Bull/Bear FVG Density RatioThis indicator tracks the directional frequency of Fair Value Gaps (FVGs) over a configurable lookback window, offering a clean, responsive measure of market imbalance.

🔍 What It Does:

Detects bullish and bearish FVGs using a 3-bar displacement logic

Calculates the ratio of FVGs to candles over the last N bars

Plots separate density curves for bullish and bearish FVGs

Includes a threshold line to help identify regime shifts (e.g., drought vs spate)

📈 How to Use:

Use rising density to confirm trend strength or breakout momentum

Watch for crossovers above the threshold to signal active imbalance regimes

Combine with price action or volume overlays for high-confluence setups

⚙️ Inputs:

Lookback Window: Number of candles used to calculate FVG density

Threshold: Visual guide for regime classification (default: 0.2)

This tool is ideal for traders who want to move beyond symptomatic signals and model structural causality. It pairs well with lifecycle scoring, retest velocity, and HTF overlays.

经济周期

Easy [CHE] Easy — Minimalist Pine Script for detecting EMA direction changes to define fixed price zones for simple support and resistance visualization, ideal for manual trading workflows.

Summary

This indicator's programming is kept minimalist and super simple, with core logic in under 20 lines for easy comprehension and modification. It creates fixed price zones based on divergences between a base exponential moving average and its smoother counterpart, helping traders spot potential consolidation or reversal areas without dynamic adjustments. By locking the zone at the high and low of the signal bar, it avoids over-expansion in volatile conditions, offering a stable reference line colored by price position relative to the zone. This approach differs from expanding channels by prioritizing simplicity and persistence until a new qualifying signal, reducing visual clutter while highlighting directional bias through midpoint coloring.

Motivation: Why this design?

Traders often face noisy signals from moving averages that flip frequently in sideways markets or lag during breakouts, leading to premature entries or missed opportunities. This indicator addresses that by focusing on confirmed direction shifts between the base and smoothed averages, then anchoring a non-expanding zone to capture the initial price range of the shift. The result is a cleaner tool for marking equilibrium levels, assuming price respects these bounds in ranging or mildly trending conditions.

What’s different vs. standard approaches?

- Reference baseline: Traditional moving average crossovers or simple channels that update every bar.

- Architecture differences:

- Zones are set only on new divergence signals and remain fixed until reset by a gap from the prior zone.

- No ongoing high-low expansion; relies on persistent variables to hold bounds across bars.

- Midpoint plotting with conditional coloring based on close position, plus a highlight for zone initiations.

- Practical effect: Charts show persistent horizontal references instead of drifting lines, making it easier to gauge if price is rejecting or embracing the zone—useful for avoiding false breaks in low-volatility setups.

How it works (technical)

The indicator first computes a base exponential moving average of closing prices over a user-defined length, then applies a second exponential moving average to smooth that base. It checks if both the base and smoothed values are increasing or decreasing compared to their prior values, indicating aligned direction. A signal triggers when this alignment breaks, marking a potential shift.

On a new signal, if the current bar's high and low fall outside any existing zone (or none exists), the zone bounds update to those extremes and persist via dedicated variables. The midpoint of these bounds becomes the primary plot line, colored green if below the close (bullish lean), red if above (bearish lean), or gray otherwise. A secondary thick line highlights the midpoint briefly when a zone first sets, aiding visual confirmation. No higher timeframe data or external fetches are used, so updates occur on each bar close without lookahead.

Parameter Guide

EMA Length — Sets the period for the base moving average; longer values smooth more, reducing signal frequency but increasing lag. Default: 50. Trade-offs/Tips: Shorter for faster response in intraday charts (risks noise); longer for daily trends (may miss early shifts).

Smoother Length — Defines the period for the secondary smoothing on the base average; higher values dampen minor wiggles for stabler direction checks. Default: 3. Trade-offs/Tips: Keep low (2–5) for sensitivity; increase to 7+ if zones trigger too often in choppy markets, at cost of delayed signals.

Reading & Interpretation

The main circle plot at the zone midpoint serves as a dynamic equilibrium line: green suggests price is above the zone (potential strength), red indicates below (potential weakness), and gray shows containment within bounds (neutral consolidation). A sudden thick foreground line at the midpoint flags a fresh zone start, prompting review of the prior bar's context. Absence of a plot means no active zone, implying reliance on price action alone until the next signal.

Practical Workflows & Combinations

- Trend following: Enter long on green midpoint after a higher low touches the zone lower bound, confirmed by structure like higher highs; filter shorts similarly on red with lower highs.

- Exits/Stops: Use the opposite zone bound as a conservative stop (e.g., below lower for longs); trail aggressively to midpoint on strong moves, tightening near gray neutrality.

- Multi-asset/Multi-TF: Defaults work across forex and stocks on 1H–Daily; for crypto volatility, shorten EMA Length to 20–30. Pair with volume oscillators for confirmation, avoiding isolated use.

Behavior, Constraints & Performance

- Repaint/confirmation: Plots update on bar close using historical closes, so confirmed signals hold; live bars may shift until close but without future references.

- security()/HTF: Not used, eliminating related repaint risks.

- Resources: Minimal overhead—no loops, arrays, or bar limits exceeded; suitable for real-time on any timeframe.

- Known limits: Fixed zones may lag in strong trends (price drifts away without reset); signals skip if no gap from prior zone, potentially missing clustered shifts. Assumes standard OHLC data; untested on non-equity assets.

Sensible Defaults & Quick Tuning

Start with EMA Length at 50 and Smoother Length at 3 for balanced daily charts. If signals fire too frequently (e.g., in ranges), extend EMA Length to 100 for fewer but stabler zones. For sluggish response in trends, drop Smoother Length to 2 and EMA Length to 30, monitoring for added noise. In high-vol setups, widen both to 75/5 to filter extremes, trading speed for reliability.

What this indicator is—and isn’t

This is a lightweight visualization layer for EMA-driven zones, aiding manual chart reading and basic signal spotting. It is not a standalone system, predictive model, or automated alert generator—integrate with broader analysis like market structure and risk rules. (Unknown/Optional: No built-in alerts or multi-timeframe scaling.)

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Trading Range Aggression Histogram

This indicator is a histogram that accumulates the net volume of aggressive buying and selling per candle, representing the dominant market pressure within defined time-frame.

The indicator works by continuously summing volumes as long as the aggression remains in the same direction, resetting and reversing the accumulation when the pressure changes sides.

This creates visual waves that facilitate the perception of phases dominated by buyers and sellers over time. The tool is useful to identify moments of strength, weakness, and potential reversals in a dynamic market, especially in short-term trading.

RSI Regime: Continuation vs Reversal Indicator Description: RSI Regime (Continuation vs. Reversal)

This indicator uses the standard Relative Strength Index (RSI) to analyze market momentum and categorize it into three "regimes." Its primary goal is to help you determine if an overbought (OB) or oversold (OS) signal is likely to be a continuation of the current trend or a reversal point.

It also identifies "Fast Trend Starts," which are exceptionally fast and powerful moves from one extreme to the other.

Core Features & How to Read It

1. The Three RSI Regimes (Background Color) The script calculates a moving average (SMA) of the RSI to determine the dominant medium-term momentum. This is shown as the background color:

Bull Regime (Green Background): The RSI's average is high (e.g., above 55). The market is in a clear uptrend.

Bear Regime (Red Background): The RSI's average is low (e.g., below 45). The market is in a clear downtrend.

Range Regime (Orange Background): The RSI's average is in the middle. The market is consolidating or undecided.

2. Overbought (OB) & Oversold (OS) Signals

When the RSI line crosses into the overbought (e.g., >70) or oversold (e.g., <30) zones, the indicator generates one of two types of signals:

A) Continuation Signals (Small Triangles: ►)

These signals suggest an OB/OS reading is just a "pause" and the main trend will likely continue.

Orange ► (at the top): Appears when RSI becomes overbought while the market is already in a Bull Regime. This suggests the uptrend is strong, and this OB signal may not lead to a big drop.

Teal ► (at the bottom): Appears when RSI becomes oversold while the market is already in a Bear Regime. This suggests the downtrend is strong, and this OS signal may not lead to a big bounce.

(Note: An optional Price EMA filter can be enabled to make these signals more strict.)

B) Reversal Signals (Small Labels: "OS→>50" / "OB→<50")

These labels appear after an OB/OS signal to confirm that a reversal has actually occurred.

"OS→>50 Reversal" (Aqua Label): Appears if the RSI becomes oversold and then recovers back above the 50 midline within a set number of bars. This confirms the oversold dip was a reversal point.

"OB→<50 Reversal" (Orange Label): Appears if the RSI becomes overbought and then falls back below the 50 midline within a set number of bars. This confirms the overbought peak was a reversal point.

3. "Fast Trend Starts" (Large Labels)

This is a unique feature that identifies the fastest percentile of market moves. It measures how many bars it takes for the RSI to go from one extreme to the other and flags when a move is in the top 5% (default) of all historical moves.

"Long Pullbacks (Fast OS→BullRange)" (Large Green Label): This powerful signal appears when the RSI moves from oversold (<30) all the way up to the bull range (>60) exceptionally fast. It identifies a very strong, fast, and decisive bounce that could signal the start of a new uptrend.

"Short Pumps (Fast OB→BearRange)" (Large Red Label): This appears when the RSI moves from overbought (>70) all the way down to the bear range (<40) exceptionally fast. It identifies a very sharp, fast rejection or "pump-and-dump" that could signal the start of a new downtrend.

Key User Inputs

RSI Length (14): The lookback period for the main RSI calculation.

OB (70) / OS (30): The standard overbought and oversold levels.

Bull/Bear Range Threshold (60/40): These are the levels used to confirm the "Fast Trend Starts." They are separate from the OB/OS levels.

RSI Regime SMA Length (21): The lookback period for the moving average that determines the background regime.

Use Price EMA filter (true): If checked, the small "Continuation" triangles will only appear if the price is also above (for bulls) or below (for bears) its own 50-period EMA.

Fastest X% duration (5.0): This sets the percentile for the "Fast Trend Start" labels. 5.0 means it only flags moves that are in the fastest 5% of all recorded moves.

VWAP CATS background flipped 4.0VWAP CATS Background Flipped 4.0 is a sophisticated Pine Script v5 indicator for TradingView that combines a configurable moving average (MA) with dynamic Gann Square of 9 levels to create a multi-layered background shading system for price action analysis. It visualizes support/resistance zones around a central MA (often VWAP or RVWAP) using incremental offsets (either % or absolute points), generating symmetrical bands that resemble a "CATS" (Concentric Adaptive Tiered System) — hence the name.The background is "flipped" in the sense that shading intensity and structure emphasize higher-tier zones, and labels are placed to the right of the chart for future projection.Key FeaturesFeature

Description

Multi-MA Engine

Supports 20+ MA types: EMA, DEMA, TEMA, SMA, VWAP, RVWAP, HMA, ALMA, custom volume blends (CVB1–4)

RVWAP Mode

Rolling VWAP with adaptive or fixed time window (days/hours/minutes)

Gann Square of 9 Logic

Generates 80+ symmetric levels (0.25x to 17x increment) above/below the MA

Dual Increment Mode

Choose Percent or Points for spacing

Background Fills

Tiered transparency fills between Gann levels (darker = stronger zones)

Visual MA Offset

Shift MA line left/right without breaking fill alignment

Smart Labels

Projected labels on last bar: "FV", "normal", "high", "3/4" at key levels

Performance Optimized

Hidden plots + label cleanup to prevent lag

Primary Use Cases

1. Institutional VWAP Anchoring

Use RVWAP (1-day fixed) as maRaw

Set Increment = 0.5 points or 0.05%

Watch price interaction with "normal" (2x), "high" (4x), "3/4" (6x) zones

Ideal for intraday scalping on indices (ES, NQ) or forex

2. Swing Trading with Gann Projections

Use 400-period SMA/EMA on daily chart

Increment in Percent mode (~1.22%)

Identify confluence when price rejects at 2x, 4x, or 6x bands

Labels project future targets to the right

3. Volume-Weighted Mean Reversion

Select CVB1–CVB4 for heavy volume smoothing

Use Points mode for stocks with stable tick sizes (e.g. $0.50 increments)

Trade mean reversion between ±1x and ±2x bands

4. Risk Management & Stop Placement

Place stops beyond 2x or 4x bands

Take profits at next major tier (e.g. 4x → 6x)

Pro Tips

Enable "Use Fixed Time Period" for RVWAP to avoid session reset issues

Increase i_label_offset on lower timeframes to avoid overlap

Combine with volume profile or order flow for confluence

The "FV" label marks the Fair Value MA — core anchor

Summary"VWAP CATS Background Flipped 4.0" turns any moving average into a dynamic Gann-based pricing grid with intelligent background shading and forward-projected labels — perfect for institutional-style mean reversion, swing targeting, and risk-defined trading."

Moving Average Ribbon (10x, per-MA timeframe)A flexible moving‑average ribbon that plots up to 10 MAs, each with its own type, length, source, color, and independent timeframe selector for true multi‑timeframe analysis without repainting on higher‑timeframe pulls.

What it does

Plots ten moving averages with selectable types: SMA, EMA, SMMA (RMA), WMA, and VWMA.

Allows per‑line timeframe inputs (e.g., 5, 15, 60, 1D, 1W) so you can overlay higher‑ or equal‑timeframe MAs on the current chart.

Uses a non‑repainting request pattern for higher‑timeframe series to keep lines stable in realtime.

How to use

Leave a TF field blank to keep that MA on the chart’s timeframe; type a timeframe (like 15 or 1D) to fetch it from another timeframe.

Typical trend‑following setup: fast MAs (10–21) on chart TF, mid/slow MAs (34–200) from higher TFs for bias and dynamic support/resistance.

Color‑code faster vs slower lines and optionally hide lines you don’t need to reduce clutter.

Best practices

Prefer pulling equal or higher timeframes for stability; mixing lower TFs into a higher‑TF chart can create choppy visuals.

Combine with price action and volume/volatility tools (e.g., RSI, Bollinger Bands) for confirmation rather than standalone signals.

Showcase example charts in your publish post and explain default settings so users know how to interpret the ribbon.

Inputs

Show/Hide per MA, Type (SMA/EMA/SMMA/WMA/VWMA), Source, Length, Color, Timeframe.

Defaults cover common lengths (10/20/50/100/200 etc.) and can be customized to fit intraday or swing styles.

Limitations

This is an analysis overlay, not a signal generator; it doesn’t place trades or alerts by default.

Effectiveness depends on instrument liquidity and user configuration; avoid overfitting to one market or regime.

Attribution and etiquette

Provide a brief explanation of your calculation choices and note that MA formulas are standard; credit any borrowed concepts or snippets if used.

US Leverage Overlay — Margin Debt & Total Credit (YoY / Z-score)What this does

An overlay indicator that brings U.S. leverage proxies from FRED onto your main price chart (left axis). Choose between a proxy for investor margin debt or total credit market debt and view them as YoY %, Z-score of YoY, or an Indexed Level so they’re comparable with price without wrecking the scale.

Data sources (FRED symbols)

--- Margin (investor leverage proxy): FRED:BOGZ1FL663067003Q

Brokers & Dealers; Receivables Due from Customers ≈ margin loans (quarterly).

--- TotalCredit (economy-wide leverage): FRED:TCMDO

All sectors; Debt Securities & Loans; Liability (quarterly).

Note: These are quarterly series. The indicator samples monthly and holds values between official prints, so you’ll see step-like updates when new data drops.

Views (pick one in settings)

--- YoY % — 12-month rate of change. Above 0% = leverage expanding; below 0% = contracting.

--- Z-score (YoY) — Standardizes YoY vs. its recent history to flag unusual moves (regime shifts).

--- Indexed Level — 100 × (level / moving average), a compact “above/below trend” view.

How to read quickly

--- Rising YoY % > 0 → leverage expansion (often supportive for risk).

--- Falling YoY % < 0 → deleveraging headwind.

--- Z-score spikes (±2) → unusually fast changes; watch for volatility or policy inflections.

--- Indexed Level crossing down through 100 → slipping below trend.

Inputs

--- Data source: Margin or TotalCredit

--- YoY/Z-score lookbacks and Index baseline length

--- Overlay: overlay=true, scale=scale.left (uses its own left axis by default)

Tips

--- If it spawns in a sub-pane, right-click the label → Move to → Main chart.

--- For context, consider adding related series on separate panes:

FRED:TOTALSL (Consumer Credit), FRED:REVOLSL (Credit Cards),

FRED:BUSLOANS (C&I Loans), FRED:TDSP (Debt Service Ratio).

--- Occasionally FRED returns “Failed to fetch”; re-add or reload fixes it.

Why it’s useful

Equity drawdowns often line up with turns in leverage (households, corporates, or brokers). This overlay gives you a clean, normalized read so you can spot expansion vs. contraction alongside price action.

Compatibility

--- Pine Script® v6

--- Works on any chart timeframe (data internally sampled monthly)

Educational use only — not financial advice.

Morning Star & Rising Star Detector - Neon CandlesMorning Star & Rising Star to determine several levels and forecast what might happen next with the price.

Improved ICT MultiTF A+ IndicatorThis indicator provides ICT-style multi time frame fair value gaps with a 4-hour moving average bias. It prioritizes 15-minute gaps and falls back to 5-minute and 1-minute gaps when none are present. It also includes alert conditions for long and short signals based on session filters and bias.

Contango/Backwardation Monitor

This is an indicator to display the spread difference between two products. I designed it around VX1! and VX2! but any other two products can be chosen. It is a simple subtraction of VX2-VX1. I will go through the options first and what they do followed by what contango/backwardation is in my own words. You will need the data package for VX futures for the default version to work.

INPUTS

-Apply Smoothing: choose to apply smoothing or not.

-Smoothing Method: choose between SMA,EMA,WMA, etc.

-Line Width: Width of line if line is chosen style(can be changed in style section)

-Threshold 1-5: This is the level at which the line will change colors(defaults are for VX)

-Color 1-5: The color the line will change to when crossing threshold.

Towards Backwardation: Background color change when line is slanted down

Towards Contango: Background color change when line is slanted up

Bars to Confirm Trend: This is my method to cut down on background color changes. It is how many bars consecutive going back needed to change color.

STYLE

-All colors and whatnot can be changed here(threshold colors can be changed here or on the input page).

T1 Line-T5 line: These are simple horizontal lines that can be used to denote threshold areas or whatever you want.

Contango/Backwardation-These terms are used mostly with futures to define the calendar spread between two contracts. Contango is when that spread is is getting longer and backwardation is when that spread is closing. In terms of VIX futures, Contango would imply that volatility is stabilizing and the S and P will likely gain. Backwardation, woudl eb the opposite.

The most simple way to read this indicator with default settings- If the line is up, red, and the background is red, then you can assume S and P prices are going down. And if the opposite is true, then prices are likely going up.

Please feel free to ask any questions and I will do my best to answer them.

Hourly ORB NY Session (5/15min) - FixedDrawing ORB each hour in NY session

First ORB is 9.30 to 11.00am

then every hour we have a 15 min ORB

11am

12pm

1pm

2pm

3pm

You dont need anything else than this! Simple and powerful

週一普跌策略 Monday shit Strategy Strategy Description / 策略敘述

EN

This strategy takes a short position at the start of each Monday, based on the hypothesis that cryptocurrency markets tend to experience post-weekend risk-off behavior.

The system enters a full-equity short position at the Tokyo open (Taipei 08:00), aiming to capture Monday downside pressure resulting from accumulated weekend information and macro sentiment adjustments when traditional financial markets reopen.

Risk management uses fixed percentage take-profit and stop-loss levels, emphasizing asymmetric reward-to-risk (large occasional gains, small frequent losses).

The model reflects the increasing alignment between crypto price behavior and traditional financial market cycles.

ZH-TW

本策略於每週一開盤時做空,基於假設加密資產在週末後具有風險釋放與補跌傾向。

系統會在台北時間早上 08:00 以全倉做空,目標捕捉因週末累積消息與傳統金融市場重新開盤所造成的下跌壓力。

風控採固定止盈、止損百分比,強調高報酬/低風險的不對稱結構(小虧多次、偶爾大賺)。

此模型反映加密貨幣市場行為與華爾街週期愈趨一致的市場現象。

ALN Sessions Box Breakout — Auto- DSTDevoleper: Sheikh Rakib

What it does

This indicator draws session range boxes for Asia (Dhaka), London, and New York using each market’s own local time (DST-aware). After a session closes, it watches for the first close above the session high or below the session low and then marks that breakout once per session with clear chart markers and optional alerts.

Key features

Auto-DST, per-city timezones

London session uses Europe/London

New York session uses America/New_York

Asia session uses Asia/Dhaka

Your chart timezone doesn’t matter—the sessions track real local hours.

Clean range boxes with adjustable opacity and optional outlines.

Session labels that auto-center at the end of each session.

One-shot breakout signals per session:

Triangle up when price closes above the session high.

Triangle down when price closes below the session low.

Built-in alerts for: session starts and each breakout direction.

Inputs

London / New York / Asia (Dhaka)

Show Session: toggle each session on/off

Time Range: default London 08:00–17:00 (local), New York 08:00–17:00 (local), Asia 06:00–15:00 (Dhaka)

Colour: box color for each session

Settings

Show Session Labels

Show Range Outline

Opacity Preset: Dark / Medium / Light

(UTC Offset input is kept for display, not used in session detection.)

Visuals & alerts

Boxes extend from session open to close, continually updating the high/low.

When the session ends, the final high/low are locked in, the label is centered, and the indicator begins monitoring for a breakout.

Alerts

Session start: Asia/London/New York

Breakouts: “High Breakout” (close > high) and “Low Breakout” (close < low) for each session

Create alerts from the TradingView alert dialog and choose the desired alertcondition.

Logic notes (how signals fire)

While a session is open, its box grows to contain all highs/lows.

On the first bar after close, the script starts listening for a breakout:

Close > session high → one up signal (fires once)

Close < session low → one down signal (fires once)

When the next same session begins, internal flags reset and a new box starts—so signals are inherently scoped to the period between that session’s close and its next open.

Tips

Use on intraday timeframes (e.g., 1m–30m) for clearer box structure.

If you only want specific markets, toggle others off for a cleaner chart.

For systematic entries, combine with your trend/volatility filters and use the breakout alerts as triggers or confirmations—this script doesn’t place trades.

Disclaimer: Market timing and risk management are your responsibility. Past session behavior does not guarantee future performance.

ALN Sessions Box — Auto- DSTDevoleper: Sheikh Rakib

What it does

Draws candle-synced high/low range boxes for the three major sessions—Asia (Dhaka view), London, and New York—on any timeframe. London and New York are DST-aware (times auto-shift on DST changes). Boxes update live with session high/low and close exactly on the session’s final bar.

Key features

Auto-DST: Uses Europe/London and America/New_York time zones, so session windows auto-adjust when DST turns on/off.

Asia (BDT) window: Default 06:00–15:00 Asia/Dhaka (no DST).

Candle-linked boxes: Top/bottom track session High/Low; right edge finalizes on the session end bar—clean breakout zones.

Clean UI: Optional labels, outline toggle, and three opacity presets (Dark/Medium/Light).

Plug & play: Drop in, customize colors/times, done.

Inputs you can tweak

Time Range (LOCAL) for each session

Defaults: Asia 06:00–15:00 (Asia/Dhaka), London 08:00–17:00 (Europe/London), New York 08:00–17:00 (America/New_York)

For equities, switch New York to 09:30–16:00—DST handling remains automatic.

Colour per session, Show Session Labels, Show Range Outline, Opacity Preset.

UTC Offset input is retained for compatibility but not used for session detection.

Quick BDT reference (for the default 08:00–17:00 local windows)

London → DST ON (BST): 13:00–22:00 BDT · DST OFF (GMT): 14:00–23:00 BDT

New York → DST ON (EDT): 18:00–03:00 BDT (next day) · DST OFF (EST): 19:00–04:00 BDT (next day)

Asia (Dhaka) → 06:00–15:00 BDT (no DST)

Tips

If you see dotted vertical lines, that’s TradingView Session breaks (Chart Settings → Appearance). Turn off if you prefer a cleaner view.

Some symbols don’t trade during parts of a session—adjust Time Range as needed.

Labels are placed inside the box; adjust opacity/colors to suit your theme.

A sharp, professional session map for spotting breakouts, reversals, and volatility windows at a glance.

TopBot [CHE] TopBot — Structure pivots with buffered acceptance and gradient trend visualization

Summary

TopBot detects swing structure from confirmed pivot highs and lows, derives support and resistance levels, and switches trend only after a buffered and accepted break. It renders labels for recent structure points, maintains dynamic support and resistance lines that freeze on contact, and colors candles using a gradient that reflects consecutive trend persistence. The gradient communicates strength without extra panels, while the buffered acceptance reduces fragile flips around key levels. Everything runs in the main chart for immediate context.

Motivation: Why this design?

Classical swing tools often flip on single-bar spikes and produce lines that extend forever without acknowledging when price invalidates them. This script addresses that by requiring a user-controlled buffer and a run of consecutive closes before changing trend, while also freezing lines once price interacts with them. The gradient color layer communicates regime persistence so users can quickly judge whether a move is maturing or just starting.

What’s different vs. standard approaches?

Baseline reference: Simple pivot labeling and unbuffered break-of-structure tools.

Architecture differences:

Buffered level testing using ticks, percent, or ATR.

Acceptance logic that requires multiple consecutive closes.

Synchronized structure labeling with a single Top and Bottom within the active set.

Progressive support and resistance management that freezes lines on first contact.

Gradient candle and wick coloring driven by consecutive trend counts with windowed normalization and gamma control.

Practical effect: Fewer whipsaw flips, clearer status of active levels, and visual feedback about trend persistence without a secondary pane.

How it works (technical)

The script confirms swing points using left and right bar pivots, then forms a current structure window to classify each pivot as higher high, lower high, higher low, or lower low. Recent labels are trimmed to a user cap, and a postprocess step ensures one highest and one lowest label while preserving side information for the others. Support updates on higher low events, resistance on lower high events. Trend flips only after the close has moved beyond the active level by a chosen buffer and this condition holds for a chosen number of consecutive bars. Lines for new levels extend to the right and freeze once price touches them. A running count of consecutive trend bars produces a strength score, which is normalized over a rolling window, shaped by gamma, and mapped to user-defined dark and neon colors for both up and down regimes. Wick coloring uses `plotcandle`; fallback bar coloring uses `barcolor`. No higher-timeframe data is requested. Signals confirm only after the right-bar lookback of the pivot function.

Parameter Guide

Left Bars / Right Bars (default five each): Pivot sensitivity. Larger values confirm later and reduce noise; smaller values respond faster with more noise.

Draw S/R Lines (default true): Enables support and resistance line creation and updates.

Support / Resistance Colors (lime, red): Line colors for each side.

Line Style (Solid, Dashed, Dotted; default Dotted) and Width (default three): Visual style of S/R lines.

Max Labels & Lines (default ten): Cap for objects to control clutter and resource usage.

Change Bar Color (default true), Up/Down colors (blue, black): Fallback bar coloring when gradients or wick coloring are disabled.

Show Neutral Candles (default false): Optional coloring when no trend is active.

Enable Gradient Bar Colors (default true): Turns on gradient body coloring from the strength score.

Enable Wick Coloring (default true): Colors wicks and borders using `plotcandle`.

Collection Period (default one hundred): Rolling window used to scale the strength score. Shorter windows react faster but vary more.

Gamma Bars / Gamma Plots (defaults zero point seven and zero point eight): Shapes perceived contrast of bar and wick gradients. Lower values brighten early; higher values compress until stronger runs appear.

Gradient Transparency / Wick Transparency (default zero): Visual transparency for bodies and wicks.

Up/Down Trend Dark and Neon Colors: Endpoints for gradient mapping in each regime.

Acceptance closes (n) (default two): Number of consecutive closes beyond a level required before trend flips. Larger values reduce false breaks but react later.

Break buffer (None, Ticks, Percent, ATR; default ATR) and Value (default zero point five) and ATR Len (default fourteen): Defines the safety margin beyond the level. ATR mode adapts to volatility; Percent and Ticks are static.

Reading & Interpretation

Labels: “Top” and “Bottom” mark the most extreme points in the active set; “LT” and “HB” indicate side labels for lower top and higher bottom.

Lines: New support or resistance is drawn when structure confirms. A line freezes once price touches it, signaling that the dynamic phase ended.

Trend: Internal state switches to up or down only after buffered acceptance.

Colors: Brighter neon tones indicate stronger and more persistent runs; darker tones suggest early or weakening runs. When gradients are off, fallback bar colors indicate trend sign.

Practical Workflows & Combinations

Trend following: Wait for a buffered and accepted break through the most recent level, then use gradient intensity to stage entries or scale-ins.

Structure-first filtering: Trade only in the direction of the last accepted trend while price remains above support or below resistance.

Exits and stops: Consider exiting on loss of gradient intensity combined with a return through the most recent structure level.

Multi-asset / Multi-timeframe: Works on liquid symbols across common timeframes. Use larger pivot bars and higher acceptance on lower timeframes. No built-in higher-timeframe aggregation is used.

Behavior, Constraints & Performance

Repaint/confirmation: Pivot confirmation waits for the right bar window; trend acceptance is based on closes and can change during a live bar. Final signals stabilize on bar close.

security/HTF: Not used. No cross-timeframe data.

Resources: Arrays and loops are used for labels, lines, and structure search up to a capped historical span. Object counts are clamped by user input and platform limits.

Known limits: Delayed confirmation at sharp turns due to pivot windows; rapid gaps can jump over buffers; gradient scaling depends on the chosen collection period.

Sensible Defaults & Quick Tuning

Start with the defaults: pivot windows at five, ATR buffer with value near one half, acceptance at two, collection period near one hundred, gamma near zero point seven to zero point eight.

Too many flips: increase acceptance, increase buffer value, or increase pivot windows.

Too sluggish: reduce acceptance, reduce buffer value, or reduce pivot windows.

Colors too flat: lower gamma or shorten the collection period.

Visual clutter: reduce the max labels and lines cap or disable wicks.

What this indicator is—and isn’t

This is a visualization and signal layer that encodes swing structure, level state, and regime persistence. It is not a complete trading system, not predictive, and does not manage orders. Use it with broader context such as higher timeframe structure, session behavior, and defined risk controls.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Acknowledgment

Thanks to LonesomeTheBlue for the fantastic and inspiring "Higher High Lower Low Strategy" .

Original script:

Credit for the original concept and implementation goes to the author; any adaptations or errors here are mine.

BRS STC Schaff Trend CycleSTC with custom settings for 2min charts; Buy/Sell signals are close, but works very well with other indicators for validation; Borrowed from everget and another;

Seasonality Forecast Line (White BG • Stable)Seasonality Forecast Line (White BG • Stable)

Seasonality Forecast Line (White BG • Stable)

Seasonality Forecast Line (White BG • Stable)

Time Range HighlighterThis indicator highlights up to two custom time ranges on your chart with fully adjustable settings:

🔧 Features:

Define two separate time sessions

Set custom start and end times (in any time zone)

Choose unique highlight colors and opacity for each session

Toggle each range on or off independently

Timezone input allows syncing sessions to any global market hours (e.g., UTC, Asia/Tehran, New York)

🕒 Example Use Cases:

Highlight market opening hours (e.g. NYSE: 0930–1600)

Track your personal trading hours or peak volatility sessions

Visualize specific algorithm time filters

📌 Usage:

Enter your desired timezone string (e.g., "Asia/Tehran" or "Etc/UTC")

Customize session times like "0930-1200" and "1500-1700"

Adjust colors and visibility to fit your strategy

Ideal for traders who rely on time-based setups or session overlays.

24h Change Shows TF‑independent 24‑hour % change in the status line. The value is computed strictly on fixed 1‑minute data—last confirmed 1m close vs. the 1m close 1,440 minutes earlier—so changing chart timeframes does not affect the result. Updates once per minute; for best parity with an exchange, use the matching symbol/price type (Last vs. Mark/Index) and ensure ≥1,440 minutes of history.

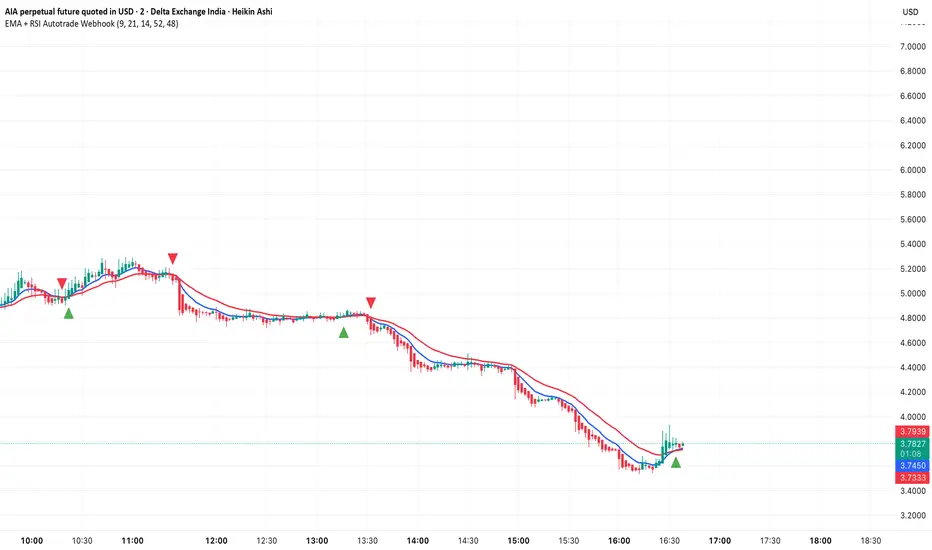

EMA + RSI Autotrade Webhook - VarunOverview

The EMA + RSI Autotrade Webhook is a powerful trend-following indicator designed for automated crypto futures trading. This indicator combines the reliability of Exponential Moving Average (EMA) crossovers with RSI momentum filtering to generate high-probability buy and sell signals optimized for webhook integration with crypto exchanges like Delta Exchange, Binance Futures, and Bybit.Key Features

Simple & Effective: Uses proven EMA 9/21 crossover strategy

RSI Momentum Filter: Eliminates low-probability trades in ranging markets

Webhook Ready: Two clean alerts (LONG Entry, SHORT Entry) for seamless automation

Exchange Compatible: Works with Delta Exchange, 3Commas, Alertatron, and other webhook platforms

Zero Lag Signals: Real-time alerts on crossover confirmation

Visual Clarity: Clean chart markers for easy signal identification

How It Works

Entry Signals:

LONG Entry: Triggers when EMA 9 crosses above EMA 21 AND RSI is above 52 (bullish momentum confirmed)

SHORT Entry: Triggers when EMA 9 crosses under EMA 21 AND RSI is below 48 (bearish momentum confirmed)

Technical Components:

Fast EMA: 9-period (tracks short-term price action)

Slow EMA: 21-period (identifies primary trend)

RSI: 14-period (confirms momentum strength)

RSI Long Threshold: 52 (filters weak bullish signals)

RSI Short Threshold: 48 (filters weak bearish signals)

Best Use Cases

Crypto Futures Trading: Bitcoin, Ethereum, Altcoin perpetual contracts

Automated Trading Bots: Integration with Delta Exchange webhooks, TradingView alerts

Timeframes: Optimized for 15-minute charts (works on 5min-1H)

Markets: Trending crypto markets with clear directional moves

Risk Management: Best used with 1-2% stop loss per trade (managed externally)

Webhook Automation Setup

Add indicator to your TradingView chart

Create alerts for "LONG Entry" and "SHORT Entry"

Configure webhook URL from your exchange (Delta Exchange, Binance, etc.)

Use alert message: Entry LONG {{ticker}} @ {{close}} or Entry SHORT {{ticker}} @ {{close}}

Exchange automatically reverses positions on opposite signals

Advantages

✅ No manual trading required - fully automated

✅ Eliminates emotional trading decisions

✅ Catches trending moves early with EMA crossovers

✅ RSI filter reduces whipsaws in choppy markets

✅ Works 24/7 without monitoring

✅ Simple two-alert system (easy to manage)

✅ Compatible with multiple exchanges via webhooksStrategy Philosophy

This indicator follows a trend-following with momentum confirmation approach. By waiting for both EMA crossover AND RSI confirmation, it ensures you're entering trades with genuine momentum behind them, not just random price noise. The tight RSI thresholds (52/48) keep you aligned with the prevailing trend.Recommended Settings

Timeframe: 15-minute (primary), 5-minute (scalping), 1-hour (swing)

Markets: BTC/USDT, ETH/USDT, high-liquidity altcoin perpetuals

Position Sizing: 100% capital per signal (exchange manages reversals)

Stop Loss: 2% (managed via exchange or external bot)

Leverage: 1-2x for conservative approach, up to 5x for aggressive

Important Notes

⚠️ This indicator generates entry signals only - position reversals are handled automatically by your exchange

⚠️ Always backtest on historical data before live trading

⚠️ Use proper risk management and position sizing

⚠️ Best performance in trending markets; may generate false signals in tight ranges

⚠️ Requires TradingView Premium or higher for webhook functionalityTags

cryptocurrency futures automated-trading ema-crossover rsi webhook delta-exchange tradingview-alerts trend-following momentum bitcoin ethereum crypto-bot algo-trading 15-minute-strategy

Market Sessions — VerticalA clean visual guide to global market sessions.

This indicator plots vertical lines at the opening and closing times of the four major forex sessions:

London, New York, Tokyo, and Sydney.

Fully customizable — toggle each session on/off, choose separate colors for open/close, and enable/disable labels.

Supports both Local (auto-DST) and GMT (fixed) modes — switch between realistic market-clock times or the standardized UTC schedule used by most trading resources.

Helps you visually identify session overlaps (e.g., London–New York) where volatility typically increases.

Ideal for forex, indices, and commodities traders who trade around session opens.

Default session times (GMT mode):

Sydney 21:00 – 06:00 GMT

Tokyo 00:00 – 09:00 GMT

London 08:00 – 17:00 GMT

New York 13:00 – 22:00 GMT

Tip: Set Anchor times by → Local (auto-DST) if you want the lines to follow each region’s real-world daylight-saving adjustments automatically.

Clean, lightweight, and built for traders who want precise, minimal clutter — just the key time windows that move the market.