[blackcat] L2 Ehlers HP-LP Roofing FilterLevel: 2

Background

John F. Ehlers introuced HP-LP Roofing Filter in his "Cycle Analytics for Traders" chapter 7 on 2013.

Function

A “roofing filter” can be used to limit the frequency content of an input before proceeding to construct an indicator. The roofing filter is composed of a highpass filter that passes only frequency components whose periods are shorter than 48 bars, for example. It also is composed of a SuperSmoother filter that passes frequency components whose periods are longer than 10 bars. Thus, the roofing filter is a wide bandwidth band-pass filter that passes only frequency components whose periods fall between 10 bars and 48 bars. This, by itself, is a simple indicator.

While the roofing filter indicator wiggles in proportion to the wiggles in the price data as you would expect, it is noticeable that the indicator is above zero for extended periods where the market is in an uptrend. In other words, the filter output does not have a zero mean as you would expect if the output consisted only of cyclic components whose periods fall between 10 bars and 48 bars.

Key Signal

Filt --> HP-LP Roofing Filter fast line

Trigger --> HP-LP Roofing Filter slow line

Pros and Cons

100% John F. Ehlers definition translation of original work, even variable names are the same. This help readers who would like to use pine to read his book. If you had read his works, then you will be quite familiar with my code style.

Remarks

The 41th script for Blackcat1402 John F. Ehlers Week publication.

Readme

In real life, I am a prolific inventor. I have successfully applied for more than 60 international and regional patents in the past 12 years. But in the past two years or so, I have tried to transfer my creativity to the development of trading strategies. Tradingview is the ideal platform for me. I am selecting and contributing some of the hundreds of scripts to publish in Tradingview community. Welcome everyone to interact with me to discuss these interesting pine scripts.

The scripts posted are categorized into 5 levels according to my efforts or manhours put into these works.

Level 1 : interesting script snippets or distinctive improvement from classic indicators or strategy. Level 1 scripts can usually appear in more complex indicators as a function module or element.

Level 2 : composite indicator/strategy. By selecting or combining several independent or dependent functions or sub indicators in proper way, the composite script exhibits a resonance phenomenon which can filter out noise or fake trading signal to enhance trading confidence level.

Level 3 : comprehensive indicator/strategy. They are simple trading systems based on my strategies. They are commonly containing several or all of entry signal, close signal, stop loss, take profit, re-entry, risk management, and position sizing techniques. Even some interesting fundamental and mass psychological aspects are incorporated.

Level 4 : script snippets or functions that do not disclose source code. Interesting element that can reveal market laws and work as raw material for indicators and strategies. If you find Level 1~2 scripts are helpful, Level 4 is a private version that took me far more efforts to develop.

Level 5 : indicator/strategy that do not disclose source code. private version of Level 3 script with my accumulated script processing skills or a large number of custom functions. I had a private function library built in past two years. Level 5 scripts use many of them to achieve private trading strategy.

在脚本中搜索"美国财长:10年期美债收益率"

Fibonacci-Trading-Indikator_3Daily (weekly, monthly) profits with the Fibonacci trading indicator_3

Quotes move in Fibonacci ratios in liquid markets. With this indicator you receive information for daily trades or for position trades based on a week or on a monthly basis, in which area you should ideally enter the market and where the minimum achievable price target is. This price target is 61.8% of yesterday's trading range, or the trading range of the previous week, or the trading range of the previous month, depending on the time frame for which the indicator should calculate the minimum achievable high / low. This is also where you realize your profit.

For this calculation, the following entries must be made in the properties window of the indicator:

• Preselection uptrend / downtrend.

• Time frame (day, week, ...) of the price bar for the possible high / low to be determined.

• Trading range of the previous day, or the previous week, or the previous month.

• Current lowest low of the selected time frame when trading has started and prices are rising.

• Current highest high of the selected time frame when trading has started and prices are falling.

Important areas for trading are:

• The entry range 0% - 23.6% for long or short.

• The target price level 61.8%.

Choose a suitable time frame to detect the direction of movement while the quotes are still moving in the entry area. The camelback indicator can be of great help. Also test the resolution setting of the camelback indicator. With a resolution of 1 hour in the 6 or 12 minute chart, you get a perspective for the broader direction. Movement patterns of corrections or consolidations, if they last more than a day or a week, also give clues to the coming direction of movement for the trade. So look back to see what happened yesterday, a week ago, or a month ago. Pay attention to the market anatomy, find out how the market works, count the price bars in consolidations and trends.

After entering the values the indicator will show the Fibonacci expansion price levels for the possible high or low for the selected time frame. Buy / sell within the entry range between 0% and 23.6% as the market moves towards the last long / or short entry point. This is the course range up to the 23.6% course level. The 61.8% price level is the minimum expected price target. We assume that the current bar will reach at least 61.8% of the trading range of the previous day, week or month. Depending on the set time frame. You should therefore realize the profits you have made with 50% of the position when the prices have reached the 61.8% level. With a suitable trailing stop you can be stopped with the rest of the position, but do not risk more than 50% of the profits.

With the quarter or year preselection and the corresponding entries, the minimum expected quarterly high / quarterly low or annual high / annual low can be determined.

The Fibonacci price levels can be shown and hidden. In the chart click on the gear wheel for “Chart Settings”. In the “Scaling” menu, the price levels can be displayed with the preselection “Label for indicator names” and “Label for last indicator value”. Slide the chart to the right to find possible support and resistance at the price levels that could provide confirmation of the target.

In the event of input errors or missing entries for a time frame, the indicator is hidden.

Pay attention to your trade management to avoid losses.

The new Fibonacci Trading Indicator_3 has the following additions and changes:

Area code for the quarter time frame has been added.

The entry area received a 23.6% and a 50% subdivision. Two envelope lines above the 23.6% entry level in the case of an upward trend and below the 23.6% entry level in the case of a downtrend, with a width of 23.6% and 14.6% of the entry level, are intended to indicate that the closing price is higher the quotations have broken out of the entry-level area.

A volatility stop for upward and downward trends can be activated.

A factor is added to the fluctuation range of each price bar for the stop. Then a moving average is calculated with an adjustable period. The period setting should be set between 5 and 10. The result can be smoothed adjustable.

Presetting:

Periods = 10

Factor = 1.4

Smoothing = 7

With the assumption that the market entry in an upward trend occurs when the prices break out above a bar high, the result of the stop calculation is subtracted from the bar high. In the case of a downward trend, the result of the stop calculation is added to the price bar low.

When entering the market, set the factor to 2.4. If inside bars follow a trend movement, the stop should be brought closer. Try the factor setting 0.4 or less. The smallest adjustable factor is 0.1.

For the entry into an established trend, as described in an idea contribution by me, there are two switchable moving averages. The application for the (MA_H) takes place on high and for the (MA_L) adjustable on high, low, shot, h + 1/2 etc. Period and offset (shift) are adjustable. With this idea, the entry into the market occurs between a 618% correction (the Fibonacci entry point) and the DEP (average entry point). The DEP in this case is the MA_H with period = 4 and an offset = 1 in the case of a downward trend, or the MA_L with the same setting and application to lows in an upward trend.

Also test the MA_L in trends with the settings (period, offset) 3.3 or 5, 3 or 7.5 and applying it to closing prices for a close encompassing of the highs / lows.

Tägliche (wöchentliche, monatliche) Gewinne mit dem Fibonacci-Trading Indikator_3

Kursnotierungen bewegen sich in liquiden Märkten in Fibonacci-Verhältnisse. Mit diesem Indikator erhalten Sie für Tagesgeschäfte, oder für Positionstrades auf Basis einer Woche, oder auf Basis eines Monats Informationen, in welchem Bereich Sie idealerweise in den Markt einsteigen sollten und wo das mindeste erreichbare Kursziel liegt. Dieses Kursziel liegt bei 61,8% der gestrigen Handelspanne, oder der Handelspanne der Vorwoche, oder der Handelspanne des Vormonats, also abhängig davon für welchen Zeitrahmen der Indikator das mindeste erreichbare Hoch/Tief berechnen soll. Dort realisieren Sie auch Ihren Gewinn.

Für diese Berechnung sind folgende Eingaben im Eigenschaftenfenster des Indikators einzustellen:

• Vorwahl Aufwärtstrend/ Abwärtstrend.

• Zeitrahmen (Tag, Woche, …) des Kursbalkens für das zu ermittelnde mögliche Hoch/ Tief.

• Handelspanne des vorherigen Tages, oder der vorherigen Woche, oder des vorherigen Monats.

• Aktuell tiefstes Tief des vorgewählten Zeitrahmens, wenn der Handel begonnen hat und die Notierungen steigen.

• Aktuell höchstes Hoch des vorgewählten Zeitrahmens, wenn der Handel begonnen hat und die Notierungen fallen.

Wichtige Bereiche für das Trading sind:

• Der Einstiegsbereich 0% - 23,6% für long oder short.

• Der Kursziellevel 61,8%.

Wählen Sie für die Erkennung der Bewegungsrichtung einen geeigneten Zeitrahmen, während sich die Notierungen noch im Einstiegsbereich bewegen. Der Camelback-Indikator kann eine gute Hilfe sein. Testen Sie auch die Auflösung-Einstellung des Camelback-Indikators. Mit der Auflösung 1 Stunde Im 6- oder 12 Minuten-Chart erhalten Sie einen Blickwinkel für die große Richtung. Auch Bewegungsmuster von Korrekturen oder Konsolidierungen, wenn sie mehr als einen Tag oder eine Woche andauern geben Hinweise auf die kommende Bewegungsrichtung für den Trade. Schauen Sie also zurück um zu prüfen, was sich gestern, vor einer Woche oder vor einem Monat abgespielt hat. Achten sie auf die Marktanatomie, finden Sie heraus wie der Markt funktioniert, zählen Sie Kursstäbe in Konsolidierungen und Trends.

Nach Eingabe der Werte zeigt der Indikator die Fibonacci-Ausweitungskurslevels für das mögliche Hoch oder Tief für den ausgewählten Zeitrahmen. Kaufen/ verkaufen Sie innerhalb des Einstiegsbereichs zwischen 0% und 23,6%, während sich der Markt in Richtung des letzten long-/ oder short-Einstiegspunktes bewegt. Das ist der Kursbereich bis zum 23,6%- Kurslevel. Der 61,8%-Kurslevel ist das mindeste erwartbare Kursziel. Wir gehen davon aus, dass der aktuelle Kursbalken mindestens 61,8% der Handelsspanne des vorherigen Tages, der vorherigen Woche oder des vorherigen Monats erreichen wird. Abhängig vom eingestellten Zeitrahmen. Realisieren Sie deshalb die angelaufenen Gewinne mit 50% der Position, wenn die Notierungen den 61,8% - Level erreicht haben. Mit einem geeigneten Trailing-Stopp lassen Sie sich mit der restlichen Position ausstoppen, riskieren Sie dafür aber nicht mehr als 50 % der angelaufenen Gewinne.

Mit der Vorwahl Quartal oder Jahr und den entsprechenden Eingaben kann auch das mindeste erwartbare Quartalshoch/ Quartalstief bzw. Jahreshoch/ Jahrestief ermittelt werden.

Die Fibonacci-Kurslevels lassen sich ein- und ausblenden. Klicken Sie im Chart auf das Zahnrad für „Chart Einstellungen“. Im Menü „Skalierungen“ kann mit der Vorwahl „Label für Indikatornahmen“ und „Label für letzten Indikatorwert“ die Kurslevels angezeigt werden. Schieben Sie den Chart nach rechts um mögliche Unterstützungen und Widerstände an den Kurslevels zu finden, die Bestätigung für das Ziel geben könnten.

Bei Eingabefehlern oder fehlenden Eingaben zu einem Zeitrahmen wird der Indikator ausgeblendet.

Achten Sie zur Vermeidung von Verlusten auf ihr Handelsmanagement.

Der neue Fibonacci-Trading-Indikator_3 besitz folgende Zusätze und Änderungen:

Vorwahl für den Zeitrahmen Quartal wurde hinzugefügt.

Der Einstiegsbereich erhielt eine 23,6% und eine 50% Unterteilung. Zwei Umschlagslinien über dem 23,6%-Einstiegslevel bei einem Aufwärtstrend, bzw. unter dem 23,6%-Einstiegslevel bei einem Abwärtstrend, mit der Breite 23,6% und 14,6% vom Einstiegsbereich, sollen bei höherem Schlusskurs signalisieren, dass die Notierungen aus dem Einstiegsbereich ausgebrochen sind.

Ein Volatilitätsstopp jeweils für Aufwärts- und Abwärtstrend kann zugeschaltet werden.

Für den Stopp wird die Schwankungsbreite jedes Kursbalkens wird mit einem Faktor beaufschlagt. Danach erfolgt die Berechnung eines gleitenden Durchschnitts mit einstellbarer Periode. Die Periodeneinstellung sollte zwischen 5 und 10 eingestellt werden. Das Ergebnis kann einstellbar geglättet werden.

Voreinstellung:

Perioden = 10

Faktor = 1,4

Glättung = 7

Mit der Annahme, dass der Markteinstieg in einem Aufwärtstrend bei Ausbruch der Notierungen über ein Kursbalkenhoch erfolgt, wird das Ergebnis der Stoppberechnung vom Kursbalkenhoch subtrahiert. Bei einem Abwärtstrend wird das Ergebnis der Stoppberechnung zum Kursbalkentief addiert.

Stellen Sie bei Markteintritt den Faktor auf 2,4. Folgen nach einer Trendbewegung Innenstäbe sollte der Stopp näher herangeführt werden. Probieren Sie die Faktoreinstellung 0,4 oder kleiner. Der kleinste einstellbare Faktor ist 0,1.

Für den Einstieg in einen etablierten Trend, wie in einem Ideenbeitrag von mir beschrieben, gibt es zwei zuschaltbare gleitende Durchschnitte. Die Anwendung für den (MA_H) erfolgt auf Hochs und für den (MA_L) einstellbar auf Hoch, Tief, Schuss, h+l/2 usw.. Periode und Offset (Verschiebung) sind einstellbar. Bei dieser Idee erfolgt der Einstieg in den Markt zwischen einer 618%-Korrektur (dem Fibonacci-Einstiegspunkt) und dem DEP (Durchschnittlicher Einstiegspunkt). Der DEP ist in diesem Fall der MA_H mit Periode = 4 und einem Offset = 1, bei einem Abwärtstrend, oder der MA_L mit identischer Einstellung und Anwendung auf Tiefs in einem Aufwärtstrend.

Testen Sie den MA_L auch in Trends mit den Einstellungen (Periode, Offset) 3,3 oder 5, 3 oder 7,5 und Anwendung auf Schlusskurse für eine enge Umfassung der Hochs/ Tiefs.

Polynomial Regression Bands + Channel [DW]This is an experimental study designed to calculate polynomial regression for any order polynomial that TV is able to support.

This study aims to educate users on polynomial curve fitting, and the derivation process of Least Squares Moving Averages (LSMAs).

I also designed this study with the intent of showcasing some of the capabilities and potential applications of TV's fantastic new array functions.

Polynomial regression is a form of regression analysis in which the relationship between the independent variable x and the dependent variable y is modeled as a polynomial of nth degree (order).

For clarification, linear regression can also be described as a first order polynomial regression. The process of deriving linear, quadratic, cubic, and higher order polynomial relationships is all the same.

In addition, although deriving a polynomial regression equation results in a nonlinear output, the process of solving for polynomials by least squares is actually a special case of multiple linear regression.

So, just like in multiple linear regression, polynomial regression can be solved in essentially the same way through a system of linear equations.

In this study, you are first given the option to smooth the input data using the 2 pole Super Smoother Filter from John Ehlers.

I chose this specific filter because I find it provides superior smoothing with low lag and fairly clean cutoff. You can, of course, implement your own filter functions to see how they compare if you feel like experimenting.

Filtering noise prior to regression calculation can be useful for providing a more stable estimation since least squares regression can be rather sensitive to noise.

This is especially true on lower sampling lengths and higher degree polynomials since the regression output becomes more "overfit" to the sample data.

Next, data arrays are populated for the x-axis and y-axis values. These are the main datasets utilized in the rest of the calculations.

To keep the calculations more numerically stable for higher periods and orders, the x array is filled with integers 1 through the sampling period rather than using current bar numbers.

This process can be thought of as shifting the origin of the x-axis as new data emerges.

This keeps the axis values significantly lower than the 10k+ bar values, thus maintaining more numerical stability at higher orders and sample lengths.

The data arrays are then used to create a pseudo 2D matrix of x power sums, and a vector of x power*y sums.

These matrices are a representation the system of equations that need to be solved in order to find the regression coefficients.

Below, you'll see some examples of the pattern of equations used to solve for our coefficients represented in augmented matrix form.

For example, the augmented matrix for the system equations required to solve a second order (quadratic) polynomial regression by least squares is formed like this:

(∑x^0 ∑x^1 ∑x^2 | ∑(x^0)y)

(∑x^1 ∑x^2 ∑x^3 | ∑(x^1)y)

(∑x^2 ∑x^3 ∑x^4 | ∑(x^2)y)

The augmented matrix for the third order (cubic) system is formed like this:

(∑x^0 ∑x^1 ∑x^2 ∑x^3 | ∑(x^0)y)

(∑x^1 ∑x^2 ∑x^3 ∑x^4 | ∑(x^1)y)

(∑x^2 ∑x^3 ∑x^4 ∑x^5 | ∑(x^2)y)

(∑x^3 ∑x^4 ∑x^5 ∑x^6 | ∑(x^3)y)

This pattern continues for any n ordered polynomial regression, in which the coefficient matrix is a n + 1 wide square matrix with the last term being ∑x^2n, and the last term of the result vector being ∑(x^n)y.

Thanks to this pattern, it's rather convenient to solve the for our regression coefficients of any nth degree polynomial by a number of different methods.

In this script, I utilize a process known as LU Decomposition to solve for the regression coefficients.

Lower-upper (LU) Decomposition is a neat form of matrix manipulation that expresses a 2D matrix as the product of lower and upper triangular matrices.

This decomposition method is incredibly handy for solving systems of equations, calculating determinants, and inverting matrices.

For a linear system Ax=b, where A is our coefficient matrix, x is our vector of unknowns, and b is our vector of results, LU Decomposition turns our system into LUx=b.

We can then factor this into two separate matrix equations and solve the system using these two simple steps:

1. Solve Ly=b for y, where y is a new vector of unknowns that satisfies the equation, using forward substitution.

2. Solve Ux=y for x using backward substitution. This gives us the values of our original unknowns - in this case, the coefficients for our regression equation.

After solving for the regression coefficients, the values are then plugged into our regression equation:

Y = a0 + a1*x + a1*x^2 + ... + an*x^n, where a() is the ()th coefficient in ascending order and n is the polynomial degree.

From here, an array of curve values for the period based on the current equation is populated, and standard deviation is added to and subtracted from the equation to calculate the channel high and low levels.

The calculated curve values can also be shifted to the left or right using the "Regression Offset" input

Changing the offset parameter will move the curve left for negative values, and right for positive values.

This offset parameter shifts the curve points within our window while using the same equation, allowing you to use offset datapoints on the regression curve to calculate the LSMA and bands.

The curve and channel's appearance is optionally approximated using Pine's v4 line tools to draw segments.

Since there is a limitation on how many lines can be displayed per script, each curve consists of 10 segments with lengths determined by a user defined step size. In total, there are 30 lines displayed at once when active.

By default, the step size is 10, meaning each segment is 10 bars long. This is because the default sampling period is 100, so this step size will show the approximate curve for the entire period.

When adjusting your sampling period, be sure to adjust your step size accordingly when curve drawing is active if you want to see the full approximate curve for the period.

Note that when you have a larger step size, you will see more seemingly "sharp" turning points on the polynomial curve, especially on higher degree polynomials.

The polynomial functions that are calculated are continuous and differentiable across all points. The perceived sharpness is simply due to our limitation on available lines to draw them.

The approximate channel drawings also come equipped with style inputs, so you can control the type, color, and width of the regression, channel high, and channel low curves.

I also included an input to determine if the curves are updated continuously, or only upon the closing of a bar for reduced runtime demands. More about why this is important in the notes below.

For additional reference, I also included the option to display the current regression equation.

This allows you to easily track the polynomial function you're using, and to confirm that the polynomial is properly supported within Pine.

There are some cases that aren't supported properly due to Pine's limitations. More about this in the notes on the bottom.

In addition, I included a line of text beneath the equation to indicate how many bars left or right the calculated curve data is currently shifted.

The display label comes equipped with style editing inputs, so you can control the size, background color, and text color of the equation display.

The Polynomial LSMA, high band, and low band in this script are generated by tracking the current endpoints of the regression, channel high, and channel low curves respectively.

The output of these bands is similar in nature to Bollinger Bands, but with an obviously different derivation process.

By displaying the LSMA and bands in tandem with the polynomial channel, it's easy to visualize how LSMAs are derived, and how the process that goes into them is drastically different from a typical moving average.

The main difference between LSMA and other MAs is that LSMA is showing the value of the regression curve on the current bar, which is the result of a modelled relationship between x and the expected value of y.

With other MA / filter types, they are typically just averaging or frequency filtering the samples. This is an important distinction in interpretation. However, both can be applied similarly when trading.

An important distinction with the LSMA in this script is that since we can model higher degree polynomial relationships, the LSMA here is not limited to only linear as it is in TV's built in LSMA.

Bar colors are also included in this script. The color scheme is based on disparity between source and the LSMA.

This script is a great study for educating yourself on the process that goes into polynomial regression, as well as one of the many processes computers utilize to solve systems of equations.

Also, the Polynomial LSMA and bands are great components to try implementing into your own analysis setup.

I hope you all enjoy it!

--------------------------------------------------------

NOTES:

- Even though the algorithm used in this script can be implemented to find any order polynomial relationship, TV has a limit on the significant figures for its floating point outputs.

This means that as you increase your sampling period and / or polynomial order, some higher order coefficients will be output as 0 due to floating point round-off.

There is currently no viable workaround for this issue since there isn't a way to calculate more significant figures than the limit.

However, in my humble opinion, fitting a polynomial higher than cubic to most time series data is "overkill" due to bias-variance tradeoff.

Although, this tradeoff is also dependent on the sampling period. Keep that in mind. A good rule of thumb is to aim for a nice "middle ground" between bias and variance.

If TV ever chooses to expand its significant figure limits, then it will be possible to accurately calculate even higher order polynomials and periods if you feel the desire to do so.

To test if your polynomial is properly supported within Pine's constraints, check the equation label.

If you see a coefficient value of 0 in front of any of the x values, reduce your period and / or polynomial order.

- Although this algorithm has less computational complexity than most other linear system solving methods, this script itself can still be rather demanding on runtime resources - especially when drawing the curves.

In the event you find your current configuration is throwing back an error saying that the calculation takes too long, there are a few things you can try:

-> Refresh your chart or hide and unhide the indicator.

The runtime environment on TV is very dynamic and the allocation of available memory varies with collective server usage.

By refreshing, you can often get it to process since you're basically just waiting for your allotment to increase. This method works well in a lot of cases.

-> Change the curve update frequency to "Close Only".

If you've tried refreshing multiple times and still have the error, your configuration may simply be too demanding of resources.

v4 drawing objects, most notably lines, can be highly taxing on the servers. That's why Pine has a limit on how many can be displayed in the first place.

By limiting the curve updates to only bar closes, this will significantly reduce the runtime needs of the lines since they will only be calculated once per bar.

Note that doing this will only limit the visual output of the curve segments. It has no impact on regression calculation, equation display, or LSMA and band displays.

-> Uncheck the display boxes for the drawing objects.

If you still have troubles after trying the above options, then simply stop displaying the curve - unless it's important to you.

As I mentioned, v4 drawing objects can be rather resource intensive. So a simple fix that often works when other things fail is to just stop them from being displayed.

-> Reduce sampling period, polynomial order, or curve drawing step size.

If you're having runtime errors and don't want to sacrifice the curve drawings, then you'll need to reduce the calculation complexity.

If you're using a large sampling period, or high order polynomial, the operational complexity becomes significantly higher than lower periods and orders.

When you have larger step sizes, more historical referencing is used for x-axis locations, which does have an impact as well.

By reducing these parameters, the runtime issue will often be solved.

Another important detail to note with this is that you may have configurations that work just fine in real time, but struggle to load properly in replay mode.

This is because the replay framework also requires its own allotment of runtime, so that must be taken into consideration as well.

- Please note that the line and label objects are reprinted as new data emerges. That's simply the nature of drawing objects vs standard plots.

I do not recommend or endorse basing your trading decisions based on the drawn curve. That component is merely to serve as a visual reference of the current polynomial relationship.

No repainting occurs with the Polynomial LSMA and bands though. Once the bar is closed, that bar's calculated values are set.

So when using the LSMA and bands for trading purposes, you can rest easy knowing that history won't change on you when you come back to view them.

- For those who intend on utilizing or modifying the functions and calculations in this script for their own scripts, I included debug dialogues in the script for all of the arrays to make the process easier.

To use the debugs, see the "Debugs" section at the bottom. All dialogues are commented out by default.

The debugs are displayed using label objects. By default, I have them all located to the right of current price.

If you wish to display multiple debugs at once, it will be up to you to decide on display locations at your leisure.

When using the debugs, I recommend commenting out the other drawing objects (or even all plots) in the script to prevent runtime issues and overlapping displays.

[WJ] - Corrected Seconds Volume** ONLY WORKS FOR SECONDS CHARTS **

After staring at a chart and scratching my head, I realized that the volumes were being incorrectly reported for lower time frames.

A chart that has no updated tick for 5 minutes will report the volume that occurred in the WHOLE 5 minutes - in one tick.

For a 5 second chart like above, we have now a chart that at first appearance is giving us numbers to believe that there is MUCH more liquidity than is real.

This can really confuse us, and other scripts that rely on volume information.

This script simply takes into consideration the time delay before the next tick. If it took 5 minutes to update a tick, the volume should be divided into whatever seconds we are currently using. I also changed the coloring code - if there is no length to the candle it will look at the candle before it to determine if it is a positive or negative movement.

It does make technical sense to have the volume that occurred over 5 minutes in one tick as it is the true volume. However, this script should not be viewed as the absolute value, but a consistent, usable number that will be more accurate with tools.

To give a quick example on why this is important:

In a 10 second chart, we are given an updated tick every minute. In 2 minutes we have 2 ticks that have 1K volume each.

Alternatively, we have a 10 second chart, and we are given an updated tick every 10 seconds. In 2 minutes we have 12 ticks that have 100 volume each.

With quick mental math we can determine that the second scenario is actually (albeit slightly) more busy. However, a script would not do that extra layer of math and would assume that the first scenario is bouncing off the walls with activity and the second is a graveyard.

It's exactly for this example that I have created this script, and I hope it helps someone else out.

EulerMethod: V-ProfileVolume profile

50 rows | 50 рядов

Depth — Depth of history | Глубина истории

Range ± — Floating range | Плавающий диапазон

∟ % — Floating range % | Плавающий диапазон %

Amp — Amplitude of histogram | Амплитуда гистограммы

Minimum right margin: 10 bars | Минимальное правое поле: 10 баров

Supply and Demand ZonesThis indicators should be used along with price action breakout

Red zones - Red zones are formed daily

10 days average ranges

Blue zones - Blue zones are formed every week

10 weeks average ranges

Green zones - Green zones are formed every month

10 months averange ranges

CustomScreenerTo apply your indicator with screener , please modify the section which i mention "Start your indicator pine script" & "End your indicator pine script"

At the pinescript section you will able to change the ticket symbol .

I only able to show screener result with 10 item in 1 times . To view more result, please go to setting and change stock list "1-10">"11,20">"21-30".....

Able to screener 100 items with this indicator.

Kindly change the exchange and stock in the pinescript according your watchlist.

As examples, my indicator is to determine the stock in which trend, i want to find out all stock with aqua color trend

The screener result show only 9 of 10 are in aqua color trend.

Donchian Channel CloudsFor this indicator, I got inspired by this paragraph in an article on Investopedia:

"Donchian channels also make natural partners with another moving average indicator for a crossover strategy. The Donchian moving average middle line is likely to form the short-term average in these situations, although some have used a 20-day Donchian channel in conjunction with a five- or 10-day channel to exit a position before a consolidation eats into short-term profits."

The default is a 20-period Donchian channel with the middle line from a 10-period channel superimposed on it. Red for 20, green for 10. When 10 is over 20, the cloud between them is green; the cloud is red when 20 is over 10.

Stochastic RibbonA series of highs and lows of different lengths to create a ribbon-like indicator to emulate the stochastic oscillator's top (100), middle (50) and bottom (0). Traders can determine the strength of the support and resistance by the number of converging lines, choose price points and visualise momentum waves.

Inputs:

Theme: multiple colours/themes (theme 2)

Length: high/low length (14)

Start: plot number to start ribbon on (1)

PlotNumber: number of plots to show; maximum 10 per top, middle, bottom (10)

Example:

Length: 14

Start: 5

PlotNumber: 10

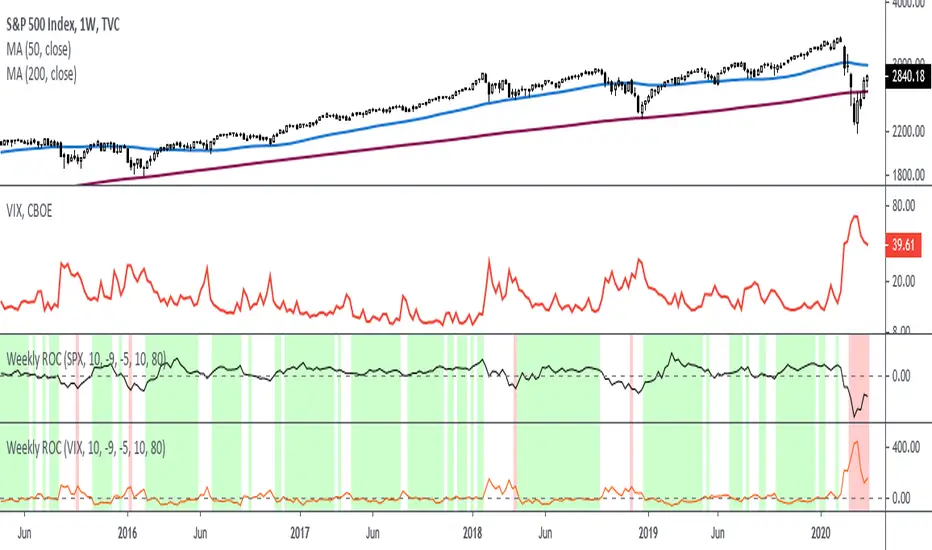

Rate Of Change - Weekly SignalsRate of Change - Weekly Signals

This indicator gives a potential "buy signal" using Rate of Change of SPX and VIX together,

using the following criteria:

SPX Weekly ROC(10) has been BELOW -9 and now rises ABOVE -5

*PLUS*

VIX Weekly ROC(10) has been ABOVE +80 and now falls BELOW +10

The background will turn RED when ROC(SPX) is below -9 and ROC(VIX) is above +80.

The background will turn GREEN when ROC(SPX) is above -5 and ROC(VIX) is below +10.

So the potential "buy signal" is when you start to get GREEN BARS AFTER RED - usually with

some white/empty bars in between...but wait for the green. This indicates that the volatility

has settled down, and the market is starting to turn up.

This indicator gives excellent entry points, but be careful of the occasional false signals.

See Nov. 2001 and Nov. 2008, in both cases the market dropped another 25-30% before the final

bottom was formed. Always have an exit strategy, especially when buying in after a downtrend.

How I use this indicator, pretty much as shown in the preview. Weekly SPX as the main chart with

some medium/long moving averages to identify the trend, VIX added as a "Compare Symbol" in red,

and then the Weekly ROC signals below.

For the ROC graphs, you can show SPX+VIX together, SPX alone, or VIX alone. I prefer to display

them separately because they don't scale well together (VIX crowds out the SPX when it spikes).

Background color is still based on both SPX/VIX together, regardless of which graph is shown.

Note that there is no VIX data available on Trading View prior to 1990, so for those dates the

formula is using only ROC(SPX) and the assigned thresholds (-9 and -5, or whatever you choose).

Price Swing IndicatorThis indicator shows you the highs and lows of the previous "X" amount of bars. This is an objective way of identifying previous price swings. For example, an input of "10" will show you the Swing High (SH) of the previous 10 bars and the Swing Low (SL) of the previous 10 bars. The higher the number, the higher number of bars included in the calculation. Therefore, the higher the number, the less "noise" taken into consideration. This means that higher input values will not take into consideration smaller retracements. Lower input values will take into account small retracements within larger movements.

Volume Profile [Makit0]VOLUME PROFILE INDICATOR v0.5 beta

Volume Profile is suitable for day and swing trading on stock and futures markets, is a volume based indicator that gives you 6 key values for each session: POC, VAH, VAL, profile HIGH, LOW and MID levels. This project was born on the idea of plotting the RTH sessions Value Areas for /ES in an automated way, but you can select between 3 different sessions: RTH, GLOBEX and FULL sessions.

Some basic concepts:

- Volume Profile calculates the total volume for the session at each price level and give us market generated information about what price and range of prices are the most traded (where the value is)

- Value Area (VA): range of prices where 70% of the session volume is traded

- Value Area High (VAH): highest price within VA

- Value Area Low (VAL): lowest price within VA

- Point of Control (POC): the most traded price of the session (with the most volume)

- Session HIGH, LOW and MID levels are also important

There are a huge amount of things to know of Market Profile and Auction Theory like types of days, types of openings, relationships between value areas and openings... for those interested Jim Dalton's work is the way to come

I'm in my 2nd trading year and my goal for this year is learning to daytrade the futures markets thru the lens of Market Profile

For info on Volume Profile: TV Volume Profile wiki page at www.tradingview.com

For info on Market Profile and Market Auction Theory: Jim Dalton's book Mind over markets (this is a MUST)

BE AWARE: this indicator is based on the current chart's time interval and it only plots on 1, 2, 3, 5, 10, 15 and 30 minutes charts.

This is the correlation table TV uses in the Volume Profile Session Volume indicator (from the wiki above)

Chart Indicator

1 - 5 1

6 - 15 5

16 - 30 10

31 - 60 15

61 - 120 30

121 - 1D 60

This indicator doesn't follow that correlation, it doesn't get the volume data from a lower timeframe, it gets the data from the current chart resolution.

FEATURES

- 6 key values for each session: POC (solid yellow), VAH (solid red), VAL (solid green), profile HIGH (dashed silver), LOW (dashed silver) and MID (dotted silver) levels

- 3 sessions to choose for: RTH, GLOBEX and FULL

- select the numbers of sessions to plot by adding 12 hours periods back in time

- show/hide POC

- show/hide VAH & VAL

- show/hide session HIGH, LOW & MID levels

- highlight the periods of time out of the session (silver)

- extend the plotted lines all the way to the right, be careful this can turn the chart unreadable if there are a lot of sessions and lines plotted

SETTINGS

- Session: select between RTH (8:30 to 15:15 CT), GLOBEX (17:00 to 8:30 CT) and FULL (17:00 to 15:15 CT) sessions. RTH by default

- Last 12 hour periods to show: select the deph of the study by adding periods, for example, 60 periods are 30 natural days and around 22 trading days. 1 period by default

- Show POC (Point of Control): show/hide POC line. true by default

- Show VA (Value Area High & Low): show/hide VAH & VAL lines. true by default

- Show Range (Session High, Low & Mid): show/hide session HIGH, LOW & MID lines. true by default

- Highlight out of session: show/hide a silver shadow over the non session periods. true by default

- Extension: Extend all the plotted lines to the right. false by default

HOW TO SETUP

BE AWARE THIS INDICATOR PLOTS ONLY IN THE FOLLOWING CHART RESOLUTIONS: 1, 2, 3, 5, 10, 15 AND 30 MINUTES CHARTS. YOU MUST SELECT ONE OF THIS RESOLUTIONS TO THE INDICATOR BE ABLE TO PLOT

- By default this indicator plots all the levels for the last RTH session within the last 12 hours, if there is no plot try to adjust the 12 hours periods until the seesion and the periods match

- For Globex/Full sessions just select what you want from the dropdown menu and adjust the periods to plot the values

- Show or hide the levels you want with the 3 groups: POC line, VA lines and Session Range lines

- The highlight and extension options are for a better visibility of the levels as POC or VAH/VAL

THANKS TO

@watsonexchange for all the help, ideas and insights on this and the last two indicators (Market Delta & Market Internals) I'm working on my way to a 'clean chart' but for me it's not an easy path

@PineCoders for all the amazing stuff they do and all the help and tools they provide, in special the Script-Stopwatch at that was key in lowering this indicator's execution time

All the TV and Pine community, open source and shared knowledge are indeed the best way to help each other

IF YOU REALLY LIKE THIS WORK, please send me a comment or a private message and TELL ME WHAT you trade, HOW you trade it and your FAVOURITE SETUP for pulling out money from the market in a consistent basis, I'm learning to trade (this is my 2nd year) and I need all the help I can get

GOOD LUCK AND HAPPY TRADING

BO - Bar M15 2/3 SignalBO - Bar M15 2/3 Signal show the signal to trade Binary Option with rule below:

A. Indicator

* Bollinger Band (20,2): avoid waterfall

B. Rule of Signal

1. Rule1: Split Bar M15 to 3 part and load them on M5 chart (recommend use M5 IDC chart)

2. Rule 2: Delay 10' after bar M15 open => wait for price's pattern

3. Rule 3: Put Signal row 30-32

* Delay 10' after bar M15 open.

* Direction of 1/3 and 2/3 Bar M15 is upward

* close of 2/3 Bar M15 below upper band Bb(20,2) on M5 chart => avoid strong buy

4. Rule 4: Call Signal row 36-38

* Delay 10' after bar M15 open.

* Direction of 1/3 and 2/3 Bar M15 is downward

* close of 2/3 Bar M15 above lower band Bb(20,2) on M5 chart => avoid strong sell

C. Recommend Expiry time: Bar M15 close

* We try to catch the shadow of Bar M15 but dont trade when price run on the upper or lower band of BB(20,2,M5)

Cradle zone with BBand & SARHi All,

I have combined a number of indicators all into this 1 option.

It has the following:

> The Cradle zone represents a methodology to using the 10 and 20 EMA's at your selected time-frame.

Where the shading between the 10 and 20 EMA is green for an uptrend and red for a downtrend.

Default EMAs

10, 12, 20, and 50

> Those who are familiar using the Cradle method will find this option convenient.

> I have also added the Bollinger Band and Parabolic SAR as additional options to this item, to help give additional information by default.

Good luck with your trading strategy.

Please don't forget to give me a tick\like, as I would appreciate it.

Regards,

S.Sari /CryptoProspa

Point and Figure (PnF) Moving AveragesThis is live and non-repainting Point and Figure Chart Moving Averages tool. The script has it’s own P&F engine and not using integrated function of Trading View.

Point and Figure method is over 150 years old. It consist of columns that represent filtered price movements. Time is not a factor on P&F chart but as you can see with this script P&F chart created on time chart.

P&F chart provide several advantages, some of them are filtering insignificant price movements and noise, focusing on important price movements and making support/resistance levels much easier to identify.

Moving averages on Point & Figure charts are based on the average price of each column while bar chart moving averages are based closing price. Average Price means (ClosePrice + OpenPrice) / 2.

Because of there is double smoothing, you should use shorter lengths for moving averages. Double smoothing means: using average price smooths once, using length greater than 2 smooths price second time.

If you are new to Point & Figure Chart then you better get some information about it before using this tool. There are very good web sites and books. Please PM me if you need help about resources.

Options in the Script

Box size is one of the most important part of Point and Figure Charting. Chart price movement sensitivity is determined by the Point and Figure scale. Large box sizes see little movement across a specific price region, small box sizes see greater price movement on P&F chart. There are four different box scaling with this tool: Traditional, Percentage, Dynamic (ATR), or User-Defined

4 different methods for Box size can be used in this tool.

User Defined: The box size is set by user. A larger box size will result in more filtered price movements and fewer reversals. A smaller box size will result in less filtered price movements and more reversals.

ATR: Box size is dynamically calculated by using ATR, default period is 20.

Percentage: uses box sizes that are a fixed percentage of the stock's price. If percentage is 1 and stock’s price is $100 then box size will be $1

Traditional: uses a predefined table of price ranges to determine what the box size should be.

Price Range Box Size

Under 0.25 0.0625

0.25 to 1.00 0.125

1.00 to 5.00 0.25

5.00 to 20.00 0.50

20.00 to 100 1.0

100 to 200 2.0

200 to 500 4.0

500 to 1000 5.0

1000 to 25000 50.0

25000 and up 500.0

Default value is “ATR”, you may use one of these scaling method that suits your trading strategy.

If ATR or Percentage is chosen then there is rounding algorithm according to mintick value of the security. For example if mintick value is 0.001 and box size (ATR/Percentage) is 0.00124 then box size becomes 0.001.

And also while using dynamic box size (ATR or Percentage), box size changes only when closing price changed.

Reversal : It is the number of boxes required to change from a column of Xs to a column of Os or from a column of Os to a column of Xs. Default value is 3 (most used). For example if you choose reversal = 2 then you get the chart similar to Renko chart.

Source: Closing price or High-Low prices can be chosen as data source for P&F charting.

Options for P&F Moving Averages:

Moving averages on P&F charts are based on the average price of each column. Bar chart moving averages are based on each close price. While 10-day SMA on a bar chart is the average of the last ten closing prices, on a P&F chart, a 10-period SMA is the average price of the last 10 column averages. Average price means “(ClosePrice + OpenPrice) / 2”

2 P&F moving averages are shown on the chart.

It can show Exponental Moving Average ( EMA ) or Simple Moving Average ( SMA )

Source: You can choose Close Price or Average Price as source. Default is Average Price.

“Fast Length” and “Slow Length” are lengths for two moving averages. Default values are 1 and 5.

“Fill between MAs” is the option to fill between Moving averages by predefined colors 'Lime/Blue', 'Lime/Red', 'Green/Red', 'Green/Blue', 'Blue/Red'

There are alerts when Fast MA crossover or crossunder Slow MA. While adding alert “Once Per Bar Close” option should be chosen.

Pocket Pivot IndicatorFrom Gil Morales and Chris Kacher (O'Neil's disciples). Designed to find buy points in bases and continuation buy points in an uptrend. The volume today must be greater then the maximum down volume of the past 10 trading days. Recommended to use in conjunction with the 10 day and/or 50 day moving average.

Typical use :

Scan for pocket pivots.

Is stock strong fundamentally? i.e- leader in it's sector

Has the stock developed a base ?(see O'Neil's work for base discussion)

Is the stock breaking through or bouncing off the 10 period sma? (can use 50 sma too)

If so.. a possible buy.

Cheers

David

PIP HUNTERSCR STOCH RSI SIGNALScript made in combination of Stoch and RSI, made by and for PIPHUNTERS on 03/10/2019

Stoch default values 10-3-3 higher band level 90, lower band level 10

RSI default value 14 color:blue

Simplified SizingEnsure you Uncheck #1 , #2, #3 in the STYLE tab or it draws the lines you only need the numbers for.

The first number is the deviation from the EMA , anything below 1.75 == 1. (less than 0.75 % deviation)

NOTE: The fill area turns yellow @ 1.50 and red above 2.75

There are steps built in to slightly lower share size when specific levels of divergence register:

From 1.75 to 10 , 1 == 1.10 (10% reduction)

From 10 and up, 1 == 1.20 (20% reduction)

The second number is the Average True Range , calculated by the input length (RMA smoothed) and a multiplier (in decimal form).

NOTE: From 930-936 this value is multiplied by 1.5

The third number is the max share size.

The 4th number is the lot price if you take a position at the max size.

INPUTS:

ATR Length

EMA Length for divergence calculation

ATR Multiplier (0.1 - 10)

Equity in account

Max loss per trade.

Good Luck!

Ultimate Moving Average Package (17 MA's)Included is the:

VWAP

Current time frame 10 EMA

Current time frame 20 EMA

Current time frame 50 EMA

Current time frame 10 SMA

Current time frame 20 SMA

Current time frame 50 SMA

Daily 10 EMA

Daily 20 EMA

Daily 50 EMA

Daily 50 SMA

Daily 100 SMA

Daily 200 SMA

Weekly 100 SMA

Weekly 200 SMA

Monthly 100 SMA

Monthly 200 SMA

All Daily/Weekly/Monthly MA's can be seen on intraday charts. Current time frame MA's change depending on your time frame. Obviously you dont need all 17 on your chart but you can pick the ones you like and disable the rest.

A.I.Driven Aggressive Intraday Models For 20190610(New to TradingView and trying to learn how best to share our daily Model Trades with the awesome community here. Still learning the tools here and may not be using the best approaches to publish ideas/charts/scirpts - please help us learn by suggesting best practices)

>>>>> Model Trades Published pre-market this morning at tradersai blogspot <<<<<

***** Medium-Frequency Models*****: For today, Monday 06/10, our medium-frequency models indicate going long on a break above 2903 with a 10-point trailing stop, and going short on a break below 2845 with an 8-point trailing stop.

---Note: For the trades to trigger, the breaks should occur during the regular session hours starting at 9:30am ET. By design, these models do NOT open any new positions after 3:45pm. Only one open position at any given time.---

***** Aggressive Intraday Models *****: For today, Monday 06/10, our aggressive intraday models indicate going long on a break above 2895 or 2886 or 2874 with an 8-point trailing stop, and going short on a break below 2890 or 2882 or 2870 with a 6-point trailing stop.

---- Note: For the trades to trigger, the breaks should occur during regular session hours starting at 9:30am ET. Due to the intraday nature of these aggressive models, they indicate closing any open trades at 3:55pm and remaining flat into the session close. No opening of new positions after 3:45pm. Only one open position at any given time.----

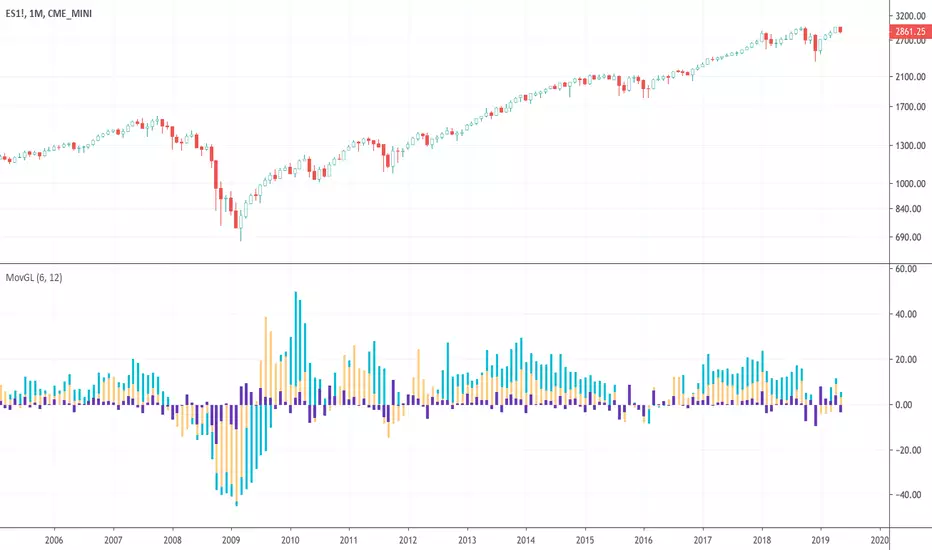

Moving Gain Loss PercentTracks the percentage gain/loss in three ranges:

single candle (can be turned on or off)

custom range of candles

custom range of candles

For example, with a range of 3 candles, and the serie:

1 - close 10

2 - close 5

3 - close 20

The moving gain would be:

1 - close 10 - gain 10, infinite%

2 - close 5 - gain 5, infinite%

3 - close 18 - gain 8, 80%

Or, for example if the range is 12 candles on a monthly chart, then the result is the Year-To-Date gain/loss plotted as a percentage.

Sexy RSI for sexy tradersHello fellow sexy traders.

I was tired of constantly having to add my own horizontals/MAs to the default RSI so I decided to make this modification.

The default settings include channels from 40-80 (green horizontals) for a bullish range, and 20-60 (red horizontals) for the bearish range.

Also includes white line at 50 level, and blue horizontals at extremes (90 and 10).

If RSI stays in one of the red or green range that can signify the trend direction, as directed by Andrew Cardwell (inventor of the RSI).

If you wish for other levels to be included, just let me know! Comment on here or dm me on twitter @boss_charts and I can add the settings for you, so all you have to do is click a button and it will set it to your desired config. I want this to be a tool that is useful for heavy traders to save them time.

Additionally, in order to tell the level of the RSI and how overextended it might be, I added the setting for the RSI to change color depending on its level. Current settings are as follows:

Normal RSI (30-70) = PURPLE

Conventional Overbought/Oversold (30-20 + 70-80) = RED

1st extended (20-15 + 80-85) = PINK

2nd extended (15-10 + 85-90) = ORANGE

VERY EXTENDED (<10 + >90) = YELLOW

That way you can get an idea of how drastic a move is by the color alone. According to Dr. Cardwell, a drastic move to over/under extended can be a sign of strength.

Finally, there are the default MAs added that Mr. Cardwell defines as useful for defining the trend. These being the 9 MA and 45 EMA/WMA.

The strategy with these is to have the MAs on both price and RSI. If the 9MA is above the 45 MA on both price and RSI, then this is bullish and you can look for longs.

Conversely, if the 9 is below the 45 on both RSI and price that is bearish, and you can look for shorts.

I added the background color change for the points where the MAs cross each other, so you do not have to have the MAs fogging up your charts to know where they are relative to one another. This is similar to my MA cross indicator which contains the same functionality.

Never financial advice. Backtest it for yourself and find MA configurations that work for you.

Enjoy! Feel free to send feedback/requests whenever.

Multi SMA EMA WMA HMA BB (5x8 MAs Bollinger Bands) MAX MTF - RRBMulti SMA EMA WMA HMA 4x7 Moving Averages with Bollinger Bands MAX MTF by RagingRocketBull 2019

Version 1.0

All available MAX MTF versions are listed below (They are very similar and I don't want to publish them as separate indicators):

ver 1.0: 4x7 = 28 MTF MAs + 28 Levels + 3 BB = 59 < 64

ver 2.0: 5x6 = 30 MTF MAs + 30 Levels + 3 BB = 63 < 64

ver 3.0: 3x10 = 30 MTF MAs + 30 Levels + 3 BB = 63 < 64

ver 4.0: 5(4+1)x8 = 8 CurTF MAs + 32 MTF MAs + 20 Levels + 3 BB = 63 < 64

ver 5.0: 6(5+1)x6 = 6 CurTF MAs + 30 MTF MAs + 24 Levels + 3 BB = 63 < 64

ver 6.0: 4(3+1)x10 = 10 CurTF MAs + 30 MTF MAs + 20 Levels + 3 BB = 63 < 64

Fib numbers: 8, 13, 21, 34, 55, 89, 144, 233, 377

This indicator shows multiple MAs of any type SMA EMA WMA HMA etc with BB and MTF support, can show MAs as dynamically moving levels.

There are 4 MA groups + 1 BB group, a total of 4 TFs * 7 MAs = 28 MAs. You can assign any type/timeframe combo to a group, for example:

- EMAs 9,12,26,50,100,200,400 x H1, H4, D1, W1 (4 TFs x 7 MAs x 1 type)

- EMAs 8,13,21,30,34,50,55,89,100,144,200,233,377,400 x M15, H1 (2 TFs x 14 MAs x 1 type)

- D1 EMAs and SMAs 8,13,21,30,34,50,55,89,100,144,200,233,377,400 (1 TF x 14 MAs x 2 types)

- H1 WMAs 13,21,34,55,89,144,233; H4 HMAs 9,12,26,50,100,200,400; D1 EMAs 12,26,89,144,169,233,377; W1 SMAs 9,12,26,50,100,200,400 (4 TFs x 7 MAs x 4 types)

- +1 extra MA type/timeframe for BB

There are several versions: Simple, MTF, Pro MTF, Advanced MTF, MAX MTF and Ultimate MTF. This is the MAX MTF version. The Differences are listed below. All versions have BB

- Simple: you have 2 groups of MAs that can be assigned any type (5+5)

- MTF: +2 custom Timeframes for each group (2x5 MTF) +1 TF for BB, TF XY smoothing

- Pro MTF: 4 custom Timeframes for each group (4x3 MTF), 1 TF for BB, MA levels and show max bars back options

- Advanced MTF: +4 extra MAs/group (4x7 MTF), custom Ticker/Symbols, Timeframe <>= filter, Remove Duplicates Option

- MAX MTF: +2 subtypes/group, packed to the limit with max possible MAs/TFs: 4x7, 5x6, 3x10, 4(3+1)x10, 5(4+1)x8, 6(5+1)x6

- Ultimate MTF: +individual settings for each MA, custom Ticker/Symbols

MAX MTF version tests the limits of Pinescript trying to squeeze as many MAs/TFs as possible into a single indicator.

It's basically a maxed out Advanced version with subtypes allowing for mixed types within a group (i.e. both emas and smas in a single group/TF)

Pinescript has the following limits:

- max 40 security calls (6 calls are reserved for dupe checks and smoothing, 2 are used for BB, so only 32 calls are available)

- max 64 plot outputs (BB uses 3 outputs, so only 61 plot outputs are available)

- max 50000 (50kb) size of the compiled code

Based on those limits, you can only have the following MAs/TFs combos in a single script:

1. 4x7, 5x6, 3x10 - total number of MTF MAs must always be <= 32, and you can still have BB and Num Levels = total MAs, without any compromises

2. 5(4+1)x8, 6(5+1)x6, 4(3+1)x10 - you can use the Current Symbol/Timeframe as an extra (+1) fixed TF with the same number of MTF MAs

- you don't need to call security to display MAs on the Current Symbol/Timeframe, so the total number of MTF MAs remains the same and is still <= 32

- to fit that many MAs into the max 64 plot outputs limit you need to reduce the number of levels (not every MA Group will have corresponding levels)

Features:

- 4x7 = 28 MAs of any type

- 4x MTF groups with XY step line smoothing

- +1 extra TF/type for BB MAs

- 2 MA subtypes within each group/TF

- 4x7 = 28 MA levels with adjustable group offsets, indents and shift

- supports any existing type of MA: SMA, EMA, WMA, Hull Moving Average (HMA)

- custom tickers/symbols for each group

- show max bars back option

- show/hide both groups of MAs/levels/BB and individual MAs

- timeframe filter: show only MAs/Levels with TFs <>= Current TF

- hide MAs/Levels with duplicate TFs

- support for custom TFs that are not available in free accounts: 2D, 3D etc

- support for timeframes in H: H, 2H, 4H etc

Notes:

- Uses timeframe textbox instead of input resolution dropdown to allow for 240 120 and other custom TFs

- Uses symbol textbox instead of input symbol to avoid establishing multiple dummy security connections to the current ticker - otherwise empty symbols will prevent script from running

- Possible reasons for missing MAs on a chart:

- there may not be enough bars in history to start plotting it. For example, W1 EMA200 needs at least 200 bars on a weekly chart.

- for charts with low/fractional prices i.e. 0.00002 << 0.001 (default Y smoothing step) decrease Y smoothing as needed (set Y = 0.0000001) or disable it completely (set X,Y to 0,0)

- for charts with high price values i.e. 20000 >> 0.001 increase Y smoothing as needed (set Y = 10-20). Higher values exceeding MAs point density will cause it to disappear as there will be no points to plot. Different TFs may require diff adjustments

- TradingView Replay Mode UI and Pinescript security calls are limited to TFs >= D (D,2D,W,MN...) for free accounts

- attempting to plot any TF < D1 in Replay Mode will only result in straight lines, but all TFs will work properly in history and real-time modes. This is not a bug.

- Max Bars Back (num_bars) is limited to 5000 for free accounts (10000 for paid), will show error when exceeded. To plot on all available history set to 0 (default)

- Slow load/redraw times. This indicator becomes slower, its UI less responsive when:

- Pinescript Node.js graphics library is too slow and inefficient at plotting bars/objects in a browser window. Code optimization doesn't help much - the graphics engine is the main reason for general slowness.

- the chart has a long history (10000+ bars) in a browser's cache (you have scrolled back a couple of screens in a max zoom mode).

- Reload the page/Load a fresh chart and then apply the indicator or

- Switch to another Timeframe (old TF history will still remain in cache and that TF will be slow)

- in max possible zoom mode around 4500 bars can fit on 1 screen - this also slows down responsiveness. Reset Zoom level

- initial load and redraw times after a param change in UI also depend on TF. For example: D1/W1 - 2 sec, H1/H4 - 5-6 sec, M30 - 10 sec, M15/M5 - 4 sec, M1 - 5 sec. M30 usually has the longest history (up to 16000 bars) and W1 - the shortest (1000 bars).

- when indicator uses more MAs (plots) and timeframes it will redraw slower. Seems that up to 5 Timeframes is acceptable, but 6+ Timeframes can become very slow.

- show_last=last_bars plot limit doesn't affect load/redraw times, so it was removed from MA plot

- Max Bars Back (num_bars) default/custom set UI value doesn't seem to affect load/redraw times

- In max zoom mode all dynamic levels disappear (they behave like text)

- Dupe check includes symbol: symbol, tf, both subtypes - all must match for a duplicate group

- For the dupe check to work correctly a custom symbol must always include an exchange prefix. BB is not checked for dupes

Good Luck! Feel free to learn from/reuse the code to build your own indicators.