MTF K-Means Price Regimes [matteovesperi] ⚠️ The preview uses a custom example to identify support/resistance zones. due to the fact that this identifier clusterizes, this is possible. this example was set up "in a hurry", therefore it has a possible inaccuracy. When setting up the indicator, it is extremely important to select the correct parameters and double-check them on the selected history.

📊 OVERVIEW

Purpose

MTF K-Means Price Regimes is a TradingView indicator that automatically identifies and classifies the current market regime based on the K-Means machine learning algorithm. The indicator uses data from a higher timeframe (Multi-TimeFrame, MTF) to build stable classification and applies it to the working timeframe in real-time.

Key Features

✅ Automatic market regime detection — the algorithm finds clusters of similar market conditions

✅ Multi-timeframe (MTF) — clustering on higher TF, application on lower TF

✅ Adaptive — model recalculates when a new HTF bar appears with a rolling window

✅ Non-Repainting — classification is performed only on closed bars

✅ Visualization — bar coloring + information panel with cluster characteristics

✅ Flexible settings — from 2 to 10 clusters, customizable feature periods, HTF selection

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🔬 TECHNICAL DETAILS

K-Means Clustering Algorithm

What is K-Means?

K-Means is one of the most popular clustering algorithms (unsupervised machine learning). It divides a dataset into K groups (clusters) so that similar elements are within each cluster, and different elements are between clusters.

Algorithm objective:

Minimize within-cluster variance (sum of squared distances from points to their cluster center).

How Does K-Means Work in Our Indicator?

Step 1: Data Collection

The indicator accumulates history from the higher timeframe (HTF):

RSI (Relative Strength Index) — overbought/oversold indicator

ATR% (Average True Range as % of price) — volatility indicator

ΔP% (Price Change in %) — trend strength and direction indicator

By default, 200 HTF bars are accumulated (clusterLookback parameter).

Step 2: Creating Feature Vectors

Each HTF bar is described by a three-dimensional vector:

Vector =

Step 3: Normalization (Z-Score)

All features are normalized to bring them to a common scale:

Normalized_Value = (Value - Mean) / StdDev

This is critically important, as RSI is in the range 0-100, while ATR% and ΔP% have different scales. Without normalization, one feature would dominate over others.

Step 4: K-Means++ Centroid Initialization

Instead of random selection of K initial centers, an improved K-Means++ method is used:

First centroid is randomly selected from the data

Each subsequent centroid is selected with probability proportional to the square of the distance to the nearest already selected centroid

This ensures better initial centroid distribution and faster convergence

Step 5: Iterative Optimization (Lloyd's Algorithm)

Repeat until convergence (or maxIterations):

1. Assignment step:

For each point find the nearest centroid and assign it to this cluster

2. Update step:

Recalculate centroids as the average of all points in each cluster

3. Convergence check:

If centroids shifted less than 0.001 → STOP

Euclidean distance in 3D space is used:

Distance = sqrt((RSI1 - RSI2)² + (ATR1 - ATR2)² + (ΔP1 - ΔP2)²)

Step 6: Adaptive Update

With each new HTF bar:

The oldest bar is removed from history (rolling window method)

New bar is added to history

K-Means algorithm is executed again on updated data

Model remains relevant for current market conditions

Real-Time Classification

After building the model (clusters + centroids), the indicator works in classification mode:

On each closed bar of the current timeframe, RSI, ATR%, ΔP% are calculated

Feature vector is normalized using HTF statistics (Mean/StdDev)

Distance to all K centroids is calculated

Bar is assigned to the cluster with minimum distance

Bar is colored with the corresponding cluster color

Important: Classification occurs only on a closed bar (barstate.isconfirmed), which guarantees no repainting .

Data Architecture

Persistent variables (var):

├── featureVectors - Normalized HTF feature vectors

├── centroids - Cluster center coordinates (K * 3 values)

├── assignments - Assignment of each HTF bar to a cluster

├── htfRsiHistory - History of RSI values from HTF

├── htfAtrHistory - History of ATR values from HTF

├── htfPcHistory - History of price changes from HTF

├── htfCloseHistory - History of close prices from HTF

├── htfRsiMean, htfRsiStd - Statistics for RSI normalization

├── htfAtrMean, htfAtrStd - Statistics for ATR normalization

├── htfPcMean, htfPcStd - Statistics for Price Change normalization

├── isCalculated - Model readiness flag

└── currentCluster - Current active cluster

All arrays are synchronized and updated atomically when a new HTF bar appears.

Computational Complexity

Data collection: O(1) per bar

K-Means (one pass):

- Assignment: O(N * K) where N = number of points, K = number of clusters

- Update: O(N * K)

- Total: O(N * K * I) where I = number of iterations (usually 5-20)

Example: With N=200 HTF bars, K=5 clusters, I=20 iterations:

200 * 5 * 20 = 20,000 operations (executes quickly)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📖 USER GUIDE

Quick Start

1. Adding the Indicator

TradingView → Indicators → Favorites → MTF K-Means Price Regimes

Or copy the code from mtf_kmeans_price_regimes.pine into Pine Editor.

2. First Launch

When adding the indicator to the chart, you'll see a table in the upper right corner:

┌─────────────────────────┐

│ Status │ Collecting HTF │

├─────────────────────────┤

│ Collected│ 15 / 50 │

└─────────────────────────┘

This means the indicator is accumulating history from the higher timeframe. Wait until the counter reaches the minimum (default 50 bars for K=5).

3. Active Operation

After data collection is complete, the main table with cluster information will appear:

┌────┬──────┬──────┬──────┬──────────────┬────────┐

│ ID │ RSI │ ATR% │ ΔP% │ Description │Current │

├────┼──────┼──────┼──────┼──────────────┼────────┤

│ 1 │ 68.5 │ 2.15 │ 1.2 │ High Vol,Bull│ │

│ 2 │ 52.3 │ 0.85 │ 0.1 │ Low Vol,Flat │ ► │

│ 3 │ 35.2 │ 1.95 │ -1.5 │ High Vol,Bear│ │

└────┴──────┴──────┴──────┴──────────────┴────────┘

The arrow ► indicates the current active regime. Chart bars are colored with the corresponding cluster color.

Customizing for Your Strategy

Choosing Higher Timeframe (HTF)

Rule: HTF should be at least 4 times higher than the working timeframe.

| Working TF | Recommended HTF |

|------------|-----------------|

| 1 min | 15 min - 1H |

| 5 min | 1H - 4H |

| 15 min | 4H - D |

| 1H | D - W |

| 4H | D - W |

| D | W - M |

HTF Selection Effect:

Lower HTF (closer to working TF): More sensitive, frequently changing classification

Higher HTF (much larger than working TF): More stable, long-term regime assessment

Number of Clusters (K)

K = 2-3: Rough division (e.g., "uptrend", "downtrend", "flat")

K = 4-5: Optimal for most cases (DEFAULT: 5)

K = 6-8: Detailed segmentation (requires more data)

K = 9-10: Very fine division (only for long-term analysis with large windows)

Important constraint:

clusterLookback ≥ numClusters * 10

I.e., for K=5 you need at least 50 HTF bars, for K=10 — at least 100 bars.

Clustering Depth (clusterLookback)

This is the rolling window size for building the model.

50-100 HTF bars: Fast adaptation to market changes

200 HTF bars: Optimal balance (DEFAULT)

500-1000 HTF bars: Long-term, stable model

If you get an "Insufficient data" error:

Decrease clusterLookback

Or select a lower HTF (e.g., "4H" instead of "D")

Or decrease numClusters

Color Scheme

Default 10 colors:

Red → Often: strong bearish, high volatility

Orange → Transition, medium volatility

Yellow → Neutral, decreasing activity

Green → Often: strong bullish, high volatility

Blue → Medium bullish, medium volatility

Purple → Oversold, possible reversal

Fuchsia → Overbought, possible reversal

Lime → Strong upward momentum

Aqua → Consolidation, low volatility

White → Undefined regime (rare)

Important: Cluster colors are assigned randomly at each model recalculation! Don't rely on "red = bearish". Instead, look at the description in the table (RSI, ATR%, ΔP%).

You can customize colors in the "Colors" settings section.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚙️ INDICATOR PARAMETERS

Main Parameters

Higher Timeframe (htf)

Type: Timeframe selection

Default: "D" (daily)

Description: Timeframe on which the clustering model is built

Recommendation: At least 4 times larger than your working TF

Clustering Depth (clusterLookback)

Type: Integer

Range: 50 - 2000

Default: 200

Description: Number of HTF bars for building the model (rolling window size)

Recommendation:

- Increase for more stable long-term model

- Decrease for fast adaptation or if there's insufficient historical data

Number of Clusters (K) (numClusters)

Type: Integer

Range: 2 - 10

Default: 5

Description: Number of market regimes the algorithm will identify

Recommendation:

- K=3-4 for simple strategies (trending/ranging)

- K=5-6 for universal strategies

- K=7-10 only when clusterLookback ≥ 100*K

Max K-Means Iterations (maxIterations)

Type: Integer

Range: 5 - 50

Default: 20

Description: Maximum number of algorithm iterations

Recommendation:

- 10-20 is sufficient for most cases

- Increase to 30-50 if using K > 7

Feature Parameters

RSI Period (rsiLength)

Type: Integer

Default: 14

Description: Period for RSI calculation (overbought/oversold feature)

Recommendation:

- 14 — standard

- 7-10 — more sensitive

- 20-25 — more smoothed

ATR Period (atrLength)

Type: Integer

Default: 14

Description: Period for ATR calculation (volatility feature)

Recommendation: Usually kept equal to rsiLength

Price Change Period (pcLength)

Type: Integer

Default: 5

Description: Period for percentage price change calculation (trend feature)

Recommendation:

- 3-5 — short-term trend

- 10-20 — medium-term trend

Visualization

Show Info Panel (showDashboard)

Type: Checkbox

Default: true

Description: Enables/disables the information table on the chart

Cluster Color 1-10

Type: Color selection

Description: Customize colors for visual cluster distinction

Recommendation: Use contrasting colors for better readability

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📊 INTERPRETING RESULTS

Reading the Information Table

┌────┬──────┬──────┬──────┬──────────────┬────────┐

│ ID │ RSI │ ATR% │ ΔP% │ Description │Current │

├────┼──────┼──────┼──────┼──────────────┼────────┤

│ 1 │ 68.5 │ 2.15 │ 1.2 │ High Vol,Bull│ │

│ 2 │ 52.3 │ 0.85 │ 0.1 │ Low Vol,Flat │ ► │

│ 3 │ 35.2 │ 1.95 │ -1.5 │ High Vol,Bear│ │

│ 4 │ 45.0 │ 1.20 │ -0.3 │ Low Vol,Bear │ │

│ 5 │ 72.1 │ 3.05 │ 2.8 │ High Vol,Bull│ │

└────┴──────┴──────┴──────┴──────────────┴────────┘

"ID" Column

Cluster number (1-K). Order doesn't matter.

"RSI" Column

Average RSI value in the cluster (0-100):

< 30: Oversold zone

30-45: Bearish sentiment

45-55: Neutral zone

55-70: Bullish sentiment

> 70: Overbought zone

"ATR%" Column

Average volatility in the cluster (as % of price):

< 1%: Low volatility (consolidation, narrow range)

1-2%: Normal volatility

2-3%: Elevated volatility

> 3%: High volatility (strong movements, impulses)

Compared to the average volatility across all clusters to determine "High Vol" or "Low Vol".

"ΔP%" Column

Average price change in the cluster (in % over pcLength period):

> +0.05%: Bullish regime

-0.05% ... +0.05%: Flat (sideways movement)

< -0.05%: Bearish regime

"Description" Column

Automatic interpretation:

"High Vol, Bull" → Strong upward momentum, high activity

"Low Vol, Flat" → Consolidation, narrow range, uncertainty

"High Vol, Bear" → Strong decline, panic, high activity

"Low Vol, Bull" → Slow growth, low activity

"Low Vol, Bear" → Slow decline, low activity

"Current" Column

Arrow ► shows which cluster the last closed bar of your working timeframe is in.

Typical Cluster Patterns

Example 1: Trend/Flat Division (K=3)

Cluster 1: RSI=65, ATR%=2.5, ΔP%=+1.5 → Bullish trend

Cluster 2: RSI=50, ATR%=0.8, ΔP%=0.0 → Flat/Consolidation

Cluster 3: RSI=35, ATR%=2.3, ΔP%=-1.4 → Bearish trend

Strategy: Open positions when regime changes Flat → Trend, avoid flat.

Example 2: Volatility Breakdown (K=5)

Cluster 1: RSI=72, ATR%=3.5, ΔP%=+2.5 → Strong bullish impulse (high risk)

Cluster 2: RSI=60, ATR%=1.5, ΔP%=+0.8 → Moderate bullish (optimal entry point)

Cluster 3: RSI=50, ATR%=0.7, ΔP%=0.0 → Flat

Cluster 4: RSI=40, ATR%=1.4, ΔP%=-0.7 → Moderate bearish

Cluster 5: RSI=28, ATR%=3.2, ΔP%=-2.3 → Strong bearish impulse (panic)

Strategy: Enter in Cluster 2 or 4, avoid extremes (1, 5).

Example 3: Mixed Regimes (K=7+)

With large K, clusters can represent condition combinations:

High RSI + Low volatility → "Quiet overbought"

Neutral RSI + High volatility → "Uncertainty with high activity"

Etc.

Requires individual analysis of each cluster.

Regime Changes

Important signal: Transition from one cluster to another!

Trading situation examples:

Flat → Bullish trend → Buy signal

Bullish trend → Flat → Take profit, close longs

Flat → Bearish trend → Sell signal

Bearish trend → Flat → Close shorts, wait

You can build a trading system based on the current active cluster and transitions between them.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💡 USAGE EXAMPLES

Example 1: Scalping with HTF Filter

Task: Scalping on 5-minute charts, but only enter in the direction of the daily regime.

Settings:

Working TF: 5 min

HTF: D (daily)

K: 3 (simple division)

clusterLookback: 100

Logic:

IF current cluster = "Bullish" (ΔP% > 0.5)

→ Look for long entry points on 5M

IF current cluster = "Bearish" (ΔP% < -0.5)

→ Look for short entry points on 5M

IF current cluster = "Flat"

→ Don't trade / reduce risk

Example 2: Swing Trading with Volatility Filtering

Task: Swing trading on 4H, enter only in regimes with medium volatility.

Settings:

Working TF: 4H

HTF: D (daily)

K: 5

clusterLookback: 200

Logic:

Allowed clusters for entry:

- ATR% from 1.5% to 2.5% (not too quiet, not too chaotic)

- ΔP% with clear direction (|ΔP%| > 0.5)

Prohibited clusters:

- ATR% > 3% → Too risky (possible gaps, sharp reversals)

- ATR% < 1% → Too quiet (small movements, commissions eat profit)

Example 3: Portfolio Rotation

Task: Managing a portfolio of multiple assets, allocate capital depending on regimes.

Settings:

Working TF: D (daily)

HTF: W (weekly)

K: 4

clusterLookback: 100

Logic:

For each asset in portfolio:

IF regime = "Strong trend + Low volatility"

→ Increase asset weight in portfolio (40-50%)

IF regime = "Medium trend + Medium volatility"

→ Standard weight (20-30%)

IF regime = "Flat" or "High volatility without trend"

→ Minimum weight or exclude (0-10%)

Example 4: Combining with Other Indicators

MTF K-Means as a filter:

Main strategy: MA Crossover

Filter: MTF K-Means on higher TF

Rule:

IF MA_fast > MA_slow AND Cluster = "Bullish regime"

→ LONG

IF MA_fast < MA_slow AND Cluster = "Bearish regime"

→ SHORT

ELSE

→ Don't trade (regime doesn't confirm signal)

This dramatically reduces false signals in unsuitable market conditions.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📈 OPTIMIZATION RECOMMENDATIONS

Optimal Settings for Different Styles

Day Trading

Working TF: 5M - 15M

HTF: 1H - 4H

numClusters: 4-5

clusterLookback: 100-150

Swing Trading

Working TF: 1H - 4H

HTF: D

numClusters: 5-6

clusterLookback: 150-250

Position Trading

Working TF: D

HTF: W - M

numClusters: 4-5

clusterLookback: 100-200

Scalping

Working TF: 1M - 5M

HTF: 15M - 1H

numClusters: 3-4

clusterLookback: 50-100

Backtesting

To evaluate effectiveness:

Load historical data (minimum 2x clusterLookback HTF bars)

Apply the indicator with your settings

Study cluster change history:

- Do changes coincide with actual trend transitions?

- How often do false signals occur?

Optimize parameters:

- If too much noise → increase HTF or clusterLookback

- If reaction too slow → decrease HTF or increase numClusters

Combining with Other Techniques

Regime-Based Approach:

MTF K-Means (regime identification)

↓

+---+---+---+

| | | |

v v v v

Trend Flat High_Vol Low_Vol

↓ ↓ ↓ ↓

Strategy_A Strategy_B Don't_trade

Examples:

Trend: Use trend-following strategies (MA crossover, Breakout)

Flat: Use mean-reversion strategies (RSI, Bollinger Bands)

High volatility: Reduce position sizes, widen stops

Low volatility: Expect breakout, don't open positions inside range

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📞 SUPPORT

Report an Issue

If you found a bug or have a suggestion for improvement:

Describe the problem in as much detail as possible

Specify your indicator settings

Attach a screenshot (if possible)

Specify the asset and timeframe where the problem is observed

Clustering

Lorentzian Key Support and Resistance Level Detector [mishy]🧮 Lorentzian Key S/R Levels Detector

Advanced Support & Resistance Detection Using Mathematical Clustering

The Problem

Traditional S/R indicators fail because they're either subjective (manual lines), rigid (fixed pivots), or break when price spikes occur. Most importantly, they don't tell you where prices actually spend time, just where they touched briefly.

The Solution: Lorentzian Distance Clustering

This indicator introduces a novel approach by using Lorentzian distance instead of traditional Euclidean distance for clustering. This is groundbreaking for financial data analysis.

Data Points Clustering:

🔬 Why Euclidean Distance Fails in Trading

Traditional K-means uses Euclidean distance:

• Formula: distance = (price_A - price_B)²

• Problem: Squaring amplifies differences exponentially

• Real impact: One 5% price spike has 25x more influence than a 1% move

• Result: Clusters get pulled toward outliers, missing real support/resistance zones

Example scenario:

Prices: ← flash spike

Euclidean: Centroid gets dragged toward 150

Actual S/R zone: Around 100 (where prices actually trade)

⚡ Lorentzian Distance: The Game Changer

Our approach uses Lorentzian distance:

• Formula: distance = log(1 + (price_difference)² / σ²)

• Breakthrough: Logarithmic compression keeps outliers in check

• Real impact: Large moves still matter, but don't dominate

• Result: Clusters focus on where prices actually spend time

Same example with Lorentzian:

Prices: ← flash spike

Lorentzian: Centroid stays near 100 (real trading zone)

Outlier (150): Acknowledged but not dominant

🧠 Adaptive Intelligence

The σ parameter isn't fixed,it's calculated from market disturbance/entropy:

• High volatility: σ increases, making algorithm more tolerant of large moves

• Low volatility: σ decreases, making algorithm more sensitive to small changes

• Self-calibrating: Adapts to any instrument or market condition automatically

Why this matters: Traditional methods treat a 2% move the same whether it's in a calm or volatile market. Lorentzian adapts the sensitivity based on current market behavior.

🎯 Automatic K-Selection (Elbow Method)

Instead of guessing how many S/R levels to draw, the indicator:

• Tests 2-6 clusters and calculates WCSS (tightness measure)

• Finds the "elbow" - where adding more clusters stops helping much

• Uses sharpness calculation to pick the optimal number automatically

Result: Perfect balance between detail and clarity.

How It Works

1. Collect recent closing prices

2. Calculate entropy to adapt to current market volatility

3. Cluster prices using Lorentzian K-means algorithm

4. Auto-select optimal cluster count via statistical analysis

5. Draw levels at cluster centers with deviation bands

📊 Manual K-Selection Guide (Using WCSS & Sharpness Analysis)

When you disable auto-selection, use both WCSS and Sharpness metrics from the analysis table to choose manually:

What WCSS tells you:

• Lower WCSS = tighter clusters = better S/R levels

• Higher WCSS = scattered clusters = weaker levels

What Sharpness tells you:

• Higher positive values = optimal elbow point = best K choice

• Lower/negative values = poor elbow definition = avoid this K

• Measures the "sharpness" of the WCSS curve drop-off

Decision strategy using both metrics:

K=2: WCSS = 150.42 | Sharpness = - | Selected =

K=3: WCSS = 89.15 | Sharpness = 22.04 | Selected = ✓ ← Best choice

K=4: WCSS = 76.23 | Sharpness = 1.89 | Selected =

K=5: WCSS = 73.91 | Sharpness = 1.43 | Selected =

Quick decision rules:

• Pick K with highest positive Sharpness (indicates optimal elbow)

• Confirm with significant WCSS drop (30%+ reduction is good)

• Avoid K values with negative or very low Sharpness (<1.0)

• K=3 above shows: Big WCSS drop (41%) + High Sharpness (22.04) = Perfect choice

Why this works:

The algorithm finds the "elbow" where adding more clusters stops being useful. High Sharpness pinpoints this elbow mathematically, while WCSS confirms the clustering quality.

Elbow Method Visualization:

Traditional clustering problems:

❌ Price spikes distort results

❌ Fixed parameters don't adapt

❌ Manual tuning is subjective

❌ No way to validate choices

Lorentzian solution:

☑️ Outlier-resistant distance metric

☑️ Entropy-based adaptation to volatility

☑️ Automatic optimal K selection

☑️ Statistical validation via WCSS & Sharpness

Features

Visual:

• Color-coded levels (red=highest resistance, green=lowest support)

• Optional deviation bands showing cluster spread

• Strength scores on labels: Each cluster shows a reliability score.

• Higher scores (0.8+) = very strong S/R levels with tight price clustering

• Lower scores (0.6-0.7) = weaker levels, use with caution

• Based on cluster tightness and data point density

• Clean line extensions and labels

Analytics:

• WCSS analysis table showing why K was chosen

• Cluster metrics and statistics

• Real-time entropy monitoring

Control:

• Auto/manual K selection toggle

• Customizable sample size (20-500 bars)

• Show/hide bands and metrics tables

The Result

You get mathematically validated S/R levels that focus on where prices actually cluster, not where they randomly spiked. The algorithm adapts to market conditions and removes guesswork from level selection.

Best for: Traders who want objective, data-driven S/R levels without manual chart analysis.

Credits: This script is for educational purposes and is inspired by the work of @ThinkLogicAI and an amazing mentor @DskyzInvestments . It demonstrates how Lorentzian geometrical concepts can be applied not only in ML classification but also quite elegantly in clustering.

Machine Learning Key Levels [AlgoAlpha]🟠 OVERVIEW

This script plots Machine Learning Key Levels on your chart by detecting historical pivot points and grouping them using agglomerative clustering to highlight price levels with the most past reactions. It combines a pivot detection, hierarchical clustering logic, and an optional silhouette method to automatically select the optimal number of key levels, giving you an adaptive way to visualize price zones where activity concentrated over time.

🟠 CONCEPTS

Agglomerative clustering is a bottom-up method that starts by treating each pivot as its own cluster, then repeatedly merges the two closest clusters based on the average distance between their members until only the desired number of clusters remain. This process creates a hierarchy of groupings that can flexibly describe patterns in how price reacts around certain levels. This offers an advantage over K-means clustering, since the number of clusters does not need to be predefined. In this script, it uses an average linkage approach, where distance between clusters is computed as the average pairwise distance of all contained points.

The script finds pivot highs and lows over a set lookback period and saves them in a buffer controlled by the Pivot Memory setting. When there are at least two pivots, it groups them using agglomerative clustering: it starts with each pivot as its own group and keeps merging the closest pairs based on their average distance until the desired number of clusters is left. This number can be fixed or chosen automatically with the silhouette method, which checks how well each point fits in its cluster compared to others (higher scores mean cleaner separation). Once clustering finishes, the script takes the average price of each cluster to create key levels, sorts them, and draws horizontal lines with labels and colors showing their strength. A metrics table can also display details about the clusters to help you understand how the levels were calculated.

🟠 FEATURES

Agglomerative clustering engine with average linkage to merge pivots into level groups.

Dynamic lines showing each cluster’s price level for clarity.

Labels indicating level strength either as percent of all pivots or raw counts.

A metrics table displaying pivot count, cluster count, silhouette score, and cluster size data.

Optional silhouette-based auto-selection of cluster count to adaptively find the best fit.

🟠 USAGE

Add the indicator to any chart. Choose how far back to detect pivots using Pivot Length and set Pivot Memory to control how many are kept for clustering (more pivots give smoother levels but can slow performance). If you want the script to pick the number of levels automatically, enable Auto No. Levels ; otherwise, set Number of Levels . The colored horizontal lines represent the calculated key levels, and circles show where pivots occurred colored by which cluster they belong to. The labels beside each level indicate its strength, so you can see which levels are supported by more pivots. If Show Metrics Table is enabled, you will see statistics about the clustering in the corner you selected. Use this tool to spot areas where price often reacts and to plan entries or exits around levels that have been significant over time. Adjust settings to better match volatility and history depth of your instrument.

Dynamic Volume Clusters with Retest Signals (Zeiierman)█ Overview

The Dynamic Volume Clusters with Retest Signals indicator is designed to detect key Volume Clusters and provide Retest Signals. This tool is specifically engineered for traders looking to capitalize on volume-based trends, reversals, and key price retest points.

The indicator seamlessly combines volume analysis, dynamic cluster calculations, and retest signal logic to present a comprehensive trading framework. It adapts to market conditions, identifying clusters of volume activity and signaling when the price retests critical zones.

█ How It Works

⚪ Volume Cluster Detection

The indicator dynamically calculates volume clusters by analyzing the highest and lowest price points within a specified lookback period.

Cluster Logic:

Bright Lines (Strong Red/Green):

These indicate that the price has frequently revisited these levels, creating a dense cluster.

Such areas serve as support or resistance, where significant historical trading has occurred, often acting as barriers to price movement.

Traders should consider these levels as potential reversal zones or consolidation points.

Faded or Darker Lines:

These lines indicate areas where the price has less historical activity, suggesting weaker clustering.

These zones have less market memory and are more likely to break, supporting trend continuation and rapid price movement.

⚪ Candle Color Logic (Market Memory)

Blue Candles (High Cluster Density):

Candles turn blue when the price has revisited a particular area many times.

This signals a highly clustered zone, likely to act as a barrier, creating consolidation or range phases.

These areas indicate strong market memory, potentially rejecting price attempts to break through.

Green or Red Candles (Low Cluster Density):

Once the price breaks out of these dense clusters, the candles turn green (bullish) or red (bearish).

This suggests the price has moved into a less clustered territory, where the path forward is clearer and trends are likely to extend without immediate resistance.

⚪ Retest Signal Logic

The indicator identifies critical retest points where the price crosses a cluster boundary and then reverses. These points are essential for traders looking to catch continuation or reversal setups.

⚪ Dynamic Price Clustering

The indicator dynamically adapts the clustering logic based on price movement and volume shifts.

Uses a dynamic moving average (VPMA) to maintain adaptive cluster levels.

Integrates a Kalman Filter for smoothing, reducing noise, and improving trend clarity.

Automatically updates as new data is received, keeping the clusters relevant in real-time.

█ How to Use

⚪ Trend Following & Reversal Detection

Use Retest signals to identify potential trend continuation or reversal points.

⚪ Trading Volume Clusters and Market Memory

Identify Key Zones:

Focus on bright, saturated cluster lines (strong red or green) as they indicate high market memory, where price has spent significant time in the past.

These zones are likely to exhibit a more choppy market. Apply range or mean reversion strategies.

Spot Potential Breakouts:

Faded or darker cluster lines indicate areas of low market memory, where the price has moved quickly and spent less time.

Use these areas to identify possible trend setups, as they represent lower resistance to price movement.

⚪ Interpreting Candle Colors for Market Phases

Blue Candles (High Cluster Density):

When candles turn blue, it signals that the price has revisited this area multiple times, creating a dense cluster.

These zones often trap price movement, leading to consolidations or range phases.

Use these areas as caution zones, where price can slow down or reverse.

Green or Red Candles (Low Cluster Density):

Once the price breaks out of these clustered zones, the candles turn green (bullish) or red (bearish), indicating lower market memory.

This signals a trend initiation with less immediate resistance, ideal for momentum and breakout trades.

Use these signals to identify emerging trends and ride the momentum.

█ Settings

Range Lookback Period: Sets the number of bars for calculating the range.

Zone Width (% of Range): Determines how wide the volume clusters are relative to the calculated range.

Volume Line Colors: Customize the appearance of bullish and bearish lines.

Retest Signals: Toggle the appearance of Triangle Up/Down retest markers.

Minimum Bars for Retest: Define the minimum number of bars required before a retest is valid.

Maximum Bars for Retest: Set the maximum number of bars within which a retest can occur.

Price Cluster Period: Adjusts the sensitivity of the dynamic clustering logic.

Cluster Confirmation: Controls how tightly the clusters respond to price action.

Price Cluster Start/Peak: Sets the minimum and maximum touches required to fully form a cluster.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Market Flow Volatility Oscillator (AiBitcoinTrend)The Market Flow Volatility Oscillator (AiBitcoinTrend) is a cutting-edge technical analysis tool designed to evaluate and classify market volatility regimes. By leveraging Gaussian filtering and clustering techniques, this indicator provides traders with clear insights into periods of high and low volatility, helping them adapt their strategies to evolving market conditions. Built for precision and clarity, it combines advanced mathematical models with intuitive visual feedback to identify trends and volatility shifts effectively.

👽 How the Indicator Works

👾 Volatility Classification with Gaussian Filtering

The indicator detects volatility levels by applying Gaussian filters to the price series. Gaussian filters smooth out noise while preserving significant price movements. Traders can adjust the smoothing levels using sigma parameters, enabling greater flexibility:

Low Sigma: Emphasizes short-term volatility.

High Sigma: Captures broader trends with reduced sensitivity to small fluctuations.

👾 Clustering Algorithm for Regime Detection

The core of this indicator is its clustering model, which classifies market conditions into two distinct regimes:

Low Volatility Regime: Calm periods with reduced market activity.

High Volatility Regime: Intense periods with heightened price movements.

The clustering process works as follows:

A rolling window of data is analyzed to calculate the standard deviation of price returns.

Two cluster centers are initialized using the 25th and 75th percentiles of the data distribution.

Each price volatility value is assigned to the nearest cluster based on its distance to the centers.

The cluster centers are refined iteratively, providing an accurate and adaptive classification.

👾 Oscillator Generation with Slope R-Values

The indicator computes Gaussian filter slopes to generate oscillators that visualize trends:

Oscillator Low: Captures low-frequency market behavior.

Oscillator High: Tracks high-frequency, faster-changing trends.

The slope is measured using the R-value of the linear regression fit, scaled and adjusted for easier interpretation.

👽 Applications

👾 Trend Trading

When the oscillator rises above 0.5, it signals potential bullish momentum, while dips below 0.5 suggest bearish sentiment.

👾 Pullback Detection

When the oscillator peaks, especially in overbought or oversold zones, provide early warnings of potential reversals.

👽 Indicator Settings

👾 Oscillator Settings

Sigma Low/High: Controls the smoothness of the oscillators.

Smaller Values: React faster to price changes but introduce more noise.

Larger Values: Provide smoother signals with longer-term insights.

👾 Window Size and Refit Interval

Window Size: Defines the rolling period for cluster and volatility calculations.

Shorter windows: adapt faster to market changes.

Longer windows: produce stable, reliable classifications.

Disclaimer: This information is for entertainment purposes only and does not constitute financial advice. Please consult with a qualified financial advisor before making any investment decisions.

Correlation Clusters [LuxAlgo]The Correlation Clusters is a machine learning tool that allows traders to group sets of tickers with a similar correlation coefficient to a user-set reference ticker.

The tool calculates the correlation coefficients between 10 user-set tickers and a user-set reference ticker, with the possibility of forming up to 10 clusters.

🔶 USAGE

Applying clustering methods to correlation analysis allows traders to quickly identify which set of tickers are correlated with a reference ticker, rather than having to look at them one by one or using a more tedious approach such as correlation matrices.

Tickers belonging to a cluster may also be more likely to have a higher mutual correlation. The image above shows the detailed parts of the Correlation Clusters tool.

The correlation coefficient between two assets allows traders to see how these assets behave in relation to each other. It can take values between +1.0 and -1.0 with the following meaning

Value near +1.0: Both assets behave in a similar way, moving up or down at the same time

Value close to 0.0: No correlation, both assets behave independently

Value near -1.0: Both assets have opposite behavior when one moves up the other moves down, and vice versa

There is a wide range of trading strategies that make use of correlation coefficients between assets, some examples are:

Pair Trading: Traders may wish to take advantage of divergences in the price movements of highly positively correlated assets; even highly positively correlated assets do not always move in the same direction; when assets with a correlation close to +1.0 diverge in their behavior, traders may see this as an opportunity to buy one and sell the other in the expectation that the assets will return to the likely same price behavior.

Sector rotation: Traders may want to favor some sectors that are expected to perform in the next cycle, tracking the correlation between different sectors and between the sector and the overall market.

Diversification: Traders can aim to have a diversified portfolio of uncorrelated assets. From a risk management perspective, it is useful to know the correlation between the assets in your portfolio, if you hold equal positions in positively correlated assets, your risk is tilted in the same direction, so if the assets move against you, your risk is doubled. You can avoid this increased risk by choosing uncorrelated assets so that they move independently.

Hedging: Traders may want to hedge positions with correlated assets, from a hedging perspective, if you are long an asset, you can hedge going long a negatively correlated asset or going short a positively correlated asset.

Grouping different assets with similar behavior can be very helpful to traders to avoid over-exposure to those assets, traders may have multiple long positions on different assets as a way of minimizing overall risk when in reality if those assets are part of the same cluster traders are maximizing their risk by taking positions on assets with the same behavior.

As a rule of thumb, a trader can minimize risk via diversification by taking positions on assets with no correlations, the proposed tool can effectively show a set of uncorrelated candidates from the reference ticker if one or more clusters centroids are located near 0.

🔶 DETAILS

K-means clustering is a popular machine-learning algorithm that finds observations in a data set that are similar to each other and places them in a group.

The process starts by randomly assigning each data point to an initial group and calculating the centroid for each. A centroid is the center of the group. K-means clustering forms the groups in such a way that the variances between the data points and the centroid of the cluster are minimized.

It's an unsupervised method because it starts without labels and then forms and labels groups itself.

🔹 Execution Window

In the image above we can see how different execution windows provide different correlation coefficients, informing traders of the different behavior of the same assets over different time periods.

Users can filter the data used to calculate correlations by number of bars, by time, or not at all, using all available data. For example, if the chart timeframe is 15m, traders may want to know how different assets behave over the last 7 days (one week), or for an hourly chart set an execution window of one month, or one year for a daily chart. The default setting is to use data from the last 50 bars.

🔹 Clusters

On this graph, we can see different clusters for the same data. The clusters are identified by different colors and the dotted lines show the centroids of each cluster.

Traders can select up to 10 clusters, however, do note that selecting 10 clusters can lead to only 4 or 5 returned clusters, this is caused by the machine learning algorithm not detecting any more data points deviating from already detected clusters.

Traders can fine-tune the algorithm by changing the 'Cluster Threshold' and 'Max Iterations' settings, but if you are not familiar with them we advise you not to change these settings, the defaults can work fine for the application of this tool.

🔹 Correlations

Different correlations mean different behaviors respecting the same asset, as we can see in the chart above.

All correlations are found against the same asset, traders can use the chart ticker or manually set one of their choices from the settings panel. Then they can select the 10 tickers to be used to find the correlation coefficients, which can be useful to analyze how different types of assets behave against the same asset.

🔶 SETTINGS

Execution Window Mode: Choose how the tool collects data, filter data by number of bars, time, or no filtering at all, using all available data.

Execute on Last X Bars: Number of bars for data collection when the 'Bars' execution window mode is active.

Execute on Last: Time window for data collection when the `Time` execution window mode is active. These are full periods, so `Day` means the last 24 hours, `Week` means the last 7 days, and so on.

🔹 Clusters

Number of Clusters: Number of clusters to detect up to 10. Only clusters with data points are displayed.

Cluster Threshold: Number used to compare a new centroid within the same cluster. The lower the number, the more accurate the centroid will be.

Max Iterations: Maximum number of calculations to detect a cluster. A high value may lead to a timeout runtime error (loop takes too long).

🔹 Ticker of Reference

Use Chart Ticker as Reference: Enable/disable the use of the current chart ticker to get the correlation against all other tickers selected by the user.

Custom Ticker: Custom ticker to get the correlation against all the other tickers selected by the user.

🔹 Correlation Tickers

Select the 10 tickers for which you wish to obtain the correlation against the reference ticker.

🔹 Style

Text Size: Select the size of the text to be displayed.

Display Size: Select the size of the correlation chart to be displayed, up to 500 bars.

Box Height: Select the height of the boxes to be displayed. A high height will cause overlapping if the boxes are close together.

Clusters Colors: Choose a custom colour for each cluster.

RSI K-Means Clustering [UAlgo]The "RSI K-Means Clustering " indicator is a technical analysis tool that combines the Relative Strength Index (RSI) with K-means clustering techniques. This approach aims to provide more nuanced insights into market conditions by categorizing RSI values into overbought, neutral, and oversold clusters.

The indicator adjusts these clusters dynamically based on historical RSI data, allowing for more adaptive and responsive thresholds compared to traditional fixed levels. By leveraging K-means clustering, the indicator identifies patterns in RSI behavior, which can help traders make more informed decisions regarding market trends and potential reversals.

🔶 Key Features

K-means Clustering: The indicator employs K-means clustering, an unsupervised machine learning technique, to dynamically determine overbought, neutral, and oversold levels based on historical RSI data.

User-Defined Inputs: You can customize various aspects of the indicator's behavior, including:

RSI Source: Select the data source used for RSI calculation (e.g., closing price).

RSI Length: Define the period length for RSI calculation.

Training Data Size: Specify the number of historical RSI values used for K-means clustering.

Number of K-means Iterations: Set the number of iterations performed by the K-means algorithm to refine cluster centers.

Overbought/Neutral/Oversold Levels: You can define initial values for these levels, which will be further optimized through K-means clustering.

Alerts: The indicator can generate alerts for various events, including:

Trend Crossovers: Alerts for when the RSI crosses above/below the neutral zone, signaling potential trend changes.

Overbought/Oversold: Alerts when the RSI reaches the dynamically determined overbought or oversold thresholds.

Reversals: Alerts for potential trend reversals based on RSI crossing above/below the calculated overbought/oversold levels.

RSI Classification: Alerts based on the current RSI classification (ranging, uptrend, downtrend).

🔶 Interpreting Indicator

Adjusted RSI Value: The primary plot represents the adjusted RSI value, calculated based on the relative position of the current RSI compared to dynamically adjusted overbought and oversold levels. This value provides an intuitive measure of the market's momentum. The final overbought, neutral, and oversold levels are determined by K-means clustering and are displayed as horizontal lines. These levels serve as dynamic support and resistance points, indicating potential reversal zones.

Classification Symbols : The "RSI K-Means Clustering " indicator uses specific symbols to classify the current market condition based on the position of the RSI value relative to dynamically determined clusters. These symbols provide a quick visual reference to help traders understand the prevailing market sentiment. Here's a detailed explanation of each classification symbol:

Ranging Classification ("R")

This symbol appears when the RSI value is closest to the neutral threshold compared to the overbought or oversold thresholds. It indicates a ranging market, where the price is moving sideways without a clear trend direction. In this state, neither buyers nor sellers are in control, suggesting a period of consolidation or indecision. This is often seen as a time to wait for a breakout or reversal signal before taking a position.

Up-Trend Classification ("↑")

The up-trend symbol, represented by an upward arrow, is displayed when the RSI value is closer to the overbought threshold than to the neutral or oversold thresholds. This classification suggests that the market is in a bullish phase, with buying pressure outweighing selling pressure. Traders may consider this as a signal to enter or hold long positions, as the price is likely to continue rising until the market reaches an overbought condition.

Down-Trend Classification ("↓")

The down-trend symbol, depicted by a downward arrow, appears when the RSI value is nearest to the oversold threshold. This indicates a bearish market condition, where selling pressure dominates. The market is likely experiencing a downward movement, and traders might view this as an opportunity to enter or hold short positions. This symbol serves as a warning of potential further declines, especially if the RSI continues to move toward the oversold level.

Bullish Reversal ("▲")

This signal occurs when the RSI value crosses above the oversold threshold. It indicates a potential shift from a downtrend to an uptrend, suggesting that the market may start to move higher. Traders might use this signal as an opportunity to enter long positions.

Bearish Reversal ("▼")

This signal appears when the RSI value crosses below the overbought threshold. It suggests a possible transition from an uptrend to a downtrend, indicating that the market may begin to decline. This signal can alert traders to consider entering short positions or taking profits on long positions.

These classification symbols are plotted near the adjusted RSI line, with their positions adjusted based on the standard deviation and a distance multiplier. This placement helps in visualizing the classification's strength and ensuring clarity in the indicator's presentation. By monitoring these symbols, traders can quickly assess the market's state and make more informed trading decisions.

🔶 Disclaimer

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

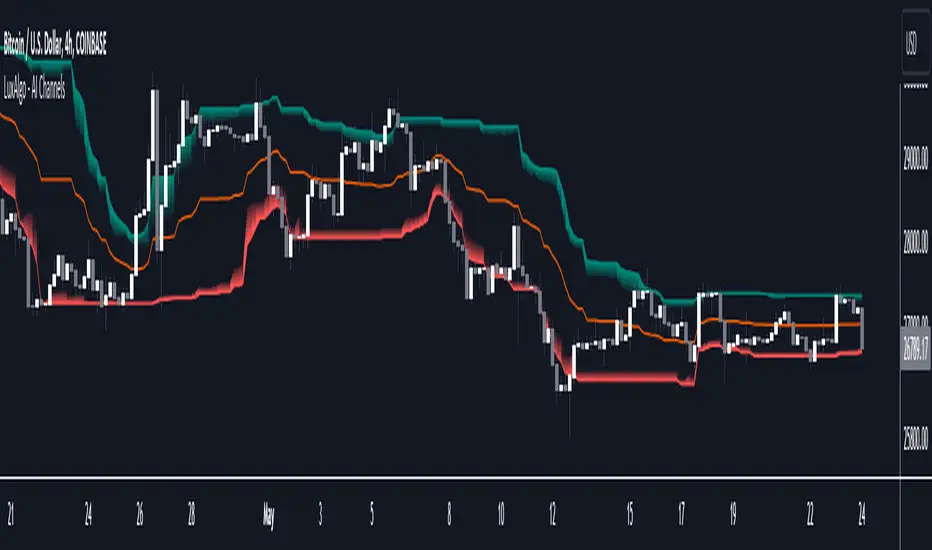

AI Channels (Clustering) [LuxAlgo]The AI Channels indicator is constructed based on rolling K-means clustering, a common machine learning method used for clustering analysis. These channels allow users to determine the direction of the underlying trends in the price.

We also included an option to display the indicator as a trailing stop from within the settings.

🔶 USAGE

Each channel extremity allows users to determine the current trend direction. Price breaking over the upper extremity suggesting an uptrend, and price breaking below the lower extremity suggesting a downtrend. Using a higher Window Size value will return longer-term indications.

The "Clusters" setting allows users to control how easy it is for the price to break an extremity, with higher values returning extremities further away from the price.

The "Denoise Channels" is enabled by default and allows to see less noisy extremities that are more coherent with the detected trend.

Users who wish to have more focus on a detected trend can display the indicator as a trailing stop.

🔹 Centroid Dispersion Areas

Each extremity is made of one area. The width of each area indicates how spread values within a cluster are around their centroids. A wider area would suggest that prices within a cluster are more spread out around their centroid, as such one could say that it is indicative of the volatility of a cluster.

Wider areas around a specific extremity can indicate a larger and more spread-out amount of prices within the associated cluster. In practice price entering an area has a higher chance to break an associated extremity.

🔶 DETAILS

The indicator performs K-means clustering over the most recent Window Size prices, finding a number of user-specified clusters. See here to find more information on cluster detection.

The channel extremities are returned as the centroid of the lowest, average, and highest price clusters.

K-means clustering can be computationally expensive and as such we allow users to determine the maximum number of iterations used to find the centroids as well as the number of most historical bars to perform the indicator calculation. Do note that increasing the calculation window of the indicator as well as the number of clusters will return slower results.

🔶 SETTINGS

Window Size: Amount of most recent prices to use for the calculation of the indicator.

Clusters": Amount of clusters detected for the calculation of the indicator.

Denoise Channels: When enabled, return less noisy channels extremities, disabling this setting will return the exact centroids at each time but will produce less regular extremities.

As Trailing Stop: Display the indicator as a trailing stop.

🔹 Optimization

This group of settings affects the runtime performance of the script.

Maximum Iteration Steps: Maximum number of iterations allowed for finding centroids. Excessively low values can return a better script load time but poor clustering.

Historical Bars Calculation: Calculation window of the script (in bars).

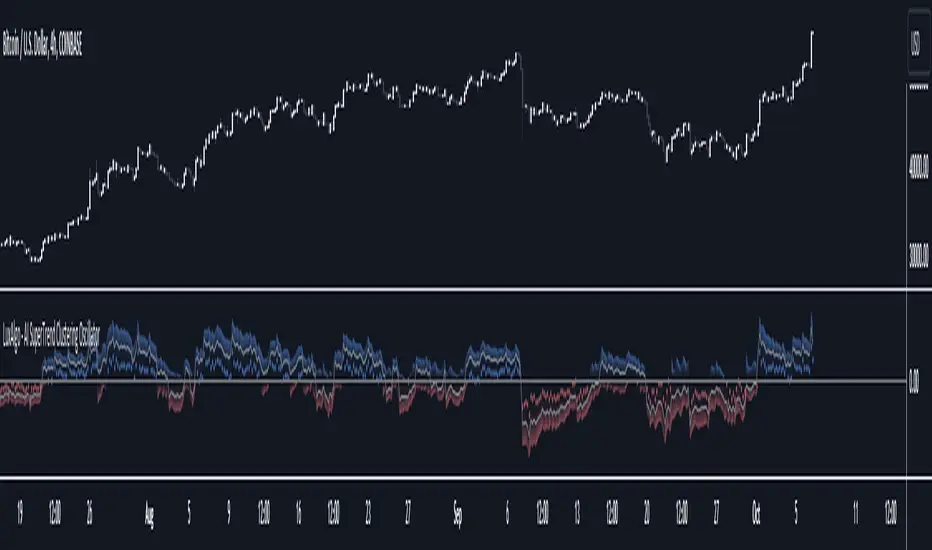

AI SuperTrend Clustering Oscillator [LuxAlgo]The AI SuperTrend Clustering Oscillator is an oscillator returning the most bullish/average/bearish centroids given by multiple instances of the difference between SuperTrend indicators.

This script is an extension of our previously posted SuperTrend AI indicator that makes use of k-means clustering. If you want to learn more about it see:

🔶 USAGE

The AI SuperTrend Clustering Oscillator is made of 3 distinct components, a bullish output (always the highest), a bearish output (always the lowest), and a "consensus" output always within the two others.

The general trend is given by the consensus output, with a value above 0 indicating an uptrend and under 0 indicating a downtrend. Using a higher minimum factor will weigh results toward longer-term trends, while lowering the maximum factor will weigh results toward shorter-term trends.

Strong trends are indicated when the bullish/bearish outputs are indicating an opposite sentiment. A strong bullish trend would for example be indicated when the bearish output is above 0, while a strong bearish trend would be indicated when the bullish output is below 0.

When the consensus output is indicating a specific trend direction, an opposite indication from the bullish/bearish output can highlight a potential reversal or retracement.

🔶 DETAILS

The indicator construction is based on finding three clusters from the difference between the closing price and various SuperTrend using different factors. The centroid of each cluster is then returned. This operation is done over all historical bars.

The highest cluster will be composed of the differences between the price and SuperTrends that are the highest, thus creating a more bullish group. The lowest cluster will be composed of the differences between the price and SuperTrends that are the lowest, thus creating a more bearish group.

The consensus cluster is composed of the differences between the price and SuperTrends that are not significant enough to be part of the other clusters.

🔶 SETTINGS

ATR Length: ATR period used for the calculation of the SuperTrends.

Factor Range: Determine the minimum and maximum factor values for the calculation of the SuperTrends.

Step: Increments of the factor range.

Smooth: Degree of smoothness of each output from the indicator.

🔹 Optimization

This group of settings affects the runtime performances of the script.

Maximum Iteration Steps: Maximum number of iterations allowed for finding centroids. Excessively low values can return a better script load time but poor clustering.

Historical Bars Calculation: Calculation window of the script (in bars).

Support/Resistance DBSCANHello, my friends. This is a new version of the support and resistance indicator implemented by the fast clustering algorithm DBSCAN

(1) Indicator description

The indicator clusters key top and bottom points in the historical K-line to find support and resistance areas with a high probability of occurrence

The clustering algorithm used for this indicator is the density-based fast clustering algorithm DBSCAN

The minimum unit of support and resistance found by this indicator is the core region, i.e., the key top and bottom points that frequently occur within a certain price range

Core regions may be superimposed on the chart. The more they are superimposed, the stronger possibility of support and resistance

The clustering algorithm does not work for all markets, so you need to adjust the parameters to suit different markets and timeframe

(2) Key parameters

- Support/Resistance Clustering

Pivot Lookback Period: Number of K-lines to look back left/right from the pivot top/bottom

Max of Lookback Forward: The maximum number of historical K-lines

Min Strength of Clustering Core: Minimum strength of the clustered core region, the higher the strength, the smaller the core region

Min Points of Clustering Core: Minimum number of clustering points in the core region of clustering

(3) Script description

Due to some circumstances that I don't want to see, subsequent scripts will not be open source, but you can still use the script for free. Thanks for your understanding and support!

If you have any suggestions or comments about the script, please feel free to leave your comments!

Happy trading, and enjoy your life!

————————————————————————————————————————

各位朋友大家好,这是一个全新的基于快速聚类算法DBSCAN的支撑压力位指标

(1) 指标说明

该指标通过对历史K线中的关键顶底点进行聚类,查找大概率出现的支撑和压力区间

该指标采用的聚类算法为基于密度的快速聚类算法 DBSCAN

该指标找到的支撑压力的最小单位为核心区间,即在一定价格范围内频繁出现的关键顶底点

核心区间可能会在图表上叠加,叠加越多,支持和压力的可能性越强

聚类算法不适用于所有的市场,因此需要您调整参数以适应不同的市场和时间周期

(2) 关键参数

- Support/Resistance Clustering

Pivot Lookback Period: 枢纽顶/底点往左/右回顾的 K线 数量

Max of Lookback Forward: 回顾历史 K线 的最大数量

Min Strength of Clustering Core: 聚类核心区间的最小强度,强度越大,区间越小

Min Points of Clustering Core: 聚类核心区间的最小聚类点数量

(3) 脚本说明

因为出现了一些我不希望看到的情况,后续的脚本将不再开源代码,但是您依然可以免费使用该脚本,感谢理解和支持!

如果您存在对于该脚本的使用建议或者意见,欢迎各位留言!

祝大家交易愉快