OPEN-SOURCE SCRIPT

已更新 Normalized True Range - Grouped by Weekdays

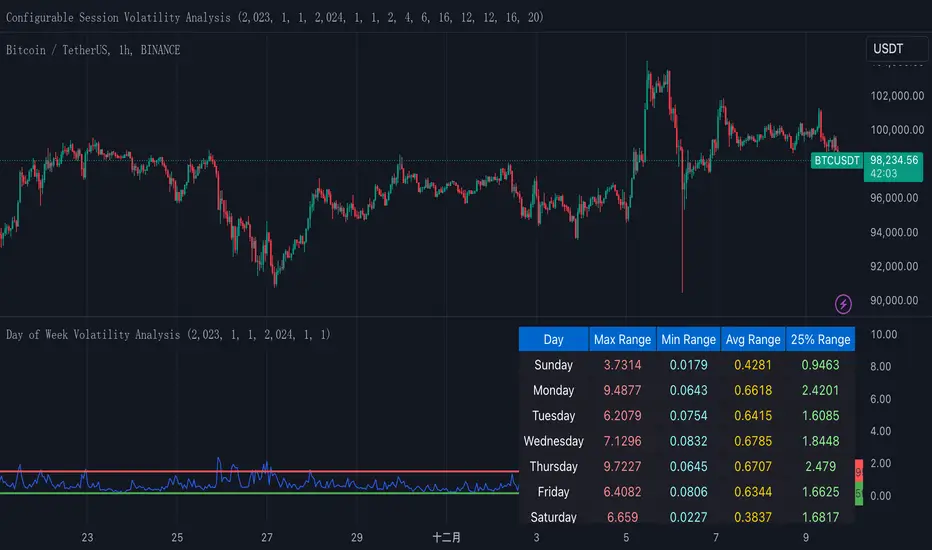

This indicator helps traders analyze daily volatility patterns across different days of the week by calculating normalized price ranges.

These bounds appear as horizontal lines on the chart, making it easy to spot when current volatility breaks out of its historical norms.

These bounds appear as horizontal lines on the chart, making it easy to spot when current volatility breaks out of its historical norms.

版本注释

This indicator helps traders analyze daily volatility patterns across different days of the week by calculating normalized price ranges.Unlike traditional volatility measures, it uses a normalized approach by dividing the daily range (high-low) by the midpoint price and multiplying by 100, providing a percentage-based measure that's comparable across different price levels. This normalization makes it particularly useful for comparing volatility patterns across different assets or time periods.

The indicator also includes a statistical overlay that highlights extreme volatility events. By calculating the 5th and 95th percentiles of the normalized ranges within your specified date range, it creates upper and lower bounds that help identify outlier days where volatility was exceptionally high or low.

These bounds appear as horizontal lines on the chart, making it easy to spot when current volatility breaks out of its historical norms.

The data is presented in both visual and tabular formats, with a comprehensive table showing the maximum, minimum, average, and 25th percentile ranges for each day of the week. This dual presentation allows traders to both quickly spot patterns visually and access detailed statistics for deeper analysis.

The user can customize the analysis period through simple date range inputs, making it flexible for different analytical timeframes.

开源脚本

秉承TradingView的精神,该脚本的作者将其开源,以便交易者可以查看和验证其功能。向作者致敬!您可以免费使用该脚本,但请记住,重新发布代码须遵守我们的网站规则。

免责声明

这些信息和出版物并非旨在提供,也不构成TradingView提供或认可的任何形式的财务、投资、交易或其他类型的建议或推荐。请阅读使用条款了解更多信息。

免责声明

这些信息和出版物并非旨在提供,也不构成TradingView提供或认可的任何形式的财务、投资、交易或其他类型的建议或推荐。请阅读使用条款了解更多信息。