Monthly MA Close Generates buy or sell signal if monthly candle closes above or below the signal MA.

Long positions only.

Inputs:

-Change timeframe MA

-Change period MA

-Use SMA or EMA

-Display MA

-Use another ticker as signal

-Select time period for backtesting

This script is not necessarily written to maximize profits, but to minimize losses.

Although it can outperform 'Buy & Hold' on some occasions when there is a multiple month bearisch trend.

You can optimise this strategy by changing the signal MA inputs.

I would suggest aiming for the best Profit Factor starting from the monthly ("M") setting.

You can always fine-tune the results at a lower timeframe.

The option to use another ticker for providing signals can give you a more stable and unified results.

For example using AMEX:SPY as signal with default parameters gives better results with NASDAQ:AAPL than if you would use NASDAQ:AAPL itself.

I used the anti-repainting function from PineCoders to prevent repainting.

This script is best used for multi-month trading positions & Daily or 4H setting of your chart.

在脚本中搜索"文华财经tick价格"

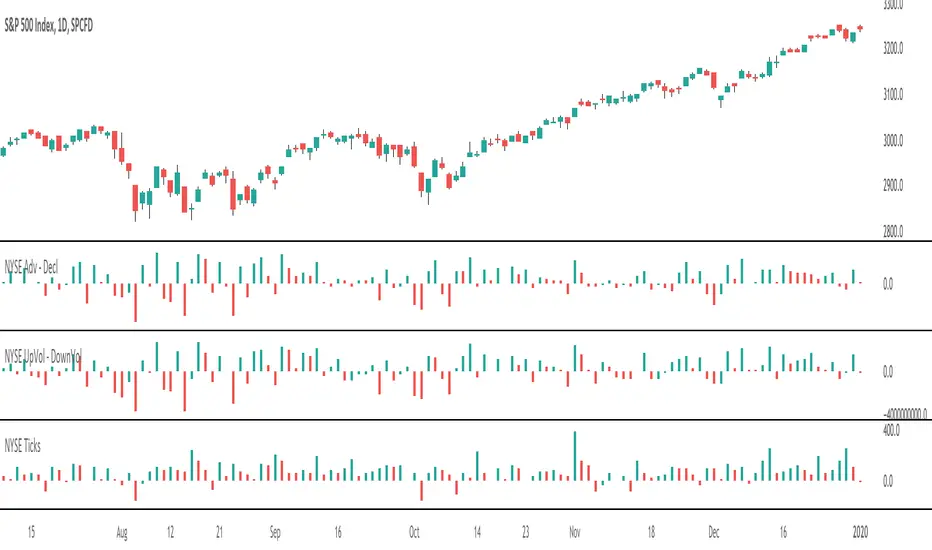

NYSE TicksDisplays NYSE ticks as histogram.

Part of market internals dashboard, so make sure to check the other indicators as well.

NeoButane Bitfinex BTC Longs vs. Shorts Tickers Simplified (MtF)With optional overlay for high/low candle values and daily resolution close. Now with MtF to add customization .

Made because I'm too lazy to constantly re-add tickers and to reduce noise.

High Tick Volume Alert (Classic Style)This indicator has the classic appearance of the volume indicator for tick volume. It notifies you according to your individual settings when there is increased volume on price.

Hammer + EMA Strategy with Tick-based SL/TPWhat This Script Does:

Detects Hammer (bullish reversal) and Inverted Hammer (bearish reversal) patterns

Requires a simple trend context (using 2 bars back)

Confirms price position relative to EMA 50

Applies tick-based SL and TP

Plots buy/sell signals on chart with emoji labels

Futures Tick and Point Value TableDisplays a table in the upper right corner of the chart showing the tick and point value in USD.

Big 8 Intraday TICKAt the start of each trading day (0930 EST), this indicator calculates the intraday price difference between open and close for the eight largest market cap stocks (AAPL, AMZN, GOOGLE, META, MSFT, NFLX, NVDA, and TSLA), assigns a +/-1 for each, and then plots the cumulative change. An EMA has been added for smoothing purposes that is set to 5 but can be changed. Please note indicator is best used on lower timeframes (15 min or less) and has no applicability to time frames above 1 hour.

The thought behind this indicator is those eight major stocks drive a majority of intraday price change in indices like SPY and QQQ that are heavily weighted towards these stocks, therefore they should be a leading indicator in price change. You can often catch a move in SPY or QQQ one to two bars (on 1 min chart) ahead of the actual move because you see this indicator moving strong to one direction.

It's not perfect as there are divergences you will see when you compare historical charts, but oftentimes those divergences ultimately lead to significant price swings in the same direction as this indicator, so recommend being on watch to pull the trigger when you see those and price confirms.

You can use this indicator in a few ways:

1. Confirmation that your current trade is in the same direction as this indicator

2. Use the zero cross as a trigger for put or call entry

3. Focusing only on calls/longs if the value is above 0, or only puts/shorts if the value is below zero. Just be sure to keep an eye on reversals.

If you have recommendations on how to improve, let me know and I'll do my best to make changes.

Inflation Adjusted Performance: Ticker/M2 money supplyPlots current ticker / M2 money supply, to give an idea of 'inflation adjusted performance'.

~In the above, see the last decade of bullish equities is not nearly as impressive as it seems when adjusted to account for the FED's money printing.

~Works on all timeframes/ assets; though M2 money supply is daily data release, so not meaningful to plot this on timeframe lower than daily.

~To display on same pane; comment-out line 6 and un-comment line 7; then save, remove and re-add indicator.

~Scale on the right is meaningless; this indicator is just to show/compare the shape of the charts.

Get Ticker Name - JDThis is a small helper script that can help you in case you need to enter exact ticker names in a script.

Gr, JD.

[CLX][#01] Animation - Price Ticker (Marquee)This indicator displays a classic animated price ticker overlaid on the user’s current chart. It is possible to fully customize it or to select one of the predefined styles.

A detailed description will follow in the next few days.

Used Pinescript technics:

- varip (view/animation)

- tulip instance (config/codestructur)

- table (view/position)

By the way, for me, one of the coolest animated effects is by Duyck

We hope you enjoy it! 🎉

CRYPTOLINX - jango_blockchained 😊👍

Disclaimer:

Trading success is all about following your trading strategy and the indicators should fit within your trading strategy, and not to be traded upon solely.

The script is for informational and educational purposes only. Use of the script does not constitute professional and/or financial advice. You alone have the sole responsibility of evaluating the script output and risks associated with the use of the script. In exchange for using the script, you agree not to hold dgtrd TradingView user liable for any possible claim for damages arising from any decision you make based on use of the script.

Crypto Base TickerAn example of using str.replace_all() function to extract a crypto ticker without its pair.

It can be useful if you didn't know syminfo.basecurrency existed.

I didn't know syminfo.basecurrency exists. Lol

Average True Range Pivot(2) High and ATR tick colorsTakes original colored ATR tick code from Autarch_Capital and adds pivot (2) high. In image the green upticks are thickened to make them easier to see. Can change in settings.

HG Scalpius - ATR Up/Down Tick HighlightHG Scalpius - ATR Up/Down Tick Highlight

This indicator highlights ATR(14) upticks (green) and downticks (red) and has the below application:

- If a new trend closing high (low) is made on a downtick in ATR, decreasing volatility mode turns on

If you come across or think of any other useful scripts for the HG Scalpius system please comment below!

Links to 2 previous HG Scalpius scripts:

-

-

Happy trading!

Code:

study(title="Average True Range", shorttitle="ATR", overlay=false)

length = input(title="Length", defval=14, minval=1)

smoothing = input(title="Smoothing", defval="RMA", options= )

ma_function(source, length) =>

if smoothing == "RMA"

rma(source, length)

else

if smoothing == "SMA"

sma(source, length)

else

if smoothing == "EMA"

ema(source, length)

else

wma(source, length)

ATR = ma_function(tr(true), length)

c = ATR >= ATR ? color.lime : color.red

plot(ATR, title = "ATR", color=c, transp=0)

Volume per minimum tickThis script calculates the volume traded per minimum tick of a scrip and is an indicator that the price move is justified by volume and trader interest

ApicodeLibrary "Apicode"

percentToTicks(percent, from)

Converts a percentage of the average entry price or a specified price to ticks when the

strategy has an open position.

Parameters:

percent (float) : (series int/float) The percentage of the `from` price to express in ticks, e.g.,

a value of 50 represents 50% (half) of the price.

from (float) : (series int/float) Optional. The price from which to calculate a percentage and convert

to ticks. The default is `strategy.position_avg_price`.

Returns: (float) The number of ticks within the specified percentage of the `from` price if

the strategy has an open position. Otherwise, it returns `na`.

percentToPrice(percent, from)

Calculates the price value that is a specific percentage distance away from the average

entry price or a specified price when the strategy has an open position.

Parameters:

percent (float) : (series int/float) The percentage of the `from` price to use as the distance. If the value

is positive, the calculated price is above the `from` price. If negative, the result is

below the `from` price. For example, a value of 10 calculates the price 10% higher than

the `from` price.

from (float) : (series int/float) Optional. The price from which to calculate a percentage distance.

The default is `strategy.position_avg_price`.

Returns: (float) The price value at the specified `percentage` distance away from the `from` price

if the strategy has an open position. Otherwise, it returns `na`.

percentToCurrency(price, percent)

Parameters:

price (float) : (series int/float) The price from which to calculate the percentage.

percent (float) : (series int/float) The percentage of the `price` to calculate.

Returns: (float) The amount of the symbol's currency represented by the percentage of the specified

`price`.

percentProfit(exitPrice)

Calculates the expected profit/loss of the open position if it were to close at the

specified `exitPrice`, expressed as a percentage of the average entry price.

NOTE: This function may not return precise values for positions with multiple open trades

because it only uses the average entry price.

Parameters:

exitPrice (float) : (series int/float) The position's hypothetical closing price.

Returns: (float) The expected profit percentage from exiting the position at the `exitPrice`. If

there is no open position, it returns `na`.

priceToTicks(price)

Converts a price value to ticks.

Parameters:

price (float) : (series int/float) The price to convert.

Returns: (float) The value of the `price`, expressed in ticks.

ticksToPrice(ticks, from)

Calculates the price value at the specified number of ticks away from the average entry

price or a specified price when the strategy has an open position.

Parameters:

ticks (float) : (series int/float) The number of ticks away from the `from` price. If the value is positive,

the calculated price is above the `from` price. If negative, the result is below the `from`

price.

from (float) : (series int/float) Optional. The price to evaluate the tick distance from. The default is

`strategy.position_avg_price`.

Returns: (float) The price value at the specified number of ticks away from the `from` price if

the strategy has an open position. Otherwise, it returns `na`.

ticksToCurrency(ticks)

Converts a specified number of ticks to an amount of the symbol's currency.

Parameters:

ticks (float) : (series int/float) The number of ticks to convert.

Returns: (float) The amount of the symbol's currency represented by the tick distance.

ticksToStopLevel(ticks)

Calculates a stop-loss level using a specified tick distance from the position's average

entry price. A script can plot the returned value and use it as the `stop` argument in a

`strategy.exit()` call.

Parameters:

ticks (float) : (series int/float) The number of ticks from the position's average entry price to the

stop-loss level. If the position is long, the value represents the number of ticks *below*

the average entry price. If short, it represents the number of ticks *above* the price.

Returns: (float) The calculated stop-loss value for the open position. If there is no open position,

it returns `na`.

ticksToTpLevel(ticks)

Calculates a take-profit level using a specified tick distance from the position's average

entry price. A script can plot the returned value and use it as the `limit` argument in a

`strategy.exit()` call.

Parameters:

ticks (float) : (series int/float) The number of ticks from the position's average entry price to the

take-profit level. If the position is long, the value represents the number of ticks *above*

the average entry price. If short, it represents the number of ticks *below* the price.

Returns: (float) The calculated take-profit value for the open position. If there is no open

position, it returns `na`.

calcPositionSizeByStopLossTicks(stopLossTicks, riskPercent)

Calculates the entry quantity required to risk a specified percentage of the strategy's

current equity at a tick-based stop-loss level.

Parameters:

stopLossTicks (float) : (series int/float) The number of ticks in the stop-loss distance.

riskPercent (float) : (series int/float) The percentage of the strategy's equity to risk if a trade moves

`stopLossTicks` away from the entry price in the unfavorable direction.

Returns: (int) The number of contracts/shares/lots/units to use as the entry quantity to risk the

specified percentage of equity at the stop-loss level.

calcPositionSizeByStopLossPercent(stopLossPercent, riskPercent, entryPrice)

Calculates the entry quantity required to risk a specified percentage of the strategy's

current equity at a percent-based stop-loss level.

Parameters:

stopLossPercent (float) : (series int/float) The percentage of the `entryPrice` to use as the stop-loss distance.

riskPercent (float) : (series int/float) The percentage of the strategy's equity to risk if a trade moves

`stopLossPercent` of the `entryPrice` in the unfavorable direction.

entryPrice (float) : (series int/float) Optional. The entry price to use in the calculation. The default is

`close`.

Returns: (int) The number of contracts/shares/lots/units to use as the entry quantity to risk the

specified percentage of equity at the stop-loss level.

exitPercent(id, lossPercent, profitPercent, qty, qtyPercent, comment, alertMessage)

A wrapper for the `strategy.exit()` function designed for creating stop-loss and

take-profit orders at percentage distances away from the position's average entry price.

NOTE: This function calls `strategy.exit()` without a `from_entry` ID, so it creates exit

orders for *every* entry in an open position until the position closes. Therefore, using

this function when the strategy has a pyramiding value greater than 1 can lead to

unexpected results. See the "Exits for multiple entries" section of our User Manual's

"Strategies" page to learn more about this behavior.

Parameters:

id (string) : (series string) Optional. The identifier of the stop-loss/take-profit orders, which

corresponds to an exit ID in the strategy's trades after an order fills. The default is

`"Exit"`.

lossPercent (float) : (series int/float) The percentage of the position's average entry price to use as the

stop-loss distance. The function does not create a stop-loss order if the value is `na`.

profitPercent (float) : (series int/float) The percentage of the position's average entry price to use as the

take-profit distance. The function does not create a take-profit order if the value is `na`.

qty (float) : (series int/float) Optional. The number of contracts/lots/shares/units to close when an

exit order fills. If specified, the call uses this value instead of `qtyPercent` to

determine the order size. The exit orders reserve this quantity from the position, meaning

other orders from `strategy.exit()` cannot close this portion until the strategy fills or

cancels those orders. The default is `na`, which means the order size depends on the

`qtyPercent` value.

qtyPercent (float) : (series int/float) Optional. A value between 0 and 100 representing the percentage of the

open trade quantity to close when an exit order fills. The exit orders reserve this

percentage from the open trades, meaning other calls to this command cannot close this

portion until the strategy fills or cancels those orders. The percentage calculation

depends on the total size of the applicable open trades without considering the reserved

amount from other `strategy.exit()` calls. The call ignores this parameter if the `qty`

value is not `na`. The default is 100.

comment (string) : (series string) Optional. Additional notes on the filled order. If the value is specified

and not an empty "string", the Strategy Tester and the chart show this text for the order

instead of the specified `id`. The default is `na`.

alertMessage (string) : (series string) Optional. Custom text for the alert that fires when an order fills. If the

value is specified and not an empty "string", and the "Message" field of the "Create Alert"

dialog box contains the `{{strategy.order.alert_message}}` placeholder, the alert message

replaces the placeholder with this text. The default is `na`.

Returns: (void) The function does not return a usable value.

closeAllAtEndOfSession(comment, alertMessage)

A wrapper for the `strategy.close_all()` function designed to close all open trades with a

market order when the last bar in the current day's session closes. It uses the command's

`immediately` parameter to exit all trades at the last bar's `close` instead of the `open`

of the next session's first bar.

Parameters:

comment (string) : (series string) Optional. Additional notes on the filled order. If the value is specified

and not an empty "string", the Strategy Tester and the chart show this text for the order

instead of the automatically generated exit identifier. The default is `na`.

alertMessage (string) : (series string) Optional. Custom text for the alert that fires when an order fills. If the

value is specified and not an empty "string", and the "Message" field of the "Create Alert"

dialog box contains the `{{strategy.order.alert_message}}` placeholder, the alert message

replaces the placeholder with this text. The default is `na`.

Returns: (void) The function does not return a usable value.

closeAtEndOfSession(entryId, comment, alertMessage)

A wrapper for the `strategy.close()` function designed to close specific open trades with a

market order when the last bar in the current day's session closes. It uses the command's

`immediately` parameter to exit the trades at the last bar's `close` instead of the `open`

of the next session's first bar.

Parameters:

entryId (string)

comment (string) : (series string) Optional. Additional notes on the filled order. If the value is specified

and not an empty "string", the Strategy Tester and the chart show this text for the order

instead of the automatically generated exit identifier. The default is `na`.

alertMessage (string) : (series string) Optional. Custom text for the alert that fires when an order fills. If the

value is specified and not an empty "string", and the "Message" field of the "Create Alert"

dialog box contains the `{{strategy.order.alert_message}}` placeholder, the alert message

replaces the placeholder with this text. The default is `na`.

Returns: (void) The function does not return a usable value.

sortinoRatio(interestRate, forceCalc)

Calculates the Sortino ratio of the strategy based on realized monthly returns.

Parameters:

interestRate (simple float) : (simple int/float) Optional. The *annual* "risk-free" return percentage to compare against

strategy returns. The default is 2, meaning it uses an annual benchmark of 2%.

forceCalc (bool) : (series bool) Optional. A value of `true` forces the function to calculate the ratio on the

current bar. If the value is `false`, the function calculates the ratio only on the latest

available bar for efficiency. The default is `false`.

Returns: (float) The Sortino ratio, which estimates the strategy's excess return per unit of

downside volatility.

sharpeRatio(interestRate, forceCalc)

Calculates the Sharpe ratio of the strategy based on realized monthly returns.

Parameters:

interestRate (simple float) : (simple int/float) Optional. The *annual* "risk-free" return percentage to compare against

strategy returns. The default is 2, meaning it uses an annual benchmark of 2%.

forceCalc (bool) : (series bool) Optional. A value of `true` forces the function to calculate the ratio on the

current bar. If the value is `false`, the function calculates the ratio only on the latest

available bar for efficiency. The default is `false`.

Returns: (float) The Sortino ratio, which estimates the strategy's excess return per unit of

total volatility.

Strategy█ OVERVIEW

This library is a Pine Script™ programmer’s tool containing a variety of strategy-related functions to assist in calculations like profit and loss, stop losses and limits. It also includes several useful functions one can use to convert between units in ticks, price, currency or a percentage of the position's size.

█ CONCEPTS

The library contains three types of functions:

1 — Functions beginning with `percent` take either a portion of a price, or the current position's entry price and convert it to the value outlined in the function's documentation.

Example: Converting a percent of the current position entry price to ticks, or calculating a percent profit at a given level for the position.

2 — Functions beginning with `tick` convert a tick value to another form.

These are useful for calculating a price or currency value from a specified number of ticks.

3 — Functions containing `Level` are used to calculate a stop or take profit level using an offset in ticks from the current entry price.

These functions can be used to plot stop or take profit levels on the chart, or as arguments to the `limit` and `stop` parameters in strategy.exit() function calls.

Note that these calculated levels flip automatically with the position's bias.

For example, using `ticksToStopLevel()` will calculate a stop level under the entry price for a long position, and above the entry price for a short position.

There are also two functions to assist in calculating a position size using the entry's stop and a fixed risk expressed as a percentage of the current account's equity. By varying the position size this way, you ensure that entries with different stop levels risk the same proportion of equity.

█ NOTES

Example code using some of the library's functions is included at the end of the library. To see it in action, copy the library's code to a new script in the Pine Editor, and “Add to chart”.

For each trade, the code displays:

• The entry level in orange.

• The stop level in fuchsia.

• The take profit level in green.

The stop and take profit levels automatically flip sides based on whether the current position is long or short.

Labels near the last trade's levels display the percentages used to calculate them, which can be changed in the script's inputs.

We plot markers for entries and exits because strategy code in libraries does not display the usual markers for them.

Look first. Then leap.

█ FUNCTIONS

percentToTicks(percent) Converts a percentage of the average entry price to ticks.

Parameters:

percent : (series int/float) The percentage of `strategy.position_avg_price` to convert to ticks. 50 is 50% of the entry price.

Returns: (float) A value in ticks.

percentToPrice(percent) Converts a percentage of the average entry price to a price.

Parameters:

percent : (series int/float) The percentage of `strategy.position_avg_price` to convert to price. 50 is 50% of the entry price.

Returns: (float) A value in the symbol's quote currency (USD for BTCUSD).

percentToCurrency(price, percent) Converts the percentage of a price to money.

Parameters:

price : (series int/float) The symbol's price.

percent : (series int/float) The percentage of `price` to calculate.

Returns: (float) A value in the symbol's currency.

percentProfit(exitPrice) Calculates the profit (as a percentage of the position's `strategy.position_avg_price` entry price) if the trade is closed at `exitPrice`.

Parameters:

exitPrice : (series int/float) The potential price to close the position.

Returns: (float) Percentage profit for the current position if closed at the `exitPrice`.

priceToTicks(price) Converts a price to ticks.

Parameters:

price : (series int/float) Price to convert to ticks.

Returns: (float) A quantity of ticks.

ticksToPrice(price) Converts ticks to a price offset from the average entry price.

Parameters:

price : (series int/float) Ticks to convert to a price.

Returns: (float) A price level that has a distance from the entry price equal to the specified number of ticks.

ticksToCurrency(ticks) Converts ticks to money.

Parameters:

ticks : (series int/float) Number of ticks.

Returns: (float) Money amount in the symbol's currency.

ticksToStopLevel(ticks) Calculates a stop loss level using a distance in ticks from the current `strategy.position_avg_price` entry price. This value can be plotted on the chart, or used as an argument to the `stop` parameter of a `strategy.exit()` call. NOTE: The stop level automatically flips based on whether the position is long or short.

Parameters:

ticks : (series int/float) The distance in ticks from the entry price to the stop loss level.

Returns: (float) A stop loss level for the current position.

ticksToTpLevel(ticks) Calculates a take profit level using a distance in ticks from the current `strategy.position_avg_price` entry price. This value can be plotted on the chart, or used as an argument to the `limit` parameter of a `strategy.exit()` call. NOTE: The take profit level automatically flips based on whether the position is long or short.

Parameters:

ticks : (series int/float) The distance in ticks from the entry price to the take profit level.

Returns: (float) A take profit level for the current position.

calcPositionSizeByStopLossTicks(stopLossTicks, riskPercent) Calculates the position size needed to implement a given stop loss (in ticks) corresponding to `riskPercent` of equity.

Parameters:

stopLossTicks : (series int) The stop loss (in ticks) that will be used to protect the position.

riskPercent : (series int/float) The maximum risk level as a percent of current equity (`strategy.equity`).

Returns: (int) A quantity of contracts.

calcPositionSizeByStopLossPercent(stopLossPercent, riskPercent, entryPrice) Calculates the position size needed to implement a given stop loss (%) corresponding to `riskPercent` of equity.

Parameters:

stopLossPercent : (series int/float) The stop loss in percent that will be used to protect the position.

riskPercent : (series int/float) The maximum risk level as a percent of current equity (`strategy.equity`).

entryPrice : (series int/float) The entry price of the position.

Returns: (int) A quantity of contracts.

exitPercent(id, lossPercent, profitPercent, qty, qtyPercent, comment, when, alertMessage) A wrapper of the `strategy.exit()` built-in which adds the possibility to specify loss & profit in as a value in percent. NOTE: this function may work incorrectly with pyramiding turned on due to the use of `strategy.position_avg_price` in its calculations of stop loss and take profit offsets.

Parameters:

id : (series string) The order identifier of the `strategy.exit()` call.

lossPercent : (series int/float) Stop loss as a percent of the entry price.

profitPercent : (series int/float) Take profit as a percent of the entry price.

qty : (series int/float) Number of contracts/shares/lots/units to exit a trade with. The default value is `na`.

qtyPercent : (series int/float) The percent of the position's size to exit a trade with. If `qty` is `na`, the default value of `qty_percent` is 100.

comment : (series string) Optional. Additional notes on the order.

when : (series bool) Condition of the order. The order is placed if it is true.

alertMessage : (series string) An optional parameter which replaces the {{strategy.order.alert_message}} placeholder when it is used in the "Create Alert" dialog box's "Message" field.

Waindrops [Makit0]█ OVERALL

Plot waindrops (custom volume profiles) on user defined periods, for each period you get high and low, it slices each period in half to get independent vwap, volume profile and the volume traded per price at each half.

It works on intraday charts only, up to 720m (12H). It can plot balanced or unbalanced waindrops, and volume profiles up to 24H sessions.

As example you can setup unbalanced periods to get independent volume profiles for the overnight and cash sessions on the futures market, or 24H periods to get the full session volume profile of EURUSD

The purpose of this indicator is twofold:

1 — from a Chartist point of view, to have an indicator which displays the volume in a more readable way

2 — from a Pine Coder point of view, to have an example of use for two very powerful tools on Pine Script:

• the recently updated drawing limit to 500 (from 50)

• the recently ability to use drawings arrays (lines and labels)

If you are new to Pine Script and you are learning how to code, I hope you read all the code and comments on this indicator, all is designed for you,

the variables and functions names, the sometimes too big explanations, the overall structure of the code, all is intended as an example on how to code

in Pine Script a specific indicator from a very good specification in form of white paper

If you wanna learn Pine Script form scratch just start HERE

In case you have any kind of problem with Pine Script please use some of the awesome resources at our disposal: USRMAN , REFMAN , AWESOMENESS , MAGIC

█ FEATURES

Waindrops are a different way of seeing the volume and price plotted in a chart, its a volume profile indicator where you can see the volume of each price level

plotted as a vertical histogram for each half of a custom period. By default the period is 60 so it plots an independent volume profile each 30m

You can think of each waindrop as an user defined candlestick or bar with four key values:

• high of the period

• low of the period

• left vwap (volume weighted average price of the first half period)

• right vwap (volume weighted average price of the second half period)

The waindrop can have 3 different colors (configurable by the user):

• GREEN: when the right vwap is higher than the left vwap (bullish sentiment )

• RED: when the right vwap is lower than the left vwap (bearish sentiment )

• BLUE: when the right vwap is equal than the left vwap ( neutral sentiment )

KEY FEATURES

• Help menu

• Custom periods

• Central bars

• Left/Right VWAPs

• Custom central bars and vwaps: color and pixels

• Highly configurable volume histogram: execution window, ticks, pixels, color, update frequency and fine tuning the neutral meaning

• Volume labels with custom size and color

• Tracking price dot to be able to see the current price when you hide your default candlesticks or bars

█ SETTINGS

Click here or set any impar period to see the HELP INFO : show the HELP INFO, if it is activated the indicator will not plot

PERIOD SIZE (max 2880 min) : waindrop size in minutes, default 60, max 2880 to allow the first half of a 48H period as a full session volume profile

BARS : show the central and vwap bars, default true

Central bars : show the central bars, default true

VWAP bars : show the left and right vwap bars, default true

Bars pixels : width of the bars in pixels, default 2

Bars color mode : bars color behavior

• BARS : gets the color from the 'Bars color' option on the settings panel

• HISTOGRAM : gets the color from the Bearish/Bullish/Neutral Histogram color options from the settings panel

Bars color : color for the central and vwap bars, default white

HISTOGRAM show the volume histogram, default true

Execution window (x24H) : last 24H periods where the volume funcionality will be plotted, default 5

Ticks per bar (max 50) : width in ticks of each histogram bar, default 2

Updates per period : number of times the histogram will update

• ONE : update at the last bar of the period

• TWO : update at the last bar of each half period

• FOUR : slice the period in 4 quarters and updates at the last bar of each of them

• EACH BAR : updates at the close of each bar

Pixels per bar : width in pixels of each histogram bar, default 4

Neutral Treshold (ticks) : delta in ticks between left and right vwaps to identify a waindrop as neutral, default 0

Bearish Histogram color : histogram color when right vwap is lower than left vwap, default red

Bullish Histogram color : histogram color when right vwap is higher than left vwap, default green

Neutral Histogram color : histogram color when the delta between right and left vwaps is equal or lower than the Neutral treshold, default blue

VOLUME LABELS : show volume labels

Volume labels color : color for the volume labels, default white

Volume Labels size : text size for the volume labels, choose between AUTO, TINY, SMALL, NORMAL or LARGE, default TINY

TRACK PRICE : show a yellow ball tracking the last price, default true

█ LIMITS

This indicator only works on intraday charts (minutes only) up to 12H (720m), the lower chart timeframe you can use is 1m

This indicator needs price, time and volume to work, it will not work on an index (there is no volume), the execution will not be allowed

The histogram (volume profile) can be plotted on 24H sessions as limit but you can plot several 24H sessions

█ ERRORS AND PERFORMANCE

Depending on the choosed settings, the script performance will be highly affected and it will experience errors

Two of the more common errors it can throw are:

• Calculation takes too long to execute

• Loop takes too long

The indicator performance is highly related to the underlying volatility (tick wise), the script takes each candlestick or bar and for each tick in it stores the price and volume, if the ticker in your chart has thousands and thousands of ticks per bar the indicator will throw an error for sure, it can not calculate in time such amount of ticks.

What all of that means? Simply put, this will throw error on the BITCOIN pair BTCUSD (high volatility with tick size 0.01) because it has too many ticks per bar, but lucky you it will work just fine on the futures contract BTC1! (tick size 5) because it has a lot less ticks per bar

There are some options you can fine tune to boost the script performance, the more demanding option in terms of resources consumption is Updates per period , by default is maxed out so lowering this setting will improve the performance in a high way.

If you wanna know more about how to improve the script performance, read the HELP INFO accessible from the settings panel

█ HOW-TO SETUP

The basic parameters to adjust are Period size , Ticks per bar and Pixels per bar

• Period size is the main setting, defines the waindrop size, to get a better looking histogram set bigger period and smaller chart timeframe

• Ticks per bar is the tricky one, adjust it differently for each underlying (ticker) volatility wise, for some you will need a low value, for others a high one.

To get a more accurate histogram set it as lower as you can (min value is 1)

• Pixels per bar allows you to adjust the width of each histogram bar, with it you can adjust the blank space between them or allow overlaping

You must play with these three parameters until you obtain the desired histogram: smoother, sharper, etc...

These are some of the different kind of charts you can setup thru the settings:

• Balanced Waindrops (default): charts with waindrops where the two halfs are of same size.

This is the default chart, just select a period (30m, 60m, 120m, 240m, pick your poison), adjust the histogram ticks and pixels and watch

• Unbalanced Waindrops: chart with waindrops where the two halfs are of different sizes.

Do you trade futures and want to plot a waindrop with the first half for the overnight session and the second half for the cash session? you got it;

just adjust the period to 1860 for any CME ticker (like ES1! for example) adjust the histogram ticks and pixels and watch

• Full Session Volume Profile: chart with waindrops where only the first half plots.

Do you use Volume profile to analize the market? Lucky you, now you can trick this one to plot it, just try a period of 780 on SPY, 2760 on ES1!, or 2880 on EURUSD

remember to adjust the histogram ticks and pixels for each underlying

• Only Bars: charts with only central and vwap bars plotted, simply deactivate the histogram and volume labels

• Only Histogram: charts with only the histogram plotted (volume profile charts), simply deactivate the bars and volume labels

• Only Volume: charts with only the raw volume numbers plotted, simply deactivate the bars and histogram

If you wanna know more about custom full session periods for different asset classes, read the HELP INFO accessible from the settings panel

EXAMPLES

Full Session Volume Profile on MES 5m chart:

Full Session Unbalanced Waindrop on MNQ 2m chart (left side Overnight session, right side Cash Session):

The following examples will have the exact same charts but on four different tickers representing a futures contract, a forex pair, an etf and a stock.

We are doing this to be able to see the different parameters we need for plotting the same kind of chart on different assets

The chart composition is as follows:

• Left side: Volume Labels chart (period 10)

• Upper Right side: Waindrops (period 60)

• Lower Right side: Full Session Volume Profile

The first example will specify the main parameters, the rest of the charts will have only the differences

MES :

• Left: Period size: 10, Bars: uncheck, Histogram: uncheck, Execution window: 1, Ticks per bar: 2, Updates per period: EACH BAR,

Pixels per bar: 4, Volume labels: check, Track price: check

• Upper Right: Period size: 60, Bars: check, Bars color mode: HISTOGRAM, Histogram: check, Execution window: 2, Ticks per bar: 2,

Updates per period: EACH BAR, Pixels per bar: 4, Volume labels: uncheck, Track price: check

• Lower Right: Period size: 2760, Bars: uncheck, Histogram: check, Execution window: 1, Ticks per bar: 1, Updates per period: EACH BAR,

Pixels per bar: 2, Volume labels: uncheck, Track price: check

EURUSD :

• Upper Right: Ticks per bar: 10

• Lower Right: Period size: 2880, Ticks per bar: 1, Pixels per bar: 1

SPY :

• Left: Ticks per bar: 3

• Upper Right: Ticks per bar: 5, Pixels per bar: 3

• Lower Right: Period size: 780, Ticks per bar: 2, Pixels per bar: 2

AAPL :

• Left: Ticks per bar: 2

• Upper Right: Ticks per bar: 6, Pixels per bar: 3

• Lower Right: Period size: 780, Ticks per bar: 1, Pixels per bar: 2

█ THANKS TO

PineCoders for all they do, all the tools and help they provide and their involvement in making a better community

scarf for the idea of coding a waindrops like indicator, I did not know something like that existed at all

All the Pine Coders, Pine Pros and Pine Wizards, people who share their work and knowledge for the sake of it and helping others, I'm very grateful indeed

I'm learning at each step of the way from you all, thanks for this awesome community;

Opensource and shared knowledge: this is the way! (said with canned voice from inside my helmet :D)

█ NOTE

This description was formatted following THIS guidelines

═════════════════════════════════════════════════════════════════════════

I sincerely hope you enjoy reading and using this work as much as I enjoyed developing it :D

GOOD LUCK AND HAPPY TRADING!

SMT Divergences [LuxAlgo]The SMT Divergences indicator highlights SMT divergences between the chart symbol and two user-selected tickers (ES and YM by default).

A dashboard returning the SMT divergences statistics is also provided within the settings.

🔶 SETTINGS

Swing Lookback: Calculation window used to detect swing points.

Comparison Ticker: If enabled, will detect SMT divergences between the chart prices and the prices of the selected ticker.

🔹 Dashboard

Show Dashboard: Displays statistics dashboard on the chart.

Location: Location of the dashboard on the chart.

Size: Size of the displayed dashboard.

🔶 USAGE

SMT Divergences are characterized by diverging swing points between two securities.

The detection of SMT Divergences is performed by detecting swing points using the user chart prices as well as the prices of the selected external tickers. If a swing point on the chart ticker is detected at the same time on external tickers, comparison is performed.

Due to the detection requiring swing point confirmation (3 candles by default), this indicator can better be used to study price behaviors on the occurrence of an SMT divergence.

The dashboard highlights the number of SMT divergences that occurred on a swing high and swing low between the chart ticker and the selected external tickers.

The returned percentage indicates the proportion of swing highs or swing lows that led to an SMT divergence.

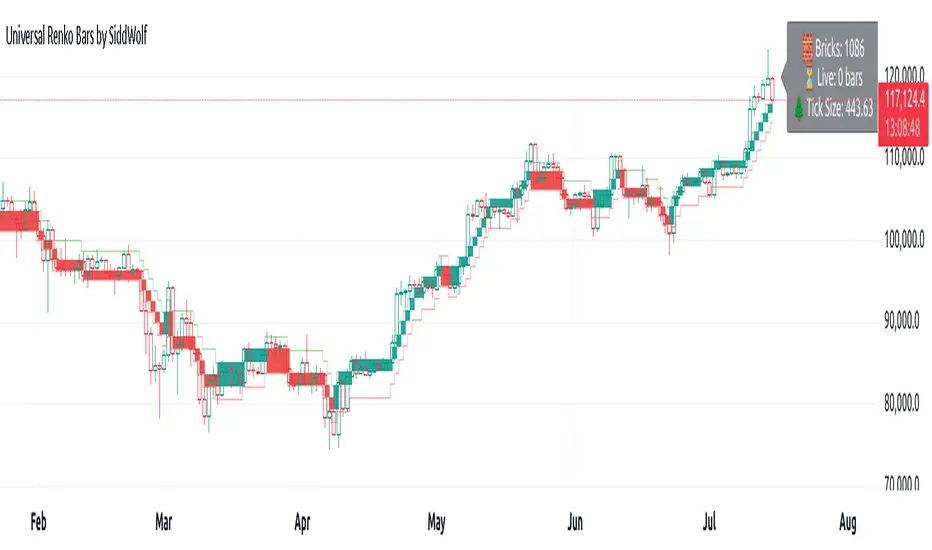

Universal Renko Bars by SiddWolfUniversal Renko Bars or UniRenko Bars is an overlay indicator that applies the logic of Renko charting directly onto a standard candlestick chart. It generates a sequence of price-driven bricks, where each new brick is formed only when the price moves a specific amount, regardless of time. This provides a clean, price-action-focused visualization of the market's trend.

WHAT IS UNIVERSAL RENKO BARS?

For years, traders have faced a stark choice: the clean, noise-free world of Renko charts, or the rich, time-based context of Candlesticks. Choosing Renko meant giving up your favorite moving averages, volume profiles, and the fundamental sense of time. Choosing Candlesticks meant enduring the market noise that often clouds true price action.

But what if you didn't have to choose?

Universal Renko Bars is a revolutionary indicator that ends this dilemma. It's not just another charting tool; it's a powerful synthesis that overlays the pure, price-driven logic of Renko bricks directly onto your standard candlestick chart. This hybrid approach gives you the best of both worlds:

❖ The Clarity of Renko: By filtering out the insignificant noise of time, Universal Renko reveals the underlying trend with unparalleled clarity. Up trends are clean successions of green bricks; down trends are clear red bricks. No more guesswork.

❖ The Context of Candlesticks: Because the Renko logic is an overlay, you retain your time axis, your volume data, and full compatibility with every other time-based indicator in your arsenal (RSI, MACD, Moving Averages, etc.).

The true magic, however, lies in its live, Unconfirmed Renko brick. This semi-transparent box is your window into the current bar's real-time struggle. It grows, shrinks, and changes color with every tick, showing you exactly how close the price is to confirming the trend or forcing a reversal. It’s no longer a lagging indicator; it’s a live look at the current battle between buyers and sellers.

Universal Renko Bars unifies these two powerful charting methods, transforming your chart into a more intelligent, noise-free, and predictive analytical canvas.

HOW TO USE

To get the most out of Universal Renko Bars, here are a few tips and a full breakdown of the settings.

Initial Setup for the Best Experience

For the cleanest possible view, it's highly recommended that you hide the body of your standard candlesticks, that shows only the skelton of the candle. This allows the Renko bricks to become the primary focus of your chart.

→ Double click on the candles and uncheck the body checkbox.

Settings Breakdown

The indicator is designed to be powerful yet intuitive. The settings are grouped to make customization easy.

First, What is a "Tick"?

Before we dive in, it's important to understand the concept of a "Tick." In Universal Renko, a Tick is not the same as a market tick. It's a fundamental unit of price movement that you define. For example, if you set the Tick Size to $0.50, then a price move of $1.00 is equal to 2 Ticks. This is the core building block for all Renko bricks. Tick size here is dynamically determined by the settings provided in the indicator.

❖ Calculation Method (The "Tick Size" Engine)

This section determines the monetary value of a single "Tick."

`Calculation Method` : Choose your preferred engine for defining the Tick Size.

`ATR Based` (Default): The Tick Size becomes dynamic, based on market volatility (Average True Range). Bricks will get larger in volatile markets and smaller in quiet ones. Use the `ATR 14 Multiplier` to control the sensitivity.

`Percentage` : The Tick Size is a simple percentage of the current asset price, controlled by the `Percent Size (%)` input.

`Auto` : The "set it and forget it" mode. The script intelligently calculates a Tick Size based on the asset's price. Use the `Auto Sensitivity` slider to make these automatically calculated bricks thicker (value > 1.0) or thinner (value < 1.0).

❖ Parameters (The Core Renko Engine)

This group controls how the bricks are constructed based on the Tick Size.

`Tick Trend` : The number of "Ticks" the price must move in the same direction to print a new continuation brick. A smaller value means bricks form more easily.

`Tick Reversal` : The number of "Ticks" the price must move in the opposite direction to print a new reversal brick. This is typically set higher than `Tick Trend` (e.g., double) to filter out minor pullbacks and market noise.

`Open Offset` : Controls the visual overlap of the bricks. A value of `0` creates gapless bricks that start where the last one ended. A value of `2` (with a `Tick Reversal` of 4) creates the classic 50% overlap look.

❖ Visuals (Controlling What You See)

This is where you tailor the chart to your visual preference.

`Show Confirmed Renko` : Toggles the solid-colored, historical bricks. These are finalized and will never change. They represent the confirmed past trend.

`Show Unconfirmed Renko` : This is the most powerful visual feature. It toggles the live, semi-transparent box that represents the developing brick. It shows you exactly where the price is right now in relation to the levels needed to form the next brick.

`Show Max/Min Levels` : Toggles the horizontal "finish lines" on your chart. The green line is the price target for a bullish brick, and the red line is the target for a bearish brick. These are excellent for spotting breakouts.

`Show Info Label` : Toggles the on-chart label that provides key real-time stats:

🧱 Bricks: The total count of confirmed bricks.

⏳ Live: How many chart bars the current live brick has been forming. These bars forms the Renko bricks that aren't confirmed yet. Live = 0 means the latest renko brick is confirmed.

🌲 Tick Size: The current calculated value of a single Tick.

Hover over the label for a tooltip with live RSI(14), MFI(14), and CCI(20) data for additional confirmation.

TRADING STRATEGIES & IDEAS

Universal Renko Bars isn't just a visual tool; it's a foundation for building robust trading strategies.

Trend Confirmation: The primary use is to instantly identify the trend. A series of green bricks indicates a strong uptrend; a series of red bricks indicates a strong downtrend. Use this to filter out trades that go against the primary momentum.

Reversal Spotting: Pay close attention to the Unconfirmed Brick . When a strong trend is in place and the live brick starts to fight against it—changing color and growing larger—it can be an early warning that a reversal is imminent. Wait for the brick to be confirmed for a higher probability entry.

Breakout Trading: The `Max/Min Levels` are your dynamic breakout zones. A long entry can be considered when the price breaks and closes above the green Max Level, confirming a new bullish brick. A short entry can be taken when price breaks below the red Min Level.

Confluence & Indicator Synergy: This is where Universal Renko truly shines. Overlay a moving average (e.g., 20 EMA). Only take long trades when the green bricks are forming above the EMA. Combine it with RSI or MACD; a bearish reversal brick forming while the RSI shows bearish divergence is a very powerful signal.

A FINAL WORD

Universal Renko Bars was designed to solve a fundamental problem in technical analysis. It brings together the best elements of two powerful methodologies to give you a clearer, more actionable view of the market. By filtering noise while retaining context, it empowers you to make decisions with greater confidence.

Add Universal Renko Bars to your chart today and elevate your analysis. We welcome your feedback and suggestions for future updates!

Follow me to get notified when I publish New Indicator.

~ SiddWolf

Yelober_Momentum_BreadthMI# Yelober_Momentum_BreadthMI: Market Breadth Indicator Analysis

## Overview

The Yelober_Momentum_BreadthMI is a comprehensive market breadth indicator designed to monitor market internals across NYSE and NASDAQ exchanges. It tracks several key metrics including up/down volume ratios, TICK readings, and trend momentum to provide traders with real-time insights into market direction, strength, and potential turning points.

## Indicator Components

This indicator displays a table with data for:

- NYSE breadth metrics

- NASDAQ breadth metrics

- NYSE TICK data and trends

- NASDAQ TICK (TICKQ) data and trends

## Table Columns and Interpretation

### Column 1: Market

Identifies the data source:

- **NYSE**: New York Stock Exchange data

- **NASDAQ**: NASDAQ exchange data

- **Tick**: NYSE TICK index

- **TickQ**: NASDAQ TICK index

### Column 2: Ratio

Shows the current ratio values with different calculations depending on the row:

- **For NYSE/NASDAQ rows**: Displays the up/down volume ratio

- Positive values (green): More up volume than down volume

- Negative values (red): More down volume than up volume

- The magnitude indicates the strength of the imbalance

- **For Tick/TickQ rows**: Shows the ratio of positive to negative ticks plus the current TICK reading in parentheses

- Format: "Ratio (Current TICK value)"

- Positive values (green): More stocks ticking up than down

- Negative values (red): More stocks ticking down than up

### Column 3: Trend

Displays the directional trend with both a symbol and value:

- **For NYSE/NASDAQ rows**: Shows the VOLD (volume difference) slope

- "↗": Rising trend (positive slope)

- "↘": Falling trend (negative slope)

- "→": Neutral/flat trend (minimal slope)

- **For Tick/TickQ rows**: Shows the slope of the ratio history

- Color-coding: Green for positive momentum, Red for negative momentum, Gray for neutral

The trend column is particularly important as it shows the current momentum of the market. The indicator applies specific thresholds for color-coding:

- NYSE: Green when normalized value > 2, Red when < -2

- NASDAQ: Green when normalized value > 3.5, Red when < -3.5

- TICK/TICKQ: Green when slope > 0.01, Red when slope < -0.01

## How to Use This Indicator

### Basic Interpretation

1. **Market Direction**: When multiple rows show green ratios and upward trends, it suggests strong bullish market internals. Conversely, red ratios and downward trends indicate bearish internals.

2. **Market Breadth**: The magnitude of the ratios indicates how broad-based the market movement is. Higher absolute values suggest stronger market breadth.

3. **Momentum Shifts**: When trend arrows change direction or colors shift, it may signal a potential reversal or change in market momentum.

4. **Divergences**: Look for divergences between different markets (NYSE vs NASDAQ) or between ratios and trends, which can indicate potential market turning points.

### Advanced Usage

- **Volume Normalization**: The indicator includes options to normalize volume data (none, tens, thousands, millions, 10th millions) to handle different exchange scales.

- **Trend Averaging**: The slope calculation uses an averaging period (default: 5) to smooth out noise and identify more reliable trend signals.

## Examples for Interpretation

### Example 1: Strong Bullish Market

```

| Market | Ratio | Trend |

|--------|---------|-----------|

| NYSE | 1.75 | ↗ 2.85 |

| NASDAQ | 2.10 | ↗ 4.12 |

| Tick | 2.45 (485) | ↗ 0.05 |

| TickQ | 1.95 (320) | ↗ 0.03 |

```

**Interpretation**: All metrics are positive and trending upward (green), indicating a strong, broad-based rally. The high ratio values show significant bullish dominance. This suggests continuation of the upward move with good momentum.

### Example 2: Weakening Market

```

| Market | Ratio | Trend |

|--------|---------|-----------|

| NYSE | 0.45 | ↘ -1.50 |

| NASDAQ | 0.85 | → 0.30 |

| Tick | 0.95 (105) | ↘ -0.02 |

| TickQ | 1.20 (160) | → 0.00 |

```

**Interpretation**: The market is showing mixed signals with positive but low ratios, while NYSE and TICK trends are turning negative. NASDAQ shows neutral to slightly positive momentum. This divergence often occurs near market tops or during consolidation phases. Traders should be cautious and consider reducing position sizes.

### Example 3: Negative Market Turning Positive

```

| Market | Ratio | Trend |

|--------|---------|-----------|

| NYSE | -1.25 | ↗ 1.75 |

| NASDAQ | -0.95 | ↗ 2.80 |

| Tick | -1.35 (-250) | ↗ 0.04 |

| TickQ | -1.10 (-180) | ↗ 0.02 |

```

**Interpretation**: This is a potential bottoming pattern. Current ratios are still negative (red) showing overall negative breadth, but the trends are all positive (green arrows), indicating improving momentum. This divergence often occurs at market bottoms and could signal an upcoming reversal. Look for confirmation with price action before establishing long positions.

### Example 4: Mixed Market with Divergence

```

| Market | Ratio | Trend |

|--------|---------|-----------|

| NYSE | 1.45 | ↘ -2.25 |

| NASDAQ | -0.85 | ↘ -3.80 |

| Tick | 1.20 (230) | ↘ -0.03 |

| TickQ | -0.75 (-120) | ↘ -0.02 |

```

**Interpretation**: There's a significant divergence between NYSE (positive ratio) and NASDAQ (negative ratio), while all trends are negative. This suggests sector rotation or a market that's weakening but with certain segments still showing strength. Often seen during late-stage bull markets or in transitions between leadership groups. Consider reducing risk exposure and focusing on relative strength sectors.

## Practical Trading Applications

1. **Confirmation Tool**: Use this indicator to confirm price movements. Strong breadth readings in the direction of the price trend increase confidence in trade decisions.

2. **Early Warning System**: Watch for divergences between price and breadth metrics, which often precede market turns.

3. **Intraday Trading**: The real-time nature of TICK and volume data makes this indicator valuable for day traders to gauge intraday momentum shifts.

4. **Market Regime Identification**: Sustained readings can help identify whether the market is in a trend or chop regime, allowing for appropriate strategy selection.

This breadth indicator is most effective when used in conjunction with price action and other technical indicators rather than in isolation.

Correlation Clusters [LuxAlgo]The Correlation Clusters is a machine learning tool that allows traders to group sets of tickers with a similar correlation coefficient to a user-set reference ticker.

The tool calculates the correlation coefficients between 10 user-set tickers and a user-set reference ticker, with the possibility of forming up to 10 clusters.

🔶 USAGE

Applying clustering methods to correlation analysis allows traders to quickly identify which set of tickers are correlated with a reference ticker, rather than having to look at them one by one or using a more tedious approach such as correlation matrices.

Tickers belonging to a cluster may also be more likely to have a higher mutual correlation. The image above shows the detailed parts of the Correlation Clusters tool.

The correlation coefficient between two assets allows traders to see how these assets behave in relation to each other. It can take values between +1.0 and -1.0 with the following meaning

Value near +1.0: Both assets behave in a similar way, moving up or down at the same time

Value close to 0.0: No correlation, both assets behave independently

Value near -1.0: Both assets have opposite behavior when one moves up the other moves down, and vice versa

There is a wide range of trading strategies that make use of correlation coefficients between assets, some examples are:

Pair Trading: Traders may wish to take advantage of divergences in the price movements of highly positively correlated assets; even highly positively correlated assets do not always move in the same direction; when assets with a correlation close to +1.0 diverge in their behavior, traders may see this as an opportunity to buy one and sell the other in the expectation that the assets will return to the likely same price behavior.

Sector rotation: Traders may want to favor some sectors that are expected to perform in the next cycle, tracking the correlation between different sectors and between the sector and the overall market.

Diversification: Traders can aim to have a diversified portfolio of uncorrelated assets. From a risk management perspective, it is useful to know the correlation between the assets in your portfolio, if you hold equal positions in positively correlated assets, your risk is tilted in the same direction, so if the assets move against you, your risk is doubled. You can avoid this increased risk by choosing uncorrelated assets so that they move independently.

Hedging: Traders may want to hedge positions with correlated assets, from a hedging perspective, if you are long an asset, you can hedge going long a negatively correlated asset or going short a positively correlated asset.

Grouping different assets with similar behavior can be very helpful to traders to avoid over-exposure to those assets, traders may have multiple long positions on different assets as a way of minimizing overall risk when in reality if those assets are part of the same cluster traders are maximizing their risk by taking positions on assets with the same behavior.

As a rule of thumb, a trader can minimize risk via diversification by taking positions on assets with no correlations, the proposed tool can effectively show a set of uncorrelated candidates from the reference ticker if one or more clusters centroids are located near 0.

🔶 DETAILS

K-means clustering is a popular machine-learning algorithm that finds observations in a data set that are similar to each other and places them in a group.

The process starts by randomly assigning each data point to an initial group and calculating the centroid for each. A centroid is the center of the group. K-means clustering forms the groups in such a way that the variances between the data points and the centroid of the cluster are minimized.

It's an unsupervised method because it starts without labels and then forms and labels groups itself.

🔹 Execution Window

In the image above we can see how different execution windows provide different correlation coefficients, informing traders of the different behavior of the same assets over different time periods.

Users can filter the data used to calculate correlations by number of bars, by time, or not at all, using all available data. For example, if the chart timeframe is 15m, traders may want to know how different assets behave over the last 7 days (one week), or for an hourly chart set an execution window of one month, or one year for a daily chart. The default setting is to use data from the last 50 bars.

🔹 Clusters

On this graph, we can see different clusters for the same data. The clusters are identified by different colors and the dotted lines show the centroids of each cluster.

Traders can select up to 10 clusters, however, do note that selecting 10 clusters can lead to only 4 or 5 returned clusters, this is caused by the machine learning algorithm not detecting any more data points deviating from already detected clusters.

Traders can fine-tune the algorithm by changing the 'Cluster Threshold' and 'Max Iterations' settings, but if you are not familiar with them we advise you not to change these settings, the defaults can work fine for the application of this tool.

🔹 Correlations

Different correlations mean different behaviors respecting the same asset, as we can see in the chart above.

All correlations are found against the same asset, traders can use the chart ticker or manually set one of their choices from the settings panel. Then they can select the 10 tickers to be used to find the correlation coefficients, which can be useful to analyze how different types of assets behave against the same asset.

🔶 SETTINGS

Execution Window Mode: Choose how the tool collects data, filter data by number of bars, time, or no filtering at all, using all available data.

Execute on Last X Bars: Number of bars for data collection when the 'Bars' execution window mode is active.

Execute on Last: Time window for data collection when the `Time` execution window mode is active. These are full periods, so `Day` means the last 24 hours, `Week` means the last 7 days, and so on.

🔹 Clusters

Number of Clusters: Number of clusters to detect up to 10. Only clusters with data points are displayed.

Cluster Threshold: Number used to compare a new centroid within the same cluster. The lower the number, the more accurate the centroid will be.

Max Iterations: Maximum number of calculations to detect a cluster. A high value may lead to a timeout runtime error (loop takes too long).

🔹 Ticker of Reference

Use Chart Ticker as Reference: Enable/disable the use of the current chart ticker to get the correlation against all other tickers selected by the user.

Custom Ticker: Custom ticker to get the correlation against all the other tickers selected by the user.

🔹 Correlation Tickers

Select the 10 tickers for which you wish to obtain the correlation against the reference ticker.

🔹 Style

Text Size: Select the size of the text to be displayed.

Display Size: Select the size of the correlation chart to be displayed, up to 500 bars.

Box Height: Select the height of the boxes to be displayed. A high height will cause overlapping if the boxes are close together.

Clusters Colors: Choose a custom colour for each cluster.