OPEN-SOURCE SCRIPT

CHAN CRYPTO RS

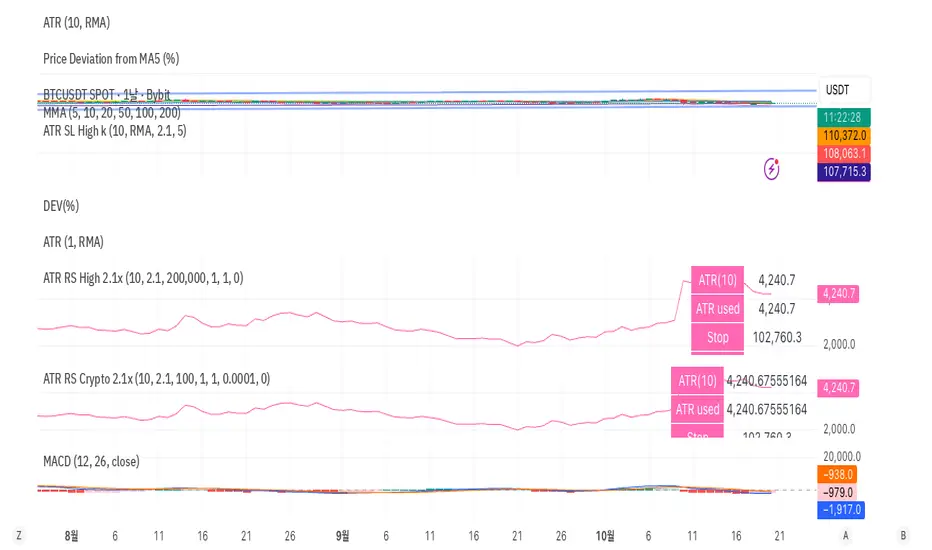

🩷 ATR RS (Crypto / High-based 2.1x, Decimal Safe v2)

This indicator is designed for crypto position sizing and stop calculation using ATR-based risk management. It helps traders automatically determine the stop price, per-unit risk, and optimal position size based on a fixed risk amount in USDT.

🔧 Core Logic

ATR Length (Daily RMA) — calculates the daily Average True Range (ATR) using RMA smoothing.

ATR Multiplier (2.1× default) — defines how far the stop is placed from the daily high.

Stop Price (for Longs) = Daily High − ATR × Multiplier

Per-Unit Risk = (Entry − Stop) × Point Value

Position Size = Risk Amount ÷ Per-Unit Risk

Automatically handles decimal precision for micro-priced crypto assets (e.g., PEPE, SHIB).

Includes safeguards for minimum size and maximum position caps.

💡 Features

Uses Daily ATR without lookahead (no repainting).

Dynamically switches between current and previous ATR for stable results when the daily bar isn’t yet confirmed.

“Snap to tick” ensures stop prices align with the symbol’s tick size.

Table display summarizes ATR, stop price, per-unit risk, total risk, size, and bet amount.

Optional stop label on the chart for visual clarity.

🧮 Output Table

Metric Description

ATR(10) Daily RMA-based ATR

ATR used Chosen ATR (current or previous)

Stop Calculated stop price

Per-unit Risk per coin/unit

Risk Total risk in USDT

Size Optimal position size

Bet Total position value (Entry × Size)

🧠 Ideal For

Crypto traders who use fixed-risk ATR strategies and need precise, decimal-safe position sizing even for ultra-low-priced tokens.

This indicator is designed for crypto position sizing and stop calculation using ATR-based risk management. It helps traders automatically determine the stop price, per-unit risk, and optimal position size based on a fixed risk amount in USDT.

🔧 Core Logic

ATR Length (Daily RMA) — calculates the daily Average True Range (ATR) using RMA smoothing.

ATR Multiplier (2.1× default) — defines how far the stop is placed from the daily high.

Stop Price (for Longs) = Daily High − ATR × Multiplier

Per-Unit Risk = (Entry − Stop) × Point Value

Position Size = Risk Amount ÷ Per-Unit Risk

Automatically handles decimal precision for micro-priced crypto assets (e.g., PEPE, SHIB).

Includes safeguards for minimum size and maximum position caps.

💡 Features

Uses Daily ATR without lookahead (no repainting).

Dynamically switches between current and previous ATR for stable results when the daily bar isn’t yet confirmed.

“Snap to tick” ensures stop prices align with the symbol’s tick size.

Table display summarizes ATR, stop price, per-unit risk, total risk, size, and bet amount.

Optional stop label on the chart for visual clarity.

🧮 Output Table

Metric Description

ATR(10) Daily RMA-based ATR

ATR used Chosen ATR (current or previous)

Stop Calculated stop price

Per-unit Risk per coin/unit

Risk Total risk in USDT

Size Optimal position size

Bet Total position value (Entry × Size)

🧠 Ideal For

Crypto traders who use fixed-risk ATR strategies and need precise, decimal-safe position sizing even for ultra-low-priced tokens.

开源脚本

秉承TradingView的精神,该脚本的作者将其开源,以便交易者可以查看和验证其功能。向作者致敬!您可以免费使用该脚本,但请记住,重新发布代码须遵守我们的网站规则。

免责声明

这些信息和出版物并非旨在提供,也不构成TradingView提供或认可的任何形式的财务、投资、交易或其他类型的建议或推荐。请阅读使用条款了解更多信息。

开源脚本

秉承TradingView的精神,该脚本的作者将其开源,以便交易者可以查看和验证其功能。向作者致敬!您可以免费使用该脚本,但请记住,重新发布代码须遵守我们的网站规则。

免责声明

这些信息和出版物并非旨在提供,也不构成TradingView提供或认可的任何形式的财务、投资、交易或其他类型的建议或推荐。请阅读使用条款了解更多信息。