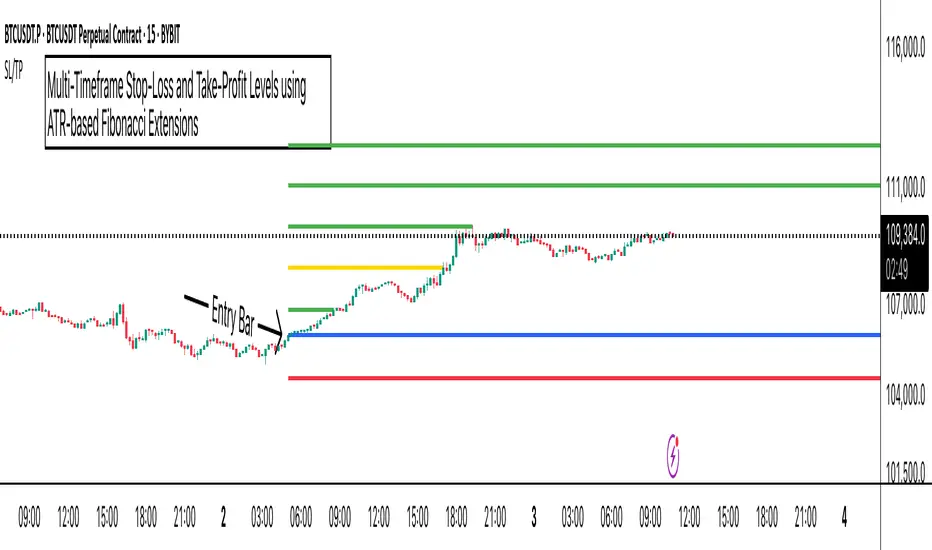

ATR Stop-Loss with Fibonacci Take-Profit [jpkxyz]ATR Stop-Loss with Fibonacci Take-Profit Indicator

This comprehensive indicator combines Average True Range (ATR) volatility analysis with Fibonacci extensions to create dynamic stop-loss and take-profit levels. It's designed to help traders set precise risk management levels and profit targets based on market volatility and mathematical ratios.

Two Operating Modes

Default Mode (Rolling Levels)

In default mode, the indicator continuously plots evolving stop-loss and take-profit levels based on real-time price action. These levels update dynamically as new bars form, creating rolling horizontal lines across the chart. I use this mode primarily to plot the rolling ATR-Level which I use to trail my Stop-Loss into profit.

Characteristics:

Levels recalculate with each new bar

All selected Fibonacci levels display simultaneously

Uses plot() functions with trackprice=true for price tracking

Custom Anchor Mode (Fixed Levels)

This is the primary mode for precision trading. You select a specific timestamp (typically your entry bar), and the indicator locks all calculations to that exact moment, creating fixed horizontal lines that represent your actual trade levels.

Characteristics:

Entry line (blue) marks your anchor point

Stop-loss calculated using ATR from the anchor bar

Fibonacci levels projected from entry-to-stop distance

Lines terminate when price breaks through them

Includes comprehensive alert system

Core Calculation Logic

ATR Stop-Loss Calculation:

Stop Loss = Entry Price ± (ATR × Multiplier)

Long positions: SL = Entry - (ATR × Multiplier)

Short positions: SL = Entry + (ATR × Multiplier)

ATR uses your chosen smoothing method (RMA, SMA, EMA, or WMA)

Default multiplier is 1.5, adjustable to your risk tolerance

Fibonacci Take-Profit Projection:

The distance from entry to stop-loss becomes the base unit (1.0) for Fibonacci extensions:

TP Level = Entry + (Entry-to-SL Distance × Fibonacci Ratio)

Available Fibonacci Levels:

Conservative: 0.618, 1.0, 1.618

Extended: 2.618, 3.618, 4.618

Complete range: 0.0 to 4.764 (23 levels total)

Multi-Timeframe Functionality

One of the indicator's most powerful features is timeframe flexibility. You can analyze on one timeframe while using stop-loss and take-profit calculations from another.

Best Practices:

Identify your entry point on execution timeframe

Enable "Custom Anchor" mode

Set anchor timestamp to your entry bar

Select appropriate analysis timeframe

Choose relevant Fibonacci levels

Enable alerts for automated notifications

Example Scenario:

Analyse trend on 4-hour chart

Execute entry on 5-minute chart for precision

Set custom anchor to your 5-minute entry bar

Configure timeframe setting to "4h" for swing-level targets

Select appropriate Fibonacci Extension levels

Result: Precise entry with larger timeframe risk management

Visual Intelligence System

Line Behaviour in Custom Anchor Mode:

Active levels: Lines extend to the right edge

Hit levels: Lines terminate at the breaking bar

Entry line: Always visible in blue

Stop-loss: Red line, terminates when hit

Take-profits: Green lines (1.618 level in gold for emphasis)

Customisation Options:

Line width (1-4 pixels)

Show/hide individual Fibonacci levels

ATR length and smoothing method

ATR multiplier for stop-loss distance

IU Fibonacci Levels For IntradayDESCRIPTION

This indicator draws intraday Fibonacci levels from the opening price of the day using percentage-based retracements. It helps traders identify potential intraday support and resistance zones derived from the day’s opening bias. The levels are dynamically calculated and displayed with optional labels and customizable colors, making it an effective tool for both breakout and mean-reversion intraday strategies.

USER INPUTS

Direction Of The Level

Choose whether to show Upside, Downside, or Both level sets based on your directional bias.

Show Labels of Levels

Option to enable or disable text labels displaying Fibonacci values and prices.

Individual Level Toggles & Colors

You can choose to show or hide each of the following Fibonacci levels and set their respective colors:

* 0.236

* 0.328

* 0.500

* 0.618

* 0.786

* 1.000

INDICATOR LOGIC

On the first bar of the session, the opening price is captured.

Fibonacci levels are then calculated above and below this open using percentage multipliers (for example, day\_open + (day\_open \* 0.236%) for the 0.236 level).

Depending on the selected direction, upside and/or downside levels are plotted.

Filled zones are drawn between levels to visually highlight key price zones.

Optionally, each level can be labeled with its Fibonacci value and price.

WHY IT IS UNIQUE

Unlike traditional swing-based Fibonacci retracements, this tool uses the day’s opening price as an anchor, specifically designed for intraday traders.

Allows traders to quickly visualize micro-support and resistance levels that adapt every day.

Highly customizable and easy to read, with filled level bands for better zone recognition.

Works independently of indicators like RSI, MACD, or moving averages – purely based on price action logic.

HOW USER CAN BENEFIT FROM IT

Spot precise intraday reversal zones or breakout regions.

Combine with price action or volume analysis for smarter entries.

Filter trades by choosing directional bias (Up Site, Down Site, or Both).

Set profit targets or stop-losses based on Fibonacci bands.

Works great for scalpers, day traders, and even short-term swing traders looking to align with opening price momentum.

Disclaimer

This indicator is not financial advice, it's for educational purposes only highlighting the power of coding( pine script) in TradingView, I am not a SEBI-registered advisor. Trading and investing involve risk, and you should consult with a qualified financial advisor before making any trading decisions. I do not guarantee profits or take responsibility for any losses you may incur.

[ BETA ][ IND ][ LIB ] Dynamic LookBack RSI RangeGet visual confirmation with this indicator if the current range selected had been oversold or overbough in the latest n bars

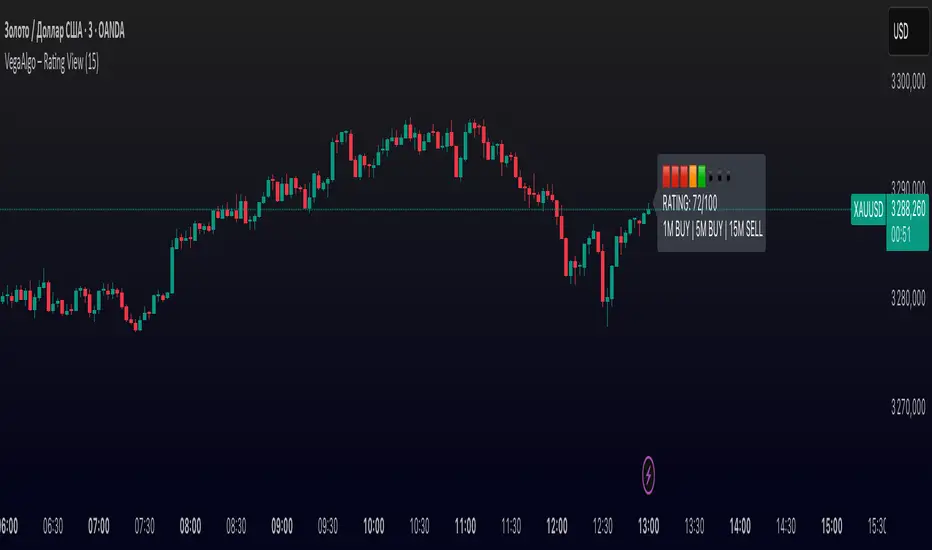

VegaAlgo – Rating ViewVegaAlgo – Rating View is a market condition analysis tool designed to evaluate the current price structure.

The indicator calculates a RATING (from 0 to 100) that reflects how clean, directional, and structured the recent price movement is. The rating is based on the number of price direction changes (from bullish to bearish candles and vice versa) within a selected period. Fewer direction changes indicate a clearer trend and result in a higher rating, while a choppy or highly volatile market leads to a lower score.

Additionally, the indicator provides directional signals on three key timeframes — 1M, 5M, and 15M, using a comparison of fast and slow moving averages. This allows traders to quickly assess the dominant trend both locally and across higher timeframes.

This script is intended for visual market analysis only and should not be considered financial advice.

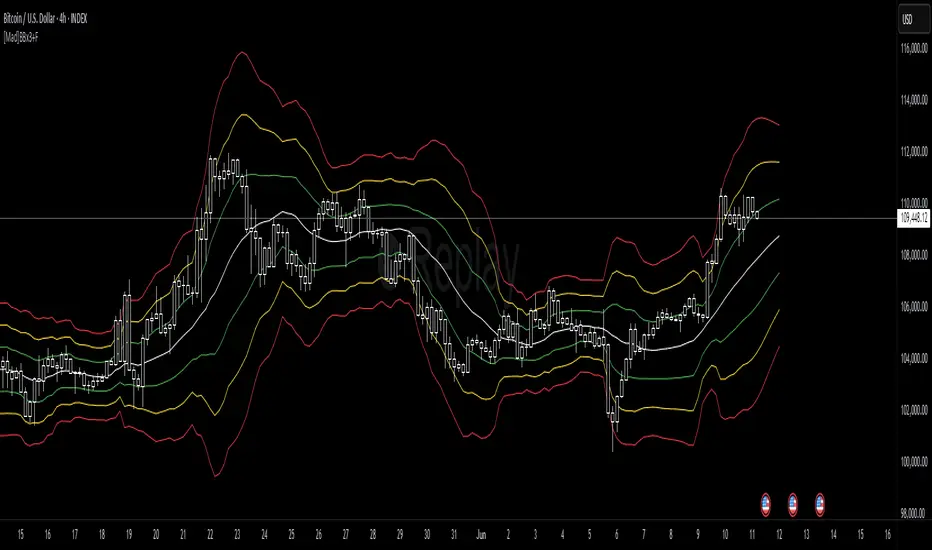

[Mad]Triple Bollinger Bands ForecastTriple Bollinger Bands Forecast (BBx3+F)

This open-source indicator is an advanced version of the classic Bollinger Bands, designed to provide a more comprehensive and forward-looking view of market volatility and potential price levels.

It plots three distinct sets of Bollinger Bands and projects them into the future based on statistical calculations.

How It Is Built and Key Features

Triple Bollinger Bands: Instead of a single set of bands, this indicator plots three. All three share the same central basis line (a Simple Moving Average), but each has a different standard deviation multiplier. This creates three distinct volatility zones for analyzing price deviation from its mean.

Multi-Timeframe (MTF) Capability: The indicator can calculate and display Bollinger Bands from a higher timeframe (e.g., showing daily bands on a 4-hour chart). This allows for contextualizing price action within the volatility structure of a more significant trend.

(Lower HTF selection will result in script-crash!)

Future Forecasting: This is the indicator's main feature. It projects the calculated Bollinger Bands up to 8 bars into the future. This forecast is a recalculation of the Simple Moving Average and Standard Deviation based on a projected future source price.

Selectable Forecast Methods: The mathematical model for estimating the future source price can be selected:

Flat: A model that uses the most recent closing price as the price for all future bars in the calculation window.

Linreg (Linear Regression): A model that calculates a linear regression trend on the last few bars and projects it forward to estimate the future source price.

Efficient Drawing with Polylines: The future projections are drawn on the chart using Pine Script's polyline object. This is an efficient method that draws the forecast data only on the last bar, which avoids repainting issues.

Differences from a Classical Bollinger Bands Indicator

Band Count: A classical indicator shows one set of bands. This indicator plots three sets for a multi-layered view of volatility.

Perspective: Classical Bollinger Bands are purely historical. This indicator is both historical and forward-looking .

Forecasting: The classic version has no forecasting capability. This indicator projects the bands into the future .

Timeframe: The classic version works only on the current timeframe. This indicator has full Multi-Timeframe (MTF) support .

The Mathematics Behind the Future Predictions

The core challenge in forecasting Bollinger Bands is that a future band value depends on future prices, which are unknown. This indicator solves this by simulating a future price series. Here is the step-by-step logic:

Forecast the Source Price for the Next Bar

First, the indicator estimates what the price will be on the next bar.

Flat Method: The forecasted price is the current bar's closing price.

Price_forecast = close

Linreg Method: A linear regression is calculated on the last few bars and extrapolated one step forward.

Price_forecast = ta.linreg(close, linreglen, 1)

Calculate the Future SMA (Basis)

To calculate the Simple Moving Average for the next bar, a new data window is simulated. This window includes the new forecasted price and drops the oldest historical price. For a 1-bar forecast, the calculation is:

SMA_future = (Price_forecast + close + close + ... + close ) / length

Calculate the Future Standard Deviation

Similarly, the standard deviation for the next bar is calculated over this same simulated window of prices, using the new SMA_future as its mean.

// 1. Calculate the sum of squared differences from the new mean

d_f = Price_forecast - SMA_future

d_0 = close - SMA_future

// ... and so on for the rest of the window's prices

SumOfSquares = (d_f)^2 + (d_0)^2 + ... + (d_length-2)^2

// 2. Calculate future variance and then the standard deviation

Var_future = SumOfSquares / length

StDev_future = sqrt(Var_future)

Extending the Forecast (2 to 8 Bars)

For forecasts further into the future (e.g., 2 bars), the script uses the same single Price_forecast for all future steps in the calculation. For a 2-bar forecast, the simulated window effectively contains the forecasted price twice, while dropping the two oldest historical prices. This provides a statistically-grounded projection of where the Bollinger Bands are likely to form.

Usage as a Forecast Extension

This indicator's functionality is designed to be modular. It can be used in conjunction with as example Mad Triple Bollinger Bands MTF script to separate the rendering of historical data from the forward-looking forecast.

Configuration for Combined Use:

Add both the Mad Triple Bollinger Bands MTF and this Triple Bollinger Bands Forecast indicator to your chart.

Open the Settings for this indicator (BBx3+F).

In the 'General Settings' tab, disable the Activate Plotting option.

To ensure data consistency, the Bollinger Length, Multipliers, and Higher Timeframe settings should be identical across both indicators.

This configuration prevents the rendering of duplicate historical bands. The Mad Triple Bollinger Bands MTF script will be responsible for visualizing the historical and current bands, while this script will overlay only the forward-projected polyline data.

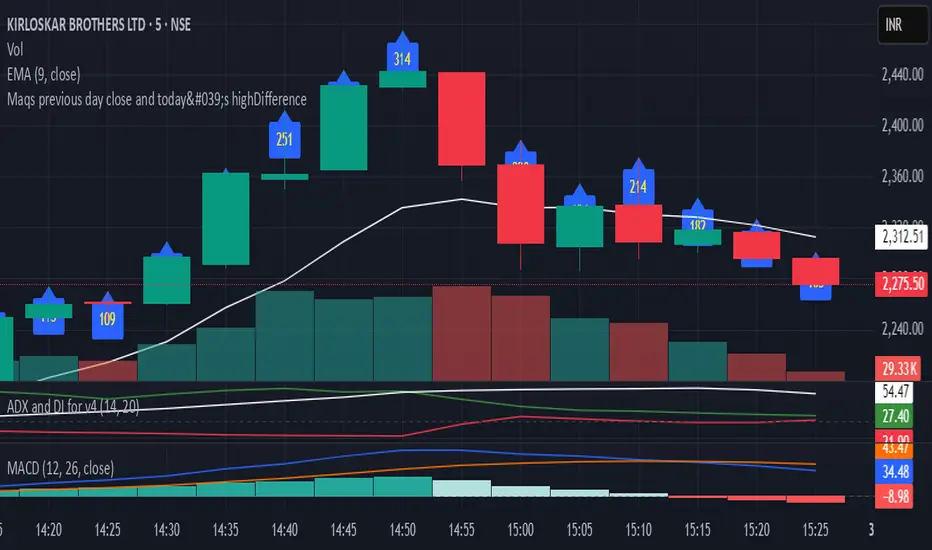

Maqs previous day close and today's highDifferenceIt gives previous day close and today's high Difference and hence capacity of the stock

Opening Range Breakout (ORB) with Fib RetracementOverview

“ORB with Fib Retracement” is a Pine Script indicator that anchors a full Fibonacci framework to the first minutes of the trading day (the opening-range breakout, or ORB).

After the ORB window closes the script:

Locks-in that session’s high and low.

Calculates a complete ladder of Fibonacci retracement levels between them (0 → 100 %).

Projects symmetric extension levels above and below the range (±1.618, ±2.618, ±3.618, ±4.618 by default).

Sub-divides every extension slice with additional 23.6 %, 38.2 %, 50 %, 61.8 % and 78.6 % mid-lines so each “zone” has its own inner fib grid.

Plots the whole structure and—optionally—extends every line into the future for ongoing reference.

**Session time / timezone** – Defines the ORB window (defaults 09:30–09:45 EST).

**Show All Fib Levels** – Toggles every retracement and extension line on or off.

**Show Extended Lines** – Draws dotted, extend-right projections of every level.

**Color group** – Assigns colors to buy-side (green), sell-side (red), and internal fibs (gray).

**Extension value inputs** – Allows custom +/- 1.618 to 4.618 fib levels for personalized projection zones.

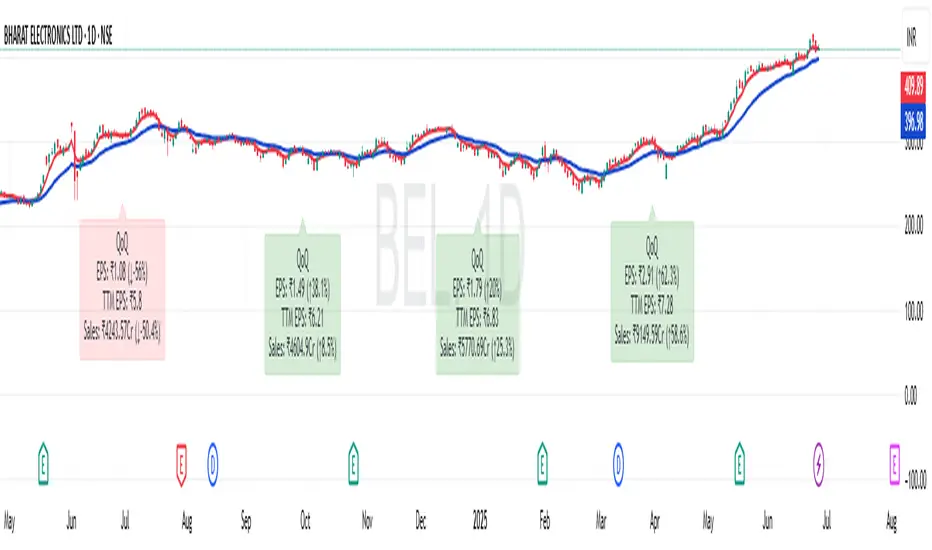

EPS and Sales Magic Indicator V2EPS and Sales Magic Indicator V2

EPS and Sales Magic Indicator V2

Short Title: EPS V2

Author: Trading_Tomm

Platform: TradingView (Pine Script v6)

License: Free for public use under fair usage guidelines

Overview

The EPS and Sales Magic Indicator V2 is a powerful stock fundamental visualization tool built specifically for TradingView users who wish to incorporate earnings intelligence directly onto their price chart. Designed and developed by Trading_Tomm, this upgraded version of the original 'EPS and Sales Magic Indicator' includes an enriched and more insightful presentation of company performance metrics — now with TTM EPS support, advanced color-coding, label sizing, and refined control options.

This indicator is tailored for retail traders, swing investors, and long-term fundamental analysts who need to view Quarter-over-Quarter (QoQ) earnings and revenue changes directly on the price chart without switching tabs or breaking focus.

What Does It Display?

The EPS and Sales Magic Indicator V2 intelligently detects quarterly financial updates and displays the following data points via labels:

1. EPS (Earnings Per Share) – Current Quarterly Value

This is the most recent Diluted EPS published by the company, fetched using TradingView’s request.financial() function.

Displayed in the format: EPS: ₹20.45

2. EPS QoQ Percentage Change

Shows the percentage change in EPS compared to the previous quarter.

Highlights improvement or decline using arrows (up for improvement, down for decline).

Displayed in the format: EPS: ₹20.45 (up 15.3 percent)

3. Sales (Revenue) – Current Quarterly Value

Fetches and displays Total Revenue of the company in ₹Crores for easier Indian-market readability.

Displayed in the format: Sales: ₹460Cr

4. Sales QoQ Percentage Change

Measures and presents the quarter-over-quarter percentage change in total revenue.

Uses arrows to indicate growth or contraction.

Displayed in the format: Sales: ₹460Cr (down 3.8 percent)

5. EPS TTM (Trailing Twelve Months)

You now get the TTM EPS — the sum of the last four quarterly EPS values.

This value provides a better long-term earnings snapshot compared to a single quarter.

Displayed in the format: TTM EPS: ₹78.12

All of these values are automatically calculated and displayed only on the bars where a new financial report is detected, keeping your chart clean and insightful.

Customization Features

This indicator is built with user control in mind, allowing you to personalize how and what you want to see:

Show EPS in Label: Enable or disable the display of EPS and EPS QoQ values.

Show Sales in Label: Toggle the visibility of revenue and sales change percentage.

Color Options for Label Themes: The label background color is automatically determined based on performance.

Green: Both EPS and Sales increased QoQ.

Red: Both decreased.

Orange: One increased and the other decreased.

Gray: Default color (if values are unavailable or mixed).

Label Text Size: Choose from Tiny, Small (default), or Normal.

Visual Design

Placement: The labels are positioned just below the candlesticks using yloc.belowbar, so they do not obstruct price action or interfere with technical indicators.

Anchor: Aligned precisely with the financial reporting bars to maintain clarity in historical comparisons.

Background Style: Clean, semi-transparent styling with soft text colors for comfortable viewing.

How It Works

The indicator relies on TradingView’s powerful request.financial() function to extract fiscal quarterly financials (FQ). Internally, it uses detection logic to identify fresh data updates by comparing current vs. previous values, arithmetic to compute QoQ percentage changes in EPS and Sales, logic to build formatted labels dynamically based on user selections, and conditional color and sizing logic to enhance interpretability.

Use Cases

For Long-Term Investors: Quickly identify if a company’s profitability and revenue are improving over time.

For Swing Traders: Combine recent earnings trends with price action to evaluate if post-result momentum has real backing.

For Technical and Fundamental Traders: Layer it with moving averages, RSI, or volume to create a hybrid analysis environment.

Limitations and Notes

Financial data is provided by TradingView’s financial API, and occasional missing values may occur for less-covered stocks.

This tool does not repaint but depends on the timing of the official financial updates.

All values are rounded and formatted to prioritize readability.

Works best on Daily or higher timeframes (weekly or monthly also supported).

License and Fair Use

This script is free to use and share under TradingView’s open-use guidelines. You may copy, fork, and build upon this indicator for personal or educational purposes, but commercial usage requires attribution to the author: Trading_Tomm.

Future Enhancements (Planned)

Addition of Net Profit (QoQ and TTM)

Inclusion of Operating Margin, Profit Margin, and Book Value

Option to switch between numeric and graphical display (table mode)

Alerts on extreme earnings deviation or sales slumps

Final Thoughts

The EPS and Sales Magic Indicator V2 represents a clean, visual, and smart way to monitor a company’s core performance from your chart screen. It helps you align fundamental strength with technical strategies and provides instant financial clarity, which is especially vital in today’s fast-moving markets.

Whether you’re preparing for an earnings season or scanning past performance to pick your next investment, this indicator saves time, enhances insights, and sharpens decisions.

Initial balance - weeklyWeekly Initial Balance (IB) — Indicator Description

The Weekly Initial Balance (IB) is the price range (High–Low) established during the week’s first trading session (most commonly Monday). You can measure it over the entire day or just the first X hours (e.g. 60 or 120 minutes). Once that session ends, the IB High and IB Low define the key levels where the initial weekly range formed.

Why Measure the Weekly IB?

Week-Opening Sentiment:

Monday’s range often sets the tone for the rest of the week. Trading above the IB High signals bullish control; trading below the IB Low signals bearish control.

Key Liquidity Zones:

Large institutions tend to place orders around these extremes, so you’ll frequently see tests, breakouts, or rejections at these levels.

Support & Resistance:

The IB High and IB Low become natural barriers. Price will often return to them, bounce off them, or break through them—ideal spots for entries and exits.

Volatility Forecast:

The width of the IB (High minus Low) indicates whether to expect a volatile week (wide IB) or a quieter one (narrow IB).

Significance of IB Levels

Breakout:

A clear break above the IB High (for longs) or below the IB Low (for shorts) can ignite a strong trending move.

Fade:

A rejection off the IB High/Low during low momentum (e.g. low volume or pin-bar formations) offers a high-probability reversal trade.

Mid-Point:

The 50% level of the IB range often “magnetizes” price back to it, providing entry points for continuation or reversal strategies.

Three Core Monday IB Strategies

A. Breakout (Open-Range Breakout)

Entry: Wait for 1–2 candles (e.g. 5-minute) to close above IB High (long) or below IB Low (short).

Stop-Loss: A few pips below IB High (long) or above IB Low (short).

Profit-Target: 2–3× your risk (Reward:Risk ≥ 2:1).

Best When: You spot a clear impulse—such as a strong pre-open volume spike or news-driven move.

B. Fade (Reversal at Extremes)

Entry: When price tests IB High but shows weakening momentum (shrinking volume, upper-wick candles), enter short; vice versa for IB Low and longs.

Stop-Loss: Just beyond the IB extreme you’re fading.

Profit-Target: Back toward the IB mid-point (50% level) or all the way to the opposite IB extreme.

Best When: Monday’s action is range-bound and lacks a clear directional trend.

C. Mid-Point Trading

Entry: When price returns to the 50% level of the IB range.

In an up-trend: buy if it bounces off mid-point back toward IB High.

In a down-trend: sell if it reverses off mid-point back toward IB Low.

Stop-Loss: Just below the nearest swing-low (for longs) or above the nearest swing-high (for shorts).

Profit-Target: To the corresponding IB extreme (High or Low).

Best When: You see a strong initial move away from the IB, followed by a pullback to the mid-point.

Usage Steps

Configure your session: Measure IB over your chosen Monday timeframe (whole day or first X hours).

Choose your strategy: Align Breakout, Fade, or Mid-Point entries with the current market context (trend vs. range).

Manage risk: Keep risk per trade ≤ 1% of account and maintain at least a 2:1 Reward:Risk ratio.

Backtest & forward-test: Verify performance over multiple Mondays and in a paper-trading environment before going live.

Candle Closer Levels & TP Zones📝 Description:

This indicator is designed to provide intrabar trade levels for high-speed execution strategies, such as scalping and intraday momentum trading.

🧩 Key Features:

Plots High, Low, Mid, and two Quarter Levels on the current candle only, keeping charts clean

Take Profit (TP) lines are calculated as a percentage of candle range, not fixed ticks — this makes it highly adaptable for futures like NQ/ES or volatile markets like crypto

Supports both long and short setups via a simple toggle

Customizable colors, line thickness, and length

Each TP level can be enabled or muted individually

📈 Use Case:

Apply this tool to spot candle-based breakouts or rejections. You can scale TPs dynamically based on the strength of the current candle. This is especially helpful in assets where volatility fluctuates greatly intrabar.

This is not a repackaged built-in indicator — it’s purpose-built for real-time tactical level plotting without historical noise.

Multi-Position DashMulti-Position Dash — Risk Dashboard for Forex, Stocks & Indices

Overview:

The Multi-Position Dash is a highly customizable trading dashboard designed to help active traders manage up to 8 simultaneous positions across Forex, Stocks, and Indices. Whether you're trading single entries, layering positions, using DCA (Dollar Cost Averaging), or running complex hedging setups, this tool provides essential, real-time risk and P&L insights—directly on your chart.

Key Features:

✔️ Supports Forex, Stocks, Indices — with automatic pip and contract conversions

✔️ Track up to 8 manual positions, each with customizable direction, lot size or contracts, entry price, Take Profit, and Stop Loss

✔️ Full GBP-based P&L and risk calculation, including automatic USD-to-GBP conversion for non-FX assets

✔️ Real-time display of:

Total potential Take Profit (GBP)

Total potential Stop Loss (GBP)

Risk % relative to account balance

Live P&L (GBP) based on current price

✔️ Breakeven price calculation, even across mixed-direction positions (DCA & hedging aware)

✔️ Visual breakeven line, live P&L arrows, and entry price markers

✔️ Shared Stop Loss option for all positions — perfect for DCA traders

✔️ Easy export strings for logging trades to external tools like spreadsheets

Ideal For:

✅ Forex traders using lot-based risk models

✅ Stock & Index traders wanting simplified contract-based position tracking

✅ Traders managing multiple active positions, with or without hedging

✅ Anyone needing at-a-glance P&L and risk monitoring, independent of broker platforms

Notes & Usage:

This is a manual tracking tool—you enter your positions, TP, SL levels, etc., and the dashboard calculates the rest. It does not place or manage live orders.

Supports both Long and Short positions.

All calculations are based on your inputs and market price—accuracy depends on maintaining your inputs properly.

Shared Stop Loss feature applies a single, unified stop across all active positions for simplified risk control in DCA setups.

GBP is used as the account currency—USD-to-GBP conversion is applied to stocks and indices as needed.

Disclaimer:

This tool is for educational and planning purposes only. It does not place or manage live trades, and is not a substitute for broker risk management tools. Always double-check your own position sizing and risk before placing live orders.

ATR FX DashboardATR FX Dashboard – Multi-Timeframe Volatility Monitor

Overview:

The ATR FX Dashboard provides a quick, at-a-glance view of market volatility across multiple timeframes for any forex pair. It uses the well-known Average True Range (ATR) indicator to display real-time volatility information in both pips and percentage terms, helping traders assess potential risk, position sizing, and market conditions.

How It Works:

This dashboard displays:

✔ ATR in Pips — The average price movement over a given timeframe, converted to pips for easy interpretation, automatically adjusting for JPY pairs.

✔ ATR as a Percentage of Price — Shows how significant the ATR is relative to the current price. Higher percentages often signal higher volatility or more active markets.

✔ Color-Coded Volatility Highlights — On the daily timeframe, ATR % cells are color-coded:

Green: High volatility

Orange: Moderate volatility

Red: Low volatility

Timeframes Displayed:

15 Minutes

1 Hour

4 Hour

Daily

This gives traders a clear, multi-timeframe view of short-term and broader market volatility conditions, directly on the chart.

Ideal For:

✅ Forex traders seeking quick, reliable volatility reference points

✅ Day traders and swing traders needing help with risk assessment and position sizing

✅ Anyone using ATR-based strategies or simply wanting to stay aware of changing market conditions

Additional Features:

Toggle option to display or hide ATR % relative to price

Automatic pip conversion for JPY pairs

Simple, clean table layout in the bottom-right corner of the chart

Supports all forex symbols

Disclaimer:

This tool is for informational purposes only and is not financial advice. As with all technical indicators, it should be used in conjunction with other tools and proper risk management.

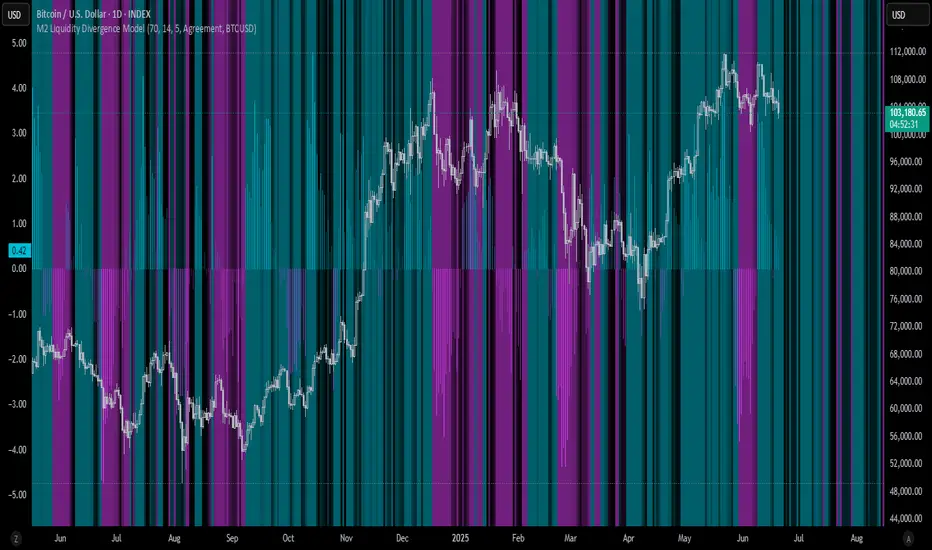

M2 Liquidity Divergence ModelM2 Liquidity Divergence Model

The M2 Liquidity Divergence Model is a macro-aware visualization tool designed to compare shifts in global liquidity (M2) against the performance of a benchmark asset (default: Bitcoin). This script captures liquidity flows across major global economies and highlights whether price action is aligned ("Agreement") or diverging ("Divergence") from macro trends.

🔍 Core Features

M2 Global Liquidity Index (GLI):

Aggregates M2 money supply from major global economies, FX-adjusted, including extended contributors like India, Brazil, and South Africa. The slope of this composite is used to infer macro liquidity trends.

Lag Offset Control:

Allows the M2 signal to lead benchmark asset price by a configurable number of days (Lag Offset), useful for modeling the forward-looking nature of macro flows.

Gradient Macro Context (Background):

Displays a color-gradient background—aqua for expansionary liquidity, fuchsia for contraction—based on the slope and volatility of M2. This contextual backdrop helps users visually anchor price action within macro shifts.

Divergence Histogram (Optional):

Plots a histogram showing dynamic correlation or divergence between the liquidity index and the selected benchmark.

Agreement Mode: M2 and asset are moving together.

Divergence Mode: Highlights break in expected macro-asset alignment.

Adaptive Transparency Scaling:

Histogram and background gradients scale their visual intensity based on statistical deviation to emphasize stronger signals.

Toggle Options:

Show/hide the M2 Liquidity Index line.

Show/hide divergence histogram.

Enable/disable visual offset of M2 to benchmark.

🧠 Suggested Usage

Macro Positioning: Use the background context to align directional trades with macro liquidity flows.

Disagreement as Signal: Use divergence plots to identify when price moves against macro expectations—potential reversal or exhaustion zones.

Time-Based Alignment: Adjust Lag Offset to synchronize M2 signals with asset price behavior across different market conditions.

⚠️ Disclaimer

This indicator is designed for educational and analytical purposes only. It does not constitute financial advice or an investment recommendation. Always conduct your own research and consult a licensed financial advisor before making trading decisions.

MNQ/NQ Risk Management ToolThis tool helps MNQ and NQ futures traders automatically calculate position size based on either a fixed dollar risk or a percentage of account balance.

Simply enter your stop loss level and choose whether to risk a set dollar amount or a percentage of your account. The script will display how many contracts to trade based on your setup.

Features:

Calculates contracts based on stop loss and risk size

Toggle between dollar-based or percent-of-account risk

Works with both MNQ ($2/point) and NQ ($20/point)

Automatically updates based on current price and direction (long or short)

Displays a clean info box on your chart with risk, contracts, and settings

This tool is ideal for intraday or swing traders who want to stay consistent with risk management across trades.

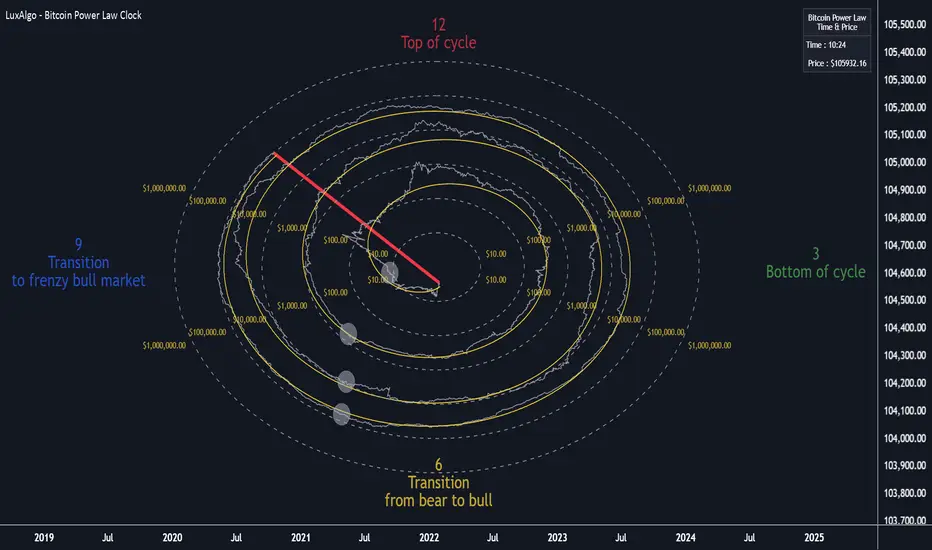

Bitcoin Power Law Clock [LuxAlgo]The Bitcoin Power Law Clock is a unique representation of Bitcoin prices proposed by famous Bitcoin analyst and modeler Giovanni Santostasi.

It displays a clock-like figure with the Bitcoin price and average lines as spirals, as well as the 12, 3, 6, and 9 hour marks as key points in the cycle.

🔶 USAGE

Giovanni Santostasi, Ph.D., is the creator and discoverer of the Bitcoin Power Law Theory. He is passionate about Bitcoin and has 12 years of experience analyzing it and creating price models.

As we can see in the above chart, the tool is super intuitive. It displays a clock-like figure with the current Bitcoin price at 10:20 on a 12-hour scale.

This tool only works on the 1D INDEX:BTCUSD chart. The ticker and timeframe must be exact to ensure proper functionality.

According to the Bitcoin Power Law Theory, the key cycle points are marked at the extremes of the clock: 12, 3, 6, and 9 hours. According to the theory, the current Bitcoin prices are in a frenzied bull market on their way to the top of the cycle.

🔹 Enable/Disable Elements

All of the elements on the clock can be disabled. If you disable them all, only an empty space will remain.

The different charts above show various combinations. Traders can customize the tool to their needs.

🔹 Auto scale

The clock has an auto-scale feature that is enabled by default. Traders can adjust the size of the clock by disabling this feature and setting the size in the settings panel.

The image above shows different configurations of this feature.

🔶 SETTINGS

🔹 Price

Price: Enable/disable price spiral, select color, and enable/disable curved mode

Average: Enable/disable average spiral, select color, and enable/disable curved mode

🔹 Style

Auto scale: Enable/disable automatic scaling or set manual fixed scaling for the spirals

Lines width: Width of each spiral line

Text Size: Select text size for date tags and price scales

Prices: Enable/disable price scales on the x-axis

Handle: Enable/disable clock handle

Halvings: Enable/disable Halvings

Hours: Enable/disable hours and key cycle points

🔹 Time & Price Dashboard

Show Time & Price: Enable/disable time & price dashboard

Location: Dashboard location

Size: Dashboard size