.BXBT IndexThe current .BXBT index weighted as close as possible to BitMEX's with updates as BitMEX refreshes their index.

Difference between this and the script titled '2020 March 27 .BXBT Index': this one will receive updates because it doesn't have a date in its title.

Methodology

www.bitmex.com

"BitMEX Index Weights, assuming no constituent exchanges have been excluded due to Index Protection Rules, last updated 27 December 2019 at 12:00:05 UTC."

Binance: -

Bitstamp: 10.61%

Bittrex: 2.53%

Coinbase: 52.30%

Gemini: 6.89%

Huobi: -

Itbit: 4.21%

Kraken: 23.46%

Poloniex: -

ItBit's weight is combined with Gemini's due to ItBit not being on TradingView as of now. BITTREX:BTCUSD substituted with BITTREX:BTCUSDT*POLONIEX:USDTUSD to backfill because Bittrex only recently (late 2018) started to offer a fiat BTC/USD pair. Not that it matters since the index used in 2018 didn't include Bittrex if I remember correctly.

What is actually used for 27/12/2019 to 27/03/2020:

Binance: -

Bitstamp: 10.61%

Bittrex: 2.53%

Coinbase: 52.30%

Gemini: 11.10%

Huobi: -

Itbit: -

Kraken: 23.46%

Poloniex: -

Options:

Toggle candlesticks or close line

Change price source to be used for indicators

To be added: Change quarter to show indexes for different times, with labels that apply to the appropriate index used

Reasons to use this vs. the index itself: (not many)

It is helpful as a reference for other indicators or creation of an index.

在脚本中搜索"12月4号是什么星座"

Hourly 50\100\200 EMA on 5M barsHello. This script was created for traders using a 5 minute timeframe. The script allows you to plot EMA from a higher level timeframe. Its formula includes the multiplication of the classical values of 50/100/200 EMA by 12, because in one hour it is 12 times for 5 minutes. You must use script only at 5M timeframe, because his interval is unique and not compare with other timeframes.

Often, an hourly EMA on a 5-minute timeframe becomes a strong level of support or price resistance. You can use this script on 5M timeframe with "daily 50/100/200 EMA" script on 1H timeframe for best scalping results.

Good luck in trading!

CCI strategy on OIL1HThis indicator is based on Commodity Channel Index.

It buys when CCI on period 200 is under -130 and it´s rising last 12 bars. It closes the position by hitting Take Profit, Stop Loss or opening short position.

It sells when CCI on period 200 is over 130 and it´s falling last 12 bars. It closes the position by hitting Take Profit, Stop Loss or opening short position.

This strategy seems to working just on USOIL on 1 hour chart. This can predict that it´s just luck and not proper strategy or indicator I would use for trading.

This script is just for educational purposes and that´s why the script is open. I will be happy if you will leave comment and try to come up with some ideas how to improve this strategy, so it can be used also on other commodities/forex pairs.

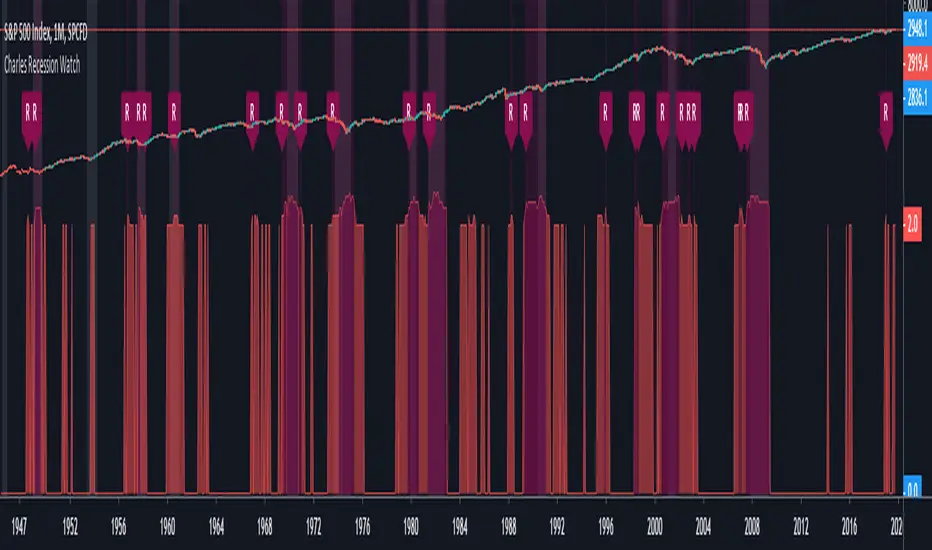

Charles Recession WatchThe “Recession Watch” indicator tracks 7 key economic metrics which have historically preceded US recessions. It provides a real-time indication of incoming recession risk.

This indicator gives a picture of when risk is increasing, and therefore when you might want to start taking some money out of risky assets.

All of the last seven recessions were preceded by a risk score of 3 or higher. Six of them were preceded by a risk score of 4 or higher. Unfortunately data prior to 1965 was inconsistent and prior recessions could not be considered.

Based on the indicator hit rate at successfully flagging recessions over the last 50 years, risk scores have the following approximate probabilities of recession:

- 0-1: Low

- 2: 25% within next 18 months

- 3: 30% within next 12 months

- 4-7: 50% within next 12 months

Note that a score of 3 is not necessarily a cause for panic. After all, there are substantial rewards to be had in the lead up to recessions (averaging 19% following yield curve inversion). For the brave, staying invested until the score jumps to 4+, or until the S&P500 drops below the 200day MA, will likely yield the best returns.

Notes on use:

- use MONTHLY time period only (the economic metrics are reported monthly)

- If you want to view the risk Score (1-7) you need to set your chart axis to "Logarithmic"

Enjoy and good luck!

ATR - Baby WhaleScript that shows you the ATR and 0.5 ATR.

You can use this to define your stop loss level when you see a SFP.

Standard setting is the 24 period ATR. You can use this for a 1h chart (24 hours in a day).

So when you play on a 5m chart, you can change the setting to 12 period (12 5m candles in 1 hour).

Saturn–Pluto Cycle

Indicator colors background of the chart in the following way:

Saturn - Pluto Cycle in conjunction: Blue

Saturn - Pluto Cycle in opposition: Yellow

While opposition periods are indicated according to the actual date ranges an opposition occurs, conjunctions last only for one day.

Conjunctions indicated with this indicator mark a period around the actual conjunction date.

The actual date a conjunction occurs is indicated in the script.

Following the dates which were considered for this indicator:

Dates of Saturn–Pluto Conjunctions

October 5, 1914 at 2° Cancer (recurrence on May 20, 1915)

August 11, 1947 at 13° Leo

November 8, 1982 at 27° Libra

January 12, 2020 at 22° Capricorn

Dates of Saturn–Pluto Oppositions

February 17, 1931 – December 13, 1931 at 19°–21° Capricorn–Cancer (conjunct their respective North and South Nodes)

April 23, 1965 – February 20, 1966 at 14°–17° Pisces–Virgo

August 5, 2001 – May 26, 2002 at 12°–16° Gemini–Sagittarius (conjunct the lunar nodes)

Consensio Vision MA - Tribute to Late Dean Tyler JenksA wonderful mentor, fearless leader and incredibly humble man, father alike and world renowned bitcoin influencer also known for the invention of robust money management system named consensio moving averages, Tribute to Late Dean Tyler Jenks who made this possible.

Explanation

this indicator make use of three simple moving averages, idea is to incrementally invest little by little in the bull market when all moving average is moving up

A more in-depth guide for consensio is available here

How to use this indicator?

This indicator plots weekly moving average on daily and/or hourly time frame, the basic idea is to see how smaller time frame like daily and hourly trend reacts to larger time frame like weekly moving averages and what are the possible support and resistance area on these smaller time frame and also to arrive at better entry points while doing that.

The name Consensio Vision is chosen cuz.. it's a free reminder to never loose long-term vision (in this case weekly trend) of where you're going

Consensio Vision MA - Tribute to Late Dean Tyler Jenks

Lucid's Principles Of Investing - These are principles foretold by Late dean tyler jenks.. he goes on to saying that those 12 principles will keep you out of trouble or will identify trouble or will identify your human behavioral problems

1. CASH IS KING - in terms of my investing principles is very simple cash is king, I would rather be in cash than any other asset class, unless an asset class is trending to the upside (or bull market) the cash is king

2. Market doesn't move in straight line - all asset classes trimmed up and down, as tyler goes on to say he dont believe in buy and hold strategy, i'm giving you the tools to get you out of market so you dont have drive down bear events like 2009 crash, he further suggests you sould react (or make decision) before a 10% drop in market.

3. Timeframe - trends are short days or weeks intermediate weeks or months and long months or years so principle number three is don't just talk about something is in a trend be precise are you talking about a short-term trend an intermediate term trend or a long-term trend...

just saying something is in a trend is irresponsible, you've got to identify your time frame

4. Wait! Bear market is different - cash is king and unless asset class is trending up there are times that you want to take advantage of a trend that is down but it is not the equivalent of investing in a trend that is up it is far more dangerous far more difficult it can be done but that's not one of the main principles, (also check rule number 7 as both are related)

5. Only long-term trends are investments - word trading is not really an investment term trading means buying or selling it has nothing to do with what you're attempting to achieve in terms of either speculation gambling investing ... those are not opportunities for investing because they're short or they're intermediate.. that doesn't mean that you can't speculate and have that turn into a position trade and have it turn into a possible swing trade and then have it turn in to an investment however be prepared once you've made an investment where that investment in a short or an intermediate term time frame to move against you

6. Never invest in a FOMO (fear of missing out)- loss of money loss of cash loss of wealth is not equivalent to a loss of opportunity

it is 100 times more important than a loss of opportunity

7. understand the importance of Percentage - a 50% gain is not an inverse equivalence of a 50% loss that is the single most important rule or principle that Lucid uses in determining when to get into or out of an investment and it goes back to number six that a loss of money is not equivalent to a loss of opportunity

8. all long-term trends are fundamentally based, repeat all long-term trends are fundamentally based

9. number nine is a corollary but it's separate all short and intermediate term trends are not fundamentally based, long term trends are not affected by news are not affected by headlines are not affected by company announcements or country announcements they are affected in the short in the intermediate term and therefore your probability of success goes way up as your timeframe frame goes longer

10. Fundamental vs technical - technical tools are invaluable in identifying trends fundamental tools are not invaluable in identifying trends - that's why technical analysis is so important it gives you something that fundamental analysis will never give you in time so technical a pro active mechanism or money management tool and fundamental is a lagging indicator hoever its what drives the market in log term

11. Profitability based on time aka VISION- I see even very sophisticated investors doing is they let the technical tools give them a signal on the short-termer intermediate-term and they believe because it's the tool that they're using that it's giving them an equivalent probability of success and it is not!

it's probability of success at the short-term is less than at the intermediate term and is less than at the long-term

12. the last one long-term trends are more important than intermediate which are more important than short term, tyler developed a scale where he ranks

long-term trend 5,

intermediate term trend 3,

short-term with a 1

(note: if you add both 3 & 1 its still smaller then 5)

if you add together my intermediate term weighting of 3 and the short term weighting of 1 that you do not equal the long term weighting of 5 that means that both the short and the intermediate term can be going in a direction but that does not negate the direction of the long term trend it's a simple way of looking at it and I use the word in number 12 important not simply to mean importance in terms of the weighting system but the probability of success of each of those 3

so if you're using a short term 15 minute 30 minute one hour signals or probability of success drops dramatically and therefore you've got to factor in where your stops are relative to that probability when you're in a long term trend a five waiting you don't need to use stops when you're in an intermediate term trend you've got to use stops and when you're in a short term trend you've got to use closed stops

official website- lucidinvestmentstrategies.com

A.I.Driven TradersAI Model Trades for 20190612The entry and exit levels here are NOT derived from any specific indicator but are coming from our A.I. driven proprietary models.

This is an attempt at exploring the trading community here at TradingView and sharing our daily trading plans published at our site with the community here in the form a Pine Script - just starting and learning this platform. Please help point out any obvious errors or gotchas committed in the scripts. Thanks and have a great trading day!

**** The Trading Plan Published for today ****

>>>> Medium-Frequency Models: <<<<< For today, Wednesday 06/12, our medium-frequency models indicate using the 2895 as a pivot point - opening a long on a break above 2895, and opening a short on a break below 2895 (wait for a close on at least a five minute chart to determine the break), both sides with a 9-point trailing stop.

Note: For the trades to trigger, the breaks should occur during the regular session hours starting at 9:30am ET. By design, these models do NOT open any new positions after 3:45pm. Only one open position at any given time.

>>>>> Aggressive Intraday Models: <<<<< For today, Wednesday 06/12, our aggressive intraday models indicate going long on a break above 2892 or 2875 with an 6-point trailing stop, and going short on a break below 2887 or 2878 with an 8-point trailing stop.

Note: For the trades to trigger, the breaks should occur during regular session hours starting at 9:30am ET. Due to the intraday nature of these aggressive models, they indicate closing any open trades at 3:55pm and remaining flat into the session close. No opening of new positions after 3:45pm. Only one open position at any given time.

Edward EMA 8-21-89-144Explain the application of moving averages through the disk surface:

When the price runs above 89, it only looks for the buy signal.

When the price runs below 89, it only looks for sell signals.

The first step up through the 89 moving average after the first confirmation can buy homeoply,

The first pull down after crossing the 89 moving average for the first time confirms that it can be sold in line with the trend.

Price horizontal finishing, moving average frequently across the field observation.

The yellow area in the interval from 8 to 21 is the homeopathic warehouse addition signal.

When the price is above the 89 moving average, the k-line closes below the 21-day moving average as a callback signal

Prices below the 89 ema close above the 21 - day ema as a rebound signal

After the correction and rebound signals come out, we should make half of the profit and the other half of the stop loss in the break-even place.

Moving average is very suitable for the trend of strong varieties, is not suitable for volatile market.

Only at the end of the shock market moving average upward or downward divergent when it is possible to be used.

1. Repeatedly entangle the mean line of horizontal disk stage and observe it from the field

2. Sell the three EMA moving averages when they can't exceed 89EMA with downward crossing

3, many times can not break the new low when prices go sideways profit

4. Buy when the price reaches 89EMA after the convergence of triangle 3 is broken

5, the Angle of price rise slowed and closed below the 21 moving average when profit

6. Left field observation during transverse oscillation.

Sit tight while news or data cause prices to fall quickly

8. Buy when the price triangle breaks through the 89 moving average upward

9, the price does not rise to slow down when the horizontal closed below the 21 moving average when profit

10, price horizontal shock finishing at the same time the average line also transverse finishing field observation

11, the price of the triangle after finishing through the 89 moving average to buy.At this point all the averages have turned up

12, the second time can not break through the new high when the negative line can profit

13, the price of the first time in the same period of time through 89 after the first step back can be re-bought.

通过盘面讲解均线运用:

价格在89上面运行时时只找买入信号、

价格在89下面运行时只寻找卖出信号、

第一次向上穿过89均线后的第一次回踩确认可以顺势买入、

第一次向下穿过89均线后的第一次回抽确认可以顺势卖出、

价格横盘整理,均线频繁穿越时离场观察。

8-21区间里面黄色区域为顺势加仓信号,

价格在89均线上面时K线收盘在21天均线下面时为回调信号

价格在89均线下面时K线收盘在21天均线上面时为反弹信号

在回调和反弹信号出来之后我们应该获利一半的头寸,另外一半止损放到盈亏平衡的地方。

均线非常适合趋势性很强的品种,并不适合震荡行情。

只有在震荡行情结束时均线向上或向下发散时才有被运用的可能。

1、横盘阶段均线反复纠缠,离场观察

2、三条EMA均线向下交叉回抽无法超越89EMA时卖出

3、多次不能破新低时价格走横时获利

4、价格在3处三角形收敛被突破后站上了89EMA时买入

5、价格上涨角度变缓并收盘在21均线下面时获利

6、横盘震荡时离场观察。

7、见死不救新闻或数据导致价格快速下跌时观望

8、价格三角形向上突破时穿过89均线时买入

9、价格不升减速走横时收盘于21均线下面时获利

10、价格横盘震荡整理同时均线也横向整理时离场观察

11、价格突破三角形整理后重新穿过89均线时买入。此时所有均线已经向上翘头

12、第二次不能突破新高时收阴线可以获利

13、价格在同一个时间周期内第一次穿过89以后的第一次回踩可以重新买入

14、89-144作为牛熊的分水岭。在89-144区域之下只考虑做空,89-144只考虑做多。如果89-144走横则以位置决定高位倾向空低位倾向多。

15、K线会因为指标的设置自动变成两个颜色块,绿色看涨,红色看跌。做趋势看K线颜色。牛市的红色可以当成入场K熊市绿色当成入场K

2 Exponential Moving AveragesThe Power of the 8 & 21 Day Moving Averages

Traders often ask me why I talk about the 8 & 21 day moving averages so much. Whether you see me on CNBC, Twitter, or the Virtual Trading Floor®, odds are you'll see me talking about them.

It's because these moving averages are the most accurate short-term road map I've found.

www.t3live.com

Complete EMA/SMA/BOLL setWhen you are on a simple plan and can't afford all the indicators... why not get them all in one!

Here are the main EMA's that I use on a day trading basis.. and no I don't have them all on at once!

I'm a big fan of the 12/26 EMA's on ALL time frames, however I sometimes just like to look at the 4 hourly chart. Problem is that I can't see the 12/26 Daily EMA's ?????

Well, with this tool you can.. just overlay the 'Dto4-ema12' etc

Also overlay weekly too if you feel the need!

PS: Threw the Bollinger Bands in there too, just for shits and giggles.

Enjoy!

Investing - Weekly EMA's mapped to Daily ChartWhen there isn't enough time in your day to day-trade, yet you want to utilise all the technical analysis skills you have... why not make a long term investing or swing trading indicator set to help you along the way!

So I did....

When it comes to long term investing and swing trading, I often find the weekly 12/26/52 EMA's do a great job in capturing the main market swings from bull to bear.

However, I like to use the Daily chart to see the candle patterns and shapes with more detail and divergences often show up better on the daily chart.

So I have decided to combine the two!

I have basically taken the EMA 12/26/52 from the weekly and transferred them over to the daily (mathematically they are not exact, but for me they are close enough).

I have also developed a simple scale in / scale out strategy for using these exponential moving averages. It isn't as simple as buying in on each signal, however I use my own special strategy to take advantage of the alerts.

Enjoy!

Simple Alt Coin Strategy - EMA and MACD w/Profit and StopThis script prints BUY and SELL signals based on settings you input. I use it to save time while scrolling through charts deciding what alts I want to look at.

BUY SIGNALS

Positive EMA Crossover

Positive MACD Crossover

Single Candle Gains

SELL SIGNALS

Profit Capture

Stop Loss

I don't trade based just on the BUY or SELL from this strategy, but I have found that these indicators do very well well looking at the large cap alt coins. It backtests well.

Default Settings EMA 5/12/50, MACD 9/12/26, Single Candle Gain 10%, Stop 10%, Profit Capture 45%

[astropark] MACD, RSI+, AO, DMI, ADX, OBV, ADI//******************************************************************************

// Copyright by astropark v4.1.0

// MACD, RSI+, Awesome Oscillator, DMI, ADX, OBV, ADI

// 24/10/2018 Added RSI with Center line to have clear glue of current trend

// 10/12/2018 Added MACD

// 13/12/2018 Added multiplier for MACD in order to make it clearly visible over RSI graph

// 11/01/2019 Added Awesome Ascillator (AO)

// 11/01/2019 Added Directional Movement Index (DMI) with ADX

// 14/01/2019 Added On Balance Volume (OBV)

// 14/01/2019 Added Accelerator Decelerator Indicator (ADI)

//******************************************************************************

[astropark] MACD, RSI+, Awesome Oscillator, DMI, ADX, OBV//******************************************************************************

// Copyright by astropark v4.0.0

// MACD, RSI+, Awesome Oscillator, DMI, ADX, OBV

// 24/10/2018 Added RSI with Center line to have clear glue of current trend

// 10/12/2018 Added MACD

// 13/12/2018 Added multiplier for MACD in order to make it clearly visible over RSI graph

// 11/01/2019 Added Awesome Oscillator (AO)

// 11/01/2019 Added Directional Movement Index (DMI) with ADX

// 14/01/2019 Added On Balance Volume (OBV)

//******************************************************************************

[astropark] MACD, RSI+, Awesome Oscillator, DMI with ADX//******************************************************************************

// Copyright by astropark v3.1.0

// MACD, RSI+, Awesome Oscillator, DMI, ADX

// 24/10/2018 Added RSI with Center line to have clear glue of current trend

// 10/12/2018 Added MACD

// 13/12/2018 Added multiplier for MACD in order to make it clearly visible over RSI graph

// 11/01/2019 Added Awesome Ascillator (AO)

// 11/01/2019 Added Directional Movement Index (DMI) with ADX

//******************************************************************************

[astropark] MACD, RSI+, Awesome Oscillator//******************************************************************************

// Copyright by astropark v3.0.0

// MACD, RSI+, Awesome Oscillator

// 24/10/2018 Added RSI with Center line to have clear glue of current trend

// 10/12/2018 Added MACD

// 13/12/2018 Added multiplier for MACD in order to make it clearly visible over RSI graph

// 11/01/2019 Added Awesome Ascillator (AO)

//******************************************************************************

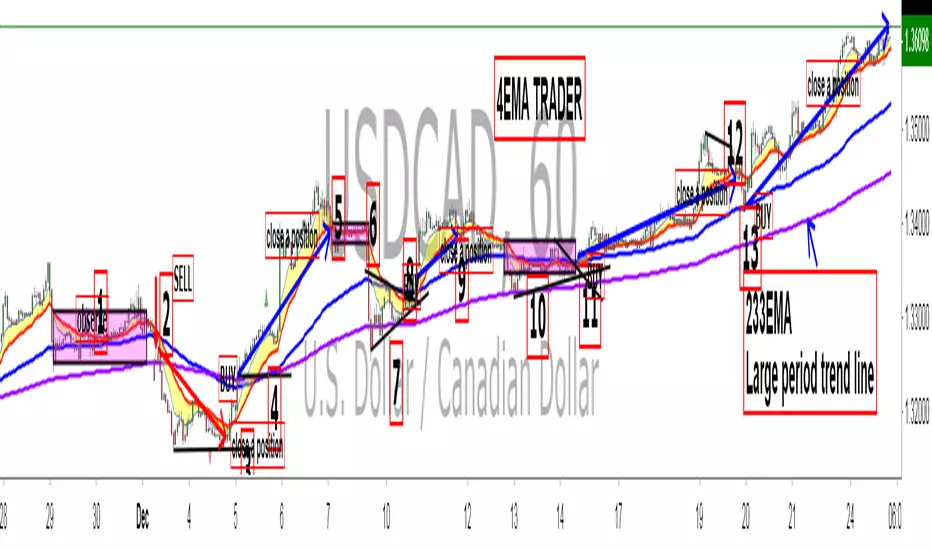

King 4EMA TraderKing 4EMA trader 8/21/89EMA+(233)V3.3

Explain the application of moving averages through the disk surface:

When the price runs above 89, it only looks for the buy signal.

When the price runs below 89, it only looks for sell signals.

The first step up through the 89 moving average after the first confirmation can buy homeoply,

The first pull down after crossing the 89 moving average for the first time confirms that it can be sold in line with the trend.

Price horizontal finishing, moving average frequently across the field observation.

The yellow area in the interval from 8 to 21 is the homeopathic warehouse addition signal.

When the price is above the 89 moving average, the k-line closes below the 21-day moving average as a callback signal

Prices below the 89 ema close above the 21 - day ema as a rebound signal

After the correction and rebound signals come out, we should make half of the profit and the other half of the stop loss in the break-even place.

Moving average is very suitable for the trend of strong varieties, is not suitable for volatile market.

Only at the end of the shock market moving average upward or downward divergent when it is possible to be used.

1. Repeatedly entangle the mean line of horizontal disk stage and observe it from the field

2. Sell the three EMA moving averages when they can't exceed 89EMA with downward crossing

3, many times can not break the new low when prices go sideways profit

4. Buy when the price reaches 89EMA after the convergence of triangle 3 is broken

5, the Angle of price rise slowed and closed below the 21 moving average when profit

6. Left field observation during transverse oscillation.

Sit tight while news or data cause prices to fall quickly

8. Buy when the price triangle breaks through the 89 moving average upward

9, the price does not rise to slow down when the horizontal closed below the 21 moving average when profit

10, price horizontal shock finishing at the same time the average line also transverse finishing field observation

11, the price of the triangle after finishing through the 89 moving average to buy.At this point all the averages have turned up

12, the second time can not break through the new high when the negative line can profit

13, the price of the first time in the same period of time through 89 after the first step back can be re-bought.

通过盘面讲解均线运用:

价格在89上面运行时时只找买入信号、

价格在89下面运行时只寻找卖出信号、

第一次向上穿过89均线后的第一次回踩确认可以顺势买入、

第一次向下穿过89均线后的第一次回抽确认可以顺势卖出、

价格横盘整理,均线频繁穿越时离场观察。

8-21区间里面黄色区域为顺势加仓信号,

价格在89均线上面时K线收盘在21天均线下面时为回调信号

价格在89均线下面时K线收盘在21天均线上面时为反弹信号

在回调和反弹信号出来之后我们应该获利一半的头寸,另外一半止损放到盈亏平衡的地方。

均线非常适合趋势性很强的品种,并不适合震荡行情。

只有在震荡行情结束时均线向上或向下发散时才有被运用的可能。

1、横盘阶段均线反复纠缠,离场观察

2、三条EMA均线向下交叉回抽无法超越89EMA时卖出

3、多次不能破新低时价格走横时获利

4、价格在3处三角形收敛被突破后站上了89EMA时买入

5、价格上涨角度变缓并收盘在21均线下面时获利

6、横盘震荡时离场观察。

7、见死不救新闻或数据导致价格快速下跌时观望

8、价格三角形向上突破时穿过89均线时买入

9、价格不升减速走横时收盘于21均线下面时获利

10、价格横盘震荡整理同时均线也横向整理时离场观察

11、价格突破三角形整理后重新穿过89均线时买入。此时所有均线已经向上翘头

12、第二次不能突破新高时收阴线可以获利

13、价格在同一个时间周期内第一次穿过89以后的第一次回踩可以重新买入。

Synergy StatsSynergy Stats

This indicator is intended to complement the Synergy indicator. It provides the following statistics:

A percentage showing how often the two assets move in the opposite direction over a given lookback period.

Similarly, another percentage showing how often the two assets move in the same direction over the same lookback period.

Count the number of times (occurrences) when the two assets move in the same direction for more than 4 bars.

Count the number of times the alternative asset moves more than x%

Count the number of times that chart asset moved in the same direction of the alternative asset when the alternative asset moved more than x%

Both indicators were developed for use in an investigation/tutorial using Pine Script to analyse Gold and US Dollar Index correlation.

The full free post can be found here: backtest-rookies.com

SynergySynergy

This indicator was developed for use in an investigation/tutorial using Pine Script to analyse Gold and US Dollar Index correlation.

The first indicator shall measure the percentage change between the open and close of each bar and compare it to the same percentage change of an alternative asset. Additionally, we shall color the background when the two assets move in the same direction. This should allow us to more easily see when the two assets move together and spot trends in their moment.

The yellow bars show use the percentage change in the price of gold. The blue bars show the percentage change in the price of the US Dollar index. If the bar is above zero, it means that the asset closed up. Conversely, if it is below zero, it means the asset closed down. Finally, the grey bars show bars in which the two assets closed in the same direction.

It can be used in conjunction with a second indicator (to be published soon) that provides statistics generated from this indicator.

The full free post can be found here: backtest-rookies.com

[astropark] MACD & RSI+//******************************************************************************

// Copyright by astropark v2.0

// MACD RSI+

// 24/10/2018 Added RSI with Center line to have clear glue of current trend

// 10/12/2018 Added MACD

// 13/12/2018 Added multiplier for MACD in order to make it clearly visible over RSI graph

//******************************************************************************

[astropark] Power Tools Overlay//******************************************************************************

// Power Tools Overlay

// Inner Version 1.2 20/12/2018

// Developer: iDelphi

// Developer: astropark (Ichimoku Cloud), SMA EMA & Cross tools

//------------------------------------------------------------------------------

// 21/11/2018 Added EMA SMA WMA

// 21/11/2018 Added SMA-EMA EMA-WMA WMA-SMA (Thanks to mariobros1 for the idea of the Simultaneous MA)

// 21/11/2018 Added Bollinger Bands

// 21/11/2018 Added Ichimoku Cloud (Thanks to astropark for all the code of the Ichimoku Cloud)

// 23/11/2018 Show all the indicator as default

// 23/11/2018 Added a cross when single Moving Averages crossing (Thanks to astropark for the idea)

// 24/11/2018 Descriptions Fix

// 24/11/2018 Added Option to enable/disable all Moving Averages

// 10/12/2018 Added EMAs and Crosses

//******************************************************************************

EMA fasterDraw EMA(12) and put a signal when EMA(12) cross with EMA(50).

EMA(50) is not rendered on the canvas.