Linear Regression Channel Screener [Daveatt]Hello traders

First and foremost, I want to extend a huge thank you to @LonesomeTheBlue for his exceptional Linear Regression Channel indicator that served as the foundation for this screener.

Original work can be found here:

Overview

This project demonstrates how to transform any open-source indicator into a powerful multi-asset screener.

The principles shown here can be applied to virtually any indicator you find interesting.

How to Transform an Indicator into a Screener

Step 1: Identify the Core Logic

First, identify the main calculations of the indicator.

In our case, it's the Linear Regression

Channel calculation:

get_channel(src, len) =>

mid = math.sum(src, len) / len

slope = ta.linreg(src, len, 0) - ta.linreg(src, len, 1)

intercept = mid - slope * math.floor(len / 2) + (1 - len % 2) / 2 * slope

endy = intercept + slope * (len - 1)

dev = 0.0

for x = 0 to len - 1 by 1

dev := dev + math.pow(src - (slope * (len - x) + intercept), 2)

dev

dev := math.sqrt(dev / len)

Step 2: Use request.security()

Pass the function to request.security() to analyze multiple assets:

= request.security(sym, timeframe.period, get_channel(src, len))

Step 3: Scale to Multiple Assets

PineScript allows up to 40 request.security() calls, letting you monitor up to 40 assets simultaneously.

Features of This Screener

The screener provides real-time trend detection for each monitored asset, giving you instant insights into market movements.

It displays each asset's position relative to its middle regression line, helping you understand price momentum.

The data is presented in a clean, organized table with color-coded trends for easy interpretation.

At its core, the screener performs trend detection based on regression slope calculations, clearly indicating whether an asset is in a bullish or bearish trend.

Each asset's price is tracked relative to its middle regression line, providing additional context about trend strength.

The color-coded visual feedback makes it easy to spot changes at a glance.

Built-in alerts notify you instantly when any asset experiences a trend change, ensuring you never miss important market moves.

Customization Tips

You can easily expand the screener by adding more symbols to the symbols array, adapting it to your watchlist.

The regression parameters can be adjusted to match your preferred trading timeframes and sensitivity.

The alert system is already configured to notify you of trend changes, but you can customize the alert messages and conditions to your needs.

Limitations

While powerful, the screener is bound by PineScript's limitation of 40 security calls, capping the maximum number of monitored assets.

Using AI to Help With Conversion

An interesting tip:

You can use AI tools to help convert single-asset indicators to screeners.

Simply provide the original code and ask for assistance in transforming it into a screener format. While the AI output might need some syntax adjustments, it can handle much of the heavy lifting in the conversion process.

Prompt (example) : " Please make a pinescript version 5 screener out of this indicator below or in attachment to scan 20 instruments "

I prefer Claude AI (Opus model) over ChatGPT for pinescript.

Conclusion

This screener transformation technique opens up endless possibilities for market analysis.

By following these steps, you can convert any indicator into a powerful multi-asset scanner, enhancing your trading toolkit significantly.

Remember: The power of a screener lies not just in monitoring multiple assets, but in applying consistent analysis across your entire watchlist in real-time.

Feel free to fork and modify this screener for your own needs.

Happy trading! 🚀📈

Daveatt

在脚本中搜索"信达股份40周年"

Industry Group Strength - IndiaPresenting the Industry Group Strength Indicator for India market, designed to help traders identify top-performing stocks within specific industry groups that are predefined.

⦿ Identifies Leading Stocks in Industry Groups

⦿ Analyses the following metrics

YTD Return : Measures stock performance from the start of the year.

RS Rating : Relative Strength rating for user-selected periods.

% Return : Percentage return over a user-selected lookback period.

Features

This indicator dynamically recognises the industry group of the current stock on the chart and ranks stocks within that group based on predefined data points. Traders can add this indicator to focus on top-performing stocks relative to their industry.

⦿ Color-coded for Easy Visualisation

You can choose from the following key metrics to rank stocks:

YTD Return

RS Rating

% Return

⦿ Table Format with Performance Metrics Compact mode

Vertical View

Horizontal View

All of the three metrics are shown in the compact mode and the current stock that is viewed is highlighted!

Vertical view

Horizontal view

Stock Ranking

Stocks are ranked based on their performance within industry groups, enabling traders to easily spot leaders and laggards in each sector. Color-coded gradients visually represent the stocks’ performance rankings, with higher percentile rankings indicating better performance.

Relative Strength (RS)

Relative Strength (RS) compares a stock’s performance against the benchmark index. The RS value is normalized from 1 to 99, making it easier to compare across different stocks. A rising RS value indicates that the stock is outperforming the market, helping traders quickly gauge relative performance within industry groups.

Limitations

At the time of developing this indicator, Pine requests are limited to 40 per script so the predefined symbols had to be filtered to 40 per Industry group

Stocks Filters

Filters that are used to filter the stocks in an Industry group to have maximum of 40 stocks

⦿ Auto, Chemical, Engineering, Finance, Pharma

Market Cap >= 1000 Crores and Market Cap <= 60000 Crores

Price >= 30 and Price <= 6000

50 Days Average ( Price * Volume ) >= 6 Crores

⦿ For rest of the Industry groups

Market Cap >= 1000 Crores and Market Cap <= 100000 Crores

Price >= 20 and Price <= 10000

50 Days Average ( Price * Volume ) >= 3 Crores

Credits

This indicator is forked from the Script for US market by @Amphibiantrading Thanks Brandon for the beginning of this indicator.

This indicator is built on TradingView’s new dynamic requests feature, thanks to @PineCoders for making this possible!

ICT IPDA Liquidity Matrix By AlgoCadosThe ICT IPDA Liquidity Matrix by AlgoCados is a sophisticated trading tool that integrates the principles of the Interbank Price Delivery Algorithm (IPDA), as taught by The Inner Circle Trader (ICT). This indicator is meticulously designed to support traders in identifying key institutional levels and liquidity zones, enhancing their trading strategies with data-driven insights. Suitable for both day traders and swing traders, the tool is optimized for high-frequency and positional trading, providing a robust framework for analyzing market dynamics across multiple time horizons.

# Key Features

Multi-Time Frame Analysis

High Time Frame (HTF) Levels : The indicator tracks critical trading levels over multiple days, specifically at 20, 40, and 60-day intervals. This functionality is essential for identifying long-term trends and significant support and resistance levels that aid in strategic decision-making for swing traders and positional traders.

Low Time Frame (LTF) Levels : It monitors price movements within 20, 40, and 60-hour intervals on lower time frames. This granularity provides a detailed view of intraday price actions, which is crucial for scalping and short-term trading strategies favored by day traders.

Daily Open Integration : The indicator includes the daily opening price, providing a crucial reference point that reflects the market's initial sentiment. This feature helps traders assess the market's direction and volatility, enabling them to make informed decisions based on the day's early movements, which is particularly useful for day trading strategies.

IPDA Reference Points : By leveraging IPDA's 20, 40, and 60-period lookbacks, the tool identifies Key Highs and Lows, which are used by IPDA as Draw On Liquidity. IPDA is an electronic and algorithmic system engineered for achieving price delivery efficiency, as taught by ICT. These reference points serve as benchmarks for understanding institutional trading behavior, allowing traders to align their strategies with the dominant market forces and recognize institutional key levels.

Dynamic Updates and Overlap Management : The indicator is updated daily at the beginning of a new daily candle with the latest market data, ensuring that traders operate with the most current information. It also features intelligent overlap management that prioritizes the most relevant levels based on the timeframe hierarchy, reducing visual clutter and enhancing chart readability.

Comprehensive Customization Options : Traders can tailor the indicator to their specific needs through an extensive input menu. This includes toggles for visibility, line styles, color selections, and label display preferences. These customization options ensure that the tool can adapt to various trading styles and preferences, enhancing user experience and analytical capabilities.

User-Friendly Interface : The tool is designed with a user-friendly interface that includes clear, concise labels for all significant levels. It supports various font families and sizes, making it easier to interpret and act upon the displayed data, ensuring that traders can focus on making informed trading decisions without being overwhelmed by unnecessary information.

# Usage Note

The indicator is segmented into two key functionalities:

LTF Displays : The Low Time Frame (LTF) settings are exclusive to timeframes up to 1 hour, providing detailed analysis for intraday traders. This is crucial for traders who need precise and timely data to make quick decisions within the trading day.

HTF Displays : The High Time Frame (HTF) settings apply to the daily timeframe and any shorter intervals, allowing for comprehensive analysis over extended periods. This is beneficial for swing traders looking to identify broader trends and market directions.

# Inputs and Configurations

BINANCE:BTCUSDT

Offset: Adjustable setting to shift displayed data horizontally for better visibility, allowing traders to view past levels and make informed decisions based on historical data.

Label Styles: Choose between compact or verbose label formats for different levels, offering flexibility in how much detail is displayed on the chart.

Daily Open Line: Customizable line style and color for the daily opening price, providing a clear visual reference for the start of the trading day.

HTF Levels: Configurable high and low lines for HTF with options for style and color customization, allowing traders to highlight significant levels in a way that suits their trading style.

LTF Levels: Similar customization options for LTF levels, ensuring flexibility in how data is presented, making it easier for traders to focus on the most relevant intraday levels.

Text Utils: Settings for font family, size, and text color, allowing for personalized display preferences and ensuring that the chart is both informative and aesthetically pleasing.

# Advanced Features

Overlap Management : The script intelligently handles overlapping levels, particularly where multiple timeframes intersect, by prioritizing the more significant levels and removing redundant ones. This ensures that the charts remain clear and focused on the most critical data points, allowing traders to concentrate on the most relevant market information.

Real-Time Updates : The indicator updates its calculations at the start of each new daily bar, incorporating the latest market data to provide timely and accurate trading signals. This real-time updating is crucial for traders who rely on up-to-date information to execute their strategies effectively and make informed trading decisions.

# Example Use Cases

Scalpers/Day traders: Can utilize the LTF features to make rapid decisions based on hourly market movements, identifying short-term trading opportunities with precision.

Swing Traders: Will benefit from the HTF analysis to identify broader trends and key levels that influence longer-term market movements, enabling them to capture significant market swings.

By providing a clear, detailed view of key market dynamics, the ICT IPDA Liquidity Matrix by AlgoCados empowers traders to make more informed and effective trading decisions, aligning with institutional trading methodologies and enhancing their market understanding.

# Usage Disclaimer

This tool is designed to assist in trading decisions, but it should be used in conjunction with other analysis methods and risk management strategies. Trading involves significant risk, and it is essential to understand the market conditions thoroughly before making trading decisions.

Moving Average Momentum SignalsBest for trade execution in lower timeframe (1m,5m,15m) with momentum confirmation in higher timeframes (2h,4h,1d)

This indicator relies on three key conditions to determine buy and sell signals: the price's deviation from a short-term moving average, the change in the moving average over time (past 10 candles), and the price's deviation from a historical price (40 candles). The strategy aims to target moments where the asset's price is likely to experience a reversal or momentum shift.

Conditions

Price deviation from short-term Moving Average (MA): Current candle close minus the 10-period MA (price action past 10 candles)

Change in Moving Average over time: Current 10-period MA minus the 10-period MA from 10 candles ago (price action past 20 candles)

Price deviation from historical price: Current close minus the close from 40 candles ago (price action past 40 candles)

Signal Generation Logic

Buy Signal: Triggered when all three conditions are positive. Confirmed if the previous signal was a sell or if there were no previous signals

Sell Signal: Triggered when all three conditions are negative. Confirmed if the previous signal was a buy or if there were no previous signals

Usage and Strategy

After back testing, I observed the higher timeframes were a good indication of momentum/sentiment that you can take note of while trading intraday on the lower time frames (time intervals stated above). Background highlights are also displayed for easier visualization of bullish/bearish skew in terms of the volume of signals generated.

Triple EMA + QQE Trend Following Strategy [TradeDots]The "Triple EMA + QQE Trend Following Strategy" harnesses the power of two sophisticated technical indicators, the Triple Exponential Moving Average (TEMA) and the Qualitative Quantitative Estimation (QQE), to generate precise buy and sell signals. This strategy excels in capturing shifts in trends by identifying short-term price momentum and dynamic overbought or oversold conditions.

HOW IT WORKS

This strategy integrates two pivotal indicators:

Triple Exponential Moving Average (TEMA): TEMA enhances traditional moving averages by reducing lag and smoothing the data more effectively. It achieves this by applying the EMA formula three times onto the price, as follows:

tema(src, length) =>

ema1 = ta.ema(src, length)

ema2 = ta.ema(ema1, length)

ema3 = ta.ema(ema2, length)

tema = 3*ema1 - 3*ema2 + ema3

This computation helps to sharpen the sensitivity to price movements.

Qualitative Quantitative Estimation (QQE): The QQE indicator improves upon the standard RSI by incorporating a smoothing mechanism. It starts with the standard RSI, overlays a 5-period EMA on this RSI, and then enhances the result using a double application of a 27-period EMA. A slow trailing line is then derived by multiplying the result with a factor number. This approach establishes a more refined and less jittery trend-following signal, complementing the TEMA to enhance overall market timing during fluctuating conditions.

APPLICATION

Referenced from insights on "Trading Tact," the strategy implementation follows:

First of all, we utilize two TEMA lines: one set at a 20-period and the other at a 40-period. Then following the rules below:

40-period TEMA is rising

20-period TEMA is above 40-period TEMA

Price closes above 20-period TEMA

Today is not Monday

RSI MA crosses the Slow trailing line

This strategy does not employ an active take profit mechanism; instead, it utilizes a trailing stop loss to allow the price to reach the stop loss naturally, thereby maximizing potential profit margins.

DEFAULT SETUP

Commission: 0.01%

Initial Capital: $10,000

Equity per Trade: 80%

Users are advised to adjust and personalize this trading strategy to better match their individual trading preferences and style.

RISK DISCLAIMER

Trading entails substantial risk, and most day traders incur losses. All content, tools, scripts, articles, and education provided by TradeDots serve purely informational and educational purposes. Past performances are not definitive predictors of future results.

Reference:

Trading Tact. What Is the QQE Indicator? Retrieved from: tradingtact.com

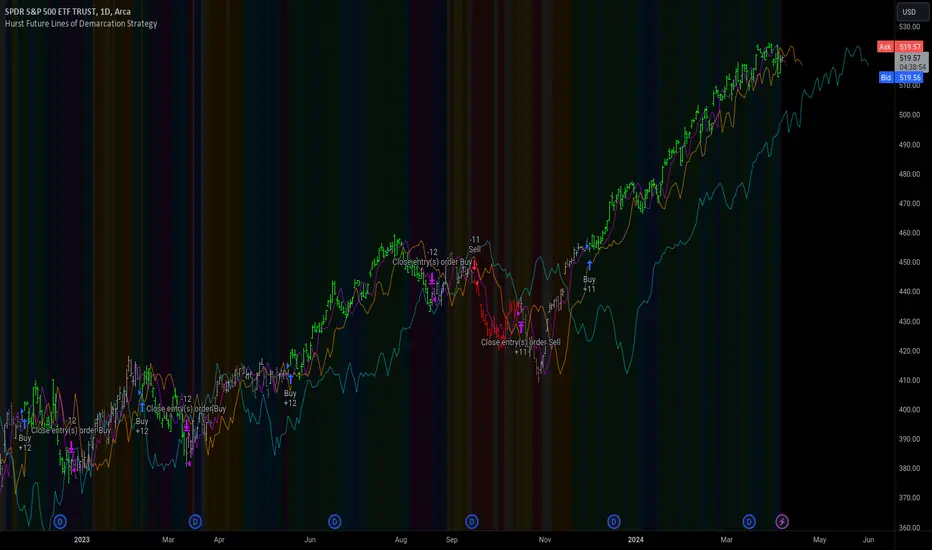

Hurst Future Lines of Demarcation StrategyJ. M. Hurst introduced a concept in technical analysis known as the Future Line of Demarcation (FLD), which serves as a forward-looking tool by incorporating a simple yet profound line into future projections on a financial chart. Specifically, the FLD is constructed by offsetting the price half a cycle ahead into the future on the time axis, relative to the Hurst Cycle of interest. For instance, in the context of a 40 Day Cycle, the FLD would be represented by shifting the current price data 20 days forward on the chart, offering an idea of future price movement anticipations.

The utility of FLDs extends into three critical areas of insight, which form the backbone of the FLD Trading Strategy:

A price crossing the FLD signifies the confirmation of either a peak or trough formation, indicating pivotal moments in price action.

Such crossings also help determine precise price targets for the upcoming peak or trough, aligned with the cycle of examination.

Additionally, the occurrence of a peak in the FLD itself signals a probable zone where the price might experience a trough, helping to anticipate of future price movements.

These insights by Hurst in his "Cycles Trading Course" during the 1970s, are instrumental for traders aiming to determine entry and exit points, and to forecast potential price movements within the market.

To use the FLD Trading Strategy, for example when focusing on the 40 Day Cycle, a trader should primarily concentrate on the interplay between three Hurst Cycles:

The 20 Day FLD (Signal) - Half the length of the Trade Cycle

The 40 Day FLD (Trade) - The Cycle you want to trade

The 80 Day FLD (Trend) - Twice the length of the Trade Cycle

Traders can gauge trend or consolidation by watching for two critical patterns:

Cascading patterns, characterized by several FLDs running parallel with a consistent separation, typically emerge during pronounced market trends, indicating strong directional momentum.

Consolidation patterns, on the other hand, occur when multiple FLDs intersect and navigate within the same price bandwidth, often reversing direction to traverse this range multiple times. This tangled scenario results in the formation of Pause Zones, areas where price momentum is likely to temporarily stall or where the emergence of a significant trend might be delayed.

This simple FLD indicator provides 3 FLDs with optional source input and smoothing, A-through-H FLD interaction background, adjustable “Close the Trade” triggers, and a simple strategy for backtesting it all.

The A-through-H FLD interactions are a framework designed to classify the different types of price movements as they intersect with or diverge from the Future Line of Demarcation (FLD). Each interaction (designated A through H by color) represents a specific phase or characteristic within the cycle, and understanding these can help traders anticipate future price movements and make informed decisions.

The adjustable “Close the Trade” triggers are for setting the crossover/under that determines the trade exits. The options include: Price, Signal FLD, Trade FLD, or Trend FLD. For example, a trader may want to exit trades only when price finally crosses the Trade FLD line.

Shoutouts & Credits for all the raw code, helpful information, ideas & collaboration, conversations together, introductions, indicator feedback, and genuine/selfless help:

🏆 @TerryPascoe

🏅 @Hpotter

👏 @parisboy

Rate of Change RSIIndicator Name: Rate of Change RSI

Description:

The Rate of Change (ROC) of the Relative Strength Index (RSI) is a technical indicator designed to provide insights into the momentum of an asset's price movement. It combines the Relative Strength Index (RSI), a popular momentum oscillator, with the Rate of Change (ROC) concept to assess the speed at which RSI values are changing.

How It Works:

Relative Strength Index (RSI): The RSI measures the magnitude of recent price changes to evaluate overbought or oversold conditions in an asset. It oscillates between 0 and 100, with readings above 70 typically indicating overbought conditions and readings below 30 indicating oversold conditions.

Rate of Change (ROC): The ROC calculates the percentage change in a given indicator over a specified period. In this indicator, we apply the ROC to the RSI values to determine how quickly the RSI is changing over time.

Key Features:

Acceleration and Deceleration: The ROC of RSI helps traders identify whether the momentum of the RSI is accelerating or decelerating. Positive values suggest increasing momentum, while negative values indicate decreasing momentum.

Dynamic Color Change: The color of the ROC RSI line changes dynamically based on the RSI level. When the RSI is between 0 and 40, the line color is blue, indicating potential oversold conditions. When the RSI is between 40 and 60, the line color is yellow, suggesting neutral conditions. When the RSI is above 60, the line color changes to green, indicating potential overbought conditions.

How to Use:

Acceleration: When the ROC RSI is positive and increasing while the RSI is above 60 (green), it may signal strong upward momentum.

Deceleration: Conversely, if the ROC RSI is negative and decreasing while the RSI is below 40 (blue), it may indicate weakening downward momentum.

Originality and Usefulness:

This indicator combines the RSI, a well-known momentum oscillator, with the ROC concept to provide a unique perspective on momentum dynamics. By dynamically adjusting the color of the ROC RSI line based on RSI levels, traders can quickly assess potential overbought or oversold conditions in the market.

Chart:

The chart displayed alongside this script provides a clean and easy-to-understand visualization of the ROC RSI indicator. The ROC RSI line color changes dynamically based on RSI levels, allowing traders to visually identify potential market conditions at a glance.

Cycles 90mThe cycles are separated by vertical lines. The first cycle (Q1) is marked with a red line because it is a manipulative cycle where you should not open positions. Other cycles are green (Q2, Q3, Q4).

You can add the time of the current candle, its size and position on the chart in the settings

The time is highlighted in red in the timeframes 9:30-9:40, 10:00-10:10, 11:00-11:30, 15:30-15:40, 16:00-16:10, 17:00-17:10, 17:30-17:40, as price movements are most often expected during these timeframes.

The cycle lines automatically disappear if you open a timeframe above M15

Optics Alert ZoneOptics Alert Zone shows price ranges for prices 17 days and 40 days ago. These can be adjusted based on asset class and volatility.

Bullish is when price is above 17 and 40 day.

Bearish is when price is below 17 and 40 day.

RSI & Backed-Weighted MA StrategyRSI & MA Strategy :

INTRODUCTION :

This strategy is based on two well-known indicators that work best together: the Relative Strength Index (RSI) and the Moving Average (MA). We're going to use the RSI as a trend-follower indicator, rather than a reversal indicator as most are used to. To the signals sent by the RSI, we'll add a condition on the chart's MA, filtering out irrelevant signals and considerably increasing our winning rate. This is a medium/long-term strategy. There's also a money management method enabling us to reinvest part of the profits or reduce the size of orders in the event of substantial losses.

RSI :

The RSI is one of the best-known and most widely used indicators in trading. Its purpose is to warn traders when an asset is overbought or oversold. It was designed to send reversal signals, but we're going to use it as a trend indicator by increasing its length to 20. The RSI formula is as follows :

RSI (n) = 100 - (100 / (1 + (H (n)/L (n))))

With n the length of the RSI, H(n) the average of days closing above the open and L(n) the average of days closing below the open.

MA :

The Moving Average is also widely used in technical analysis, to smooth out variations in an asset. The SMA formula is as follows :

SMA (n) = (P1 + P2 + ... + Pn) / n

where n is the length of the MA.

However, an SMA does not weight any of its terms, which means that the price 10 days ago has the same importance as the price 2 days ago or today's price... That's why in this strategy we use a RWMA, i.e. a back-weighted moving average. It weights old prices more heavily than new ones. This will enable us to limit the impact of short-term variations and focus on the trend that was dominating. The RWMA used weights :

The 4 most recent terms by : 100 / (4+(n-4)*1.30)

The other oldest terms by : weight_4_first_term*1.30

So the older terms are weighted 1.30 more than the more recent ones. The moving average thus traces a trend that accentuates past values and limits the noise of short-term variations.

PARAMETERS :

RSI Length : Lenght of RSI. Default is 20.

MA Type : Choice between a SMA or a RWMA which permits to minimize the impact of short term reversal. Default is RWMA.

MA Length : Length of the selected MA. Default is 19.

RSI Long Signal : Minimum value of RSI to send a LONG signal. Default is 60.

RSI Short signal : Maximum value of RSI to send a SHORT signal. Default is 40.

ROC MA Long Signal : Maximum value of Rate of Change MA to send a LONG signal. Default is 0.

ROC MA Short signal : Minimum value of Rate of Change MA to send a SHORT signal. Default is 0.

TP activation in multiple of ATR : Threshold value to trigger trailing stop Take Profit. This threshold is calculated as multiple of the ATR (Average True Range). Default value is 5 meaning that to trigger the trailing TP the price need to move 5*ATR in the right direction.

Trailing TP in percentage : Percentage value of trailing Take Profit. This Trailing TP follows the profit if it increases, remaining selected percentage below it, but stops if the profit decreases. Default is 3%.

Fixed Ratio : This is the amount of gain or loss at which the order quantity is changed. Default is 400, which means that for each $400 gain or loss, the order size is increased or decreased by a user-selected amount.

Increasing Order Amount : This is the amount to be added to or subtracted from orders when the fixed ratio is reached. The default is $200, which means that for every $400 gain, $200 is reinvested in the strategy. On the other hand, for every $400 loss, the order size is reduced by $200.

Initial capital : $1000

Fees : Interactive Broker fees apply to this strategy. They are set at 0.18% of the trade value.

Slippage : 3 ticks or $0.03 per trade. Corresponds to the latency time between the moment the signal is received and the moment the order is executed by the broker.

Important : A bot has been used to test the different parameters and determine which ones maximize return while limiting drawdown. This strategy is the most optimal on BITSTAMP:ETHUSD with a timeframe set to 6h. Parameters are set as follows :

MA type: RWMA

MA Length: 19

RSI Long Signal: >60

RSI Short Signal : <40

ROC MA Long Signal : <0

ROC MA Short Signal : >0

TP Activation in multiple ATR : 5

Trailing TP in percentage : 3

ENTER RULES :

The principle is very simple:

If the asset is overbought after a bear market, we are LONG.

If the asset is oversold after a bull market, we are SHORT.

We have defined a bear market as follows : Rate of Change (20) RWMA < 0

We have defined a bull market as follows : Rate of Change (20) RWMA > 0

The Rate of Change is calculated using this formula : (RWMA/RWMA(20) - 1)*100

Overbought is defined as follows : RSI > 60

Oversold is defined as follows : RSI < 40

LONG CONDITION :

RSI > 60 and (RWMA/RWMA(20) - 1)*100 < -1

SHORT CONDITION :

RSI < 40 and (RWMA/RWMA(20) - 1)*100 > 1

EXIT RULES FOR WINNING TRADE :

We have a trailing TP allowing us to exit once the price has reached the "TP Activation in multiple ATR" parameter, i.e. 5*ATR by default in the profit direction. TP trailing is triggered at this point, not limiting our gains, and securing our profits at 3% below this trigger threshold.

Remember that the True Range is : maximum(H-L, H-C(1), C-L(1))

with C : Close, H : High, L : Low

The Average True Range is therefore the average of these TRs over a length defined by default in the strategy, i.e. 20.

RISK MANAGEMENT :

This strategy may incur losses. The method for limiting losses is to set a Stop Loss equal to 3*ATR. This means that if the price moves against our position and reaches three times the ATR, we exit with a loss.

Sometimes the ATR can result in a SL set below 10% of the trade value, which is not acceptable. In this case, we set the SL at 10%, limiting losses to a maximum of 10%.

MONEY MANAGEMENT :

The fixed ratio method was used to manage our gains and losses. For each gain of an amount equal to the value of the fixed ratio, we increase the order size by a value defined by the user in the "Increasing order amount" parameter. Similarly, each time we lose an amount equal to the value of the fixed ratio, we decrease the order size by the same user-defined value. This strategy increases both performance and drawdown.

Enjoy the strategy and don't forget to take the trade :)

TICK - Custom Tickers [Pt]Traditionally, the TICK index is a technical analysis indicator that shows the difference in the number of stocks that are trading on an uptick vs a downtick in a particular period of time. This indicator allows user to choose up to 40 tickers to calculate TICK.

By default, it uses the SPY Top 40 stocks, but can be changed to any tickers.

There are options to show:

- Top 7 , ie. can be used for just showing TICK for FAANGMT => $FB + $AMZN + $AAPL + $NFLX + $GOOG + $MSFT + $TSLA

- Top 10

- Top 20

- Top 30

- Top 40

Data can be displayed in candle bars, line, or both.

Enjoy~

Strategy Myth-Busting #23 - 2xEMA+DPO- [MYN]#23 on the Myth-Busting bench, we are automating the "Best Funded Account Trading Strategy (Pass EVERY Challenge!)" strategy from "Trade with Pat" who claims this strategy will pass every trading challenge out there.

This strategy uses 3 open source indicators. 2 EMA's. The first one (Slow) is set to a length of 40 and a fast EMA which is set to 12. This strategy uses the crossover of the fast( 12) EMA over the Slow EMA ( 40 ) as the primary means to enter a long position. The opposite when the fast EMA crosses under the slow EMA as a means to indicate a short position. This strategy uses the DPO (Detrended Price Oscillaor) from the Uptrend Price DPO indicator in the same way we would traditionally use a stochastic or moving average convergence/divergence indicator like the MACD . Basically, the DPO helps evaluate and estimate the length of the price cycle from peak to peek or through to trough and in this strategy confirms entry of a long / short condition complimenting the EMA crossover/crossunders.

And as always, If you know of or have a strategy you want to see myth-busted or just have an idea for one, please feel free to message me.

This strategy uses a combination of 2 open-source public indicators:

EMA x2 ( 40 and 12)

Untrend Price DPO indicator by jTradeuh

Trading Rules

1 or 4 hour candles

Stop loss at previous highest-high (Short) and lowest-low (Long).

Take Profit 2 - 2.5 the risk

Strategy Template includes open source code from the following:

Performance Summary Dashboard by @VertMT

Time Of Day Window by @ddctv

Monthly Table Performance Dashboard by @QuantNomad

Chop and explode (ps5)Description : This is a renovated version of my previous mod that was based on the original script from fhenry0331.

Added are:

a data cleaning function

a seasonal random index function

an updated scaler and

a signalling procedure.

-

The following description is moved here from the old script.

The purpose of this script is to decipher chop zones from runs/movement/explosion spans. The chop is RSI movement between 40 and 60. Tight chop is RSI movement between 45 and 55. There should be an explosion after RSI breaks through 60 (long) or 40 (short). Tight chop bars are colored gray, a series of gray bars indicates a tight consolidation and should explode imminently. The longer the chop the longer the explosion will go for. The tighter the better. Loose chop (jig saw/gray bars on the silver background) will range between 40 and 60. The move begins with green and red bars.

Couple it with your trading system to help stay out of chop and enter when there is a movement.

Counting Stars Overlay [Market Overview Series]Hi fellow tradeurs,

So it's always been my goal to provide one of my best scripts. This is from what I call my "Market Overview" series. It is a scanner for my second best script to date. Market Overview bc of its origins as a scanner of the Kucoin Margin Coins. I realize that there are more coins that there are more margin coins that Kucoin has but I wanted to have a solid 40 coins on each coin "set". If you are unfamiliar with what I mean by 'sets' then you can view my other scanner scripts on this account for futher elaboration but to sum it up....there are 4 sets of coins I have to choose from in the settings. Each set has 40 coins in them (as there is a cap of 40 security calls that can be made per each iteration of the script on the chart). That being said...if you have the capabilities then add this script 4 times to your chart and select a diff set for each copy of the script. This has the scanner in a way that I've yet to present in my others scripts. When the alert for a coin goes off then the coins name will be printed as a label over the main chart. BTW, this was built for the 1 min timeframe and have used it EXTENSIVELY and this is the best TF for how the settings are set. I will also publish another script that will be a visual aid for this one but will rather show all the plots associated with the code that is in this scanner. Know that for the scanner it'll be best to choose a coin that has at least 1 trade/update/printed candle per minute (to be safe use BTC or ETH chart or else some of the signals will be printed if the signal arrives at a point in time where the coin on the screen does not print a candle bc no new trade or update to trades occur in TradingView. For the visual aid script that I will add right after this, there will be 20 different plots that appear. When the AVG of all of these plots is beyond the OverBought line and then the AVG line is falling for 2 bars...THEN the long signal for that coin is generated (and vise versa for short signals) Lastly regarding the visual aid script, THAT ONE will ONLY show the 20 plots that are associated with the coin that the chart is selected for. So that one is not a scanner and is just a stand alone script (again) to show whats going on in the background of this scanner. Now, once you add it however many time you want to see however many sets of coins you want, I recommend merging the scales so that they are all on one scale. I prefer mine being on the left side but all you have to do is select the 3 dots in the scripts settings in the chart window and select the scale location line and it'll open another set of lines at which point you can select "merge to scale Z" (that will be the left scale) and will put all the scales together on the left. I forgot ****If you want to see a whole diff exchange's coins you much make changes to this original script and it is further described how to do so in one of my first publications**** I REALLY hope it becomes of some benefit to you in your trading as it abundantly has in my own. It is after all one of the best of my best. Ohh, I forgot to add alerts to this but will do so immediately following this. To finish, this script DOES NOT REPAINT as far as I have EVER seen (and I have extensively searched for it bc of how good the signals were, I figured I MUST HAVE made a mistake and it did so...but alas...it does not. If you notice something on the contrary do notify me immediately with the coin, exchange, TF, and time of the occurrence and we can go from there. If anyone has any great ideas for the script then please do also let me know and if I find anyone with some abilities that mingle well with my own then lets talk as I'm always looking for good ol chaps to help me out with other scripts bc if you think this is good....well....you must imagine that I've got better that I have not/am not publishing. Aaaaaanywho, goodluck to you all. I wish you the best. ***I've got good info on how to look out for false signals but I want to see what yall come up with first before I give away all my alpha.

AND if anyone asks questions that Ive already touched on in this description or already in the comments sections then maybe someone there would be willing to waste their time answering them bc I've done quite a bit of work here that I am HAPPY to hand over to the general public but if you are not willing to do the work in reading to possibly answer your inquiries that have already been answered then I am not willing to do that work for you again. Peace and love people...peace and love. Im out.

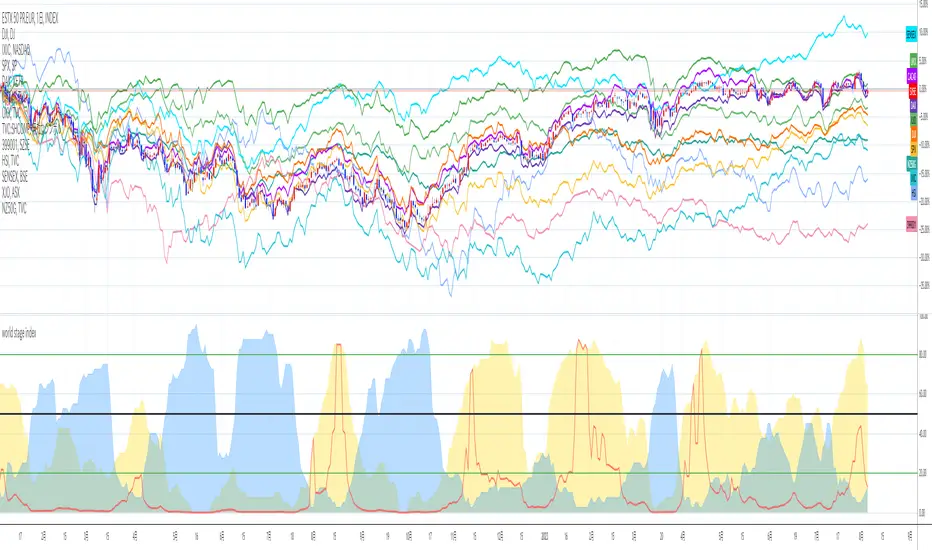

world stage index ver02This is an indicator that expresses the ratio of "stage1" and "stage4" of world index.

40 symbols are as follows

("TVC:SHCOMP" is revised to "SSE:000001")

(JAPAN, US, EUROPE, and CANADA)

OSE:NK2251!, DJ:DJI , NASDAQ:IXIC, SP:SPX , XETR:DAX, TVC:CAC40 , TVC:UKX, TSX:TSX

(ASIA)

SSE:000001, SZSE:399001, TVC:HSI, TWSE:TAIEX, BSE:SENSEX , OANDA:SG30SGD, INDEX:KSI, SET:SET

(EUROPE)

INDEX:SX5E, INDEX:FTSEMIB, SIX:SMI , BME:IBC, EURONEXT:BEL20, TVC:AEX, OMXCOP:OMXC25, XETR:0Q5X

(Pacific Ocean)

ASX:XJO, TVC:NZ50G, IDX:COMPOSITE, FTSEMYX:FBMKLCI, BMFBOVESPA:IBOV, BMV:ME , BVL:SPBLPGPT, BYMA:IMV

(Eastern Europe & Middle East)

MOEX:IMOEX, GPW:WIG20, OMXHEX:OMXH25, OMXSTO:OMXS30, DFM:DFMGI, TADAWUL:TASI, OSE:GNRI, EGX:EGX30

The criteria are as follows:

EMA5≧EMA20≧EMA40 : Stage1

EMA5≦EMA20≦EMA40 : Stage4

A.The sum of Stage1 was multiplied by 2.5 and drawn on a scale of 0 to 100, with yellow area

B.The Sum of Stage4 was multiplied by 2.5 and drawn on a scale of 0 to 100, with blue area.

C. The ratio of A/B was multiplied by 2.5 and drawn on a scale of 0 to 100, with red lines.

This idea is from Kojirou Kousi.

40 symbols of this script are partially different from Kojiro kousi's idea.

But he said the difference isn't matter.

tradingview社の上海総合指数の銘柄コード変更に合わせて、"TVC:SHCOMP" を "SSE:000001"に改訂しました。

「小次郎講師指数」に着想を得た、世界40カ国の株価指数stage状態です。

参考文献は、小次郎講師著書「世界一わかりやすい投資の勝ち方」です。

小次郎講師とは一部異なるシンボルを採用していますが、

多少の違いは余り大した問題では無いと御本人から教わった事があります。

先進国に関してはおそらくほとんど同じだと思います。

stage1の合計の%を黄色、stage4の合計の%を青色、stage1の合計/stage4の合計の%を赤で表示しています。

雰囲気で分かればいいので、正確な数字までは表示しませんでした。

個人的には現状分析以外にも、プラクティス時に世界情勢を把握するのに重宝しています。

world stage indexThis is an indicator that expresses the ratio of "stage1" and "stage4" of world index.

40 symbols are as follows

(JAPAN, US, EUROPE, and CANADA)

OSE:NK2251!, DJ:DJI, NASDAQ:IXIC, SP:SPX, XETR:DAX, TVC:CAC40, TVC:UKX, TSX:TSX

(ASIA)

TVC:SHCOMP, SZSE:399001, TVC:HSI, TWSE:TAIEX, BSE:SENSEX, OANDA:SG30SGD, INDEX:KSI, SET:SET

(EUROPE)

INDEX:SX5E, INDEX:FTSEMIB, SIX:SMI, BME:IBC, EURONEXT:BEL20, TVC:AEX, OMXCOP:OMXC25, XETR:0Q5X

(Pacific Ocean)

ASX:XJO, TVC:NZ50G, IDX:COMPOSITE, FTSEMYX:FBMKLCI, BMFBOVESPA:IBOV, BMV:ME, BVL:SPBLPGPT, BYMA:IMV

(Eastern Europe & Middle East)

MOEX:IMOEX, GPW:WIG20, OMXHEX:OMXH25, OMXSTO:OMXS30, DFM:DFMGI, TADAWUL:TASI, OSE:GNRI, EGX:EGX30

The criteria are as follows:

EMA5≧EMA20≧EMA40 : Stage1

EMA5≦EMA20≦EMA40 : Stage4

A.The sum of Stage1 was multiplied by 2.5 and drawn on a scale of 0 to 100, with yellow area

B.The Sum of Stage4 was multiplied by 2.5 and drawn on a scale of 0 to 100, with blue area.

C. The ratio of A/B was multiplied by 2.5 and drawn on a scale of 0 to 100, with red lines.

This idea is from Kojirou Kousi.

40 symbols of this script are partially different from Kojiro kousi's idea.

But he said the difference isn't matter.

「小次郎講師指数」に着想を得た、世界40カ国の株価指数stage状態です。

参考文献は、小次郎講師著書「世界一わかりやすい投資の勝ち方」です。

小次郎講師とは一部異なるシンボルを採用していますが、

多少の違いは余り大した問題では無いと御本人から教わった事があります。

先進国に関してはおそらくほとんど同じだと思います。

stage1の合計の%を黄色、stage4の合計の%を青色、stage1の合計/stage4の合計の%を赤で表示しています。

雰囲気で分かればいいので、正確な数字までは表示しませんでした。

個人的には現状分析以外にも、プラクティス時に世界情勢を把握するのに重宝しています。

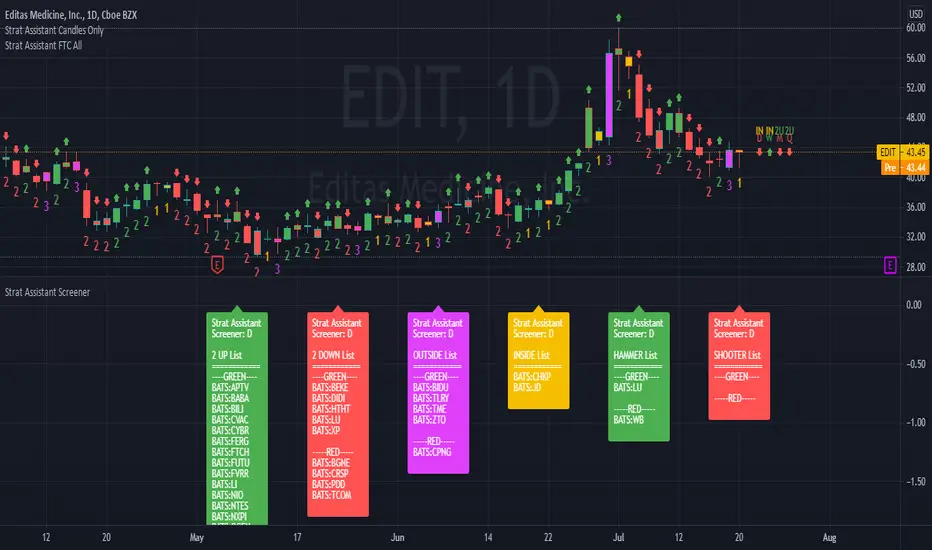

Strat Assistant ScreenerStrat Assistant Screener

----------------------------

█ OVERVIEW

This script is intended to provide screening/scanning functionality for the strat for the time period provided in the input (Day is the default).

When added, the script provides a chart with labels separated for each type of candle (2 up, 2 down, outside, inside) as well as actionable signals (inside already provided, hammer, shooter). Trading view is limited to 40 "security/ticker/symbol" calls so only 40 at a time are available. It's best to run this on higher time frames as it will occasionally push peak trading view memory limits and throw an error. Various inputs are provided a detailed below. It's not FAST so be patient please.

█ DETAIL

Inputs

----------

Security/Screener Time Frame: The screener will only run for one time frame, the time frame selected and this can be changed

Actionable Wick Percentage: The percentage of the WICK to determine a hammer or a shooter. For example, the default is .75 or 75%, which means 75% of the candle must be a WICK (top wick 75% for shooter, bottom wick 75% for hammer). If you wish to be more conservative scale it down or more aggressive scale it up

Label Index Offset Factor: There are 6 separate labels that will appear at the bottom separated by this indicator. If you feel like things are too tight or too narrow you can adjust this to spread things out further, or push them closer together.

Security/SXX: The various securities that can be input to track. If you find this is a pain, you can always copy the source code, put it in the pine editor yourself, and manually modify them there. Trading view limits you to 40 securities/symbols/tickers so I've pushed the limit as far as I can with this script.

Outputs

----------

The screener will provide a second chart at the bottom of the primary chart with labels for the types of candles and actionable signals

Each label will be present even if no results are found.

The label will display the time frame selected toward the end of the header - Strat Assistant Screener:

Each label is colored for quick reference to indicate the various bull/bear/inside/outside "patterns"

Best Practices

----------

It is not fast, so please be patient and let it run.

This screener is best used as a utility a few times a day, not recommended for intraday. I will create a scaled down version of this will only 5 securities/symbols/tickers that can be used intraday.

The screener pushes the limits of training views provided memory, so you may occasionally see errors, please try a higher time frame.

The bottom chart can be scaled and moved just like the top one, play around with it to determine what works best for you. I recommend decreasing the scale and then moving it up so you can see it better.

When the time frame is changed, it will take a minute, you can verify the results by seeing the time frame change in the label - Strat Assistant Screener:

I have not played with this thoroughly intraday yet. So it may be buggy/slower.

Modified RSI Multi-Time Frame (HM)Effective RSI with Multi-Timeframe with Hilema - Milega(HM) concept (HM=WMA -EMA). RSI Script is included with WMA and EMA band for RSI1 and it works very simple

i) When the RSI band turns to Green its a Buy signal. Normally whenever Bearish strength weakens and move towards the Bullish area, the WMA and EMA cross each other and that tends to provide a possible trend change. A trade at crossover normally provides a very good trading oppertunity. One can combine with some other Price action if needed for double confirmation.

ii)When RSI band turns to RED its a Sell signal. As explained in the point 1 , its a vice-versa where a crossover of WMA and EMA is perfect entry to get a good swing trade. Once can combine this tool with Price action for double confirmation.

iii) Using the Multi timeframe user could able to find the trend at higher timeframe to take double confirm on the trend strength and take a perfect oppertunity to take the trade.

By default, script uses the RSI with length 14, WMA 21 and EMA 3 which perfectly working for Index in NSE. Please change as per your requirement.

Apart from the above band, RSI is not have the different levels like 20/ 40 /50/60/80

Multi-timeframes currently set as

RSI1 - Same as Chart

RSI2 - 15 Min

RSI3 - 60 Min

RSI4 - Daily

Script has enabled the option to change the values for these timeframes as per the user requirement.

These ranges can be interpreted and acts as a probable swing points based on the trend and momentum.

40-60 - Neutral Range or Sideways

20 - 60 Bearish range

40 - 70 - Bullish range

Below 20 -- Over Sold Zone

Above 80 - over Bought zone

Also, the crossovers of the WMA and EMA on the RSI gives a very good momentum towards that trend.

ADX with SignalsThis indicator basicly usind ADX ( Average Directional Index )

ADX can show us how trend is strong

ADX below 20: the market is currently not trending

ADX crosses above 20: signifies that a new trend is emerging. Traders may start placing sell or buy orders in the direction of the price movement.

ADX between 20 and 40: When the ADX is growing between 20 and 40 it is considered as a confirmation of an emerging trend. Traders should use this opportunity to buy or short sell in the trend's direction.

ADX above 40: the trend is very strong.

ADX crosses 50: the trend is extremely strong.

ADX crosses 70: a very rare occasion, which is called a “Power Trend.”

If we use ADX with DI+ and DI+ indactor can tell us to buy.

How can we calculate this all?

Directional Movement (DI) is defined as the largest part of the current period’s price range that lies outside the previous period’s price range. For each period calculate:

+DI = positive or plus DI = High - Previous High

-DI = negative or minus DI = Previous Low - Low

The smaller of the two values is reset to zero, i.e., if +DI > -DI , then -DI = 0. On an inside bar (a lower high and higher low), both +DI and -DI are negative values, so both get reset to zero as there was no directional movement for that period.

The True Range ( TR ) is calculated for each period, where:

TR = Max of ( High - Low ), ( High -PreviousClose ), ( PreviousClose - Low )

The +DI , -DI and TR are each accumulated and smoothed using a custom smoothing method proposed by Wilder. For an n period smoothing, 1/n of each period’s value is added to the total each period, similar to an exponential smoothing:

+DIt = (+DIt-1 - (+DIt-1 / n)) + (+DIt)

-DIt = (-DIt-1 - (-DIt-1 / n)) + (-DIt)

TRt = (TRt-1 - (TRt-1 / n)) + ( TRt )

Compute the positive/negative Directional Indexes, +DI and -DI , as a percentage of the True Range:

+DI = ( +DI / TR ) * 100

-DI = ( -DI / TR ) * 100

Compute the Directional Difference as the absolute value of the differences: DIdiff = | (( +DI ) - ( -DI )) |

Sum the directional indicator values: DIsum = (( +DI ) + ( -DI )) .

Calculate the Directional Movement index: DX = ( DIdiff / DIsum ) * 100 . The DX is always between 0 and 100.

Finally, apply Wilder’s smoothing technique to produce the final ADX value:

ADXt = ( ( ADXt-1 * ( n - 1) ) + DXt ) / n

When indicator tell us to buy?

If when DI+ crosses DI- and ADX is bigger than DI- indicator tell us to buy.

RSI Step Oscillator [racer8]Purpose of RSO is to identify when RSI has reached key levels. These levels are 80, 70, 60, 40, 30, and 20.

When indicator displays a bar with color...

Purple : RSI > 80

Blue : RSI > 70

Green : RSI > 60

Gray : RSI is inbetween 40 and 60.

Yellow : RSI < 40

Orange : RSI < 30

Red : RSI < 20

Hit the like button and enjoy 😁

ADX+DMI_by_BIMashed together Chris Moody's ADX thing with his DMI thing.

So you can see trend strength + direction

green-ish = uptrend-ish//red-ish = downtrend-ish

Colors can be adjusted though.

below 10 = gray, not much going on

10 - 20 = light green/light red, could be the beginning o something

20 - 40 = bright green / bright red, something is going on

above 40 = dark green, dark red, exhaustion (default is 40, can be adjusted to whatever)

RSI with Visual Buy/Sell Setup | Corrective/Impulsive IndicatorRSI with Visual Buy/Sell Setup | 40-60 Support/Resistance | Corrective/Impulsive Indicator v2.15

|| RSI - The Complete Guide PDF ||

Modified Zones with Colors for easy recognition of Price Action.

Resistance @ downtrend = 60

Support @ uptrend = 40

Over 70 = Strong Bullish Impulse

Under 30 = Strong Bearish Impulse

Uptrend : 40-80

Downtrend: 60-20

--------------------

Higher Highs in price, Lower Highs in RSI = Bearish Divergence

Lower Lows in price, Higher Lows in RSI = Bullish Divergence

--------------------

Trendlines from Higher/Lower Peaks, breakout + retest for buy/sell setups.

###################

There are multiple ways for using RSI, not only divergences, but it confirms the trend, possible bounce for continuation and signals for possible trend reversal.

There's more advanced use of RSI inside the book RSI: The Complete Guide

Go with the force, and follow the trend.

"The Force is more your friend than the trend"

Chop and explodeThe purpose of this script is to decipher chop zones from runs/movement/explosion

The chop is RSI movement between 40 and 60

tight chop is RSI movement between 45 and 55. There should be an explosion after RSI breaks through 60 (long) or 40 (short). Tight chop bars are colored black, a series of black bars is tight consolidation and should explode imminently. The longer the chop the longer the explosion will go for. tighter the better.

Loose chop (whip saw/yellow bars) will range between 40 and 60.

the move begins with blue bars for long and purple bars for short.

Couple it with your trading system to help stay out of chop and enter when there is movement. Use with "Simple Trender."

Best of luck in all you do. Get money.