Bitcoin - MA Crossover StrategyBefore You Begin:

Please read these warnings carefully before using this script, you will bear all fiscal responsibility for your own trades.

Trading Strategy Warning - Past performance of this strategy may not equal future performance, due to macro-environment changes, etc.

Account Size Warning - Performance based upon default 10% risk per trade, of account size $100,000. Adjust BEFORE you trade to see your own drawdown.

Time Frame - D1 and H4. H4 has a lower profit factor (more fake-outs, and account drawdown), D1 recommended.

Trend Following System - Profitability of this system is dependent on STRONG future trends in Bitcoin (BTCUSD).

Default Settings:

This script was tested on Daily and 4 Hourly charts using the following default settings. Note that 4 Hourly exhibits higher drawdowns and lower profit factor, whilst Daily appears more stable.

Account Size ($): 100,000 (please adjust to simulate your own risk)

Equity Risk (%): 10 (please adjust to simulate your own risk)

Fast Moving Average (Period): 20

Slow Moving Average (Period): 40

Relative Strength Index (Period): 14

Trading Mechanism:

Trend following strategies work well for assets that display the tendency of long-trends. Please do not use this script on financial assets that have a historical tendency for mean reversion. Bitcoin has historically exhibited strong trends, and thus this script is designed to capitalise on that behaviour. It is hoped (but we cannot predict), that Bitcoin will strongly trend in the coming days.

LONG:

Enter Long - When fast moving average (20) crosses ABOVE slow moving average (40)

Exit Long - When fast moving average (20) crosses BELOW slow moving average (40)

SHORT:

Enter Short - When fast moving average (20) crosses BELOW slow moving average (40)

Exit Short - When fast moving average (20) crosses ABOVE slow moving average (40)

Risk Warnings:

Do note that "moving averages" are a lagging indicator, and as such heavy drawdowns could occur when a trade is open. If you are trading this system manually, it is best to avoid emotions and let the system tell you when to enter and exit. Do not panic and exit manually when under heavy drawdown, always follow the system. Do not be emotional. If possible, connect this to your broker for auto-trading. Ensure that your risk per trade (Equity Risk) is SMALL enough that it does not result in a margin-call on your trading account. Equity risk must always be considered relative to your total account size.

Remember: You bear all financial responsibility for your trades, best of luck.

在脚本中搜索"泰国一寺庙被曝藏有40多具尸体"

Simple Harmonic Oscillator (SHO)The indicator is based on Akram El Sherbini's article "Time Cycle Oscillators" published in IFTA journal 2018 (pages 78-80) (www.ftaa.org.hk)

The SHO is a bounded oscillator for the simple harmonic index that calculates the period of the market’s cycle. The oscillator is used for short and intermediate terms and moves within a range of -100 to 100 percent. The SHO has overbought and oversold levels at +40 and -40, respectively. At extreme periods, the oscillator may reach the levels of +60 and -60. The zero level demonstrates an equilibrium between the periods of bulls and bears. The SHO oscillates between +40 and -40. The crossover at those levels creates buy and sell signals. In an uptrend, the SHO fluctuates between 0 and +40 where the bulls are controlling the market. On the contrary, the SHO fluctuates between 0 and -40 during downtrends where the bears control the market. Reaching the extreme level -60 in an uptrend is a sign of weakness. Mostly, the oscillator will retrace from its centerline rather than the upper boundary +40. On the other hand, reaching +60 in a downtrend is a sign of strength and the oscillator will not be able to reach its lower boundary -40.

Centerline Crossover Tactic

This tactic is tested during uptrends. The buy signals are generated when the WPO/SHI cross their centerlines to the upside. The sell signals are generated when the WPO/SHI cross down their centerlines. To define the uptrend in the system, stocks closing above their 50-day EMA are considered while the ADX is above 18.

Uptrend Tactic

During uptrends, the bulls control the markets, and the oscillators will move above their centerline with an increase in the period of cycles. The lower boundaries and equilibrium line crossovers generate buy signals, while crossing the upper boundaries will generate sell signals. The “Re-entry” and “Exit at weakness” tactics are combined with the uptrend tactic. Consequently, we will have three buy signals and two sell signals.

Sideways Tactic

During sideways, the oscillators fluctuate between their upper and lower boundaries. Crossing the lower boundary to the upside will generate a buy signal. On the other hand, crossing the upper boundary to the downside will generate a sell signal. When the bears take control, the oscillators will cross down the lower boundaries, triggering exit signals. Therefore, this tactic will consist of one buy signal and two sell signals. The sideway tactic is defined when stocks close above their 50-day EMA and the ADX is below 18

NG [Simple Harmonic Oscillator]The SHO is a bounded oscillator for the simple harmonic index that calculates the period of the market’s cycle.

The oscillator is used for short and intermediate terms and moves within a range of -100 to 100 percent.

The SHO has overbought and oversold levels at +40 and -40, respectively.

At extreme periods, the oscillator may reach the levels of +60 and -60.

The zero level demonstrates an equilibrium between the periods of bulls and bears.

The SHO oscillates between +40 and -40.

The crossover at those levels creates buy and sell signals.

In an uptrend, the SHO fluctuates between 0 and +40 where the bulls are controlling the market.

On the contrary, the SHO fluctuates between 0 and -40 during downtrends where the bears controlthe market.

Reaching the extreme level -60 in an uptrend is a sign of weakness.

多周期趋势动量面板加强版(Multi-Timeframe Trend Momentum Panel - User Guide)多周期趋势动量面板(Multi-Timeframe Trend Momentum Panel - User Guide)(english explanation follows.)

📖 指标功能详解 (精简版):

🎯 核心功能:

1. 多周期趋势分析 同时监控8个时间周期(1m/5m/15m/1H/4H/D/W/M)

2. 4维度投票系统 MA趋势+RSI动量+MACD+布林带综合判断

3. 全球交易时段 可视化亚洲/伦敦/纽约交易时间

4. 趋势强度评分 0100%量化市场力量

5. 智能警报 强势多空信号自动推送

________________________________________

📚 重要名词解释:

🔵 趋势状态 (MA均线分析):

名词 含义 信号强度

强势多头 快MA远高于慢MA(差值≥0.35%) ⭐⭐⭐⭐⭐ 做多

多头倾向 快MA略高于慢MA(差值<0.35%) ⭐⭐⭐ 谨慎做多

震荡 快慢MA缠绕,无明确方向 ⚠️ 观望

空头倾向 快MA略低于慢MA ⭐⭐⭐ 谨慎做空

强势空头 快MA远低于慢MA ⭐⭐⭐⭐⭐ 做空

简单理解: 快MA就像短跑运动员(反应快),慢MA是长跑运动员(稳定)。短跑远超长跑=强势多头,反之=强势空头。

________________________________________

🟠 动量状态 (RSI力度分析):

名词 含义 操作建议

动量上攻↗ RSI>60且快速上升 强烈买入信号

动量高位 RSI>60但上升变慢 警惕回调,可减仓

动量中性 RSI在4060之间,平稳 等待方向明确

动量低位 RSI<40但下跌变慢 警惕反弹,可止盈

动量下压↘ RSI<40且快速下降 强烈卖出信号

简单理解: RSI就像汽车速度表。"动量上攻"=油门踩到底加速,"动量高位"=已经很快但不再加速了。

________________________________________

🟣 辅助信号:

MACD:

• MACD多头 = 柱状图>0 = 买方力量强

• MACD空头 = 柱状图<0 = 卖方力量强

布林带(BB):

• BB超买 = 价格在布林带上轨附近 = 可能回调

• BB超卖 = 价格在布林带下轨附近 = 可能反弹

• BB中轨 = 价格在中间位置 = 平衡状态

________________________________________

💡 快速上手 3步看懂面板:

第1步: 看"综合结论标签" (K线上方)

• 绿色"多头占优" → 可以做多

• 红色"空头占优" → 可以做空

• 橙色"震荡/均衡" → 观望

第2步: 看"票数 多/空" (面板最下方)

• 多头票数远大于空头 (差距>2) → 趋势强

• 票数接近 (差距<1) → 震荡市

第3步: 看"趋势强度" (综合标签中)

• 强度>70% → 强势趋势,可重仓

• 强度5070% → 中等趋势,正常仓位

• 强度<50% → 弱势,轻仓或观望

________________________________________

🎨 时段背景色含义:

• 紫色背景 = 亚洲时段 (东京交易时间) 波动较小

• 橙色背景 = 伦敦时段 (欧洲交易时间) 波动增大

• 蓝色背景 = 纽约凌晨 美盘准备阶段

• 红色背景 = 纽约关键5分钟 (09:3009:35) ⚠️ 最重要! 市场最活跃,趋势易形成

• 绿色背景 = 纽约上午后段 延续早盘趋势

交易建议: 重点关注红色关键时段,这5分钟往往决定全天方向!

________________________________________

⚙️ 三大市场推荐设置

🥇 黄金: Hull MA 12/EMA 34, 阈值0.250.35%

₿ 比特币: EMA 21/EMA 55, 阈值0.801.20%

💎 以太坊: TEMA 21/EMA 55, 阈值0.600.80%

参数优化建议

黄金 (XAUUSD)

快速MA: Hull MA 12 (超灵敏捕捉黄金快速波动)

慢速MA: EMA 34 (斐波那契数列)

RSI周期: 9 (加快反应)

强趋势阈值: 0.25%

周期: 5, 15, 60, 240, 1440

比特币 (BTCUSD)

快速MA: EMA 21

慢速MA: EMA 55

RSI周期: 14

强趋势阈值: 0.8% (波动大,阈值需提高)

周期: 15, 60, 240, D, W

外汇 EUR/USD

快速MA: TEMA 10 (快速响应)

慢速MA: T3 30, 因子0.7 (平滑噪音)

RSI周期: 14

强趋势阈值: 0.08% (外汇波动小)

周期: 5, 15, 60, 240, 1440

📖 Indicator Function Details (Concise Version):

🎯 Core Functions:

1. MultiTimeframe Trend Analysis Monitors 8 timeframes simultaneously (1m/5m/15m/1H/4H/D/W/M)

2. 4Dimensional Voting System Comprehensive judgment based on MA trend + RSI momentum + MACD + Bollinger Bands

3. Global Trading Sessions Visualizes Asia/London/New York trading hours

4. Trend Strength Score Quantifies market strength from 0100%

5. Smart Alerts Automatically pushes strong bullish/bearish signals

📚 Key Term Explanations:

🔵 Trend Status (MA Analysis):

| Term | Meaning | Signal Strength |

| | | |

| Strong Bull | Fast MA significantly > Slow MA (Diff ≥0.35%) | ⭐⭐⭐⭐⭐ Long |

| Bullish Bias | Fast MA slightly > Slow MA (Diff <0.35%) | ⭐⭐⭐ Caution Long |

| Ranging | MAs intertwined, no clear direction | ⚠️ Wait & See |

| Bearish Bias | Fast MA slightly < Slow MA | ⭐⭐⭐ Caution Short |

| Strong Bear | Fast MA significantly < Slow MA | ⭐⭐⭐⭐⭐ Short |

Simple Understanding: Fast MA = sprinter (fast reaction), Slow MA = longdistance runner (stable). Sprinter far ahead = Strong Bull, opposite = Strong Bear.

🟠 Momentum Status (RSI Analysis):

| Term | Meaning | Trading Suggestion |

| | | |

| Momentum Up ↗ | RSI >60 & rising rapidly | Strong Buy Signal |

| Momentum High | RSI >60 but rising slower | Watch for pullback, consider reducing position |

| Momentum Neutral | RSI between 4060, stable | Wait for clearer direction |

| Momentum Low | RSI <40 but falling slower | Watch for rebound, consider taking profit |

| Momentum Down ↘ | RSI <40 & falling rapidly | Strong Sell Signal |

Simple Understanding: RSI = car speedometer. "Momentum Up" = full throttle acceleration, "Momentum High" = already fast but not accelerating further.

🟣 Auxiliary Signals:

MACD:

MACD Bullish = Histogram >0 = Strong buyer power

MACD Bearish = Histogram <0 = Strong seller power

Bollinger Bands (BB):

BB Overbought = Price near upper band = Possible pullback

BB Oversold = Price near lower band = Possible rebound

BB Middle = Price near middle band = Balanced state

💡 Quick Start 3 Steps to Understand the Panel:

Step 1: Check "Composite Conclusion Label" (Above the chart)

Green "Bulls Favored" → Consider Long

Red "Bears Favored" → Consider Short

Orange "Ranging/Balanced" → Wait & See

Step 2: Check "Votes Bull/Bear" (Bottom of the panel)

Bull votes significantly > Bear votes (Difference >2) → Strong Trend

Votes close (Difference <1) → Ranging Market

Step 3: Check "Trend Strength" (In the composite label)

Strength >70% → Strong Trend, consider heavier position

Strength 5070% → Moderate Trend, normal position size

Strength <50% → Weak Trend, light position or wait & see

🎨 Trading Session Background Color Meanings:

Purple = Asian Session (Tokyo hours) Lower volatility

Orange = London Session (European hours) Increased volatility

Blue = NY Early Morning US session preparation phase

Red = NY Critical 5 Minutes (09:3009:35) ⚠️ Most Important! Market most active, trends easily form

Green = NY Late Morning Continuation of early session trend

Trading Tip: Focus on the red critical period; these 5 minutes often determine the day's direction!

⚙️ Recommended Settings for Three Major Markets

🥇 Gold (XAUUSD):

Fast MA: Hull MA 12 (Highly sensitive for gold's fast moves)

Slow MA: EMA 34 (Fibonacci number)

RSI Period: 9 (Faster reaction)

Strong Trend Threshold: 0.25%

Timeframes: 5, 15, 60, 240, 1440

₿ Bitcoin (BTCUSD):

Fast MA: EMA 21

Slow MA: EMA 55

RSI Period: 14

Strong Trend Threshold: 0.8% (High volatility, requires higher threshold)

Timeframes: 15, 60, 240, D, W

💎 Ethereum (ETHUSD):

Fast MA: TEMA 21

Slow MA: EMA 55

RSI Period: 14

Strong Trend Threshold: 0.600.80%

Timeframes: 15, 60, 240, D, W

💱 Forex EUR/USD:

Fast MA: TEMA 10 (Fast response)

Slow MA: T3 30, Factor 0.7 (Smooths noise)

RSI Period: 14

Strong Trend Threshold: 0.08% (Forex has low volatility)

Timeframes: 5, 15, 60, 240, 1440

多周期趋势动量面板(Multi-Timeframe Trend Momentum Panel - User Guide)多周期趋势动量面板(Multi-Timeframe Trend Momentum Panel - User Guide)(english explanation follows.)

📖 指标功能详解 (精简版):

🎯 核心功能:

1. 多周期趋势分析 同时监控8个时间周期(1m/5m/15m/1H/4H/D/W/M)

2. 4维度投票系统 MA趋势+RSI动量+MACD+布林带综合判断

3. 全球交易时段 可视化亚洲/伦敦/纽约交易时间

4. 趋势强度评分 0100%量化市场力量

5. 智能警报 强势多空信号自动推送

________________________________________

📚 重要名词解释:

🔵 趋势状态 (MA均线分析):

名词 含义 信号强度

强势多头 快MA远高于慢MA(差值≥0.35%) ⭐⭐⭐⭐⭐ 做多

多头倾向 快MA略高于慢MA(差值<0.35%) ⭐⭐⭐ 谨慎做多

震荡 快慢MA缠绕,无明确方向 ⚠️ 观望

空头倾向 快MA略低于慢MA ⭐⭐⭐ 谨慎做空

强势空头 快MA远低于慢MA ⭐⭐⭐⭐⭐ 做空

简单理解: 快MA就像短跑运动员(反应快),慢MA是长跑运动员(稳定)。短跑远超长跑=强势多头,反之=强势空头。

________________________________________

🟠 动量状态 (RSI力度分析):

名词 含义 操作建议

动量上攻↗ RSI>60且快速上升 强烈买入信号

动量高位 RSI>60但上升变慢 警惕回调,可减仓

动量中性 RSI在4060之间,平稳 等待方向明确

动量低位 RSI<40但下跌变慢 警惕反弹,可止盈

动量下压↘ RSI<40且快速下降 强烈卖出信号

简单理解: RSI就像汽车速度表。"动量上攻"=油门踩到底加速,"动量高位"=已经很快但不再加速了。

________________________________________

🟣 辅助信号:

MACD:

• MACD多头 = 柱状图>0 = 买方力量强

• MACD空头 = 柱状图<0 = 卖方力量强

布林带(BB):

• BB超买 = 价格在布林带上轨附近 = 可能回调

• BB超卖 = 价格在布林带下轨附近 = 可能反弹

• BB中轨 = 价格在中间位置 = 平衡状态

________________________________________

💡 快速上手 3步看懂面板:

第1步: 看"综合结论标签" (K线上方)

• 绿色"多头占优" → 可以做多

• 红色"空头占优" → 可以做空

• 橙色"震荡/均衡" → 观望

第2步: 看"票数 多/空" (面板最下方)

• 多头票数远大于空头 (差距>2) → 趋势强

• 票数接近 (差距<1) → 震荡市

第3步: 看"趋势强度" (综合标签中)

• 强度>70% → 强势趋势,可重仓

• 强度5070% → 中等趋势,正常仓位

• 强度<50% → 弱势,轻仓或观望

________________________________________

🎨 时段背景色含义:

• 紫色背景 = 亚洲时段 (东京交易时间) 波动较小

• 橙色背景 = 伦敦时段 (欧洲交易时间) 波动增大

• 蓝色背景 = 纽约凌晨 美盘准备阶段

• 红色背景 = 纽约关键5分钟 (09:3009:35) ⚠️ 最重要! 市场最活跃,趋势易形成

• 绿色背景 = 纽约上午后段 延续早盘趋势

交易建议: 重点关注红色关键时段,这5分钟往往决定全天方向!

________________________________________

⚙️ 三大市场推荐设置

🥇 黄金: Hull MA 12/EMA 34, 阈值0.250.35%

₿ 比特币: EMA 21/EMA 55, 阈值0.801.20%

💎 以太坊: TEMA 21/EMA 55, 阈值0.600.80%

参数优化建议

黄金 (XAUUSD)

快速MA: Hull MA 12 (超灵敏捕捉黄金快速波动)

慢速MA: EMA 34 (斐波那契数列)

RSI周期: 9 (加快反应)

强趋势阈值: 0.25%

周期: 5, 15, 60, 240, 1440

比特币 (BTCUSD)

快速MA: EMA 21

慢速MA: EMA 55

RSI周期: 14

强趋势阈值: 0.8% (波动大,阈值需提高)

周期: 15, 60, 240, D, W

外汇 EUR/USD

快速MA: TEMA 10 (快速响应)

慢速MA: T3 30, 因子0.7 (平滑噪音)

RSI周期: 14

强趋势阈值: 0.08% (外汇波动小)

周期: 5, 15, 60, 240, 1440

📖 Indicator Function Details (Concise Version):

🎯 Core Functions:

1. MultiTimeframe Trend Analysis Monitors 8 timeframes simultaneously (1m/5m/15m/1H/4H/D/W/M)

2. 4Dimensional Voting System Comprehensive judgment based on MA trend + RSI momentum + MACD + Bollinger Bands

3. Global Trading Sessions Visualizes Asia/London/New York trading hours

4. Trend Strength Score Quantifies market strength from 0100%

5. Smart Alerts Automatically pushes strong bullish/bearish signals

📚 Key Term Explanations:

🔵 Trend Status (MA Analysis):

| Term | Meaning | Signal Strength |

| | | |

| Strong Bull | Fast MA significantly > Slow MA (Diff ≥0.35%) | ⭐⭐⭐⭐⭐ Long |

| Bullish Bias | Fast MA slightly > Slow MA (Diff <0.35%) | ⭐⭐⭐ Caution Long |

| Ranging | MAs intertwined, no clear direction | ⚠️ Wait & See |

| Bearish Bias | Fast MA slightly < Slow MA | ⭐⭐⭐ Caution Short |

| Strong Bear | Fast MA significantly < Slow MA | ⭐⭐⭐⭐⭐ Short |

Simple Understanding: Fast MA = sprinter (fast reaction), Slow MA = longdistance runner (stable). Sprinter far ahead = Strong Bull, opposite = Strong Bear.

🟠 Momentum Status (RSI Analysis):

| Term | Meaning | Trading Suggestion |

| | | |

| Momentum Up ↗ | RSI >60 & rising rapidly | Strong Buy Signal |

| Momentum High | RSI >60 but rising slower | Watch for pullback, consider reducing position |

| Momentum Neutral | RSI between 4060, stable | Wait for clearer direction |

| Momentum Low | RSI <40 but falling slower | Watch for rebound, consider taking profit |

| Momentum Down ↘ | RSI <40 & falling rapidly | Strong Sell Signal |

Simple Understanding: RSI = car speedometer. "Momentum Up" = full throttle acceleration, "Momentum High" = already fast but not accelerating further.

🟣 Auxiliary Signals:

MACD:

MACD Bullish = Histogram >0 = Strong buyer power

MACD Bearish = Histogram <0 = Strong seller power

Bollinger Bands (BB):

BB Overbought = Price near upper band = Possible pullback

BB Oversold = Price near lower band = Possible rebound

BB Middle = Price near middle band = Balanced state

💡 Quick Start 3 Steps to Understand the Panel:

Step 1: Check "Composite Conclusion Label" (Above the chart)

Green "Bulls Favored" → Consider Long

Red "Bears Favored" → Consider Short

Orange "Ranging/Balanced" → Wait & See

Step 2: Check "Votes Bull/Bear" (Bottom of the panel)

Bull votes significantly > Bear votes (Difference >2) → Strong Trend

Votes close (Difference <1) → Ranging Market

Step 3: Check "Trend Strength" (In the composite label)

Strength >70% → Strong Trend, consider heavier position

Strength 5070% → Moderate Trend, normal position size

Strength <50% → Weak Trend, light position or wait & see

🎨 Trading Session Background Color Meanings:

Purple = Asian Session (Tokyo hours) Lower volatility

Orange = London Session (European hours) Increased volatility

Blue = NY Early Morning US session preparation phase

Red = NY Critical 5 Minutes (09:3009:35) ⚠️ Most Important! Market most active, trends easily form

Green = NY Late Morning Continuation of early session trend

Trading Tip: Focus on the red critical period; these 5 minutes often determine the day's direction!

⚙️ Recommended Settings for Three Major Markets

🥇 Gold (XAUUSD):

Fast MA: Hull MA 12 (Highly sensitive for gold's fast moves)

Slow MA: EMA 34 (Fibonacci number)

RSI Period: 9 (Faster reaction)

Strong Trend Threshold: 0.25%

Timeframes: 5, 15, 60, 240, 1440

₿ Bitcoin (BTCUSD):

Fast MA: EMA 21

Slow MA: EMA 55

RSI Period: 14

Strong Trend Threshold: 0.8% (High volatility, requires higher threshold)

Timeframes: 15, 60, 240, D, W

💎 Ethereum (ETHUSD):

Fast MA: TEMA 21

Slow MA: EMA 55

RSI Period: 14

Strong Trend Threshold: 0.600.80%

Timeframes: 15, 60, 240, D, W

💱 Forex EUR/USD:

Fast MA: TEMA 10 (Fast response)

Slow MA: T3 30, Factor 0.7 (Smooths noise)

RSI Period: 14

Strong Trend Threshold: 0.08% (Forex has low volatility)

Timeframes: 5, 15, 60, 240, 1440

Market Sentiment Trend Gauge [LevelUp]Market Sentiment Trend Gauge simplifies technical analysis by mathematically combining momentum, trend direction, volatility position, and comparison against a market benchmark, into a single trend score from -100 to +100. Displayed in a separate pane below your chart, it resolves conflicting signals from RSI, moving averages, Bollinger Bands, and market correlations, providing clear insights into trend direction, strength, and relative performance.

THE PROBLEM MARKET SENTIMENT TREND GAUGE (MSTG) SOLVES

Traditional indicators often produce conflicting signals, such as RSI showing overbought while prices rise or moving averages indicating an uptrend despite market underperformance. MSTG creates a weighted composite score to answer: "What's the overall bias for this asset?"

KEY COMPONENTS AND WEIGHTINGS

The trend score combines

▪ Momentum (25%): Normalized 14-period RSI, capped at ±100.

▪ Trend Direction (35%): 10/21-period EMA relationships,

▪ Volatility Position (20%): Price position, 20-period Bollinger Bands, capped at ±100.

▪ Market Comparison (20%): Daily performance vs. SPY benchmark, capped at ±100.

Final score = Weighted sum, smoothed with 5-period EMA.

INTERPRETING THE MSTG CHART

Trend Score Ranges and Colors

▪ Bright Green (>+30): Strong bullish; ideal for long entries.

▪ Light Green (+10 to +30): Weak bullish; cautiously favorable.

▪ Gray (-10 to +10): Neutral; avoid directional trades.

▪ Light Red (-10 to -30): Weak bearish; exercise caution.

▪ Bright Red (<-30): Strong bearish; high-risk for longs, consider shorts.

Reference Lines

▪ Zero Line (Gray): Separates bullish/bearish; crossovers signal trend changes.

▪ ±30 Lines (Dotted, Green/Red): Thresholds for strong trends.

▪ ±60 Lines (Dashed, Green/Red): Extreme strength zones (not overbought/oversold); manage risk (tighten stops, partial profits) but trends may persist.

Background Colors

▪ Green Tint (>+20): Bullish environment; favorable for longs.

▪ Red Tint (<-20): Bearish environment; caution for longs.

▪ Light Gray Tint (-20 to +20): Neutral/range-bound; wait for signals.

Extreme Readings vs. Traditional Signals

MSTG ±60 indicates maximum alignment of all factors, not reversals (unlike RSI >70/<30). Use for risk management, not automatic exits. Strong trends can sustain extremes; breakdowns occur below +30 or above -30.

INFORMATION TABLE INTERPRETATION

Trend Score Symbols

▲▲ >+30 strong bullish

▲ +10 to +30

● -10 to +10 neutral

▼ -30 to -10

▼▼ <-30 strong bearish

Colors: Green (positive), White (neutral), Red (negative).

Momentum Score

+40 to +100 strong bullish

0 to +40 moderate bullish

-40 to 0 moderate bearish

-100 to -40 strong bearish

Market vs. Stock

▪ Green: Stock outperforming market

▪ Red: Stock underperforming market

Example Interpretations:

-0.45% / +1.23% (Green): Market down, stock up = Strong relative strength

+2.10% / +1.50% (Red): Both rising, but stock lagging = Relative weakness

-1.20% / -0.80% (Green): Both falling, but stock declining less = Defensive strength

UNDERSTANDING EXTREME READINGS VS TRADITIONAL OVERBOUGHT/OVERSOLD

⚠️ Critical distinctions

Traditional Overbought/Oversold Signals:

▪ Single indicator (like RSI >70 or <30) showing momentum excess

▪ Often suggests immediate reversal or pullback expected

▪ Based on "price moved too far, too fast" concept

MSTG Extreme Readings (±60):

▪ Composite alignment of 4 different factors (momentum, trend, volatility, relative strength)

▪ Indicates maximum strength in current direction

▪ NOT a reversal signal - means "all systems extremely bullish/bearish"

Key Differences:

▪ RSI >70: "Price got ahead of itself, expect pullback"

▪ MSTG >+60: "Everything is extremely bullish right now"

▪ Strong trends can maintain extreme MSTG readings during major moves

▪ Breakdowns happen when MSTG falls below +30, not at +60

Proper Usage of Extreme Readings:

▪ Risk Management: Tighten stops, take partial profits

▪ Position Sizing: Reduce new position sizes at extremes

▪ Trend Continuation: Watch for sustained extreme readings in strong markets

▪ Exit Signals: Look for breakdown below +30, not reversal from +60

TRADING WITH MSTG

Quick Assessment

1. Check trend symbol for direction.

2. Confirm momentum strength.

3. Note relative performance color.

Examples:

▲▲ 55.2 (Green), Momentum +28.4, Outperforming: Strong buy setup.

▼ -18.6 (Red), Momentum -43.2, Underperforming: Defensive positioning.

Entry Conditions

▪ Long: stock outperforming market

- Score >+30 (bright green)

- Sustained green background

- ▲▲ symbol,

▪ Short: stock underperforming market

- Score <-30 (bright red)

- Sustained red background

- ▼▼ symbol

Avoid Trading When:

▪ Gray zone (-10 to +10).

▪ Rapid color changes or frequent zero-line crosses (choppy market).

▪ Gray background (range-bound).

Risk Management:

▪ Stop Loss: Exit on zero-line crossover against position.

▪ Take Profit: Partial at ±60 for risk control.

▪ Position Sizing: Larger when signals align; smaller in extremes or mixed conditions.

KEY ADVANTAGES

▪ Unified View: Weighted composite reduces noise and conflicts.

▪ Visual Clarity: 5-color system with gradients for rapid recognition.

▪ Market Context: Relative strength vs. SPY identifies leaders/laggards.

▪ Flexibility: Works across timeframes (1-min to weekly); customizable table.

▪ Noise Reduction: EMA smoothing minimizes false signals.

EXAMPLES

Strong Bull: Trend Score 71.9, Momentum Score 76.9

Neutral: Trend Score 0.1, Momentum Score -9.2

Strong Bear: Trend Score -51.7, Momentum Score -51.5

PERFORMANCE AND LIMITATIONS

Strengths: Trend identification, noise reduction, relative performance versus market.

Limitations: Lags at turning points, less effective in extreme volatility or non-trending markets.

Recommendations: View on multiple timeframes, combine with price action and fundamentals.

Small Business Economic Conditions - Statistical Analysis ModelThe Small Business Economic Conditions Statistical Analysis Model (SBO-SAM) represents an econometric approach to measuring and analyzing the economic health of small business enterprises through multi-dimensional factor analysis and statistical methodologies. This indicator synthesizes eight fundamental economic components into a composite index that provides real-time assessment of small business operating conditions with statistical rigor. The model employs Z-score standardization, variance-weighted aggregation, higher-order moment analysis, and regime-switching detection to deliver comprehensive insights into small business economic conditions with statistical confidence intervals and multi-language accessibility.

1. Introduction and Theoretical Foundation

The development of quantitative models for assessing small business economic conditions has gained significant importance in contemporary financial analysis, particularly given the critical role small enterprises play in economic development and employment generation. Small businesses, typically defined as enterprises with fewer than 500 employees according to the U.S. Small Business Administration, constitute approximately 99.9% of all businesses in the United States and employ nearly half of the private workforce (U.S. Small Business Administration, 2024).

The theoretical framework underlying the SBO-SAM model draws extensively from established academic research in small business economics and quantitative finance. The foundational understanding of key drivers affecting small business performance builds upon the seminal work of Dunkelberg and Wade (2023) in their analysis of small business economic trends through the National Federation of Independent Business (NFIB) Small Business Economic Trends survey. Their research established the critical importance of optimism, hiring plans, capital expenditure intentions, and credit availability as primary determinants of small business performance.

The model incorporates insights from Federal Reserve Board research, particularly the Senior Loan Officer Opinion Survey (Federal Reserve Board, 2024), which demonstrates the critical importance of credit market conditions in small business operations. This research consistently shows that small businesses face disproportionate challenges during periods of credit tightening, as they typically lack access to capital markets and rely heavily on bank financing.

The statistical methodology employed in this model follows the econometric principles established by Hamilton (1989) in his work on regime-switching models and time series analysis. Hamilton's framework provides the theoretical foundation for identifying different economic regimes and understanding how economic relationships may vary across different market conditions. The variance-weighted aggregation technique draws from modern portfolio theory as developed by Markowitz (1952) and later refined by Sharpe (1964), applying these concepts to economic indicator construction rather than traditional asset allocation.

Additional theoretical support comes from the work of Engle and Granger (1987) on cointegration analysis, which provides the statistical framework for combining multiple time series while maintaining long-term equilibrium relationships. The model also incorporates insights from behavioral economics research by Kahneman and Tversky (1979) on prospect theory, recognizing that small business decision-making may exhibit systematic biases that affect economic outcomes.

2. Model Architecture and Component Structure

The SBO-SAM model employs eight orthogonalized economic factors that collectively capture the multifaceted nature of small business operating conditions. Each component is normalized using Z-score standardization with a rolling 252-day window, representing approximately one business year of trading data. This approach ensures statistical consistency across different market regimes and economic cycles, following the methodology established by Tsay (2010) in his treatment of financial time series analysis.

2.1 Small Cap Relative Performance Component

The first component measures the performance of the Russell 2000 index relative to the S&P 500, capturing the market-based assessment of small business equity valuations. This component reflects investor sentiment toward smaller enterprises and provides a forward-looking perspective on small business prospects. The theoretical justification for this component stems from the efficient market hypothesis as formulated by Fama (1970), which suggests that stock prices incorporate all available information about future prospects.

The calculation employs a 20-day rate of change with exponential smoothing to reduce noise while preserving signal integrity. The mathematical formulation is:

Small_Cap_Performance = (Russell_2000_t / S&P_500_t) / (Russell_2000_{t-20} / S&P_500_{t-20}) - 1

This relative performance measure eliminates market-wide effects and isolates the specific performance differential between small and large capitalization stocks, providing a pure measure of small business market sentiment.

2.2 Credit Market Conditions Component

Credit Market Conditions constitute the second component, incorporating commercial lending volumes and credit spread dynamics. This factor recognizes that small businesses are particularly sensitive to credit availability and borrowing costs, as established in numerous Federal Reserve studies (Bernanke and Gertler, 1995). Small businesses typically face higher borrowing costs and more stringent lending standards compared to larger enterprises, making credit conditions a critical determinant of their operating environment.

The model calculates credit spreads using high-yield bond ETFs relative to Treasury securities, providing a market-based measure of credit risk premiums that directly affect small business borrowing costs. The component also incorporates commercial and industrial loan growth data from the Federal Reserve's H.8 statistical release, which provides direct evidence of lending activity to businesses.

The mathematical specification combines these elements as:

Credit_Conditions = α₁ × (HYG_t / TLT_t) + α₂ × C&I_Loan_Growth_t

where HYG represents high-yield corporate bond ETF prices, TLT represents long-term Treasury ETF prices, and C&I_Loan_Growth represents the rate of change in commercial and industrial loans outstanding.

2.3 Labor Market Dynamics Component

The Labor Market Dynamics component captures employment cost pressures and labor availability metrics through the relationship between job openings and unemployment claims. This factor acknowledges that labor market tightness significantly impacts small business operations, as these enterprises typically have less flexibility in wage negotiations and face greater challenges in attracting and retaining talent during periods of low unemployment.

The theoretical foundation for this component draws from search and matching theory as developed by Mortensen and Pissarides (1994), which explains how labor market frictions affect employment dynamics. Small businesses often face higher search costs and longer hiring processes, making them particularly sensitive to labor market conditions.

The component is calculated as:

Labor_Tightness = Job_Openings_t / (Unemployment_Claims_t × 52)

This ratio provides a measure of labor market tightness, with higher values indicating greater difficulty in finding workers and potential wage pressures.

2.4 Consumer Demand Strength Component

Consumer Demand Strength represents the fourth component, combining consumer sentiment data with retail sales growth rates. Small businesses are disproportionately affected by consumer spending patterns, making this component crucial for assessing their operating environment. The theoretical justification comes from the permanent income hypothesis developed by Friedman (1957), which explains how consumer spending responds to both current conditions and future expectations.

The model weights consumer confidence and actual spending data to provide both forward-looking sentiment and contemporaneous demand indicators. The specification is:

Demand_Strength = β₁ × Consumer_Sentiment_t + β₂ × Retail_Sales_Growth_t

where β₁ and β₂ are determined through principal component analysis to maximize the explanatory power of the combined measure.

2.5 Input Cost Pressures Component

Input Cost Pressures form the fifth component, utilizing producer price index data to capture inflationary pressures on small business operations. This component is inversely weighted, recognizing that rising input costs negatively impact small business profitability and operating conditions. Small businesses typically have limited pricing power and face challenges in passing through cost increases to customers, making them particularly vulnerable to input cost inflation.

The theoretical foundation draws from cost-push inflation theory as described by Gordon (1988), which explains how supply-side price pressures affect business operations. The model employs a 90-day rate of change to capture medium-term cost trends while filtering out short-term volatility:

Cost_Pressure = -1 × (PPI_t / PPI_{t-90} - 1)

The negative weighting reflects the inverse relationship between input costs and business conditions.

2.6 Monetary Policy Impact Component

Monetary Policy Impact represents the sixth component, incorporating federal funds rates and yield curve dynamics. Small businesses are particularly sensitive to interest rate changes due to their higher reliance on variable-rate financing and limited access to capital markets. The theoretical foundation comes from monetary transmission mechanism theory as developed by Bernanke and Blinder (1992), which explains how monetary policy affects different segments of the economy.

The model calculates the absolute deviation of federal funds rates from a neutral 2% level, recognizing that both extremely low and high rates can create operational challenges for small enterprises. The yield curve component captures the shape of the term structure, which affects both borrowing costs and economic expectations:

Monetary_Impact = γ₁ × |Fed_Funds_Rate_t - 2.0| + γ₂ × (10Y_Yield_t - 2Y_Yield_t)

2.7 Currency Valuation Effects Component

Currency Valuation Effects constitute the seventh component, measuring the impact of US Dollar strength on small business competitiveness. A stronger dollar can benefit businesses with significant import components while disadvantaging exporters. The model employs Dollar Index volatility as a proxy for currency-related uncertainty that affects small business planning and operations.

The theoretical foundation draws from international trade theory and the work of Krugman (1987) on exchange rate effects on different business segments. Small businesses often lack hedging capabilities, making them more vulnerable to currency fluctuations:

Currency_Impact = -1 × DXY_Volatility_t

2.8 Regional Banking Health Component

The eighth and final component, Regional Banking Health, assesses the relative performance of regional banks compared to large financial institutions. Regional banks traditionally serve as primary lenders to small businesses, making their health a critical factor in small business credit availability and overall operating conditions.

This component draws from the literature on relationship banking as developed by Boot (2000), which demonstrates the importance of bank-borrower relationships, particularly for small enterprises. The calculation compares regional bank performance to large financial institutions:

Banking_Health = (Regional_Banks_Index_t / Large_Banks_Index_t) - 1

3. Statistical Methodology and Advanced Analytics

The model employs statistical techniques to ensure robustness and reliability. Z-score normalization is applied to each component using rolling 252-day windows, providing standardized measures that remain consistent across different time periods and market conditions. This approach follows the methodology established by Engle and Granger (1987) in their cointegration analysis framework.

3.1 Variance-Weighted Aggregation

The composite index calculation utilizes variance-weighted aggregation, where component weights are determined by the inverse of their historical variance. This approach, derived from modern portfolio theory, ensures that more stable components receive higher weights while reducing the impact of highly volatile factors. The mathematical formulation follows the principle that optimal weights are inversely proportional to variance, maximizing the signal-to-noise ratio of the composite indicator.

The weight for component i is calculated as:

w_i = (1/σᵢ²) / Σⱼ(1/σⱼ²)

where σᵢ² represents the variance of component i over the lookback period.

3.2 Higher-Order Moment Analysis

Higher-order moment analysis extends beyond traditional mean and variance calculations to include skewness and kurtosis measurements. Skewness provides insight into the asymmetry of the sentiment distribution, while kurtosis measures the tail behavior and potential for extreme events. These metrics offer valuable information about the underlying distribution characteristics and potential regime changes.

Skewness is calculated as:

Skewness = E / σ³

Kurtosis is calculated as:

Kurtosis = E / σ⁴ - 3

where μ represents the mean and σ represents the standard deviation of the distribution.

3.3 Regime-Switching Detection

The model incorporates regime-switching detection capabilities based on the Hamilton (1989) framework. This allows for identification of different economic regimes characterized by distinct statistical properties. The regime classification employs percentile-based thresholds:

- Regime 3 (Very High): Percentile rank > 80

- Regime 2 (High): Percentile rank 60-80

- Regime 1 (Moderate High): Percentile rank 50-60

- Regime 0 (Neutral): Percentile rank 40-50

- Regime -1 (Moderate Low): Percentile rank 30-40

- Regime -2 (Low): Percentile rank 20-30

- Regime -3 (Very Low): Percentile rank < 20

3.4 Information Theory Applications

The model incorporates information theory concepts, specifically Shannon entropy measurement, to assess the information content of the sentiment distribution. Shannon entropy, as developed by Shannon (1948), provides a measure of the uncertainty or information content in a probability distribution:

H(X) = -Σᵢ p(xᵢ) log₂ p(xᵢ)

Higher entropy values indicate greater unpredictability and information content in the sentiment series.

3.5 Long-Term Memory Analysis

The Hurst exponent calculation provides insight into the long-term memory characteristics of the sentiment series. Originally developed by Hurst (1951) for analyzing Nile River flow patterns, this measure has found extensive application in financial time series analysis. The Hurst exponent H is calculated using the rescaled range statistic:

H = log(R/S) / log(T)

where R/S represents the rescaled range and T represents the time period. Values of H > 0.5 indicate long-term positive autocorrelation (persistence), while H < 0.5 indicates mean-reverting behavior.

3.6 Structural Break Detection

The model employs Chow test approximation for structural break detection, based on the methodology developed by Chow (1960). This technique identifies potential structural changes in the underlying relationships by comparing the stability of regression parameters across different time periods:

Chow_Statistic = (RSS_restricted - RSS_unrestricted) / RSS_unrestricted × (n-2k)/k

where RSS represents residual sum of squares, n represents sample size, and k represents the number of parameters.

4. Implementation Parameters and Configuration

4.1 Language Selection Parameters

The model provides comprehensive multi-language support across five languages: English, German (Deutsch), Spanish (Español), French (Français), and Japanese (日本語). This feature enhances accessibility for international users and ensures cultural appropriateness in terminology usage. The language selection affects all internal displays, statistical classifications, and alert messages while maintaining consistency in underlying calculations.

4.2 Model Configuration Parameters

Calculation Method: Users can select from four aggregation methodologies:

- Equal-Weighted: All components receive identical weights

- Variance-Weighted: Components weighted inversely to their historical variance

- Principal Component: Weights determined through principal component analysis

- Dynamic: Adaptive weighting based on recent performance

Sector Specification: The model allows for sector-specific calibration:

- General: Broad-based small business assessment

- Retail: Emphasis on consumer demand and seasonal factors

- Manufacturing: Enhanced weighting of input costs and currency effects

- Services: Focus on labor market dynamics and consumer demand

- Construction: Emphasis on credit conditions and monetary policy

Lookback Period: Statistical analysis window ranging from 126 to 504 trading days, with 252 days (one business year) as the optimal default based on academic research.

Smoothing Period: Exponential moving average period from 1 to 21 days, with 5 days providing optimal noise reduction while preserving signal integrity.

4.3 Statistical Threshold Parameters

Upper Statistical Boundary: Configurable threshold between 60-80 (default 70) representing the upper significance level for regime classification.

Lower Statistical Boundary: Configurable threshold between 20-40 (default 30) representing the lower significance level for regime classification.

Statistical Significance Level (α): Alpha level for statistical tests, configurable between 0.01-0.10 with 0.05 as the standard academic default.

4.4 Display and Visualization Parameters

Color Theme Selection: Eight professional color schemes optimized for different user preferences and accessibility requirements:

- Gold: Traditional financial industry colors

- EdgeTools: Professional blue-gray scheme

- Behavioral: Psychology-based color mapping

- Quant: Value-based quantitative color scheme

- Ocean: Blue-green maritime theme

- Fire: Warm red-orange theme

- Matrix: Green-black technology theme

- Arctic: Cool blue-white theme

Dark Mode Optimization: Automatic color adjustment for dark chart backgrounds, ensuring optimal readability across different viewing conditions.

Line Width Configuration: Main index line thickness adjustable from 1-5 pixels for optimal visibility.

Background Intensity: Transparency control for statistical regime backgrounds, adjustable from 90-99% for subtle visual enhancement without distraction.

4.5 Alert System Configuration

Alert Frequency Options: Three frequency settings to match different trading styles:

- Once Per Bar: Single alert per bar formation

- Once Per Bar Close: Alert only on confirmed bar close

- All: Continuous alerts for real-time monitoring

Statistical Extreme Alerts: Notifications when the index reaches 99% confidence levels (Z-score > 2.576 or < -2.576).

Regime Transition Alerts: Notifications when statistical boundaries are crossed, indicating potential regime changes.

5. Practical Application and Interpretation Guidelines

5.1 Index Interpretation Framework

The SBO-SAM index operates on a 0-100 scale with statistical normalization ensuring consistent interpretation across different time periods and market conditions. Values above 70 indicate statistically elevated small business conditions, suggesting favorable operating environment with potential for expansion and growth. Values below 30 indicate statistically reduced conditions, suggesting challenging operating environment with potential constraints on business activity.

The median reference line at 50 represents the long-term equilibrium level, with deviations providing insight into cyclical conditions relative to historical norms. The statistical confidence bands at 95% levels (approximately ±2 standard deviations) help identify when conditions reach statistically significant extremes.

5.2 Regime Classification System

The model employs a seven-level regime classification system based on percentile rankings:

Very High Regime (P80+): Exceptional small business conditions, typically associated with strong economic growth, easy credit availability, and favorable regulatory environment. Historical analysis suggests these periods often precede economic peaks and may warrant caution regarding sustainability.

High Regime (P60-80): Above-average conditions supporting business expansion and investment. These periods typically feature moderate growth, stable credit conditions, and positive consumer sentiment.

Moderate High Regime (P50-60): Slightly above-normal conditions with mixed signals. Careful monitoring of individual components helps identify emerging trends.

Neutral Regime (P40-50): Balanced conditions near long-term equilibrium. These periods often represent transition phases between different economic cycles.

Moderate Low Regime (P30-40): Slightly below-normal conditions with emerging headwinds. Early warning signals may appear in credit conditions or consumer demand.

Low Regime (P20-30): Below-average conditions suggesting challenging operating environment. Businesses may face constraints on growth and expansion.

Very Low Regime (P0-20): Severely constrained conditions, typically associated with economic recessions or financial crises. These periods often present opportunities for contrarian positioning.

5.3 Component Analysis and Diagnostics

Individual component analysis provides valuable diagnostic information about the underlying drivers of overall conditions. Divergences between components can signal emerging trends or structural changes in the economy.

Credit-Labor Divergence: When credit conditions improve while labor markets tighten, this may indicate early-stage economic acceleration with potential wage pressures.

Demand-Cost Divergence: Strong consumer demand coupled with rising input costs suggests inflationary pressures that may constrain small business margins.

Market-Fundamental Divergence: Disconnection between small-cap equity performance and fundamental conditions may indicate market inefficiencies or changing investor sentiment.

5.4 Temporal Analysis and Trend Identification

The model provides multiple temporal perspectives through momentum analysis, rate of change calculations, and trend decomposition. The 20-day momentum indicator helps identify short-term directional changes, while the Hodrick-Prescott filter approximation separates cyclical components from long-term trends.

Acceleration analysis through second-order momentum calculations provides early warning signals for potential trend reversals. Positive acceleration during declining conditions may indicate approaching inflection points, while negative acceleration during improving conditions may suggest momentum loss.

5.5 Statistical Confidence and Uncertainty Quantification

The model provides comprehensive uncertainty quantification through confidence intervals, volatility measures, and regime stability analysis. The 95% confidence bands help users understand the statistical significance of current readings and identify when conditions reach historically extreme levels.

Volatility analysis provides insight into the stability of current conditions, with higher volatility indicating greater uncertainty and potential for rapid changes. The regime stability measure, calculated as the inverse of volatility, helps assess the sustainability of current conditions.

6. Risk Management and Limitations

6.1 Model Limitations and Assumptions

The SBO-SAM model operates under several important assumptions that users must understand for proper interpretation. The model assumes that historical relationships between economic variables remain stable over time, though the regime-switching framework helps accommodate some structural changes. The 252-day lookback period provides reasonable statistical power while maintaining sensitivity to changing conditions, but may not capture longer-term structural shifts.

The model's reliance on publicly available economic data introduces inherent lags in some components, particularly those based on government statistics. Users should consider these timing differences when interpreting real-time conditions. Additionally, the model's focus on quantitative factors may not fully capture qualitative factors such as regulatory changes, geopolitical events, or technological disruptions that could significantly impact small business conditions.

The model's timeframe restrictions ensure statistical validity by preventing application to intraday periods where the underlying economic relationships may be distorted by market microstructure effects, trading noise, and temporal misalignment with the fundamental data sources. Users must utilize daily or longer timeframes to ensure the model's statistical foundations remain valid and interpretable.

6.2 Data Quality and Reliability Considerations

The model's accuracy depends heavily on the quality and availability of underlying economic data. Market-based components such as equity indices and bond prices provide real-time information but may be subject to short-term volatility unrelated to fundamental conditions. Economic statistics provide more stable fundamental information but may be subject to revisions and reporting delays.

Users should be aware that extreme market conditions may temporarily distort some components, particularly those based on financial market data. The model's statistical normalization helps mitigate these effects, but users should exercise additional caution during periods of market stress or unusual volatility.

6.3 Interpretation Caveats and Best Practices

The SBO-SAM model provides statistical analysis and should not be interpreted as investment advice or predictive forecasting. The model's output represents an assessment of current conditions based on historical relationships and may not accurately predict future outcomes. Users should combine the model's insights with other analytical tools and fundamental analysis for comprehensive decision-making.

The model's regime classifications are based on historical percentile rankings and may not fully capture the unique characteristics of current economic conditions. Users should consider the broader economic context and potential structural changes when interpreting regime classifications.

7. Academic References and Bibliography

Bernanke, B. S., & Blinder, A. S. (1992). The Federal Funds Rate and the Channels of Monetary Transmission. American Economic Review, 82(4), 901-921.

Bernanke, B. S., & Gertler, M. (1995). Inside the Black Box: The Credit Channel of Monetary Policy Transmission. Journal of Economic Perspectives, 9(4), 27-48.

Boot, A. W. A. (2000). Relationship Banking: What Do We Know? Journal of Financial Intermediation, 9(1), 7-25.

Chow, G. C. (1960). Tests of Equality Between Sets of Coefficients in Two Linear Regressions. Econometrica, 28(3), 591-605.

Dunkelberg, W. C., & Wade, H. (2023). NFIB Small Business Economic Trends. National Federation of Independent Business Research Foundation, Washington, D.C.

Engle, R. F., & Granger, C. W. J. (1987). Co-integration and Error Correction: Representation, Estimation, and Testing. Econometrica, 55(2), 251-276.

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. Journal of Finance, 25(2), 383-417.

Federal Reserve Board. (2024). Senior Loan Officer Opinion Survey on Bank Lending Practices. Board of Governors of the Federal Reserve System, Washington, D.C.

Friedman, M. (1957). A Theory of the Consumption Function. Princeton University Press, Princeton, NJ.

Gordon, R. J. (1988). The Role of Wages in the Inflation Process. American Economic Review, 78(2), 276-283.

Hamilton, J. D. (1989). A New Approach to the Economic Analysis of Nonstationary Time Series and the Business Cycle. Econometrica, 57(2), 357-384.

Hurst, H. E. (1951). Long-term Storage Capacity of Reservoirs. Transactions of the American Society of Civil Engineers, 116(1), 770-799.

Kahneman, D., & Tversky, A. (1979). Prospect Theory: An Analysis of Decision under Risk. Econometrica, 47(2), 263-291.

Krugman, P. (1987). Pricing to Market When the Exchange Rate Changes. In S. W. Arndt & J. D. Richardson (Eds.), Real-Financial Linkages among Open Economies (pp. 49-70). MIT Press, Cambridge, MA.

Markowitz, H. (1952). Portfolio Selection. Journal of Finance, 7(1), 77-91.

Mortensen, D. T., & Pissarides, C. A. (1994). Job Creation and Job Destruction in the Theory of Unemployment. Review of Economic Studies, 61(3), 397-415.

Shannon, C. E. (1948). A Mathematical Theory of Communication. Bell System Technical Journal, 27(3), 379-423.

Sharpe, W. F. (1964). Capital Asset Prices: A Theory of Market Equilibrium under Conditions of Risk. Journal of Finance, 19(3), 425-442.

Tsay, R. S. (2010). Analysis of Financial Time Series (3rd ed.). John Wiley & Sons, Hoboken, NJ.

U.S. Small Business Administration. (2024). Small Business Profile. Office of Advocacy, Washington, D.C.

8. Technical Implementation Notes

The SBO-SAM model is implemented in Pine Script version 6 for the TradingView platform, ensuring compatibility with modern charting and analysis tools. The implementation follows best practices for financial indicator development, including proper error handling, data validation, and performance optimization.

The model includes comprehensive timeframe validation to ensure statistical accuracy and reliability. The indicator operates exclusively on daily (1D) timeframes or higher, including weekly (1W), monthly (1M), and longer periods. This restriction ensures that the statistical analysis maintains appropriate temporal resolution for the underlying economic data sources, which are primarily reported on daily or longer intervals.

When users attempt to apply the model to intraday timeframes (such as 1-minute, 5-minute, 15-minute, 30-minute, 1-hour, 2-hour, 4-hour, 6-hour, 8-hour, or 12-hour charts), the system displays a comprehensive error message in the user's selected language and prevents execution. This safeguard protects users from potentially misleading results that could occur when applying daily-based economic analysis to shorter timeframes where the underlying data relationships may not hold.

The model's statistical calculations are performed using vectorized operations where possible to ensure computational efficiency. The multi-language support system employs Unicode character encoding to ensure proper display of international characters across different platforms and devices.

The alert system utilizes TradingView's native alert functionality, providing users with flexible notification options including email, SMS, and webhook integrations. The alert messages include comprehensive statistical information to support informed decision-making.

The model's visualization system employs professional color schemes designed for optimal readability across different chart backgrounds and display devices. The system includes dynamic color transitions based on momentum and volatility, professional glow effects for enhanced line visibility, and transparency controls that allow users to customize the visual intensity to match their preferences and analytical requirements. The clean confidence band implementation provides clear statistical boundaries without visual distractions, maintaining focus on the analytical content.

Synthetic Point & Figure on RSIHere is a detailed description and user guide for the Synthetic Point & Figure RSI indicator, including how to use it for long and short trade considerations:

*

## Synthetic Point & Figure RSI Indicator – User Guide

### What It Is

This indicator applies classic Point & Figure (P&F) charting logic to the Relative Strength Index (RSI) instead of price. It transforms the RSI into synthetic “P&F candles” that filter out noise and highlight significant momentum moves and reversals based on configurable box size and reversal settings.

### How It Works

- The RSI is calculated normally over the selected length.

- The P&F engine tracks movements in the RSI above or below a defined “box size,” creating columns that switch direction only after a larger reversal.

- The synthetic candles connect these filtered RSI values visually, reducing false noise and emphasizing strong RSI trends.

- Optional EMA and SMA overlays on the synthetic P&F RSI allow smoother trend signals.

- Reference RSI levels at 33, 40, 50, 60, and 66 provide further context for momentum strength.

### How to Use for Trading

#### Long (Buy) Considerations

- The synthetic P&F RSI candle direction flips to *up (green candles)* indicating strength in momentum.

- Look for the RSI P&F value moving above the *40 or 50 level*, suggesting increasing bullish momentum.

- Confirmation is stronger if the synthetic RSI is above the EMA or SMA overlays.

- Ideal entries are after a reversal from a synthetic P&F downtrend (red candles) to an uptrend (green candles) near or above these levels.

#### Short (Sell) Considerations

- The candle direction flips to *down (red candles)*, showing weakening momentum or bearish reversal.

- Monitor if the synthetic RSI falls below the *60 or 50 level*, signaling momentum loss.

- Confirm bearish bias if the price is below the EMA or SMA overlays.

- Exit or short positions are signaled when the synthetic candle reverses from green to red near or below these threshold levels.

### Important RSI Levels to Watch

- *Level 33*: Lower bound indicating deep oversold conditions.

- *Level 40*: Early bullish zone suggesting momentum improvement.

- *Level 50*: Neutral midpoint; crossing above often signals bullish strength, below signals weakness.

- *Level 60*: Advanced bullish momentum; breaking below signals potential reversal.

- *Level 66*: Strong overbought area warning of possible pullback.

### Tips

- Use in conjunction with price action analysis and other volume/trend indicators for higher conviction.

- Adjust box size and reversal settings based on instrument volatility and timeframe for ideal filtering.

- The P&F RSI is best for identifying sustained momentum trends and avoiding false RSI whipsaws.

- Combine this indicator’s signals with stop-loss and risk management strategies.

*

This indicator converts RSI momentum analysis into a simplified, noise-filtered P&F chart format, helping traders better visualize and trade momentum shifts. It is especially useful when RSI signal noise can cause confusion in volatile markets.

Let me know if you want me to generate a shorter summary or code alerts based on these levels!

Sources

Relative Strength Index (RSI) — Indicators and Strategies in.tradingview.com

Indicators and strategies in.tradingview.com

Relative Strength Index (RSI) Indicator: Tutorial www.youtube.com

Stochastic RSI (STOCH RSI) in.tradingview.com

RSI Strategy docs.algotest.in

Stochastic RSI Indicator: Tutorial www.youtube.com

Relative Strength Index (RSI): What It Is, How It Works, and ... www.investopedia.com

rsi — Indicators and Strategies in.tradingview.com

Relative Strength Index (RSI) in.tradingview.com

Relative Strength Index (RSI) — Indicators and Strategies www.tradingview.com

% of Average Volume% of Average Volume (RVOL)

What it is

This indicator measures cumulative volume during pre market and separately during the first 10 minutes of trading and compares it to the average 30 day volume. This matters as a high ratio of volume within the premarket and then during the first 10 minutes of trading can correlate to a stock that has a higher probability of trending in that direction throughout the day.

What it’s meant to do

Identify abnormally high or low participation early in the day.

Normalize volume by time of session, so 9:40 volume is compared to past 9:40 volume—not to the full-day total.

Provide consistent RVOL across 1–5–15–60 minute charts (the same market state yields similar readings).

Handle pre-market cleanly (optional) without inflating RVOL.

How it works (plain English)

Cumulative Intraday Volume: Adds up all bars from the session (or pre-market, if enabled) up to “now.”

Time-Matched Baseline: For each prior day in your lookback, it accumulates only up to the same intraday minute and averages those values.

RVOL %: RVOL = (Today cumulative / Average cumulative at same time) × 100.

This “like-for-like” approach prevents the classic mistakes that overstate RVOL in pre-market or make it drift with timeframe changes.

Works best on

Intraday charts: 1, 2, 3, 4, 5, 10, 15, 30, 45, 60 min

Regular & extended hours: NYSE/Nasdaq equities, futures, ETFs

Daily/weekly views are supported for reference, but the edge comes from intraday time-matched analysis.

Tip: For thin names or very early pre-market, expect more variability—lower liquidity increases noise.

Customization (Inputs → Settings)

Lookback Sessions (e.g., 20): How many prior trading days to build the average.

Include Pre-Market (on/off): If on, RVOL accumulates from pre-market start and compares to historical pre-market at the same time; if off, it begins at the regular session open only.

Session Timezone / Exchange Hours: Choose the session definition that matches your market (e.g., NYSE) so “time-matched” means the same thing every day.

Cutoff Minute (Optional): Fix a reference minute (e.g., 6:40 a.m. PT / 9:40 a.m. ET) to evaluate RVOL at a standard check-in time.

Smoothing (Optional): Apply a short moving average to the RVOL line to reduce jitter.

Thresholds & Colors: Set levels (e.g., 150%, 300%) to color the plot/labels and trigger alerts.

Show Labels/Debug: Toggle on-chart labels (current RVOL%, baseline vols) for quick audits.

On-chart visuals & alerts

RVOL% Line/Histogram: Color-coded by thresholds (e.g., >300% “exceptional”, >150% “elevated”).

Session Markers: Optional vertical lines for pre-market/regular open.

Alerts:

RVOL Crosses Above X% (e.g., 150%, 300%)

RVOL Crosses Below X%

RVOL Rising/Falling (slope-based, optional)

Good defaults to start

Lookback: 20 sessions

Pre-market: Off for large caps, On for momentum screens

Thresholds: 150% (notable), 300% (exceptional)

Smoothing: 0–3 bars (or off for fastest response)

Notes & best practices

Timeframe consistency: Because calculations are time-matched, RVOL should remain directionally consistent across intraday timeframes. If you see divergences, confirm your session hours & timezone match your instrument’s exchange.

Holiday/half days: These are included in history; you can shorten lookback or exclude such sessions if your workflow prefers.

Low-float names: Consider a slightly longer lookback to reduce outlier effects.

TL;DR

A time-matched RVOL that treats pre-market correctly, stays stable across intraday timeframes, and is fully customizable for your exchange hours, thresholds, and alerts—so you can spot real participation when it matters.

S&P 500 Weighted Advance Decline LineS&P 500 Weighted Advance Decline Line Indicator

Overview

This indicator creates a market cap weighted advance/decline line for the S&P 500 that tracks breadth based on actual index weights rather than treating all stocks equally. By weighting each stock's contribution according to its true S&P 500 impact, it provides more accurate market breadth analysis and better insights into underlying market strength and potential turning points.

Key Features

Market Cap Weighted: Each stock contributes based on its actual S&P 500 weight

Top 40 Stocks: Covers ~51% of the index with the largest companies

(limited by TradingView's 40 security call maximum for Premium accounts)

Real-Time Updates: Cumulative line shows long-term breadth trends

Visual Indicators: Background coloring, moving average option, and data table

Stock Coverage

Sector Breakdown:

Technology (29.8%) - Dominates the coverage as expected

Financials (5.8%) - Major banking and payment companies

Consumer/Retail (3.7%) - Consumer staples and retail giants

Healthcare (3.2%) - Pharma and healthcare services

Communication (1.97%) - Telecom and tech services

Energy (1.35%) - Oil and gas majors

Industrial (0.9%) - Aerospace and industrial equipment

Other Sectors (4.6%) - Miscellaneous including software and payments

Includes the 40 largest S&P 500 companies by weight, featuring:

Tech Leaders (29.8%): AAPL (7.0%), MSFT (6.5%), NVDA (4.5%), AMZN (3.5%), META (2.5%), GOOGL/GOOG (3.8%), AVGO (1.5%), ORCL (1.22%), AMD (0.51%), plus others

Financials (5.8%): BRK.B (1.8%), JPM (1.2%), V (1.0%), MA (0.8%), BAC (0.63%), WFC (0.46%)

Healthcare (3.2%): LLY (1.2%), UNH (1.2%), JNJ (1.1%), ABBV (0.8%), PG (0.9%)

Consumer/Retail (3.7%): WMT (0.8%), HD (0.8%), COST (0.7%), KO (0.6%), PEP (0.6%), NKE (0.4%)

Communication (1.97%): TMUS (0.47%), CSCO (0.47%), DIS (0.5%), CRM (0.5%)

Energy** (1.35%): XOM (0.8%), CVX (0.55%)

Industrial** (0.9%): GE (0.5%), BA (0.4%)

Other Sectors (4.6%): PLTR (0.65%), ADBE (0.6%), PYPL (0.3%), plus others

How to Interpret

Trend Signals

Rising A/D Line: Broad market strength, more weighted buying than selling

Falling A/D Line: Market weakness, more weighted selling pressure

Flat A/D Line: Balanced market conditions

Divergence Analysis

Bullish Divergence: S&P 500 makes new lows but A/D Line holds higher

Bearish Divergence: S&P 500 makes new highs but A/D Line fails to confirm

Confirmation

Strong trends occur when both price and A/D Line move in the same direction

Weak trends show when price moves but breadth doesn't follow

Settings

Lookback Period: Days for advance/decline comparison (default: 1)

Show Moving Average: Optional trend smoothing

MA Length: Moving average period (default: 20)

Limitations

Covers ~51% of S&P 500 (not complete market breadth)

Optimized for TradingView Premium accounts (40 security limit)

Heavy weighting toward mega-cap technology stocks

Dependent on real-time data quality

Cardwell RSI by TQ📌 Cardwell RSI – Enhanced Relative Strength Index

This indicator is based on Andrew Cardwell’s RSI methodology , extending the classic RSI with tools to better identify bullish/bearish ranges and trend dynamics.

In uptrends, RSI tends to hold between 40–80 (Cardwell bullish range).

In downtrends, RSI tends to stay between 20–60 (Cardwell bearish range).

Key Features :

Standard RSI with configurable length & source

Fast (9) & Slow (45) RSI Moving Averages (toggleable)

Cardwell Core Levels (80 / 60 / 40 / 20) – enabled by default

Base Bands (70 / 50 / 30) in dotted style

Optional custom levels (up to 3)

Alerts for MA crosses and level crosses

Data Window metrics: RSI vs Fast/Slow MA differences

How to Use :

Monitor RSI behavior inside Cardwell’s bullish (40–80) and bearish (20–60) ranges

Watch RSI crossovers with Fast (9) and Slow (45) MAs to confirm momentum or trend shifts

Use levels and alerts as confluence with your trading strategy

Default Settings :

RSI Length: 14

MA Type: WMA

Fast MA: 9 (hidden by default)

Slow MA: 45 (hidden by default)

Cardwell Levels (80/60/40/20): ON

Base Bands (70/50/30): ON

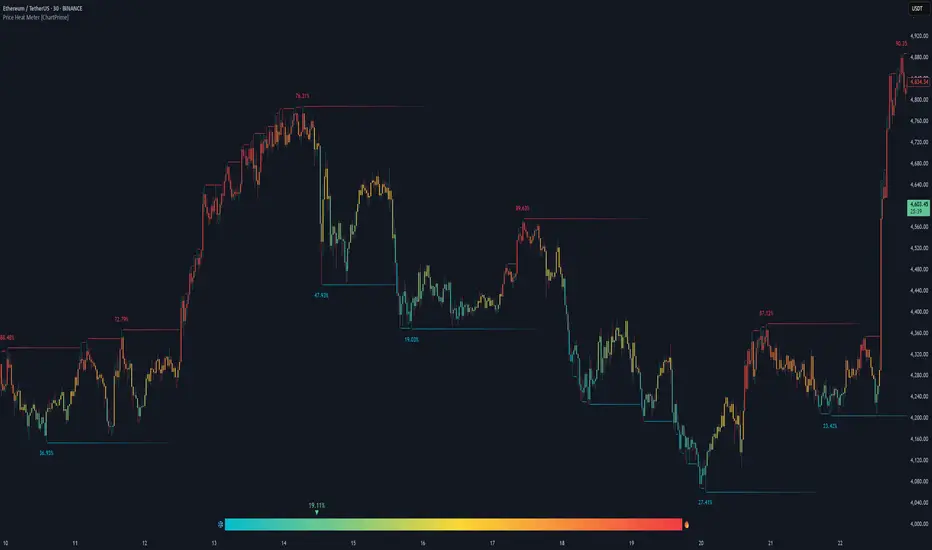

Price Heat Meter [ChartPrime]⯁ OVERVIEW

Price Heat Meter visualizes where price sits inside its recent range and turns that into an intuitive “temperature” read. Using rolling extremes, candles fade from ❄️ aqua (cold) near the lower bound to 🔥 red (hot) near the upper bound. The tool also trails recent extreme levels, tags unusually persistent extremes with a % “heat” label, and shows a bottom gauge (0–100%) with a live arrow so you can read market heat at a glance.

⯁ KEY FEATURES

Rolling Heat Map (0–100%):

The script measures where the close sits between the current Lowest Low and Highest High over the chosen Length (default 50).

Candles use a two-stage gradient: aqua → yellow (0–50%), then yellow → red (50–100%). This makes “how stretched are we?” instantly visible.

Dynamic Extremes with Time Decay:

When a new rolling High or Low is set, the script starts a faint horizontal trail at that price. Each bar that passes without a new extreme increases a counter; the line’s color gradually fades over time and fully disappears after ~100 bars, keeping the chart clean.

Persistent-Extreme Tags (Reversal Hints):

If an extreme persists for 40 bars (i.e., price hasn’t reclaimed or surpassed it), the tool stamps the original extreme pivot with its recorded Heat% at the moment the extreme formed.

• Upper extremes print a red % label (possible exhaustion/resistance context).

• Lower extremes print an aqua % label (possible exhaustion/support context).

Bottom Heat Gauge (0–100% Scale):

A compact, gradient bar renders at the bottom center showing the current Heat% with an arrow/label. ❄️ anchors the left (0%), 🔥 anchors the right (100%). The arrow adopts the same candle heat color for consistency.

Minimal Inputs, Clear Theme:

• Length (lookback window for H/L)

• Heat Color set (Cold / Mid / Hot)

The defaults give a balanced, legible gradient on most assets/timeframes.

Signal Hygiene by Design:

The meter doesn’t “call” reversals. Instead, it contextualizes price within its range and highlights the aging of extremes. That keeps it robust across regimes and assets, and ideal as a confluence layer with your existing triggers.

⯁ HOW IT WORKS (UNDER THE HOOD)

Range Model:

H = Highest(High, Length), L = Lowest(Low, Length). Heat% = 100 × (Close − L) / (H − L).

Extreme Tracking & Fade:

When High == H , we record/update the current upper extreme; same for Low == L on the lower side. If the extreme doesn’t change on the next bar, a counter increments and the plotted line’s opacity shifts along a 0→100 fade scale (visual decay).

40-Bar Persistence Labels:

On the bar after the extreme forms, the code stores the bar_index and the contemporaneous Heat% . If the extreme survives 40 bars, it places a % label at the original pivot price and index—flagging levels that were meaningfully “tested by time.”

Unified Color Logic:

Both candles and the gauge use the same two-stage gradient (Cold→Mid, then Mid→Hot), so your eye reads “heat” consistently across all elements.

⯁ USAGE

Treat >80% as “hot” and <20% as “cold” context; combine with your trigger (e.g., structure, OB, div, breakouts) instead of acting on heat alone.

Watch persistent extreme labels (40-bar marks) as reference zones for reaction or liquidity grabs.

Use the fading extreme lines as a memory map of where price last stretched—levels that slowly matter less as they decay.

Tighten Length for intraday sensitivity or increase it for swing stability.

⯁ WHY IT’S UNIQUE

Rather than another oscillator, Price Heat Meter translates simple market geometry (rolling extremes) into a readable temperature layer with time-aware extremes and a synchronized gauge . You get a continuously updated sense of stretch, persistence, and potential reversal context—without clutter or overfitting.

VWAP For Loop [BackQuant]VWAP For Loop

What this tool does—in one sentence

A volume-weighted trend gauge that anchors VWAP to a calendar period (day/week/month/quarter/year) and then scores the persistence of that VWAP trend with a simple for-loop “breadth” count; the result is a clean, threshold-driven oscillator plus an optional VWAP overlay and alerts.

Plain-English overview

Instead of judging raw price alone, this indicator focuses on anchored VWAP —the market’s average price paid during your chosen institutional period. It then asks a simple question across a configurable set of lookback steps: “Is the current anchored VWAP higher than it was i bars ago—or lower?” Each “yes” adds +1, each “no” adds −1. Summing those answers creates a score that reflects how consistently the volume-weighted trend has been rising or falling. Extreme positive scores imply persistent, broad strength; deeply negative scores imply persistent weakness. Crossing predefined thresholds produces objective long/short events and color-coded context.

Under the hood

• Anchoring — VWAP using hlc3 × volume resets exactly when the selected period rolls:

Day → session change, Week → new week, Month → new month, Quarter/Year → calendar quarter/year.

• For-loop scoring — For lag steps i = , compare today’s VWAP to VWAP .

– If VWAP > VWAP , add +1.

– Else, add −1.

The final score ∈ , where N = (end − start + 1). With defaults (1→45), N = 45.

• Signal logic (stateful)

– Long when score > upper (e.g., > 40 with N = 45 → VWAP higher than ~89% of checked lags).

– Short on crossunder of lower (e.g., dropping below −10).

– A compact state variable ( out ) holds the current regime: +1 (long), −1 (short), otherwise unchanged. This “stickiness” avoids constant flipping between bars without sufficient evidence.

Why VWAP + a breadth score?

• VWAP aggregates both price and volume—where participants actually traded.

• The breadth-style count rewards consistency of the anchored trend, not one-off spikes.

• Thresholds give you binary structure when you need it (alerts, automation), without complex math.

What you’ll see on the chart

• Sub-pane oscillator — The for-loop score line, colored by regime (long/short/neutral).

• Main-pane VWAP (optional) — Even though the indicator runs off-chart, the anchored VWAP can be overlaid on price (toggle visibility and whether it inherits trend colors).

• Threshold guides — Horizontal lines for the long/short bands (toggle).

• Cosmetics — Optional candle painting and background shading by regime; adjustable line width and colors.

Input map (quick reference)

• VWAP Anchor Period — Day, Week, Month, Quarter, Year.

• Calculation Start/End — The for-loop lag window . With 1→45, you evaluate 45 comparisons.

• Long/Short Thresholds — Default upper=40, lower=−10 (asymmetric by design; see below).

• UI/Style — Show thresholds, paint candles, background color, line width, VWAP visibility and coloring, custom long/short colors.

Interpreting the score

• Near +N — Current anchored VWAP is above most historical VWAP checkpoints in the window → entrenched strength.

• Near −N — Current anchored VWAP is below most checkpoints → entrenched weakness.

• Between — Mixed, choppy, or transitioning regimes; use thresholds to avoid reacting to noise.

Why the asymmetric default thresholds?

• Long = score > upper (40) — Demands unusually broad upside persistence before declaring “long regime.”

• Short = crossunder lower (−10) — Triggers only on downward momentum events (a fresh breach), not merely being below −10. This combination tends to:

– Capture sustained uptrends only when they’re very strong.

– Flag downside turns as they occur, rather than waiting for an extreme negative breadth.

Tuning guide

Choose an anchor that matches your horizon

– Intraday scalps : Day anchor on intraday charts.

– Swing/position : Month or Quarter anchor on 1h/4h/D charts to capture institutional cycles.

Pick the for-loop window

– Larger N (bigger end) = stronger evidence requirement, smoother oscillator.

– Smaller N = faster, more reactive score.

Set achievable thresholds

– Ensure upper ≤ N and lower ≥ −N ; if N=30, an upper of 40 can never trigger.