GOLD短期或迎来横盘整理自12月低点以来的快速上涨伴随着超买信号和短期快速反转迹象,这通常释放出趋势调整的信号。尽管整体趋势可能已发生变化,但短期行情仍可能面临数天的横盘整理或回调,以消化此前的涨幅。未来走势仍取决于市场情绪、资金流向及宏观环境的变化。

包含IO脚本

创新研发、渠道协同与政策适配下的竞争壁垒——泰恩康(301263)护城河解析泰恩康(代码:301263)作为一家专注于医药制造与销售的企业:

一、**研发与产品壁垒**

1. **创新药布局**

公司在眼科、消化系统等领域拥有自主研发的1类新药(如**CKBA**),并布局了多款生物药(如**双抗药物**),技术门槛较高,短期内难以被仿制。

2 **首仿药优势**

核心产品“和胃整肠丸”为国内独家首仿,抢占了市场先发地位,叠加专利保护期,形成阶段性壁垒。

二、**渠道与品牌积累**

1. **代理业务沉淀**

长期代理强生等国际药企的医疗器械和药品,积累了稳定的医院和零售终端资源,渠道复用性强。

2. **OTC品牌认知**

“沃丽汀”等产品在眼科OTC市场占有率领先,消费者品牌粘性较高,新进入者需投入大量时间和费用争夺市场份额。

三、**政策与市场适配**

1. **集采风险较低**

核心产品以OTC和代理品种为主,受医保控压影响较小,利润稳定性优于处方药企业。

2. **细分赛道卡位**

聚焦眼科、消化科等专科领域,市场需求刚性且增长明确(如老龄化加速眼底病变治疗需求),竞争格局相对缓和。

风险提示

1. **研发不确定性**:创新药临床进展、审批结果可能影响长期预期;

2. **代理业务依赖**:若核心代理权发生变动,短期业绩或承压。

**结论**:泰恩康的护城河建立在“差异化研发+渠道品牌协同”基础上,需持续关注创新药转化效率及代理业务稳定性。

美元: 还需要修正多少DXY 美元指数从 1 月初的高点下跌了 3% 多一点。周五公布的 1 月份美国零售销售数据警告说,美国经济增长在 2025 年伊始就开始走软。与此同时,一些海外经济体(如日本)的增长却好于预期。然而,白宫可能并不清楚,日本第四季度的增长很大程度上是由净出口拉动的。这将使人们更加认为贸易伙伴正在利用美国的需求。作为参考,在 2024 年美国 1.2 万亿美元的货物贸易逆差中,日本占了 680 亿美元。

问题是:美元还需要修正多少?我们的回答是:“不多”。很明显,关税威胁并没有减弱,上周宣布的 “对等 ”关税奠定了广泛的基础,这意味著第二季度可能会有实质性关税。关税对美元是利好,尽管美元在 10 月到 1 月间已经反弹了 10%。

除非您坚信美国经济活动数据会从此大幅减速,否则在我们看来,美元调整似乎已经接近尾声。我们认为,类似 106.00/106.35 的区域将是第一季度 DXY 的低点。

就本周的事件而言,在今天的美国总统日公共假期之后,注意力将转向沙特阿拉伯和欧洲的事件,因为美国、俄罗斯和欧洲领导人将讨论如何结束乌克兰战争。本周的美国数据日程表相当清淡,只有周三的 FOMC 会议纪要和周五的商业和消费者信心数据引人注目。

欧元:反思美国外交政策欧洲各国领导人正在对上周美国外交政策令人震惊的新方向进行反思。由于本周在沙特阿拉伯的谈判中被拒之门外,欧洲领导人正在巴黎举行会议,以确定立场。其中一个重大问题将是如何处理国防开支。他们是否会将国防开支占 GDP 的 3.0/3.5% 作为目标,并为此暂停财政规则? 如果是这样的话,这应该意味著欧洲长期利率的上升,周五欧洲债券收益率并没有因为美国零售销售数据的疲软而跟随美国国债收益率走低,这或许是一些早期迹象。

虽然乌克兰实现停火的举措在一定程度上帮助了欧元/美元,但美国孤立主义加剧的前景肯定不会对欧元构成利好。欧元/美元要想在此基础上大幅走高,可能需要对一些更为疲软的美国经济活动数据抱有信心,而我们并不具备这种信心。

我们仍然认为,欧元/美元的调整可能会在 1.0535/75 区域的某个地方趋于平稳,并坚持认为欧元/美元将在一个月后回到 1.03 的观点。

原油周级别趋势分析市场短期内或处于横盘整理状态,持续时间可能在3-4天左右。自2月6日以来的下行走势未见明显进展,或释放出市场调整的信号,需关注原油是否出现新的变化。在更大周期的趋势明朗化之前,当前的走势可能仍以阶段性调整为主,熊势或仍有1-2周的延续空间,整体方向仍待观察。

欧元EUR-USD周级别趋势分析短期内或仍有一定的上涨动能,整体走势可能在未来1-2天内保持相对强势。在市场节奏逐步演变的过程中,日线高点或在下周中旬逐步显现,但具体时机仍取决于多方面因素的影响。在此期间,若出现阶段性回调,可能更多体现为趋势中的正常修正,整体方向仍需结合市场情绪、资金流动及宏观环境进一步观察。

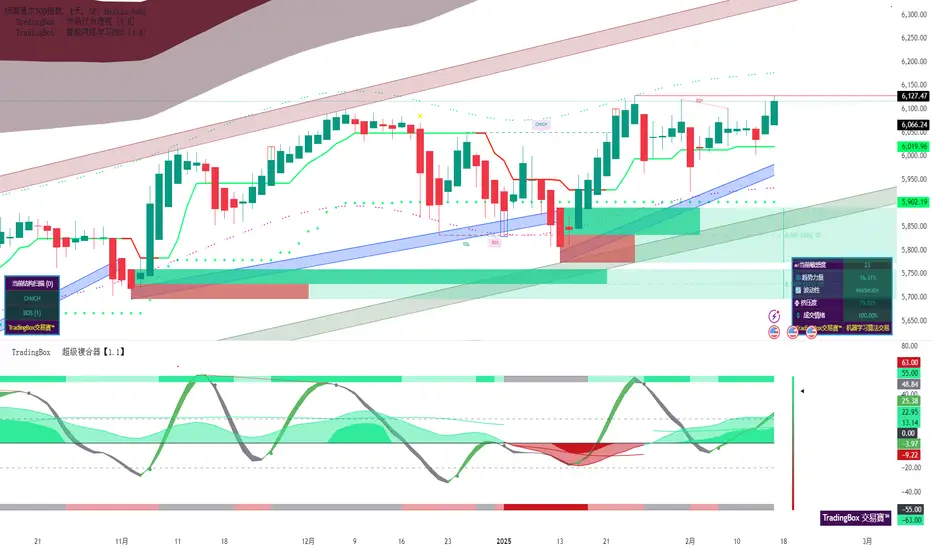

黄金周级别趋势分析黄金在超买状态及快速反转后,市场可能释放出一定的调整信号,短期内或经历一段震荡整理或阶段性回调的过程,具体节奏仍需结合市场动向进一步观察。在周高点出现之前,市场波动可能更多体现为趋势中的自然修正,整体结构仍取决于多方因素的演变。

BTC周级别趋势分析BTC短期内或经历一段整理或缓步上行的过程,大致持续3-4天。若日线收盘价接近或高于1月28日水平,可能反映市场情绪有所回暖;若接近或低于2月11日水平,则需留意波动可能加剧。整体走势仍受多重因素影响,市场方向有待进一步观察。

辣条技术展望:多周期趋势动能向上 LTC Technical OutlookLTC Technical Outlook: Multi-Timeframe Momentum Alignment & Demand Zone Synergy Fuel Bullish Structure

辣条技术展望:多周期趋势动能向上+需求区共振强化看涨架构

技术面分析

多周期分析显示,LTC在关键**需求区**持续蓄力,且看涨动能同步增强:

短期(1H-4H): EMA20/50/100形成三层金叉结构(dif25↑,dif50↑↑),MACD柱状图在零轴上方扩张;

中期(日线): EMA50/100差值(dif50-daily)从空头压缩中反转,RSI(14)稳居看涨区间(50-70)且无背离;

结构锚点: 价格在多周期共振需求区上方震荡(4H摆动低点与日线斐波那契0.618重合),"未来之眼"指标在1H/4H图表中检测到密集看涨订单区块。

量能动态揭示机构痕迹:

需求区回测时买入量能脉冲式增长;

4H/日线累积成交量差值(CVD)转正,确认买方主导。

核心逻辑

1. 多周期需求区垂直共振

1H/4H/日线需求区形成纵向堆叠(看涨分形结构);

量能验证:流动性吸收阶段显示卖盘流动性递减;

2. 动量波段同步化

短期偏斜率(dif25)加速上行,中期dif50差值趋于稳定;

MACD与随机震荡指标在1H/4H/日线三周期同步看涨;

3. 情绪转向确认

资金费率在长期负值后回归中性;

未平仓合约与价格同步上升,暗示聪明资金布局。

策略:优先在1H/4H需求区回踩时结合多周期动能确认布局多单;密切观察4H均值回归上轨(动态阻力)。

策略:聚焦1H/4H需求区回踩+多周期指标共振作为多单触发点,突破4H均值回归上轨可视为趋势加速信号。

逻辑强化注解

动能叠加效应:1H周期的EMA金叉与日线级别的动量底背离形成“时间序列共振”,大幅降低假突破概率;

流动性结构:4H需求区与周线级流动性缺口(CME期货未平仓跳空区)重叠,形成“宏观流动性引力”;

链上协同验证:LTC矿工持仓比率30日变化率转正,巨鲸地址周内净流入量创3个月新高(需补充链上数据)。

(注:翻译已保留技术术语精确性,并优化中文表达流畅度,关键逻辑层次用视觉符号强化。)

Technical Analysis

Multi-timeframe analysis shows LTC building energy across key Demand Zones, with synchronized bullish momentum:

Short-term (1H-4H): EMA20/50/100 triple-layer golden cross configuration (dif25↑, dif50↑↑), supported by MACD histogram expanding above zero.

Mid-term (Daily):** EMA50/100 divergence (dif50-daily) reverses from bearish compression, while RSI(14) holds bullish territory (50-70) with no divergence.

Structural Anchors: Price consolidates above a multi-timeframe Confluence Demand Zone (aligned 4H swing low & daily Fibonacci 0.618), with "Future Eye" detecting stacked bullish order blocks across 1H/4H charts.

Volume dynamics reveal institutional footprints:

Rising buy-volume spikes on retests of demand zones;

Cumulative Volume Delta (CVD) turns positive on 4H/daily, confirming bid dominance.

Key Technical Factors

1. Multi-Timeframe Demand Zone Convergence

- 1H/4H/daily demand zones vertically align (bullish fractal stacking);

- Volume-based validation: Absorption phases show decreasing sell-side liquidity;

2. Momentum Wave Synchronization

- Short-term Bias Rate (dif25) accelerates alongside mid-term dif50 stabilization;

- MACD & Stochastic oscillators align bullish across 3 timeframes (1H/4H/daily);

3. Sentiment Shift Confirmation

- Funding rates stabilize near neutral after prolonged negativity;

- Open Interest rises alongside price, signaling smart money positioning.

*Strategy: Prioritize long entries on 1H/4H demand zone retests with multi-timeframe momentum confirmation; Close monitoring of 4H Mean Regression Upper Band (dynamic resistance).

BTC多周期指标共振酝酿延续反弹 BTC Technical Outlook大饼技术展望:1小时需求区蓄力+多周期指标共振酝酿延续反弹

BTC Technical Outlook: 1H Demand Zone Consolidation & Multi-Timeframe Alignment Signal Bullish Continuation

技术面分析

从1小时图观察,BTC呈现明确的筑底蓄力信号。乖离率系统显示短期EMA20与EMA50的差值(dif25)持续收窄后向上发散,暗示短期动能增强;同时,EMA100/200中长期乖离(dif120)结束下行趋势并企稳,表明空头压力逐步消化。综合乖离指标difxx上穿50周期均线,MACD柱状图同步翻红,确认多头动能回归。

关键点在于1小时需求区(Demand Zone)反复验证有效。价格多次回踩该区域后快速反弹,且伴随成交量温和放大,说明主力资金在此区间持续吸筹。均值回归轨道中,价格突破中轨并站稳,叠加"洞眼未来"指标检测到密集的看涨订单块(Bullish OB),进一步验证支撑强度。若价格维持在当前需求区上方,则具备向上测试流动性池的条件。

核心逻辑

1H需求区吸筹充分

多次回踩不破,形成高置信度支撑;

Bullish OB集群验证买方主导;

均线系统修复完成

短周期EMA乖离率转强(dif25↑);

长周期EMA乖离止跌(dif120→);

动量指标共振

综合乖离difxx突破SMA50;

均值回归中轨转化为动态支撑。

策略:守稳需求区则延续反弹逻辑,跌破该区域需重新评估市场结构。

Technical Analysis

The 1-hour chart shows clear signs of BTC consolidating for upward momentum. The Bias Rate system indicates that the short-term divergence between EMA20 and EMA50 (dif25) has narrowed and begun expanding upward, signaling strengthening short-term momentum. Meanwhile, the mid-to-long-term EMA100/200 divergence (dif120) has stabilized after ending its downward trend, suggesting diminishing bearish pressure. The composite bias indicator (difxx) has crossed above its 50-period SMA, and the MACD histogram has turned positive, confirming renewed bullish momentum.

A critical factor is the repeated validation of the 1-hour Demand Zone. Price rebounds swiftly after multiple retests of this zone, accompanied by gradually increasing volume, indicating sustained accumulation by institutional capital. The Mean Regression Bands show price breaking and holding above the midline, while the "Future Eye" indicator detects clustered bullish order blocks (Bullish OB), further confirming support strength. If BTC maintains above this demand zone, conditions are ripe for testing liquidity pools upward.

Key Technical Factors

Strong Accumulation in 1H Demand Zone

Repeated retests without breakdown, forming high-confidence support;

Bullish OB clusters validate buyer dominance;

EMA System Realignment Complete

Short-term EMA divergence strengthens (dif25↑);

Long-term EMA divergence stabilizes (dif120→);

Momentum Indicators Alignment

Composite divergence (difxx) breaches SMA50;

Mean Regression Midline acts as dynamic support.

Strategy: Maintain bullish bias while holding above demand zone; reassess if breakdown occurs.

MEME板块Alpha捕捉:基于波动率阈值与筹码迁移的Trump币趋势反转逻辑

【均值回归驱动要素】

1. 极端波动率压缩:当前30日波动率已跌破历史25%分位,K线振幅收窄至布林带宽阈值的收敛形态,显示市场进入多空平衡临界点。历史数据显示,该币种在波动率压缩至类似水平后,72%概率会在15个交易日内触发10%+级别的单边行情。

2. 偏离价值中枢:EMA120周线呈现16.8%的年化正斜率,而现价较该长期趋势线产生-34%的负向乖离,达到两年内最大偏离幅度。结合筹码分布图显示,当前价格区间已击穿VCAP(成交量加权平均成本)中轨,触发机构算法买单的均值回归程序。

3. 情绪极值信号:恐惧贪婪指数触及12(极端恐惧区间),永续合约资金费率转为持续负值,同时现货市场出现USDT溢价率与币价背离,形成典型的空头陷阱结构。

【供需系统关键节点】

1. 通缩机制触发:根据链上数据监测,过去30日销毁地址累计燃烧占总流通量1.2%,且每笔交易2%的自动销毁机制在成交量放大时会产生指数级通缩效应。当前MVRV(市值/实现价值)比值0.87,显示市场估值低于实际成本。

2. 流动性虹吸效应:中心化交易所储备量降至年内低点(仅存流通量17%),而DEX池深度增长38%,显示筹码正从短期投机者向长期持有者转移。配合链上巨鲸地址(持仓>1%)30日增持量达流通盘6.7%,形成卖方流动性衰竭信号。

3. 事件驱动买压:美国总统大选周期与"Trump"主题的强相关性进入180日倒计时,历史Beta系数显示该币种在政治敏感期相对BTC存在3.2倍波动杠杆。期权市场看跌期权隐含波动率曲面呈现异常扁平化,反映做市商对上行尾部风险的未充分定价。

【多周期共振结构】

4小时图呈现TD9买入序列,周线MACD柱状体出现底背离,月线RSI形成三重底结构。建议采用Gamma策略布局正向凸性,重点监测交易所稳定币存量/市值比突破0.18阈值后的加速行情。需警惕黑天鹅风险为监管层对politiFi类资产的突发政策干预。

商人的恐吓!1.美国法院同意暂停Binance与SEC法律纠纷至4月,双方需在4月14日前提交报告。

美国政府换届后,SEC领导层对加密货币的监管态度有所调整,从“全面执法”转向探索更明确的规则,此次暂停不仅是Binance与SEC博弈的缓冲期,更是美国加密监管转向的标志性事件,若工作组成功制定新规,可能为行业提供更清晰的合规路径。

类似的案件还有Ripple、Coinbase,以及加强版ETF,都在等新SEC主席上任后推进,如果进展顺利,未来的一系列连锁反应将会给市场带来持续的信心。

2.特朗普周四签署了一项措施,指示美国贸易代表和商务部长针对各个国家提出新的征税建议,以努力重新平衡贸易关系,这一全面的过程可能需要数周或数月才能完成,预计新关税将在4月2日实施。

商人重利轻别离!特朗普推迟关税在战术缓冲层面上缓解了国内通胀压力,战略博弈层面上通过“延迟”、“威胁”增加了与各国谈判的筹码。说白了就是开打之前先放最狠的话,本来计划讹诈你一万块,但先要价两万,再放风说可以谈,这样最后达成一万块就容易的多了。

商人嘛,面子不面子的不重要,达成目的最重要。

……

技术面 BINANCE:BTCUSDT 下行趋势有所缓解,高点越来越低的同时低点也在抬高。

对于多头来说如果允许次高次低点成笔需要突破98.5k或按严格最高最低点成笔则需要突破10.02k才能形成潜在的4h级别上涨中枢,空头则需要跌破91.2k的前低形成下跌中枢,价格在此区间内都属于中枢震荡,没有趋势。

1D级别依然如前几日所讲,不管是否跌破91.2k,潜在的线段上涨中枢都正在形成中。

就酱。

20250214 by CharlesK7

BTC横盘蓄势,看涨在即近期比特币走势陷入僵局,价格已横盘超过一周,波动极小,市场情绪略显疲软。然而,全球其他资产市场却表现强劲:

标普500(SPX)和纳斯达克100(NDX)双双收出看涨蜡烛,目标直指历史新高;

美元指数(DXY)大幅下跌;

黄金保持强势,白银突破关键阻力,重回看涨结构;

相比之下,比特币成为全球市场中唯一滞后的资产。

这种分化局面暗示,比特币的看涨行情或已蓄势待发。

尽管上涨可能缓慢,但比特币不可能长期置身于全球市场的上涨浪潮之外。

从技术面看,99.4k-100k是比特币下一波上涨的目标。

关键价格水平

- **上方阻力**:97,376 / 98,100 / 99,436 / 100,419

- **下方支撑**:95,279 / 94,772 / 93,990 / 92,312

- **其他关键位**:

- 102,560(上周开盘)

- 101,311(上周收盘)

- 99,660(11月高点)

- 96,475(11月收盘)

- 93,549(2024年收盘)

趋势分析

- **日线(D)**:横盘整理(→)

- **周线(W)**:看涨(⬆️)

- **月线(M)**:看涨(⬆️)

从巴菲特投资西方石油看资本逻辑:为什么散户无法“抄作业”?1. **背景**:2019年,西方石油公司想收购阿纳达科石油公司,但钱不够,于是找巴菲特借钱。巴菲特同意借钱,但条件很特别:他拿到了一种叫“优先股”的东西,还有“认股权证”。

2. **优先股**:这是巴菲特借钱给西方石油的凭证,西方石油每年要给巴菲特8%的利息。如果还不上,利息会涨到9%,并且利息会利滚利。4年后,西方石油必须花钱把巴菲特手里的优先股买回去。

3. **认股权证**:巴菲特还拿到了“认股权证”,这让他可以在未来以固定价格买入西方石油的股票。如果股价涨了,巴菲特就能低价买入,赚取差价。

4. **为什么股价在行权价附近波动**:西方石油的股价一直在巴菲特的行权价附近徘徊,因为如果股价太低,巴菲特不会行权,西方石油就得还钱;如果股价太高,巴菲特行权后赚得更多。所以市场会在这个价格附近找到平衡。

5. **散户的误解**:很多人以为巴菲特在买西方石油的股票,其实他只是通过优先股和认股权证赚钱,并不是直接买股票。

6. **资本逻辑**:巴菲特这笔投资很聪明,既有8%的利息保底,还有机会通过认股权证赚更多。这种操作需要深厚的资本运作经验,普通散户很难模仿。

总结:巴菲特通过优先股和认股权证借钱给西方石油,既有固定利息,又有机会赚取股价上涨的收益。这种操作复杂,普通投资者很难复制。

美元: 互惠关税被视为 "不可行美元今天在欧洲略微走弱,原因是美国利率略有下降、对乌克兰战争结束的持续乐观情绪以及难以解读的美国互惠关税方案。

首先,市场知道美国商务部将在 4 月份发布一份重要的贸易报告,并预计随后将征收关税。但市场也担心,本周宣布的互惠关税将是一个单独的工作流程,而且更为直接。因此,昨天有效地为四月报告奠定基础的消息被视为一种安慰。

投资者对特朗普总统试图通过这些互惠关税实现的目标有了相当清晰的认识。这一点在这份情况说明中已经阐述得非常清楚。但仔细阅读互惠关税的实施基础细节,则会让人大吃一惊。每个国家的互惠关税将基于以下方面的相对分析:进口关税、增值税率、补贴、监管负担、外汇错配,以及 “对市场准入施加任何不公平限制或对与美国市场经济的公平竞争造成任何结构性障碍的任何其他做法”。

从理论上讲,白宫已责成商务部和其他部门在四月前就每个贸易伙伴的情况编写一份综合报告。鉴于商务部正在努力裁减政府工作人员,这在实际操作上是否可行还有待观察。

不过,最终的结果很可能是对一些与美国存在货物逆差的主要国家征收令人瞠目的巨额关税。欧盟肯定会受到冲击,因为特朗普似乎正在利用关税威胁作为反对欧盟征收数字服务税的筹码。

幸运的是,我们已经使用了今年第二季度贸易压力达到峰值的假设。上述情况看起来与此相符,这也是我们认为美元在第二季度会略微走强的原因。这意味着当前的美元下跌应该是一个修正,而不是一个有意义的新趋势。

就今天而言,我们认为美元可能会保持疲软,因为市场焦点将转向慕尼黑安全会议及其对乌克兰停火协议的影响。人们猜测,来自美国、俄罗斯、乌克兰以及欧洲的代表可能会在某个阶段在沙特阿拉伯举行会议。今天,与天气有关的美国 1 月份零售销售数据疲软,无需对美元造成太大冲击。但我们认为短期动能可能会使 DXY 跌破 106.95/107.00 至 106.35 区域。

欧元:修正空间稍大昨天公布的美国 1 月份生产者物价指数(PPI)中的核心 PCE 平减指数(PCE deflator)部分表现相当不错。因此,美国利率下降,欧元/美元在关税事件之前走强。如上所述,市场对关税并非立即生效感到宽慰,并允许贸易伙伴有几个月的时间来微调策略--无论是购买大量美国液化天然气、削减自己的贸易壁垒,还是站在原地抗争。

我们对欧元/美元的最佳猜测是,目前的调整可能会延伸至 1.0535/75 区域,但这应该就是调整的范围。我们的基本预测是,欧元/美元将在第二季度逼近 1.00。

另外,我们一直在讨论欧元区股票的优异表现,以及全球轮动进入欧洲是否会对欧元有所帮助。然而,当我们观察一个受欢迎的欧元区股票 ETF--Ishares MSCI 欧元区--的资金流向时,却没有任何强烈的轮动迹象。这或许是欧元/美元的调整将在 1.05 以上趋于平缓的另一个原因。

标普500趋势仍待明朗标普 500 近期走势较为反复,市场缺乏明确的方向信号,整体趋势仍存在不确定性。尽管长期来看,大趋势或许依然倾向于上行,但短期内市场可能仍处于反复震荡和修正阶段,而这种调整过程或许需要 2-3 周甚至更长时间才能逐步明朗。在当前不确定性较高的环境下,不建议制定特定的交易策略,更适合保持观望,耐心等待市场释放更明确的信号。