Deviation BandsThis indicator plots the 1, 2 and 3 standard deviations from the mean as bands of color (hot and cold). Useful in identifying likely points of mean reversion.

Default mean is WMA 200 but can be SMA, EMA, VWMA, and VAWMA.

Calculating the standard deviation is done by first cleaning the data of outliers (configurable).

Deviationbands

3 Leg Short Strangle BandsDraws 3 leg bands along with safe zone(green lines) based on input

1) Input ATR, Week Day, Current Market Close

2) Input ATR - Previous day 1H Max ATR

3) ADX < 25

4) Input Current Market Close

5) Trading Day - Mon/Tue/Wed/Thu/Fri - Bands distance calculated based on day M/Tu/F 2*(Max ATR), W/Th 1.5(ATR)

6) Safe zone green lines - CMPCls +/- (1.5 * Max ATR)

7) Leg 1 Upper Lower Legs - M/Tu/F - CMPCls +/-(2 * Max ATR), W/Th - CMPCls +/-(1.5 * ATR)

8) Leg 2 & 3 Calculates based on Leg 2 = Leg 1 +/- 100 pts distance, Leg 3 = Leg 2 +/- 100 pts distance'

9) All figures rounded to nearest 100's

10) Safe zone broken exit all positions

This is a popular technic used by Profitable traders on sideway markets for Intraday

One can keep 3K as SL per 1 set of 3 legs for better R:R

Realized Volatility IIR Filters with BandsDISCLAIMER:

The Following indicator/code IS NOT intended to be a formal investment advice or recommendation by the author, nor should be construed as such. Users will be fully responsible by their use regarding their own trading vehicles/assets.

The following indicator was made for NON LUCRATIVE ACTIVITIES and must remain as is following TradingView's regulations. Use of indicator and their code are published by Invitation Only for work and knowledge sharing. All access granted over it, their use, copy or re-use should mention authorship(s) and origin(s).

WARNING NOTICE!

THE INCLUDED FUNCTION MUST BE CONSIDERED AS TESTING. The models included in the indicator have been taken from open sources on the web and some of them has been modified by the author, problems could occur at diverse data sceneries.

WHAT'S THIS...?

Work derived by previous own research for study:

This is mainly an INFINITE IMPULSE RESPONSE FILTERING INDICATOR , it's purpose is to catch trend given by the nature of lag given by a VOLATILITY ESTIMATION ALGORITHM as it's coefficient. It provides as well an INFINITE IMPULSE RESPONSE DEVIATION FILTER that uses the same coefficients of the main filter to plot deviation bands as an auxiliary tool.

The given Filter based indicator provides my own Multi Volatility-Estimators Function with only 3 models:

ELASTIC VOLUME WEIGHTED VOLATILITY : This is a Modified Daigler & Padungsaksawasdi "Volume Weighted Volatility" as on DOI: 10.1504/IJBAAF.2018.089423 but with Elastic Volume Weighted Moving Average instead of VWAP (intraday) for faster (but inaccurate) calculation. A future version is planned on the way using intra-bar inspection for intraday timeframe as described in original paper.

GARMAN & KLASS / YANG-ZANG EXTENSION : As one of the best range based (OHLC) with open gaps inclusion in a single bar.

PETER MARTIN'S ULCER INDEX : This is a better approach to measure realized volatility than standard deviation of log returns given it's proven convex risk metric for DrawDowns as shown in Chekhlov et al. (2005) . Regarding this particular model, I take a different approach to use it as coefficient feed: Given that the UI only takes in consideration DrawDawns, I code myself the inverse of this to compute Draw-Ups as well and use both of them to filter minimums volatility levels in order to create a SLOW version of the IIR filter, and maximums of both to calculate as FAST variation. This approach can be used as a better proxy instead of any other common moving average given that with NO COMPOUND IN TIME AT ALL (N=1) or only using as long as N=3 bars of compund, the filter can catch a trend easily, making the indicator nearly a NON PARAMETRIC FILTER.

NOTES:

This version DO NOT INCLUDE ALERTS.

This version DO NOT INCLUDE STRATEGY: ALL Feedback welcome.

DERIVED WORK:

Incremental calculation of weighted mean and variance by Tony Finch (fanf2@cam. ac .uk) (dot@dotat.at), 2009.

Volume weighted volatility: empirical evidence for a new realised volatility measure by Chaiyuth Padungsaksawasdi & Robert T. Daigler, 2018.

Basic DSP Tips & Trics by TradingView user @alexgrover

CHEERS!

@XeL_Arjona 2020.

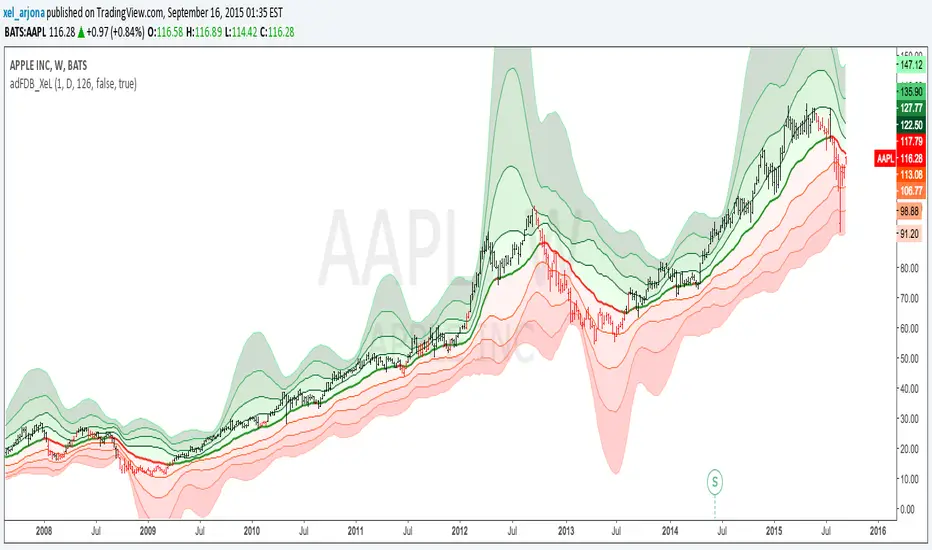

Acc/DistAMA with FRACTAL DEVIATION BANDS by @XeL_ArjonaACCUMULATION/DISTRIBUTION ADAPTIVE MOVING AVERAGE with FRACTAL DEVIATION BANDS

Ver. 2.5 @ 16.09.2015

By Ricardo M Arjona @XeL_Arjona

DISCLAIMER:

The Following indicator/code IS NOT intended to be a formal investment advice or recommendation by the

author, nor should be construed as such. Users will be fully responsible by their use regarding their own trading vehicles/assets.

The embedded code and ideas within this work are FREELY AND PUBLICLY available on the Web for NON LUCRATIVE ACTIVITIES and must remain as is.

Pine Script code MOD's and adaptations by @XeL_Arjona with special mention in regard of:

Buy (Bull) and Sell (Bear) "Power Balance Algorithm" by:

Stocks & Commodities V. 21:10 (68-72): "Bull And Bear Balance Indicator by Vadim Gimelfarb"

Fractal Deviation Bands by @XeL_Arjona.

Color Cloud Fill by @ChrisMoody

CHANGE LOG:

Following a "Fractal Approach" now the lookback window is hardcode correlated with a given timeframe. (Default @ 126 days as Half a Year / 252 bars)

Clean and speed up of Adaptive Moving Average Algo.

Fractal Deviation Band Cloud coloring smoothed.

>

ALL NEW IDEAS OR MODIFICATIONS to these indicator(s) are Welcome in favor to deploy a better and more accurate readings. I will be very glad to be notified at Twitter or TradingVew accounts at: @XeL_Arjona

Any important addition to this work MUST REMAIN PUBLIC by means of CreativeCommons CC & TradingView. Copyright 2015