PROTECTED SOURCE SCRIPT

Cross-Asset Risk Appetite Index

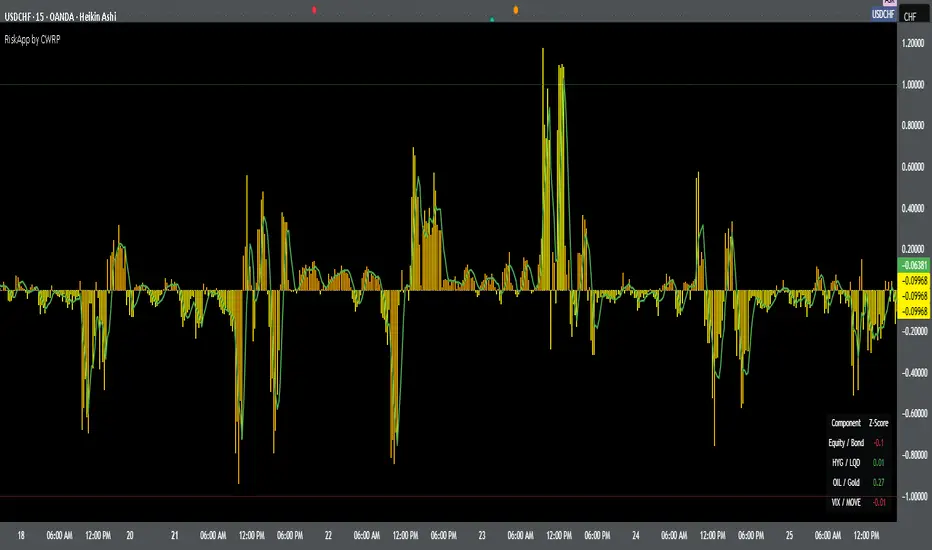

Cross-Asset Risk Appetite Index (RiskApp) by CWRP combines multiple asset classes into a single risk sentiment signal to help traders and investors detect when the market is in a risk-on or risk-off regime.

It calculates a composite Z-score index based on relative performance between:

SPY / IEF: Equities vs Bonds

HYG / LQD: High Yield vs Investment Grade Credit

CL / GC: Oil vs Gold

VIX / MOVE: Equity vs Bond Market Volatility (inverted)

Each component reflects capital flows toward riskier or safer assets, with dynamic weighting (Equity/Bond: 30%, Credit: 25%, Commodities: 25%, Volatility: 20%) and smoothing applied for a cleaner signal.

How to Read:

Highlighting

Yellow = Risk-On sentiment (market favors risk assets)

Orange = Risk-Off sentiment (flight to safety)

Black Background = Neutral design for emotional detachment

Table

Equity/Bond Z-Score:

Positive (> +1) --> Stocks outperforming bonds --> Risk-On

Negative (< -1) --> Bonds outperforming stocks --> Risk-Off

Credit Spread Z-Score (HYG/LQD):

Positive --> High yield outperforming --> Investors seeking yield

Negative --> Flight to quality --> Credit concerns

Oil/Gold Z-Score:

Positive --> Oil outperforming --> Economic optimism

Negative --> Gold outperforming --> Defensive positioning

Volatility Spread (VIX/MOVE):

Positive --> Equity vol falling relative to bond vol --> Risk stabilizing

Negative --> Equity vol rising --> Caution / Risk-Off

Composite Index:

> +1 --> Strong Risk Appetite

< -1 --> Strong Risk Aversion

Between -1 and +1 --> Neutral regime

Thank you for using the Cross-Asset Risk Appetite Index by CWRP!

I'm open to all critiques and discussion around macro-finance and hope this model adds clarity to your decision-making.

It calculates a composite Z-score index based on relative performance between:

SPY / IEF: Equities vs Bonds

HYG / LQD: High Yield vs Investment Grade Credit

CL / GC: Oil vs Gold

VIX / MOVE: Equity vs Bond Market Volatility (inverted)

Each component reflects capital flows toward riskier or safer assets, with dynamic weighting (Equity/Bond: 30%, Credit: 25%, Commodities: 25%, Volatility: 20%) and smoothing applied for a cleaner signal.

How to Read:

Highlighting

Yellow = Risk-On sentiment (market favors risk assets)

Orange = Risk-Off sentiment (flight to safety)

Black Background = Neutral design for emotional detachment

Table

Equity/Bond Z-Score:

Positive (> +1) --> Stocks outperforming bonds --> Risk-On

Negative (< -1) --> Bonds outperforming stocks --> Risk-Off

Credit Spread Z-Score (HYG/LQD):

Positive --> High yield outperforming --> Investors seeking yield

Negative --> Flight to quality --> Credit concerns

Oil/Gold Z-Score:

Positive --> Oil outperforming --> Economic optimism

Negative --> Gold outperforming --> Defensive positioning

Volatility Spread (VIX/MOVE):

Positive --> Equity vol falling relative to bond vol --> Risk stabilizing

Negative --> Equity vol rising --> Caution / Risk-Off

Composite Index:

> +1 --> Strong Risk Appetite

< -1 --> Strong Risk Aversion

Between -1 and +1 --> Neutral regime

Thank you for using the Cross-Asset Risk Appetite Index by CWRP!

I'm open to all critiques and discussion around macro-finance and hope this model adds clarity to your decision-making.

受保护脚本

此脚本以闭源形式发布。 但是,您可以自由使用,没有任何限制 — 了解更多信息这里。

免责声明

这些信息和出版物并非旨在提供,也不构成TradingView提供或认可的任何形式的财务、投资、交易或其他类型的建议或推荐。请阅读使用条款了解更多信息。

免责声明

这些信息和出版物并非旨在提供,也不构成TradingView提供或认可的任何形式的财务、投资、交易或其他类型的建议或推荐。请阅读使用条款了解更多信息。