Daily Dynamic Grid StrategyHi everyone,

This strategy is built around a dynamic daily grid concept, using an upper and lower daily range that is automatically divided into multiple grid levels.

The idea is to take advantage of daily volatility by executing DCA entries on specific grid levels, based on predefined conditions.

Key points of the strategy & feature:

I recommend using 1H or 2H timeframe for this strategy

Take profit by grid

When DCA is active (>1 entry), the exit condition switches to close above the average price

A hard stop loss is applied

Includes an optional Trailing TP / SL to help maximize profit during strong moves

Like most DCA-based strategies, it tends to have a high win rate, but during strong market dumps, losses can become relatively large

Can also be used for backtest on Forex markets such as Gold, where using the trailing option is generally more effective

And still trial for the webhook, may continue to improve and update this strategy in future versions.

真实波动幅度均值(ATR)

AlgoIndex NQ/MNQ FuturesAlgoIndex Futures v3.15 - NQ/MNQ (10-Minute RTH)

This strategy is specifically tailored for trading CME Nasdaq futures - NQ and MNQ, including continuous symbols such as NQ1!/MNQ1!. It is optimized for a 10-minute chart during U.S. Regular Trading Hours (RTH), utilizing session settings defined in the Inputs. This strategy is not intended for other futures contracts or markets.

Core Concept

The strategy employs an ATR-based trend-band model similar to Supertrend for identifying directional mechanism changes in NQ/MNQ. Trade signals are evaluated at the bar close, incorporating session and time-based safety techniques to mitigate lower-quality trading opportunities near session boundaries.

Recommended Use (Optimized Defaults)

The default input parameters are fine-tuned for NQ/MNQ on the 10-minute chart. Users are encouraged to utilize these defaults initially and to make incremental adjustments to one variable at a time to understand the impact on the strategy's performance, trading frequency, and risk profile.

Configurable Inputs

- Take Profit / Stop Loss Settings:

- Enable Stop Loss and define Stop Loss (Points)

- Enable Take Profit and define Take Profit (Points)

- Enable Trailing Stop and set both Trailing Stop (Points) and Trailing Offset (Points)

- Time Avoidance Filter:

- Enable Time Avoidance

- Avoid First X Minutes

- Avoid Last X Minutes

- Display Avoidance Zones (visual overlay)

- Session Filter and End-of-Day Management:

- Enable Session Filter

- Define Trading Session (default: 09:30-16:00)

- Select Session Timezone

- Option to Close Positions at Session End

- Specify EOD Close Minutes Before (default: 20)

- Safety Controls:

- Option to Close Before Holidays (when enabled, this feature allows the strategy to flatten positions prior to holiday or early close conditions)

- Automation Settings (Optional):

- Ticker Override (optional)

- Define Contracts (position size)

- Strategy Configuration:

- Trade Direction: Both / Long Only / Short Only

- Visual Configuration:

- Option to Show Buy/Sell Signals

- Highlight Trend Zones

- Display Info Table

- Customizable Bull/Bear Colors

Alerts and Automation (Optional)

This strategy can generate order-fill alert payloads for hooking into webhook-based automation solutions. Keep in mind to validate your alert type and your bridge/broker configuration during Replay and paper trading. Note that reversals may trigger two sequential actions (e.g., exit followed by new entry).

Backtest Notes (Optional)

For more precise historical fill data, consider enabling TradingView’s Bar Magnifier in Strategy Properties. Always apply consistent assumptions for commission and slippage when comparing backtest results.

Disclaimer

This script is intended for informational and educational purposes only and does not constitute investment advice. Trading futures carries significant risk and may result in losses that exceed the initial deposit. Backtested results are hypothetical and do not guarantee future performance.

StrategyScript77 Is a rule-based strategy built on top of an Ichimoku based engine.

Ichimoku concepts are used as the backbone for trend and momentum filtering, so the strategy tends to stay on the side of the dominant move instead of fighting it.

The name “Super77” comes from the behavior I consistently observed in testing because the win rate tends to hover around the 70–80% range, often clustering around ~77% when used as intended.

It’s not a promise or guarantee, but it reflects the core design philosophy: frequent, relatively small but steady wins, with controlled and manageable losses.

Trading Style – Built for Conservative Traders

Super77 is intentionally designed for traders who prefer a conservative and calm approach:

Entries only at bar close

The strategy waits for bar close confirmation before entering a position. No intrabar guessing, no chasing half-formed signals. If the signal is still valid at close, only then will it enter.

Exits automated on bar close

Exits are also managed on bar close, which makes the logic transparent, easy to review on the chart, and more robust in backtesting compared to tick-based or intrabar hacks.

Semi-auto friendly

If you like to keep some discretion, you can treat it as semi-automatic:

Let the strategy generate entry signals

Manually cancel or skip certain trades if market context changes (news, extreme volatility, etc.)

This combination makes Super77 suitable for traders who don’t want to stare at the screen all day but still want structure and automation.

How to Use

Works best with bar-close execution (avoid trying to simulate intrabar fills if you want consistent behavior).

Designed for conservative, trend-aligned trading, not for hyper-scalping or news gambling.

Can be used as:

Fully automated (let all entries/exits trigger on bar close), or

Semi-automated (use alerts/signals but manually cancel some entries).

Step-by-Step: Automation with Cornix (Webhook Setup)

You can automate Super77 using Cornix by connecting TradingView alerts to your Cornix group via webhook.

Note: Exact button names may differ slightly depending on Cornix / TradingView updates, but the flow is always the same:

Cornix group → get webhook URL & mapping → TradingView alerts → signals sent to Cornix.

(Optional) Map specific pairs / directions

If you use UUID / signal mapping per symbol and per side (long/short), set them up in Cornix according to your own template.

Super77 can be used either:

On a single pair (simple setup), or

On multiple pairs if your alert / webhook structure supports that. So you can pick many pairs with 1 script.

Final Notes & Disclaimer

Super77 is an educational and experimental trading tool, not financial advice.

Past performance in back tests does not guarantee future results.

Always:

Test on demo or paper first

Adjust risk to match your own profile

Accept that losses and drawdowns are a natural part of any strategy

If you’re looking for a strategy that reflects a conservative, confirmation-based trading style with a focus on steady win rate and smoother equity behavior, Super77 was built exactly with that mindset in mind.

NYAM Trend PullbackThis is an trend-following strategy designed for trades taken during New York Morning. It aims to capture trend continuations by entering positions when price aligns with the dominant trend relative to a Exponential Moving Average (EMA).

If price is above the EMA then it is bullish and enters long, and if its below the EMA it is bearish and enters a short.

Pro Bollinger Bands Strategy [Breno]This strategy excels in highly volatile financial instruments, including cryptocurrencies, high-beta stocks, commodity futures, and certain exchange-traded funds (ETFs) that exhibit clear mean-reversion characteristics around their Bollinger Bands. The system's ability to utilize scaling (position averaging) and an ATR-based stop loss makes it particularly effective in markets with significant price swings, allowing the trader to capture profits from price extremes while managing increased volatility-related risk.

Core Strategy Logic

This Strategy implements a comprehensive trend-following and mean-reversion strategy primarily leveraging the Bollinger Bands (BB) indicator for entry and exit signals, complemented by an Average True Range (ATR)-based Stop Loss mechanism and an optional EMA filter. It is designed with robust features for capital management, including configurable leverage and a sophisticated position averaging (scaling) system.

Long Entry: A long position is initiated when the closing price crosses over the Lower Bollinger Band (ta.crossover(close,lowerBB)). This signals a potential mean-reversion opportunity following a price dip.

Short Entry: A short position is initiated when the closing price crosses under the Upper Bollinger Band (ta.crossunder(close,upperBB)). (Note: Short entries are disabled by default in the script inputs).

Exit Conditions (Profit Target): Long positions aim to exit upon interaction with the Upper Bollinger Band. Users can select from three exit methods:

"Close When Touch": Exits when close≥upperBB.

"Close Above then Below": Exits when the previous close was above the upper band, and the current close is below it (a reversal signal).

"High Above": Exits when high>upperBB. The strategy features an optional profitOnly setting, which restricts all exits to only occur if the trade is currently in profit (i.e., close is above the strategy.position_avg_price for longs).

Key Features and Customization

Bollinger Bands & Filters -

Customizable BB Parameters: The Length and Deviation of the Bollinger Bands are fully adjustable, allowing users to fine-tune the sensitivity of the entry and exit signals.

Optional EMA Filter: An optional EMA Filter can be enabled to align entries with the prevailing trend, where a Long entry is only permitted if close≥EMA(EmaFilterRange).

Risk and Capital Management -

Equity Allocation: Position size is dynamically calculated based on a Percentage of Equity (capitalPerc) combined with the set Leverage multiplier.

Dynamic Stop Loss (ATR-Based):

An optional Stop Loss (SL) is calculated using a multiple (slAtrInput) of the Average True Range (ATR).

The SL is set relative to the entry price upon trade activation, providing a volatility-adjusted risk management layer.

Position Averaging (Scaling): The script supports the addition of multiple units (pyramiding) to an existing position based on three user-selected criteria:

"No": No averaging.

"Percent": Adds to the position if the price has dropped by a set percentage (addPct) from the average price.

"ATR": Adds to the position if the current price is significantly below a calculated ATR-based support level from the average price.

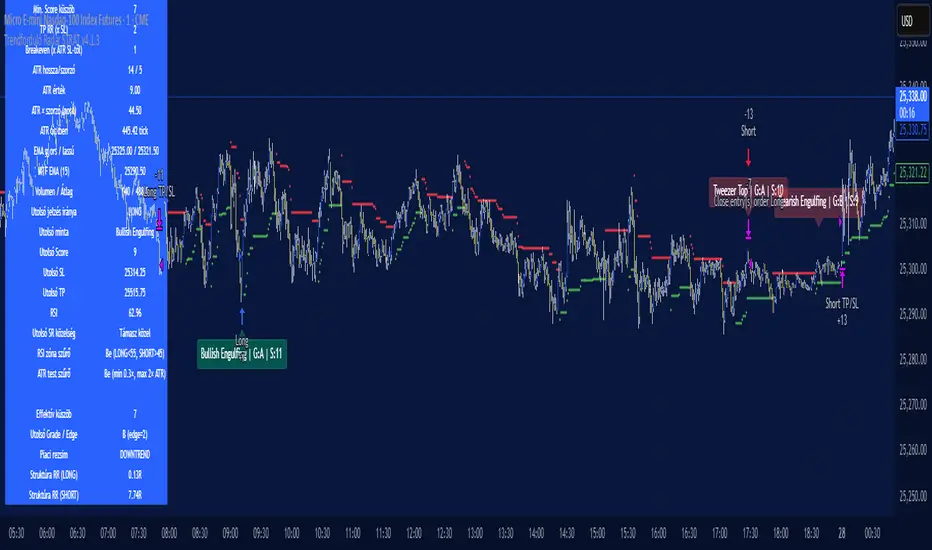

Trendforduló Radar STRAT v4.1.3Trend Reversal Radar is a proprietary indicator that examines potential turning points in market trends. It combines data from multiple time frames, support and resistance levels, and volume movements to provide visual signals to traders. Its purpose is not to provide trading advice, but to complement technical analysis and provide more confident decision support.- A Trendforduló Radar egy saját fejlesztésű indikátor, amely a piaci trendek lehetséges fordulópontjait vizsgálja. Több idősík adatait, támasz–ellenállás szinteket és volumenmozgásokat kombinálva ad vizuális jelzést a kereskedőnek. A célja nem a kereskedési tanácsadás, hanem hogy kiegészítse a technikai elemzést és magabiztosabb döntéstámogatást adjon.

15m ORB Breakout NAS100 (5m Mgmt) v6 - OptimizedOpening Range Breakout Strategy

Buy and sell signals are given upon break of market session opening range. Best utilized for 30 minute NY opening range, managed on 5 min timeframe on NAS100. Tweak the settings for higher win rate on backtesting dashboard before implementing strategy.

SMC Trend Filter Strategy (EMA50/EMA200 + FVG)Overview

This strategy implements a multi-timeframe Smart Money Concept (SMC) trading system designed for intraday and swing trading.

It combines a Daily trend filter, Break of Structure (BOS) detection, Order Block (OB) zones, Fair Value Gap (FVG) confirmation, and an ATR-based trailing stop system to achieve structured and rule-based entries.

The strategy is fully automated for backtesting and allows users to evaluate SMC concepts without repainting or discretionary interpretation.

- Core Components

1. Higher-Timeframe Trend Filter (Daily EMA50/EMA200)

The strategy retrieves D1 data and determines market direction using EMA50 and EMA200:

Uptrend → EMA50 > EMA200

Downtrend → EMA50 < EMA200

Trades are only taken in the direction of the Daily trend to avoid counter-trend setups.

2. Market Structure & Break of Structure (BOS)

The strategy identifies swing highs/lows and detects when price breaks beyond them:

Bullish BOS: price closes above previous swing high

Bearish BOS: price closes below previous swing low

This forms the foundation of SMC market structure recognition.

3. Order Block Zone (OB)

Upon detecting a BOS, the strategy marks the previous candle as a potential Order Block:

For bullish BOS → OB = previous candle’s high/low

For bearish BOS → OB = previous candle’s high/low

The OB zone is visualized using a semi-transparent box extended forward

Aquas TrendIt’s a trend-following crossover system with:

A local fast/slow EMA cross for timing entries

A higher-timeframe EMA filter to only trade in the dominant trend

An ATR-based volatility filter so it only trades when the market is moving

ATR-based stop loss and take profit with fixed RR

It tries to catch swings in the direction of the larger trend and ignore chop.

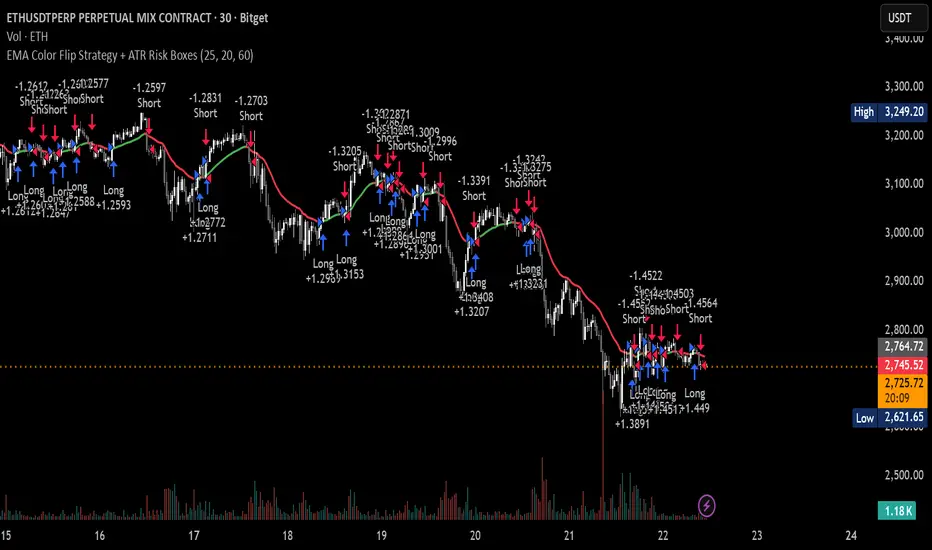

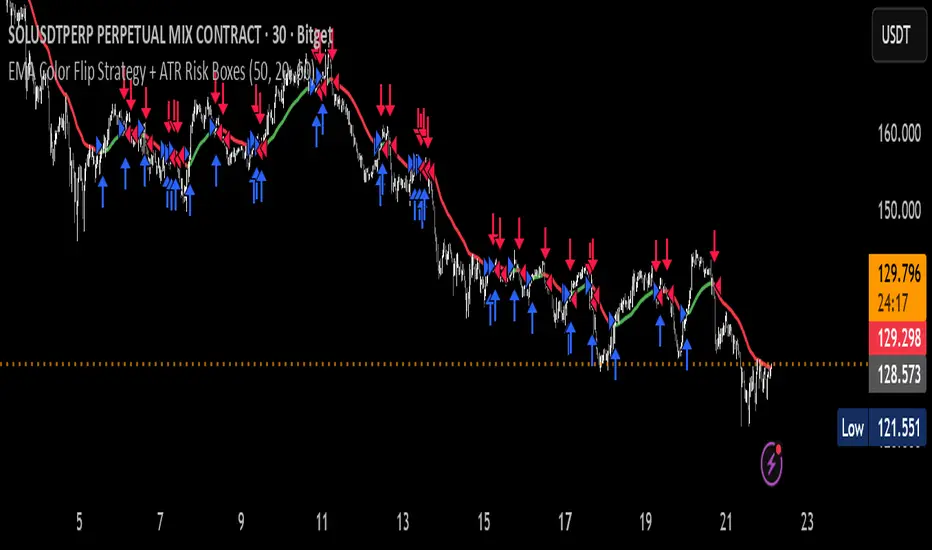

EMA Color Flip Strategy Experimenting on SOL 30 min chart, it seems good!

Let me know what you think!

SMC MTF + FVG + Trailing TP 100% [FIXED]Component Description

Entry Timeframe: H1

Trend Filter: D1 (EMA50 vs EMA200)

Trend Filter Only enter BUY orders if EMA50 > EMA200 on D1 (uptrend)

Only enter SELL orders if EMA50 < EMA200 (downtrend)

Break of Structure (BOS) Identify the previous swing high/low breakout point

Order Block (OB) The candle area before BOS is marked with an orange box

Fair Value Gap (FVG) Check for the presence of a price gap to confirm Entry

Trailing TP Trigger trailing after reaching the desired R (in pips or ATR)

KDH v2.0 (English) Trading Strategy Indicator# KDH Diamond Strategy v3.3 - TradingView Description

---

## 🇬🇧 ENGLISH VERSION

### 📊 KDH Diamond Strategy v3.3

**Professional High-Leverage Futures Trading System**

---

#### 🎯 Overview

KDH Diamond is an advanced algorithmic trading strategy specifically optimized for **1-hour timeframe futures trading** with high-leverage environments. Built on proven institutional concepts including Fair Value Gaps (FVG), Volume Profile analysis, and multi-layered confirmation filters, this strategy delivers consistent results without repainting.

---

#### ✨ Key Features

**🔥 Optimized for 1H Timeframe**

- Extensively backtested across multiple markets

- Highest profit rate achieved on 1-hour charts

- Perfect for swing traders and active position management

**🎨 No Repainting - 100% Reliable Signals**

- All signals are confirmed and locked on bar close

- What you see in backtest is what you get in real-time

- Complete transparency with `calc_on_order_fills=true`

**💎 Automated Risk Management**

- Automatic Stop Loss and Take Profit calculation

- Intelligent SL/TP placement based on market structure

- Built-in position sizing controls (adjustable % per trade)

**🚀 High-Leverage Futures Optimized**

- Designed specifically for leveraged futures trading

- Risk-reward ratios calibrated for 10-20x leverage environments

- Precision entry timing to maximize profit potential

**🔄 Advanced Position Management**

- Automatic reversal entries at TP levels

- Multiple re-entry opportunities per signal

- Dynamic trade management based on market conditions

**🎛️ Multi-Layer Confirmation System**

- **SMA50 Filter (1H)**: Trend alignment confirmation

- **Momentum Filter**: KAMA-based directional strength

- **RSI Divergence Filter**: Reversal detection at extremes

- **Volume Profile Filter**: Order flow and liquidity analysis

---

#### 📈 How It Works

**Signal Generation**

The strategy identifies **Inverted Fair Value Gaps (IFVG)** - institutional order blocks that signal high-probability reversal or continuation zones. Each signal is validated through multiple confirmation filters before execution.

**Entry Logic**

- Limit orders placed at optimal price levels within FVG zones

- Price must touch the midline and close in favorable direction

- All filters must align for signal activation

**Exit Strategy**

- Stop Loss: Placed at the next opposing FVG level

- Take Profit: Calculated using nearest FVG in profit direction

- Automatic reversal entry option at TP levels

**Visual System**

- Color-coded boxes show FVG zones (green/red)

- Real-time position tracking with entry, SL, and TP lines

- Comprehensive dashboard displaying filter status and P&L

---

#### 🎯 Who Is This For?

✅ **Perfect For:**

- Futures traders using 10-20x leverage

- Traders seeking systematic, rule-based strategies

- Those who want automated SL/TP management

- 1-hour chart swing traders

- Traders familiar with institutional concepts (FVG, order flow)

❌ **Not Ideal For:**

- Scalpers (designed for 1H timeframe)

- Spot-only traders (optimized for leveraged futures)

- Beginners unfamiliar with leverage risks

- Set-and-forget automated trading (requires monitoring)

---

#### 📊 What You Get

**Strategy Features:**

- Complete FVG detection and inversion system

- 4 professional-grade confirmation filters

- Automated SL/TP calculation and placement

- TP reversal entry system

- Volume Profile sentiment analysis

- Real-time position tracking dashboard

- Webhook alert support for automation

- Clean, organized code with detailed comments

**Visual Components:**

- FVG boxes with inversion coloring

- Volume Profile sentiment boxes (optional)

- Entry, SL, and TP lines for each position

- Position status table with live P&L

- Filter status dashboard

---

#### ⚙️ Customization Options

**Adjustable Filters (User Control):**

- SMA50 Filter (1H) - Trend alignment ON/OFF

- Momentum Filter - Directional strength ON/OFF

- RSI Divergence Filter - Reversal detection ON/OFF

- Volume Profile Filter - Order flow analysis ON/OFF

**Fixed Parameters (Optimized):**

- All core parameters are pre-optimized for 1H timeframe

- Ensures consistent performance without overwhelming options

- Prevents parameter over-fitting by users

---

#### ⚠️ Important Disclaimers

**Risk Warning:**

This strategy is designed for leveraged futures trading, which carries substantial risk. High leverage (10-20x) can result in rapid losses. Only trade with capital you can afford to lose.

**Performance:**

Past performance does not guarantee future results. Always backtest on your specific market and timeframe before live trading.

**Usage:**

This is a trading tool, not financial advice. Users are responsible for their own trading decisions and risk management.

**Requirements:**

- Understanding of futures trading and leverage

- Familiarity with Fair Value Gaps and institutional concepts

- Ability to monitor positions (not fully automated)

- Proper risk management discipline

---

#### 🔧 Technical Specifications

- **Platform:** TradingView Pine Script v5

- **Type:** Strategy (with backtesting capabilities)

- **Timeframe:** Optimized for 1H (works on other timeframes)

- **Markets:** Any futures market (crypto, stocks, indices, forex)

- **Repainting:** NO - All signals are final on bar close

- **Alerts:** Full webhook support for automation

- **Default Settings:** 10% position size, pyramiding enabled (max 10 positions)

---

#### 📞 Support

Questions about setup or usage? Contact the author through TradingView messages.

**Note:** This indicator is for educational and trading tool purposes only. The author is not responsible for trading losses. Trade responsibly and within your risk tolerance.

Machiavelli v2.5The purpose of this script is straightforward — to provide a reliable source of passive income.

Results speak for themselves.

BB SPY Mean Reversion Investment StrategySummary

Mean reversion first, continuation second. This strategy targets equities and ETFs on daily timeframes. It waits for price to revert from a Bollinger location with candle and EMA agreement, then manages risk with ATR based exits. Uniqueness comes from two elements working together. One, an adaptive band multiplier driven by volatility of volatility that expands or contracts the envelope as conditions change. Two, a bias memory that re arms the same direction after any stop, target, or time exit until a true opposite signal appears. Add it to a clean chart, use the markers and levels, and select on bar close for conservative alerts. Shapes can move while the bar is open and settle on close.

Scope and intent

• Markets. Currently adapted for SPY, needs to be optimized for other assets

• Timeframes. Daily primary. Other frames are possible but not the default

• Default demo. SPY on daily

• Purpose. Trade mean reversion entries that can chain into a longer swing by splitting holds into ATR or time segments

Originality and usefulness

• Novelty. Adaptive band width from volatility of volatility plus a persistent bias array that keeps the original direction alive across sequential entries until an opposite setup is confirmed

• Failure modes mitigated. False starts in chop are reduced by candle color and EMA location. Missed continuation after a take profit or stop is addressed by the re arm engine. Oversized envelopes during quiet regimes are avoided by the adaptive multiplier

• Testability. Every module has Inputs and visible levels so users can see why a suggestion appears

• Portable yardstick. All risk and targets are expressed in ATR units

Method overview in plain language

The engine measures where price sits relative to Bollinger bands, confirms with candle color and EMA location, requires ADX for shorts(in our case long close since we use it currently as long only), and optionally requires a trend or mean reversion regime using band width percent rank and basis slope. Risk uses ATR for stop, target, and optional breakeven. A small array stores the last confirmed direction. While flat, the engine keeps a pending order in that direction. The array flips only when a true opposite setup appears.

Base measures

• Range basis. True Range smoothed over a user defined ATR Length

• Return basis. Not required

Components

• Bollinger envelope. SMA length and standard deviation multiplier. Entry is based on cross of close through the band with location bias

• Candle and EMA filter. Close relative to open and close relative to EMA align direction

• ADX gate for shorts. Requires minimum trend strength for short trades

• Adaptive multiplier. Band width scales using volatility of volatility so envelopes breathe with conditions

• Regime gate optional. Band width percent rank and basis slope identify trend or mean reversion regimes

• Risk manager. ATR stop, ATR target, optional breakeven, optional time exit

• Bias memory. Array stores last confirmed direction and re arms entries while flat

Fusion rule

Minimum satisfied gates count style. All required gates must be true. Optional gates are controlled in Inputs. Bias memory never overrides an opposite confirmed setup.

Signal rule

• Long setup when close crosses up through the lower band, the bar closes green, and close is above the long EMA

• Short setup when close crosses down through the upper band, the bar closes red, close is below the short EMA, and ADX is above the minimum

• While flat the model keeps a pending order in the stored direction until a true opposite setup appears

• IN LONG or IN SHORT describes states between entry and exit

What you will see on the chart

• Markers for Long and Short setups

• Exit markers from ATR or time rules

• Reference levels for entry, stop, and target

• Bollinger bands and optional adaptive bands

Inputs with guidance

Setup

• Signal timeframe. Uses the chart timeframe

• Invert direction optional. Flips long and short

Logic

• BB Length. Typical 10 to 50. Higher smooths more

• BB Mult. Typical 1.0 to 2.5. Higher widens entries

• EMA Length long. Typical 10 to 50

• EMA Length short. Typical 5 to 30

• ADX Minimum for short. Typical 15 to 35

Filters

• Regime Type. none or trend or mean reversion

• Rank Lookback. Typical 100 to 300

• Basis Slope Length and Threshold. Larger values reduce false trends

Risk

• ATR Length. Typical 10 to 21

• ATR Stop Mult. Typical 1.0 to 3.0

• ATR Take Profit Mult. Typical 2.0 to 5.0

• Breakeven Trigger R. Move stop to entry after the chosen multiple

• Time Exit. Minimum bars and extension when profit exceeds a fraction of ATR

Bias and rearm

• Bias flips kept. Array depth

• Keep rearm when flat. Maintain a pending order while flat

UI

• Show markers and levels. Clean defaults

Usage recipes

Alerts update in real time and can change while the bar forms. Select on bar close for conservative workflows.

Properties visible in this publication

• Initial capital 25000

• Base currency USD

• If any higher timeframe calls are enabled, request.security uses lookahead off

• Commission 0.03 percent

• Slippage 3 ticks

• Default order size method Percent of equity with value 5

• Pyramiding 0

• Process orders on close On

• Bar magnifier Off

• Recalculate after order is filled Off

• Calc on every tick Off

Realism and responsible publication

No performance claims. Costs and fills vary by venue. Shapes can move intrabar and settle on close. Strategies use standard candles only.

Honest limitations and failure modes

High impact releases and thin liquidity can break assumptions. Gap heavy symbols may require larger ATR. Very quiet regimes can reduce contrast in the mean reversion signal. If stop and target can both be touched inside one bar, outcome follows the TradingView order model for that bar path.

Regimes with extreme one sided trend and very low volatility can reduce mean reversion edges. Results vary by symbol and venue. Past results never guarantee future outcomes.

Open source reuse and credits

None.

Backtest realism

Costs are realistic for liquid equities. Sizing does not exceed five percent per trade by default. Any departure should be justified by the user.

If you got any questions please le me know

PSAR with ATR Trailing Stop + SMA Filter📈 Strategy Overview: PSAR + 6×ATR Trailing Stop with SMA Filter

This strategy is built around the principle of “Cut the losers, let the winners run” — a disciplined, trend-following approach that combines the Parabolic SAR indicator with dynamic risk management and a Simple Moving Average (SMA) trend filter.

🔍 Strategy Logic

Trend Filter Trades are only taken in the direction of the prevailing trend, defined by a user-selected SMA (default: 100).

✅ Long trades only when price is above the SMA

✅ Short trades only when price is below the SMA

Entry Signal: A trade is triggered when the Parabolic SAR flips to the opposite side of the price bars, signaling a potential trend reversal.

Stop Loss: The stop loss is dynamically set at 6×ATR from the entry price. This adapts to market volatility and is recalculated every bar — effectively acting as a trailing stop.

Exit Logic: There is no fixed take profit. The trade remains open until the trailing stop is hit — allowing winners to run and losers to be cut quickly.

Risk Management: Each trade risks 0.5% of total equity, ensuring consistent position sizing and capital preservation.

📊 Visual Elements

PSAR dots mark trend direction changes

SMA line shows the broader trend filter

Trailing stop crosses (with 50% opacity) indicate the current stop level without cluttering the chart

⚙️ Customizable Inputs

PSAR parameters: Start, Increment, Maximum

ATR length and multiplier

SMA length

Risk percentage per trade

This strategy is ideal for traders who want to stay aligned with the trend, automate disciplined exits, and avoid emotional decision-making. Clean, simple, and powerful.

Wishing you calm and successful trades!

Hyper SAR Reactor Trend StrategyHyperSAR Reactor Adaptive PSAR Strategy

Summary

Adaptive Parabolic SAR strategy for liquid stocks, ETFs, futures, and crypto across intraday to daily timeframes. It acts only when an adaptive trail flips and confirmation gates agree. Originality comes from a logistic boost of the SAR acceleration using drift versus ATR, plus ATR hysteresis, inertia on the trail, and a bear-only gate for shorts. Add to a clean chart and run on bar close for conservative alerts.

Scope and intent

• Markets: large cap equities and ETFs, index futures, major FX, liquid crypto

• Timeframes: one minute to daily

• Default demo: BTC on 60 minute

• Purpose: faster yet calmer PSAR that resists chop and improves short discipline

• Limits: this is a strategy that places simulated orders on standard candles

Originality and usefulness

• Novel fusion: PSAR AF is boosted by a logistic function of normalized drift, trail is monotone with inertia, entries use ATR buffers and optional cooldown, shorts are allowed only in a bear bias

• Addresses false flips in low volatility and weak downtrends

• All controls are exposed in Inputs for testability

• Yardstick: ATR normalizes drift so settings port across symbols

• Open source. No links. No solicitation

Method overview

Components

• Adaptive AF: base step plus boost factor times logistic strength

• Trail inertia: one sided blend that keeps the SAR monotone

• Flip hysteresis: price must clear SAR by a buffer times ATR

• Volatility gate: ATR over its mean must exceed a ratio

• Bear bias for shorts: price below EMA of length 91 with negative slope window 54

• Cooldown bars optional after any entry

• Visual SAR smoothing is cosmetic and does not drive orders

Fusion rule

Entry requires the internal flip plus all enabled gates. No weighted scores.

Signal rule

• Long when trend flips up and close is above SAR plus buffer times ATR and gates pass

• Short when trend flips down and close is below SAR minus buffer times ATR and gates pass

• Exit uses SAR as stop and optional ATR take profit per side

Inputs with guidance

Reactor Engine

• Start AF 0.02. Lower slows new trends. Higher reacts quicker

• Max AF 1. Typical 0.2 to 1. Caps acceleration

• Base step 0.04. Typical 0.01 to 0.08. Raises speed in trends

• Strength window 18. Typical 10 to 40. Drift estimation window

• ATR length 16. Typical 10 to 30. Volatility unit

• Strength gain 4.5. Typical 2 to 6. Steepness of logistic

• Strength center 0.45. Typical 0.3 to 0.8. Midpoint of logistic

• Boost factor 0.03. Typical 0.01 to 0.08. Adds to step when strength rises

• AF smoothing 0.50. Typical 0.2 to 0.7. Adds inertia to AF growth

• Trail smoothing 0.35. Typical 0.15 to 0.45. Adds inertia to the trail

• Allow Long, Allow Short toggles

Trade Filters

• Flip confirm buffer ATR 0.50. Typical 0.2 to 0.8. Raise to cut flips

• Cooldown bars after entry 0. Typical 0 to 8. Blocks re entry for N bars

• Vol gate length 30 and Vol gate ratio 1. Raise ratio to trade only in active regimes

• Gate shorts by bear regime ON. Bear bias window 54 and Bias MA length 91 tune strictness

Risk

• TP long ATR 1.0. Set to zero to disable

• TP short ATR 0.0. Set to 0.8 to 1.2 for quicker shorts

Usage recipes

Intraday trend focus

Confirm buffer 0.35 to 0.5. Cooldown 2 to 4. Vol gate ratio 1.1. Shorts gated by bear regime.

Intraday mean reversion focus

Confirm buffer 0.6 to 0.8. Cooldown 4 to 6. Lower boost factor. Leave shorts gated.

Swing continuation

Strength window 24 to 34. ATR length 20 to 30. Confirm buffer 0.4 to 0.6. Use daily or four hour charts.

Properties visible in this publication

Initial capital 10000. Base currency USD. Order size Percent of equity 3. Pyramiding 0. Commission 0.05 percent. Slippage 5 ticks. Process orders on close OFF. Bar magnifier OFF. Recalculate after order filled OFF. Calc on every tick OFF. No security calls.

Realism and responsible publication

No performance claims. Past results never guarantee future outcomes. Shapes can move while a bar forms and settle on close. Strategies execute only on standard candles.

Honest limitations and failure modes

High impact events and thin books can void assumptions. Gap heavy symbols may prefer longer ATR. Very quiet regimes can reduce contrast and invite false flips.

Open source reuse and credits

Public domain building blocks used: PSAR concept and ATR. Implementation and fusion are original. No borrowed code from other authors.

Strategy notice

Orders are simulated on standard candles. No lookahead.

Entries and exits

Long: flip up plus ATR buffer and all gates true

Short: flip down plus ATR buffer and gates true with bear bias when enabled

Exit: SAR stop per side, optional ATR take profit, optional cooldown after entry

Tie handling: stop first if both stop and target could fill in one bar

Fincandle ATR Direction TrackerOverview

The Fincandle ATR Direction Tracker is a strategy designed to capture momentum moves in the market using a dynamic ATR-based trailing stop. It identifies strong momentum candles and filters signals using trend alignment with moving averages.

Partial exits allow users to take a portion of profit at a predefined ATR multiple while keeping the remaining position open until the opposite signal occurs.

How It Works

Momentum Detection:

Measures candle body size relative to the Average True Range (ATR).

A candle is considered momentum if its body size exceeds ATR × Multiplier.

Trend Filter:

Uses two moving averages (Fast MA and Slow MA) to determine the market trend.

Bullish trend: Fast MA > Slow MA → long trades allowed

Bearish trend: Fast MA < Slow MA → short trades allowed

Trend filter can be toggled on or off.

ATR Trailing Stop:

A dynamic trailing stop adapts to price volatility.

Crossing above the trail triggers a buy signal, crossing below triggers a sell signal.

Partial Exit / Take Profit:

Step 1: Exit 50% of the position when price moves a configurable multiple of ATR in your favor.

Step 2: Close the remaining position when the opposite signal occurs (e.g., price crosses below/above the ATR trail).

How to Use

Add the strategy to any chart (stocks, indices, forex, crypto).

Configure ATR period, sensitivity, take profit multiple, and moving average lengths to suit the timeframe and asset.

Monitor buy/sell markers and dynamic ATR trail on the chart.

Optional: Set alerts for real-time notifications when signals trigger.

Adjust partial exit multiplier to control risk/reward.

Example Settings

ATR Period: 10

ATR Sensitivity: 3 × ATR

Take Profit: 2 × ATR

Fast MA: 50

Slow MA: 200

Partial Exit: 50% of position at take profit, remaining exits on opposite signal

Key Features

Adaptive ATR trailing stop for volatility-based entries/exits.

Trend alignment filter with Fast/Slow MA.

Partial exit logic for better risk management.

Visual BUY/SELL markers and alerts.

Fully Pine Script v6 compatible.

Disclaimer

This strategy is for educational and analytical purposes only.

It does not guarantee profits. Traders should always use proper risk management.

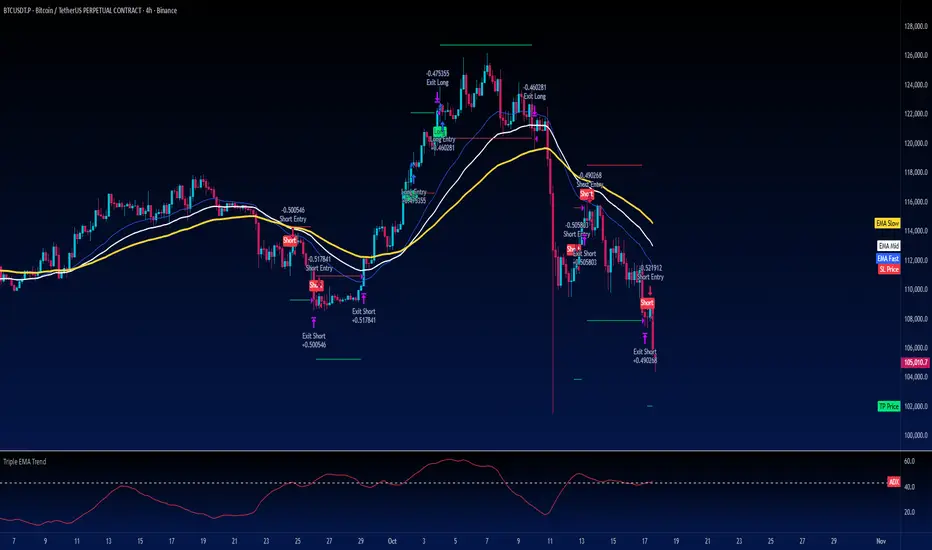

Turtle Strategy - Triple EMA Trend with ADX and ATRDescription

The Triple EMA Trend strategy is a directional momentum system built on the alignment of three exponential moving averages and a strong ADX confirmation filter. It is designed to capture established trends while maintaining disciplined risk management through ATR-based stops and targets.

Core Logic

The system activates only under high-trend conditions, defined by the Average Directional Index (ADX) exceeding a configurable threshold (default: 43).

A bullish setup occurs when the short-term EMA is above the mid-term EMA, which in turn is above the long-term EMA, and price trades above the fastest EMA.

A bearish setup is the mirror condition.

Execution Rules

Entry:

• Long when ADX confirms trend strength and EMA alignment is bullish.

• Short when ADX confirms trend strength and EMA alignment is bearish.

Exit:

• Stop Loss: 1.8 × ATR below (for longs) or above (for shorts) the entry price.

• Take Profit: 3.3 × ATR in the direction of the trade.

Both parameters are configurable.

Additional Features

• Start/end date inputs for controlled backtesting.

• Selective activation of long or short trades.

• Built-in commission and position sizing (percent of equity).

• Full visual representation of EMAs, ADX, stop-loss, and target levels.

This strategy emphasizes clean trend participation, strict entry qualification, and consistent reward-to-risk structure. Ideal for swing or medium-term testing across trending assets.

Trend-Following & Breakout — Index Quant Strategy (NASDAQ)📈 Trend-Following & Breakout — Index Quant Strategy (NASDAQ & S&P 500)

Type: Invite-only strategy

Markets: NASDAQ 100 (NAS100 / US100 / NQ), S&P 500 (US500 / SPX), and other major equity indices.

🧠 Concept: Continuous trend model combining EWMAC (trend-following) and Donchian (breakout) signals, scaled by forecast strength and portfolio risk.

⚙️ Execution: Rebalances only on decision-bar closes, using hysteresis and a no-trade band to reduce churn.

📊 Default bias: Long-only — aligned with equity index drift.

🧩 How it works

• EWMAC Trend: Difference between fast and slow EMAs, normalized by an EWMA of absolute returns.

• Donchian Breakout: Distance beyond a 200-bar channel (Strict mode) or relative z-score position within it.

• Forecast combination: Weighted sum of trend and breakout points, clamped to ± capPoints.

• Hysteresis: Prevents quick sign flips near zero forecast.

• Risk scaling: Maps forecast strength to position size using equity × risk budget × ATR-based stop distance.

• Rebalance: Executes only if the required quantity change exceeds the Δqty threshold; can optionally block increases on Sundays (for CFDs).

⚙️ Default parameters

Deployed on NQ / US100 / NAS100 on Daily Timeframe

• Decision timeframe = 360 min (other options from 1 min to 1 week).

• Trend (EWMAC): Fast = 64, Slow = 256, Vol Norm = 32, Weight = 0.8.

• Breakout (Donchian): Length = 200, Mode = Strict, Weight = 0.2.

• Forecast scaling: ptsPerSigma = 1.0, capPoints = 10.

• Risk % per rebalance = 4 % of equity.

• ATR stop: ATR(14) × 1.0.

• No-trade band (Δqty) = 4 units.

• Hysteresis = 2 forecast points.

• Bias = Long-only (Neutral / Long-bias 50 % optional).

• Skip Sunday increases = false (default).

📋 Backtest properties (documented)

• Initial capital = 100 000 USD.

• Commission = 0.20 % per trade.

• Pyramiding = 10.

• Calc on every tick = false.

• Point value = 1 (for NAS100 CFD).

• No financing or slippage modeled.

• If using CFDs, account for overnight funding.

• On futures (NQ / ES), carry is implicit.

📊 Typical behaviour

• Many small scratches, a few large winners.

• Performs best during multi-week / multi-month trends.

• Underperforms in tight or volatile ranges.

• Average hold ≈ 30 – 90 days in historical tests.

💡 Risk and performance guide (illustrative)

Sharpe ≈ 1.25

Sortino ≈ 1.10 – 1.30

Max drawdown ≈ –18 % to –25 %

Annual volatility ≈ 24 – 28 %

CAGR ≈ 50 – 60 % (at 4 % risk)

Edge ratio ≈ 5 (MFE / MAE)

Historical backtests only — past performance does not guarantee future results.

🌍 Intended markets and timeframes

Optimized for NASDAQ 100 and S&P 500; also effective on similar indices (DAX, Dow Jones, FTSE).

Best on Daily or higher timeframes.

Aligns with long-term index drift — suitable for long-bias systematic trend portfolios.

⚠️ Limitations

• Backtests exclude CFD funding costs.

• Trend models will have losing streaks in range-bound markets.

• Designed for experienced traders seeking systematic exposure.

🔑 Requesting access

Send a private TradingView message to with the text:

“Request access to Trend-Following & Breakout — Index Quant Strategy.”

Access is granted only on explicit request.

For further information, see my TradingView Signature.

🆕 Release notes (v1.0)

• Initial release (360 min TF): EWMAC 64/256 + Donchian 200 Strict.

• Risk 4 %, ATR × 1.0, Long-only bias, hysteresis 2 pts, Δqty ≥ 4.

• Developed for NASDAQ 100 and S&P 500 indices.

• Implements continuous risk-scaled positioning and no-trade band logic.

🧾 Originality statement

This strategy is original work built entirely from TradingView built-ins (EMA, ATR, Highest, Lowest).

It does not reuse open-source invite-only code.

Any future reuse of open scripts will be done with explicit permission and credit.

Liquidity SweeperStrategy Overview

This Pine Script implements a Liquidity Sweep Trading Strategy, a sophisticated approach that capitalizes on market manipulation tactics commonly used by institutional traders. The strategy identifies when price "sweeps" above recent swing highs or below swing lows to trigger stop losses and grab liquidity, then quickly reverses direction - creating high-probability trading opportunities.

Core Concept: What is a Liquidity Sweep?

A liquidity sweep occurs when:

Price breaks above a swing high (or below a swing low) to trigger retail stop losses

Institutional players absorb this liquidity at favorable prices

Price quickly reverses back into the previous range

This creates a "fake breakout" or "stop hunt" pattern

The strategy exploits these manipulative moves by entering trades in the direction of the reversal.

How the Strategy Works

1. Swing Point Detection

Uses a lookback period (default: 20 bars) to identify significant swing highs and lows

Employs proper pivot point detection using ta.highestbars() and ta.lowestbars()

Only considers confirmed swing points (not just recent highs/lows)

2. Liquidity Sweep Identification

High Sweep (Short Setup):

Price moves above the last swing high (triggering buy stops)

Same bar closes back below the swing high (showing rejection)

Low Sweep (Long Setup):

Price moves below the last swing low (triggering sell stops)

Same bar closes back above the swing low (showing support)

3. Confirmation Process

Requires price to stay within the swept range for a specified number of bars (default: 3)

This confirms the sweep was genuine and not just normal volatility

Prevents false signals and improves trade quality

4. Entry Logic

Long Entries: Triggered after confirmed low sweeps

Short Entries: Triggered after confirmed high sweeps

5. Risk Management

Stop Loss: Placed at a multiple of ATR (default: 1.5x) from entry price

Take Profit: Risk/Reward ratio based (default: 2:1)

Position Sizing: 10% of equity per trade (configurable)

Red X-crosses: High sweeps detected

Green X-crosses: Low sweeps detected

Red triangles (down): Short entry signals

Green triangles (up): Long entry signals

Horizontal lines: Current swing high/low levels

Info label: Shows last detected swing levels

Optimal Conditions:

Timeframes: 1H, 4H, and Daily work best

Market Conditions: Ranging and trending markets both suitable

Volatility: Moderate to high volatility preferred

Session Times: Most effective during active trading sessions

Strengths:

✅ Exploits institutional manipulation tactics

✅ Clear entry/exit rules with defined risk

✅ Works across multiple asset classes

✅ Includes proper confirmation to reduce false signals

✅ Visual clarity for manual verification

✅ Reasonable risk/reward parameters

Limitations:

⚠️ Requires patience - not a high-frequency strategy

⚠️ Market dependent - fewer signals in low volatility periods

⚠️ Needs sufficient lookback data for swing identification

⚠️ May have drawdown periods during strong trending moves

⚠️ Requires understanding of market structure concepts

Best Practices for Users

Optimization Tips:

Adjust lookback period based on timeframe (shorter for lower TFs)

Test different confirmation periods for your market

Consider market session times when backtesting

Use alongside volume analysis for additional confirmation

Risk Management:

Never risk more than 2-3% per trade of total capital

Consider reducing position size during high-impact news

Monitor correlation if trading multiple pairs simultaneously

Use additional filters (trend, support/resistance) for confluence

Backtesting Recommendations:

Test on at least 6 months of historical data

Include different market conditions (trending, ranging, volatile)

Consider transaction costs and slippage in results

Forward test on demo before live implementation

Expected Results

Based on typical liquidity sweep strategy performance:

Disclaimer

This strategy is based on market structure analysis and institutional trading behavior patterns. Past performance doesn't guarantee future results. Users should:

Thoroughly backtest before live trading

Start with small position sizes

Understand the underlying concepts before implementation

Consider combining with other analysis methods

Always use proper risk management

The strategy works best when traders understand the psychological and structural elements of liquidity sweeps rather than just following signals blindly.