Multi-Anchor VWAP | Trade Symmetry🧩 Multi-Anchor VWAP

Description:

Dynamic VWAP anchored to Session, Week, Month, Quarter, and Year — all in one view.

Full Description:

This indicator plots multiple VWAPs (Volume-Weighted Average Prices) simultaneously — each anchored to a different time period:

Session, Week, Month, Quarter, and Year.

💡 Ideal for traders who track institutional mean reversion and liquidity zones across multiple timeframes.

Features

✅ Session, Weekly, Monthly, Quarterly, and Yearly Anchored VWAPs

✅ Independent color and visibility controls for each anchor

✅ Adjustable label position and size

✅ Option to hide VWAPs on Daily or higher charts

✅ Clean and efficient performance

This tool helps you visualize volume-weighted mean levels where price often reacts — offering a clear map of bias and equilibrium across all major time horizons.

在脚本中搜索"vwap"

Multi VWAP from Gaps [MW]Multi VWAP from Gaps

Introduction

The Multi VWAP from Gaps tool extends the concept of using the Anchored Volume Weighted Average Price, popularized by its founder, Brian Shannon, founder of AlphaTrends. It creates automatic AVWAPS for anchor points originating at the biggest gaps of the week, month, quarter and year. Currently, most standard VWAP tools allow users to place custom anchored VWAPs, but the routine of doing this for every equity being watched can become cumbersome. This tool makes that process multi-times easier. Considering that large gaps can represent a shift in market structure, this tool provides unique and immediate insight into how past daily price gaps can and have affected price action.

Settings

LABEL SETTINGS

Show Biggest Gap of Week | Month | Quarter : Toggle labels that identify the location of the biggest gaps for the selected time period.

Show Big Labels : Toggle labels from showing the date and gap size to just showing a single letter (W/M/Q/Y) designating the time period that the gap is from.

Hide All Labels : Turn labels off and on.

MAX VWAP LINES

Max Weekly | Monthly | Quarterly | Yearly Lines : How many VWAP lines, starting from today, should be shown for the specified time period. Max: 5

SHOW VWAP LINES

Show Weekly | Monthly | Quarterly | Yearly Lines : This feature allows you to remove lines for the specified time period.

Calculations

This indicator does not provide buy or sell signals. It is simply the VWAP calculated starting from an “anchor point”, or start time. It is calculated by the summation of Price x Volume / Volume for the period starting at the anchor point.

How to Interpret

According to Brian Shannon, VWAP is an objective measure of what the average trader has paid for a particular equity over a given period, and is the value that large institutional investors frequently use as a trade signal. Therefore, by definition, when the price is above an AVWAP, buyers are in control for that period of time. Likewise, if the price is below the AVWAP, sellers are in control for that period of time.

VWAPs that coincide with important events, such as FOMC meetings, CPI reports, earnings reports, have added significance. In many cases, these events can cause gaps to happen in day-to-day price movement, and can affect market structure going forward.

Practically speaking, price action can tend to change direction when a significant VWAP is hit, voiding buy and sell signals. Like moving averages, this indicator can show, in real-time, how a buy or sell signal should be interpreted. A significant AVWAP line is a point of interest, and can serve as strong support or resistance, because large institutions may be using those values for entries or exits. For a great analysis of how to use AVWAP, visit the AlphaTrends channel on Youtube here or you can buy Brian Shannon’s “Anchored VWAP” book on Amazon.

Other Usage Notes and Limitations

It's important for traders to be aware of the limitations of any indicator and to use them as part of a broader, well-rounded trading strategy that includes risk management, fundamental analysis, and other tools that can help with reducing false signals, determining trend direction, and providing additional confirmation for a trade decision. Diversifying strategies and not relying solely on one type of indicator or analysis can help mitigate some of these risks.

Additionally, in order to build the VWAP calculations, past data is needed that may not be available on shorter timeframes. The workaround is that for some longer-term VWAP lines on shorter timeframes, you may see less than the total of lines that you selected in settings. This is particularly the case with quarterly VWAP lines on the 5 minute timeframe for some equities.

Acknowledgements

This script uses the MarketHolidays library by @Protervus. Also, for debugging, the JavaScript-style Debug Console by @algotraderdev was invaluable. Special thanks to @antsmuzic for helping review and debug the script. And, of course, without Brian Shannon's books, videos, and interviews, this indicator would would not have happened.

Kviatek - Multi Hour VWAPThis is an experimental script, that plots 24 VWAPs, each starting at a new hour and lasting for 24hours.

After using session anchored VWAPs i kept wondering if the price reacts to VWAPs that begin at periods lower than sessions.

Color of each VWAP changes upon crossovers of the following VWAP, giving us an understanding of trends and whether we're trading with the trend or against it.

By the nature of the script I recommend using it on low timeframes, 5 and 15-minute ones ideally.

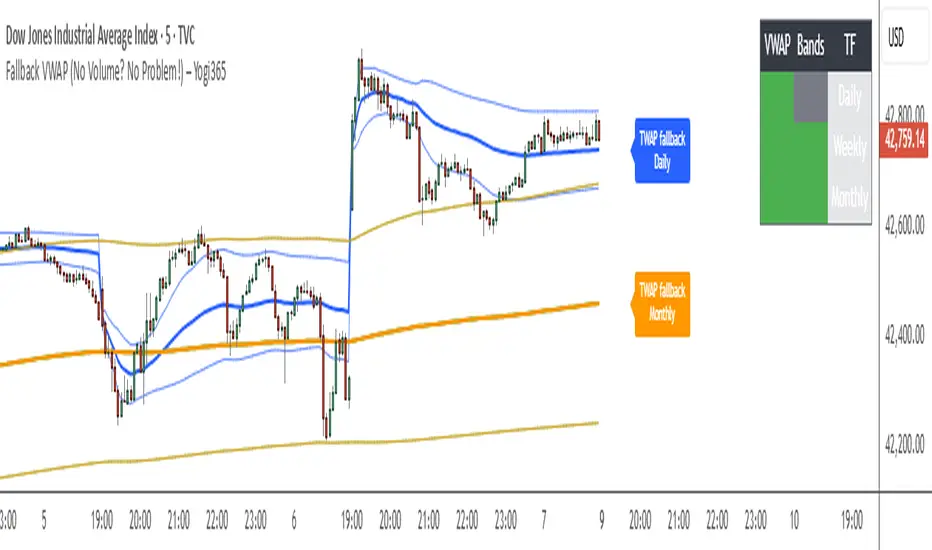

Fallback VWAP (No Volume? No Problem!) – Yogi365Fallback VWAP (No Volume? No Problem!) – Yogi365

This script plots Daily, Weekly, and Monthly VWAPs with ±1 Standard Deviation bands. When volume data is missing or zero (common in indices or illiquid assets), it automatically falls back to a TWAP-style calculation, ensuring that your VWAP levels always remain visible and accurate.

Features:

Daily, Weekly, and Monthly VWAPs with ±1 Std Dev bands.

Auto-detection of missing volume and seamless fallback.

Clean, color-coded trend table showing price vs VWAP/bands.

Uses hlc3 for VWAP source.

Labels indicate when fallback is used.

Best Used On:

Any asset or index where volume is unavailable.

Intraday and swing trading.

Works on all timeframes but optimized for overlay use.

How it Works:

If volume == 0, the script uses a constant fallback volume (1), turning the VWAP into a TWAP (Time-Weighted Average Price) — still useful for intraday or index-based analysis.

This ensures consistent plotting on instruments like indices (e.g., NIFTY, SENSEX,DJI etc.) which might not provide volume on TradingView.

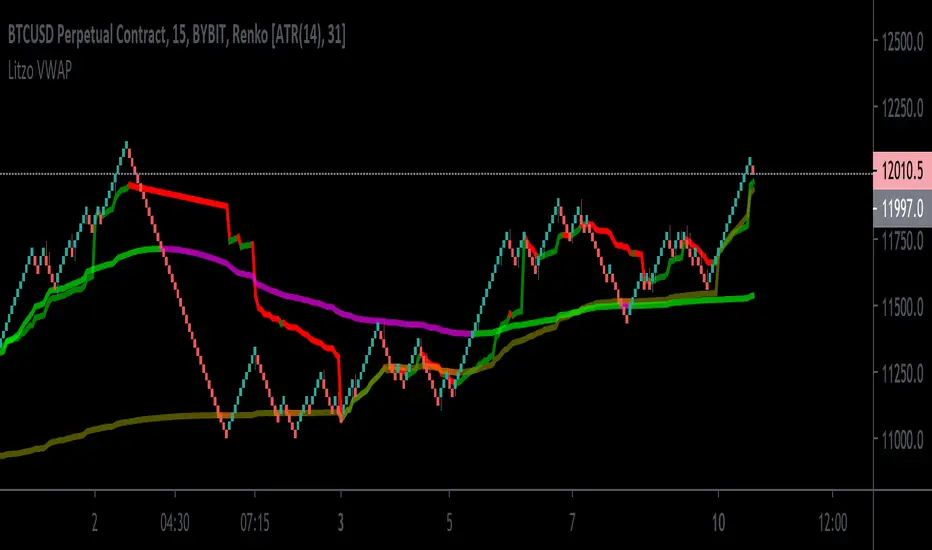

Litzo VWAPA basic VWAP that shows both session and weekly VWAP in one.

Defaults: source HLC3

Session VWAP: Price above : Line=Green. Price Below: Line=Red

Weekly VWAP: Price above: Line=Blue, Price Below: Line=Orange

VWAP & Band Cross Strategy v6VWAP & Band Cross Strategy v6: Script Summary

This Pine Script implements a highly flexible, multi-layered trading strategy centered around the Volume Weighted Average Price (VWAP) and its associated Standard Deviation Bands.

The strategy is designed to test various entry/exit models based on how the price interacts with the central VWAP line and the upper/lower volatility bands, with extensive risk management and confirmation filters.

1. Core Mechanics (VWAP & Bands)

VWAP Calculation: Calculates the VWAP based on a user-defined source (default is the close price).

Standard Deviation Bands: Creates upper and lower bands by calculating the standard deviation of the price (over 20 periods by default) and multiplying it by a user-defined Multiplier (default is 2.0). These bands dynamically expand and contract with volatility.

Plotting: The script clearly plots the VWAP (purple), the Upper Band (green), and the Lower Band (red), with a colored fill between the bands.

2. Entry Triggers

The core entry logic is based on a single, user-selected cross event between the price and the VWAP/Bands. The user can choose from six predefined entry types:

Entry Type Category

Entry Trigger (Long)

Entry Trigger (Short)

Mean Reversion

Price crosses over the Lower Band.

Price crosses under the Upper Band.

Trend Following

Price crosses over the Upper Band (Breakout).

Price crosses under the Lower Band (Breakout).

VWAP Cross

Price crosses over the VWAP.

Price crosses under the VWAP.

3. Filters and Confirmation

Trades are only executed if they pass a series of optional filters, making the strategy highly customizable:

Technical Confirmation (Optional): Users can enable and configure up to three additional indicators that must align with the trade direction:

RSI: Price must be Oversold (for Long) or Overbought (for Short).

SMMA: Price must be above the SMMA (for Long) or below (for Short).

MACD: MACD line must cross the Signal line and the Histogram must be positive/negative.

Time and Day Filters: Trades are restricted to a defined Entry Start/End Hour/Minute window, and only execute on user-selected Trading Days of the week.

Trade Direction: Can be toggled to execute Long Only, Short Only, or Both.

4. Advanced Risk Management (Daily Limits)

The strategy incorporates robust daily limits that reset at a configured Daily Reset Hour/Minute:

Daily Profit/Loss Limits: If the running total of Realized PnL (closed trades) + Unrealized PnL (open position) exceeds a user-defined Daily Take Profit (in Ticks) or falls below the Daily Stop Loss (in Ticks), the strategy locks out new trades and immediately closes any open position.

Max Daily Trades: Prevents the strategy from entering more than a specified number of trades per day.

5. Exit Logic

The strategy exit is also highly configurable via the Exit Type setting:

Fixed Ticks / ATR / Capped ATR: If one of these is selected, the script calculates a static Stop Loss and Take Profit level upon entry, using either fixed tick values or dynamic values based on the Average True Range (ATR), which are then executed using Pine Script's strategy.exit function.

Cross Exits (VWAP/Bands): If selected, the position is closed when the price crosses the VWAP or a specific band in the opposite direction.

End-of-Day Close: An unconditional exit that closes all open positions at a user-defined Close All Hour/Minute, regardless of profit/loss or limit status, preventing positions from being held overnight.

Advanced VWAP [CryptoSea]The Advanced VWAP is a comprehensive volume-weighted average price (VWAP) tool designed to provide traders with a deeper understanding of market trends through multi-layered VWAP analysis. This indicator is ideal for those who want to track price movements in relation to VWAP bands and detect key market levels with greater precision.

Key Features

Multi-Timeframe VWAP Bands: Includes multiple VWAP bands with different lookback periods (5, 10, 25, and 50), allowing traders to observe short-term and long-term price behavior.

Smoothed Band Options: Offers optional smoothing of VWAP bands to reduce noise and highlight significant trends more clearly.

Dynamic Median Line Display: Plots the median line of the VWAP bands, providing a reference for price movements and potential reversal zones.

VWAP Trend Strength Calculation: Measures the strength of the trend based on the price's position relative to the VWAP bands, normalized between -1 and 1 for easier interpretation.

In the example below we can see the VWAP Forecastd Cloud, which consists of multiple layers of VWAP bands with varying lookback periods, creating a dynamic forecast visualization. The cloud structure represents potential future price ranges by projecting VWAP-based bands outward, with darker areas indicating higher density and overlap of the bands, suggesting stronger support or resistance zones. This approach helps traders anticipate price movement and identify areas of potential consolidation or breakout as the price interacts with different layers of the forecast cloud.

How it Works

VWAP Calculation: Utilizes multiple VWAP calculations based on various lookback periods to capture a broad range of price behaviors. The indicator adapts to different market conditions by switching between short-term and long-term VWAP references.

Smoothing Algorithms: Provides the ability to smooth the VWAP bands using different moving average types (SMA, EMA, SMMA, WMA, VWMA) to suit various trading strategies and reduce market noise.

Trend Strength Analysis: Computes the trend strength based on the price's distance from the VWAP bands, with a value range of -1 to 1. This feature helps traders identify the intensity of uptrends and downtrends.

Alert Conditions: Includes alert options for crossing above or below the smoothed median line, as well as touching the smoothed upper or lower bands, providing timely notifications for potential trading opportunities.

This image below illustrates the use of smoothed VWAP bands, which provide a cleaner representation of the price's relationship to the VWAP by reducing market noise. The smoothed bands create a flowing cloud-like structure, making it easier to observe significant trends and potential reversal points. The circles highlight areas where the price interacts with the smoothed bands, indicating potential key levels for trend continuation or reversal. This setup helps traders focus on meaningful movements and filter out minor fluctuations, improving the identification of strategic entry and exit points based on smoother trend signals.

Application

Strategic Entry and Exit Points: Helps traders identify optimal entry and exit points based on the interaction with VWAP bands and trend strength readings.

Trend Confirmation: Assists in confirming trend strength by analyzing price movements relative to the VWAP bands and detecting significant breaks or touches.

Customized Analysis: Supports a wide range of trading styles by offering adjustable smoothing, band settings, and alert conditions to meet specific trading needs.

The Advanced VWAP by is a valuable addition to any trader's toolkit, offering versatile features to navigate different market scenarios with confidence. Whether used for day trading or longer-term analysis, this tool enhances decision-making by providing a robust view of price behavior relative to VWAP levels.

Timeweighted Colored VWAP with SlopeHey, traders!

This script calculates the VWAP's change rate against ATR in a number of k-lines. It controls the VWAP line's color based on the average change rate, and it changes its color in a time-weighted way.

1. Calculating vwapValue's rate of change

2. Controlling Line's color based on the average change rate against ATR

3. Calculating average change rate in the past k-lines

K线的数量:计算多少根K线的VWAP值的变化率的平均值,相当于用K线的数量来时间加权

变化率阈值:线条颜色变化的阈值,VWAP值的变化率比这个大或者小时改变颜色,否则延续原来的颜色

Good luck with your trading!

VWAP + MACD Estrategia MilloVWAP + MACD Strategy

This indicator combines the VWAP (Volume Weighted Average Price) with MACD (Moving Average Convergence Divergence) to create buy and sell signals. It helps traders identify potential market entry and exit points based on price action and momentum.

Conditions for Buy:

The price must be above the VWAP.

The MACD line crosses above the signal line (bullish crossover).

The MACD line is below the zero line.

Conditions for Sell:

The price must be below the VWAP.

The MACD line crosses below the signal line (bearish crossover).

The MACD line is above the zero line.

Features:

The VWAP line is plotted to represent the average price, weighted by volume, over a specified period.

Buy signals appear when all conditions are met for an upward price movement.

Sell signals appear when all conditions are met for a downward price movement.

MACD and Signal Line: The MACD helps to confirm momentum, while the signal line indicates possible trend reversals.

Customizable: You can modify the VWAP and MACD parameters to suit different trading strategies.

This strategy is designed for intraday traders and scalpers, aiming to catch quick movements while being aware of market momentum.

Feel free to share this description along with the code! Let me know if you need any adjustments or further explanations.

Institutional VWAP Suite (Lite Compatible)The **Institutional VWAP Suite (Lite Compatible)** brings true institutional volume-weighted price analysis to every trader — even on TradingView Lite/Free accounts where standard VWAP tools are restricted.

This script recreates the most important VWAP models used by banks, funds, and high-frequency desks, including:

• **Daily VWAP** (exchange-accurate)

• **Weekly VWAP** (manually accumulated)

• **Monthly VWAP** (manually accumulated)

• **Rolling Window VWAP** (array-based, fully Lite-compatible)

All calculations avoid blocked functions like `ta.sum` or session-restricted VWAP calls. Everything is built manually from volume and price to ensure accuracy across all accounts and all markets.

### Features

• Multi-timeframe VWAPs (Daily/Weekly/Monthly)

• Manual Rolling VWAP with adjustable length

• Optional VWAP bands (Lite-safe)

• Clean visuals with color-coded levels

• Optimized arrays for fast, stable performance

• Free-tier compatible — no premium functions required

This tool is designed for traders who want institutional structure, premium-level VWAP calculations, and consistent execution regardless of plan level. Perfect for scalpers, day traders, futures traders, and anyone who uses intraday volume profiles.

### Recommended Use

• Map directional bias using Daily vs Weekly VWAP

• Use Monthly VWAP for macro trend context

• Track intraday mean reversion with Rolling VWAP

• Use VWAP bands as dynamic support/resistance zones

A simple, powerful, no-restrictions VWAP engine — built for everyone.

VWAP – Pivot Pairs (SECONDS‑BASED RESET)VWAP – Pivot Pairs (SECONDS-BASED RESET) is a Pine Script v6 indicator for TradingView that combines pivot-based breakout detection with resettable VWAP (Volume Weighted Average Price) calculations over user-defined rolling time periods in seconds.It identifies high and low swing pivots via breakout logic, then calculates two VWAP lines per anchor:One using high/low as the price source,

One using close as the price source.

These form "pivot pairs" that reset automatically at the start of each custom-duration period (e.g., every 300 seconds), starting from a user-defined UTC time of day (default: 09:30 UTC).Visuals include:Colored VWAP lines (high pair: red, low pair: green),

Semi-transparent fill zones between each pair,

Optional toggles to show/hide high or low pairs.

Use CasesUse Case

Description

Intraday Scalping (1–15 min charts)

Use 60–300 second resets to capture micro-trends within larger sessions. VWAP pairs act as dynamic support/resistance after breakouts.

High-Frequency / Algo Validation

Backtest strategies on tick/second charts where traditional session resets fail. Align resets with exchange micro-sessions or volatility windows.

Opening Range Breakout (ORB) Enhancement

Set period_seconds = 1800 (30 min) and start time = 09:30 UTC → VWAP builds only on first 30 mins post-open, then floats. Pairs show deviation from ORB mean.

Range-Bound Market Analysis

In choppy markets, VWAP pairs converge near fair value. Divergence signals potential breakout. Fill color intensity shows conviction.

Multi-Timeframe Confluence

Overlay on 1-second chart with 300s reset → matches 5-minute structure. Use close-based VWAP for entries, high/low-based for stops.

Key Features SummaryFeature

Function

period_seconds

Rolling window length in seconds (e.g., 300 = 5 min)

period_start_time

UTC time-of-day anchor (default: 09:30)

new_period logic

Triggers full reset of pivots + VWAP on exact second boundary

breakingHigher / breakingLower

Detects confirmed breakouts (not just close above high)

Dual VWAP per anchor

ta.vwap(high) and ta.vwap(close) for range-aware mean

Fill zones

Visual value area between high/close VWAPs

Toggle visibility

Independently show/hide high or low pivot pairs

How It Works – Step-by-StepTime Engine Converts user inputs → milliseconds

Calculates current period start time using integer division from epoch

Detects exact bar when new period begins (new_period = true)

On New Period Resets both high/low anchors to current bar’s h and l

Forces VWAP recalculation from this bar forward

Breakout Detection Only triggers on strong candles (rising/falling, non-doji)

Requires open/close beyond prior pivot → avoids wicks-only breaks

VWAP Accumulation ta.vwap(source, reset_condition) restarts when anchor resets

Two sources per side → shows where volume clustered (at highs vs closes)

Plotting Four lines + two fills

Clean, customizable, overlay-friendly

Pro TipsUse on Heikin Ashi for smoother breakout signals.

Combine with volume profile to validate VWAP clusters.

For crypto, set period_start_time = 0 (00:00 UTC) for clean 4-hour resets.

Add alerts on new_period or breakingHigher for automation.

In short: This is a precision VWAP tool for time-boxed, pivot-driven mean reversion and breakout trading, ideal for scalpers, day traders, and algo developers needing sub-session granularity.

Rolling Midpoint of Price & VWAP with ATR BandsThe Rolling Midpoint of Price & VWAP with ATR Bands indicator is a dual-equilibrium concept that fuses price-range structure and traded-volume flow into one continuously updating hybrid model. Traditional VWAPs reset each session and reflect where trading occurred by volume, while midpoints used here reveal where price has structurally balanced between extremes. This script merges both ideas into a cohesive, dynamic system. The Rolling Price Midpoint (50 % of range) represents the structural fair-value line, calculated as the average of the highest high and lowest low over a selected window. The Rolling VWAP (Volume-Weighted Window) tracks the flow-based fair-value line by weighting each bar’s typical price by its volume. Together, these components form the Hybrid Equilibrium — the adaptive center of gravity that shifts as price and volume evolve. Surrounding this equilibrium, ATR Bands at ± 2.226 ATR and ± 5.382 ATR define volatility envelopes that expand and contract with market energy. The result is a living cloud that breathes with the market: compressing during phases of balance and widening during impulsive movements, offering traders a clear visual framework for understanding equilibrium, volatility, and directional bias in real time.

➖

⚙️ Auto-Preset System

The Auto-Preset System intelligently adjusts lookback windows for both the Price Midpoint and VWAP calculations according to the active chart timeframe.

This ensures that the indicator automatically adapts to any trading style — from scalping on 1-minute charts to swing trading on daily or weekly charts — without manual tuning.

🔹 How It Works

When Auto-Preset mode is enabled, the script dynamically selects the most effective lookback lengths for each timeframe.

These presets are optimized to balance responsiveness and stability, maintaining consistent real-world coverage (e.g., the same approximate duration of price data) across all intervals.

📊 Preset Mapping Table

| Chart Timeframe | Price Midpoint Lookback | VWAP Lookback |

|:----------------:|:-----------------------:|:--------------:|

| 1–3m | 13 bars | 21 bars

| 5–10m | 21 bars | 34 bars

| 15–30m | 34 bars | 55 bars

| 1–2 hr | 55 bars | 89 bars

| 4 hr-1D | 89 bars | 144 bars

| 1W | 144 bars | 233 bars

| 1M | 233 bars | 377 bars

⚡ Notes & Customization

- Manual Override: Turn off Auto-Preset Mode to specify your own custom lookback lengths.

- Consistency Across Scales: These adaptive values keep the indicator visually coherent when switching between timeframes — avoiding distortions that can occur with static lengths.

- Practical Benefit: Traders can maintain a single chart layout that self-tunes seamlessly, removing the need to manually recalibrate settings when shifting from short-term to long-term analysis.

In short, the Auto-Preset System is designed to make this hybrid equilibrium tool timeframe-aware — automatically scaling its logic so that the cloud behaves consistently, regardless of chart resolution.

➖

🌐 Hybrid Equilibrium Envelope

The core hybrid midpoint acts as the mean of structural (price) and volumetric (VWAP) balance.

ATR-based bands project natural expansion zones:

🔸+2.226 / –2.226 ATR → inner equilibrium (controlled trend)

*🔸+5.382 / –5.382 ATR → outer volatility extension (over-stretch / reversion zones)

Color-coded fills show regime strength:

* 🟧 Upper Outer (+5.382) – strong bullish expansion

* 🟩 Upper Inner (+2.226) – trending equilibrium

* 🔴 Lower Inner (–2.226) – mild bearish control

* 🟣 Lower Outer (–5.382) – volatility exhaustion

➖

🧭 Higher-Timeframe Framework

Two macro anchors — Price length of 144 and VWAP length of 233 — outline higher-timeframe bias zones. These help confirm when local momentum aligns with (or fades against) long-term structure.

Labels on the right show active lookback values for quick readout:

`$(13) V(21)` → current rolling pair

`$144 / V233` → macro anchors

➖

🧩 Chart Examples

**AMD 15m (Equilibrium Expansion)**

Price steadily rides above the hybrid midpoint as teal and orange (bullish) ATR zones widen, confirming a phase of controlled bullish volatility and healthy trend expansion.

BTCUSD 1m (Volatility Compression)

Bitcoin coils tightly inside the teal-to-maroon equilibrium bands before breaking out.

The hybrid midpoint flattens and ATR envelopes contract, signaling a state of balance before volatility expansion.

ETHUSD 15m (Transition from Compression → Impulse)

Ethereum transitions from purple-zone compression into a clear upper-band expansion.

The hybrid midpoint breaks above the macro VWAP 233, confirming the shift from equilibrium to directional momentum.

SOFI 1m (Micro Bias Reversal)

SOFI’s intraday structure flips as price reclaims the hybrid midpoint.

The macro VWAP 233 flattens, signaling a transition from oversold lower bands back toward equilibrium and early trend recovery.

➖

🎯 How to Use

1. Bias Detection – Price > Hybrid Midpoint → bullish; < → bearish.

2. Volatility Gauge – Watch band spacing for compression / expansion cycles.

3. Confluence Checks – Align Hybrid Midpoint with HTF 233 VWAP for strong continuation signals.

4. Mean Reversion Zones – Outer bands highlight areas where probability of snap-back increases.

➖

🔧 Inputs & Customization

Auto Presets toggle

🔸Manual Lookback Overrides** for fine-tuning

🔸Plot Window Length** (show recent vs full history)

🔸ATR Sensitivity & Fill Opacity** controls

🔸Label Padding / Font Size** for cleaner overlay visuals

➖

🧮 Formula Highlights

➖Rolling Midpoint = (highest(high,N) + lowest(low,N)) / 2

➖Rolling VWAP = Σ(Typical Price×Vol) / Σ(Vol)

➖Hybrid = (PriceMid + VWAP) / 2

➖Upper₂ = Hybrid + ATR×2.226

➖Lower₂ = Hybrid − ATR×2.226

➖Upper₅ = Hybrid + ATR×5.382

➖Lower₅ = Hybrid − ATR×5.382

➖

🎯 Ideal For

➡️ Traders who want adaptive fair-value zones that evolve with both price and volume.

➡️ Analysts who shift between scalping, swing, and position timeframes, and need a tool that self-adjusts.

➡️ Those who rely on visual structure clarity to confirm setups across changing volatility conditions.

➡️ Anyone seeking a hybrid model that unites structural range logic (midpoint) and flow-based balance (VWAP).

➖

🏁 Final Word

This script is more than a visual overlay — it’s a complete trend and structure framework built to adapt with market rhythm. It helps traders visualize equilibrium, momentum, and volatility as one cohesive system. Whether you’re seeking clean trend alignment, dynamic support/resistance, or early warning signs of reversals, this indicator is tuned to help you react with confidence — not hindsight.

➖

Remember — no single indicator should ever stand alone. For best results, pair it with price action context, higher-timeframe structure, and complementary tools such as moving averages or trendlines. Use it to confirm setups, not define them in isolation.

💡 Turn logic into clarity, structure into trades, and uncertainty into confidence.

Anchored EMA/VWAP### Anchored EMA/VWAP Indicator

**Description:**

The **Anchored EMA/VWAP Indicator** is a powerful and versatile tool designed for traders seeking to analyze price trends and momentum from a user-defined anchor point in time. Built for TradingView using Pine Script v6, this indicator calculates and displays multiple **Exponential Moving Averages (EMAs)**, **Volume-Weighted Exponential Moving Averages (VWEMAs)**, and a **Volume-Weighted Average Price (VWAP)**, all anchored to a specific date and time chosen by the user. By anchoring these calculations, traders can focus on price action relative to significant market events, such as news releases, earnings reports, or key support/resistance levels.

The indicator supports multi-timeframe (MTF) analysis, allowing users to compute EMAs, VWEMAs, and VWAP on a higher or custom timeframe (e.g., 5-minute, 1-hour, daily) while overlaying the results on the current chart. It also includes customizable cross signals for EMA and VWEMA pairs, marked with distinct shapes (circles, diamonds, squares) to highlight potential trend changes or reversals. These features make the indicator ideal for trend-following, momentum trading, and identifying key price levels across various markets, including stocks, forex, cryptocurrencies, and commodities.

**Key Features:**

- **Anchored Calculations**: EMAs, VWEMAs, and VWAP start calculations from a user-specified anchor time, enabling analysis relative to significant market moments.

- **Multi-Timeframe Support**: Compute indicators on any timeframe (e.g., 60-minute, daily) and display them on the chart’s timeframe for flexible analysis.

- **Customizable EMAs and VWEMAs**: Four EMAs and four VWEMAs with adjustable lengths (default: 9, 21, 50, 100) and colors, with options to show or hide each.

- **Volume-Weighted Metrics**: VWAP and VWEMAs incorporate volume data, providing a more robust representation of market activity compared to standard EMAs.

- **Cross Signals**: Visual markers (circles, diamonds, squares) for crossovers between EMA and VWEMA pairs, with customizable visibility to highlight bullish (up) or bearish (down) signals.

- **User-Friendly Interface**: Organized input groups for General, EMA, VWEMA, VWAP, Arrow Settings, and Cross Visibility, with intuitive inline inputs for length and color customization.

- **Visual Clarity**: Overlaid on the price chart with distinct colors and line styles (dotted for EMAs, dashed for VWEMAs, solid for VWAP) to ensure easy interpretation.

**How to Use:**

1. **Set the Anchor Time**: Click a specific bar or enter a date/time (default: June 1, 2025) to start calculations from a significant market event.

2. **Select Timeframe**: Choose a timeframe (e.g., "5" for 5-minute, "D" for daily) to compute the indicators, allowing alignment with your trading strategy.

3. **Customize EMAs and VWEMAs**: Adjust lengths and colors for up to four EMAs and VWEMAs, and toggle their visibility to focus on relevant lines.

4. **Enable VWAP**: Display the anchored VWAP to identify volume-weighted price levels, useful as dynamic support/resistance.

5. **Monitor Cross Signals**: Enable cross visibility for specific EMA or VWEMA pairs to spot potential trend changes. Bullish crosses (e.g., shorter EMA crossing above longer EMA) are marked with green shapes below the bar, while bearish crosses are marked with red shapes above the bar.

6. **Interpret Signals**: Use EMA/VWEMA crossovers for trend confirmation, VWAP as a mean-reversion level, and volume-weighted VWEMAs for momentum analysis in high-volume markets.

**Use Cases:**

- **Trend Trading**: Identify trend direction using EMA and VWEMA crossovers, with shorter lengths (e.g., 9, 21) for faster signals and longer lengths (e.g., 50, 100) for trend confirmation.

- **Mean Reversion**: Use the anchored VWAP as a dynamic support/resistance level to trade pullbacks or breakouts.

- **Event-Based Analysis**: Anchor the indicator to significant events (e.g., earnings, economic data releases) to analyze price behavior post-event.

- **Multi-Timeframe Strategies**: Combine higher timeframe EMAs/VWAPs with lower timeframe price action for high-probability setups.

**Settings:**

- **Anchor Time**: Set the starting point for calculations (default: June 1, 2025).

- **Timeframe**: Choose the timeframe for calculations (default: 5-minute).

- **EMA/VWEMA Lengths**: Default lengths of 9, 21, 50, and 100 for both EMAs and VWEMAs, adjustable per user preference.

- **Colors**: Customizable colors with slight transparency for visual clarity.

- **Cross Visibility**: Toggle specific EMA and VWEMA cross signals (e.g., EMA1/EMA2, VWEMA1/VWEMA3) to reduce chart clutter.

- **Arrow Colors**: Green for bullish crosses, red for bearish crosses.

**Notes:**

- The indicator is overlaid on the price chart, ensuring seamless integration with price action analysis.

- VWEMAs and VWAP are volume-sensitive, making them particularly effective in markets with significant volume fluctuations.

- Ensure the anchor time is set to a valid historical or future bar to avoid calculation errors.

- Cross signals are conditional on non-NA values to prevent false positives during initialization.

**Author**: NEPOLIX

**Version**: 6 (Pine Script v6)

**Published**: For TradingView Community

This indicator is a must-have for traders looking to combine anchored, volume-weighted, and multi-timeframe analysis into a single, customizable tool. Whether you're a day trader, swing trader, or long-term investor, the Anchored EMA/VWAP Indicator provides actionable insights for informed trading decisions.

VWAP Confluência 3x VWAP Confluence 3x — Daily · Weekly · Anchored

Purpose

A pragmatic VWAP suite for execution and risk management. It plots three institutional reference lines: Daily VWAP, Weekly VWAP, and an Anchored VWAP (AVWAP) starting from a user-defined event (news, earnings, session open, swing high/low).

Why it matters

VWAP is the market’s “fair price” weighted by where volume actually traded. Confluence across timeframes and events turns noisy charts into actionable bias and clean levels.

What it does

Daily VWAP — resets each trading day; intraday “fair value.”

Weekly VWAP — resets each week; swing context and larger player defense.

Anchored VWAP — starts at a precise timestamp you set (e.g., news release).

Price source toggle — Typical Price

(

𝐻

+

𝐿

+

𝐶

)

/

3

(H+L+C)/3 or Close.

Visibility switches — enable/disable each line independently.

Anchor marker — labels the first bar of the AVWAP.

Inputs

Show Daily VWAP (on/off)

Show Weekly VWAP (on/off)

Show Anchored VWAP (on/off)

Price Source: Typical (H+L+C)/3 or Close

Anchor Time: timestamp of your event (uses the chart/exchange timezone)

How to anchor to a news event

Find the exact release time as shown in your chart’s timezone.

Open the indicator settings → set Anchor Time to that minute.

The AVWAP begins at that bar and accumulates forward.

Playbook (examples, not signals)

Strong long bias: price above Daily and Weekly VWAP; AVWAP reclaimed after news.

Strong short bias: price below Daily and Weekly; AVWAP reject after news.

Mean-revert zones: price stretches far from the active VWAPs and snaps back; size around VWAP with tight risk.

Targets: opposite VWAP, prior day/week highs/lows, or liquidity pools near AVWAP.

Best used with

Session highs/lows, liquidity sweeps, volume profile, and time-of-day filters.

Notes & limitations

Works best on markets with reliable volume (equities, futures, liquid crypto). FX spot uses synthetic volume—interpret accordingly.

Anchor Time respects the chart’s timezone. Convert news times before setting.

This is an indicator, not a backtestable strategy. No trade advice.

Disclaimer

For educational purposes only. Trading involves risk. Do your own research and manage risk responsibly.

(JS) VWAP BandsThis is a pretty simple script here - I took the VWAP and combined it with Bollinger Bands.

The bands can vary a lot based on chart resolution, so I wanted to make sure the resolution could be modified so you can use the resolution you're most comfortable with, or find the most success with.

Length:

Length of bars used to calculate the bands.

Standard Deviation Band 1-3:

There's three bands all together, this option allows you to modify the number of standard deviations per band.

VWAP Period:

This modifies when you want the VWAP to begin (Session, Week, Month, Year).

Offset:

This moves the VWAP and the bands the amount of bars you select, default is of course set to zero.

Source:

This selects the source of calculation, HLC/3 is the default VWAP calculation.

This is a pretty self explanatory script, I thought being able to see the standard deviations of the VWAP could prove to be useful - hope you all like it!

2 VWAP with selective timeframe and Display liked Ichimoku CloudSET:CKP

This is my first indicator of VWAP that I fork from the original script by public script "VWAP Periodic".

You can see that original script by type "VWAP Periodic" from "New" in "Pine Indicator".

The reason that I want to share my script is only one thing. That I need to discuss, Is this indicator can identify the trend and can use it to adapt to the "Buy-On-Dip" strategy?

Double VWAP can show you 2 lines of VWAP form different periods as my default is "Week" and "Month" timeframe.

Not at all, it fulfils with the background of the simple colour which can be defined Trend just liked "Ichimoku Cound" (Yes indeed, green is uptrend and red is downtrend).

I hope this indicator will help :)

Wishing you good health and get wealth too. :) :) :)

---------------------------------------------------------------------------------------------

สวัสดีครับมิตรสหายทุกท่าน อินดิเคเตอร์ที่ผมจะมานำเสนอมิตรสหายนี้ เป็นอินดี้ที่จะแสดงเส้น VWAP ได้ทั้งหมด 2 เส้น โดยท่านสามารถระบุ Timeframe ของ VWAP ที่ท่านต้องการได้เลยครับ

ก่อนอื่นผมของออกตัวก่อนครับ ว่าอินดิเคเตอร์นี้ผมโฟร์คมาจาก Original Public Script จากใน Pinescript แห่ง Trading View นี่ละครับ จากอินดิเคเตอร์ที่มีชื่อว่า "VWAP Periodic" ซึ่งท่านสามารถ กดดู Original Script ได้จากการกดที่

1) ไพน์อินดิเคเตอร์

2) กดเลือกคำว่า "ใหม่"

3) หาอินดิเคเตอร์ที่ชื่อว่า "VWAP Periodic"

้เท่านี้ท่านก็จะได้สคลิปต้นแบบที่ผมนำมาปรับใช้ได้ทันทีครับ

แต่กระนั้นแล้ว ผมจะเปิดโชว์สคริปของผมที่นำมาโฟร์คแล้วให้ทุกท่านได้รับชมกันด้านล่างในส่วนของโค้ดนะครับ

จุดประสงค์ของอินดิเคเตอร์นี้คือได้ฟังแนวคิดของ VWAP จากกัลยาณมิตรเทรดเดอร์ด้วยกันแล้วรู้สึกคลิ๊ก กับอินดิเคเตอร์นี้มากครับ

จะมีอะไรดีไปกว่าการได้รู้ต้นทุนราคาของแต่ละช่วงเวลา ทั้งไทม์เฟรมที่ใหญ่อย่างระดับ "เดือน (เส้นสีเขียว)" และ ระดับ "สัปดาห์ (เส้นสีแดง)" ได้พร้อมกันและดูแท่งเทียนเพื่อ "จับจังหวะซื้อ"(ในไทม์เฟรม ระดับ วัน) ที่ราคาต่ำกว่าค่า VWAP อีกเล่าอรชุน

จุดประสงค์หลักของอินดิเคเตอร์นี้ คือมีไว้เพื่อระบุเทรนด์โดยอาศัยการดูระยะห่างของเส้น VWAP ทั้ง 2 เส้นนี้ และระบุ "จุดกลับตัว" เมื่อก้อนเมฆสีเขียวและแดงเริ่มหายไป เสมือนกับอินดิเคเตอร์ "เมฆหมอกแห่งอิชิโมคุ"

นอกจากนี้เมื่อราคาหุ้นปรับตัวเป็นเทรนด์ขาขึ้นแล้ว เรายังสามารถซื้อเฉลี่ยขาขึ้น หรือใช้กลยุทธ์ Buy-on-Dip ได้อีกด้วยครับ โดยเฉลี่ยซื้อเมื่อราคาตกย่อมาอยู่ที่เส้นสีเขียว แบบนี้เป็นต้นครับ

ผมหวังว่าอินดิเคเตอร์นี้จะเป็นประโยชน์ให้แก่มิตรสหาย และกัลยาณมิตรเทรดเดอร์ทุกท่านนะครับ

ผมขออวยพรให้ทุกท่านมีความสุข ออกจากสนามแข่งหนูนี้ ได้รับอิสระภาพทางการเงิน และ "มีสุขภาพที่แข็งแรง" Work life balance ทุกท่านครับ

ขอบคุณครับ :) :) :)

8 EMA. 21 EMA. VWAP This trio is popular for momentum, scalping, and trend-following on 1m–15m charts (stocks, futures, indices).

1. Trend & Bias Filter

• Overall bullish when: Price > VWAP and 8 EMA > 21 EMA

• Overall bearish when: Price < VWAP and 8 EMA < 21 EMA

VWAP adds volume context — many ignore EMA signals against the VWAP side.

2. Crossover Signals (Primary Entries)

• Bullish crossover: 8 EMA crosses above 21 EMA → potential long (especially if price is already above VWAP)

• Bearish crossover: 8 EMA crosses below 21 EMA → potential short (especially if price is below VWAP)

VWAP confirmation reduces whipsaws: only take longs above VWAP, shorts below it.

3. Pullback / Retest Entries (Higher Probability)

• In an uptrend (price > VWAP, 8 > 21): Wait for dips to the 8 EMA (or sometimes 21 EMA) → buy the bounce.

• In a downtrend: Wait for rallies to the 8 EMA → short the rejection.

VWAP often acts as a magnet or pivot — price gravitating toward it can signal mean-reversion trades.

Volume + VWAP + Prior Session Levels DashboardVolume Spike + VWAP + Session Levels Dashboard

This indicator is a real-time market context dashboard designed to help traders quickly understand participation, value, and key reference levels without cluttering the chart with multiple indicators.

Instead of plotting lines or signals, the script summarizes critical intraday information into a compact on-chart table, allowing traders to make faster, more informed decisions based on how active the market is, where fair value is, and where important reference levels exist.

Core Concepts Used

This script is built on three widely used market principles:

Relative Volume Participation

Volume-Weighted Average Price (VWAP)

Prior Session Reference Levels

The indicator does not attempt to predict direction. Its purpose is to provide objective context that traders can combine with their own strategies.

How the Indicator Works

1. Volume Spike Analysis (Relative Volume)

Rather than showing raw volume, the script measures how unusual the current bar’s volume is compared to recent activity.

A moving average of volume is calculated using a user-defined lookback period.

Current volume is divided by this average to produce a volume multiple (for example, 2.0× normal volume).

This multiple is translated into a descriptive strength label, ranging from Below Threshold to Legendary.

This approach helps traders immediately recognize when participation is significantly above normal, which often coincides with institutional activity, breakouts, or important reactions near key levels.

2. Daily VWAP (Current and Prior Day)

VWAP (Volume-Weighted Average Price) represents the average price traded, weighted by volume, and is commonly used as a measure of fair value.

This script calculates VWAP internally by:

Accumulating price × volume throughout the day

Dividing by total volume

Automatically resetting at the start of each new trading day

The dashboard displays:

Current day VWAP – real-time session fair value

Prior day VWAP – an important reference from the previous session

Traders often use these levels to evaluate whether price is trading at a premium, discount, or near equilibrium.

3. Previous Day High and Low

The indicator also displays:

Previous day high

Previous day low

These levels frequently act as liquidity targets, support/resistance zones, or reaction points, especially during intraday trading sessions.

Dashboard Design

All information is presented in a two-column dashboard showing:

Metric name

Current value or status

The dashboard can be positioned in any corner of the chart and updates in real time, allowing traders to maintain awareness without constantly switching indicators or timeframes.

How to Use This Indicator

This script is best used as a decision-support tool, not a standalone trading system.

Typical uses include:

Identifying abnormally high volume near important price levels

Evaluating price position relative to VWAP

Monitoring reactions around prior day highs and lows

Staying oriented during fast market conditions without chart clutter

The indicator works on any timeframe and adapts automatically to the instrument’s trading session.

Customization Options

Users can:

Adjust the volume moving average length to define what “normal” volume means

Choose the price source used for VWAP calculation

Change the dashboard’s on-screen position

Summary

The Volume Spike + VWAP + Session Levels Dashboard provides a clear, objective snapshot of market conditions by combining participation, value, and reference levels into a single visual tool. It is designed to help traders answer a simple but critical question:

“Is the market doing something meaningful right now — and where?”

This indicator focuses on context, clarity, and usability for traders who want insight without unnecessary complexity.

Bollinger Bands + VWAP + 4-State MACD BackgroundBollinger Bands + VWAP + 4-State MACD Background

An all-in-one technical analysis indicator combining three proven tools with an intelligent momentum-based background visualization system.

📊 FEATURES

Bollinger Bands

Standard Bollinger Bands implementation with full customization options:

Adjustable period length (default: 20)

Multiple moving average types: SMA, EMA, SMMA (RMA), WMA, VWMA

Configurable standard deviation multiplier (default: 2.0)

Visual fill between bands to highlight volatility zones

Offset capability for forward/backward display

Session VWAP (Volume Weighted Average Price)

Automatically resets at the start of each trading session:

Calculates true volume-weighted average price

Resets daily to provide fresh reference levels

Customizable source input (default: HLC3)

Adjustable line appearance (color and width)

Can be toggled on/off as needed

4-State MACD Background System

This is the unique feature of this indicator. The chart background dynamically changes based on MACD momentum analysis, providing instant visual feedback on trend strength and direction:

🟢 Strong Bullish (Bright Green)

MACD line is above signal line

Histogram is growing (momentum accelerating upward)

Indicates strong upward momentum

🟢 Weak Bullish (Pale Green)

MACD line is above signal line

Histogram is shrinking (momentum decelerating)

Early warning signal that uptrend may be weakening

🔴 Strong Bearish (Bright Red)

MACD line is below signal line

Histogram is falling (momentum accelerating downward)

Indicates strong downward momentum

🔴 Weak Bearish (Pale Red)

MACD line is below signal line

Histogram is rising (momentum decelerating)

Early warning signal that downtrend may be weakening

🎯 HOW TO USE

For Trend Trading:

Strong colored backgrounds indicate confirmed momentum in that direction - consider staying with the trend

Weak colored backgrounds signal potential momentum exhaustion - watch for possible reversals

Use VWAP as a dynamic support/resistance level

Bollinger Band breakouts combined with strong MACD backgrounds can confirm trend strength

Price above VWAP + strong bullish background = bullish bias

Price below VWAP + strong bearish background = bearish bias

For Mean Reversion:

Price touching upper/lower Bollinger Bands with weak MACD background may suggest potential reversal

VWAP acts as a mean reversion anchor during range-bound sessions

Background color shifts from strong to weak often precede price direction changes

Look for price return to VWAP when extended beyond bands with weakening momentum

Signal Confirmation:

Strongest signals occur when multiple indicators align:

BB breakout + MACD strong color + price above/below VWAP

Price rejection at BB bands + MACD color weakening

VWAP support/resistance hold + MACD color change

⚙️ SETTINGS

All components are fully customizable through organized input groups:

Bollinger Bands Group:

Period length

Moving average type (SMA/EMA/SMMA/WMA/VWMA)

Source (close/open/high/low/etc.)

Standard deviation multiplier

Offset

VWAP Group:

Toggle show/hide

Source calculation method

Line color

Line width

MACD Group:

Toggle background on/off

Fast length (default: 12)

Slow length (default: 26)

Signal length (default: 9)

Source

Four separate color settings for each momentum state

All colors include transparency controls

💡 EDUCATIONAL VALUE

This indicator teaches important concepts:

How volatility (Bollinger Bands) relates to price movement

The importance of volume-weighted pricing (VWAP)

Momentum analysis through MACD

How combining multiple timeframes and indicators can provide confluence

The difference between trend strength and trend direction

⚠️ IMPORTANT NOTES

This indicator is for educational and informational purposes only

No indicator is perfect - always use proper risk management

Past performance does not guarantee future results

Combine with your own analysis and risk tolerance

Test thoroughly on historical data before live trading

This is not financial advice - use at your own risk

🔧 TECHNICAL DETAILS

Pine Script Version 6

Overlay indicator (displays on price chart)

All calculations use standard, well-documented formulas

Minimal lag due to efficient coding

Compatible with all timeframes and instruments

No repainting - all signals are confirmed on bar close

📝 CHANGELOG

Version 1.0

Initial release

Bollinger Bands with multiple MA types

Session VWAP with daily reset

4-state MACD background system

Full customization options

Developed for traders who want multiple confirmation signals in a clean, organized format without cluttering their charts with separate indicator panels.

Custom MTF VWAP 5x This is a combination of all VWAPs I use to find high probability trade setups and targets by only taking trades when different VWAPs align

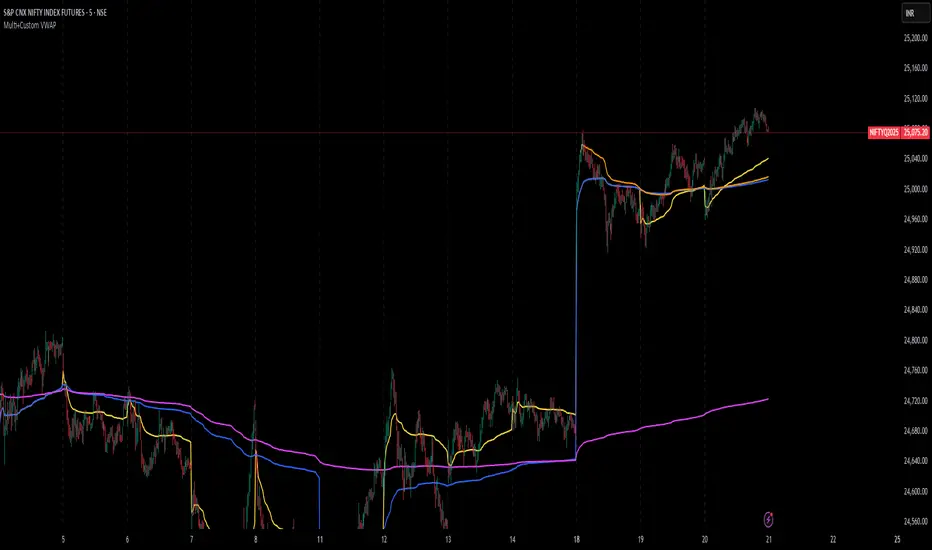

Multi+Custom VWAPMulti-VWAP (Session, Weekly, Monthly, Custom)

Description:

This script plots multiple VWAP (Volume Weighted Average Price) levels on the chart, giving traders a broader perspective of price action across different time horizons.

Features:

Session VWAP → Resets at the start of each trading session.

Weekly VWAP → Resets every Monday.

Monthly VWAP → Resets at the start of each new month.

Custom VWAP → User can specify a custom start date and time, and the script will calculate VWAP from that moment until the current bar.

Use Cases:

Compare intraday (session) VWAP with higher-timeframe VWAPs (weekly & monthly) to spot confluence levels.

Track how price interacts with institutional benchmarks.

Use custom VWAP to anchor from specific events (earnings, news releases, breakouts, etc.).

Notes:

Works on any timeframe and instrument that has volume data.

Designed to be clean and minimal with adjustable colors and line styles.

Useful for day traders, swing traders, and long-term investors who monitor VWAP across multiple time horizons.

(JS) Interchanging ATR & VWAP BandsOkay so this is pretty simple, but I think it's a great tool for day trading especially. I just took the default VWAP and Keltner channel scripts and combined them together.

The top option allows you to choose which one you'd prefer to use, "Use ATR instead of VWAP" .

The next options, "ATR Source", "KC Length", and "ATR Length" are the parameters for the ATR Bands.

"Number of Bands" allows you to choose how many bands you'd like to be on display (you can choose 1-8).

"Use Expoential MA" and "Band Style" are more default parameters from Keltner Channels used to set up the ATR Bands.

The "ATR Bands" are just stacked Keltner Channels separated by 1 ATR each, whereas the "VWAP Bands" are separated by standard deviation just like the default script from Trading View.

In these example chart, you can see the weekly VWAP with 8 deviation bands and 5 ATR bands with Keltner Channels.

Auction Context Engine ( Value Area, VWAP & Regime)📌 Indicator Name

Auction Context Engine (Value Area, VWAP & Regime)

Short name: ACE Context

🧠 Description

Auction Context Engine (ACE) is a professional market context and structure indicator based on Auction Market Theory.It is designed to help traders understand where the market is positioned, not to generate trade signals.

ACE focuses on:

• Developing Value Area (VAH / VAL)

• Developing Point of Control (POC)

• Session VWAP positioning

• Volatility regime expansion

• Opening Range context

• Failed auction / trap detection

• Market bias and environment quality

This indicator provides context only and is intended to be used alongside a separate execution strategy or system.

🎯 What This Indicator Is

✔ A context engine

✔ A market structure filter

✔ A bias alignment tool

✔ A regime and environment classifier

❌ What This Indicator Is NOT

✘ Not a signal generator

✘ Not a buy/sell system

✘ Not a strategy

✘ Not a profitability promise

📊 How To Use

Use ACE to answer:

• Is price accepting or rejecting value?

• Is the market in balance or expansion?

• Is VWAP supporting or opposing price?

• Is this a breakout environment or a trap?

• Is volatility expanding?

• Is the market trending or ranging?

You may then use your own execution strategy aligned with this context.

🟢 Core Components

Developing Value Area

• VAH / VAL dynamically update through the session

• POC tracks highest traded volume area

VWAP Position

• Above VWAP = bullish bias

• Below VWAP = bearish bias

Opening Range Context

• Detects breakouts or balance after session open

Volatility Regime

• Identifies expansion vs normal conditions

Failed Auction Detection

• Highlights trap conditions near value extremes

Market Quality

• Strong / Mixed / Weak environment classification

Context Table

• Clean 1-column vertical dashboard with color-coded bias

🔵 Visual Elements

• Developing VAH, VAL, POC lines

• Session VWAP

• Small context dots when environment turns READY

• Compact professional context table

⚙️ Settings

• Value Area bin size

• Value area percentage

• Opening range duration

• Regime expansion factor

• Line colors and thickness

• Context table ON/OFF

• Context dots ON/OFF

🧩 Best Use Case

This indicator is ideal for:

• Intraday trading

• Index futures and equities

• Options context filtering

• Trend / range regime identification

• Professional discretionary traders

⚠️ Disclaimer

This script is provided for educational and informational purposes only.It does not constitute financial or investment advice.Trading involves risk. Always use proper risk management.