Grothendieck-Teichmüller Geometric SynthesisDskyz's Grothendieck-Teichmüller Geometric Synthesis (GTGS)

THEORETICAL FOUNDATION: A SYMPHONY OF GEOMETRIES

The 🎓 GTGS is built upon a revolutionary premise: that market dynamics can be modeled as geometric and topological structures. While not a literal academic implementation—such a task would demand computational power far beyond current trading platforms—it leverages core ideas from advanced mathematical theories as powerful analogies and frameworks for its algorithms. Each component translates an abstract concept into a practical market calculation, distinguishing GTGS by identifying deeper structural patterns rather than relying on standard statistical measures.

1. Grothendieck-Teichmüller Theory: Deforming Market Structure

The Theory : Studies symmetries and deformations of geometric objects, focusing on the "absolute" structure of mathematical spaces.

Indicator Analogy : The calculate_grothendieck_field function models price action as a "deformation" from its immediate state. Using the nth root of price ratios (math.pow(price_ratio, 1.0/prime)), it measures market "shape" stretching or compression, revealing underlying tensions and potential shifts.

2. Topos Theory & Sheaf Cohomology: From Local to Global Patterns

The Theory : A framework for assembling local properties into a global picture, with cohomology measuring "obstructions" to consistency.

Indicator Analogy : The calculate_topos_coherence function uses sine waves (math.sin) to represent local price "sections." Summing these yields a "cohomology" value, quantifying price action consistency. High values indicate coherent trends; low values signal conflict and uncertainty.

3. Tropical Geometry: Simplifying Complexity

The Theory : Transforms complex multiplicative problems into simpler, additive, piecewise-linear ones using min(a, b) for addition and a + b for multiplication.

Indicator Analogy : The calculate_tropical_metric function applies tropical_add(a, b) => math.min(a, b) to identify the "lowest energy" state among recent price points, pinpointing critical support levels non-linearly.

4. Motivic Cohomology & Non-Commutative Geometry

The Theory : Studies deep arithmetic and quantum-like properties of geometric spaces.

Indicator Analogy : The motivic_rank and spectral_triple functions compute weighted sums of historical prices to capture market "arithmetic complexity" and "spectral signature." Higher values reflect structured, harmonic price movements.

5. Perfectoid Spaces & Homotopy Type Theory

The Theory : Abstract fields dealing with p-adic numbers and logical foundations of mathematics.

Indicator Analogy : The perfectoid_conv and type_coherence functions analyze price convergence and path identity, assessing the "fractal dust" of price differences and price path cohesion, adding fractal and logical analysis.

The Combination is Key : No single theory dominates. GTGS ’s Unified Field synthesizes all seven perspectives into a comprehensive score, ensuring signals reflect deep structural alignment across mathematical domains.

🎛️ INPUTS: CONFIGURING THE GEOMETRIC ENGINE

The GTGS offers a suite of customizable inputs, allowing traders to tailor its behavior to specific timeframes, market sectors, and trading styles. Below is a detailed breakdown of key input groups, their functionality, and optimization strategies, leveraging provided tooltips for precision.

Grothendieck-Teichmüller Theory Inputs

🧬 Deformation Depth (Absolute Galois) :

What It Is : Controls the depth of Galois group deformations analyzed in market structure.

How It Works : Measures price action deformations under automorphisms of the absolute Galois group, capturing market symmetries.

Optimization :

Higher Values (15-20) : Captures deeper symmetries, ideal for major trends in swing trading (4H-1D).

Lower Values (3-8) : Responsive to local deformations, suited for scalping (1-5min).

Timeframes :

Scalping (1-5min) : 3-6 for quick local shifts.

Day Trading (15min-1H) : 8-12 for balanced analysis.

Swing Trading (4H-1D) : 12-20 for deep structural trends.

Sectors :

Stocks : Use 8-12 for stable trends.

Crypto : 3-8 for volatile, short-term moves.

Forex : 12-15 for smooth, cyclical patterns.

Pro Tip : Increase in trending markets to filter noise; decrease in choppy markets for sensitivity.

🗼 Teichmüller Tower Height :

What It Is : Determines the height of the Teichmüller modular tower for hierarchical pattern detection.

How It Works : Builds modular levels to identify nested market patterns.

Optimization :

Higher Values (6-8) : Detects complex fractals, ideal for swing trading.

Lower Values (2-4) : Focuses on primary patterns, faster for scalping.

Timeframes :

Scalping : 2-3 for speed.

Day Trading : 4-5 for balanced patterns.

Swing Trading : 5-8 for deep fractals.

Sectors :

Indices : 5-8 for robust, long-term patterns.

Crypto : 2-4 for rapid shifts.

Commodities : 4-6 for cyclical trends.

Pro Tip : Higher towers reveal hidden fractals but may slow computation; adjust based on hardware.

🔢 Galois Prime Base :

What It Is : Sets the prime base for Galois field computations.

How It Works : Defines the field extension characteristic for market analysis.

Optimization :

Prime Characteristics :

2 : Binary markets (up/down).

3 : Ternary states (bull/bear/neutral).

5 : Pentagonal symmetry (Elliott waves).

7 : Heptagonal cycles (weekly patterns).

11,13,17,19 : Higher-order patterns.

Timeframes :

Scalping/Day Trading : 2 or 3 for simplicity.

Swing Trading : 5 or 7 for wave or cycle detection.

Sectors :

Forex : 5 for Elliott wave alignment.

Stocks : 7 for weekly cycle consistency.

Crypto : 3 for volatile state shifts.

Pro Tip : Use 7 for most markets; 5 for Elliott wave traders.

Topos Theory & Sheaf Cohomology Inputs

🏛️ Temporal Site Size :

What It Is : Defines the number of time points in the topological site.

How It Works : Sets the local neighborhood for sheaf computations, affecting cohomology smoothness.

Optimization :

Higher Values (30-50) : Smoother cohomology, better for trends in swing trading.

Lower Values (5-15) : Responsive, ideal for reversals in scalping.

Timeframes :

Scalping : 5-10 for quick responses.

Day Trading : 15-25 for balanced analysis.

Swing Trading : 25-50 for smooth trends.

Sectors :

Stocks : 25-35 for stable trends.

Crypto : 5-15 for volatility.

Forex : 20-30 for smooth cycles.

Pro Tip : Match site size to your average holding period in bars for optimal coherence.

📐 Sheaf Cohomology Degree :

What It Is : Sets the maximum degree of cohomology groups computed.

How It Works : Higher degrees capture complex topological obstructions.

Optimization :

Degree Meanings :

1 : Simple obstructions (basic support/resistance).

2 : Cohomological pairs (double tops/bottoms).

3 : Triple intersections (complex patterns).

4-5 : Higher-order structures (rare events).

Timeframes :

Scalping/Day Trading : 1-2 for simplicity.

Swing Trading : 3 for complex patterns.

Sectors :

Indices : 2-3 for robust patterns.

Crypto : 1-2 for rapid shifts.

Commodities : 3-4 for cyclical events.

Pro Tip : Degree 3 is optimal for most trading; higher degrees for research or rare event detection.

🌐 Grothendieck Topology :

What It Is : Chooses the Grothendieck topology for the site.

How It Works : Affects how local data integrates into global patterns.

Optimization :

Topology Characteristics :

Étale : Finest topology, captures local-global principles.

Nisnevich : A1-invariant, good for trends.

Zariski : Coarse but robust, filters noise.

Fpqc : Faithfully flat, highly sensitive.

Sectors :

Stocks : Zariski for stability.

Crypto : Étale for sensitivity.

Forex : Nisnevich for smooth trends.

Indices : Zariski for robustness.

Timeframes :

Scalping : Étale for precision.

Swing Trading : Nisnevich or Zariski for reliability.

Pro Tip : Start with Étale for precision; switch to Zariski in noisy markets.

Unified Field Configuration Inputs

⚛️ Field Coupling Constant :

What It Is : Sets the interaction strength between geometric components.

How It Works : Controls signal amplification in the unified field equation.

Optimization :

Higher Values (0.5-1.0) : Strong coupling, amplified signals for ranging markets.

Lower Values (0.001-0.1) : Subtle signals for trending markets.

Timeframes :

Scalping : 0.5-0.8 for quick, strong signals.

Swing Trading : 0.1-0.3 for trend confirmation.

Sectors :

Crypto : 0.5-1.0 for volatility.

Stocks : 0.1-0.3 for stability.

Forex : 0.3-0.5 for balance.

Pro Tip : Default 0.137 (fine structure constant) is a balanced starting point; adjust up in choppy markets.

📐 Geometric Weighting Scheme :

What It Is : Determines the framework for combining geometric components.

How It Works : Adjusts emphasis on different mathematical structures.

Optimization :

Scheme Characteristics :

Canonical : Equal weighting, balanced.

Derived : Emphasizes higher-order structures.

Motivic : Prioritizes arithmetic properties.

Spectral : Focuses on frequency domain.

Sectors :

Stocks : Canonical for balance.

Crypto : Spectral for volatility.

Forex : Derived for structured moves.

Indices : Motivic for arithmetic cycles.

Timeframes :

Day Trading : Canonical or Derived for flexibility.

Swing Trading : Motivic for long-term cycles.

Pro Tip : Start with Canonical; experiment with Spectral in volatile markets.

Dashboard and Visual Configuration Inputs

📋 Show Enhanced Dashboard, 📏 Size, 📍 Position :

What They Are : Control dashboard visibility, size, and placement.

How They Work : Display key metrics like Unified Field , Resonance , and Signal Quality .

Optimization :

Scalping : Small size, Bottom Right for minimal chart obstruction.

Swing Trading : Large size, Top Right for detailed analysis.

Sectors : Universal across markets; adjust size based on screen setup.

Pro Tip : Use Large for analysis, Small for live trading.

📐 Show Motivic Cohomology Bands, 🌊 Morphism Flow, 🔮 Future Projection, 🔷 Holographic Mesh, ⚛️ Spectral Flow :

What They Are : Toggle visual elements representing mathematical calculations.

How They Work : Provide intuitive representations of market dynamics.

Optimization :

Timeframes :

Scalping : Enable Morphism Flow and Spectral Flow for momentum.

Swing Trading : Enable all for comprehensive analysis.

Sectors :

Crypto : Emphasize Morphism Flow and Future Projection for volatility.

Stocks : Focus on Cohomology Bands for stable trends.

Pro Tip : Disable non-essential visuals in fast markets to reduce clutter.

🌫️ Field Transparency, 🔄 Web Recursion Depth, 🎨 Mesh Color Scheme :

What They Are : Adjust visual clarity, complexity, and color.

How They Work : Enhance interpretability of visual elements.

Optimization :

Transparency : 30-50 for balanced visibility; lower for analysis.

Recursion Depth : 6-8 for balanced detail; lower for older hardware.

Color Scheme :

Purple/Blue : Analytical focus.

Green/Orange : Trading momentum.

Pro Tip : Use Neon Purple for deep analysis; Neon Green for active trading.

⏱️ Minimum Bars Between Signals :

What It Is : Minimum number of bars required between consecutive signals.

How It Works : Prevents signal clustering by enforcing a cooldown period.

Optimization :

Higher Values (10-20) : Fewer signals, avoids whipsaws, suited for swing trading.

Lower Values (0-5) : More responsive, allows quick reversals, ideal for scalping.

Timeframes :

Scalping : 0-2 bars for rapid signals.

Day Trading : 3-5 bars for balance.

Swing Trading : 5-10 bars for stability.

Sectors :

Crypto : 0-3 for volatility.

Stocks : 5-10 for trend clarity.

Forex : 3-7 for cyclical moves.

Pro Tip : Increase in choppy markets to filter noise.

Hardcoded Parameters

Tropical, Motivic, Spectral, Perfectoid, Homotopy Inputs : Fixed to optimize performance but influence calculations (e.g., tropical_degree=4 for support levels, perfectoid_prime=5 for convergence).

Optimization : Experiment with codebase modifications if advanced customization is needed, but defaults are robust across markets.

🎨 ADVANCED VISUAL SYSTEM: TRADING IN A GEOMETRIC UNIVERSE

The GTTMTSF ’s visuals are direct representations of its mathematics, designed for intuitive and precise trading decisions.

Motivic Cohomology Bands :

What They Are : Dynamic bands ( H⁰ , H¹ , H² ) representing cohomological support/resistance.

Color & Meaning : Colors reflect energy levels ( H⁰ tightest, H² widest). Breaks into H¹ signal momentum; H² touches suggest reversals.

How to Trade : Use for stop-loss/profit-taking. Band bounces with Dashboard confirmation are high-probability setups.

Morphism Flow (Webbing) :

What It Is : White particle streams visualizing market momentum.

Interpretation : Dense flows indicate strong trends; sparse flows signal consolidation.

How to Trade : Follow dominant flow direction; new flows post-consolidation signal trend starts.

Future Projection Web (Fractal Grid) :

What It Is : Fibonacci-period fractal projections of support/resistance.

Color & Meaning : Three-layer lines (white shadow, glow, colored quantum) with labels showing price, topological class, anomaly strength (φ), resonance (ρ), and obstruction ( H¹ ). ⚡ marks extreme anomalies.

How to Trade : Target ⚡/● levels for entries/exits. High-anomaly levels with weakening Unified Field are reversal setups.

Holographic Mesh & Spectral Flow :

What They Are : Visuals of harmonic interference and spectral energy.

How to Trade : Bright mesh nodes or strong Spectral Flow warn of building pressure before price movement.

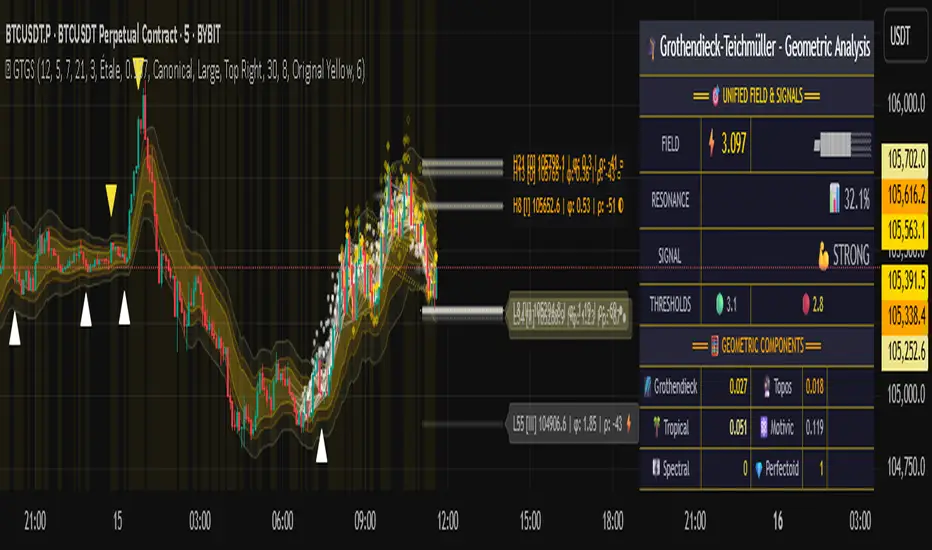

📊 THE GEOMETRIC DASHBOARD: YOUR MISSION CONTROL

The Dashboard translates complex mathematics into actionable intelligence.

Unified Field & Signals :

FIELD : Master value (-10 to +10), synthesizing all geometric components. Extreme readings (>5 or <-5) signal structural limits, often preceding reversals or continuations.

RESONANCE : Measures harmony between geometric field and price-volume momentum. Positive amplifies bullish moves; negative amplifies bearish moves.

SIGNAL QUALITY : Confidence meter rating alignment. Trade only STRONG or EXCEPTIONAL signals for high-probability setups.

Geometric Components :

What They Are : Breakdown of seven mathematical engines.

How to Use : Watch for convergence. A strong Unified Field is reliable when components (e.g., Grothendieck , Topos , Motivic ) align. Divergence warns of trend weakening.

Signal Performance :

What It Is : Tracks indicator signal performance.

How to Use : Assesses real-time performance to build confidence and understand system behavior.

🚀 DEVELOPMENT & UNIQUENESS: BEYOND CONVENTIONAL ANALYSIS

The GTTMTSF was developed to analyze markets as evolving geometric objects, not statistical time-series.

Why This Is Unlike Anything Else :

Theoretical Depth : Uses geometry and topology, identifying patterns invisible to statistical tools.

Holistic Synthesis : Integrates seven deep mathematical frameworks into a cohesive Unified Field .

Creative Implementation : Translates PhD-level mathematics into functional Pine Script , blending theory and practice.

Immersive Visualization : Transforms charts into dynamic geometric landscapes for intuitive market understanding.

The GTTMTSF is more than an indicator; it’s a new lens for viewing markets, for traders seeking deeper insight into hidden order within chaos.

" Where there is matter, there is geometry. " - Johannes Kepler

— Dskyz , Trade with insight. Trade with anticipation.

M-oscillator

Momentum ScopeOverview

Momentum Scope is a Pine Script™ v6 study that renders a –1 to +1 momentum heatmap across up to 32 lookback periods in its own pane. Using an Augmented Relative Momentum Index (ARMI) and color shading, it highlights where momentum strengthens, weakens, or stays flat over time—across any asset and timeframe.

Key Features

Full-Spectrum Momentum Map : Computes ARMI for 1–32 lookbacks, indexed from –1 (strong bearish) to +1 (strong bullish).

Flexible Scale Gradation : Choose Linear or Exponential spacing, with adjustable expansion ratio and maximum depth.

Trending Bias Control : Apply a contrast-style curve transform to emphasize trending vs. mean-reverting behavior.

Duotone & Tritone Palettes : Select between two vivid color styles, with user-definable hues for bearish, bullish, and neutral momentum.

Compact, Overlay-Free Display : Renders solely in its own pane—keeping your price chart clean.

Inputs & Customization

Scale Gradation : Linear or Exponential spacing of intervals

Scale Expansion : Ratio governing step-size between successive lookbacks

Scale Maximum : Maximum lookback period (and highest interval)

Trending Bias : Curve-transform bias to tilt the –1 … +1 grid

Color Style : Duotone or Tritone rendering modes

Reducing / Increasing / Neutral Colors : Pick your own hues for bearish, bullish, and flat zones

How to Use

Add to Chart : Apply “Momentum Scope” as a separate indicator.

Adjust Scale : For exponential spacing, switch your indicator Y-axis to Logarithmic .

Set Bias & Colors : Tweak Trending Bias and choose a palette that stands out on your layout.

Interpret the Heatmap :

Red tones = weakening/bearish momentum

Green tones = strengthening/bullish momentum

Neutral hues = indecision or flat momentum

Copyright © 2025 MVPMC. Licensed under MIT. For full license see opensource.org

Market Sell-Off GaugeOVERVIEW

The Market Sell‑Off Gauge identifies high‑conviction, risk‑off entry opportunities by detecting broad market sell‑off behavior and rising stablecoin dominance, then confirming risk‑off sentiment via NDX weakness, VIX spikes, and elevated volume. It uses fuzzy logic and sigmoid scaling to convert raw signals into a smooth, bounded metric.

FEATURES

Sell‑Off Detection - calculates percentage drops in the primary asset over a user‑defined lookback.

Stablecoin Dominance Surge - tracks combined USDT/USDC dominance rises as a proxy for on‑chain “flight to safety.”

Macro Confirmation

NDX Weakness (NASDAQ‑100)

VIX Spikes (CBOE Volatility Index)

Elevated Volume on declining bars

Fuzzy Logic & Scaling - component values feed into a fuzzy‑logic membership scor and are passed through a sigmoid compressor (–1 to +1). Weighted aggregation derives the final result of the gauge (or metric).

VISUALISATION

Continuous line plot - Smoothed metric (–1 to +1), colored cold‑to‑warm.

Entry circles - Highlighted when all conditions (fuzzy or crisp) are met after the time offset.

Time‑Offset marker - Vertical line/label showing the user‑specified “start” bar.

Component table - Displays real‑time % changes & volume multiples in the lower right of the indicator.

USAGE

Asset drop % - The threshold percent decline to register a sell‑off.

Stables rise % - The threshold percent increase in stablecoin dominance to qualify as a “flight to safety.”

NDX drop % - The threshold percent decline in the NASDAQ‑100 for macro confirmation.

VIX rise % - The threshold percent increase in VIX. Contributes to risk‑off validation.

Volume Multiplier - Defines how many times above SMA volume must rise to confirm conviction.

Lookback Period - Controls the number of bars over which % changes are measured.

Time Offset - Point in time beyond which bars to “fade” historical signals, enables focus on recent data only.

Fuzzy Logic Settings - Enables fuzzy scoring and set membership threshold & sensitivity.

Weights - allows for adjusting the relative importance of each component (Asset, Stables, NDX, VIX, Volume).

Sigmoid Steepness (k) - Controls curve steepness for compression (0.1 = very flat → 5.0 = very sharp S‑curve).

Chart & settings

Best applied on 4H or Daily BTCUSD (or similar) charts to capture meaningful sell‑off events.

Combine with broader trend filters (e.g., moving averages) for trend‑aligned entries.

Adjust Sigmoid Steepness and Membership Sensitivity to fine‑tune signal crispness vs. smoothness. Refer to tooltips.

Disclaimer

This indicator is intended for educational purposes only. Always perform your own due diligence before making financial decisions.

Flux Capacitor (FC)# Flux Capacitor

**A volume-weighted, outlier-resistant momentum oscillator designed to expose hidden directional pressure from institutional participants.**

---

### Why "Flux Capacitor"?

The name pays homage to the fictional energy core in *Back to the Future* — an invisible engine that powers movement. Similarly, this indicator detects whether price movement is being powered by real market participation (volume) or if it's coasting without conviction.

---

### Methodology

The Flux Capacitor fuses three statistical layers:

- **Normalized Momentum**: `(Close – Open) / ATR`

Controls for raw price size and volatility.

- **Volume Scaling**:

Amplifies the effect of price moves that occur with elevated volume.

- **Robust Normalization**:

- *Winsorization* caps outlier spikes.

- *MAD-Z scoring* normalizes the signal across assets (crypto, futures, stocks).

- This produces consistent scaling across timeframes and symbols.

The result is a smooth oscillator that reliably indicates **liquidity-backed momentum** — not just price movement.

---

### Signal Events

- **Divergence (D)**: Price makes higher highs or lower lows, but Flux does not.

- **Absorption (A)**: Candle shows high volume and small body, while Flux opposes the candle direction — indicates smart money stepping in.

- **Compression (◆)**: High volume with low momentum — potential breakout zone.

- **Zero-Cross**: Indicates directional regime flip.

- **Flux Acceleration**: Histogram shows pressure rate of change.

- **Regime Background**: Color fades with weakening trend conviction.

All signals are color-coded and visually compact for easy pattern recognition.

---

### Interpreting Divergence & Absorption Correctly

Signal strength improves significantly when it appears **in the correct zone**:

#### Divergence:

| Signal | Zone | Meaning | Strength |

|--------|------------|------------------------------------------|--------------|

| Green D | Below 0 | Bullish reversal forming in weakness | **Strong** |

| Green D | Above 0 | Bullish, but less convincing | Moderate |

| Red D | Above 0 | Bearish reversal forming in strength | **Strong** |

| Red D | Below 0 | Bearish continuation — low warning value | Weak |

#### Absorption:

| Signal | Zone | Meaning | Strength |

|--------|------------|-----------------------------------------|--------------|

| Green A | Below 0 | Buyers absorbing panic-selling | **Strong** |

| Green A | Above 0 | Support continuation | Moderate |

| Red A | Above 0 | Sellers absorbing FOMO buying | **Strong** |

| Red A | Below 0 | Trend continuation — not actionable | Weak |

Look for **absorption or divergence signals in “enemy territory”** for the most actionable entries.

---

### Reducing Visual Footprint

If your chart shows a long line of numbers across the top of the Flux Capacitor pane (e.g. "FC 14 20 9 ... Bottom Right"), it’s due to TradingView’s *status line input display*.

**To fix this**:

Right-click the indicator pane → **Settings** → **Status Line** tab → uncheck “Show Indicator Arguments”.

This frees up vertical space so top-edge signals (like red `D` or yellow `◆`) remain visible and unobstructed.

---

### Features

- Original MAD-Z based momentum design

- True volume-based divergence and absorption logic

- Built-in alerts for all signal types

- Works across timeframes (1-min to weekly)

- Minimalist, responsive layout

- 25+ customizable parameters

- No future leaks, no repainting

---

### Usage Scenarios

- **Trend confirmation**: Flux > 0 confirms bullish trend strength

- **Reversal detection**: Divergence or absorption in opposite territory = high-probability reversal

- **Breakout anticipation**: Compression signal inside range often precedes directional move

- **Momentum shifts**: Watch for zero-crosses + flux acceleration spikes

---

### ⚠ Visual Note for BTC, ETH, Crude Oil & Futures

These high-priced or rapidly accelerating instruments can visually compress any linear oscillator. You may notice the Flux Capacitor’s line appears "flat" or muted on these assets — especially over long lookbacks.

> **This does not affect signal validity.** Divergence, absorption, and compression triggers still fire based on underlying logic — only the line’s amplitude appears reduced due to scaling constraints.

---

### Disclaimer

This indicator is for educational purposes only. It is not trading advice. Past results do not guarantee future performance. Use in combination with your own risk management and analysis.

Chaikin Bull-Power OscillatorThis indicator is given with much love and care to the community to help you in your trading operations.

How to use the "Chaikin-Bull-PW" Indicator

The Chaikin-Bull-PW is an oscillator based on the Accumulation/Distribution (AD) line smoothed by different methods, called here the "Hull Chaikin Oscillator." It compares two smoothed averages of the AD line — a short period and a long period — to indicate the strength and direction of buying and selling pressure in the market.

Adjustable Parameters:

Short Period: Number of bars used to calculate the short smoothed average of the AD line. Shorter periods make the indicator more sensitive.

Long Period: Number of bars used to calculate the long smoothed average of the AD line. Longer periods smooth the indicator more.

Background Offset: Controls the offset of the chart’s background color.

Smoothing Type: Choose the smoothing method for the AD line among HMA, SMA, SMMA, EMA, WMA, and JMA. This affects how the averages are calculated and how the oscillator responds to price.

Indicator Interpretation:

The oscillator is the difference between the short and long smoothed averages of the AD line.

When the oscillator is above zero (green), it indicates increasing buying pressure, suggesting an uptrend.

When the oscillator is below zero (red), it indicates increasing selling pressure, suggesting a downtrend.

The zero line acts as a reference for trend changes.

Usage Suggestions:

Use the oscillator crossing the zero line to identify potential entry or exit points.

Combine with other indicators or chart analysis to confirm signals.

Adjust the periods and smoothing type to fit your asset and timeframe.

BB Oscillator - Price Relative to Bollinger BandsThis Bollinger Band Oscillator visualizes where the current price sits relative to its Bollinger Bands, scaled between 0 and 100. It helps identify overbought and oversold conditions based on the price’s position within the bands and provides dynamic signals when momentum shifts occur.

Features

Price Relative to Bollinger Bands

The main oscillator plots the price’s relative position within the Bollinger Bands on a scale from 0 (lower band) to 100 (upper band), giving an intuitive view of where price stands.

Customizable Moving Average Overlay

An optional moving average (SMA or EMA) smooths the oscillator for trend analysis, with adjustable length and color options.

Crossover & Crossunder Signals

Alerts and background highlights trigger when the oscillator crosses over or under its moving average, signaling potential momentum shifts or trend changes.

Fully Customizable Colors

Choose your preferred colors for the oscillator line, moving average and crossover signals to match your charting style.

This tool offers a unique oscillator view of Bollinger Bands, combining volatility context with momentum signals for clearer decision-making.

Market Strength Buy Sell Indicator [TradeDots]A specialized tool designed to assist traders in evaluating market conditions through a multifaceted analysis of relative performance, beta-adjusted returns, momentum, and volume—allowing you to identify optimal points for long or short trades. By integrating multiple benchmarks (default S&P 500) and percentile-based thresholds, the script provides clear, actionable insights suitable for both day trading and higher-level timeframe assessments.

📝 HOW IT WORKS

1. Multi-Factor Composite Score

Relative Performance (RS Ratio): Compares your asset’s performance to a chosen benchmark (default: SPY). Values above 1.0 indicate outperformance, while below 1.0 suggest underperformance.

Beta-Adjusted Returns: Checks the ticker’s excess movement relative to expected market-related moves. This helps distinguish pure “alpha” from broad market effects.

Volume & Correlation: Volume spikes often confirm the momentum behind a move, while correlation measures how closely the asset tracks or diverges from its benchmark.

These components merge into a 0–100 composite score. Scores above 50 frequently imply bullish strength; drops below 50 often point to underperformance—potentially flagging short opportunities.

2. Intraday & Day Trading Focus

Monitoring Below 50: During the trading day, the script calculates live data against the benchmark, offering an intraday-sensitive composite score. A dip under 50 may indicate a short bias for that session, especially when accompanied by high volume or momentum shifts.

3. Higher Timeframe Monitoring

Daily Strategies: On daily or weekly charts, the script reveals overall relative strength or weakness compared to the S&P 500. This higher-level perspective helps form broader trading biases—crucial for swing or position trades spanning multiple days.

Long/Short Thresholds: Persistent readings above 50 on a daily chart typically reinforce a long bias, while consistent dips below 50 can sustain a short or cautious outlook.

4. Pair Trading Applications

Custom Benchmark Selection: By setting a specific ticker pair as your benchmark instead of the default S&P 500, you can identify spread trading opportunities between two correlated assets. This allows you to go long the outperforming asset while shorting the underperforming one when the spread reaches extreme levels.

4. Color-Coded Signals & Alerts

Visual Zones (25–75): Color-coded bands highlight strong outperformance (above 75) or pronounced underperformance (below 25).

Alerts on Strong Shifts: Automatic alerts can notify you of sudden entries or exits from bullish or bearish zones, so you can potentially act on new market information without delay.

⚙️ HOW TO USE

1. Select Your Timeframe: For scalping or day trading, lower intervals (e.g., 5-minute) offer immediate data resets at the session’s start. For multi-day insight, daily or weekly charts reveal broader performance trends.

2. Watch Key Levels Around 50: Intraday dips under 50 may be a cue to consider short trades, while bounces above 50 can confirm renewed strength.

3. Assess Benchmark Relationships: Compare your asset’s score and signals to the broader market. A stock falling below its pair’s relative strength line might lag overall market momentum.

4. Combine Tools & Validate: This script excels when integrated with other technical analysis methods (e.g., support/resistance, chart patterns) and fundamental factors for a holistic market view.

❗ LIMITATIONS

No Direction Guarantee: The indicator identifies relative strength but does not guarantee directional price moves.

Delayed Updates: Since calculations update after each bar close, sudden intrabar changes may not immediately reflect.

Market-Specific Behaviors: Some assets or unusual market conditions may deviate from typical benchmarks, weakening signal reliability.

Past ≠ Future: High or low relative strength in the past may not predict continued performance.

RISK DISCLAIMER

All forms of trading and investing involve risk, including the possible loss of principal. This indicator analyzes relative performance but cannot assure profits or eliminate losses. Past performance of any strategy does not guarantee future results. Always combine analysis with proper risk management and your broader trading plan. Consult a licensed financial advisor if you are unsure of your individual risk tolerance or investment objectives.

TradeQUO Herrick Payoff RSIHerrick Payoff Index RSI (HPI-RSI) with Signal Line

An advanced oscillator that measures market strength not just by price, but by "smart money flow."

This indicator is not a typical RSI. Instead of applying the Relative Strength Index to price alone, it calculates it on the cumulative Herrick Payoff Index (HPI) . This creates a unique oscillator that reflects the underlying sentiment and capital flow in the market.

What is the Herrick Payoff Index (HPI)?

The HPI is a classic sentiment indicator that combines three crucial elements to determine if money is flowing into or out of an asset:

Price Change: The direction and momentum of the market.

Trading Volume: The conviction behind the price movement.

Open Interest (OI): The total number of open contracts (mainly in futures), which indicates if new capital is entering the market.

By combining these factors, the HPI provides a more comprehensive picture of market strength than indicators based solely on price.

How This Indicator Works

The script follows a logical, multi-step process:

It calculates the raw Herrick Payoff Index for each bar.

It creates a cumulative sum of this index to generate a continuous money flow value.

This cumulative value is smoothed with a short-period EMA to reduce noise.

The RSI is then applied to this smoothed HPI value.

An additional, configurable signal line (moving average) is added to facilitate trading signals.

Interpretation and Application

You can use this indicator much like a standard RSI, but with the added context of money flow:

Overbought/Oversold: Values above 70 suggest an overbought condition, while values below 30 signal an oversold condition.

Signal Line Crossovers: A cross of the HPI-RSI line above the signal line can be seen as a bullish signal. A cross below can be seen as a bearish signal.

Divergences: Look for divergences between the indicator and the price. A bullish divergence (price makes a lower low, indicator makes a higher low) can indicate an upcoming move to the upside. A bearish divergence (price makes a higher high, indicator makes a lower high) can signal a potential move to the downside.

Settings

The indicator has been deliberately kept simple:

HPI Smoothing Length: Smoothing length (1-5) for the cumulative HPI.

RSI Length: The lookback period for the RSI calculation.

Signal Line Settings: Here you can enable/disable the signal line and customize its type and length.

Display Settings: Adjust the colors of the RSI and signal lines to your preference.

This indicator is a tool for analysis and should always be used in combination with other methods and a solid risk management strategy. Happy trading!

StochFusion – Multi D-LineStochFusion – Multi D-Line

An advanced fusion of four Stochastic %D lines into one powerful oscillator.

What it does:

Combines four user-weighted Stochastic %D lines—from fastest (9,3) to slowest (60,10)—into a single “Fusion” line that captures both short-term and long-term momentum in one view.

How to use:

Adjust the four weights (0–10) to emphasize the speed of each %D component.

Watch the Fusion line crossing key zones:

– Above 80 → overbought condition, potential short entry.

– Below 20 → oversold condition, potential long entry.

– Around 50 → neutral/midline, watch for trend shifts.

Applications:

Entry/exit filter: Only take trades when the Fusion line confirms zone exits.

Trend confirmation: Analyze slope and cross of the midline for momentum strength.

Multi-timeframe alignment: Use on different chart resolutions to find confluence.

Tips & Tricks:

Default weights give more influence to slower %D—good for trend-focused strategies.

Equal weights provide a balanced oscillator that mimics an ensemble average.

Experiment: Increase the fastest weight to capture early reversal signals.

Developed by: TradeQUO — inspired by DayTraderRadio John

“The best momentum indicator is the one you adapt to your own trading rhythm.”

Open Interest-RSI + Funding + Fractal DivergencesIndicator — “Open Interest-RSI + Funding + Fractal Divergences”

A multi-factor oscillator that fuses Open-Interest RSI, real-time Funding-Rate data and price/OI fractal divergences.

It paints BUY/SELL arrows in its own pane and directly on the price chart, helping you spot spots where crowd positioning, leverage costs and price action contradict each other.

1 Purpose

OI-RSI – measures conviction behind position changes instead of price momentum.

Funding Rate – shows who pays to hold positions (longs → bull bias, shorts → bear bias).

Fractal Divergences – detects HH/LL in price that are not confirmed by OI-RSI.

Optional Funding filter – hides signals when funding is already extreme.

Together these elements highlight exhaustion points and potential mean-reversion trades.

2 Inputs

RSI / Divergence

RSI length – default 14.

High-OI level / Low-OI level – default 70 / 30.

Fractal period n – default 2 (swing width).

Fractals to compare – how many past swings to scan, default 3.

Max visible arrows – keeps last 50 BUY/SELL arrows for speed.

Funding Rate

mode – choose FR, Avg Premium, Premium Index, Avg Prem + PI or FR-candle.

Visual scale (×) – multiplies raw funding to fit 0-100 oscillator scale (default 10).

specify symbol – enable only if funding symbol differs from chart.

use lower tf – averages 1-min premiums for smoother intraday view.

show table – tiny two-row widget at chart edge.

Signal Filter

Use Funding filter – ON hides long signals when funding > Buy-threshold and short signals when funding < Sell-threshold.

BUY threshold (%) – default 0.00 (raw %).

SELL threshold (%) – default 0.00 (raw %).

(Enter funding thresholds as raw percentages, e.g. 0.01 = +0.01 %).

3 Visual Outputs

Sub-pane

Aqua OI-RSI curve with 70 / 50 / 30 reference lines.

Funding visualised according to selected mode (green above 0, red below 0, or other).

BUY / SELL arrows at oscillator extremes.

Price chart

Identical BUY / SELL arrows plotted with force_overlay = true above/below candles that formed qualifying fractals.

Optional table

Shows current asset ticker and latest funding value of the chosen mode.

4 Signal Logic (Summary)

Load _OI series and compute RSI.

Retrieve Funding-Rate + Premium Index (optionally from lower TF).

Find fractal swings (n bars left & right).

Check divergence:

Bearish – price HH + OI-RSI LH.

Bullish – price LL + OI-RSI HL.

If Funding-filter enabled, require funding < Buy-thr (long) or > Sell-thr (short).

Plot arrows and trigger two built-in alerts (Bearish OI-RSI divergence, Bullish OI-RSI divergence).

Signals are fixed once the fractal bar closes; they do not repaint afterwards.

5 How to Use

Attach to a liquid perpetual-futures chart (BTC, ETH, major Binance contracts).

If _OI or funding series is missing you’ll see an error.

Choose timeframe:

15 m – 4 h for intraday;

1 D+ for swing trades.

Lower TFs → more signals; raise Fractals to compare or use Funding filter to trim noise.

Trade checklist

Funding positive and rising → longs overcrowded.

Price makes higher high; OI-RSI makes lower high; Funding above Sell-threshold → consider short.

Reverse logic for longs.

Combine with trend filter (EMA ribbon, SuperTrend, etc.) so you fade only when price is stretched.

Automation – set TradingView alerts on the two alertconditions and send to webhooks/bots.

Performance tips

Keep Max visible arrows ≤ 50.

Disable lower-TF premium aggregation if script feels heavy.

6 Limitations

Some symbols lack _OI or funding history → script stops with a console message.

Binance Premium Index begins mid-2020; older dates show na.

Divergences confirm only after n bars (no forward repaint).

7 Changelog

v1.0 – 10 Jun 2025

Initial public release.

Added price-chart arrows via force_overlay.

Market Arterial PressureIndicator Description: Pulse-Market – Market Blood Pressure

"I slept and had a dream."

In that dream, I wore a white lab coat and shiny black pointed shoes. I felt like a doctor—not of traditional medicine, but of the financial market itself. My mission was clear: to measure the market's blood pressure and diagnose its health.

With this vision, I decided to turn the dream into code. Thus, Pulse-Market was born: an indicator designed to listen to the heartbeat of the blockchain, capturing signs of vitality or collapse, and anticipating the pulse of the next trend.

But the journey did not stop there. At the core of this creation, I incorporated a profound theory: the cycle of existence — Alpha, Beta, and Omega — concepts that resonate both in science and sacred scriptures.

Alpha (α) represents the beginning: the primary impulse, the market's accelerated pulse.

Beta (β) symbolizes the middle: the vital rhythm, the stabilizing cadence of prices.

Omega (Ω) indicates the end: structural collapse, the exhaustion of a cycle.

This logical and symbolic triad forms the foundation of Pulse-Market — the beginning, middle, and end of every market cycle.

How to Use the Indicator

Pulse-Market works as a dynamic oscillator composed of three main forces:

Alpha Pulse (α)

Measures recent price acceleration. The stronger the pulse, the more intense the market movement.

Beta Rhythm (β)

Controls the smoothing of the price rhythm and can be adjusted in four modes:

Fast – quick reactions with more sensitivity

Normal – standard smoothing (simple moving average)

Slow – slow and consistent movements

Accelerated – Hull method: reactive and smooth

Omega Collapse (Ω)

Combines entropy and reversals to detect structural collapses where the market may be losing strength.

Visual Interpretation

Green line above zero: healthy pulse, buying pressure in control.

Red line below zero: strong selling pressure, possible exhaustion.

Crossing the zero line: potential trend reversal.

Settings and Customization

In the indicator settings panel, you can calibrate the pressure reading sensitivity:

Systolic Pressure (α): controls the reaction to rapid price impulses.

Increase to highlight aggressive moves; decrease to smooth spikes.

Diastolic Pressure (β): regulates the importance of the underlying rhythm.

Increase for smooth trends; decrease for quicker responses.

Pulse Pressure (Ω): sensitivity to structural collapses and volatility.

Increase to detect reversals; decrease to ignore market noise.

Practical Applications

Confirm entry and exit signals based on the balance between Alpha and Omega.

Adjust the indicator to your trading style: scalper, day trader, or swing trader.

Use on any asset: cryptocurrencies, stocks, indices, forex.

Integrated Philosophy

We live limited by time and matter, but markets, like life, follow natural cycles: they are born, mature, collapse, and are reborn.

Pulse-Market is not just a technical indicator — it is a spiritual and analytical stethoscope that listens to the heartbeat of volatility and tries to anticipate what the eyes cannot see, but time always reveals.

Original Creator

This indicator was created by Canhoto-Medium, the sole inventor and namer of this tool. As long as time goes on, no other indicator will exist with this essence or name.

CCI Orbiting-VenusIndicator Description: CCI Orbiting-Venus

This is a customized version of the Commodity Channel Index (CCI) that measures the price deviation relative to its smoothed moving average to help identify overbought or oversold market conditions.

What does it do?

Calculates the CCI based on various price sources (such as close, open, high, low, and several price averages).

Applies customizable smoothing to the CCI using different types of moving averages (SMA, EMA, WMA, Hull, JMA, and SMMA).

Visually highlights the CCI direction with different colors:

Purple when CCI is above zero (positive momentum)

Orange when CCI is below zero (negative momentum)

Shows reference lines at +100 and -100 to help identify overbought and oversold zones.

How to use this indicator?

CCI Period Setting (CCI Period):

Adjust the number of periods used to calculate the CCI. Lower values make the indicator more sensitive, while higher values smooth out fluctuations.

Price Source (CCI Price Source):

Choose which price to base the calculation on: close, open, high, low, or weighted averages. This allows you to adapt the indicator to your trading style or strategy.

Smoothing Type (CCI Smoothing Type):

Select from different smoothing methods for the CCI calculation, which affects how the indicator behaves:

SMA (Simple Moving Average) – basic and traditional.

EMA, WMA, Hull, JMA (more advanced averages) – provide different noise filtering or faster response to price movements.

Interpreting CCI values:

Values above +100 suggest the asset may be overbought and could be near a downward reversal.

Values below -100 suggest the asset may be oversold and could be near an upward reversal.

Crossing the zero line indicates a potential change in trend or momentum.

Practical usage:

Look for buy signals when CCI moves up from the oversold region (-100) and crosses above zero, turning purple (positive).

Look for sell signals when CCI moves down from the overbought region (+100) and crosses below zero, turning orange (negative).

Combine with other indicators or chart analysis to confirm signals and avoid false entries.

Advantages of this custom indicator

Flexibility in choosing the price source and smoothing method.

Intuitive visual cues with colors indicating momentum direction.

Clear reference lines for quick assessment of extreme conditions.

RSI-GringoRSI-Gringo — Stochastic RSI with Advanced Smoothing Averages

Overview:

RSI-Gringo is an advanced technical indicator that combines the concept of the Stochastic RSI with multiple smoothing options using various moving averages. It is designed for traders seeking greater precision in momentum analysis, while offering the flexibility to select the type of moving average that best suits their trading style.

Disclaimer: This script is not investment advice. Its use is entirely at your own risk. My responsibility is to provide a fully functional indicator, but it is not my role to guide how to trade, adjust, or use this tool in any specific strategy.

The JMA (Jurik Moving Average) version used in this script is a custom implementation based on publicly shared code by TradingView users, and it is not the original licensed version from Jurik Research.

What This Indicator Does

RSI-Gringo applies the Stochastic Oscillator logic to the RSI itself (rather than price), helping to identify overbought and oversold conditions within the RSI. This often leads to more responsive and accurate momentum signals.

This indicator displays:

%K: the main Stochastic RSI line

%D: smoothed signal line of %K

Upper/Lower horizontal reference lines at 80 and 20

Features and Settings

Available smoothing methods (selectable from dropdown):

SMA — Simple Moving Average

SMMA — Smoothed Moving Average (equivalent to RMA)

EMA — Exponential Moving Average

WMA — Weighted Moving Average

HMA — Hull Moving Average (manually implemented)

JMA — Jurik Moving Average (custom approximation)

KAMA — Kaufman Adaptive Moving Average

T3 — Triple Smoothed Moving Average with adjustable hot factor

How to Adjust Advanced Averages

T3 – Triple Smoothed MA

Parameter: T3 Hot Factor

Valid range: 0.1 to 2.0

Tuning:

Lower values (e.g., 0.1) make it faster but noisier

Higher values (e.g., 2.0) make it smoother but slower

Balanced range: 0.7 to 1.0 (recommended)

JMA – Jurik Moving Average (Custom)

Parameters:

Phase: adjusts responsiveness and smoothness (-100 to 100)

Power: controls smoothing intensity (default: 1)

Tuning:

Phase = 0: neutral behavior

Phase > 0: more reactive

Phase < 0: smoother, more delayed

Power = 1: recommended default for most uses

Note: The JMA used here is not the proprietary version by Jurik Research, but an educational approximation available in the public domain on TradingView.

How to Use

Crossover Signals

Buy signal: %K crosses above %D from below the 20 line

Sell signal: %K crosses below %D from above the 80 line

Momentum Strength

%K and %D above 80: strong bullish momentum

%K and %D below 20: strong bearish momentum

With Trend Filters

Combine this indicator with trend-following tools (like moving averages on price)

Fast smoothing types (like EMA or HMA) are better for scalping and day trading

Slower types (like T3 or KAMA) are better for swing and long-term trading

Final Tips

Tweak RSI and smoothing periods depending on the time frame you're trading.

Try different combinations of moving averages to find what works best for your strategy.

This indicator is intended as a supporting tool for technical analysis — not a standalone decision-making system.

SMI-DarknessIndicator Description: SMI-Darkness

The SMI-Darkness is an indicator based on the Stochastic Momentum Index (SMI), designed to help identify the strength and direction of an asset's trend, as well as potential buy and sell signals. It displays a smoothed SMI using multiple moving average options to customize the indicator’s behavior according to the user’s trading style.

Main Features

Smoothed SMI: Calculates the traditional SMI and smooths it using a user-configurable moving average, improving signal clarity.

Signal Line: Displays a smoothed signal line to identify crossovers with the SMI, generating potential entry or exit points.

Histogram: Shows the difference between the smoothed SMI and the signal line, visually highlighting trend strength. Blue bars indicate buying strength, while yellow bars indicate selling strength.

Horizontal Lines: Includes overbought (+40) and oversold (-40) levels, plus a neutral zero level to aid interpretation.

Indicator Parameters

SMI Short Period: Sets the short period used to calculate the SMI (default 5). Lower periods make the indicator more sensitive.

SMI Signal Period: Sets the period to smooth the signal line (default 5). Adjust to control the signal line's smoothness.

Moving Average Type: Choose the moving average type to smooth the SMI and signal line. Options include:

SMA (Simple Moving Average)

SMMA (Smoothed Moving Average)

EMA (Exponential Moving Average)

WMA (Weighted Moving Average)

HMA (Hull Moving Average)

JMA (Jurik Moving Average) — Note: This is not an original or proprietary moving average but a publicly available open-source version created by TradingView users.

VWMA (Volume-Weighted Moving Average)

KAMA (Kaufman Adaptive Moving Average)

How to Use

Trend Identification: Observe the position of the smoothed SMI relative to the signal line and the histogram values.

When the histogram is positive (blue bars), momentum is bullish.

When the histogram is negative (yellow bars), momentum is bearish.

Buy and Sell Signals:

A crossover of the smoothed SMI above the signal line may indicate a buy signal.

A crossover of the smoothed SMI below the signal line may indicate a sell signal.

Overbought/Oversold Levels:

SMI values above +40 suggest potential overbought conditions, signaling caution on long positions.

Values below -40 suggest potential oversold conditions, indicating possible buying opportunities.

Customization: Adjust the parameters to balance sensitivity and noise, choosing the moving average type that best fits your trading style.

MACD Full [Titans_Invest]MACD Full — A Smarter, More Flexible MACD.

Looking for a MACD with real customization power?

We present one of the most complete public MACD indicators available on TradingView.

It maintains the classic MACD structure but is enhanced with 20 fully customizable long entry conditions and 20 short entry conditions , giving you precise control over your strategy.

Plus, it’s fully automation-ready, making it ideal for quantitative systems and algorithmic trading.

Whether you're a discretionary trader or a bot developer, this tool is built to seamlessly adapt to your style.

⯁ WHAT IS THE MACD❓

The Moving Average Convergence Divergence (MACD) is a technical analysis indicator developed by Gerald Appel. It measures the relationship between two moving averages of a security’s price to identify changes in momentum, direction, and strength of a trend. The MACD is composed of three components: the MACD line, the signal line, and the histogram.

⯁ HOW TO USE THE MACD❓

The MACD is calculated by subtracting the 26-period Exponential Moving Average (EMA) from the 12-period EMA. A 9-period EMA of the MACD line, called the signal line, is then plotted on top of the MACD line. The MACD histogram represents the difference between the MACD line and the signal line.

Here are the primary signals generated by the MACD:

Bullish Crossover: When the MACD line crosses above the signal line, indicating a potential buy signal.

Bearish Crossover: When the MACD line crosses below the signal line, indicating a potential sell signal.

Divergence: When the price of the security diverges from the MACD, suggesting a potential reversal.

Overbought/Oversold Conditions: Indicated by the MACD line moving far away from the signal line, though this is less common than in oscillators like the RSI.

⯁ ENTRY CONDITIONS

The conditions below are fully flexible and allow for complete customization of the signal.

______________________________________________________

🔹 CONDITIONS TO BUY 📈

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

🔹 MACD > Signal Smoothing

🔹 MACD < Signal Smoothing

🔹 Histogram > 0

🔹 Histogram < 0

🔹 Histogram Positive

🔹 Histogram Negative

🔹 MACD > 0

🔹 MACD < 0

🔹 Signal > 0

🔹 Signal < 0

🔹 MACD > Histogram

🔹 MACD < Histogram

🔹 Signal > Histogram

🔹 Signal < Histogram

🔹 MACD (Crossover) Signal

🔹 MACD (Crossunder) Signal

🔹 MACD (Crossover) 0

🔹 MACD (Crossunder) 0

🔹 Signal (Crossover) 0

🔹 Signal (Crossunder) 0

______________________________________________________

______________________________________________________

🔸 CONDITIONS TO SELL 📉

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

🔸 MACD > Signal Smoothing

🔸 MACD < Signal Smoothing

🔸 Histogram > 0

🔸 Histogram < 0

🔸 Histogram Positive

🔸 Histogram Negative

🔸 MACD > 0

🔸 MACD < 0

🔸 Signal > 0

🔸 Signal < 0

🔸 MACD > Histogram

🔸 MACD < Histogram

🔸 Signal > Histogram

🔸 Signal < Histogram

🔸 MACD (Crossover) Signal

🔸 MACD (Crossunder) Signal

🔸 MACD (Crossover) 0

🔸 MACD (Crossunder) 0

🔸 Signal (Crossover) 0

🔸 Signal (Crossunder) 0

______________________________________________________

______________________________________________________

🤖 AUTOMATION 🤖

• You can automate the BUY and SELL signals of this indicator.

______________________________________________________

______________________________________________________

⯁ UNIQUE FEATURES

______________________________________________________

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Table of Conditions: BUY/SELL

Conditions Label: BUY/SELL

Plot Labels in the graph above: BUY/SELL

Automate & Monitor Signals/Alerts: BUY/SELL

______________________________________________________

📜 SCRIPT : MACD Full

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy!

______________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

Adaptive MACD Deluxe [AlgoAlpha]OVERVIEW

This script is an advanced rework of the classic MACD indicator, designed to be more adaptive, visually informative, and customizable. It enhances the original MACD formula using a dynamic feedback loop and a correlation-based weighting system that adjusts in real-time based on how deterministic recent price action is. The signal line is flexible, offering several smoothing types including Heiken Ashi, while the histogram is color-coded with gradients to help users visually identify momentum shifts. It also includes optional normalization by volatility, allowing MACD values to be interpreted as relative percentage moves, making the indicator more consistent across different assets and timeframes.

CONCEPTS

This version of MACD introduces a deterministic weight based on R-squared correlation with time, which modulates how fast or slow the MACD adapts to price changes. Higher correlation means smoother, slower MACD responses, and low correlation leads to quicker reaction. The momentum calculation blends traditional EMA math with feedback and damping components to create a smoother, less noisy series. Heiken Ashi is optionally used for signal smoothing to better visualize short-term trend bias. When normalization is enabled, the MACD is scaled by an EMA of the high-low range, converting it into a bounded, volatility-relative indicator. This makes extreme readings more meaningful across markets.

FEATURES

The script offers six distinct options for signal line smoothing: EMA, SMA, SMMA (RMA), WMA, VWMA, and a custom Heiken Ashi mode based on the MACD series. Each option provides a different response speed and smoothing behavior, allowing traders to match the indicator’s behavior to their strategy—whether it's faster reaction or reduced noise.

Normalization is another key feature. When enabled, MACD values are scaled by a volatility proxy, converting the indicator into a relative percentage. This helps standardize the MACD across different assets and timeframes, making overbought and oversold readings more consistent and easier to interpret.

Threshold zones can be customized using upper and lower boundaries, with inner zones for early warnings. These zones are highlighted on the chart with subtle background fills and directional arrows when MACD enters or exits key levels. This makes it easier to spot strong or weak reversals at a glance.

Lastly, the script includes multiple built-in alerts. Users can set alerts for MACD crossovers, histogram flips above or below zero, and MACD entries into strong or weak reversal zones. This allows for hands-free monitoring and quick decision-making without staring at the chart.

USAGE

To use this script, choose your preferred signal smoothing type, enable normalization if you want MACD values relative to volatility, and adjust the threshold zones to fit your asset or timeframe. Use the colored histogram to detect changes in momentum strength—brighter colors indicate rising strength, while faded colors imply weakening. Heiken Ashi mode smooths out noise and provides clearer signals, especially useful in choppy conditions. Use alert conditions for crossover and reversal detection, or monitor the arrow markers for entries into potential exhaustion zones. This setup works well for trend following, momentum trading, and reversal spotting across all market types.

Trending Indicator: Price % of Pivots# Price % of Pivots Indicator

## Overview

A trend-following indicator that measures current price position relative to recent pivot highs and lows as percentages, providing normalized trend analysis across all timeframes and instruments.

## Key Features

- **Real-time trend table** with live signal updates (Strong Bullish/Bearish, Leaning Bullish/Bearish, Neutral)

- **Dual percentage tracking**: Price % of high pivot and low pivot % of current price

- **Universal compatibility** - works on any timeframe and asset class

- **Faster than some other trend indicators** - catches trend changes earlier with less lag

## Trading Signals

- **Bullish bias**: When price % of high pivot > low pivot % of price

- **Bearish bias**: When low pivot % of price > price % of high pivot

- **Customizable thresholds** (default 99%) with alert system

- **Color-coded backgrounds** for immediate visual confirmation

## Configuration

- Adjustable pivot lookback period (5-100 bars)

- Customizable left/right bars for pivot confirmation

- Threshold settings from 50-110% with 0.5% increments

- Full color customization for all elements

## Advantages

- **Speed**: More responsive than traditional ATR-based indicators

- **Clarity**: Clean percentage-based display with professional info table

- **Alerts**: Multiple conditions for automated and manual trading

- **Versatility**: Effective for day trading, swing trading, and multi-timeframe analysis

Perfect for traders seeking a fast, reliable trend indicator that works consistently across all markets and timeframes.

Bilateral Filter For Loop [BackQuant]Bilateral Filter For Loop

The Bilateral Filter For Loop is an advanced technical indicator designed to filter out market noise and smooth out price data, thus improving the identification of underlying market trends. It employs a bilateral filter, which is a sophisticated non-linear filter commonly used in image processing and price time series analysis. By considering both spatial and range differences between price points, this filter is highly effective at preserving significant trends while reducing random fluctuations, ultimately making it suitable for dynamic trend-following strategies.

Please take the time to read the following:

Key Features

1. Bilateral Filter Calculation:

The bilateral filter is the core of this indicator and works by applying a weight to each data point based on two factors: spatial distance and price range difference. This dual weighting process allows the filter to preserve important price movements while reducing the impact of less relevant fluctuations. The filter uses two primary parameters:

Spatial Sigma (σ_d): This parameter adjusts the weight applied based on the distance of each price point from the current price. A larger spatial sigma means more smoothing, as further away values will contribute more heavily to the result.

Range Sigma (σ_r): This parameter controls how much weight is applied based on the difference in price values. Larger price differences result in smaller weights, while similar price values result in larger weights, thereby preserving the trend while filtering out noise.

The output of this filter is a smoothed version of the original price series, which eliminates short-term fluctuations, helping traders focus on longer-term trends. The bilateral filter is applied over a rolling window, adjusting the level of smoothing dynamically based on both the distance between values and their relative price movements.

2. For Loop Calculation for Trend Scoring:

A for-loop is used to calculate the trend score based on the filtered price data. The loop compares the current value to previous values within the specified window, scoring the trend as follows:

+1 for upward movement (when the filtered value is greater than the previous value).

-1 for downward movement (when the filtered value is less than the previous value).

The cumulative result of this loop gives a continuous trend score, which serves as a directional indicator for the market's momentum. By summing the scores over the window period, the loop provides an aggregate value that reflects the overall trend strength. This score helps determine whether the market is experiencing a strong uptrend, downtrend, or sideways movement.

3. Long and Short Conditions:

Once the trend score has been calculated, it is compared against predefined threshold levels:

A long signal is generated when the trend score exceeds the upper threshold, indicating that the market is in a strong uptrend.

A short signal is generated when the trend score crosses below the lower threshold, signaling a potential downtrend or trend reversal.

These conditions provide clear signals for potential entry points, and the color-coding helps traders quickly identify market direction:

Long signals are displayed in green.

Short signals are displayed in red.

These signals are designed to provide high-confidence entries for trend-following strategies, helping traders capture profitable movements in the market.

4. Trend Background and Bar Coloring:

The script offers customizable visual settings to enhance the clarity of the trend signals. Traders can choose to:

Color the bars based on the trend direction: Bars are colored green for long signals and red for short signals.

Change the background color to provide additional context: The background will be shaded green for a bullish trend and red for a bearish trend. This visual feedback helps traders to stay aligned with the prevailing market sentiment.

These features offer a quick visual reference for understanding the market's direction, making it easier for traders to identify when to enter or exit positions.

5. Threshold Lines for Visual Feedback:

Threshold lines are plotted on the chart to represent the predefined long and short levels. These lines act as clear markers for when the market reaches a critical threshold, triggering a potential buy (long) or sell (short) signal. By showing these threshold lines on the chart, traders can quickly gauge the strength of the market and assess whether the trend is strong enough to warrant action.

These thresholds can be adjusted based on the trader's preferences, allowing them to fine-tune the indicator for different market conditions or asset behaviors.

6. Customizable Parameters for Flexibility:

The indicator offers several parameters that can be adjusted to suit individual trading preferences:

Window Period (Bilateral Filter): The window size determines how many past price values are used to calculate the bilateral filter. A larger window increases smoothing, while a smaller window results in more responsive, but noisier, data.

Spatial Sigma (σ_d) and Range Sigma (σ_r): These values control how sensitive the filter is to price changes and the distance between data points. Fine-tuning these parameters allows traders to adjust the degree of noise reduction applied to the price series.

Threshold Levels: The upper and lower thresholds determine when the trend score crosses into long or short territory. These levels can be customized to better match the trader's risk tolerance or asset characteristics.

Visual Settings: Traders can customize the appearance of the chart, including the line width of trend signals, bar colors, and background shading, to make the indicator more readable and aligned with their charting style.

7. Alerts for Trend Reversals:

The indicator includes alert conditions for real-time notifications when the market crosses the defined thresholds. Traders can set alerts to be notified when:

The trend score crosses the long threshold, signaling an uptrend.

The trend score crosses the short threshold, signaling a downtrend.

These alerts provide timely information, allowing traders to take immediate action when the market shows a significant change in direction.

Final Thoughts

The Bilateral Filter For Loop indicator is a robust tool for trend-following traders who wish to reduce market noise and focus on the underlying trend. By applying the bilateral filter and calculating trend scores, this indicator helps traders identify strong uptrends and downtrends, providing reliable entry signals with minimal market noise. The customizable parameters, visual feedback, and alerting system make it a versatile tool for traders seeking to improve their timing and capture profitable market movements.

Thus following all of the key points here are some sample backtests on the 1D Chart

Disclaimer: Backtests are based off past results, and are not indicative of the future.

INDEX:BTCUSD

INDEX:ETHUSD

CRYPTO:SOLUSD

Market Zone Analyzer[BullByte]Understanding the Market Zone Analyzer

---

1. Purpose of the Indicator

The Market Zone Analyzer is a Pine Script™ (version 6) indicator designed to streamline market analysis on TradingView. Rather than scanning multiple separate tools, it unifies four core dimensions—trend strength, momentum, price action, and market activity—into a single, consolidated view. By doing so, it helps traders:

• Save time by avoiding manual cross-referencing of disparate signals.

• Reduce decision-making errors that can arise from juggling multiple indicators.

• Gain a clear, reliable read on whether the market is in a bullish, bearish, or sideways phase, so they can more confidently decide to enter, exit, or hold a position.

---

2. Why a Trader Should Use It

• Unified View: Combines all essential market dimensions into one easy-to-read score and dashboard, eliminating the need to piece together signals manually.

• Adaptability: Automatically adjusts its internal weighting for trend, momentum, and price action based on current volatility. Whether markets are choppy or calm, the indicator remains relevant.

• Ease of Interpretation: Outputs a simple “BULLISH,” “BEARISH,” or “SIDEWAYS” label, supplemented by an intuitive on-chart dashboard and an oscillator plot that visually highlights market direction.

• Reliability Features: Built-in smoothing of the net score and hysteresis logic (requiring consecutive confirmations before flips) minimize false signals during noisy or range-bound phases.

---

3. Why These Specific Indicators?

This script relies on a curated set of well-established technical tools, each chosen for its particular strength in measuring one of the four core dimensions:

1. Trend Strength:

• ADX/DMI (Average Directional Index / Directional Movement Index): Measures how strong a trend is, and whether the +DI line is above the –DI line (bullish) or vice versa (bearish).

• Moving Average Slope (Fast MA vs. Slow MA): Compares a shorter-period SMA to a longer-period SMA; if the fast MA sits above the slow MA, it confirms an uptrend, and vice versa for a downtrend.

• Ichimoku Cloud Differential (Senkou A vs. Senkou B): Provides a forward-looking view of trend direction; Senkou A above Senkou B signals bullishness, and the opposite signals bearishness.

2. Momentum:

• Relative Strength Index (RSI): Identifies overbought (above its dynamically calculated upper bound) or oversold (below its lower bound) conditions; changes in RSI often precede price reversals.

• Stochastic %K: Highlights shifts in short-term momentum by comparing closing price to the recent high/low range; values above its upper band signal bullish momentum, below its lower band signal bearish momentum.

• MACD Histogram: Measures the difference between the MACD line and its signal line; a positive histogram indicates upward momentum, a negative histogram indicates downward momentum.

3. Price Action:

• Highest High / Lowest Low (HH/LL) Range: Over a defined lookback period, this captures breakout or breakdown levels. A closing price near the recent highs (with a positive MA slope) yields a bullish score, and near the lows (with a negative MA slope) yields a bearish score.

• Heikin-Ashi Doji Detection: Uses Heikin-Ashi candles to identify indecision or continuation patterns. A small Heikin-Ashi body (doji) relative to recent volatility is scored as neutral; a larger body in the direction of the MA slope is scored bullish or bearish.

• Candle Range Measurement: Compares each candle’s high-low range against its own dynamic band (average range ± standard deviation). Large candles aligning with the prevailing trend score bullish or bearish accordingly; unusually small candles can indicate exhaustion or consolidation.

4. Market Activity:

• Bollinger Bands Width (BBW): Measures the distance between BB upper and lower bands; wide bands indicate high volatility, narrow bands indicate low volatility.

• Average True Range (ATR): Quantifies average price movement (volatility). A sudden spike in ATR suggests a volatile environment, while a contraction suggests calm.

• Keltner Channels Width (KCW): Similar to BBW but uses ATR around an EMA. Provides a second layer of volatility context, confirming or contrasting BBW readings.

• Volume (with Moving Average): Compares current volume to its moving average ± standard deviation. High volume validates strong moves; low volume signals potential lack of conviction.

By combining these tools, the indicator captures trend direction, momentum strength, price-action nuances, and overall market energy, yielding a more balanced and comprehensive assessment than any single tool alone.

---

4. What Makes This Indicator Stand Out

• Multi-Dimensional Analysis: Rather than relying on a lone oscillator or moving average crossover, it simultaneously evaluates trend, momentum, price action, and activity.

• Dynamic Weighting: The relative importance of trend, momentum, and price action adjusts automatically based on real-time volatility (Market Activity State). For example, in highly volatile conditions, trend and momentum signals carry more weight; in calm markets, price action signals are prioritized.

• Stability Mechanisms:

• Smoothing: The net score is passed through a short moving average, filtering out noise, especially on lower timeframes.

• Hysteresis: Both Market Activity State and the final bullish/bearish/sideways zone require two consecutive confirmations before flipping, reducing whipsaw.

• Visual Interpretation: A fully customizable on-chart dashboard displays each sub-indicator’s value, regime, score, and comment, all color-coded. The oscillator plot changes color to reflect the current market zone (green for bullish, red for bearish, gray for sideways) and shows horizontal threshold lines at +2, 0, and –2.

---

5. Recommended Timeframes

• Short-Term (5 min, 15 min): Day traders and scalpers can benefit from rapid signals, but should enable smoothing (and possibly disable hysteresis) to reduce false whipsaws.

• Medium-Term (1 h, 4 h): Swing traders find a balance between responsiveness and reliability. Less smoothing is required here, and the default parameters (e.g., ADX length = 14, RSI length = 14) perform well.

• Long-Term (Daily, Weekly): Position traders tracking major trends can disable smoothing for immediate raw readings, since higher-timeframe noise is minimal. Adjust lookback lengths (e.g., increase adxLength, rsiLength) if desired for slower signals.

Tip: If you keep smoothing off, stick to timeframes of 1 h or higher to avoid excessive signal “chatter.”

---

6. How Scoring Works

A. Individual Indicator Scores

Each sub-indicator is assigned one of three discrete scores:

• +1 if it indicates a bullish condition (e.g., RSI above its dynamically calculated upper bound).

• 0 if it is neutral (e.g., RSI between upper and lower bounds).

• –1 if it indicates a bearish condition (e.g., RSI below its dynamically calculated lower bound).

Examples of individual score assignments:

• ADX/DMI:

• +1 if ADX ≥ adxThreshold and +DI > –DI (strong bullish trend)

• –1 if ADX ≥ adxThreshold and –DI > +DI (strong bearish trend)

• 0 if ADX < adxThreshold (trend strength below threshold)

• RSI: