在脚本中搜索"GOLD"

[LAVA] Early Warning IndicatorCombined the RSI inverse of gold to USD with the Dollar index (or whatever stock symbol that may be inverted/complementary) with another asset/currency, like bitcoin, you can basically be well informed when a potential move is on the horizon. Settings allow for inverse settings and de-combining the two pairs as well as a nice cloud look if all the lines get annoying.

Williams FractalsBoaBias Fractals High & Lows is an indicator based on Bill Williams' fractals that helps identify key support and resistance levels on the chart. It displays horizontal lines at fractal highs (red) and lows (green), which extend to the current bar. Lines automatically disappear if the price breaks through them, leaving only the relevant levels. Additionally, the indicator shows the price values of active fractals on the price scale for convenient monitoring.

Key Features:

Customizable Fractals: Choose between 3-bar or 5-bar fractals (default: 3-bar).

Period: Adjust the number of periods for calculation

Visualization: Red lines for highs (resistance), green for lows (support). Lines are fixed on the chart and persist during scrolling or scaling changes.

Alert System: Notifications for the formation of a new fractal high/low and for level breaks (Fractal High Formed, Fractal Low Formed, Fractal High Broken, Fractal Low Broken).

How to Use:

Add the indicator to the chart.

Configure parameters: select the fractal type (3 or 5 bars) and period.

Set up alerts in TradingView to receive notifications about new fractals or breaks.

Use the lines as levels for entry/exit positions, stop-losses, or take-profits in fractal-based strategies.

Troubleshooting: If Levels Are Not Fixed on the Chart

If the levels (fractal lines) do not stay fixed on the chart and fail to move with it during scrolling or scaling (e.g., they remain stationary while the chart shifts), this is typically due to the indicator's scale settings in TradingView. The indicator may be set to "No scale," causing the lines to desynchronize from the chart's price scale.

What to Do:

Locate the Indicator Label: On the chart, find the indicator label in the top-left corner of the pane (or where "BoaBias Fractals High & Lows" is displayed).

Right-Click the Label: Click the right mouse button on this label.

Adjust the Scale:

In the context menu, look for the "Scale" or "Pin to scale" option.

If it shows "Pin to scale (now no scale)" or similar, select "Pin to right scale" (or "Pin to left scale," depending on your chart's main price scale—usually the right).

Refresh the Chart: After changing the setting, refresh the chart (press F5 or reload the page), or toggle the indicator off and on again to apply the changes.

After this, the lines should move and scale with the chart during scrolling (horizontal or vertical) or zooming. If the issue persists, check:

TradingView Limits: The indicator may draw too many lines (maximum ~500 per script). If there are many historical fractals, older lines might not display.

Chart Settings: Ensure the chart is not in logarithmic scale (if applicable) or that auto-scaling is enabled.

Indicator Version: Verify you are using the latest script version (Pine Script v6) and check for errors in the TradingView console.

This indicator is ideal for traders working with Bill Williams' chaos theory or those seeking dynamic support/resistance levels. It is based on standard fractals but with enhancements for convenience: automatic removal of broken levels and integration with the price scale.

Note: The indicator does not provide trading signals on its own — use it in combination with other tools. Test on historical data before real trading.

Code written in Pine Script v6. Original template: Mit Nayi.

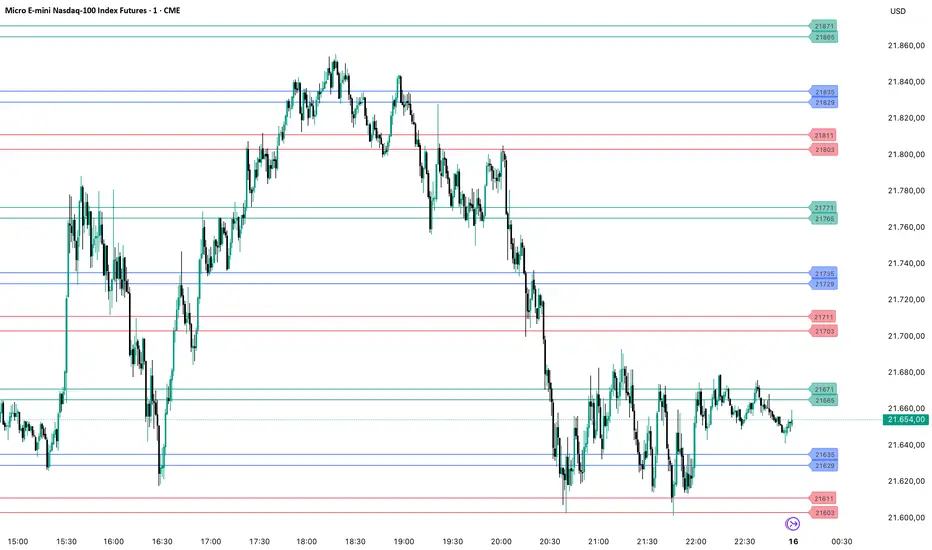

Golder/Silter SetupsGolden/Silver Strategy

Overview

The Tony Rago Golden/Silver Strategy is a high-precision mean-reversion system specifically engineered for the Nasdaq (NQ/MNQ). It leverages the psychological 100-point price blocks to identify institutional exhaustion and reversal points.

Unlike standard "grid" bots, this strategy uses a sophisticated "Arm & Fire" logic: it requires a specific price "touch" to arm the setup, followed by a retracement to a "Golden" entry level to execute.

Key Logic: The 100-Point Grid

The strategy divides price action into 100-point blocks (e.g., 19500 to 19600).

Golden Setup (Long): Triggered when price touches the 50 level (mid-point). The order is placed at the 26 level on the retracement.

Silver Setup (Short): Triggered when price touches the 00 or 100 levels (block boundaries). The order is placed at the 77 or 26 levels on the retracement.

Professional Risk Management

This edition features a Dual-Contract Management system designed for Prop Firm consistency:

Contract 1 (The Scalp): Aims for a quick 24-point target (TP1) to secure realized gains and cover costs.

Contract 2 (The Runner): Stays in the trade for an extended 51-point target (TP2).

Automated Break-Even (BE): The moment TP1 is hit, the Stop Loss for the Runner is automatically moved to the entry price (plus a small offset). This ensures a "risk-free" environment for the remainder of the trade.

Independent Stop Losses: The Scalp and the Runner use different SL distances to account for Nasdaq volatility, preventing a single "noise" wick from wiping out the entire position.

Intelligent Filters

ADX Range Filter: The strategy monitors market trend strength. It only allows trades when the ADX is below a user-defined threshold (default 25), ensuring you only play mean-reversion during ranging or "choppy" markets.

MA Visual Semaphor: The 50 EMA changes color dynamically based on ADX (Lime/Green for Range, Orange/Red for Trend), giving you an instant visual "Go/No-Go" signal.

Time-Session Filtering: Optimized for three custom sessions (NY Open, Mid-Day Reversal, and Late Night). Outside these sessions, the strategy can "Arm" setups in memory but will not "Fire" orders.

How to Use

Timeframe: Optimized for 1-Minute or 2-Minute charts for precision entry.

Asset: Nasdaq 100 (NQ, MNQ) or similar high-volatility indices.

Setup: * Enable Session Filters to avoid news volatility.

Adjust TP/SL in Points (1 Point = 4 Ticks) to suit your specific risk appetite.

Watch for the "Armados" labels—these indicate the system is ready and waiting for the Golden/Silver entry.

Visual Interface

Dynamic Boxes: Real-time visual representation of your TP1, TP2, and SL levels.

Activation Labels: Clear indications of when a Long or Short setup has been "Armed" in memory.

Status Dashboard: A clean top-right table showing current ADX values, Session status, and Risk settings.

Disclaimer

Trading involves significant risk. This strategy is a tool for decision support and backtesting. Past performance does not guarantee future results. Always test on a demo account before risking live capital.

Goldbach Timing Model This indicator is designed as a simple visual framework rather than a rigid signal system. It highlights time-based structure and key alignment zones to help identify when price behavior is more likely to be active or responsive. The logic is intentionally flexible, allowing the user to apply their own discretion instead of relying on strict conditions. Its primary value is visual clarity and context, not automatic entries or exits.

PriceLevels GBGoldbach Price Levels – Identify Algorithmic Key Zones

This open-source indicator is designed to help traders identify potential algorithmic key zones by highlighting price levels ending with specific numbers such as 03, 11, 29, 35, 65, and 71. These levels may act as inflection points or hesitation areas based on observed behavioral patterns in price movement.

What It Does:

📌 Scans and plots horizontal price levels where the price ends with one of the selected number combinations

🎯 Toggle on/off visibility for each number ending

🎨 Customize color and thickness for each level

🏷️ Shows price labels at the end of each line

🌗 Label styles (color/transparency) are adjustable for both dark and light chart themes

🧠 Why Use It:

This tool is ideal for discretionary traders who study market structure through static price anchors. It provides a visual reference for recurring numerical levels that may be used in algorithmic trading models or serve as psychological price zones.

⚠️ Disclaimer:

This script is open-source and intended for educational and analytical purposes only. No trading signals or performance guarantees are provided. Please use your own judgment when applying this tool in a trading context.

Gold 2-Week Futures LevelsYou may change the color at bottom of script and i used 1h to mark out my levels, you may change it to fit your time frame.

Gold Scalp//@version=5

indicator("scalp strategy (Boxed)", overlay=true)

// Ensure 5-minute chart

isFiveMin = timeframe.isminutes and timeframe.multiplier == 5

// New York time (EST/EDT auto)

nyHour = hour(time, "America/New_York")

nyMinute = minute(time, "America/New_York")

// Target times (exact candle close)

triggerTime =

(nyHour == 11 and nyMinute == 0) or

(nyHour == 19 and nyMinute == 0) or

(nyHour == 14 and nyMinute == 0) or

(nyHour == 6 and nyMinute == 0) or

(nyHour == 8 and nyMinute == 0) or

(nyHour == 21 and nyMinute == 0) or

(nyHour == 00 and nyMinute == 0)

// Final trigger

trigger = isFiveMin and triggerTime and barstate.isconfirmed

// Draw box + label

if trigger

box.new(bar_index - -5, high, bar_index, low, bgcolor=color.new(#0e06eb, 76), border_color=color.rgb(4, 252, 136))

label.new(bar_index, high, "", style=label.style_label_down, color=color.rgb(11, 48, 3), textcolor=color.white, size=size.small)

// Alert

alertcondition(trigger, title="LETS GO", message="5-minute candle CLOSED at key EST time")

GOLD TERTIUM estrategiaThis indicator is a visual tool for TradingView designed to help you read trend structure using EMAs and highlight potential long and short entries on the MGC 1‑minute chart, while filtering pullbacks and avoiding trades when the 200 EMA is flat.

It calculates five EMAs (32, 50, 110, 200, 250) and plots them in different colors so you can clearly see the moving‑average stack and overall direction. The main trend is defined by the 200 EMA: bullish when price and the fast EMAs (32 and 50) are above it with a positive slope, and bearish when they are below it with a negative slope; if the 200 EMA is almost flat, signals are blocked to reduce trading in choppy markets.

GOLD TERTIUM MGC 1mThis indicator is a visual tool for TradingView designed to help you read trend structure using EMAs and highlight potential long and short entries on the MGC 1‑minute chart, while filtering pullbacks and avoiding trades when the 200 EMA is flat.

It calculates five EMAs (32, 50, 110, 200, 250) and plots them in different colors so you can clearly see the moving‑average stack and overall direction. The main trend is defined by the 200 EMA: bullish when price and the fast EMAs (32 and 50) are above it with a positive slope, and bearish when they are below it with a negative slope; if the 200 EMA is almost flat, signals are blocked to reduce trading in choppy markets.

Entry logic looks for a pullback into the 32–50 EMA zone on the previous candle, then requires a trend‑aligned candle to trigger a signal: long when the trend is up, the previous bar retested the EMA zone, and the current bar closes above EMA 32 with a bullish body; short when the trend is down, there was a valid retest, the current bar closes below EMA 32 with a bearish body and EMA 32 is below EMA 50. On the chart, you will see colored EMAs plus green “L” triangles under bars for potential long entries and red “S” triangles above bars for potential short entries, which are meant as visual cues rather than automatic trade instructions

Gold Bullish Order Blocks - 3 Candle Confirmation after the OBBest Order blocks finder created by Marky using claude AI.

GOLDEN RSI (70-50-30)The fluctuation range has been expanded. Theoriginal author only set it between 40 and 60, but arange of 30 to 70 would be more reasonableAdditionally, a 50 median line has been added withinthe fluctuation range

GOLD EMA Crossover Strategy This EMA Crossover Strategy is designed for intraday trading on the 5-minute chart.

It uses three EMAs (fast, mid, slow) to identify momentum shifts and trigger long or short entries. Risk management is dollar-based, with default settings of $100 risk per trade and $300 profit target. Entries are taken when the fast EMA crosses above/below the mid or slow EMA, with stops and targets calculated dynamically. The strategy runs across all hours and uses fixed position sizing (default 3 contracts). It is intended as a framework for traders to adapt and optimize to their own instruments and risk preferences.

Gold Master: Swing + Daily Scalp (Fixed & Working)How to use it correctly

Daily chart → Focus only on big green/red triangles (Swing trades)

5m / 15m / 1H chart → Focus on small circles (Scalp trades)

You can turn each system on/off independently in the settings

Works perfectly on XAUUSD, GLD, GC futures, and even DXY (inverse signals).

golden smart entrySmart Money Concepts (SMC) is a trading methodology that focuses on understanding and following the behavior of institutional investors—often referred to as "smart money." The goal is to identify high-probability trade setups by analyzing how these large players move the market.

Golden Cross & Death Cross DetectorThis script will:

Plot both moving averages on your chart

Show triangle markers when crossovers occur

Allow you to set up alerts

Let you choose between SMA and EMA

Customize the periods for both moving averages

nadia

Gold ramon strategy based on 50 candles and atr of 12

You enter the maximum of 50 candles once the most bearish starts to rise, we expect 10 candles, if you don't go up in 10 candles, you don't enter, if you go up before 10 candles, you enter.

When is TP? Enough with 5 candles

The temporality is 1 hour. It can be adjusted to 1 minute temporality for scalping.

It is never lost, because it always exceeds the previous maximums.

Gold NY Session Key TimesJust showing to us that news come out, open market, close bond for NY Session Time For Indonesia