OPEN-SOURCE SCRIPT

已更新 Adaptive Signal Oscillator (ASO)

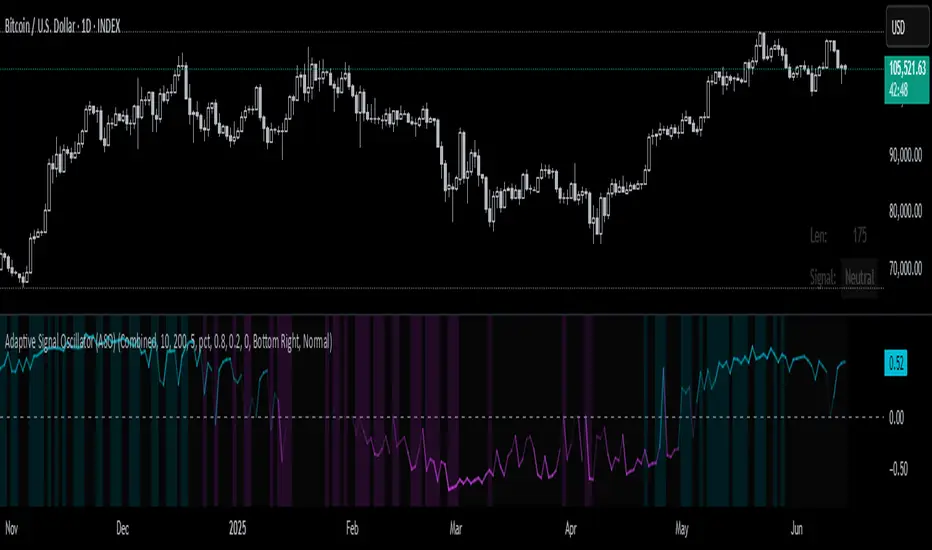

📘 Adaptive Signal Oscillator (ASO)

A fully dynamic, self-calibrating oscillator that adapts to any asset or timeframe by optimizing for real-time signal stability and volatility structure — without relying on static parameters or hardcoded thresholds.

🔍 Overview

The Adaptive Signal Oscillator (ASO) is a next-generation technical analysis tool designed to provide context-aware long/short signals across crypto, equities, or forex markets. Unlike traditional oscillators (RSI, Stochastics, MACD), ASO requires no manual tuning of lookback periods or overbought/oversold zones — it self-optimizes based on current market behavior.

🧠 How It Works

✅ 1. Dynamic Lookback Optimization

ASO evaluates a range of lookback lengths between user-defined minLen and maxLen. For each length, it calculates the standard deviation of returns and finds the one with the least volatility change (i.e., the most stable structure). This length is dynamically assigned as bestLen, recalculated on every bar.

✅ 2. Multi-Layer Signal Composition

Four independent signal layers are computed using bestLen:

RSI Layer: Measures relative price strength via a custom dynamic RSI.

Z-Score Layer: Standardized deviation of price from its mean.

Volatility Layer: Standard deviation of log or percent returns.

Price Position Layer: Current price percentile within the lookback window.

Each of these layers is transformed into a percentile score scaled to the range [-1, 1].

✅ 3. Volatility-Based Weighting

The standard deviation (volatility) of each signal layer is computed. Less volatile layers are weighted more heavily, ensuring the final composite signal prioritizes stable, consistent inputs.

Weights are normalized and combined to form a composite score, representing a dynamically blended, noise-weighted signal across the four layers.

✅ 4. Optional Adaptive Smoothing

A boolean toggle lets users apply smoothing to the final score. The smoothing window scales proportionally to bestLen, preserving adaptiveness even during trend transitions.

✅ 5. Percentile-Based Thresholding

Rather than using arbitrary fixed thresholds, ASO converts the composite score into a ranked percentile. Long/short signals are then generated based on user-defined percentile bands, adapting naturally to each asset’s behavior.

📈 Interpreting ASO

Score > Threshold → Strong long signal (highlighted in aqua).

Score < Threshold → Strong short signal (highlighted in fuchsia).

Crossing h_thresh (e.g., 0) → Neutral-to-bias change; useful for early trend cues.

The background and label update in real time to reflect the current regime and bestLen.

⚙️ Inputs

minLen, maxLen, step: Define the search range for optimal lookback length.

retMethod: Choose between log or percent return calculations.

threshHigh, threshLow: Define signal zones using percentiles.

smooth: Enable dynamic score smoothing.

h_thresh: Midline crossover zone for directional context.

⚠️ Disclaimer

This tool is designed for exploratory and educational purposes only. It does not offer financial advice or trading recommendations. Past performance is not indicative of future results.

Always consult a licensed financial advisor before making investment decisions.

A fully dynamic, self-calibrating oscillator that adapts to any asset or timeframe by optimizing for real-time signal stability and volatility structure — without relying on static parameters or hardcoded thresholds.

🔍 Overview

The Adaptive Signal Oscillator (ASO) is a next-generation technical analysis tool designed to provide context-aware long/short signals across crypto, equities, or forex markets. Unlike traditional oscillators (RSI, Stochastics, MACD), ASO requires no manual tuning of lookback periods or overbought/oversold zones — it self-optimizes based on current market behavior.

🧠 How It Works

✅ 1. Dynamic Lookback Optimization

ASO evaluates a range of lookback lengths between user-defined minLen and maxLen. For each length, it calculates the standard deviation of returns and finds the one with the least volatility change (i.e., the most stable structure). This length is dynamically assigned as bestLen, recalculated on every bar.

✅ 2. Multi-Layer Signal Composition

Four independent signal layers are computed using bestLen:

RSI Layer: Measures relative price strength via a custom dynamic RSI.

Z-Score Layer: Standardized deviation of price from its mean.

Volatility Layer: Standard deviation of log or percent returns.

Price Position Layer: Current price percentile within the lookback window.

Each of these layers is transformed into a percentile score scaled to the range [-1, 1].

✅ 3. Volatility-Based Weighting

The standard deviation (volatility) of each signal layer is computed. Less volatile layers are weighted more heavily, ensuring the final composite signal prioritizes stable, consistent inputs.

Weights are normalized and combined to form a composite score, representing a dynamically blended, noise-weighted signal across the four layers.

✅ 4. Optional Adaptive Smoothing

A boolean toggle lets users apply smoothing to the final score. The smoothing window scales proportionally to bestLen, preserving adaptiveness even during trend transitions.

✅ 5. Percentile-Based Thresholding

Rather than using arbitrary fixed thresholds, ASO converts the composite score into a ranked percentile. Long/short signals are then generated based on user-defined percentile bands, adapting naturally to each asset’s behavior.

📈 Interpreting ASO

Score > Threshold → Strong long signal (highlighted in aqua).

Score < Threshold → Strong short signal (highlighted in fuchsia).

Crossing h_thresh (e.g., 0) → Neutral-to-bias change; useful for early trend cues.

The background and label update in real time to reflect the current regime and bestLen.

⚙️ Inputs

minLen, maxLen, step: Define the search range for optimal lookback length.

retMethod: Choose between log or percent return calculations.

threshHigh, threshLow: Define signal zones using percentiles.

smooth: Enable dynamic score smoothing.

h_thresh: Midline crossover zone for directional context.

⚠️ Disclaimer

This tool is designed for exploratory and educational purposes only. It does not offer financial advice or trading recommendations. Past performance is not indicative of future results.

Always consult a licensed financial advisor before making investment decisions.

版本注释

🔄 Adaptive Signal Oscillator (ASO) – Gradient Signal UpgradeThis upgraded version of the original ASO builds on its dynamic framework by enhancing expressiveness, precision, and interpretability.

✅ Key Upgrades

📈 Gradient Signal Output (signalSharp)

The binary long/short classification has been replaced with a continuous oscillator signal ranging from -1 to +1, allowing finer insight into signal strength and sentiment momentum.

🌀 Divergence-Aware Signal Scaling

Final signal strength is now modulated by real-time divergence between the price and the oscillator. Conviction is reduced proportionally during divergence, making the signal more resilient to false positives.

📐 Non-linear Sensitivity Boost

A √x transformation sharpens midrange values. This amplifies early momentum cues and produces a more reactive yet statistically stable signal near the zero line.

🎨 Visual Gradient Enhancement

The plot uses alpha-blended color gradients, fading from neutral gray to aqua (bullish) or fuchsia (bearish), proportionally to signal strength — making visual interpretation intuitive and actionable.

📊 Dynamic Weighting & Lookback

All components (RSI, Z-score, volatility, price position) continue to be dynamically weighted based on statistical volatility and adaptively optimized over a rolling lookback for minimal lag and maximal relevance.

开源脚本

秉承TradingView的精神,该脚本的作者将其开源,以便交易者可以查看和验证其功能。向作者致敬!您可以免费使用该脚本,但请记住,重新发布代码须遵守我们的网站规则。

免责声明

这些信息和出版物并非旨在提供,也不构成TradingView提供或认可的任何形式的财务、投资、交易或其他类型的建议或推荐。请阅读使用条款了解更多信息。

免责声明

这些信息和出版物并非旨在提供,也不构成TradingView提供或认可的任何形式的财务、投资、交易或其他类型的建议或推荐。请阅读使用条款了解更多信息。