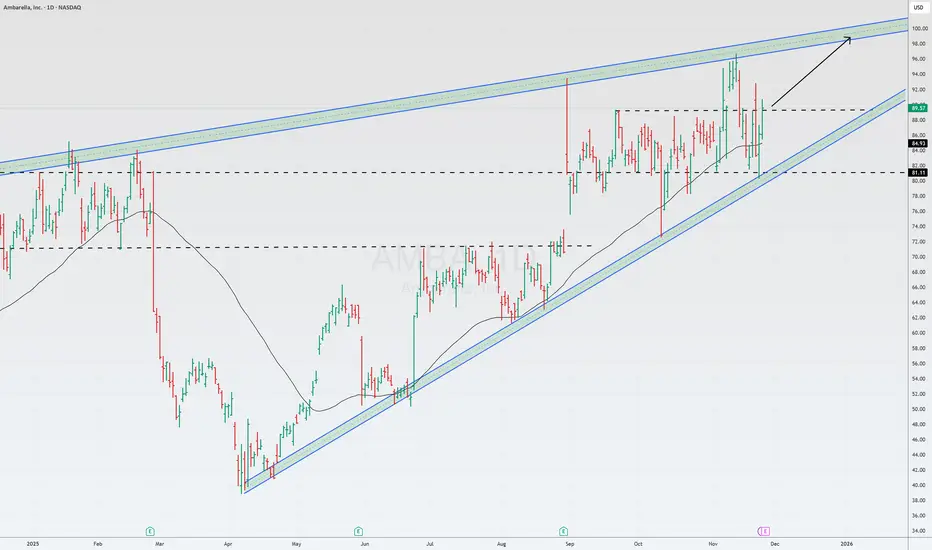

🌎 Ambarella is demonstrating impressive revenue growth, exceeding 50% year-on-year, thanks to a strategic shift in focus from the automotive market to the Internet of Things (IoT). IoT, rather than the once-primary focus of autonomous vehicles, now generates the majority of revenue and is a key driver behind the company's improved financial outlook.

Ambarella's investment case was previously based on promising but slowly developing autonomous driving projects. Today, 75% of its revenue comes from the IoT segment, which includes not only surveillance cameras but also wearable cameras, robotics, and edge computing equipment.

The foundation of this success is the new CV5/CV7 processors, manufactured using 5nm technology. These chips are unique in their ability to combine image processing, video encoding, and artificial intelligence on a single chip. This integration allows the company to offer more powerful solutions for compact, power-constrained devices (such as drones or video cameras) and set high prices, avoiding direct price competition with lower-cost manufacturers.

The short product development cycle for IoT allows R&D investments to be converted into revenue more quickly compared to the long cycle time for automotive products. Using a common technology platform (CVflow) for both IoT and automotive applications reduces development costs.

Cons:

Growth is not converting into significant free cash flow. There is a worrying dependence on a single distributor (WT Microelectronics, 71% of revenue) and a single manufacturer (Samsung), creating supply chain risks. High chip production costs may begin to pressure profitability.

Ambarella's investment case was previously based on promising but slowly developing autonomous driving projects. Today, 75% of its revenue comes from the IoT segment, which includes not only surveillance cameras but also wearable cameras, robotics, and edge computing equipment.

The foundation of this success is the new CV5/CV7 processors, manufactured using 5nm technology. These chips are unique in their ability to combine image processing, video encoding, and artificial intelligence on a single chip. This integration allows the company to offer more powerful solutions for compact, power-constrained devices (such as drones or video cameras) and set high prices, avoiding direct price competition with lower-cost manufacturers.

The short product development cycle for IoT allows R&D investments to be converted into revenue more quickly compared to the long cycle time for automotive products. Using a common technology platform (CVflow) for both IoT and automotive applications reduces development costs.

Cons:

Growth is not converting into significant free cash flow. There is a worrying dependence on a single distributor (WT Microelectronics, 71% of revenue) and a single manufacturer (Samsung), creating supply chain risks. High chip production costs may begin to pressure profitability.

免责声明

这些信息和出版物并非旨在提供,也不构成TradingView提供或认可的任何形式的财务、投资、交易或其他类型的建议或推荐。请阅读使用条款了解更多信息。

免责声明

这些信息和出版物并非旨在提供,也不构成TradingView提供或认可的任何形式的财务、投资、交易或其他类型的建议或推荐。请阅读使用条款了解更多信息。