Risk-On / Risk-Off CompositeReal-time Risk-On / Risk-Off Composite from your four ratios:

SPY / TLT (equities vs long bonds)

HYG / LQD (high-yield vs IG credit)

HG / GOLD (copper vs gold)

BTC / GOLD (speculative vs defensive)

It:

normalizes each ratio with a z-score (so they’re comparable),

lets you weight them,

plots a composite line + histogram (up = risk-on, down = risk-off),

shows a small heat-table for each sub-signal,

and includes alert conditions for Risk-On / Risk-Off flips.

在脚本中搜索"西班牙人VS奥萨苏纳"

Ripster: DTR/ATR + SMA Div + RVOL🧭 Overview

The indicator combines three major analytical tools into one TradingView Pine v6 script — designed for clean, at-a-glance insight into range, divergence, and volume activity.

It shows:

DTR vs ATR Table – current Daily True Range compared to Average True Range.

SMA Price Divergence + EMA Signal – a histogram with color-coded momentum bands.

RVOL Table + Candle Coloring + Change Labels – relative-volume analysis with visual cues on the chart.

Short title: ripcombo

Runs on chart overlay (no separate pane).

📊 1. DTR vs ATR Table

Compares today’s price range (High-Low) to the average true range over a selectable length.

Supports multiple smoothing methods: EMA, RMA, SMA, WMA.

Table position and text size are configurable.

Color logic:

🟢 ≤ 70 % of ATR → low volatility

🟡 70–90 % → average

🔴 ≥ 90 % → expanded range

📈 2. SMA Divergence + EMA Signal

Computes fast (14 SMA) and slow (30 SMA) divergences of price.

Plots two histograms plus an EMA signal line of the slow divergence.

Visuals:

Columns shaded by transparency for clarity.

Rising EMA → lime line (up momentum).

Falling EMA → red line (down momentum).

Optional upper/lower bands and zero line provide quick overbought/oversold zones.

🔥 3. RVOL (Relative Volume)

Adds powerful volume-based context:

a. Table Display

Shows:

Candle Volume

RVOL (Now)

RVOL (Prev)

Δ RVOL (change Now − Prev)

Colors:

🔴 > 200 % (very high volume)

🟠 100–200 % (high volume)

🟡 < 100 % (normal/low volume)

Δ column is green ▲ for increase, red ▼ for decrease.

b. Candle Coloring (optional)

Colors price candles themselves by current RVOL threshold so high-volume candles visually stand out.

c. Last-Bar Label (optional)

Prints a compact label on the latest candle showing:

RVOL: ### % Δ: ▲/▼## %

so you can instantly see the current volume strength and how it changed from the previous bar.

⚙️ User Settings

All major elements are toggle-controlled:

Enable/disable ATR, Divergence, or RVOL sections.

Choose table positions (top/middle/bottom × left/center/right).

Select text sizes, smoothing types, color modes, and visual transparency.

Candle coloring + label visibility are optional.

🧠 At a Glance

Component Purpose Key Visuals

DTR vs ATR Measures volatility expansion One-cell colored table

SMA Divergence Detects price momentum shifts Columns + EMA line + bands

RVOL Analysis Highlights unusual trading volume Colored table + Δ column + candle colors + label

✅ Result

You get a single on-chart tool that:

Quantifies volatility, momentum, and volume context together.

Highlights strong activity days (ATR & RVOL) in color.

Shows whether current candle’s volume is rising or falling vs the previous.

Perfect for spotting breakouts, reversals, or exhaustion moves without switching indicators.

MACD Enhanced [DCAUT]█ MACD Enhanced

📊 ORIGINALITY & INNOVATION

The MACD Enhanced represents a significant improvement over traditional MACD implementations. While Gerald Appel's original MACD from the 1970s was limited to exponential moving averages (EMA), this enhanced version expands algorithmic options by supporting 21 different moving average calculations for both the main MACD line and signal line independently.

This improvement addresses an important limitation of traditional MACD: the inability to adapt the indicator's mathematical foundation to different market conditions. By allowing traders to select from algorithms ranging from simple moving averages (SMA) for stability to advanced adaptive filters like Kalman Filter for noise reduction, this implementation changes MACD from a fixed-algorithm tool into a flexible instrument that can be adjusted for specific market environments and trading strategies.

The enhanced histogram visualization system uses a four-color gradient that helps communicate momentum strength and direction more clearly than traditional single-color histograms.

📐 MATHEMATICAL FOUNDATION

The core calculation maintains the proven MACD formula: Fast MA(source, fastLength) - Slow MA(source, slowLength), but extends it with algorithmic flexibility. The signal line applies the selected smoothing algorithm to the MACD line over the specified signal period, while the histogram represents the difference between MACD and signal lines.

Available Algorithms:

The implementation supports a comprehensive spectrum of technical analysis algorithms:

Basic Averages: SMA (arithmetic mean), EMA (exponential weighting), RMA (Wilder's smoothing), WMA (linear weighting)

Advanced Averages: HMA (Hull's low-lag), VWMA (volume-weighted), ALMA (Arnaud Legoux adaptive)

Mathematical Filters: LSMA (least squares regression), DEMA (double exponential), TEMA (triple exponential), ZLEMA (zero-lag exponential)

Adaptive Systems: T3 (Tillson T3), FRAMA (fractal adaptive), KAMA (Kaufman adaptive), MCGINLEY_DYNAMIC (reactive to volatility)

Signal Processing: ULTIMATE_SMOOTHER (low-pass filter), LAGUERRE_FILTER (four-pole IIR), SUPER_SMOOTHER (two-pole Butterworth), KALMAN_FILTER (state-space estimation)

Specialized: TMA (triangular moving average), LAGUERRE_BINOMIAL_FILTER (binomial smoothing)

Each algorithm responds differently to price action, allowing traders to match the indicator's behavior to market characteristics: trending markets benefit from responsive algorithms like EMA or HMA, while ranging markets require stable algorithms like SMA or RMA.

📊 COMPREHENSIVE SIGNAL ANALYSIS

Histogram Interpretation:

Positive Values: Indicate bullish momentum when MACD line exceeds signal line, suggesting upward price pressure and potential buying opportunities

Negative Values: Reflect bearish momentum when MACD line falls below signal line, indicating downward pressure and potential selling opportunities

Zero Line Crosses: MACD crossing above zero suggests transition to bullish bias, while crossing below indicates bearish bias shift

Momentum Changes: Rising histogram (regardless of positive/negative) signals accelerating momentum in the current direction, while declining histogram warns of momentum deceleration

Advanced Signal Recognition:

Divergences: Price making new highs/lows while MACD fails to confirm often precedes trend reversals

Convergence Patterns: MACD line approaching signal line suggests impending crossover and potential trade setup

Histogram Peaks: Extreme histogram values often mark momentum exhaustion points and potential reversal zones

🎯 STRATEGIC APPLICATIONS

Comprehensive Trend Confirmation Strategies:

Primary Trend Validation Protocol:

Identify primary trend direction using higher timeframe (4H or Daily) MACD position relative to zero line

Confirm trend strength by analyzing histogram progression: consistent expansion indicates strong momentum, contraction suggests weakening

Use secondary confirmation from MACD line angle: steep angles (>45°) indicate strong trends, shallow angles suggest consolidation

Validate with price structure: trending markets show consistent higher highs/higher lows (uptrend) or lower highs/lower lows (downtrend)

Entry Timing Techniques:

Pullback Entries in Uptrends: Wait for MACD histogram to decline toward zero line without crossing, then enter on histogram expansion with MACD line still above zero

Breakout Confirmations: Use MACD line crossing above zero as confirmation of upward breakouts from consolidation patterns

Continuation Signals: Look for MACD line re-acceleration (steepening angle) after brief consolidation periods as trend continuation signals

Advanced Divergence Trading Systems:

Regular Divergence Recognition:

Bullish Regular Divergence: Price creates lower lows while MACD line forms higher lows. This pattern is traditionally considered a potential upward reversal signal, but should be combined with other confirmation signals

Bearish Regular Divergence: Price makes higher highs while MACD shows lower highs. This pattern is traditionally considered a potential downward reversal signal, but trading decisions should incorporate proper risk management

Hidden Divergence Strategies:

Bullish Hidden Divergence: Price shows higher lows while MACD displays lower lows, indicating trend continuation potential. Use for adding to existing long positions during pullbacks

Bearish Hidden Divergence: Price creates lower highs while MACD forms higher highs, suggesting downtrend continuation. Optimal for adding to short positions during bear market rallies

Multi-Timeframe Coordination Framework:

Three-Timeframe Analysis Structure:

Primary Timeframe (Daily): Determine overall market bias and major trend direction. Only trade in alignment with daily MACD direction

Secondary Timeframe (4H): Identify intermediate trend changes and major entry opportunities. Use for position sizing decisions

Execution Timeframe (1H): Precise entry and exit timing. Look for MACD line crossovers that align with higher timeframe bias

Timeframe Synchronization Rules:

Daily MACD above zero + 4H MACD rising = Strong uptrend context for long positions

Daily MACD below zero + 4H MACD declining = Strong downtrend context for short positions

Conflicting signals between timeframes = Wait for alignment or use smaller position sizes

1H MACD signals only valid when aligned with both higher timeframes

Algorithm Considerations by Market Type:

Trending Markets: Responsive algorithms like EMA, HMA may be considered, but effectiveness should be tested for specific market conditions

Volatile Markets: Noise-reducing algorithms like KALMAN_FILTER, SUPER_SMOOTHER may help reduce false signals, though results vary by market

Range-Bound Markets: Stability-focused algorithms like SMA, RMA may provide smoother signals, but individual testing is required

Short Timeframes: Low-lag algorithms like ZLEMA, T3 theoretically respond faster but may also increase noise

Important Note: All algorithm choices and parameter settings should be thoroughly backtested and validated based on specific trading strategies, market conditions, and individual risk tolerance. Different market environments and trading styles may require different configuration approaches.

📋 DETAILED PARAMETER CONFIGURATION

Comprehensive Source Selection Strategy:

Price Source Analysis and Optimization:

Close Price (Default): Most commonly used, reflects final market sentiment of each period. Best for end-of-day analysis, swing trading, daily/weekly timeframes. Advantages: widely accepted standard, good for backtesting comparisons. Disadvantages: ignores intraday price action, may miss important highs/lows

HL2 (High+Low)/2: Midpoint of the trading range, reduces impact of opening gaps and closing spikes. Best for volatile markets, gap-prone assets, forex markets. Calculation impact: smoother MACD signals, reduced noise from price spikes. Optimal when asset shows frequent gaps, high volatility during specific sessions

HLC3 (High+Low+Close)/3: Weighted average emphasizing the close while including range information. Best for balanced analysis, most asset classes, medium-term trading. Mathematical effect: 33% weight to high/low, 33% to close, provides compromise between close and HL2. Use when standard close is too noisy but HL2 is too smooth

OHLC4 (Open+High+Low+Close)/4: True average of all price points, most comprehensive view. Best for complete price representation, algorithmic trading, statistical analysis. Considerations: includes opening sentiment, smoothest of all options but potentially less responsive. Optimal for markets with significant opening moves, comprehensive trend analysis

Parameter Configuration Principles:

Important Note: Different moving average algorithms have distinct mathematical characteristics and response patterns. The same parameter settings may produce vastly different results when using different algorithms. When switching algorithms, parameter settings should be re-evaluated and tested for appropriateness.

Length Parameter Considerations:

Fast Length (Default 12): Shorter periods provide faster response but may increase noise and false signals, longer periods offer more stable signals but slower response, different algorithms respond differently to the same parameters and may require adjustment

Slow Length (Default 26): Should maintain a reasonable proportional relationship with fast length, different timeframes may require different parameter configurations, algorithm characteristics influence optimal length settings

Signal Length (Default 9): Shorter lengths produce more frequent crossovers but may increase false signals, longer lengths provide better signal confirmation but slower response, should be adjusted based on trading style and chosen algorithm characteristics

Comprehensive Algorithm Selection Framework:

MACD Line Algorithm Decision Matrix:

EMA (Standard Choice): Mathematical properties: exponential weighting, recent price emphasis. Best for general use, traditional MACD behavior, backtesting compatibility. Performance characteristics: good balance of speed and smoothness, widely understood behavior

SMA (Stability Focus): Equal weighting of all periods, maximum smoothness. Best for ranging markets, noise reduction, conservative trading. Trade-offs: slower signal generation, reduced sensitivity to recent price changes

HMA (Speed Optimized): Hull Moving Average, designed for reduced lag. Best for trending markets, quick reversals, active trading. Technical advantage: square root period weighting, faster trend detection. Caution: can be more sensitive to noise

KAMA (Adaptive): Kaufman Adaptive MA, adjusts smoothing based on market efficiency. Best for varying market conditions, algorithmic trading. Mechanism: fast smoothing in trends, slow smoothing in sideways markets. Complexity: requires understanding of efficiency ratio

Signal Line Algorithm Optimization Strategies:

Matching Strategy: Use same algorithm for both MACD and signal lines. Benefits: consistent mathematical properties, predictable behavior. Best when backtesting historical strategies, maintaining traditional MACD characteristics

Contrast Strategy: Use different algorithms for optimization. Common combinations: MACD=EMA, Signal=SMA for smoother crossovers, MACD=HMA, Signal=RMA for balanced speed/stability, Advanced: MACD=KAMA, Signal=T3 for adaptive behavior with smooth signals

Market Regime Adaptation: Trending markets: both fast algorithms (EMA/HMA), Volatile markets: MACD=KALMAN_FILTER, Signal=SUPER_SMOOTHER, Range-bound: both slow algorithms (SMA/RMA)

Parameter Sensitivity Considerations:

Impact of Parameter Changes:

Length Parameter Sensitivity: Small parameter adjustments can significantly affect signal timing, while larger adjustments may fundamentally change indicator behavior characteristics

Algorithm Sensitivity: Different algorithms produce different signal characteristics. Thoroughly test the impact on your trading strategy before switching algorithms

Combined Effects: Changing multiple parameters simultaneously can create unexpected effects. Recommendation: adjust parameters one at a time and thoroughly test each change

📈 PERFORMANCE ANALYSIS & COMPETITIVE ADVANTAGES

Response Characteristics by Algorithm:

Fastest Response: ZLEMA, HMA, T3 - minimal lag but higher noise

Balanced Performance: EMA, DEMA, TEMA - good trade-off between speed and stability

Highest Stability: SMA, RMA, TMA - reduced noise but increased lag

Adaptive Behavior: KAMA, FRAMA, MCGINLEY_DYNAMIC - automatically adjust to market conditions

Noise Filtering Capabilities:

Advanced algorithms like KALMAN_FILTER and SUPER_SMOOTHER help reduce false signals compared to traditional EMA-based MACD. Noise-reducing algorithms can provide more stable signals in volatile market conditions, though results will vary based on market conditions and parameter settings.

Market Condition Adaptability:

Unlike fixed-algorithm MACD, this enhanced version allows real-time optimization. Trending markets benefit from responsive algorithms (EMA, HMA), while ranging markets perform better with stable algorithms (SMA, RMA). The ability to switch algorithms without changing indicators provides greater flexibility.

Comparative Performance vs Traditional MACD:

Algorithm Flexibility: 21 algorithms vs 1 fixed EMA

Signal Quality: Reduced false signals through noise filtering algorithms

Market Adaptability: Optimizable for any market condition vs fixed behavior

Customization Options: Independent algorithm selection for MACD and signal lines vs forced matching

Professional Features: Advanced color coding, multiple alert conditions, comprehensive parameter control

USAGE NOTES

This indicator is designed for technical analysis and educational purposes. Like all technical indicators, it has limitations and should not be used as the sole basis for trading decisions. Algorithm performance varies with market conditions, and past characteristics do not guarantee future results. Always combine with proper risk management and thorough strategy testing.

First Passage Time - Distribution AnalysisThe First Passage Time (FPT) Distribution Analysis indicator is a sophisticated probabilistic tool that answers one of the most critical questions in trading: "How long will it take for price to reach my target, and what are the odds of getting there first?"

Unlike traditional technical indicators that focus on what might happen, this indicator tells you when it's likely to happen.

Mathematical Foundation: First Passage Time Theory

What is First Passage Time?

First Passage Time (FPT) is a concept in stochastic processes that measures the time it takes for a random process to reach a specific threshold for the first time. Originally developed in physics and mathematics, FPT has applications in:

Quantitative Finance: Option pricing, risk management, and algorithmic trading

Neuroscience: Modeling neural firing patterns

Biology: Population dynamics and disease spread

Engineering: Reliability analysis and failure prediction

The Mathematics Behind It

This indicator uses Geometric Brownian Motion (GBM), the same stochastic model used in the Black-Scholes option pricing formula:

dS = μS dt + σS dW

Where:

S = Asset price

μ = Drift (trend component)

σ = Volatility (uncertainty component)

dW = Wiener process (random walk)

Through Monte Carlo simulation, the indicator runs 1,000+ price path simulations to statistically determine:

When each threshold (+X% or -X%) is likely to be hit

Which threshold is hit first (directional bias)

How often each scenario occurs (probability distribution)

🎯 How This Indicator Works

Core Algorithm Workflow:

Calculate Historical Statistics

Measures recent price volatility (standard deviation of log returns)

Calculates drift (average directional movement)

Annualizes these metrics for meaningful comparison

Run Monte Carlo Simulations

Generates 1,000+ random price paths based on historical behavior

Tracks when each path hits the upside (+X%) or downside (-X%) threshold

Records which threshold was hit first in each simulation

Aggregate Statistical Results

Calculates percentile distributions (10th, 25th, 50th, 75th, 90th)

Computes "first hit" probabilities (upside vs downside)

Determines average and median time-to-target

Visual Representation

Displays thresholds as horizontal lines

Shows gradient risk zones (purple-to-blue)

Provides comprehensive statistics table

📈 Use Cases

1. Options Trading

Selling Options: Determine if your strike price is likely to be hit before expiration

Buying Options: Estimate probability of reaching profit targets within your time window

Time Decay Management: Compare expected time-to-target vs theta decay

Example: You're considering selling a 30-day call option 5% out of the money. The indicator shows there's a 72% chance price hits +5% within 12 days. This tells you the trade has high assignment risk.

2. Swing Trading

Entry Timing: Wait for higher probability setups when directional bias is strong

Target Setting: Use median time-to-target to set realistic profit expectations

Stop Loss Placement: Understand probability of hitting your stop before target

Example: The indicator shows 85% upside probability with median time of 3.2 days. You can confidently enter long positions with appropriate position sizing.

3. Risk Management

Position Sizing: Larger positions when probability heavily favors one direction

Portfolio Allocation: Reduce exposure when probabilities are near 50/50 (high uncertainty)

Hedge Timing: Know when to add protective positions based on downside probability

Example: Indicator shows 55% upside vs 45% downside—nearly neutral. This signals high uncertainty, suggesting reduced position size or wait for better setup.

4. Market Regime Detection

Trending Markets: High directional bias (70%+ one direction)

Range-bound Markets: Balanced probabilities (45-55% both directions)

Volatility Regimes: Compare actual vs theoretical minimum time

Example: Consistent 90%+ bullish bias across multiple timeframes confirms strong uptrend—stay long and avoid counter-trend trades.

First Hit Rate (Most Important!)

Shows which threshold is likely to be hit FIRST:

Upside %: Probability of hitting upside target before downside

Downside %: Probability of hitting downside target before upside

These always sum to 100%

⚠️ Warning: If you see "Low Hit Rate" warning, increase this parameter!

Advanced Parameters

Drift Mode

Allows you to explore different scenarios:

Historical: Uses actual recent trend (default—most realistic)

Zero (Neutral): Assumes no trend, only volatility (symmetric probabilities)

50% Reduced: Dampens trend effect (conservative scenario)

Use Case: Switch to "Zero (Neutral)" to see what happens in a pure volatility environment, useful for range-bound markets.

Distribution Type

Percentile: Shows 10%, 25%, 50%, 75%, 90% levels (recommended for most users)

Sigma: Shows standard deviation levels (1σ, 2σ)—useful for statistical analysis

⚠️ Important Limitations & Best Practices

Limitations

Assumes GBM: Real markets have fat tails, jumps, and regime changes not captured by GBM

Historical Parameters: Uses recent volatility/drift—may not predict regime shifts

No Fundamental Events: Cannot predict earnings, news, or macro shocks

Computational: Runs only on last bar—doesn't give historical signals

Remember: Probabilities are not certainties. Use this indicator as part of a comprehensive trading plan with proper risk management.

Created by: Henrique Centieiro. feedback is more than welcome!

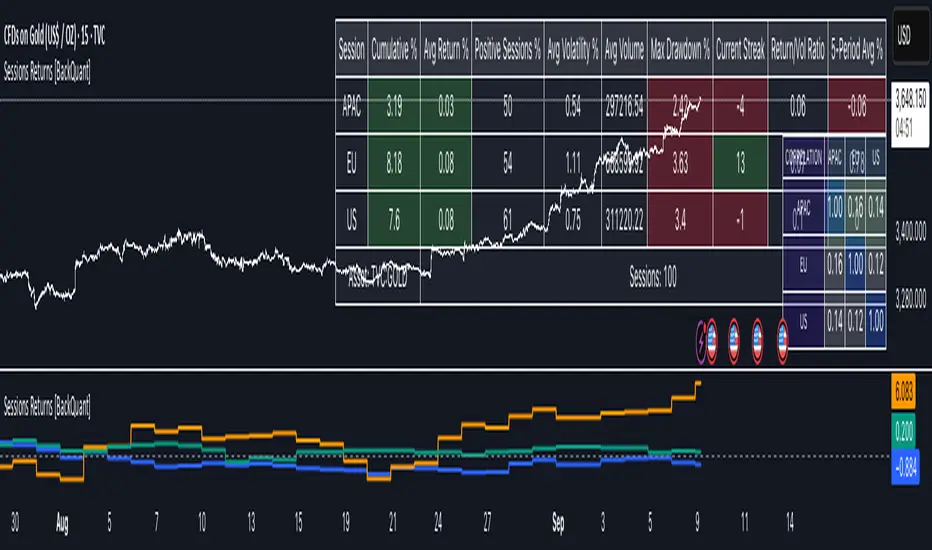

Cumulative Returns by Session [BackQuant]Cumulative Returns by Session

What this is

This tool breaks the trading day into three user-defined sessions and tracks how much each session contributes to return, volatility, and volume. It then aggregates results over a rolling window so you can see which session has been pulling its weight, how streaky each session has been, and how sessions relate to one another through a compact correlation heatmap.

We’ve also given the functionality for the user to use a simplified table, just by switching off all settings they are not interested in.

How it works

1) Session segmentation

You define APAC, EU, and US sessions with explicit hours and time zones. The script detects when each session starts and ends on every intraday bar and records its open, intraday high and low, close, and summed volume.

2) Per-session math

At each session end the script computes:

Return — either Percent: (Close−Open)÷Open×100(Close − Open) ÷ Open × 100(Close−Open)÷Open×100 or Points: (Close−Open)(Close − Open)(Close−Open), based on your selection.

Volatility — either Range: (High−Low)÷Open×100(High − Low) ÷ Open × 100(High−Low)÷Open×100 or ATR scaled by price: ATR÷Open×100ATR ÷ Open × 100ATR÷Open×100.

Volume — total volume transacted during that session.

3) Storage and lookback

Each day’s three session stats are stored as a row. You choose how many recent sessions to keep in memory. The script then:

Builds cumulative returns for APAC, EU, US across the lookback.

Computes averages, win rates, and a Sharpe-like ratio avgreturn÷avgvolatilityavg return ÷ avg volatilityavgreturn÷avgvolatility per session.

Tracks streaks of positive or negative sessions to show momentum.

Tracks drawdowns on cumulative returns to show worst runs from peak.

Computes rolling means over a short window for short-term drift.

4) Correlation heatmap

Using the stored arrays of session returns, the script calculates Pearson correlations between APAC–EU, APAC–US, and EU–US, and colors the matrix by strength and sign so you can spot coupling or decoupling at a glance.

What it plots

Three lines: cumulative return for APAC, EU, US over the chosen lookback.

Zero reference line for orientation.

A statistics table with cumulative %, average %, positive session rate, and optional columns for volatility, average volume, max drawdown, current streak, return-to-vol ratio, and rolling average.

A small correlation heatmap table showing APAC, EU, US cross-session correlations.

How to use it

Pick the asset — leave Custom Instrument empty to use the chart symbol, or point to another symbol for cross-asset studies.

Set your sessions and time zones — defaults approximate APAC, EU, and US hours, but you can align them to exchange times or your workflow.

Choose calculation modes — Percent vs Points for return, Range vs ATR for volatility. Points are convenient for futures and fixed-tick assets, Percent is comparable across symbols.

Decide the lookback — more sessions smooths lines and stats; fewer sessions makes the tool more reactive.

Toggle analytics — add volatility, volume, drawdown, streaks, Sharpe-like ratio, rolling averages, and the correlation table as needed.

Why session attribution helps

Different sessions are driven by different flows. Asia often sets the overnight tone, Europe adds liquidity and direction changes, and the US session can dominate range expansion. Separating contributions by session helps you:

Identify which session has been the main driver of net trend.

Measure whether volatility or volume is concentrated in a specific window.

See if one session’s gains are consistently given back in another.

Adapt tactics: fade during a mean-reverting session, press during a trending session.

Reading the tables

Cumulative % — sum of session returns over the lookback. The sign and slope tell you who is carrying the move.

Avg Return % and Positive Sessions % — direction and hit rate. A low average but high hit rate implies many small moves; the reverse implies occasional big swings.

Avg Volatility % — typical intrabars range for that session. Compare with Avg Return to judge efficiency.

Return/Vol Ratio — return per unit of volatility. Higher is better for stability.

Max Drawdown % — worst cumulative give-back within the lookback. A quick way to spot riskiness by session.

Current Streak — consecutive up or down sessions. Useful for mean-reversion or regime awareness.

Rolling Avg % — short-window drift indicator to catch recent turnarounds.

Correlation matrix — green clusters indicate sessions tending to move together; red indicates offsetting behavior.

Settings overview

Basic

Number of Sessions — how many recent days to include.

Custom Instrument — analyze another ticker while staying on your current chart.

Session Configuration and Times

Enable or hide APAC, EU, US rows.

Set hours per session and the specific time zone for each.

Calculation Methods

Return Calculation — Percent or Points.

Volatility Calculation — Range or ATR; ATR Length when applicable.

Advanced Analytics

Correlation, Drawdown, Momentum, Sharpe-like ratio, Rolling Statistics, Rolling Period.

Display Options and Colors

Show Statistics Table and its position.

Toggle columns for Volatility and Volume.

Pick individual colors for each session line and row accents.

Common applications

Session bias mapping — find which window tends to trend in your market and plan exposure accordingly.

Strategy scheduling — allocate attention or risk to the session with the best return-to-vol ratio.

News and macro awareness — see if correlation rises around central bank cycles or major data releases.

Cross-asset monitoring — set the Custom Instrument to a driver (index future, DXY, yields) to see if your symbol reacts in a particular session.

Notes

This indicator works on intraday charts, since sessions are defined within a day. If you change session clocks or time zones, give the script a few bars to accumulate fresh rows. Percent vs Points and Range vs ATR choices affect comparability across assets, so be consistent when comparing symbols.

Session context is one of the simplest ways to explain a messy tape. By separating the day into three windows and scoring each one on return, volatility, and consistency, this tool shows not just where price ended up but when and how it got there. Use the cumulative lines to spot the steady driver, read the table to judge quality and risk, and glance at the heatmap to learn whether the sessions are amplifying or canceling one another. Adjust the hours to your market and let the data tell you which session deserves your focus.

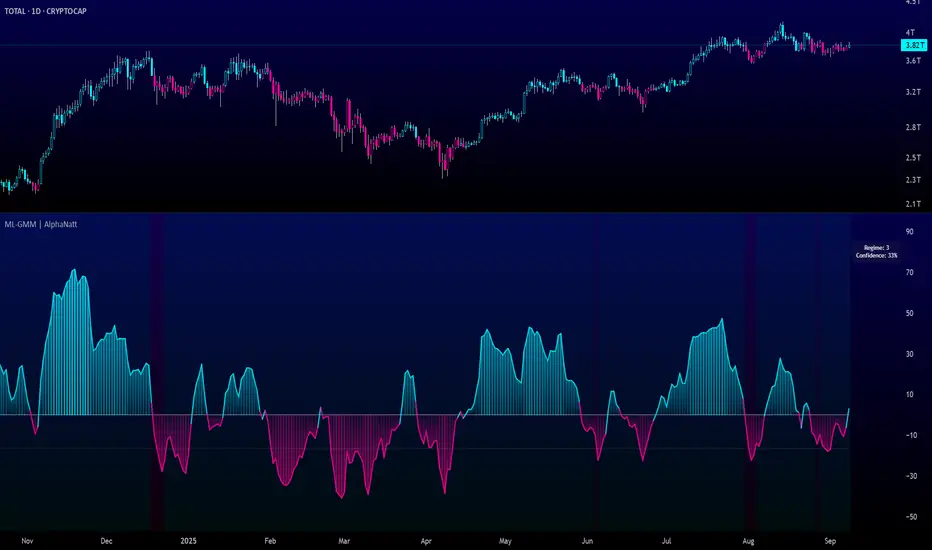

Machine Learning Gaussian Mixture Model | AlphaNattMachine Learning Gaussian Mixture Model | AlphaNatt

A revolutionary oscillator that uses Gaussian Mixture Models (GMM) with unsupervised machine learning to identify market regimes and automatically adapt momentum calculations - bringing statistical pattern recognition techniques to trading.

"Markets don't follow a single distribution - they're a mixture of different regimes. This oscillator identifies which regime we're in and adapts accordingly."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🤖 THE MACHINE LEARNING

Gaussian Mixture Models (GMM):

Unlike K-means clustering which assigns hard boundaries, GMM uses probabilistic clustering :

Models data as coming from multiple Gaussian distributions

Each market regime is a different Gaussian component

Provides probability of belonging to each regime

More sophisticated than simple clustering

Expectation-Maximization Algorithm:

The indicator continuously learns and adapts using the E-M algorithm:

E-step: Calculate probability of current market belonging to each regime

M-step: Update regime parameters based on new data

Continuous learning without repainting

Adapts to changing market conditions

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🎯 THREE MARKET REGIMES

The GMM identifies three distinct market states:

Regime 1 - Low Volatility:

Quiet, ranging markets

Uses RSI-based momentum calculation

Reduces false signals in choppy conditions

Background: Pink tint

Regime 2 - Normal Market:

Standard trending conditions

Uses Rate of Change momentum

Balanced sensitivity

Background: Gray tint

Regime 3 - High Volatility:

Strong trends or volatility events

Uses Z-score based momentum

Captures extreme moves

Background: Cyan tint

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💡 KEY INNOVATIONS

1. Probabilistic Regime Detection:

Instead of binary regime assignment, provides probabilities:

30% Regime 1, 60% Regime 2, 10% Regime 3

Smooth transitions between regimes

No sudden indicator jumps

2. Weighted Momentum Calculation:

Combines three different momentum formulas

Weights based on regime probabilities

Automatically adapts to market conditions

3. Confidence Indicator:

Shows how certain the model is (white line)

High confidence = strong regime identification

Low confidence = transitional market state

Line transparency changes with confidence

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚙️ PARAMETER OPTIMIZATION

Training Period (50-500):

50-100: Quick adaptation to recent conditions

100: Balanced (default)

200-500: Stable regime identification

Number of Components (2-5):

2: Simple bull/bear regimes

3: Low/Normal/High volatility (default)

4-5: More granular regime detection

Learning Rate (0.1-1.0):

0.1-0.3: Slow, stable learning

0.3: Balanced (default)

0.5-1.0: Fast adaptation

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📊 TRADING STRATEGIES

Visual Signals:

Cyan gradient: Bullish momentum

Magenta gradient: Bearish momentum

Background color: Current regime

Confidence line: Model certainty

1. Regime-Based Trading:

Regime 1 (pink): Expect mean reversion

Regime 2 (gray): Standard trend following

Regime 3 (cyan): Strong momentum trades

2. Confidence-Filtered Signals:

Only trade when confidence > 70%

High confidence = clearer market state

Avoid transitions (low confidence)

3. Adaptive Position Sizing:

Regime 1: Smaller positions (choppy)

Regime 2: Normal positions

Regime 3: Larger positions (trending)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🚀 ADVANTAGES OVER OTHER ML INDICATORS

vs K-Means Clustering:

Soft clustering (probabilities) vs hard boundaries

Captures uncertainty and transitions

More mathematically robust

vs KNN (K-Nearest Neighbors):

Unsupervised learning (no historical labels needed)

Continuous adaptation

Lower computational complexity

vs Neural Networks:

Interpretable (know what each regime means)

No overfitting issues

Works with limited data

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📈 PERFORMANCE CHARACTERISTICS

Best Market Conditions:

Markets with clear regime shifts

Volatile to trending transitions

Multi-timeframe analysis

Cryptocurrency markets (high regime variation)

Key Strengths:

Automatically adapts to market changes

No manual parameter adjustment needed

Smooth transitions between regimes

Probabilistic confidence measure

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🔬 TECHNICAL BACKGROUND

Gaussian Mixture Models are used extensively in:

Speech recognition (Google Assistant)

Computer vision (facial recognition)

Astronomy (galaxy classification)

Genomics (gene expression analysis)

Finance (risk modeling at investment banks)

The E-M algorithm was developed at Stanford in 1977 and is one of the most important algorithms in unsupervised machine learning.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💡 PRO TIPS

Watch regime transitions: Best opportunities often occur when regimes change

Combine with volume: High volume + regime change = strong signal

Use confidence filter: Avoid low confidence periods

Multi-timeframe: Compare regimes across timeframes

Adjust position size: Scale based on identified regime

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚠️ IMPORTANT NOTES

Machine learning adapts but doesn't predict the future

Best used with other confirmation indicators

Allow time for model to learn (100+ bars)

Not financial advice - educational purposes

Backtest thoroughly on your instruments

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🏆 CONCLUSION

The GMM Momentum Oscillator brings institutional-grade machine learning to retail trading. By identifying market regimes probabilistically and adapting momentum calculations accordingly, it provides:

Automatic adaptation to market conditions

Clear regime identification with confidence levels

Smooth, professional signal generation

True unsupervised machine learning

This isn't just another indicator with "ML" in the name - it's a genuine implementation of Gaussian Mixture Models with the Expectation-Maximization algorithm, the same technology used in:

Google's speech recognition

Tesla's computer vision

NASA's data analysis

Wall Street risk models

"Let the machine learn the market regimes. Trade with statistical confidence."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Developed by AlphaNatt | Machine Learning Trading Systems

Version: 1.0

Algorithm: Gaussian Mixture Model with E-M

Classification: Unsupervised Learning Oscillator

Not financial advice. Always DYOR.

MK_OSFT-Multi-Timeframe MA Dashboard & Smart Alerts-v2📊 Multi-Timeframe MA Dashboard & Smart Alerts v2.0

Transform your trading with the ultimate moving average monitoring system that tracks up to 8 different MA configurations across multiple timeframes simultaneously.

🎯 What This Indicator Does

This advanced dashboard eliminates the need to constantly switch between timeframes by displaying all your critical moving averages on a single chart. Whether you're scalping on 5-minute charts or swing trading on daily timeframes, you'll instantly see the big picture.

⭐ Key Features

📈 Multi-Timeframe Moving Averages

Monitor up to **8 different MA configurations** simultaneously

Support for **SMA and EMA** across 6 timeframes (5m, 15m, 1h, 4h, Daily, Weekly)

Each MA fully customizable: length, color, alert settings, and visibility

Smart visual representation with labeled horizontal lines and connecting plots

🚨 Intelligent Alert System

Cross-over/Cross-under alerts for price vs MA interactions

Three alert modes : No alerts, Once only, or Once per bar close

Smart batching system prevents alert spam during volatile periods

Queue management with 3-second delays between alerts for optimal performance

Easy alert reset functionality for "once only" alerts

📊 Real-Time Information Dashboard

Live countdown timers showing time remaining until each timeframe closes

Color-coded progress bars with gradient visualization (green → yellow → orange → red)

Instant cross-over detection with up/down arrow indicators

Price vs MA relationship clearly displayed (above/below coloring)

🎨 Professional Visualization

Anti-overlap technology prevents labels from clustering

Customizable label positioning and sizing options

Drawing order control (larger timeframes first/last)

Connecting lines link current price to MA values

Status line integration for quick value reference

💡 Perfect For

Multi-timeframe traders [/b who need complete market context

Trend followers monitoring key MA levels across timeframes

Breakout traders waiting for price to cross critical moving averages

Risk managers using MAs as dynamic support/resistance levels

Anyone wanting organized, clutter-free MA monitoring

⚙️ Highly Configurable

Moving Average Settings

Individual enable/disable for each of 8 MA slots

Flexible timeframe selection : 5m, 15m, 1h, 4h, Daily, Weekly

MA type choice : SMA or EMA for each configuration

Custom lengths from 1 to any desired period

Color customization for each MA line and label

Alert Management

Per-MA alert configuration : Choose which MAs trigger alerts

Source selection : Current bar vs last confirmed bar calculations

Frequency control : Prevent over-alerting with smart queuing

Reset functionality : Easily reactivate "fired" once-only alerts

Display Options

Table positioning : Top-right, bottom-left, or bottom-right

Label styling : Size, offset, and gap control

Line customization : Width and extension options

Timezone adjustment : Align timestamps with your local time

🔧 Technical Excellence

Optimized performance with efficient array management and single-pass calculations

Real-time vs historical mode handling for accurate backtesting

Memory-efficient label and line management prevents accumulation

Robust error handling and edge case management

Clean, well-documented code following Pine Script best practices

📋 How to Use

Add to chart and configure your desired MA combinations

Set alert preferences for each MA (none/once/per bar)

Create TradingView alert using "Any alert() function calls"

Monitor the dashboard for cross-over signals and timeframe progress

Use the info table to track all MA values and alert statuses at a glance

🎓 Educational Value

This indicator serves as an excellent educational tool for understanding:

Multi-timeframe analysis principles

Moving average confluence and divergence

Alert system design and management

Professional indicator development techniques

---

Transform your trading workflow with this professional-grade multi-timeframe MA monitoring system. No more chart hopping - get the complete moving average picture in one powerful dashboard!

© MK_OSF_TRADING | Pine Script v6 | Mozilla Public License 2.0

Multi-TF Trend Table (Configurable)1) What this tool does (in one minute)

A compact, multi‑timeframe dashboard that stacks eight timeframes and tells you:

Trend (fast MA vs slow MA)

Where price sits relative to those MAs

How far price is from the fast MA in ATR terms

MA slope (rising, falling, flat)

Stochastic %K (with overbought/oversold heat)

MACD momentum (up or down)

A single score (0%–100%) per timeframe

Alignment tick when trend, structure, slope and momentum all agree

Use it to:

Frame bias top‑down (M→W→D→…→15m)

Time entries on your execution timeframe when the higher‑TF stack is aligned

Avoid counter‑trend traps when the table is mixed

2) Table anatomy (each column explained)

The table renders 9 columns × 8 rows (one row per timeframe label you define).

TF — The label you chose for that row (e.g., Month, Week, 4H). Cosmetic; helps you read the stack.

Trend — Arrow from fast MA vs slow MA: ↑ if fastMA > slowMA (up‑trend), ↓ otherwise (down‑trend). Cell is green for up, red for down.

Price Pos — One‑character structure cue:

🔼 if price is above both fast and slow MAs (bullish structure)

🔽 if price is below both (bearish structure)

– otherwise (between MAs / mixed)

MA Dist — Distance of price from the fast MA measured in ATR multiples:

XS < S < M < L < XL according to your thresholds (see §3.3). Useful for judging stretch/mean‑reversion risk and stop sizing.

MA Slope — The fast MA one‑bar slope:

↑ if fastMA - fastMA > 0

↓ if < 0

→ if = 0

Stoch %K — Rounded %K value (default 14‑1‑3). Background highlights when it aligns with the trend:

Green heat when trend up and %K ≤ oversold

Red heat when trend down and %K ≥ overbought Tooltip shows K and D values precisely.

Trend % — Composite score (0–100%), the dashboard’s confidence for that timeframe:

+20 if trendUp (fast>slow)

+20 if fast MA slope > 0

+20 if MACD up (signal definition in §2.8)

+20 if price above fast MA

+20 if price above slow MA

Background colours:

≥80 lime (strong alignment)

≥60 green (good)

≥40 orange (mixed)

<40 grey (weak/contrary)

MACD — 🟢 if EMA(12)−EMA(26) > its EMA(9), else 🔴. It’s a simple “momentum up/down” proxy.

Align — ✔ when everything is in gear for that trend direction:

For up: trendUp and price above both MAs and slope>0 and MACD up

For down: trendDown and price below both MAs and slope<0 and MACD down Tooltip spells this out.

3) Settings & how to tune them

3.1 Timeframes (TF1–TF8)

Inputs: TF1..TF8 hold the resolution strings used by request.security().

Defaults: M, W, D, 720, 480, 240, 60, 15 with display labels Month, Week, Day, 12H, 8H, 4H, 1H, 15m.

Tips

Keep a top‑down funnel (e.g., Month→Week→Day→H4→H1→M15) so you can cascade bias into entries.

If you scalp, consider D, 240, 120, 60, 30, 15, 5, 1.

Crypto weekends: consider 2D in place of W to reflect continuous trading.

3.2 Moving Average (MA) group

Type: EMA, SMA, WMA, RMA, HMA. Changes both fast & slow MA computations everywhere.

Fast Length: default 20. Shorten for snappier trend/slope & tighter “price above fast” signals.

Slow Length: default 200. Controls the structural trend and part of the score.

When to change

Swing FX/equities: EMA 20/200 is a solid baseline.

Mean‑reversion style: consider SMA 20/100 so trend flips slower.

Crypto/indices momentum: HMA 21 / EMA 200 will read slope more responsively.

3.3 ATR / Distance group

ATR Length: default 14; longer makes distance less jumpy.

XS/S/M/L thresholds: define the labels in column MA Dist. They are compared to |close − fastMA| / ATR.

Defaults: XS 0.25×, S 0.75×, M 1.5×, L 2.5×; anything ≥L is XL.

Usage

Entries late in a move often occur at L/XL; consider waiting for a pullback unless you are trading breakouts.

For stops, an initial SL around 0.75–1.5 ATR from fast MA often sits behind nearby noise; use your plan.

3.4 Stochastic group

%K Length / Smoothing / %D Smoothing: defaults 14 / 1 / 3.

Overbought / Oversold: defaults 70 / 30 (adjust to 80/20 for trendier assets).

Heat logic (column Stoch %K): highlights when a pullback aligns with the dominant trend (oversold in an uptrend, overbought in a downtrend).

3.5 View

Full Screen Table Mode: centers and enlarges the table (position.middle_center). Great for clean screenshots or multi‑monitor setups.

4) Signal logic (how each datapoint is computed)

Per‑TF data (via a single request.security()):

fastMA, slowMA → based on your MA Type and lengths

%K, %D → Stoch(High,Low,Close,kLen) smoothed by kSmooth, then %D smoothed by dSmooth

close, ATR(atrLen) → for structure and distance

MACD up → (EMA12−EMA26) > EMA9(EMA12−EMA26)

fastMA_prev → yesterday/previous‑bar fast MA for slope

TrendUp → fastMA > slowMA

Price Position → compares close to both MAs

MA Distance Label → thresholds on abs(close − fastMA)/ATR

Slope → fastMA − fastMA

Score (0–100) → sum of the five 20‑point checks listed in §2.7

Align tick → conjunction of trend, price vs both MAs, slope and MACD (see §2.9)

Important behaviour

HTF values are sampled at the execution chart’s bar close using Pine v6 defaults (no lookahead). So the daily row updates only when a daily bar actually closes.

5) How to trade with it (playbooks)

The table is a framework. Entries/exits still follow your plan (e.g., S/D zones, price action, risk rules). Use the table to know when to be aggressive vs patient.

Playbook A — Trend continuation (pullback entry)

Look for Align ✔ on your anchor TFs (e.g., Week+Day both ≥80 and green, Trend ↑, MACD 🟢).

On your execution TF (e.g., H1/H4), wait for Stoch heat with the trend (oversold in uptrend or overbought in downtrend), and MA Dist not at XL.

Enter on your trigger (break of pullback high/low, engulfing, retest of fast MA, or S/D first touch per your plan).

Risk: consider ATR‑based SL beyond structure; size so 0.25–0.5% account risk fits your rules.

Trail or scale at M/L distances or when score deteriorates (<60).

Playbook B — Breakout with confirmation

Mixed stack turns into broad green: Trend % jumps to ≥80 on Day and H4; MACD flips 🟢.

Price Pos shows 🔼 across H4/H1 (above both MAs). Slope arrows ↑.

Enter on the first clean base‑break with volume/impulse; avoid if MA Dist already XL.

Playbook C — Mean‑reversion fade (advanced)

Use only when higher TFs are not aligned and the row you trade shows XL distance against the higher‑TF context. Take quick targets back to fast MA. Lower win‑rate, faster management.

Playbook D — Top‑down filter for Supply/Demand strategy

Trade first retests only in the direction where anchor TFs (Week/Day) have Align ✔ and Trend % ≥60. Skip counter‑trend zones when the stack is red/green against you.

6) Reading examples

Strong bullish stack

Week: ↑, 🔼, S/M, slope ↑, %K=32 (green heat), Trend 100%, MACD 🟢, Align ✔

Day: ↑, 🔼, XS/S, slope ↑, %K=45, Trend 80%, MACD 🟢, Align ✔

Action: Look for H4/H1 pullback into demand or fast MA; buy continuation.

Late‑stage thrust

H1: ↑, 🔼, XL, slope ↑, %K=88

Day/H4: only 60–80%

Action: Likely overextended on H1; wait for mean reversion or multi‑TF alignment before chasing.

Bearish transition

Day flips from 60%→40%, Trend ↓, MACD turns 🔴, Price Pos “–” (between MAs)

Action: Stand aside for longs; watch for lower‑high + Align ✔ on H4/H1 to join shorts.

7) Practical tips & pitfalls

HTF closure: Don’t assume a daily row changed mid‑day; it won’t settle until the daily bar closes. For intraday anticipation, watch H4/H1 rows.

MA Type consistency: Changing MA Type changes slope/structure everywhere. If you compare screenshots, keep the same type.

ATR thresholds: Calibrate per asset class. FX may suit defaults; indices/crypto might need wider S/M/L.

Score ≠ signal: 100% does not mean “must buy now.” It means the environment is favourable. Still execute your trigger.

Mixed stacks: When rows disagree, reduce size or skip. The tool is telling you the market lacks consensus.

8) Customisation ideas

Timeframe presets: Save layouts (e.g., Swing, Intraday, Scalper) as indicator templates in TradingView.

Alternative momentum: Replace the MACD condition with RSI(>50/<50) if desired (would require code edit).

Alerts: You can add alert conditions for (a) Align ✔ changes, (b) Trend % crossing 60/80, (c) Stoch heat events. (Not shipped in this script, but easy to add.)

9) FAQ

Q: Why do I sometimes see a dash in Price Pos? A: Price is between fast and slow MAs. Structure is mixed; seek clarity before acting.

Q: Does it repaint? A: No, higher‑TF values update on the close of their own bars (standard request.security behaviour without lookahead). Intra‑bar they can fluctuate; decisions should be made at your bar close per your plan.

Q: Which columns matter most? A: For trend‑following: Trend, Price Pos, Slope, MACD, then Stoch heat for entries. The Score summarises, and Align enforces discipline.

Q: How do I integrate with ATR‑based risk? A: Use the MA Dist label to avoid chasing at extremes and to size stops in ATR terms (e.g., SL behind structure at ~1–1.5 ATR).

Dual Volume Profiles: Session + Rolling (Range Delineation)Dual Volume Profiles: Session + Rolling (Range Delineation)

INTRO

This is a probability-centric take on volume profile. I treat the volume histogram as an empirical PDF over price, updated in real time, which makes multi-modality (multiple acceptance basins) explicit rather than assumed away. The immediate benefit is operational: if we can read the shape of the distribution, we can infer likely reversion levels (POC), acceptance boundaries (VAH/VAL), and low-friction corridors (LVNs).

My working hypothesis is that what traders often label “fat tails” or “power-law behavior” at short horizons is frequently a tail-conditioned view of a higher-level Gaussian regime. In other words, child distributions (shorter periodicities) sit within parent distributions (longer periodicities); when price operates in the parent’s tail, the child regime looks heavy-tailed without being fundamentally non-Gaussian. This is consistent with a hierarchical/mixture view and with the spirit of the central limit theorem—Gaussian structure emerges at aggregate scales, while local scales can look non-Gaussian due to nesting and conditioning.

This indicator operationalizes that view by plotting two nested empirical PDFs: a rolling (local) profile and a session-anchored profile. Their confluence makes ranges explicit and turns “regime” into something you can see. For additional nesting, run multiple instances with different lookbacks. When using the default settings combined with a separate daily VP, you effectively get three nested distributions (local → session → daily) on the chart.

This indicator plots two nested distributions side-by-side:

Rolling (Local) Profile — short-window, prorated histogram that “breathes” with price and maps the immediate auction.

Session Anchored Profile — cumulative distribution since the current session start (Premkt → RTH → AH anchoring), revealing the parent regime.

Use their confluence to identify range floors/ceilings, mean-reversion magnets, and low-volume “air pockets” for fast traverses.

What it shows

POC (dashed): central tendency / “magnet” (highest-volume bin).

VAH & VAL (solid): acceptance boundaries enclosing an exact Value Area % around each profile’s POC.

Volume histograms:

Rolling can auto-color by buy/sell dominance over the lookback (green = buying ≥ selling, red = selling > buying).

Session uses a fixed style (blue by default).

Session anchoring (exchange timezone):

Premarket → anchors at 00:00 (midnight).

RTH → anchors at 09:30.

After-hours → anchors at 16:00.

Session display span:

Session Max Span (bars) = 0 → draw from session start → now (anchored).

> 0 → draw a rolling window N bars back → now, while still measuring all volume since session start.

Why it’s useful

Think in terms of nested probability distributions: the rolling node is your local Gaussian; the session node is its parent.

VA↔VA overlap ≈ strong range boundary.

POC↔POC alignment ≈ reliable mean-reversion target.

LVNs (gaps) ≈ low-friction corridors—expect quick moves to the next node.

Quick start

Add to chart (great on 5–10s, 15–60s, 1–5m).

Start with: bins = 240, vaPct = 0.68, barsBack = 60.

Watch for:

First test & rejection at overlapping VALs/VAHs → fade back toward POC.

Acceptance beyond VA (several closes + growing outer-bin mass) → traverse to the next node.

Inputs (detailed)

General

Lookback Bars (Rolling)

Count of most-recent bars for the rolling/local histogram. Larger = smoother node that shifts slower; smaller = more reactive, “breathing” profile.

• Typical: 40–80 on 5–10s charts; 60–120 on 1–5m.

• If you increase this but keep Number of Bins fixed, each bin aggregates more volume (coarser bins).

Number of Bins

Vertical resolution (price buckets) for both rolling and session histograms. Higher = finer detail and crisper LVNs, but more line objects (closer to platform limits).

• Typical: 120–240 on 5–10s; 80–160 on 1–5m.

• If you hit performance or object limits, reduce this first.

Value Area %

Exact central coverage for VAH/VAL around POC. Computed empirically from the histogram (no Gaussian assumption): the algorithm expands from POC outward until the chosen % is enclosed.

• Common: 0.68 (≈“1σ-like”), 0.70 for slightly wider core.

• Smaller = tighter VA (more breakout flags). Larger = wider VA (more reversion bias).

Max Local Profile Width (px)

Horizontal length (in pixels) of the rolling bars/lines and its VA/POC overlays. Visual only (does not affect calculations).

Session Settings

RTH Start/End (exchange tz)

Defines the current session anchor (Premkt=00:00, RTH=your start, AH=your end). The session histogram always measures from the most recent session start and resets at each boundary.

Session Max Span (bars, 0 = full session)

Display window for session drawings (POC/VA/Histogram).

• 0 → draw from session start → now (anchored).

• > 0 → draw N bars back → now (rolling look), while still measuring all volume since session start.

This keeps the “parent” distribution measurable while letting the display track current action.

Local (Rolling) — Visibility

Show Local Profile Bars / POC / VAH & VAL

Toggle each overlay independently. If you approach object limits, disable bars first (POC/VA lines are lighter).

Local (Rolling) — Colors & Widths

Color by Buy/Sell Dominance

Fast uptick/downtick proxy over the rolling window (close vs open):

• Buying ≥ Selling → Bullish Color (default lime).

• Selling > Buying → Bearish Color (default red).

This color drives local bars, local POC, and local VA lines.

• Disable to use fixed Bars Color / POC Color / VA Lines Color.

Bars Transparency (0–100) — alpha for the local histogram (higher = lighter).

Bars Line Width (thickness) — draw thin-line profiles or chunky blocks.

POC Line Width / VA Lines Width — overlay thickness. POC is dashed, VAH/VAL solid by design.

Session — Visibility

Show Session Profile Bars / POC / VAH & VAL

Independent toggles for the session layer.

Session — Colors & Widths

Bars/POC/VA Colors & Line Widths

Fixed palette by design (default blue). These do not change with buy/sell dominance.

• Use transparency and width to make the parent profile prominent or subtle.

• Prefer minimal? Hide session bars; keep only session VA/POC.

Reading the signals (detailed playbook)

Core definitions

POC — highest-volume bin (fair price “magnet”).

VAH/VAL — upper/lower bounds enclosing your Value Area % around POC.

Node — contiguous block of high-volume bins (acceptance).

LVN — low-volume gap between nodes (low friction path).

Rejection vs Acceptance (practical rule)

Rejection at VA edge: 0–1 closes beyond VA and no persistent growth in outer bins.

Acceptance beyond VA: ≥3 closes beyond VA and outer-bin mass grows (e.g., added volume beyond the VA edge ≥ 5–10% of node volume over the last N bars). Treat acceptance as regime change.

Confluence scores (make boundary/target quality objective)

VA overlap strength (range boundary):

C_VA = 1 − |VA_edge_local − VA_edge_session| / ATR(n)

Values near 1.0 = tight overlap (stronger boundary).

Use: if C_VA ≥ 0.6–0.8, treat as high-quality fade zone.

POC alignment (magnet quality):

C_POC = 1 − |POC_local − POC_session| / ATR(n)

Higher C_POC = greater chance a rotation completes to that fair price.

(You can estimate these by eye.)

Setups

1) Range Fade at VA Confluence (mean reversion)

Context: Local VAL/VAH near Session VAL/VAH (tight overlap), clear node, local color not screaming trend (or flips to your side).

Entry: First test & rejection at the overlapped band (wick through ok; prefer close back inside).

Stop: A tick/pip beyond the wider of the two VA edges or beyond the nearest LVN, a small buffer zone can be used to judge whether price is truly rejecting a VAL/VAH or simply probing.

Targets: T1 node mid; T2 POC (size up when C_POC is high).

Flip: If acceptance (rule above) prints, flip bias or stand down.

2) LVN Traverse (continuation)

Context: Price exits VA and enters an LVN with acceptance and growing outer-bin volume.

Entry: Aggressive—first close into LVN; Conservative—retest of the VA edge from the far side (“kiss goodbye”).

Stop: Back inside the prior VA.

Targets: Next node’s VA edge or POC (edge = faster exits; POC = fuller rotations).

Note: Flatter VA edge (shallower curvature) tends to breach more easily.

3) POC→POC Magnet Trade (rotation completion)

Context: Local POC ≈ Session POC (high C_POC).

Entry: Fade a VA touch or pullback inside node, aiming toward the shared POC.

Stop: Past the opposite VA edge or LVN beyond.

Target: The shared POC; optional runner to opposite VA if the node is broad and time-of-day is supportive.

4) Failed Break (Reversion Snap-back)

Context: Push beyond VA fails acceptance (re-enters VA, outer-bin growth stalls/shrinks).

Entry: On the re-entry close, back toward POC.

Stop/Target: Stop just beyond the failed VA; target POC, then opposite VA if momentum persists.

How to read color & shape

Local color = most recent sentiment:

Green = buying ≥ selling; Red = selling > buying (over the rolling window). Treat as context, not a standalone signal. A green local node under a blue session VAH can still be a fade if the parent says “over-valued.”

Shape tells friction:

Fat nodes → rotation-friendly (fade edges).

Sharp LVN gaps → traversal-friendly (momentum continuation).

Time-of-day intuition

Right after session anchor (e.g., RTH 09:30): Session profile is young and moves quickly—treat confluence cautiously.

Mid-session: Cleanest behavior for rotations.

Close / news: Expect more traverses and POC migrations; tighten risk or switch playbooks.

Risk & execution guidance

Use tight, mechanical stops at/just beyond VA or LVN. If you need wide stops to survive noise, your entry is late or the node is unstable.

On micro-timeframes, account for fees & slippage—aim for targets paying ≥2–3× average cost.

If acceptance prints, don’t fight it—flip, reduce size, or stand aside.

Suggested presets

Scalp (5–10s): bins 120–240, barsBack 40–80, vaPct 0.68–0.70, local bars thin (small bar width).

Intraday (1–5m): bins 80–160, barsBack 60–120, vaPct 0.68–0.75, session bars more visible for parent context.

Performance & limits

Reuses line objects to stay under TradingView’s max_lines_count.

Very large bins × multiple overlays can still hit limits—use visibility toggles (hide bars first).

Session drawings use time-based coordinates to avoid “bar index too far” errors.

Known nuances

Rolling buy/sell dominance uses a simple uptick/downtick proxy (close vs open). It’s fast and practical, but it’s not a full tape classifier.

VA boundaries are computed from the empirical histogram—no Gaussian assumption.

This script does not calculate the full daily volume profile. Several other tools already provide that, including TradingView’s built-in Volume Profile indicators. Instead, this indicator focuses on pairing a rolling, short-term volume distribution with a session-wide distribution to make ranges more explicit. It is designed to supplement your use of standard or periodic volume profiles, not replace them. Think of it as a magnifying lens that helps you see where local structure aligns with the broader session.

How to trade it (TL;DR)

Fade overlapping VA bands on first rejection → target POC.

Continue through LVN on acceptance beyond VA → target next node’s VA/POC.

Respect acceptance: ≥3 closes beyond VA + growing outer-bin volume = regime change.

FAQ

Q: Why 68% Value Area?

A: It mirrors the “~1σ” idea, but we compute it exactly from empirical volume, not by assuming a normal distribution.

Q: Why are my profiles thin lines?

A: Increase Bars Line Width for chunkier blocks; reduce for fine, thin-line profiles.

Q: Session bars don’t reach session start—why?

A: Set Session Max Span (bars) = 0 for full anchoring; any positive value draws a rolling window while still measuring from session start.

Changelog (v1.0)

Dual profiles: Rolling + Session with independent POC/VA lines.

Session anchoring (Premkt/RTH/AH) with optional rolling display span.

Dynamic coloring for the rolling profile (buying vs selling).

Fully modular toggles + per-feature colors/widths.

Thin-line rendering via bar line width.

Awesome Indicator# Moving Average Ribbon with ADR% - Complete Trading Indicator

## Overview

The **Moving Average Ribbon with ADR%** is a comprehensive technical analysis indicator that combines multiple analytical tools to provide traders with a complete picture of price trends, volatility, relative performance, and position sizing guidance. This multi-faceted indicator is designed for both swing and positional traders looking for data-driven entry and exit signals.

## Key Components

### 1. Moving Average Ribbon System

- **4 Customizable Moving Averages** with default periods: 13, 21, 55, and 189

- **Multiple MA Types**: SMA, EMA, SMMA (RMA), WMA, VWMA

- **Color-coded visualization** for easy trend identification

- **Flexible configuration** allowing users to modify periods, types, and colors

### 2. Average Daily Range Percentage (ADR%)

- Calculates the average daily volatility as a percentage

- Uses a 20-period simple moving average of (High/Low - 1) * 100

- Helps traders understand the stock's typical daily movement range

- Essential for position sizing and stop-loss placement

### 3. Volume Analysis (Up/Down Ratio)

- Analyzes volume distribution over the last 55 periods

- Calculates the ratio of volume on up days vs down days

- Provides insight into buying vs selling pressure

- Values > 1 indicate more buying volume, < 1 indicate more selling volume

### 4. Absolute Relative Strength (ARS)

- **Dual timeframe analysis** with customizable reference points

- **High ARS**: Performance relative to benchmark from a high reference point (default: Sep 27, 2024)

- **Low ARS**: Performance relative to benchmark from a low reference point (default: Apr 7, 2025)

- Uses NSE:NIFTY as default comparison symbol

- Color-coded display: Green for outperformance, Red for underperformance

### 5. Relative Performance Table

- **5 timeframes**: 1 Week, 1 Month, 3 Months, 6 Months, 1 Year

- Shows stock performance **relative to benchmark index**

- Formula: (Stock Return - Index Return) for each period

- **Color coding**:

- Lime: >5% outperformance

- Yellow: -5% to +5% relative performance

- Red: <-5% underperformance

### 6. Dynamic Position Allocation System

- **6-factor scoring system** based on price vs EMAs (21, 55, 189)

- Evaluates:

- Price above/below each EMA

- EMA alignment (21>55, 55>189, 21>189)

- **Allocation recommendations**:

- 100% allocation: Score = 6 (all bullish signals)

- 75% allocation: Score = 4

- 50% allocation: Score = 2

- 25% allocation: Score = 0

- 0% allocation: Score = -2, -4, -6 (bearish signals)

## Display Tables

### Performance Table (Top Right)

Shows relative performance vs benchmark across multiple timeframes with intuitive color coding for quick assessment.

### Metrics Table (Bottom Right)

Displays key statistics:

- **ADR%**: Average Daily Range percentage

- **U/D**: Up/Down volume ratio

- **Allocation%**: Recommended position size

- **High ARS%**: Relative strength from high reference

- **Low ARS%**: Relative strength from low reference

## How to Use This Indicator

### For Trend Analysis

1. **Moving Average Ribbon**: Look for price above ascending MAs for bullish trends

2. **MA Alignment**: Bullish when shorter MAs are above longer MAs

3. **Color coordination**: Use consistent color scheme for quick visual analysis

### For Entry/Exit Timing

1. **Performance Table**: Enter when showing consistent outperformance across timeframes

2. **Volume Analysis**: Confirm entries with U/D ratio > 1.5 for strong buying

3. **ARS Values**: Look for positive ARS readings for relative strength confirmation

### For Position Sizing

1. **Allocation System**: Use the recommended allocation percentage

2. **ADR% Consideration**: Adjust position size based on volatility

3. **Risk Management**: Lower allocation in high ADR% stocks

### For Risk Management

1. **ADR% for Stop Loss**: Set stops at 1-2x ADR% below entry

2. **Relative Performance**: Reduce positions when consistently underperforming

3. **Volume Confirmation**: Be cautious when U/D ratio deteriorates

## Best Practices

### Timeframe Recommendations

- **Intraday**: Use lower MA periods (5, 13, 21, 55)

- **Swing Trading**: Default settings work well (13, 21, 55, 189)

- **Position Trading**: Consider higher periods (21, 50, 100, 200)

### Market Conditions

- **Trending Markets**: Focus on MA alignment and relative performance

- **Sideways Markets**: Rely more on ADR% for range trading

- **Volatile Markets**: Reduce allocation percentage regardless of signals

### Customization Tips

1. Adjust reference dates for ARS calculation based on significant market events

2. Change comparison symbol to sector-specific indices for better relative analysis

3. Modify MA periods based on your trading style and market characteristics

## Technical Specifications

- **Version**: Pine Script v6

- **Overlay**: Yes (plots on price chart)

- **Real-time Updates**: Yes

- **Data Requirements**: Minimum 252 bars for complete calculations

- **Compatible Timeframes**: All standard timeframes

## Limitations

- Performance calculations require sufficient historical data

- ARS calculations depend on selected reference dates

- Volume analysis may be less reliable in low-volume stocks

- Relative performance is only as good as the chosen benchmark

This indicator is designed to provide a comprehensive analysis framework rather than simple buy/sell signals. It's recommended to use this in conjunction with your overall trading strategy and risk management rules.

MTF Dashboard 9 Timeframes + Signals# MTF Dashboard Pro - Multi-Timeframe Confluence Analysis System

## WHAT THIS SCRIPT DOES

This script creates a comprehensive dashboard that simultaneously analyzes market conditions across 9 different timeframes (1m, 5m, 15m, 30m, 1H, 4H, Daily, Weekly, Monthly) using a proprietary confluence scoring methodology. Unlike simple multi-timeframe displays that show individual indicators separately, this script combines trend analysis, momentum, volatility signals, and volume analysis into unified confluence scores for each timeframe.

## WHY THIS COMBINATION IS ORIGINAL AND USEFUL

**The Problem Solved:** Most traders manually check multiple timeframes and struggle to quickly assess overall market bias when different timeframes show conflicting signals. Existing MTF scripts typically display individual indicators without synthesizing them into actionable intelligence.

**The Solution:** This script implements a mathematical confluence algorithm that:

- Weights each indicator's signal strength (trend direction, RSI momentum, MACD volatility, volume analysis)

- Calculates normalized scores across all active timeframes

- Determines overall market bias with statistical confidence levels

- Provides instant visual feedback through color-coded symbols and star ratings

**Unique Features:**

1. **Confluence Scoring Algorithm**: Mathematically combines multiple indicator signals into a single confidence rating per timeframe

2. **Market Bias Engine**: Automatically calculates overall directional bias with percentage strength across all selected timeframes

3. **Dynamic Display System**: Real-time updates with customizable layouts, color schemes, and selective timeframe activation

4. **Statistical Analysis**: Provides bullish/bearish vote counts and overall confluence percentages

## HOW THE SCRIPT WORKS TECHNICALLY

### Core Calculation Methodology:

**1. Trend Analysis (EMA-based):**

- Fast EMA (default: 9) vs Slow EMA (default: 21) crossover analysis

- Returns values: +1 (bullish), -1 (bearish), 0 (neutral)

**2. Momentum Analysis (RSI-based):**

- RSI levels: >70 (strong bullish +2), >50 (bullish +1), <30 (strong bearish -2), <50 (bearish -1)

- Provides overbought/oversold context for trend confirmation

**3. Volatility Analysis (MACD-based):**

- MACD line vs Signal line positioning

- Histogram strength comparison with previous bar

- Combined score considering both direction and momentum strength

**4. Volume Analysis:**

- Current volume vs 20-period moving average

- Thresholds: >150% MA (strong +2), >100% MA (bullish +1), <50% MA (weak -2)

**5. Confluence Calculation:**

```

Confluence Score = (Trend + RSI + MACD + Volume) / 4.0

```

**6. Market Bias Determination:**

- Counts bullish vs bearish signals across all active timeframes

- Calculates bias strength percentage: |Bullish Count - Bearish Count| / Total Active TFs * 100

- Determines overall market direction: BULLISH, BEARISH, or NEUTRAL

### Multi-Timeframe Implementation:

Uses `request.security()` calls to fetch data from each timeframe, ensuring all calculations are performed on the respective timeframe's data rather than current chart timeframe, providing accurate multi-timeframe analysis.

## HOW TO USE THIS SCRIPT

### Initial Setup:

1. **Timeframe Selection**: Enable/disable specific timeframes in "Timeframe Selection" group based on your trading style

2. **Indicator Configuration**: Adjust EMA periods (Fast: 9, Slow: 21), RSI length (14), and MACD settings (12/26/9) to match your analysis preferences

3. **Display Options**: Choose table position, text size, and color scheme for optimal visibility

### Reading the Dashboard:

**Symbol Interpretation:**

- ⬆⬆ = Strong bullish signal (score ≥ 2)

- ⬆ = Bullish signal (score > 0)

- ➡ = Neutral signal (score = 0)

- ⬇ = Bearish signal (score < 0)

- ⬇⬇ = Strong bearish signal (score ≤ -2)

**Confluence Stars:**

- ★★★★★ = Very high confidence (score > 0.75)

- ★★★★☆ = High confidence (score > 0.5)

- ★★★☆☆ = Medium confidence (score > 0.25)

- ★★☆☆☆ = Low confidence (score > 0)

- ★☆☆☆☆ = Very low confidence (score > -0.25)

**Market Bias Section:**

- Shows overall market direction across all active timeframes

- Strength percentage indicates conviction level

- Overall confluence score represents average agreement across timeframes

### Trading Applications:

**Entry Signals:**

- Look for high confluence (4-5 stars) across multiple timeframes in same direction

- Higher timeframe alignment provides stronger signal validation

- Use confluence percentage >75% for high-probability setups

**Risk Management:**

- Lower timeframe conflicts may indicate choppy conditions

- Neutral bias suggests ranging market - adjust position sizing

- Strong bias with high confluence supports larger position sizes

**Timeframe Harmony:**

- Short-term trades: Focus on 1m-1H alignment

- Swing trades: Emphasize 1H-Daily alignment

- Position trades: Prioritize Daily-Monthly confluence

## SCRIPT SETTINGS EXPLANATION

### Dashboard Settings:

- **Table Position**: Choose optimal location (Top Right recommended for most layouts)

- **Text Size**: Adjust based on screen resolution and preferences

- **Color Scheme**: Professional (default), Classic, Vibrant, or Dark themes

- **Background Color/Transparency**: Customize table appearance

### Timeframe Selection:

All timeframes optional - activate based on trading timeframe preference:

- **Lower Timeframes (1m-30m)**: Scalping and day trading

- **Medium Timeframes (1H-4H)**: Swing trading

- **Higher Timeframes (D-M)**: Position trading and long-term bias

### Indicator Parameters:

- **Fast EMA (Default: 9)**: Shorter period for trend sensitivity

- **Slow EMA (Default: 21)**: Longer period for trend confirmation

- **RSI Length (Default: 14)**: Standard momentum calculation period

- **MACD Settings (12/26/9)**: Standard MACD configuration for volatility analysis

### Alert Configuration:

- **Strong Signals**: Alerts when confluence >75% with clear directional bias

- **High Confluence**: Alerts when multiple timeframes strongly agree

- All alerts use `alert.freq_once_per_bar` to prevent spam

## VISUAL FEATURES

### Chart Elements:

- **Background Coloring**: Subtle background tint reflects overall market bias

- **Signal Labels**: Strong buy/sell labels appear on chart during high-confluence signals

- **Clean Presentation**: Dashboard overlays chart without interfering with price action

### Color Coding:

- **Green/Bullish**: Various green shades for positive signals

- **Red/Bearish**: Various red shades for negative signals

- **Gray/Neutral**: Neutral color for conflicting or weak signals

- **Transparency**: Configurable transparency maintains chart readability

## IMPORTANT USAGE NOTES

**Realistic Expectations:**

- This tool provides analysis framework, not trading signals

- Always combine with proper risk management

- Past performance does not guarantee future results

- Market conditions can change rapidly - use appropriate position sizing

**Best Practices:**

- Verify signals with additional analysis methods

- Consider fundamental factors affecting the instrument

- Use appropriate timeframes for your trading style