OPEN-SOURCE SCRIPT

已更新 VWAP Market Session Anchored

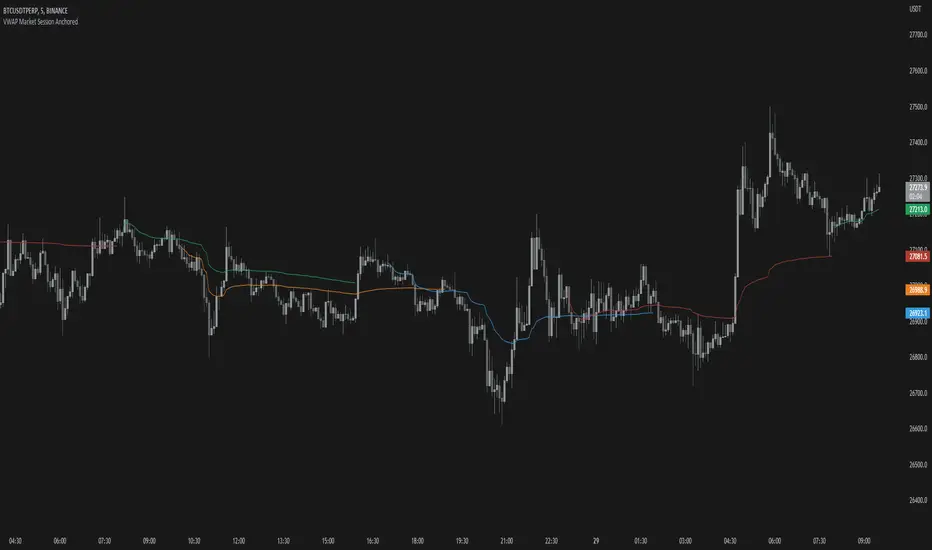

VWAP Market Session Anchored differs from the traditional VWAP or VWAP Auto Anchored indicator in that the Volume Weighted Average Price calculation is automatically anchored to four major market session starts: Sydney, London, Tokyo, New York.

Settings

Usage

Similar to the traditional VWAP, VWAP Market Session Anchored is a technical analysis tool used to measure the average price weighted by volume. VWAP Market Session Anchored can be used to identify the trend during a specific market session.

Limitations

When setting a custom session, be mindful that calculations are based off of the Coordinated Universal Time (UTC) time, you must convert your local time zone to UTC in order to have an accurate representation of your custom session.

It is not recommended to use this indicator on timeframes above 1 hour as market sessions only last a few hours.

Settings

- Source: the source for the VWAP calculation.

- Offset: changing this number will move the VWAP either Forwards or Backwards, relative to the current market. Zero is the default.

- Band: enabling this will show Standard Deviation bands.

- Band Multiplier: the value the Standard Deviation bands will be multiplied by before being plotted on the chart.

- Sessions: enabling the sessions will plot the respective anchored VWAP on chart.

- Custom: enabling this will show a custom user-defined session.

- Custom UTC: the custom session is defined by a starting UTC hour followed by the ending UTC hour.

Usage

Similar to the traditional VWAP, VWAP Market Session Anchored is a technical analysis tool used to measure the average price weighted by volume. VWAP Market Session Anchored can be used to identify the trend during a specific market session.

Limitations

When setting a custom session, be mindful that calculations are based off of the Coordinated Universal Time (UTC) time, you must convert your local time zone to UTC in order to have an accurate representation of your custom session.

It is not recommended to use this indicator on timeframes above 1 hour as market sessions only last a few hours.

版本注释

- Updated colors

- Updated chart

开源脚本

秉承TradingView的精神,该脚本的作者将其开源,以便交易者可以查看和验证其功能。向作者致敬!您可以免费使用该脚本,但请记住,重新发布代码须遵守我们的网站规则。

免责声明

这些信息和出版物并非旨在提供,也不构成TradingView提供或认可的任何形式的财务、投资、交易或其他类型的建议或推荐。请阅读使用条款了解更多信息。

免责声明

这些信息和出版物并非旨在提供,也不构成TradingView提供或认可的任何形式的财务、投资、交易或其他类型的建议或推荐。请阅读使用条款了解更多信息。