Drawdown Distribution Analysis (DDA) ACADEMIC FOUNDATION AND RESEARCH BACKGROUND

The Drawdown Distribution Analysis indicator implements quantitative risk management principles, drawing upon decades of academic research in portfolio theory, behavioral finance, and statistical risk modeling. This tool provides risk assessment capabilities for traders and portfolio managers seeking to understand their current position within historical drawdown patterns.

The theoretical foundation of this indicator rests on modern portfolio theory as established by Markowitz (1952), who introduced the fundamental concepts of risk-return optimization that continue to underpin contemporary portfolio management. Sharpe (1966) later expanded this framework by developing risk-adjusted performance measures, most notably the Sharpe ratio, which remains a cornerstone of performance evaluation in financial markets.

The specific focus on drawdown analysis builds upon the work of Chekhlov, Uryasev and Zabarankin (2005), who provided the mathematical framework for incorporating drawdown measures into portfolio optimization. Their research demonstrated that traditional mean-variance optimization often fails to capture the full risk profile of investment strategies, particularly regarding sequential losses. More recent work by Goldberg and Mahmoud (2017) has brought these theoretical concepts into practical application within institutional risk management frameworks.

Value at Risk methodology, as comprehensively outlined by Jorion (2007), provides the statistical foundation for the risk measurement components of this indicator. The coherent risk measures framework developed by Artzner et al. (1999) ensures that the risk metrics employed satisfy the mathematical properties required for sound risk management decisions. Additionally, the focus on downside risk follows the framework established by Sortino and Price (1994), while the drawdown-adjusted performance measures implement concepts introduced by Young (1991).

MATHEMATICAL METHODOLOGY

The core calculation methodology centers on a peak-tracking algorithm that continuously monitors the maximum price level achieved and calculates the percentage decline from this peak. The drawdown at any time t is defined as DD(t) = (P(t) - Peak(t)) / Peak(t) × 100, where P(t) represents the asset price at time t and Peak(t) represents the running maximum price observed up to time t.

Statistical distribution analysis forms the analytical backbone of the indicator. The system calculates key percentiles using the ta.percentile_nearest_rank() function to establish the 5th, 10th, 25th, 50th, 75th, 90th, and 95th percentiles of the historical drawdown distribution. This approach provides a complete picture of how the current drawdown compares to historical patterns.

Statistical significance assessment employs standard deviation bands at one, two, and three standard deviations from the mean, following the conventional approach where the upper band equals μ + nσ and the lower band equals μ - nσ. The Z-score calculation, defined as Z = (DD - μ) / σ, enables the identification of statistically extreme events, with thresholds set at |Z| > 2.5 for extreme drawdowns and |Z| > 3.0 for severe drawdowns, corresponding to confidence levels exceeding 99.4% and 99.7% respectively.

ADVANCED RISK METRICS

The indicator incorporates several risk-adjusted performance measures that extend beyond basic drawdown analysis. The Sharpe ratio calculation follows the standard formula Sharpe = (R - Rf) / σ, where R represents the annualized return, Rf represents the risk-free rate, and σ represents the annualized volatility. The system supports dynamic sourcing of the risk-free rate from the US 10-year Treasury yield or allows for manual specification.

The Sortino ratio addresses the limitation of the Sharpe ratio by focusing exclusively on downside risk, calculated as Sortino = (R - Rf) / σd, where σd represents the downside deviation computed using only negative returns. This measure provides a more accurate assessment of risk-adjusted performance for strategies that exhibit asymmetric return distributions.

The Calmar ratio, defined as Annual Return divided by the absolute value of Maximum Drawdown, offers a direct measure of return per unit of drawdown risk. This metric proves particularly valuable for comparing strategies or assets with different risk profiles, as it directly relates performance to the maximum historical loss experienced.

Value at Risk calculations provide quantitative estimates of potential losses at specified confidence levels. The 95% VaR corresponds to the 5th percentile of the drawdown distribution, while the 99% VaR corresponds to the 1st percentile. Conditional VaR, also known as Expected Shortfall, estimates the average loss in the worst 5% of scenarios, providing insight into tail risk that standard VaR measures may not capture.

To enable fair comparison across assets with different volatility characteristics, the indicator calculates volatility-adjusted drawdowns using the formula Adjusted DD = Raw DD / (Volatility / 20%). This normalization allows for meaningful comparison between high-volatility assets like cryptocurrencies and lower-volatility instruments like government bonds.

The Risk Efficiency Score represents a composite measure ranging from 0 to 100 that combines the Sharpe ratio and current percentile rank to provide a single metric for quick asset assessment. Higher scores indicate superior risk-adjusted performance relative to historical patterns.

COLOR SCHEMES AND VISUALIZATION

The indicator implements eight distinct color themes designed to accommodate different analytical preferences and market contexts. The EdgeTools theme employs a corporate blue palette that matches the design system used throughout the edgetools.org platform, ensuring visual consistency across analytical tools.

The Gold theme specifically targets precious metals analysis with warm tones that complement gold chart analysis, while the Quant theme provides a grayscale scheme suitable for analytical environments that prioritize clarity over aesthetic appeal. The Behavioral theme incorporates psychology-based color coding, using green to represent greed-driven market conditions and red to indicate fear-driven environments.

Additional themes include Ocean, Fire, Matrix, and Arctic schemes, each designed for specific market conditions or user preferences. All themes function effectively with both dark and light mode trading platforms, ensuring accessibility across different user interface configurations.

PRACTICAL APPLICATIONS

Asset allocation and portfolio construction represent primary use cases for this analytical framework. When comparing multiple assets such as Bitcoin, gold, and the S&P 500, traders can examine Risk Efficiency Scores to identify instruments offering superior risk-adjusted performance. The 95% VaR provides worst-case scenario comparisons, while volatility-adjusted drawdowns enable fair comparison despite varying volatility profiles.

The practical decision framework suggests that assets with Risk Efficiency Scores above 70 may be suitable for aggressive portfolio allocations, scores between 40 and 70 indicate moderate allocation potential, and scores below 40 suggest defensive positioning or avoidance. These thresholds should be adjusted based on individual risk tolerance and market conditions.

Risk management and position sizing applications utilize the current percentile rank to guide allocation decisions. When the current drawdown ranks above the 75th percentile of historical data, indicating that current conditions are better than 75% of historical periods, position increases may be warranted. Conversely, when percentile rankings fall below the 25th percentile, indicating elevated risk conditions, position reductions become advisable.

Institutional portfolio monitoring applications include hedge fund risk dashboard implementations where multiple strategies can be monitored simultaneously. Sharpe ratio tracking identifies deteriorating risk-adjusted performance across strategies, VaR monitoring ensures portfolios remain within established risk limits, and drawdown duration tracking provides valuable information for investor reporting requirements.

Market timing applications combine the statistical analysis with trend identification techniques. Strong buy signals may emerge when risk levels register as "Low" in conjunction with established uptrends, while extreme risk levels combined with downtrends may indicate exit or hedging opportunities. Z-scores exceeding 3.0 often signal statistically oversold conditions that may precede trend reversals.

STATISTICAL SIGNIFICANCE AND VALIDATION

The indicator provides 95% confidence intervals around current drawdown levels using the standard formula CI = μ ± 1.96σ. This statistical framework enables users to assess whether current conditions fall within normal market variation or represent statistically significant departures from historical patterns.

Risk level classification employs a dynamic assessment system based on percentile ranking within the historical distribution. Low risk designation applies when current drawdowns perform better than 50% of historical data, moderate risk encompasses the 25th to 50th percentile range, high risk covers the 10th to 25th percentile range, and extreme risk applies to the worst 10% of historical drawdowns.

Sample size considerations play a crucial role in statistical reliability. For daily data, the system requires a minimum of 252 trading days (approximately one year) but performs better with 500 or more observations. Weekly data analysis benefits from at least 104 weeks (two years) of history, while monthly data requires a minimum of 60 months (five years) for reliable statistical inference.

IMPLEMENTATION BEST PRACTICES

Parameter optimization should consider the specific characteristics of different asset classes. Equity analysis typically benefits from 500-day lookback periods with 21-day smoothing, while cryptocurrency analysis may employ 365-day lookback periods with 14-day smoothing to account for higher volatility patterns. Fixed income analysis often requires longer lookback periods of 756 days with 34-day smoothing to capture the lower volatility environment.

Multi-timeframe analysis provides hierarchical risk assessment capabilities. Daily timeframe analysis supports tactical risk management decisions, weekly analysis informs strategic positioning choices, and monthly analysis guides long-term allocation decisions. This hierarchical approach ensures that risk assessment occurs at appropriate temporal scales for different investment objectives.

Integration with complementary indicators enhances the analytical framework. Trend indicators such as RSI and moving averages provide directional bias context, volume analysis helps confirm the severity of drawdown conditions, and volatility measures like VIX or ATR assist in market regime identification.

ALERT SYSTEM AND AUTOMATION

The automated alert system monitors five distinct categories of risk events. Risk level changes trigger notifications when drawdowns move between risk categories, enabling proactive risk management responses. Statistical significance alerts activate when Z-scores exceed established threshold levels of 2.5 or 3.0 standard deviations.

New maximum drawdown alerts notify users when historical maximum levels are exceeded, indicating entry into uncharted risk territory. Poor risk efficiency alerts trigger when the composite risk efficiency score falls below 30, suggesting deteriorating risk-adjusted performance. Sharpe ratio decline alerts activate when risk-adjusted performance turns negative, indicating that returns no longer compensate for the risk undertaken.

TRADING STRATEGIES

Conservative risk parity strategies can be implemented by monitoring Risk Efficiency Scores across a diversified asset portfolio. Monthly rebalancing maintains equal risk contribution from each asset, with allocation reductions triggered when risk levels reach "High" status and complete exits executed when "Extreme" risk levels emerge. This approach typically results in lower overall portfolio volatility, improved risk-adjusted returns, and reduced maximum drawdown periods.

Tactical asset rotation strategies compare Risk Efficiency Scores across different asset classes to guide allocation decisions. Assets with scores exceeding 60 receive overweight allocations, while assets scoring below 40 receive underweight positions. Percentile rankings provide timing guidance for allocation adjustments, creating a systematic approach to asset allocation that responds to changing risk-return profiles.

Market timing strategies with statistical edges can be constructed by entering positions when Z-scores fall below -2.5, indicating statistically oversold conditions, and scaling out when Z-scores exceed 2.5, suggesting overbought conditions. The 95% VaR serves as a stop-loss reference point, while trend confirmation indicators provide additional validation for position entry and exit decisions.

LIMITATIONS AND CONSIDERATIONS

Several statistical limitations affect the interpretation and application of these risk measures. Historical bias represents a fundamental challenge, as past drawdown patterns may not accurately predict future risk characteristics, particularly during structural market changes or regime shifts. Sample dependence means that results can be sensitive to the selected lookback period, with shorter periods providing more responsive but potentially less stable estimates.

Market regime changes can significantly alter the statistical parameters underlying the analysis. During periods of structural market evolution, historical distributions may provide poor guidance for future expectations. Additionally, many financial assets exhibit return distributions with fat tails that deviate from normal distribution assumptions, potentially leading to underestimation of extreme event probabilities.

Practical limitations include execution risk, where theoretical signals may not translate directly into actual trading results due to factors such as slippage, timing delays, and market impact. Liquidity constraints mean that risk metrics assume perfect liquidity, which may not hold during stressed market conditions when risk management becomes most critical.

Transaction costs are not incorporated into risk-adjusted return calculations, potentially overstating the attractiveness of strategies that require frequent trading. Behavioral factors represent another limitation, as human psychology may override statistical signals, particularly during periods of extreme market stress when disciplined risk management becomes most challenging.

TECHNICAL IMPLEMENTATION

Performance optimization ensures reliable operation across different market conditions and timeframes. All technical analysis functions are extracted from conditional statements to maintain Pine Script compliance and ensure consistent execution. Memory efficiency is achieved through optimized variable scoping and array usage, while computational speed benefits from vectorized calculations where possible.

Data quality requirements include clean price data without gaps or errors that could distort distribution analysis. Sufficient historical data is essential, with a minimum of 100 bars required and 500 or more preferred for reliable statistical inference. Time alignment across related assets ensures meaningful comparison when conducting multi-asset analysis.

The configuration parameters are organized into logical groups to enhance usability. Core settings include the Distribution Analysis Period (100-2000 bars), Drawdown Smoothing Period (1-50 bars), and Price Source selection. Advanced metrics settings control risk-free rate sourcing, either from live market data or fixed rate specification, along with toggles for various risk-adjusted metric calculations.

Display options provide flexibility in visual presentation, including color theme selection from eight available schemes, automatic dark mode optimization, and control over table display, position lines, percentile bands, and standard deviation overlays. These options ensure that the indicator can be adapted to different analytical workflows and visual preferences.

CONCLUSION

The Drawdown Distribution Analysis indicator provides risk management tools for traders seeking to understand their current position within historical risk patterns. By combining established statistical methodology with practical usability features, the tool enables evidence-based risk assessment and portfolio optimization decisions.

The implementation draws upon established academic research while providing practical features that address real-world trading requirements. Dynamic risk-free rate integration ensures accurate risk-adjusted performance calculations, while multiple color schemes accommodate different analytical preferences and use cases.

Academic compliance is maintained through transparent methodology and acknowledgment of limitations. The tool implements peer-reviewed statistical techniques while clearly communicating the constraints and assumptions underlying the analysis. This approach ensures that users can make informed decisions about the appropriate application of the risk assessment framework within their broader trading and investment processes.

BIBLIOGRAPHY

Artzner, P., Delbaen, F., Eber, J.M. and Heath, D. (1999) 'Coherent Measures of Risk', Mathematical Finance, 9(3), pp. 203-228.

Chekhlov, A., Uryasev, S. and Zabarankin, M. (2005) 'Drawdown Measure in Portfolio Optimization', International Journal of Theoretical and Applied Finance, 8(1), pp. 13-58.

Goldberg, L.R. and Mahmoud, O. (2017) 'Drawdown: From Practice to Theory and Back Again', Journal of Risk Management in Financial Institutions, 10(2), pp. 140-152.

Jorion, P. (2007) Value at Risk: The New Benchmark for Managing Financial Risk. 3rd edn. New York: McGraw-Hill.

Markowitz, H. (1952) 'Portfolio Selection', Journal of Finance, 7(1), pp. 77-91.

Sharpe, W.F. (1966) 'Mutual Fund Performance', Journal of Business, 39(1), pp. 119-138.

Sortino, F.A. and Price, L.N. (1994) 'Performance Measurement in a Downside Risk Framework', Journal of Investing, 3(3), pp. 59-64.

Young, T.W. (1991) 'Calmar Ratio: A Smoother Tool', Futures, 20(1), pp. 40-42.

在脚本中搜索"100年国际黄金价格"

SCTI V28Indicator Overview | 指标概述

English: SCTI V28 (Smart Composite Technical Indicator) is a multi-functional composite technical analysis tool that integrates various classic technical analysis methods. It contains 7 core modules that can be flexibly configured to show or hide components based on traders' needs, suitable for various trading styles and market conditions.

中文: SCTI V28 (智能复合技术指标) 是一款多功能复合型技术分析指标,整合了多种经典技术分析工具于一体。该指标包含7大核心模块,可根据交易者的需求灵活配置显示或隐藏各个组件,适用于多种交易风格和市场环境。

Main Functional Modules | 主要功能模块

1. Basic Indicator Settings | 基础指标设置

English:

EMA Display: 13 configurable EMA lines (default shows 8/13/21/34/55/144/233/377/610/987/1597/2584 periods)

PMA Display: 11 configurable moving averages with multiple MA types (ALMA/EMA/RMA/SMA/SWMA/VWAP/VWMA/WMA)

VWAP Display: Volume Weighted Average Price indicator

Divergence Indicator: Detects divergences across 12 technical indicators

ATR Stop Loss: ATR-based stop loss lines

Volume SuperTrend AI: AI-powered super trend indicator

中文:

EMA显示:13条可配置EMA均线,默认显示8/13/21/34/55/144/233/377/610/987/1597/2584周期

PMA显示:11条可配置移动平均线,支持多种MA类型(ALMA/EMA/RMA/SMA/SWMA/VWAP/VWMA/WMA)

VWAP显示:成交量加权平均价指标

背离指标:12种技术指标的背离检测系统

ATR止损:基于ATR的止损线

Volume SuperTrend AI:基于AI预测的超级趋势指标

2. EMA Settings | EMA设置

English:

13 independent EMA lines, each configurable for visibility and period length

Default shows 21/34/55/144/233/377/610/987/1597/2584 period EMAs

Customizable colors and line widths for each EMA

中文:

13条独立EMA均线,每条均可单独配置显示/隐藏和周期长度

默认显示21/34/55/144/233/377/610/987/1597/2584周期的EMA

每条EMA可设置不同颜色和线宽

3. PMA Settings | PMA设置

English:

11 configurable moving averages, each with:

Selectable types (default EMA, options: ALMA/RMA/SMA/SWMA/VWAP/VWMA/WMA)

Independent period settings (12-1056)

Special ALMA parameters (offset and sigma)

Configurable data source and plot offset

Support for fill areas between MAs

Price lines and labels can be added

中文:

11条可配置移动平均线,每条均可:

选择不同类型(默认EMA,可选ALMA/RMA/SMA/SWMA/VWAP/VWMA/WMA)

独立设置周期长度(12-1056)

设置ALMA的特殊参数(偏移量和sigma)

配置数据源和绘图偏移

支持MA之间的填充区域显示

可添加价格线和标签

4. VWAP Settings | VWAP设置

English:

Multiple anchor period options (Session/Week/Month/Quarter/Year/Decade/Century/Earnings/Dividends/Splits)

3 configurable standard deviation bands

Option to hide on daily and higher timeframes

Configurable data source and offset settings

中文:

多种锚定周期选择(会话/周/月/季/年/十年/世纪/财报/股息/拆股)

3条可配置标准差带

可选择在日线及以上周期隐藏

支持数据源选择和偏移设置

5. Divergence Indicator Settings | 背离指标设置

English:

12 detectable indicators: MACD, MACD Histogram, RSI, Stochastic, CCI, Momentum, OBV, VWmacd, Chaikin Money Flow, MFI, Williams %R, External Indicator

4 divergence types: Regular Bullish/Bearish, Hidden Bullish/Bearish

Multiple display options: Full name/First letter/Hide indicator name

Configurable parameters: Pivot period, data source, maximum bars checked, etc.

Alert functions: Independent alerts for each divergence type

中文:

检测12种指标:MACD、MACD柱状图、RSI、随机指标、CCI、动量、OBV、VWmacd、Chaikin资金流、MFI、威廉姆斯%R、外部指标

4种背离类型:正/负常规背离,正/负隐藏背离

多种显示选项:完整名称/首字母/不显示指标名称

可配置参数:枢轴点周期、数据源、最大检查柱数等

警报功能:各类背离的独立警报

6. ATR Stop Loss Settings | ATR止损设置

English:

Configurable ATR length (default 13)

4 smoothing methods (RMA/SMA/EMA/WMA)

Adjustable multiplier (default 1.618)

Displays long and short stop loss lines

中文:

可配置ATR长度(默认13)

4种平滑方法(RMA/SMA/EMA/WMA)

可调乘数(默认1.618)

显示多头和空头止损线

7. Volume SuperTrend AI Settings | Volume SuperTrend AI设置

English:

AI Prediction:

Configurable neighbors (1-100) and data points (1-100)

Price trend length and prediction trend length settings

SuperTrend Parameters:

Length (default 3)

Factor (default 1.515)

5 MA source options (SMA/EMA/WMA/RMA/VWMA)

Signal Display:

Trend start signals (circle markers)

Trend confirmation signals (triangle markers)

6 Alerts: Various trend start and confirmation signals

中文:

AI预测功能:

可配置邻居数(1-100)和数据点数(1-100)

价格趋势长度和预测趋势长度设置

SuperTrend参数:

长度(默认3)

因子(默认1.515)

5种MA源选择(SMA/EMA/WMA/RMA/VWMA)

信号显示:

趋势开始信号(圆形标记)

趋势确认信号(三角形标记)

6种警报:各类趋势开始和确认信号

Usage Recommendations | 使用建议

English:

Trend Analysis: Use EMA/PMA combinations to determine market trends, with long-period EMAs (e.g., 144/233) as primary trend references

Divergence Trading: Look for potential reversals using price-indicator divergences

Stop Loss Management: Use ATR stop loss lines for risk management

AI Assistance: Volume SuperTrend AI provides machine learning-based trend predictions

Multiple Timeframes: Verify signals across different timeframes

中文:

趋势分析:使用EMA/PMA组合判断市场趋势,长周期EMA(如144/233)作为主要趋势参考

背离交易:结合价格与指标的背离寻找潜在反转点

止损设置:利用ATR止损线管理风险

AI辅助:Volume SuperTrend AI提供基于机器学习的趋势预测

多时间框架:建议在不同时间框架下验证信号

Parameter Configuration Tips | 参数配置技巧

English:

For short-term trading: Focus on 8-55 period EMAs and shorter divergence detection periods

For long-term investing: Use 144-2584 period EMAs with longer detection parameters

In ranging markets: Disable some EMAs, mainly rely on VWAP and divergence indicators

In trending markets: Enable more EMAs and SuperTrend AI

中文:

对于短线交易:可重点关注8-55周期的EMA和较短的背离检测周期

对于长线投资:建议使用144-2584周期的EMA和较长的检测参数

在震荡市:可关闭部分EMA,主要依靠VWAP和背离指标

在趋势市:可启用更多EMA和SuperTrend AI

Update Log | 更新日志

English:

V28 main updates:

Added Volume SuperTrend AI module

Optimized divergence detection algorithm

Added more EMA period options

Improved UI and parameter grouping

中文:

V28版本主要更新:

新增Volume SuperTrend AI模块

优化背离检测算法

增加更多EMA周期选项

改进用户界面和参数分组

Final Note | 最后说明

English: This indicator is suitable for technical traders with some experience. We recommend practicing with demo trading to familiarize yourself with all features before live trading.

中文: 该指标适合有一定经验的技术分析交易者使用,建议先通过模拟交易熟悉各项功能后再应用于实盘。

Ultimate Market Structure [Alpha Extract]Ultimate Market Structure

A comprehensive market structure analysis tool that combines advanced swing point detection, imbalance zone identification, and intelligent break analysis to identify high-probability trading opportunities.Utilizing a sophisticated trend scoring system, this indicator classifies market conditions and provides clear signals for structure breaks, directional changes, and fair value gap detection with institutional-grade precision.

🔶 Advanced Swing Point Detection

Identifies pivot highs and lows using configurable lookback periods with optional close-based analysis for cleaner signals. The system automatically labels swing points as Higher Highs (HH), Lower Highs (LH), Higher Lows (HL), and Lower Lows (LL) while providing advanced classifications including "rising_high", "falling_high", "rising_low", "falling_low", "peak_high", and "valley_low" for nuanced market analysis.

swingHighPrice = useClosesForStructure ? ta.pivothigh(close, swingLength, swingLength) : ta.pivothigh(high, swingLength, swingLength)

swingLowPrice = useClosesForStructure ? ta.pivotlow(close, swingLength, swingLength) : ta.pivotlow(low, swingLength, swingLength)

classification = classifyStructurePoint(structureHighPrice, upperStructure, true)

significance = calculateSignificance(structureHighPrice, upperStructure, true)

🔶 Significance Scoring System

Each structure point receives a significance level on a 1-5 scale based on its distance from previous points, helping prioritize the most important levels. This intelligent scoring system ensures traders focus on the most meaningful structure breaks while filtering out minor noise.

🔶 Comprehensive Trend Analysis

Calculates momentum, strength, direction, and confidence levels using volatility-normalized price changes and multi-timeframe correlation. The system provides real-time trend state tracking with bullish (+1), bearish (-1), or neutral (0) direction assessment and 0-100 confidence scoring.

// Calculate trend momentum using rate of change and volatility

calculateTrendMomentum(lookback) =>

priceChange = (close - close ) / close * 100

avgVolatility = ta.atr(lookback) / close * 100

momentum = priceChange / (avgVolatility + 0.0001)

momentum

// Calculate trend strength using multiple timeframe correlation

calculateTrendStrength(shortPeriod, longPeriod) =>

shortMA = ta.sma(close, shortPeriod)

longMA = ta.sma(close, longPeriod)

separation = math.abs(shortMA - longMA) / longMA * 100

strength = separation * slopeAlignment

❓How It Works

🔶 Imbalance Zone Detection

Identifies Fair Value Gaps (FVGs) between consecutive candles where price gaps create unfilled areas. These zones are displayed as semi-transparent boxes with optional center line mitigation tracking, highlighting potential support and resistance levels where institutional players often react.

// Detect Fair Value Gaps

detectPriceImbalance() =>

currentHigh = high

currentLow = low

refHigh = high

refLow = low

if currentOpen > currentClose

if currentHigh - refLow < 0

upperBound = currentClose - (currentClose - refLow)

lowerBound = currentClose - (currentClose - currentHigh)

centerPoint = (upperBound + lowerBound) / 2

newZone = ImbalanceZone.new(

zoneBox = box.new(bar_index, upperBound, rightEdge, lowerBound,

bgcolor=bullishImbalanceColor, border_color=hiddenColor)

)

🔶 Structure Break Analysis

Determines Break of Structure (BOS) for trend continuation and Directional Change (DC) for trend reversals with advanced classification as "continuation", "reversal", or "neutral". The system compares pre-trend and post-trend states for each break, providing comprehensive trend change momentum analysis.

🔶 Intelligent Zone Management

Features partial mitigation tracking when price enters but doesn't fully fill zones, with automatic zone boundary adjustment during partial fills. Smart array management keeps only recent structure points for optimal performance while preventing duplicate signals from the same level.

🔶 Liquidity Zone Detection

Automatically identifies potential liquidity zones at key structure points for institutional trading analysis. The system tracks broken structure points and provides adaptive zone extension with configurable time-based limits for imbalance areas.

🔶 Visual Structure Mapping

Provides clear visual indicators including swing labels with color-coded significance levels, dashed lines connecting break points with BOS/DC labels, and break signals for continuation and reversal patterns. The adaptive zones feature smart management with automatic mitigation tracking.

🔶 Market Structure Interpretation

HH/HL patterns indicate bullish market structure with trend continuation likelihood, while LH/LL patterns signal bearish structure with downtrend continuation expected. BOS signals represent structure breaks in trend direction for continuation opportunities, while DC signals warn of potential reversals.

🔶 Performance Optimization

Automatic cleanup of old structure points (keeps last 8 points), recent break tracking (keeps last 5 break events), and efficient array management ensure smooth performance across all timeframes and market conditions.

Why Choose Ultimate Market Structure ?

This indicator provides traders with institutional-grade market structure analysis, combining multiple analytical approaches into one comprehensive tool. By identifying key structure levels, imbalance zones, and break patterns with advanced significance scoring, it helps traders understand market dynamics and position themselves for high-probability trade setups in alignment with smart money concepts. The sophisticated trend scoring system and intelligent zone management make it an essential tool for any serious trader looking to decode market structure with precision and confidence.

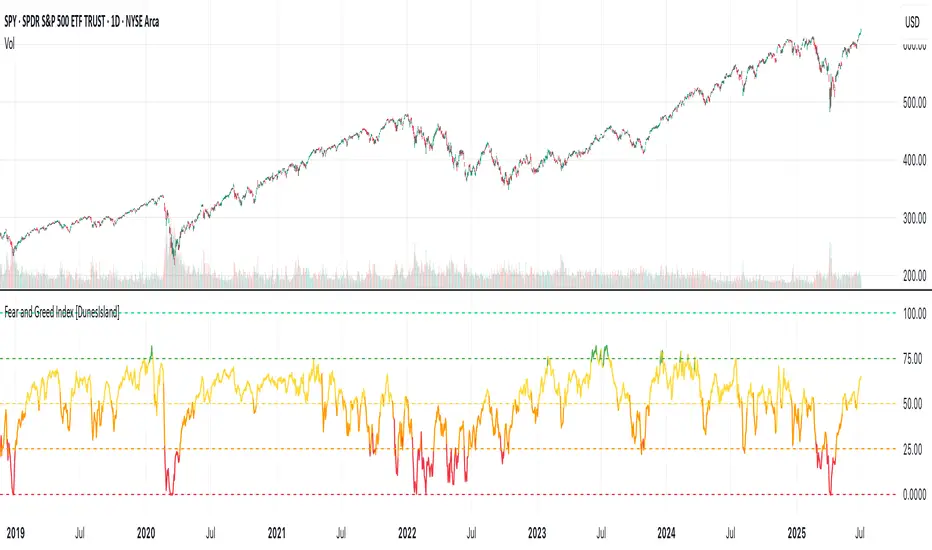

Fear and Greed Index [DunesIsland]The Fear and Greed Index is a sentiment indicator designed to measure the emotions driving the stock market, specifically investor fear and greed. Fear represents pessimism and caution, while greed reflects optimism and risk-taking. This indicator aggregates multiple market metrics to provide a comprehensive view of market sentiment, helping traders and investors gauge whether the market is overly fearful or excessively greedy.How It WorksThe Fear and Greed Index is calculated using four key market indicators, each capturing a different aspect of market sentiment:

Market Momentum (30% weight)

Measures how the S&P 500 (SPX) is performing relative to its 125-day simple moving average (SMA).

A higher value indicates that the market is trading well above its moving average, signaling greed.

Stock Price Strength (20% weight)

Calculates the net number of stocks hitting 52-week highs minus those hitting 52-week lows on the NYSE.

A greater number of net highs suggests strong market breadth and greed.

Put/Call Options (30% weight)

Uses the 5-day average of the put/call ratio.

A lower ratio (more call options being bought) indicates greed, as investors are betting on rising prices.

Market Volatility (20% weight)

Utilizes the VIX index, which measures market volatility.

Lower volatility is associated with greed, as investors are less fearful of large market swings.

Each component is normalized using a z-score over a 252-day lookback period (approximately one trading year) and scaled to a range of 0 to 100. The final Fear and Greed Index is a weighted average of these four components, with the weights specified above.Key FeaturesIndex Range: The index value ranges from 0 to 100:

0–25: Extreme Fear (red)

25–50: Fear (orange)

50–75: Neutral (yellow)

75–100: Greed (green)

Dynamic Plot Color: The plot line changes color based on the index value, visually indicating the current sentiment zone.

Reference Lines: Horizontal lines are plotted at 0, 25, 50, 75, and 100 to represent the different sentiment levels: Extreme Fear, Fear, Neutral, Greed, and Extreme Greed.

How to Interpret

Low Values (0–25): Indicate extreme fear, which may suggest that the market is oversold and could be due for a rebound.

High Values (75–100): Indicate greed, which may signal that the market is overbought and could be at risk of a correction.

Neutral Range (25–75): Suggests a balanced market sentiment, neither overly fearful nor greedy.

This indicator is a valuable tool for contrarian investors, as extreme readings often precede market reversals. However, it should be used in conjunction with other technical and fundamental analysis tools for a well-rounded view of the market.

log.info() - 5 Exampleslog.info() is one of the most powerful tools in Pine Script that no one knows about. Whenever you code, you want to be able to debug, or find out why something isn’t working. The log.info() command will help you do that. Without it, creating more complex Pine Scripts becomes exponentially more difficult.

The first thing to note is that log.info() only displays strings. So, if you have a variable that is not a string, you must turn it into a string in order for log.info() to work. The way you do that is with the str.tostring() command. And remember, it's all lower case! You can throw in any numeric value (float, int, timestamp) into str.string() and it should work.

Next, in order to make your output intelligible, you may want to identify whatever value you are logging. For example, if an RSI value is 50, you don’t want a bunch of lines that just say “50”. You may want it to say “RSI = 50”.

To do that, you’ll have to use the concatenation operator. For example, if you have a variable called “rsi”, and its value is 50, then you would use the “+” concatenation symbol.

EXAMPLE 1

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

//@version=6

indicator("log.info()")

rsi = ta.rsi(close,14)

log.info(“RSI= ” + str.tostring(rsi))

Example Output =>

RSI= 50

Here, we use double quotes to create a string that contains the name of the variable, in this case “RSI = “, then we concatenate it with a stringified version of the variable, rsi.

Now that you know how to write a log, where do you view them? There isn’t a lot of documentation on it, and the link is not conveniently located.

Open up the “Pine Editor” tab at the bottom of any chart view, and you’ll see a “3 dot” button at the top right of the pane. Click that, and right above the “Help” menu item you’ll see “Pine logs”. Clicking that will open that to open a pane on the right of your browser - replacing whatever was in the right pane area before. This is where your log output will show up.

But, because you’re dealing with time series data, using the log.info() command without some type of condition will give you a fast moving stream of numbers that will be difficult to interpret. So, you may only want the output to show up once per bar, or only under specific conditions.

To have the output show up only after all computations have completed, you’ll need to use the barState.islast command. Remember, barState is camelCase, but islast is not!

EXAMPLE 2

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

//@version=6

indicator("log.info()")

rsi = ta.rsi(close,14)

if barState.islast

log.info("RSI=" + str.tostring(rsi))

plot(rsi)

However, this can be less than ideal, because you may want the value of the rsi variable on a particular bar, at a particular time, or under a specific chart condition. Let’s hit these one at a time.

In each of these cases, the built-in bar_index variable will come in handy. When debugging, I typically like to assign a variable “bix” to represent bar_index, and include it in the output.

So, if I want to see the rsi value when RSI crosses above 0.5, then I would have something like

EXAMPLE 3

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

//@version=6

indicator("log.info()")

rsi = ta.rsi(close,14)

bix = bar_index

rsiCrossedOver = ta.crossover(rsi,0.5)

if rsiCrossedOver

log.info("bix=" + str.tostring(bix) + " - RSI=" + str.tostring(rsi))

plot(rsi)

Example Output =>

bix=19964 - RSI=51.8449459867

bix=19972 - RSI=50.0975830828

bix=19983 - RSI=53.3529808079

bix=19985 - RSI=53.1595745146

bix=19999 - RSI=66.6466337654

bix=20001 - RSI=52.2191767466

Here, we see that the output only appears when the condition is met.

A useful thing to know is that if you want to limit the number of decimal places, then you would use the command str.tostring(rsi,”#.##”), which tells the interpreter that the format of the number should only be 2 decimal places. Or you could round the rsi variable with a command like rsi2 = math.round(rsi*100)/100 . In either case you’re output would look like:

bix=19964 - RSI=51.84

bix=19972 - RSI=50.1

bix=19983 - RSI=53.35

bix=19985 - RSI=53.16

bix=19999 - RSI=66.65

bix=20001 - RSI=52.22

This would decrease the amount of memory that’s being used to display your variable’s values, which can become a limitation for the log.info() command. It only allows 4096 characters per line, so when you get to trying to output arrays (which is another cool feature), you’ll have to keep that in mind.

Another thing to note is that log output is always preceded by a timestamp, but for the sake of brevity, I’m not including those in the output examples.

If you wanted to only output a value after the chart was fully loaded, that’s when barState.islast command comes in. Under this condition, only one line of output is created per tick update — AFTER the chart has finished loading. For example, if you only want to see what the the current bar_index and rsi values are, without filling up your log window with everything that happens before, then you could use the following code:

EXAMPLE 4

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

//@version=6

indicator("log.info()")

rsi = ta.rsi(close,14)

bix = bar_index

if barstate.islast

log.info("bix=" + str.tostring(bix) + " - RSI=" + str.tostring(rsi))

Example Output =>

bix=20203 - RSI=53.1103309071

This value would keep updating after every new bar tick.

The log.info() command is a huge help in creating new scripts, however, it does have its limitations. As mentioned earlier, only 4096 characters are allowed per line. So, although you can use log.info() to output arrays, you have to be aware of how many characters that array will use.

The following code DOES NOT WORK! And, the only way you can find out why will be the red exclamation point next to the name of the indicator. That, and nothing will show up on the chart, or in the logs.

// CODE DOESN’T WORK

//@version=6

indicator("MW - log.info()")

var array rsi_arr = array.new()

rsi = ta.rsi(close,14)

bix = bar_index

rsiCrossedOver = ta.crossover(rsi,50)

if rsiCrossedOver

array.push(rsi_arr, rsi)

if barstate.islast

log.info("rsi_arr:" + str.tostring(rsi_arr))

log.info("bix=" + str.tostring(bix) + " - RSI=" + str.tostring(rsi))

plot(rsi)

// No code errors, but will not compile because too much is being written to the logs.

However, after putting some time restrictions in with the i_startTime and i_endTime user input variables, and creating a dateFilter variable to use in the conditions, I can limit the size of the final array. So, the following code does work.

EXAMPLE 5

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

// CODE DOES WORK

//@version=6

indicator("MW - log.info()")

i_startTime = input.time(title="Start", defval=timestamp("01 Jan 2025 13:30 +0000"))

i_endTime = input.time(title="End", defval=timestamp("1 Jan 2099 19:30 +0000"))

var array rsi_arr = array.new()

dateFilter = time >= i_startTime and time <= i_endTime

rsi = ta.rsi(close,14)

bix = bar_index

rsiCrossedOver = ta.crossover(rsi,50) and dateFilter // <== The dateFilter condition keeps the array from getting too big

if rsiCrossedOver

array.push(rsi_arr, rsi)

if barstate.islast

log.info("rsi_arr:" + str.tostring(rsi_arr))

log.info("bix=" + str.tostring(bix) + " - RSI=" + str.tostring(rsi))

plot(rsi)

Example Output =>

rsi_arr:

bix=20210 - RSI=56.9030578034

Of course, if you restrict the decimal places by using the rounding the rsi value with something like rsiRounded = math.round(rsi * 100) / 100 , then you can further reduce the size of your array. In this case the output may look something like:

Example Output =>

rsi_arr:

bix=20210 - RSI=55.6947486019

This will give your code a little breathing room.

In a nutshell, I was coding for over a year trying to debug by pushing output to labels, tables, and using libraries that cluttered up my code. Once I was able to debug with log.info() it was a game changer. I was able to start building much more advanced scripts. Hopefully, this will help you on your journey as well.

Omega Market Mood Meter [OmegaTools]The Omega Market Mood Meter is a precision-built sentiment oscillator that captures the market’s emotional intensity through a multi-layered RSI system. Designed for traders who seek to align with the market's true behavioral state, it blends momentum readings with a brand-new, rarely-seen innovation: the Sentiment-Weighted Moving Average (WMA-Ω)—a trend filter that dynamically adjusts to the market’s psychological tone.

🧠 Market Mood Oscillator

At its core, the Ω 3M oscillator aggregates three RSI-based components:

RSI(9) on close — captures short-term tension;

RSI(21) on HLC3 — balances medium-term positioning;

RSI(50) on HL2 — reflects long-term directional weight.

Each input is scaled and weighted to contribute to a final oscillator centered around zero, with ±50 and ±100 acting as key sentiment boundaries. When values exceed ±100, the market is likely reaching emotional extremes—zones that often precede reversals or require caution.

Visual features include:

Dynamic Background Highlighting: automatically emphasizes extreme sentiment zones.

Reference Lines: plotted at ±100, ±50, and 0 for fast sentiment interpretation.

🔥 WMA-Ω: Sentiment-Weighted Moving Average

The standout innovation of this tool is the Weighted Market Mood Moving Average, or WMA-Ω—a proprietary calculation that averages price using the absolute value of sentiment as its weighting force. This approach gives greater importance to price during periods of strong emotional conviction (either bullish or bearish), resulting in a context-aware trend filter that reacts only when sentiment truly matters.

This technique:

Filters noise during low-volatility or indecisive conditions;

Enhances reliability by reacting to meaningful sentiment surges;

Offers a more psychologically-adjusted trend baseline compared to traditional MAs.

Visually:

When price is above WMA-Ω, a semi-transparent bullish fill highlights underlying strength;

When below, a bearish fill reveals dominant downward sentiment.

This feature is unique among public TradingView tools and provides an edge in identifying trend quality with psychological context.

✅ How to Use

Extreme Sentiment Zones (±100): Use as contrarian warning zones or signal dampeners.

Crosses of WMA-Ω: Treat these as psychological trend confirmations; price above indicates structurally bullish sentiment and vice versa.

Range-bound Bias: Between ±50, sentiment may be indecisive; watch for breakout or alignment with WMA-Ω.

Advanced Confluence: Combine with other Omega tools (e.g., Ω Bias Forecaster, Ω IV Walls) for powerful regime-based strategies.

Omega Market Mood Meter is ideal for discretionary and systematic traders who want a clean, multi-timeframe sentiment readout and a cutting-edge weighted trend engine grounded in market psychology.

Heikin-Ashi Mean Reversion Oscillator [Alpha Extract]The Heikin-Ashi Mean Reversion Oscillator combines the smoothing characteristics of Heikin-Ashi candlesticks with mean reversion analysis to create a powerful momentum oscillator. This indicator applies Heikin-Ashi transformation twice - first to price data and then to the oscillator itself - resulting in smoother signals while maintaining sensitivity to trend changes and potential reversal points.

🔶 CALCULATION

Heikin-Ashi Transformation: Converts regular OHLC data to smoothed Heikin-Ashi values

Component Analysis: Calculates trend strength, body deviation, and price deviation from mean

Oscillator Construction: Combines components with weighted formula (40% trend strength, 30% body deviation, 30% price deviation)

Double Smoothing: Applies EMA smoothing and second Heikin-Ashi transformation to oscillator values

Signal Generation: Identifies trend changes and crossover points with overbought/oversold levels

Formula:

HA Close = (Open + High + Low + Close) / 4

HA Open = (Previous HA Open + Previous HA Close) / 2

Trend Strength = Normalized consecutive HA candle direction

Body Deviation = (HA Body - Mean Body) / Mean Body * 100

Price Deviation = ((HA Close - Price Mean) / Price Mean * 100) / Standard Deviation * 25

Raw Oscillator = (Trend Strength * 0.4) + (Body Deviation * 0.3) + (Price Deviation * 0.3)

Final Oscillator = 50 + (EMA(Raw Oscillator) / 2)

🔶 DETAILS Visual Features:

Heikin-Ashi Candlesticks: Smoothed oscillator representation using HA transformation with vibrant teal/red coloring

Overbought/Oversold Zones: Horizontal lines at customizable levels (default 70/30) with background highlighting in extreme zones

Moving Averages: Optional fast and slow EMA overlays for additional trend confirmation

Signal Dashboard: Real-time table showing current oscillator status (Overbought/Oversold/Bullish/Bearish) and buy/sell signals

Reference Lines: Middle line at 50 (neutral), with 0 and 100 boundaries for range visualization

Interpretation:

Above 70: Overbought conditions, potential selling opportunity

Below 30: Oversold conditions, potential buying opportunity

Bullish HA Candles: Green/teal candles indicate upward momentum

Bearish HA Candles: Red candles indicate downward momentum

MA Crossovers: Fast EMA above slow EMA suggests bullish momentum, below suggests bearish momentum

Zone Exits: Price moving out of extreme zones (above 70 or below 30) often signals trend continuation

🔶 EXAMPLES

Mean Reversion Signals: When the oscillator reaches extreme levels (above 70 or below 30), it identifies potential reversal points where price may revert to the mean.

Example: Oscillator reaching 80+ levels during strong uptrends often precedes short-term pullbacks, providing profit-taking opportunities.

Trend Change Detection: The double Heikin-Ashi smoothing helps identify genuine trend changes while filtering out market noise.

Example: When oscillator HA candles change from red to teal after oversold readings, this confirms potential trend reversal from bearish to bullish.

Moving Average Confirmation: Fast and slow EMA crossovers on the oscillator provide additional confirmation of momentum shifts.

Example: Fast EMA crossing above slow EMA while oscillator is rising from oversold levels provides strong bullish confirmation signal.

Dashboard Signal Integration: The real-time dashboard combines oscillator status with directional signals for quick decision-making.

Example: Dashboard showing "Oversold" status with "BUY" signal when HA candles turn bullish provides clear entry timing.

🔶 SETTINGS

Customization Options:

Calculation: Oscillator period (default 14), smoothing factor (1-50, default 2)

Levels: Overbought threshold (50-100, default 70), oversold threshold (0-50, default 30)

Moving Averages: Toggle display, fast EMA length (default 9), slow EMA length (default 21)

Visual Enhancements: Show/hide signal dashboard, customizable table position

Alert Conditions: Oversold bounce, overbought reversal, bullish/bearish MA crossovers

The Heikin-Ashi Mean Reversion Oscillator provides traders with a sophisticated momentum tool that combines the smoothing benefits of Heikin-Ashi analysis with mean reversion principles. The double transformation process creates cleaner signals while the integrated dashboard and multiple confirmation methods help traders identify high-probability entry and exit points during both trending and ranging market conditions.

Volume and Volatility Ratio Indicator-WODI策略名称

交易量与波动率比例策略-WODI

一、用户自定义参数

vol_length:交易量均线长度,计算基础交易量活跃度。

index_short_length / index_long_length:指数短期与长期均线长度,用于捕捉中短期与中长期趋势。

index_magnification:敏感度放大倍数,调整指数均线的灵敏度。

index_threshold_magnification:阈值放大因子,用于动态过滤噪音。

lookback_bars:形态检测回溯K线根数,用于捕捉反转模式。

fib_tp_ratio / fib_sl_ratio:斐波那契止盈与止损比率,分别对应黄金分割(0.618/0.382 等)级别。

enable_reversal:反转信号开关,开启后将原有做空信号反向为做多信号,用于单边趋势加仓。

二、核心计算逻辑

交易量百分比

使用 ta.sma 计算 vol_ma,并得到 vol_percent = volume / vol_ma * 100。

价格波动率

volatility = (high – low) / close * 100。

构建复合指数

volatility_index = vol_percent * volatility,并分别计算其短期与长期均线(乘以 index_magnification)。

动态阈值

index_threshold = index_long_ma * index_threshold_magnification,过滤常规波动。

三、信号生成与策略执行

做多/做空信号

当短期指数均线自下而上突破长期均线,且 volatility_index 突破 index_threshold 时,发出做多信号。

当短期指数均线自上而下跌破长期均线,且 volatility_index 跌破 index_threshold 时,发出做空信号。

反转信号模式(可选)

若 enable_reversal = true,则所有做空信号反向为做多,用于在强趋势行情中加仓。

止盈止损管理

进场后自动设置斐波那契止盈位(基于入场价 × fib_tp_ratio)和止损位(入场价 × fib_sl_ratio)。

支持多级止盈:可依次以 0.382、0.618 等黄金分割比率分批平仓。

四、图表展示

策略信号标记:图上用箭头标明每次做多/做空(或反转加仓)信号。

斐波那契区间:在K线图中显示止盈/止损水平线。

复合指数与阈值线:与原版相同,在独立窗口绘制短、长期指数均线、指数曲线及阈值。

量能柱状:高于均线时染色,反转模式时额外高亮。

Strategy Name

Volume and Volatility Ratio Strategy – WODI

1. User-Defined Parameters

vol_length: Length for volume SMA.

index_short_length / index_long_length: Short and long MA lengths for the composite index.

index_magnification: Sensitivity multiplier for index MAs.

index_threshold_magnification: Threshold multiplier to filter noise.

lookback_bars: Number of bars to look back for pattern detection.

fib_tp_ratio / fib_sl_ratio: Fibonacci take-profit and stop-loss ratios (e.g. 0.618, 0.382).

enable_reversal: Toggle for reversal mode; flips short signals to long for trend-following add-on entries.

2. Core Calculation

Volume Percentage:

vol_ma = ta.sma(volume, vol_length)

vol_percent = volume / vol_ma * 100

Volatility:

volatility = (high – low) / close * 100

Composite Index:

volatility_index = vol_percent * volatility

Short/long MAs applied and scaled by index_magnification.

Dynamic Threshold:

index_threshold = index_long_ma * index_threshold_magnification.

3. Signal Generation & Execution

Long/Short Entries:

Long when short MA crosses above long MA and volatility_index > index_threshold.

Short when short MA crosses below long MA and volatility_index < index_threshold.

Reversal Mode (optional):

If enable_reversal is on, invert all short entries to long to scale into trending moves.

Fibonacci Take-Profit & Stop-Loss:

Automatically set TP/SL levels at entry price × respective Fibonacci ratios.

Supports multi-stage exits at 0.382, 0.618, etc.

4. Visualization

Signal Arrows: Marks every long/short or reversal-add signal on the chart.

Fibonacci Zones: Plots TP/SL lines on the price panel.

Index & Threshold: Same as v1.0, with MAs, index curve, and threshold in a separate sub-window.

Volume Bars: Colored when above vol_ma; extra highlight if a reversal-add signal triggers

[blackcat] L1 Multi-Component CCIOVERVIEW

The " L1 Multi-Component CCI" is a sophisticated technical indicator designed to analyze market trends and momentum using multiple components of the Commodity Channel Index (CCI). This script calculates and combines various CCI-related metrics to provide a comprehensive view of price action, offering traders deeper insights into market dynamics. By integrating smoothed deviations, normalized ranges, and standard CCI values, this tool aims to enhance decision-making processes. It is particularly useful for identifying potential reversal points and confirming trend strength. 📈

FEATURES

Multi-Component CCI Calculation: Combines smoothed deviation, normalized range, percent above low, and standard CCI for a holistic analysis, providing a multifaceted view of market conditions.

Threshold Lines: Overbought (200), oversold (-200), bullish (100), and bearish (-100) thresholds are plotted for easy reference, helping traders quickly identify extreme market conditions.

Visual Indicators: Each component is plotted with distinct colors and line styles for clear differentiation, making it easier to interpret the data at a glance.

Customizable Alerts: The script includes commented-out buy and sell signal logic that can be enabled for automated trading notifications, allowing traders to set up alerts based on specific conditions. 🚀

Advanced Calculations: Utilizes a combination of simple moving averages (SMA) and exponential moving averages (EMA) to smooth out price data, enhancing the reliability of the indicator.

HOW TO USE

Apply the Script: Add the script to your chart on TradingView by searching for " L1 Multi-Component CCI" in the indicators section.

Observe the Plotted Lines: Pay close attention to the smoothed deviation, normalized range, percent above low, and standard CCI lines to identify potential overbought or oversold conditions.

Use Threshold Levels: Refer to the overbought, oversold, bullish, and bearish threshold lines to gauge extreme market conditions and potential reversal points.

Confirm Trends: Use the standard CCI line to confirm trend direction and momentum shifts, providing additional confirmation for your trading decisions.

Enable Alerts: If desired, uncomment the buy and sell signal logic to receive automated alerts when specific conditions are met, helping you stay informed even when not actively monitoring the chart. ⚠️

LIMITATIONS

Fixed Threshold Levels: The script uses fixed threshold levels (200, -200, 100, -100), which may need adjustment based on specific market conditions or asset volatility.

No Default Signals: The buy and sell signal logic is currently commented out, requiring manual activation if you wish to use automated alerts.

Complexity: The multi-component approach, while powerful, may be complex for novice traders to interpret, requiring a solid understanding of technical analysis concepts. 📉

Not for Isolation Use: This indicator is not designed for use in isolation; it is recommended to combine it with other tools and indicators for confirmation and a more robust analysis.

NOTES

Smoothing Techniques: The script uses a combination of simple moving averages (SMA) and exponential moving averages (EMA) for smoothing calculations, which helps in reducing noise and enhancing signal clarity.

Multi-Component Approach: The multi-component approach aims to provide a more nuanced view of market conditions compared to traditional CCI, offering a more comprehensive analysis.

Customization Potential: Traders can customize the script further by adjusting the parameters of the moving averages and other components to better suit their trading style and preferences. ✨

THANKS

Thanks to the TradingView community for their support and feedback on this script! Special thanks to those who contributed ideas and improvements, making this tool more robust and user-friendly. 🙏

Adaptive Volume-Weighted RSI (AVW-RSI)Concept Summary

The AVW-RSI is a modified version of the Relative Strength Index (RSI), where each price change is weighted by the relative trading volume for that period. This means periods of high volume (typically driven by institutions or “big money”) have a greater influence on the RSI calculation than periods of low volume.

Why AVW-RSI Helps Traders

Avoids Weak Signals During Low Volume

Standard RSI may show overbought/oversold zones even during low-volume periods (e.g., during lunch hours or after news).

AVW-RSI gives less weight to these periods, avoiding misleading signals.

Amplifies Strong Momentum Moves

If RSI is rising during high volume, it's more likely driven by institutional buying—AVW-RSI reflects that stronger by weighting the RSI component.

Filters Out Retail Noise

By prioritizing high-volume candles, it naturally discounts fakeouts caused by thin markets or retail-heavy moves.

Highlights Institutional Entry/Exit

Useful for spotting hidden accumulation/distribution that classic RSI would miss.

How It Works (Calculation Logic)

Traditional RSI Formula Recap

RSI = 100 - (100 / (1 + RS))

RS = Average Gain / Average Loss (over N periods)

Modified Step – Apply Volume Weight

For each period

Gain_t = max(Close_t - Close_{t-1}, 0)

Loss_t = max(Close_{t-1} - Close_t, 0)

Weight_t = Volume_t / AvgVolume(N)

WeightedGain_t = Gain_t * Weight_t

WeightedLoss_t = Loss_t * Weight_t

Weighted RSI

AvgWeightedGain = SMA(WeightedGain, N)

AvgWeightedLoss = SMA(WeightedLoss, N)

RS = AvgWeightedGain / AvgWeightedLoss

AVW-RSI = 100 - (100 / (1 + RS))

Visual Features on Chart

Line Color Gradient

Color gets darker as volume weight increases, signaling stronger conviction.

Overbought/Oversold Zones

Traditional: 70/30

Suggested AVW-RSI zones: Use dynamic thresholds based on historical volatility (e.g., 80/20 for high-volume coins).

Volume Spike Flags

Mark RSI turning points that occurred during volume spikes with a special dot/symbol.

Trading Strategies with AVW-RSI

1. Weighted RSI Divergence

Regular RSI divergence becomes more powerful when volume is high.

AVW-RSI divergence with volume spike is a strong signal of reversal.

2. Trend Confirmation

RSI crossing above 50 during rising volume is a good entry signal.

RSI crossing below 50 with high volume is a strong exit or short trigger.

3. Breakout Validation

Price breaking resistance + AVW-RSI > 60 with volume = Confirmed breakout.

Price breaking but AVW-RSI < 50 or on low volume = Potential fakeout.

Example Use Case

Stock XYZ is approaching a resistance zone. A trader sees:

Standard RSI: 65 → suggests strength.

Volume is 3x the average.

AVW-RSI: 78 → signals strong momentum with institutional backing.

The trader enters confidently, knowing this isn't just low-volume hype.

Limitations / Tips

Works best on liquid assets (Forex majors, large-cap stocks, BTC/ETH).

Should be used alongside price action and volume analysis—not standalone.

Periods of extremely high volume (news events) might need smoothing to avoid spikes.

Breadth-Driven Swing StrategyWhat it does

This script trades the S&P 500 purely on market breadth extremes:

• Data source : INDEX:S5TH = % of S&P 500 stocks above their own 200-day SMA (range 0–100).

• Buy when breadth is washed-out.

• Sell when breadth is overheated.

It is long-only by design; shorting and ATR trailing stops have been removed to keep the logic minimal and transparent.

⸻

Signals in plain English

1. Long entry

A. A 200-EMA trough in breadth is printed and the trough value is ≤ 40 %.

or

B. A 5-EMA trough appears, its prominence passes the user threshold, and the lowest breadth reading in the last 20 bars is ≤ 20 %.

(Toggle this secondary trigger on/off with “ Enter also on 5-EMA trough ”.)

2. Exit (close long)

First 200-EMA peak whose breadth value is ≥ 70 %.

3. Risk control

A fixed stop-loss (% of entry price, default 8 %) is attached to every long trade.

⸻

Key parameters (defaults shown)

• Long EMA length 200 • Short EMA length 5

• Peak prominence 0.5 pct-pts • Trough prominence 3 pct-pts

• Peak level 70 % • Trough level 40 % • 5-EMA trough level 20 %

• Fixed stop-loss 8 %

• “Enter also on 5-EMA trough” = true (allows additional entries on extreme momentum reversals)

Feel free to tighten or relax any of these thresholds to match your risk profile or account for different market regimes.

⸻

How to use it

1. Load the script on a daily SPX / SPY chart.

(The price chart drives order execution; the breadth series is pulled internally and does not need to be on the chart.)

2. Verify the breadth feed.

INDEX:S5TH is updated after each session; your broker must provide it.

3. Back-test across several cycles.

Two decades of daily data is recommended to see how the rules behave in bear markets, range markets, and bull trends.

4. Adjust position sizing in the Properties tab.

The default is “100 % of equity”; change it if you prefer smaller allocations or pyramiding caps.

⸻

Why it can help

• Breadth signals often lead price, allowing entries before index-level momentum turns.

• Simple, rule-based exits prevent “waiting for confirmation” paralysis.

• Only one input series—easy to audit, no black-box math.

Trade-offs

• Relies on a single breadth metric; other internals (advance/decline, equal-weight returns, etc.) are ignored.

• May sit in cash during shallow pullbacks that never push breadth ≤ 40 %.

• Signals arrive at the end of the session (breadth is EoD data).

⸻

Disclaimer

This script is provided for educational purposes only and is not financial advice. Markets are risky; test thoroughly and use your own judgment before trading real money.

ストラテジー概要

本スクリプトは S&P500 のマーケットブレッド(内部需給) だけを手がかりに、指数をスイングトレードします。

• ブレッドデータ : INDEX:S5TH

(S&P500 採用銘柄のうち、それぞれの 200 日移動平均線を上回っている銘柄比率。0–100 %)

• 買い : ブレッドが極端に売られたタイミング。

• 売り : ブレッドが過熱状態に達したタイミング。

余計な機能を削り、ロングオンリー & 固定ストップ のシンプル設計にしています。

⸻

シグナルの流れ

1. ロングエントリー

• 条件 A : 200-EMA がトラフを付け、その値が 40 % 以下

• 条件 B : 5-EMA がトラフを付け、

・プロミネンス条件を満たし

・直近 20 本のブレッドス最小値が 20 % 以下

• B 条件は「5-EMA トラフでもエントリー」を ON にすると有効

2. ロング決済

最初に出現した 200-EMA ピーク で、かつ値が 70 % 以上 のバーで手仕舞い。

3. リスク管理

各トレードに 固定ストップ(初期価格から 8 %)を設定。

⸻

主なパラメータ(デフォルト値)

• 長期 EMA 長さ : 200 • 短期 EMA 長さ : 5

• ピーク判定プロミネンス : 0.5 %pt • トラフ判定プロミネンス : 3 %pt

• ピーク水準 : 70 % • トラフ水準 : 40 % • 5-EMA トラフ水準 : 20 %

• 固定ストップ : 8 %

• 「5-EMA トラフでもエントリー」 : ON

相場環境やリスク許容度に合わせて閾値を調整してください。

⸻

使い方

1. 日足の SPX / SPY チャート にスクリプトを適用。

2. ブレッドデータの供給 (INDEX:S5TH) がブローカーで利用可能か確認。

3. 20 年以上の期間でバックテスト し、強気相場・弱気相場・レンジ局面での挙動を確認。

4. 資金配分 は プロパティ → 戦略実行 で調整可能(初期値は「資金の 100 %」)。

⸻

強み

• ブレッドは 価格より先行 することが多く、天底を早期に捉えやすい。

• ルールベースの出口で「もう少し待とう」と迷わずに済む。

• 入力 series は 1 本のみ、ブラックボックス要素なし。

注意点・弱み

• 単一指標に依存。他の内部需給(A/D ライン等)は考慮しない。

• 40 % を割らない浅い押し目では機会損失が起こる。

• ブレッドは終値ベースの更新。ザラ場中の変化は捉えられない。

⸻

免責事項

本スクリプトは 学習目的 で提供しています。投資助言ではありません。

実取引の前に必ず自己責任で十分な検証とリスク管理を行ってください。

NasyI## NasyI - Multi-Timeframe Technical Analysis Toolkit

### English Description

**NasyI** is a comprehensive technical analysis indicator designed to provide traders with a complete view of market dynamics across multiple timeframes. This indicator combines the power of Exponential Moving Averages (EMAs), Simple Moving Averages (MAs), Volume Weighted Average Price (VWAP), and key support/resistance levels to help traders identify trend direction, potential reversal points, and optimal entry/exit opportunities.

#### Key Features

1. **Multi-Timeframe Analysis System**

- 2-minute EMAs (13, 48) for ultra-short-term trend identification

- 5-minute EMAs (9, 13, 21, 48, 200) for short-term trend confirmation

- Daily EMAs (5, 13, 21, 48, 100, 200) and MAs (20, 50, 100, 200) for longer-term perspective

- Color-coded bands between key EMAs to visually identify trend strength and direction

2. **Advanced VWAP Integration**

- Daily VWAP for intraday support/resistance

- Weekly VWAP for medium-term price reference

- Monthly VWAP for long-term institutional price levels

- All VWAPs properly reset at their respective time period boundaries

3. **Critical Price Level Identification**

- Previous day high/low lines for identifying key breakout and breakdown levels

- Pre-market high/low tracking to identify potential intraday support/resistance zones

- All levels displayed with distinct line styles for easy identification

4. **Dynamic Trend Analysis**

- Color-coded bands between EMAs display trend strength and direction:

- Green bands indicate uptrend conditions (9 EMA > 21 EMA > 48 EMA)

- Red bands indicate downtrend conditions (9 EMA < 21 EMA < 48 EMA)

- Yellow bands indicate neutral/confused market conditions

- Visual representation makes trend changes immediately apparent

5. **Comprehensive Customization Options**

- Fully customizable colors for all indicators and bands

- Adjustable transparency settings for visual clarity

- Optional price labels with customizable placement and appearance

- Ability to show/hide specific components based on trading preferences

#### Trading Applications

This indicator is particularly valuable for:

1. **Day Trading & Scalping**: The 2-minute and 5-minute EMAs with color bands provide clear short-term trend direction and potential reversal signals.

2. **Swing Trading**: Daily EMAs and MAs offer perspective on the larger trend, helping to align short-term trades with the broader market direction.

3. **Gap Trading**: Previous day and pre-market levels help identify potential gap fill scenarios and breakout/breakdown opportunities.

4. **VWAP Trading Strategies**: Multiple timeframe VWAPs allow for identifying institutional participation levels and potential reversal zones.

5. **EMA Cross Systems**: The various EMAs can be used to identify golden crosses and death crosses across multiple timeframes.

#### How the Components Work Together

The power of NasyI comes from the integration of these different technical elements:

1. The short-timeframe EMAs (2m, 5m) provide immediate trend information, while the daily EMAs/MAs provide context about the larger market structure.

2. The color bands between EMAs offer instant visual confirmation of trend alignment or divergence across timeframes.

3. Previous day and pre-market levels add horizontal support/resistance zones to complement the dynamic moving averages.

4. Multiple timeframe VWAPs provide additional confirmation of institutional activity levels and potential reversal points.

By combining these elements, traders can develop a comprehensive market view that integrates price action, trend direction, and key support/resistance levels all in one indicator.

#### Usage Instructions

1. Apply the NasyI indicator to your chart (works best on intraday timeframes from 1-minute to 30-minute).

2. Observe the relationship between price and the various EMAs:

- Price above the 2m/5m EMAs with green bands indicates bullish short-term conditions

- Price below the 2m/5m EMAs with red bands indicates bearish short-term conditions

3. Use the daily EMAs/MAs and VWAPs as targets for potential price movements and reversal zones.

4. Previous day and pre-market high/low lines provide key levels to watch for breakouts or breakdowns.

5. Customize the appearance according to your preferences using the extensive settings options.

This indicator represents a unique approach to technical analysis by combining multiple timeframe perspectives into a single, visually intuitive display that helps traders make more informed decisions based on a comprehensive view of market conditions.

### 中文描述

**NasyI** 是一个全面的技术分析指标,旨在为交易者提供跨多个时间周期的完整市场动态视图。该指标结合了指数移动平均线(EMA)、简单移动平均线(MA)、成交量加权平均价格(VWAP)和关键支撑/阻力水平的力量,帮助交易者识别趋势方向、潜在反转点和最佳进出场机会。

#### 主要特点

1. **多时间周期分析系统**

- 2分钟EMAs(13,48)用于超短期趋势识别

- 5分钟EMAs(9,13,21,48,200)用于短期趋势确认

- 日线EMAs(5,13,21,48,100,200)和MAs(20,50,100,200)用于更长期的视角

- 关键EMAs之间的彩色带状区域直观显示趋势强度和方向

2. **高级VWAP整合**

- 日内VWAP作为日内支撑/阻力

- 周内VWAP作为中期价格参考

- 月内VWAP作为长期机构价格水平

- 所有VWAP在各自的时间周期边界正确重置

3. **关键价格水平识别**

- 前一交易日高点/低点线用于识别关键突破和跌破水平

- 盘前高点/低点跟踪用于识别潜在的日内支撑/阻力区域

- 所有水平以不同的线条样式显示,便于识别

4. **动态趋势分析**

- EMAs之间的彩色带状区域显示趋势强度和方向:

- 绿色带状区域表示上升趋势(9 EMA > 21 EMA > 48 EMA)

- 红色带状区域表示下降趋势(9 EMA < 21 EMA < 48 EMA)

- 黄色带状区域表示中性/混乱市场条件

- 视觉表示使趋势变化立即显现

5. **全面的自定义选项**

- 所有指标和带状区域的颜色完全可定制

- 可调节的透明度设置,提高视觉清晰度

- 可选的价格标签,带有可定制的位置和外观

- 能够根据交易偏好显示/隐藏特定组件

#### 交易应用

此指标对以下方面特别有价值:

1. **日内交易和短线交易**:2分钟和5分钟EMAs与色带提供清晰的短期趋势方向和潜在反转信号。

2. **摇摆交易**:日线EMAs和MAs提供对更大趋势的视角,帮助将短期交易与更广泛的市场方向对齐。

3. **缺口交易**:前一日和盘前水平帮助识别潜在的缺口填充情况和突破/跌破机会。

4. **VWAP交易策略**:多时间周期VWAP允许识别机构参与水平和潜在反转区域。

5. **EMA交叉系统**:各种EMAs可用于识别跨多个时间周期的黄金交叉和死亡交叉。

#### 组件如何协同工作

NasyI的强大之处在于这些不同技术元素的集成:

1. 短时间周期EMAs(2m,5m)提供即时趋势信息,而日线EMAs/MAs提供关于更大市场结构的背景。

2. EMAs之间的色带提供趋势对齐或跨时间周期分歧的即时视觉确认。

3. 前一日和盘前水平添加水平支撑/阻力区域,补充动态移动平均线。

4. 多时间周期VWAP提供机构活动水平和潜在反转点的额外确认。

通过结合这些元素,交易者可以发展出全面的市场视图,整合价格行动、趋势方向和关键支撑/阻力水平于一个指标中。

#### 使用说明

1. 将NasyI指标应用到您的图表上(最适合1分钟至30分钟的日内时间周期)。

2. 观察价格与各种EMAs之间的关系:

- 价格位于2m/5m EMAs之上,带有绿色带状区域,表示看涨的短期条件

- 价格位于2m/5m EMAs之下,带有红色带状区域,表示看跌的短期条件

3. 使用日线EMAs/MAs和VWAPs作为潜在价格移动和反转区域的目标。

4. 前一日和盘前高点/低点线提供需要关注的突破或跌破的关键水平。

5. 使用广泛的设置选项根据您的偏好自定义外观。

这个指标代表了一种独特的技术分析方法,将多个时间周期的视角结合到一个单一的、视觉直观的显示中,帮助交易者基于对市场条件的全面视图做出更明智的决策。

Multi-Timeframe EMAsMulti Timeframe EMA's

The 'Multi-Timeframe EMA Band Comparison' indicator is a tool designed to analyze trend direction across multiple timeframes using Exponential Moving Averages. it calculates the 50, 100, and 200 period EMAs for fiver user defined timeframes and compares their relationships to provide a visual snapshot of bullish or bearish momentum.

How it Works:

EMA Calculations: For each selected timeframe, the indicator computes the 50, 100, and 200 period EMAs based on the closing price.

Band Comparisons: Three key relationships are evaluated:

50 EMA vs 100 EMA

100 EMA vs 200 EMA

50 EMA vs 200 EMA

Scoring System: Each comparison is assigned a score:

🟢 (Green Circle): The shorter EMA is above the longer EMA, signaling bullish momentum.

🔴 (Red Circle): The shorter EMA is below the longer EMA, signaling bearish momentum.

⚪️ (White Circle): The EMAs are equal or data is unavailable (rare).

Average Score:

An overall average score is calculated across all 15 comparisons ranging from 1 to -1, displayed with two decimal places and color coded.

Customization:

This indicator is fully customizable from the timeframe setting to the color of the table. The only specific part that is not changeable is the EMA bands.

McClellan Oscillator - IRUS Optimized🧠 McClellan Oscillator (IRUS Index)

Type: Market Breadth Indicator

Category: Breadth, Momentum

Purpose: Gauge the internal strength of the IRUS index and anticipate trend reversals

📌 Based on

This indicator is built on the concept of advancing vs. declining issues — the number of stocks rising vs. falling each day within the IRUS index (a custom group of 40 Russian stocks).

It calculates the net advances (advancers minus decliners), then applies two exponential moving averages (EMA):

java

Copy

Edit

McClellan Oscillator = EMA_19(Net Advances) - EMA_39(Net Advances)

Where:

Net Advances = Number of advancing stocks - Number of declining stocks

Calculated from a fixed set of 40 IRUS stocks

🧭 What it shows

Above 0 → more stocks are rising: market is internally strong.

Below 0 → more stocks are falling: underlying weakness.

Rising from below -100 → oversold breadth, possible bullish reversal.

Falling from above +100 → overbought breadth, possible correction.

🎯 How to use it

1. Buy/Sell Signals

Buy: Oscillator drops below -100 and turns up → oversold, potential rally.

Sell: Oscillator rises above +100 and turns down → overbought, risk of pullback.

2. Trend Strength Confirmation

Sustained above 0 → confirms bullish trend.

Crosses below 0 → early warning of weakening market breadth.

3. Divergences with IRUS Price

IRUS rises, but Oscillator falls → narrowing leadership, bearish divergence.

IRUS falls, but Oscillator rises → improving breadth, bullish divergence.

⚠️ Notes

The oscillator measures participation, not price.

Works best with daily timeframe.

Does not account for volume or magnitude of price moves.

Use with price action or other indicators for confirmation.

⚙️ Custom Implementation

This version is specifically adapted for the IRUS index, using a fixed list of 40 component stocks.

Optimized for Pine Script v6 and complies with TradingView's request limits (max 40).

VIX Implied MovesKey Features:

Three Timeframe Bands:

Daily: Blue bands showing ±1σ expected move

Weekly: Green bands showing ±1σ expected move

30-Day: Red bands showing ±1σ expected move

Calculation Methodology:

Uses VIX's annualized volatility converted to specific timeframes using square root of time rule

Trading day convention (252 days/year)

Band width = Price × (VIX/100) ÷ √(number of periods)

Visual Features:

Colored semi-transparent backgrounds between bands

Progressive line thickness (thinner for shorter timeframes)

Real-time updates as VIX and ES prices change

Example Calculation (VIX=20, ES=5000):

Daily move = 5000 × (20/100)/√252 ≈ ±63 points

Weekly move = 5000 × (20/100)/√50 ≈ ±141 points

Monthly move = 5000 × (20/100)/√21 ≈ ±218 points

This indicator helps visualize expected price ranges based on current volatility conditions, with wider bands indicating higher market uncertainty. The probabilistic ranges represent 68% confidence levels (1 standard deviation) derived from options pricing.

Volume Profile [ActiveQuants]The Volume Profile indicator visualizes the distribution of trading volume across price levels over a user-defined historical period. It identifies key liquidity zones, including the Point of Control (POC) (price level with the highest volume) and the Value Area (price range containing a specified percentage of total volume). This tool is ideal for traders analyzing support/resistance levels, market sentiment , and potential price reversals .

█ CORE METHODOLOGY

Vertical Price Rows: Divides the price range of the selected lookback period into equal-height rows.

Volume Aggregation: Accumulates bullish/bearish or total volume within each price row.

POC: The row with the highest total volume.

Value Area: Expands from the POC until cumulative volume meets the user-defined threshold (e.g., 70%).

Dynamic Visualization: Rows are plotted as horizontal boxes with widths proportional to their volume.

█ KEY FEATURES

- Customizable Lookback & Resolution

Adjust the historical period ( Lookback ) and granularity ( Number of Rows ) for precise analysis.

- Configurable Profile Width & Horizontal Offset

Control the relative horizontal length of the profile rows, and set the distance from the current bar to the POC row’s anchor.

Important: Do not set the horizontal offset too high. Indicators cannot be plotted more than 500 bars into the future.

- Value Area & POC Highlighting

Set the percentage of total volume required to form the Value Area , ensuring that key volume levels are clearly identified.

Value Area rows are colored distinctly, while the POC is marked with a bold line.

- Flexible Display Options

Show bullish/bearish volume splits or total volume.

Place the profile on the right or left of the chart.

- Gradient Coloring

Rows fade in color intensity based on their relative volume strength .

- Real-Time Adjustments

Modify horizontal offset, profile width, and appearance without reloading.

█ USAGE EXAMPLES

Example 1: Basic Volume Profile with Value Area

Settings:

Lookback: 500 bars

Number of Rows: 100

Value Area: 70%

Display Type: Up/Down

Placement: Right

Image Context:

The profile appears on the right side of the chart. The POC (orange line) marks the highest volume row. Value Area rows (green/red) extend above/below the POC, containing 70% of total volume.

Example 2: Total Volume with Gradient Colors

Settings:

Lookback: 800 bars

Number of Rows: 100

Profile Width: 60

Horizontal Offset: 20

Display Type: Total

Gradient Colors: Enabled

Image Context:

Rows display total volume in a single color with gradient transparency. Darker rows indicate higher volume concentration.

Example 3: Left-Aligned Profile with Narrow Value Area

Settings:

Lookback: 600 bars

Number of Rows: 100