OPEN-SOURCE SCRIPT

Racer Correlation [racer8]

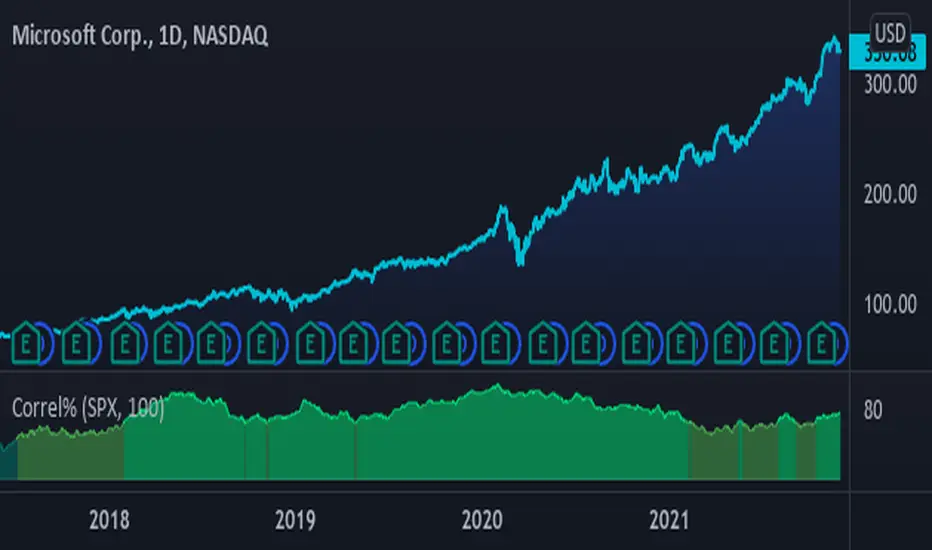

This indicator gauges correlation between 2 markets using my own method I invented. It is far superior to the correlation coefficient in that it maintains steady correlation values, meaning less false signals regarding correlation. Yet, the indicator's calculation is very simple in fact...

It simply calculates the percentage of moves in the same direction as the other market. So if MSFT moved in the same direction as SPX 80% of the time, then the indicator would show you a value of 80. Unlike correlation coefficient, you can calculate exactly how many of MSFT's bars moved in the same direction as SPX's bars. Everytime MSFT moves in the same direction as SPX, it is included in the percentage of positively correlated moves.

Closing prices are used solely in the indicator's calculations. All indicator values represent a percentage. Also, I recommend a length of at least 100 periods.

Values between 0% and 25% indicate strong negative correlation. (bright red)

Values between 25% and 33% indicate moderate negative correlation. (red)

Values between 33% and 50% indicate weak negative correlation. (dark red)

Values between 50% and 67% indicate weak positive correlation. (dark green)

Values between 67% and 75% indicate moderate positive correlation. (green)

Values between 75% and 100% indicate strong positive correlation. (bright green)........Enjoy :)

It simply calculates the percentage of moves in the same direction as the other market. So if MSFT moved in the same direction as SPX 80% of the time, then the indicator would show you a value of 80. Unlike correlation coefficient, you can calculate exactly how many of MSFT's bars moved in the same direction as SPX's bars. Everytime MSFT moves in the same direction as SPX, it is included in the percentage of positively correlated moves.

Closing prices are used solely in the indicator's calculations. All indicator values represent a percentage. Also, I recommend a length of at least 100 periods.

Values between 0% and 25% indicate strong negative correlation. (bright red)

Values between 25% and 33% indicate moderate negative correlation. (red)

Values between 33% and 50% indicate weak negative correlation. (dark red)

Values between 50% and 67% indicate weak positive correlation. (dark green)

Values between 67% and 75% indicate moderate positive correlation. (green)

Values between 75% and 100% indicate strong positive correlation. (bright green)........Enjoy :)

开源脚本

秉承TradingView的精神,该脚本的作者将其开源,以便交易者可以查看和验证其功能。向作者致敬!您可以免费使用该脚本,但请记住,重新发布代码须遵守我们的网站规则。

免责声明

这些信息和出版物并非旨在提供,也不构成TradingView提供或认可的任何形式的财务、投资、交易或其他类型的建议或推荐。请阅读使用条款了解更多信息。

免责声明

这些信息和出版物并非旨在提供,也不构成TradingView提供或认可的任何形式的财务、投资、交易或其他类型的建议或推荐。请阅读使用条款了解更多信息。