OPEN-SOURCE SCRIPT

已更新 Fractal Regression Bands [DW]

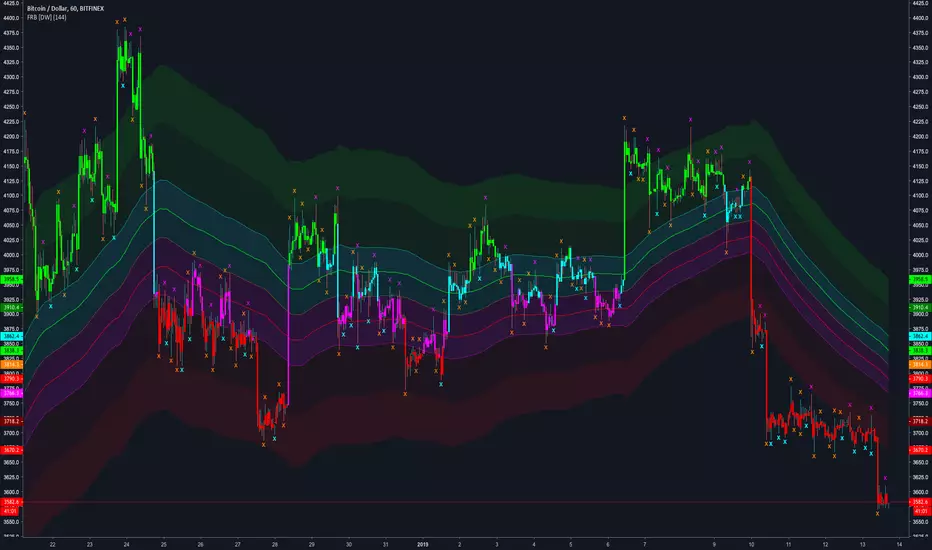

This study is an experimental regression curve built around fractal and ATR calculations.

First, Williams Fractals are calculated, and used as anchoring points.

Next, high anchor points are connected to negative sloping lines, and low anchor points to positive sloping lines. The slope is a specified percentage of the current ATR over the sampling period.

The median between the positive and negative sloping lines is then calculated, then the best fit line (linear regression) of the median is calculated to generate the basis line.

Lastly, a Golden Mean ATR is taken of price over the sampling period and multiplied by 1/2, 1, 2, and 3. The results are added and subtracted from the basis line to generate the bands.

Williams Fractals are included in the plots. The color scheme indicated whether each fractal is engulfing or non-engulfing.

Custom bar color scheme is included.

First, Williams Fractals are calculated, and used as anchoring points.

Next, high anchor points are connected to negative sloping lines, and low anchor points to positive sloping lines. The slope is a specified percentage of the current ATR over the sampling period.

The median between the positive and negative sloping lines is then calculated, then the best fit line (linear regression) of the median is calculated to generate the basis line.

Lastly, a Golden Mean ATR is taken of price over the sampling period and multiplied by 1/2, 1, 2, and 3. The results are added and subtracted from the basis line to generate the bands.

Williams Fractals are included in the plots. The color scheme indicated whether each fractal is engulfing or non-engulfing.

Custom bar color scheme is included.

版本注释

Updates:Due to inefficiencies and its arbitrary nature, the slope factor calculation has been removed from the script.

Due to the linear regression's significant amount of overshoot, especially at greater sampling lengths, the basis line is now calculated using exponential smoothing, which fits the price series much better with minimal overshoot.

Changed the size of the fractal signals.

开源脚本

秉承TradingView的精神,该脚本的作者将其开源,以便交易者可以查看和验证其功能。向作者致敬!您可以免费使用该脚本,但请记住,重新发布代码须遵守我们的网站规则。

For my full list of premium tools, check the blog:

wallanalytics.com/

Reach out on Telegram:

t.me/DonovanWall

wallanalytics.com/

Reach out on Telegram:

t.me/DonovanWall

免责声明

这些信息和出版物并非旨在提供,也不构成TradingView提供或认可的任何形式的财务、投资、交易或其他类型的建议或推荐。请阅读使用条款了解更多信息。

开源脚本

秉承TradingView的精神,该脚本的作者将其开源,以便交易者可以查看和验证其功能。向作者致敬!您可以免费使用该脚本,但请记住,重新发布代码须遵守我们的网站规则。

For my full list of premium tools, check the blog:

wallanalytics.com/

Reach out on Telegram:

t.me/DonovanWall

wallanalytics.com/

Reach out on Telegram:

t.me/DonovanWall

免责声明

这些信息和出版物并非旨在提供,也不构成TradingView提供或认可的任何形式的财务、投资、交易或其他类型的建议或推荐。请阅读使用条款了解更多信息。