原油 CRUDE 趋势与基本交易策略周线复合:熊市反转加上本周的更低收盘价,强烈表明每周⾼点已经完成(熊)

日线复合:任何下跌趋势的反弹应该都是暂时的,周熊市⾄少持续2-3周 (熊)

关键因素:日收盘低于 5999.25,是W3 完成的初步信号

交易策略建议:只要 ES 指数日收盘未⾼于6/12 ⾼点,就继续持有空头头⼨

⚠ 短期交易者应以TradingBox信号系统为准

包含IO脚本

S&P 500趋势与基本交易策略周线复合:熊市反转加上本周的更低收盘价,强烈表明每周⾼点已经完成(熊)

日线复合:任何下跌趋势的反弹应该都是暂时的,周熊市⾄少持续2-3周 (熊)

关键因素:日收盘低于 5999.25,是W3 完成的初步信号

交易策略建议:只要 ES 指数日收盘未⾼于6/12 ⾼点,就继续持有空头头⼨

⚠ 短期交易者应以TradingBox信号系统为准

6月25日比特币早盘玄学预测老宝贝们,今天出梅不下雨了,天气晴朗☀️,又到了去海边安静灰茄的一天!

昨天比特币横盘一天,今早又开始小幅反弹。

今早10点起卦得本卦中孚:信而得助,主“整固后再进”,符合目前比特币的稳定上攻的形态

二爻动为兑(口、兑泽)变震(动、雷),象“口动化雷”——主动买盘放量。

互卦离火 说明中途会有一次明-暗量能的点火;

变卦益木 增益、扶助,为顺势放大。再度扶持体爻木,意味着 最终仍以上涨收场。

总体:多方占优,日内仍有增益空间,但先稳后升。

10:00~20:00 预估收盘概率 68 % 收于 106 900 ± 200日内极值:上看 107 200 ± 100;下看 105 700 ± 200(动兑克体的最低回踩位)

预祝今天多多收米,需要雪茄和茅台的请私聊。本总不带单,只卖烟酒。

欧元EUR趋势与基本交易策略周线复合:如果周⾼点尚未完成,那么在周⾼点确认之前,上⾏空间也应该非常有限

日线复合:日低点完成前,短期趋势应为横盘下跌 2-3 天 (熊)

关键因素:欧元处于⼀个⼏乎理想的位置来完成⼀个五浪的周⾼点,但需要日收盘价低于 6/6 收盘价来进⾏确认

交易策略建议:收盘价低于6/6则确认周⾼点,之后我的主要目标将是确定欧元何时处于完成从 6 月⾼点开始的修正的位置,然后继续⽜市趋势⾄新的⾼点

⚠ 短期交易者应以TradingBox信号系统为准

技术形态乐观,基本面却危险:BTC真的准备好继续上行了吗?📉 比特币每日简报 📈

BTC 已经触及日线 20 日均线,这正是我昨天复盘中提到的短期目标位。

在更小周期上,BTC 正在 5 月月线收盘价上方构筑多头旗形,有可能引发下一轮上涨动能,目标可能冲向 107k–108k 区间。

但在那之前,仍有较大概率回踩 103600 附近。

尽管如此,在这个阶段对做多仍保持谨慎态度。

昨日的上涨是受到特朗普发出“和平”推文的推动 —— 而我对他说或写的每一个字都持怀疑态度。

他今天可能就会改变立场,伊朗或以色列也可能如此。

没有真正的停火,这场战争就不会结束 —— 它才刚刚开始。

🎯 关键技术位关注

上方阻力位:105535 / 107727 / 108900 / 110000

下方支撑位:104544 / 103246 / 102614 / 100900

🔥 BTC 清算热力图

上方密集清算价位:105890 / 106932 / 107974

下方密集清算位:104470 / 103807 / 102955 / 101913

📊 趋势方向

日线:➡️ 横盘

周线:🔼 上行

月线:🔼 上行

🧠 恐惧与贪婪指数(过去 5 天)

65 → 47 → 42 → 49 → 54(波动频繁,情绪偏中性至乐观)

黄金GOLD趋势与基本交易策略周线复合:在周低点确认前,下跌空间应当相对有限

日线复合:超波反转为空,以去完成日线低点 (熊)

关键因素:证据显示偏向多头。但若日线收盘低于 3343,即 6/10 收盘价,将使多头前景⽆效,并暗示周线⾼点已形成。周五距离 6 月 9 日的低点有 8 个交易日。周⼆将是第 10 天,最有可能完成日线低点

交易策略建议:超波反转多头且价格未收于 6 月 10 日收盘价下⽅,将形成做多策略设置

⚠ 短期交易者应以TradingBox信号系统为准

6月23日比特币早盘玄学预测昨晚主力很给面子完全按照占卜走势来走,一针插到98800以下,现在早盘持续反弹中。

今天苏州喝茶🍵,早间占卜得

本卦 · 地泽临 “临”=大地覆水,阳气由下而上,主渐进、扶持、靠近。大盘处于低位区间,资金呈缓慢回流;不适合急涨急跌,易走阶梯状(凹字或 W)走势。

变卦 · 水天需 “需”=等待、蓄势。游魂卦,主 消息或外力触发 后才展开下一波。多空都缺决心;关键突破往往在 场外资金或突发新闻 催化时完成。

分时预测走势:

10-11 100 700 – 101 450

12-13 100 900 – 101 700

18-19 100 600 – 101 250

19-20 100 800 – 101 400

风险位

下破 100 300(16–17 h 下沿)→ 卦中“需”字守不住,日线 99 800-99 500 见支撑。

上破 101 700 → 清算带大增,可能瞬拉触 102 200 然后回落。

比特币趋势与交易策略周线复合:周⾼点应该已经完成,未来2-3周为横盘⾄下跌趋势 (熊)

日线复合:超波仍未反转,但警惕日线低点临近(熊)

关键因素:时间因素表明日线低点应在 6 月 27 日之前完成,可能在下周⼆或周三。然⽽,由于周趋势转熊,任何反弹都应该是周熊趋势中的内部修正。日线收盘若⾼于6.16⾼点则预示看跌熊市失效

交易策略建议:下⼀次交易机会应该出现在周趋势转⽜应该是 2-3 周之后

⚠ 短期交易者应以TradingBox信号系统为准

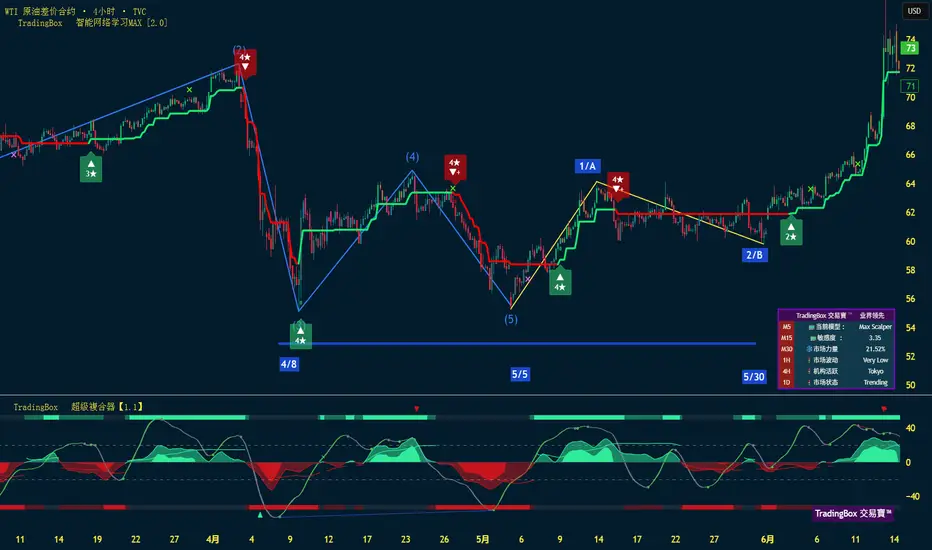

原油 CRUDE 趋势与基本交易策略周线复合:周⾼点接近,价格已达到周⾼点完成的位置(熊)

日线复合:日⾼点即将到来,应该与周⾼点重合 (熊)

关键因素:71.29-72.05(日收盘价)是⼀个关键目标区域,它与 4 月 W.2 的摆动⾼点重合。原油收于该⽔平之上,使其处于完成 W.3 和周⾼点的位置

交易策略建议:到下周中时⾄少出现⼀个日线级⾼点,同时也有可能是周⾼点

⚠ 短期交易者应以TradingBox信号系统为准

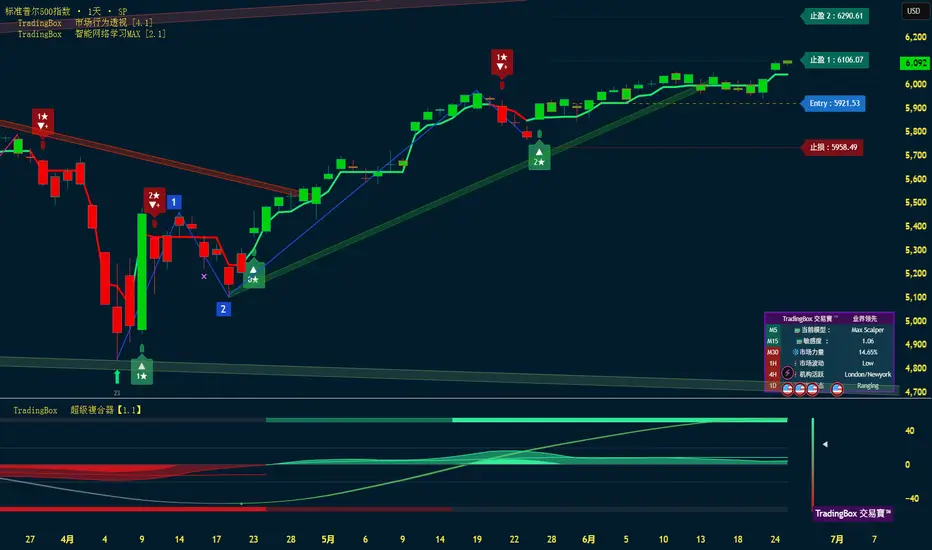

S&P 500趋势与基本交易策略周线复合:熊市反转强烈暗示着周⾼点已经完成 (熊)

日线复合: 日线复合器分歧,超波反转,并价格下跌动能强劲,确认⾼点可能已经完成 (熊)

关键因素:日收盘价低于 6 月 5 日的收盘价,将确认周⾼点已形成,随后应会出现⼀个为期 2-3 周左右的修正,并可能达到 38%回撤位左右

交易策略建议:日线收盘低于 5946(6 月 5 日收盘)即可做空

⚠ 短期交易者应以TradingBox信号系统为准

欧元EUR趋势与基本交易策略周线复合:中性,在确认周⾼点前,上涨的空间应该有些

日线复合:中性,W5浪⾼点可能在未来⼏天⾏程

关键因素:这周的新⾼使得4月作为5浪新⾼点的预测失效,但并未消除欧元已抵达周级别⾼点的技术支持

交易策略建议:接下来⼏周,我的主要目标是确定欧元何时处于完成W5⾼点开始的修正

⚠ 短期交易者应以TradingBox信号系统为准

黄金GOLD趋势与基本交易策略周线复合:价格横盘上涨2-3周以完成周⾼点(牛)

日线复合:超波反转短期内趋势横盘上涨2-3天

关键因素:正如上期周报所说,技术面权重正在转向⽜市,日线超波反转, ABC修正应该已经完成

交易策略建议:上周四已触发做多策略。预计价格将上涨⾄ 3615 或更⾼。日收盘价低于 3343 GC期货设⽌损( 6/10 摆动低点)

⚠ 短期交易者应以TradingBox信号系统为准

比特币趋势与交易策略周线复合:周⾼点应该已经出现 (熊)

日线复合:日线底部复合,但短期内上涨的空间应当有限(牛)

关键因素:5 月 22 日⾄ 6 月 5 日的下跌是强动能的,在时间和价格上都比自 4 月低点修正要⼤, 警告周⾼点应该已经完成

交易策略建议:在确认周⾼点前,任何的进⼀步价格上涨应当都会得到限制,下⼀个长线趋势交易机会是在周动能再次⽜市反转时,应该在⼏周后

⚠ 短期交易者应以TradingBox信号系统为准

一张图搞懂缠论同级别与非同级别分解

# 同级别分解

同级别分解指的是分解出的走势中,中枢级别大致相同,并不要求完全一致。

就像苹果虽大小略有差异,仍归为同一类。

在同级别分解中,只要中枢未达到“9笔升级”的标准,

即可视为同一级别走势。

如上图三个中枢,均为同级别!

# 非同级别分解

非同级别分解是在同级别分解的基础上,

将这些有重叠的同级别走势进行重新组合划分,

从而可以观察到更高级别的区间套背驰关系。

这种方法的核心在于:

- 它不仅限于当前级别的走势分析,

- 还能观察到更高级别的走势分析,

- 使分析者不再一叶障目,

- 而是可以看到整片森林。

简单地讲,

就是以本周期图上那个最大级别的中枢为中心,

将这个最大级别中枢前后的走势看成进入段和离开段。

进入段与离开段显然也有级别较小的中枢,

这些大小不同的中枢形成了级别上的嵌套关系,

其所在的走势类型也同时形成了区间套的背驰关系。

为了方便大家理解同级别分解和非同级别分解,

我们选择在同一个走势图上进行分解,

让大家更容易理解这个概念。

# 同级别分解案例

如上图,0-9是方向向上的趋势走势类型;

9-12、15-18为简单的、只有三笔构成的盘整下跌走势类型;

12-15是简单的、只有三笔构成的盘整上涨走势类型;

18-27为标准盘整上涨走势类型。

在同级别分解视角下,0-9、9-12、12-15、15-18、18-27都看作同级别走势类型的上下连接。

即便0-9间的3点与6点有重合,构成扩展中枢,0-9也被视为与9-12、12-15、15-18、18-27相同级别的走势类型。

# 非同级别分解案例

9-18内部因为有9笔重叠,按照同级分解的原则,把它划分为9-12、12-15、15-18三个同级别走势。

但同时又将这三个同级别走势组合在一起,形成高一级别走势中枢进行综合分析。

即以9-18这个最大级别中枢为中心,

0-9划分为进入段,

18-27划分为离开段。

整个0-27走势划分为三部分连接:

- “0-9趋势上涨进入段a”

- “9-18更大级别盘整中枢A”

- “18-27盘整上涨离开段b”

在0-27这个走势中,1-4、5-8、21-24三个中枢级别相同,但比9-18中枢级别小。

19-20、25-26中枢比21-24中枢级别又小。

对这些中枢级别大小不同的走势进行组合分析,称为非同级别分解。

具体表现为:

- “18-27盘整走势类型离开段”与“0-9趋势走势类型进入段”进行力度比较背驰;

- “18-27这个盘整走势类型离开段”中的24-27与18-21进行力度比较也背驰;

- 26-27与24-25进行力度比较,又形成背驰。

这样形成了走势力度层层递减的区间套背驰关系。

也就是三个大小级别的共振背驰。

因此,0-27走势在27点终结是理所当然的。

操作熟练的,甚至可以当下指出27点结束,而不需要后续下跌和二卖的确认。

在非同级别分解视角下,

走势可以划分为上涨、下跌与更大级别盘整三种走势类型的连接(即进出段a和b + 中枢A)。

而在同级别分解视角下,

只有向上和向下两个方向线段的延伸或走势类型的连接。

两种分解的连接为什么有这么大的差距呢?

原因就在于:

在同级别分解下,

那个非同级别视角下的最大级别中枢,

被同级别分解以次级别走势类型的方式拆分了,仅此而已。

同级别分解把非同级别分解下的那个最大级别中枢,

拆成几个次级别走势类型的连接,

当然都是唯一分解,唯一分类了。

因此,也可以说,

对同一个走势用两种方法分解,

同级别分解后的走势类型基本都是非同级别分解走势类型的次级别走势类型。

两种分解其实是一个东西,殊途同归,

只不过观察的侧重点不同罢了。

同级别分解聚焦在线段的延伸上,

非同级别分解聚焦在中枢的升级和后期走势的预见性上。

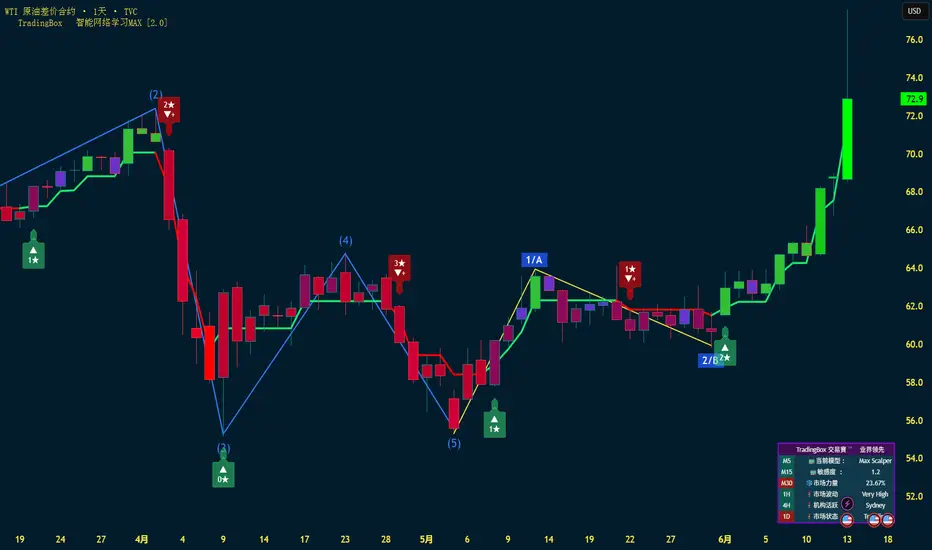

原油 CRUDE 趋势与基本交易策略周线复合:周低点应该已经完成。再持续2-3周才会完成 (牛)

日线复合:虽然日线⾼点近在眼前,但任何下跌都应是在周多头趋势中的轻微3-4 天修正

关键因素:日线收盘价⾼于了 5 月 13 日、第⼀波或 A 波的收盘价,确认了第⼆波或 B 波的低点 并延续了短期⽜市趋势

交易策略建议:原油已经达到 67.75-68.59(每日收盘价)目标区间,未来一两天内至少可能达到每日高点

⚠ 短期交易者应以TradingBox信号系统为准

S&P 500趋势与基本交易策略周线复合:周⾼点应该在接下来1-2周完成

日线复合:复合器顶部汇合,日线⾼点临近,有可能与周⾼点重合 (牛)

关键因素:根据美国历史选举年的第⼆季度周期,证据倾向于在 6 月中旬形成⼀个暂时⾼点,并在接下来的 2-3 周左右呈横盘或下跌趋势

交易策略建议:日线收盘价若低于周四收盘价,则主3浪完成

⚠ 短期交易者应以TradingBox信号系统为准

欧元EUR趋势与基本交易策略周线复合:周熊市趋势⾄少在持续2-3周以去完成周级别低点(熊)

日线复合:超波再次反转将确认日线⾼点,很可能就会在未来2-3天发⽣

关键因素:日线收盘价低于6.3日收盘价是⼀个波浪 B完成的信号,随后周熊市趋势将持续,以完成ABC的修正

交易策略建议:接下来⼏周,我的主要目标是确定欧元何时处于完成从 4 月份⾼点开始的修正

⚠ 短期交易者应以TradingBox信号系统为准

黄金GOLD趋势与基本交易策略周线复合:趋势将横盘或下跌 3-4 周左右,周低点才会完成(熊)

日线复合:黄⾦处在完成日线⾼点的位置

关键因素:黄⾦技术面是有些⽭盾的,在 5 月15 日某种程度是完成了ABC的修正

交易策略建议:如果黄⾦收盘价没有低于 5.30 日收盘价,且复合器形成⼀个底部看涨,这将是⼀个做多策略的设置

⚠ 短期交易者应以TradingBox信号系统为准

比特币趋势与交易策略周线复合:周⾼点即使没有完成也非常接近 (熊)

日线复合:日线低点应该已经完成,趋势横盘上涨3-4天 (牛)

关键因素:5 月 22 日⾄ 6 月 5 日的下跌是强动能的,在时间和价格上都比自 4 月低点修正要⼤, 警告周⾼点可能已经完成。我们会在日报上进⾏详细阐述

交易策略建议:周级别⾼点可能已经完成或非常接近。长期交易者的多头仓位应设置追逐⽌损

⚠ 短期交易者应以TradingBox信号系统为准

比特币剑指15万美金:技术面VSH与供需双轮驱动的超级周期

一、技术面:VSH奠定底层安全基石

比特币的底层技术依赖密码学哈希函数(如SHA-256),而VSH(Very Smooth Hash)作为高效抗碰撞算法 ,其安全性基于 模平方根难题(VSSR) ,为区块链提供不可篡改的信任基础。尽管VSH因伪随机性局限不直接用于比特币签名 ,但其设计思想(如高效乘法运算)反映了密码学创新的持续演进 ,强化了比特币网络抵御攻击的能力——这是长期价值存储的核心前提。

二、供需结构:史无前例的稀缺性危机

1. 供应枯竭加速

总量锁死:2100万枚BTC中95%已挖出,年通胀率仅1.7%^31,低于黄金和美元目标通胀率。

流动性枯竭:交易所可用BTC库存从2020年530万枚骤降至460万枚^35,仅够支撑6个月需求^55。

矿工惜售:减半后挖矿收益下降,矿工囤币意愿达历史高点^48。

2. 需求爆发式增长

机构鲸吞:2025年至今机构增持41.7万枚BTC(散户净卖出15.8万枚) ,美国现货ETF持仓超387亿美元^105。

全球渗透缺口:95%人口尚未持有BTC ,潜在增量需求庞大。

链上指标:活跃地址数周增15% ,累积地址月增49.5万枚^39,显示长期持有者主导市场。

三、历史周期与技术指标:15万美金的目标合理性

减半规律:历次减半后12-18个月涨幅超300%^73,当前处于2024减半后的爆发窗口。

技术形态:2025年价格走势与历史牛市高度吻合,关键支撑位65,000美金成新底部^63。

机构共识:渣打银行、Bernstein等预测2025年底目标价15万美金^164,核心逻辑是ETF资金持续流入(预计2025年达600亿美元^159)。

四、市场情绪与催化剂

情绪反转:恐惧贪婪指数从29%(恐惧)升至61%(贪婪)^120,释放买入信号。

宏观助力:全球降息周期开启,BTC作为抗通胀资产吸引力倍增^170。

结论:超级周期的完美风暴

技术面VSH代表的密码学进步保障了比特币的安全可信,而供需失衡(稀缺性+机构入场)则点燃了价格引擎。当链上流动性危机(仅460万枚可交易BTC)遇上ETF的百亿级需求^35,15万美金并非终点——渣打银行甚至看涨至25万美金^164。此刻的每次回调,都是历史级机会的入场券。

综合术数推演与市场分析:2025年6月9日-20日A股热点前瞻

一、术数框架与市场周期定位

根据《皇极经世》值年卦象,2025年(乙巳年)对应「雷火丰」卦,卦象为「离下震上」,象征光明与行动力的共振,主创新突破与技术迭代。结合纳甲筮法,6月9日(甲戌日)至20日(乙酉日)的旬卦为「水火既济」,此卦象提示市场将呈现阶段性平衡,但需警惕「初吉终乱」的波动风险。具体到板块,离火主科技、能源与文化产业,坎水主流动性及政策驱动领域,需重点关注以下方向:

二、热点题材与股票前瞻

1. AI算力与鸿蒙生态(离火之象)

驱动逻辑:卦象「离为火」对应技术创新与生态扩张,6月华为开发者大会(HDC·2025)将发布HarmonyOS新版本,叠加全球AI技术会议催化

细分方向:

算力基建:国产算力芯片(寒武纪、海光信息)、光模块(中际旭创、新易盛);

鸿蒙生态:软通动力(鸿蒙核心服务商)、润和软件(开源鸿蒙代码贡献第一);

AI应用场景:科大讯飞(教育+医疗AI)、金山办公(AI办公软件)。

风险提示:短期估值偏高(RSI超买),关注6月17日美联储议息会议对科技股流动性的扰动

2. 低空经济与商业航天(震雷之动)

驱动逻辑:卦象「震为雷」主政策突破与产业奇点,政策首次将商业航天列为未来产业,蓝箭航天技术突破降低成本30%

核心标的:

整机制造:中航沈飞(低空飞行器)、航天宏图(卫星应用);

基础设施:四川九州(北斗导航)、中国卫通(卫星通信);

材料与设备:铂力特(航天3D打印)、光启技术(超材料天线)。

催化事件:6月12日SpaceX星舰试射或带动板块情绪

3. 生物制造与创新药(巽风之渐)

驱动逻辑:卦象「巽为风」主政策扶持与产业渗透,发改委加速AI+生物制造融合,ASCO年会发布临床数据提振创新药

重点领域:

合成生物学:凯赛生物(生物基聚酰胺)、华恒生物(酶制剂);

创新药械:荣昌生物(ADC疗法)、万泰生物(九价HPV疫苗获批);

消费医疗:爱美客(医美器械)、华东医药(GLP-1类药物)。

资金动向:北向资金连续增持药明康德、泰格医药

4. 高股息与避险资产(艮山之稳)

驱动逻辑:卦象「艮为山」主防御与价值重估,美联储降息预期反复下,煤炭、电力等现金流稳定板块受捧

核心标的:

煤炭:中国神华(股息率7.2%)、陕西煤业(产能弹性);

电力:长江电力(水电龙头)、国投电力(绿电转型);

贵金属:山东黄金(金价突破2400美元)、银泰黄金(矿产储备丰富)。

风险提示:若6月经济数据超预期复苏,资金或切换至成长股

5. 消费复苏与618电商(兑泽之悦)

驱动逻辑:卦象「兑为泽」主情绪消费与社交传播,618促销数据超预期驱动「质价比」品类增长

细分机会:

智能家居:科沃斯(扫地机器人)、极米科技(投影仪);

国货美妆:珀莱雅(抖音渠道占比30%)、华熙生物(合成生物原料);

即时零售:顺丰同城(物流配送)、良品铺子(零食集合店)。

数据跟踪:关注6月18日全网GMV增速及细分品类榜单

三、风险警示与时空节点

6月12日(癸未日):美国CPI数据公布,若通胀超预期或打压降息预期,利空科技成长股

6月17日(戊子日):美联储议息会议,警惕「水火既济」卦象中「终乱」的流动性冲击

板块轮动策略:建议配置比例——科技成长(40%)+消费复苏(30%)+高股息(30%),短期关注「鸿蒙+低空经济」事件催化

象法解卦:

从「雷火丰」到「水火既济」,市场需经历「火炼真金」的结构性分化。离火主攻、坎水主守,建议以科技创新为矛,以高股息为盾,顺应政策与产业共振之势。