Volume scaled Price + auto colour change light/dark mode🔶 OVERVIEW

🔹 This script shows price in a similar style as volume . To accomplish this we use the body of the candle ( close - open ), which is placed on a zero line.

This can be useful when comparing volume ~ price .

🔹 3 options are included to show additional lines, to make comparisons easier:

· Percentile nearest rank

· Bollinger Bands (BB)

· Simple Moving Average (SMA)

🔶 SETTINGS

🔹 Option : choose whether to show price (candles) or volume . Adding 2 versions of this indicator on the chart enables you to compare these 2 options:

🔹 Lines:

· (Percentile nearest rank (only the setting mult is used for this option).

· Bollinger Bands (BB) (only the setting % perc. nearest rank is used for this option).

· Simple Moving Average (SMA )

All 3 options will use length , this is the amount of bars used for calculations.

🔹 Show wick will show you... wicks :)

🔶 PERCENTILE NEAREST RANK

🔹 This script has 2 extra types of background color

dvP = volume > volume and z < z and z < prP_ and volume > prV

· In this case:

· volume is higher than previous volume ( volume > volume )

· volume is above 90th percentile rank ( volume > prV )

· price is lower than previous price ( z < z )

· price is below 10th percentile rank ( z < prP_ )

dvV = volume < volume and z > z and z > prP and volume < prV_

· The second type background color is reversed ( volume lower, price higher)

🔶 AUTOMATIC COLOUR CHANGE WHEN SWITCHING DARK/LIGHT MODE

🔹 chart.bg_color returns the color of the chart’s background from the "Chart settings/Appearance/Background" field, while chart.fg_color returns a color providing optimal contrast with chart.bg_color .

· Following technique gives you the possibility to pick your own colour for either dark/light time.

· We first retrieve separately the red, green and blue component of the measured chart.bg_color

r = color.r(chart.bg_color)

g = color.g(chart.bg_color)

b = color.b(chart.bg_color)

The following assumption states when all 3 colour components' values are below 80, we are in the dark mode:

isDark = r < 80 and g < 80 and b < 80

Now we can use isDark to automatically show your own dark/light mode colours (chosen at settings), dependable on the mode:

Cheers!

Percentile

Volume percentrank[TV1]Volume percentrank

Volume normalized by percentile.

The indicator calculates the percentile of the trading volume . The volume in the base asset or quote asset can be selected as data. To calculate the volume of a quoted asset, the closing price or another standard method for calculating the price of a bar can be used.

A feature of percentile calculation with a small data sample length is low accuracy. Despite the fact that the script allows you to calculate a percentile with a length of 1, using a percentile length less than 100 is not recommended.

The percentile calculation method does not allow correctly calculating the percentile at the beginning of the chart due to the lack of all data in the selection, therefore, when the date of the first bar changes (this happens on small timeframes if the TradingView subscription does not allow you to see all historical data), the indicator will be repainted up to the bar number equal to the percentile sample length.

Huge values of the percentile length may cause a script error. If the indicator doesn't work, just make the percentile length smaller.

Объем, нормализованный по процентилью.

Индикатор вычисляет процентиль объема торгов. В качестве данных может быть выбран объем в базовом(base) активе или котировочном(quote) активе. Для расчета объема в котировочном активе может использоваться цена закрытия либо другой стандартный метод расчета цены бара.

Особенностью расчета процентиля при малой длине выборки данных является малая точность. Не смотря на то, что скрипт позволяет вычиcлить процентиль с длинной 1, использовать длину процентиля меньше 100 не рекомендуется.

Метод расчета процентиля не позволяет корректно рассчитать процентиль в начале графика из-за отсутствия всех данных в выборке, поэтому при изменении даты первого бара (это происходит на малых таймфреймах, если подписка TradingView не позволяет видеть все исторические данные) индикатор подвержен перерисовке вплоть до номера бара равного длине выборки процентиля.

Большие значения длины процентиля могут приводить к ошибке скрипта. Если индикатор не работает, просто сделайте длину процентиля меньше.

Weighted percentile nearest rankYo, posting it for the whole internet, took the whole day to find / to design the actual working solution for weighted percentile 'nearest rank' algorithm, almost no reliable info online and a lot of library-style/textbook-style solutions that don't provide on real world production level.

The principle:

0) initial data

data = 22, 33, 11, 44, 55

weights = 5 , 3 , 2 , 1 , 4

array(s) size = 5

1) sort data array, apply the sorting pattern to the weights array, resulting:

data = 11, 22, 33, 44, 55

weights = 2 , 5 , 3 , 1 , 4

2) get weights cumsum and sum:

weights = 2, 5, 3 , 1 , 4

weights_cum = 2, 7, 10, 11, 15

weights_sum = 15

3) say we wanna find 50th percentile, get a threshold value:

n = 50

thres = weights_sum / 100 * n

7.5 = 15 / 100 * 50

4) iterate through weights_cum until you find a value that >= the threshold:

for i = 0 to size - 1

2 >= 7.5 ? nah

7 >= 7.5 ? nah

10 >= 7.5 ? aye

5) take the iteration index that resulted "aye", and find the data value with the same index, that's gonna be the resulting percentile.

i = 2

data = 33

This one is not an approximation, not an estimator, it's the actual weighted percentile nearest rank as it is.

I tested the thing extensively and it works perfectly.

For the skeptics, check lines 40, 41, 69 in the code, you can comment/uncomment dem to switch for unit (1) weights, resulting in the usual non-weighted percentile nearest rank that ideally matches the TV's built-in function.

Shoutout for @wallneradam for the sorting function mane

...

Live Long and Prosper

Rolling QuartilesThis script will continuously draw a boxplot to represent quartiles associated with data points in the current rolling window.

Description :

A quartile is a statistical term that refers to the division of a dataset based on percentiles.

Q1 : Quartile 1 - 25th percentile

Q2 : Quartile 2 - 50th percentile, as known as the median

Q3 : Quartile 3 - 75th percentile

Other points to note:

Q0: the minimum

Q4: the maximum

Other properties :

- Q1 to Q3: a range is known as the interquartile range ( IQR ). It describes where 50% of data approximately lie.

- Line segments connecting IQR to min and max (Q0→Q1, and Q3→Q4) are known as whiskers . Data lying outside the whiskers are considered as outliers. However, such extreme values will not be found in a rolling window because whenever new datapoints are introduced to the dataset, the oldest values will get dropped out, leaving Q0 and Q4 to always point to the observable min and max values.

Applications :

This script has a feature that allows moving percentiles (moving values of Q1, Q2, and Q3) to be shown. This can be applied for trading in ways such as:

- Q2: as alternative to a SMA that uses the same lookback period. We know that the Mean (SMA) is highly sensitive to extreme values. On the other hand, Median (Q2) is less affected by skewness. Putting it together, if the SMA is significantly lower than Q2, then price is regarded as negatively skewed; prices of a few candles are likely exceptionally lower. Vice versa when price is positively skewed.

- Q1 and Q3: as lower and upper bands. As mentioned above, the IQR covers approximately 50% of data within the rolling window. If price is normally distributed, then Q1 and Q3 bands will overlap a bollinger band configured with +/- 0.67x standard deviations (modifying default: 2) above and below the mean.

- The boxplot, combined with TradingView's builtin bar replay feature, makes a great tool for studies purposes. This helps visualization of price at a chosen instance of time. Speaking of which, it can also be used in conjunction with a fixed volume profile to compare and contrast the effects (in terms of price range) with and without consideration of weights by volume.

Parameters :

- Lookback: The size of the rolling window.

- Offset: Location of boxplot, right hand side relative to recent bar.

- Source data: Data points for observation, default is closing price

- Other options such as color, and whether to show/hide various lines.

Heikin Ashi Volatility Percentile - TraderHalaiThe Heikin Ashi Volatility Percentile (HAVP) Oscillator was inspired by the legendary Bollinger Band Width Percentile indicator(known as BBWP), written by Caretaker, and made famous by Eric Krown, a famous influencer.

This script borrows aspects of the BBWP indicator which enables the HAVP oscillator to visually match the look and feel of BBWP and allows similar configuration functions (such as colouring function, smoothing MAs and alerts)

The fundamentals of this script are however different to BBWP. Instead of Bollinger band width, this script uses a reverse function of Heikin Ashi close (implemented in my Smoothed Heikin Ashi Trend

indicator, linked below).

The reverse Heikin Ashi close is smoothed using Ehler's SuperSmoother function, providing smooth oscillation and earlier signals of volatility tops and bottoms.

From an automated backtest that I have conducted on the BTCUSD index pair, I have observed comparable performance to BBWP across multiple timeframes when combining with stochastic direction to give a bias on overall direction. Using parameters I have tested, it performs better on mid-term timeframes such as 3h,4h and 6h. BBWP outperforms on 1h and 1d, with lower timeframes being comparable.

From the results, using HAVP over BBWP tends to result in reduced holding time and more frequent trades, which may or may not be desirable, although the behaviour can be adjusted using the parameters provided.

For instance, the smoother oscillation provided by HAVP provides a great predictability factor and earlier confirmation signals, which is something that Ehler emphasised in his trading style, and something which I agree with personally. I would encourage you to try out both HAVP and BBWP and see which fits your trading style.

Releasing this as open source allows for the betterment of the community and further development, criticism and discussion.

Thanks and enjoy! :)

Spinn ATR targetNot quite the usual approach to plotting targets on the chart, where the price will come with a given probability.

The indicator draws targets by studying the ATR of the target timeframe. More precisely, this is not exactly an ATR - the price move is taken from the closing price of the previous bar and is calculated both up and down separately.

The settings specify the percentage used to calculate the price move, at which the specified percentage of bars reached this price move in the past.

Simply put, if we set 50% in the settings, this means that a line will be drawn at the level at which the price reached this level in 50% of cases over a given period.

--

Не совсем обычный подход к построению целей на графике, куда цена придет с заданной вероятностью.

Индикатор рисует цели, изучая ATR целевого таймфрейма. Точнее, это не совсем ATR - ход цены берется от цены закрытия предыдущего бара и считается отдельно как вверх, так и вниз.

В настройках задается процент, исходя из которого вычисляется ход цены, при котором заданный процент баров достигал этого хода цены ранее.

Проще говоря, если мы задаем в настройках 50%, то это означает, что будет построена линия на том уровне, на котором цена в 50% случаев за заданный период достигала этого уровня.

Percentile Major Move Indicator This indicator is a powerful tool for understanding how big of a move a product, crypto, or currency has recently had.

Anything inside of the green bars is a standard move with a 68% chance of happening based on your chart timeframe.

Any move that touches the red lines to the upside or downside has a 2%+ chance of happening in either direction.

This is a powerful indicator but just one point of data and should be used as such.

ROC vs BTCThis is a modification of my Rate of Change Percentile script, used to compare the current ticker (e.g. Altcoins) to BTC.

Essentially we are looking at (Current Ticker ROC percentile) vs (Bitcoin ROC percentile).

In other words, we are using the ROC value of both the current ticker and BTC, and ranking each based on their previous ROC.

We compare the rankings to gauge the relative overperformance or underperformance of the current ticker vs BTC.

The blue line is BTC, the columns are the current ticker.

Green columns above the blue line indicate positive ROC and current ticker has higher ROC ranking than BTC.

Red columns below the blue line indicate negative ROC and current ticker has a higher ROC ranking than BTC.

*** PLEASE LEAVE A LIKE AND FOLLOW IF YOU ENJOY THE SCRIPT ***

Any questions, comments or feedback I'd love to hear from you below!

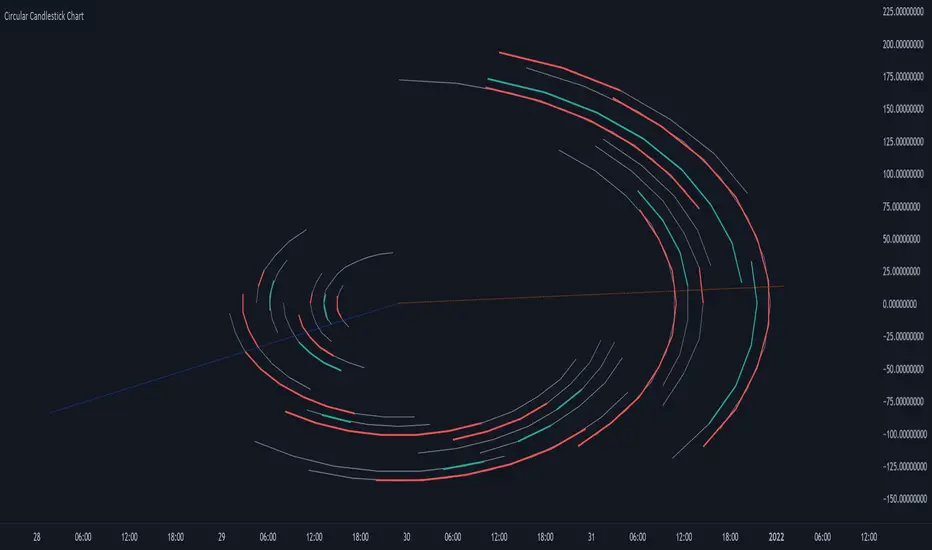

Circular Candlestick ChartAn original (but impractical) way to represent a candlestick chart using circles arc.

The most recent candles are further away from the circle origin. Note that OHLC values follow a clockwise direction. A higher arc length would indicate candles with a higher body or wick range.

The Length settings determine the number of past candles to be included in the circular candlestick chart. The Width setting control the width of the circular chart. The Spacing setting controls the space between each arcs. Finally, the Precision settings allow obtaining a more precise representation of candles, with lower values returning more precise results, however, more precision requires a higher amount of lines. Settings are quite hard to adjust, using a higher length might require a lower spacing value.

Additionally, the script includes two pointers indicating the location of the 75 (in blue) and 25 (in orange) percentiles. This allows obtaining an estimate of the current market sentiment, with the most recent arcs laying closer to the 75 percentile pointer indicating an up-trend.

This new way to represent candlesticks might be useful to more easily identify candles clusters or to find new price patterns. Who knows, we know that new ways to see prices always stimulate traders imagination.

See you next year.

Alpha Trading - Absolute Mean Entropy with A2 EPPAbsolute Mean Entropy with Alpha Squared Entropy Price Percentile

Entropy

The history of the word ―entropy can be traced back to 1865 when the German physicist Rudolf Clausius tried to give a new name to irreversible heat loss, what he previously called ―equivalent-value.

The word ―entropy was chosen because in Greek, “en+tropein” means “content transformative” or “transformation content”

Since then, entropy has played an important role in thermodynamics and many other scientific fields. Being defined as the sum of “heat supplied” divided by “temperature” it is central to the Second Law of Thermodynamics. It also helps measure the amount of order and disorder and/or chaos.

The application of entropy in finance can be regarded as an extension of “Information Entropy” and “Probability Entropy”

Entropy in Finance can be used in many ways such as Asset Selection, Asset Diversification, Measure an Assets Risk, inputs into Options pricing. While Entropy started in the field of Thermodynamics as aforementioned it has also found a home in Finance. However, studies with entropy in the field of Finance are still in their infancy.

• Entropy is a measure of randomness. Entropy is used to help model and represent the degree of uncertainty of a random variable.

• Entropy is used by financial analysts and market technicians to determine the chances of a specific type of behavior by a security or market.

• Entropy has long been a source of study and debate by market analysts and traders. It is used in quantitative analysis and can help predict the probability that a security will move in a certain direction or according to a certain pattern.

The concept of Entropy is explored in the book "A Random Walk Down Wall Street."

Entropy is plotted below the axis with negative values. Entropy can also colorize the candle color if selected.

R-squared (The Coefficient of Determination)

R-squared is a statistical measurement that examines how differences in one variable can be explained by the difference in a second variable, when predicting the outcome of a given event.

In other words, this coefficient, which is more commonly known as R-squared (or R2), assesses how strong the linear relationship is between two variables, and is heavily relied on by researchers when conducting trend analysis.

To cite an example of its application, this coefficient may contemplate the following question: if an indicator becomes pregnant on a certain day, what is the likelihood that this indicator would deliver a new indicator on a particular date in the future? In this scenario, this metric aims to calculate the correlation between two related events: conception of the indicator and the birth of the indicator.

• The coefficient of determination is a complex idea centered on the statistical analysis of models for data.

• The coefficient of determination is used to explain how much variability of one factor can be caused by its relationship to another factor.

• This coefficient is commonly known as R-squared (or R2) and is sometimes referred to as the "goodness of fit."

• This measure is represented as a value between 0.0 and 1.0, where a value of 1.0 indicates a perfect fit, and is thus a highly reliable model for future forecasts, while a value of 0.0 would indicate that the model fails to accurately model the data at all.

R2 and Price

The hypothesis that R2 is related to investors’ biases in processing information.

This theory motivates an empirical hypothesis that stocks with lower R2 should exhibit more pronounced overreaction-driven price momentum.

Alpha Trading AME/A2 EPP Settings

Settings for AME (Absolute Mean Entropy)

Length: Sample size.

Use as Barcolor: AME color as Price Action Candle color.

Show Entropy Flashes: If absolute value of entropy is very low, it gives yellow color for AME and Price Action Candle color if selected.

Band StdDev: (2 times) AME StdDev bands.1st and 2nd default.

Exponential Weighted Entropy: Weights the AME exponentially, is more reactive, but more noise.

Settings for EPP (Entropy Price Percentile)

Percentile Period: lookback for percentile range(relevant for flashes)

Background flashes: if EPP is below threshold default is below 10%, Flashes green in the background.

Std.err bands period: default 3 and multiplier 1.

EPP Column Meanings

Bright Green: Returns above the mean and increasing.

Dark Green: Returns above the mean and decreasing.

Bright Red: Returns below the mean and increasing.

Dark Red: Returns below the mean and decreasing.

Basic Trade Signal

Long – Value of AME is low, as you see EPP increasing with a coloration of green consider taking a long if you have confluence with other Alpha Trading Indicators.

Short – Value of AME is low, as you see EPP increasing with a coloration of red consider taking a short if you have confluence with other Alpha Trading Indicators.

The Chart below is showing Entries, Exponential Weighting input turned on, Percentile Period set to 30 instead of default 100, everything else is Default....

When using other Alpha Trading indicators in confluence, there are other entries available when the indicator isn't flashing and the indicator still supports the move.

References

www.investopedia.com

www.investopedia.com

www.wallstreetmojo.com

byjus.com

www.investopedia.com

en.wikipedia.org

papers.ssrn.com

Momentum Performance This Indicator displays the momentum (performance) of the symbol in percent.

You can compare the performance with other symbols.

The default benchmarks are the S&P 500, the MSCI World and the FTSE All World EX US.

The default length corresponds to one year in the timeframes monthly, weekly and daily.

In intraday the default length is 200, but you can also set your own setting.

You have also the opportunity to display a average momentum performance of the main symbol.

P-Square - Estimation of the Nth percentile of a seriesEstimation of the Nth percentile of a series

When working with built-in functions in TradingView we have to limit our length parameters to max 4999. In case we want to use a function on the whole available series (bar 0 all the way to the current bar), we can usually not do this without manually creating these calculations in our code. For things like mean or standard deviation, this is quite trivial, but for things like percentiles, this is usually very costly. In more complex scripts, this becomes impossible because of resource restrictions from the Pine Script execution servers.

One solution to this is to use an estimation algorithm to get close to the true percentile value. Therefore, I have ported this implementation of the P-Square algorithm to Pine Script. P-Square is a fast algorithm that does a good job at estimating percentiles in data streams. Here's the algorithms original paper .

The chart

On the chart we see:

The returns of the series (blue scatter plot)

The mean of the returns of the series (orange line)

The standard deviation of the returns of the series (yellow line)

The actual 84.1th percentile of the returns (white line)

The estimatedl 84.1th percentile of the returns using the P-Square algorithm (green line)

Note: We can see that the returns are not normally distributed as we can see that one standard deviation is higher than the 84.1th percentile. One standard deviation should equal the 84.1th percentile if the data is normally distributed.

Rolling summaryStatistical methods based on mean cannot be effective all the time when attributed to financial data since it doesn't usually follow normal distribution, the data can be skewed or/and have extreme values which can be described as outliers.

In order to deal with this problem it is appropriate to use median-based techniques.

The most common one is called five-number summary/box plot, which plots median of the dataset, 25th (Q1) & 75th (Q3) percentiles (the medians of lower & upper parts of the original dataset divided by the original median), and whiskers calculated by taking range between Q1 and Q3, multiplying it by 1.5 and adding it to Q3 and subtracting it from Q1. The values which are outside the whiskers are considered outliers. Default settings of the script correspond to the classic box plot.

Seven-number summary can be also plotted by this script, by turning on 4 additional percentiles/Bowley’s seven-figure summary by turning on first 2 additional percentiles and changing their values to 10 and 90 respectively.

P.S.: Mean can be also turned in just to check the difference.

Historical Volatility Percentile + SMAHistorical Volatility Percentile tells you the percentage of the days from the past year (252 trading days) that have lower volatility than the current volatility.

I included a simple moving average as a signal line to show you how volatile the stock is at the moment.

I have included simple colors to let you know when to enter or exit a position.

Buy when price higher than EMA & historical volatility higher than SMA

Sell when price lower than EMA & historical volatility higher than SMA

Please let me know if you would like me to publish any other indicators! I always love to hear from you guys.

Volatility IndexThis is a composite volatility index to show percentile of current volatility compared to that of the last 52 bars. As this is a weekly chart (and this script is intended for usage on weekly charts) we can see the yearly percentile rank of volatility.

As shown when volatility is in the lower 25%tile (viewed on weekly) the market is calm and likes to rise; when the volatility is above the 25%tile you can see that the market tends to have larger and 'choppier' moves.

This is /not/ 'just the vix' this takes into consideration the volatility of all major US indexes including the SPX500, Dow 30, Nasdaq 100, and Russel 2000.

Please remember that this is just plotting:( volatility index - lowest(index,52) )/( highest(index,52)-lowest(index,52) ) so for 'yearly percentile' check the weekly chart (52 weeks = 1yr)

Quantile BandsMiddle quantile/band color is set by confluence of the outer quantiles and not by it's own slope. Optional MTF.

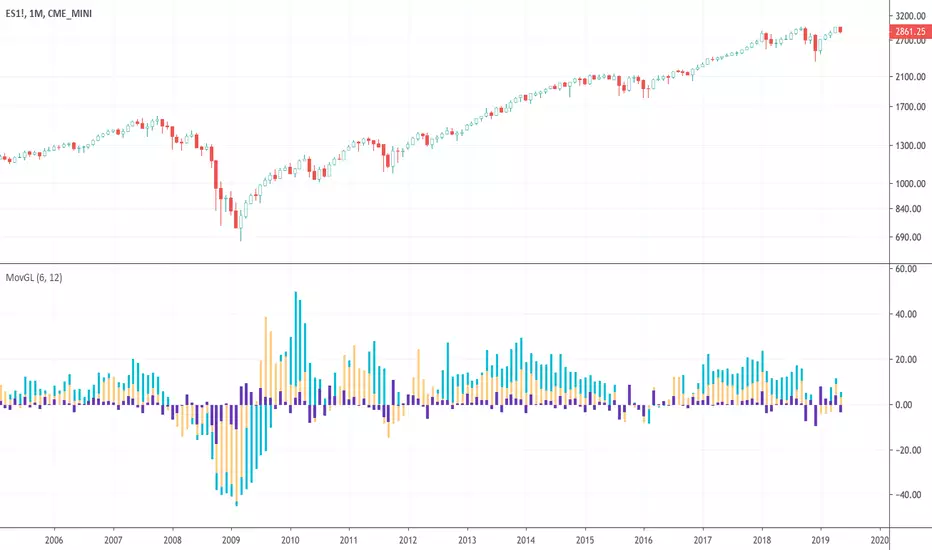

Moving Gain Loss PercentTracks the percentage gain/loss in three ranges:

single candle (can be turned on or off)

custom range of candles

custom range of candles

For example, with a range of 3 candles, and the serie:

1 - close 10

2 - close 5

3 - close 20

The moving gain would be:

1 - close 10 - gain 10, infinite%

2 - close 5 - gain 5, infinite%

3 - close 18 - gain 8, 80%

Or, for example if the range is 12 candles on a monthly chart, then the result is the Year-To-Date gain/loss plotted as a percentage.

DWP_percentile_linear_interpolation

Hope this help to see the % of winners and losers in the market.

MoveTrap.

Percentile Trend Channel [DW]This is an experimental study designed to identify the trend of price action over a specified period using percentiles.

First, the 50th percentile is calculated over the sampling period using the nearest rank method. I've found that this calculation is useful as a proxy for moving averages and other filters of that class.

Next, the channel levels are calculated. In this study, there are three channel methods to choose from:

-Percentile Donchian, which calculates Donchian Channels using the 100th and 0th percentile ranks

-Percentile Keltner, which calculates the 50th percentile true range multiplied by a specified amount, then adds it to and subtracts it from the 50th percentile

-Percentile Bollinger, which calculates 50th percentile standard deviation multiplied by a specified amount, then adds it to and subtracts it from the 50th percentile

I also included a squeeze box option within this script, which is derived from my original Squeeze Box tool.

This option detects squeezes in the specified channel's range by a specific percentage, and plots the channel values where the squeeze begins.

The box also has a range multiplier, which can be used to expand or contract its range.

Custom bar colors are included. The color scheme is based on the perceived trend over the specified sampling period.

[RESEARCH] Custom Median vs Built-in MedianI compared custom median (using the sorting solution by @apozdnyakov) with built-in median (using percentile_nearest_rank function)

If you see the zero line this means the solutions give the same results.

The best results was achieved on the odd lengths.

Conclusions:

1) Do not try to reinvent the wheel.

2) Always check the Pine Script docs to find already implemented solutions.