VIX and SKEW RSI Moving AveragesSKEW and VIX are both indicators of market volatility and risk, but they represent different aspects.

VIX (CBOE Volatility Index) :.

The VIX is a well-known indicator for predicting future market volatility. It is calculated primarily based on S&P 500 options premiums and indicates the degree of market instability and risk.

Typically, when the VIX is high, market participants view the future as highly uncertain and expect sharp volatility in stock prices. It is generally considered an indicator of market fear.

SKEW Index :.

The SKEW is a measure of how much market participants estimate the risk of future declines in stock prices, calculated by the CBOE (Chicago Board Options Exchange) and derived from the premium on S&P 500 options.

If the SKEW is high, market participants consider the risk of future declines in stock prices to be high. This generally indicates a "fat tail at the base" of the market and suggests that the market perceives it as very risky.

These indicators are used by market participants to indicate their concerns and expectations about future stock price volatility. In general, when the VIX is high and the SKEW is high, the market is considered volatile and risky. Conversely, when the VIX is low and the SKEW is low, the market is considered relatively stable and low risk.

Inverse Relationship between SKEW and VIX

It is often observed that there is an inverse correlation between SKEW and VIX. In general, the relationship is as follows

High VIX and low SKEW: When the VIX is high and the SKEW is low, the market is considered volatile while the risk of future stock price declines is low. This indicates that the market is exposed to sharp volatility, but market participants do not expect a major decline.

Low VIX and High SKEW: A low VIX and high SKEW indicates that the market is relatively stable, while the risk of future declines in stock prices is considered high. This indicates that the market is calm, but market participants are wary of a sharp future decline.

This inverse correlation is believed to be the result of market participants' psychology and expectations affecting the movements of the VIX and SKEW. For example, when the VIX is high, it is evident that the market is volatile, and under such circumstances, people tend to view the risk of a sharp decline in stock prices as low. Conversely, when the VIX is low, the market is considered relatively stable and the risk of future declines is likely to be higher.

SKEWVIX RSIMACROSS

In order to compare the trends of the SKEW and VIX, the 50-period moving average of the Relative Strength Index (RSI) was used for verification. the RSI is an indicator of market overheating or overcooling, and the 50-period moving average can be used to determine the medium- to long-term trend. This analysis reveals how the inverse correlation between the SKEW and the VIX relates to the long-term moving average of the RSI.

how to use

Moving Average Direction

Rising blue for VIXRSI indicates increased uncertainty in the market

Rising red for SKEWRSI indicates optimism and beyond

RSI moving average crossing

When the SKEW is dominant, market participants are considered less concerned about a black swan event (significant unexpected price volatility). This suggests that the market is stable and willing to take risks. On the other hand, when the VIX is dominant, it indicates increased market volatility. Investors are more concerned about market uncertainty and tend to take more conservative positions to avoid risk. The direction of the moving averages and the crossing of the moving averages of the two indicators can give an indication of the state of the market.

SKEW>VIX Optimistic/Goldilocks

VIX>SKEW Uncertainty/turbulence

The market can be judged as follows.

BestRegards

在脚本中搜索"GOLD"

Temporal Value Tracker: Inception-to-Present Inflation Lens!What we're looking at here is a chart that does more than just display the price of gold. It offers us a time-traveling perspective on value. The blue line, that's our nominal price—it's the straightforward market price of gold over time. But it's the red line that takes us on a deeper journey. This line adjusts the nominal price for inflation, showing us the real purchasing power of gold.

Now, when we talk about 'real value,' we're not just philosophizing. We're anchoring our prices to a point in time when the journey began—let's say when gold trading started on the markets, or any inception point we choose. By 'shadowing' certain years—say, from the 1970s when the gold standard was abandoned—we can adjust this chart to reflect what the inflation-adjusted price means since that key moment in history.

By doing so, we're effectively isolating our view to start from that pivotal year, giving us insight into how gold, or indeed any asset, has held up against the backdrop of economic changes, policy shifts, and the inevitable rise in the cost of living. If you're analyzing a stock index like the S&P 500, you might begin your inflation-adjusted view from the index's inception date, which allows you to measure the true growth of the market basket from the moment it started.

This adjustment isn't just academic. It influences how we perceive value and growth. Consider a period where the nominal price skyrockets. We might toast to our brilliance in investment! But if the inflation-adjusted line lags, what we're seeing is nominal growth without real gains. On the other hand, if our red line outpaces the blue even during stagnant market periods, we're witnessing real growth—our asset is outperforming the eroding effects of inflation.

Every asset class can be evaluated this way. Stocks, bonds, real estate—they all have their historical narratives, and inflation adjustment tells us if these stories are tales of genuine growth or illusions masked by inflation.

So, as informed traders and investors, we need to keep our eyes on this inflation-adjusted line. It's our measure against the silent thief that is inflation. It ensures we're not just keeping up with the Joneses of the market, but actually outpacing them, building real wealth over time

Technical Candle Alerts [SS]Releasing this fun little project indicator.

What is it?

The Technical Candle Alert indicator provides alerts based on multiple underlying technicals, including MFI, RSI, Stochastics, Z-Score, Pivot points and the EMA 50 and EMA 200 Death and Golden Cross.

What does it do?

The indicator looks back over a designated timeframe to look for max and min values of technicals, as well as track the EMA200 and EMA50.

When a candle approaches a previous max zone, pivot point or there is a death or golden cross, the indicator will signal on the candle that has triggered this event. Then you, as the trader, can determine whether you want to listen to the signal or ignore it.

How Does it Work?

The indicator is set to default and generally accepted settings for technicals, however you can modify them as you prefer.

The indicator is also programmed to identify the strongest trend period and set that as the lookback length. The theory is, you want to look at max and min technicals as well as pivot points in a recent area of a strong trend. However, if you want to over-ride the auto trend identification, you can simply unselect "Autotrend" and put in your desired manual lookback length.

The indicator will then keep track of max values for the various technicals and present you with alerts directly over the candle when a Max or Min value is triggered, or a pivot point is entered, etc.

Here are some examples:

Golden Cross:

Death Cross:

Previous Pivot Points:

Various Alerts:

Customization:

You can customize which alerts you want to turn off and on.

As well, there is a signal delay setting (wait setting). This prevents repeated, unnecessary signaling of the same signal. The default wait time is 5 signals, however you can adjust based on your desired tolerance. If you want it to always signal, adjust it to 0.

As indicated before, you can also adjust all of the technicals and the pivot bars for high and low pivots and you can manually set your lookback length.

That is the indicator in a nutshell, let me know if you have any questions that may not have been covered in the description. Its pretty straight forward once you play around with it.

Safe trades everyone and thanks for checking this out!

Cynical Cold IndexThis TradingView indicator calculates the Cynical Cold Index, which is a weighted basket of commodity prices designed to track economic conditions. It compares the price of a given asset to the index value.

Weights the commodities as percentages:

Gold: 10%

Oil: 15%

Coffee: 5%

Natural Gas: 10%

Silver: 15%

Sugar: 5%

Corn: 5%

Wheat: 5%

Cotton: 10%

Copper: 10%

Iron Ore: 5%

Live Cattle: 5%

Urea: 5%

nVPSA - Normalized Volume-Price Spread AnalysisNormalized volume-price spread analysis indicator can be helpfully tool in Tom's William metodology - VSA.

The indicator use normalized data by y/x(max) operation, where x(max) is the biggest value in range. Indicator separate spread to four levels - standard divation is separator.

The indicator graphically shows:

- normalized volume, visualized by wide column,

- normalized price spread, visualized by narrow column,

- linear regression calculated from normalized volume, visualised by crosses,

- linear regression from normalized price spread, visualized by circles.

Columns are marked by five colors according to standard deviation:

- blue xsecond deviation, xfourth deviation,

- gold when volume or price spread achive new maximum in analysis range.

Linear regression uses three colors:

- green when volume/spread is up bar by bar,

- red when volume/spread is down bar by bar,

- black when volume/spread is down two times bar by bar.

Additionally, it is posible to use alarm on Golden Bar. Colors and range values are editable from indicator settings.

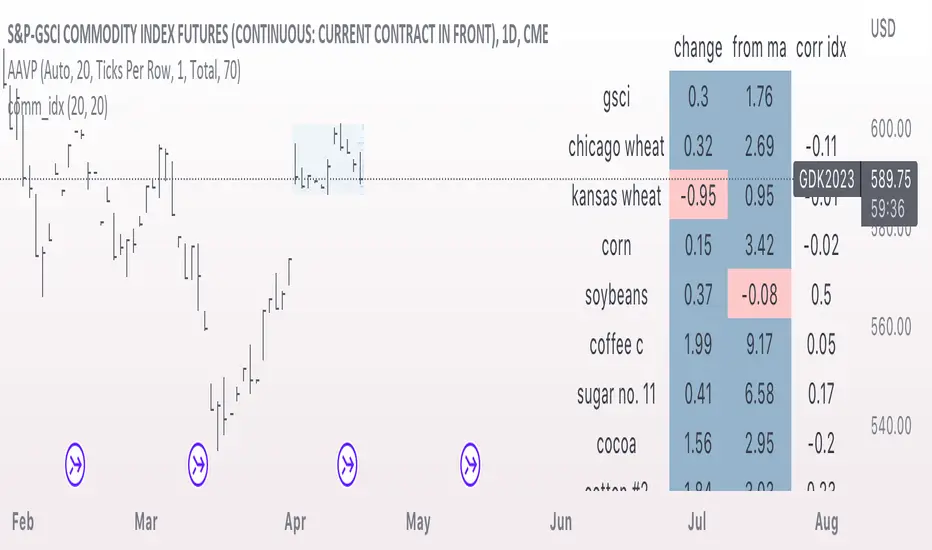

comm_idxThis script displays information about the components of the Goldman Sachs Commodity Index. The index is based on futures contracts in the categories of agricultural products, softs commodities, livestock, energies, industrial metals, and precious metals. The statistics displayed in the table are:

change: 1-day % change

from ma: the % change from a moving average

corr idx: correlation of the contract to the GSCI

The lengths for the moving average and correlation statistic can be set using the inputs.

See the script source for the symbols used for each commodity. Although most of the symbols correspond to the actual futures contract used to compute the index, LME contracts are not available on tradingview. Hence, corresponding HKEX contracts are used for the industrial metals.

Trend Indicator with RSI and Fibbonacci Band 0.702 crossingsToday we have a new Indicator set, which I created using inspiration from the Trend Magic Indicator from KivancOzbilgic and adding several new aspects to it and a slightly modified calculation of the trend indicator itself.

You can change the inputs by changing the pre set values in the settings, but I found the current settings quite accurate. Feel free to experiment to fine tune the indicators.

Here are the details of the script:

Trend indicated within candles and as a line

- bullish and bearish trends are now also indicated within the candle based on the CCI calculation.

- Bullish is indicated by a green circle below the candle or as one may call it a "dot"

- bearish trend is indicated by a red circle above the candle

Entry Signal based on RSI crossing its EMA

- my motivation was to have a clearer entry signal besides highlighting a trend, which can not really be used to identify a good entry but to give confidence or when loosing trend to give an exit signal.

- after studiying the RSI and how it works together with its EMA it looks quite interesting as an entry or exit signal. But be cautios if the EMA and RSI values are moving in a narrow area we get a lot of crosses and therefore signals which should rather be ignored rather to be act on. So the the range where the cross happens is also quite important. But this aspect is not yet reflected as a rule/ logic.

But I am thinking of adding something.. or alternativly best to switch to another timeframe to get some better data

RSI overbought and oversold as Diamonds

- I also added key indications of oversold or overbought as Blue and Pink diamonds, can be considered as additional information to maybe identify a short term top or bottom.. but its not very accurate.

Entry signal based on crossing Fibbonachi Band 0.702

- So far the 0.702 seems to be quite an interesting retracement level which seems to be met a lot of times

- based on the assumption the price will evantually hit the 0.702 either direction I wanted to get a signal when this happens

- BUT! a big but, unfortunalty the Fibbonachi bands tend to bloat up in case of high volatility so it is not easy to find the crossing on higher timeframes

Here are the standard value which I found quite accurate for the assets I use this indicator set:

CCI Period = 5

ATR Multiplier = 1

ATR Period = 1

Source = High Low Close (hlc3 average value of the candle

Here the inputs used for the RSI Crossing signal (here you should play around a little to see which entry would have been best..)

RSI Length = 14

RSI Oversold = 25 (to be used for the "golden" entry signal based on the FBB crossing)

RSI Overbought = 80 (to be used for the "golden" entry signal based on the FBB crossing)

RSI Moving Average Length

In future versions I will add options to activate or deactive some of the plotting and espacially this golden dot when the fibbonachi band is being crossed needs some fine tuning..

And lets see if there is a way to fix the bloating of those bands..

Move Magnitude Visualizer (beta)This experimental visualizer measures all price differences across a range of samples to determine what is normal for a measure of time. Based on whether a recent change in price over time has exceeded the norm, a line is drawn to indicate the magnitude/severity of that move. In short, it attempts to visualize when a move is outside the norm and when it may be risky to join that move.

A thick red line = greater than 3 standard deviations.

An orangish/goldish line = greater than 2 standard deviations.

A thin dotted yellow = greater than 1 standard deviation.

In the end, I've always wanted a tool that gave me a visual warning to when a move is abnormally severe and shouldn't be trusted. RSI and other indicators only work with specific lengths, this attempt to be a deviation detector that isn't bound by length or time-frame.

This is a work in progress, so feedback is appreciated. I don't have a strong idea yet how to properly visualize this data.

It is very compute heavy and some users may experience timeouts. I've done everything I can think of to eliminate redundant computer and to optimize for PineScript.

Visible Fibonacci█ OVERVIEW

This indicator displays Fibonacci retracement and extension levels on the price chart using data within the chart's visible range, providing traders with an automated alternative to our well-known drawing tool .

█ CONCEPTS

Fibonacci sequence and the Golden ratio

The Fibonacci sequence is a sequence of numbers where each term is the sum of the previous two terms. In his book Liber Abaci , Fibonacci used this sequence to estimate the growth of rabbit populations. Although most commonly associated with Fibonacci, this numeric sequence appeared in Indian mathematics as early as 200 BC. As this sequence approaches infinity, the ratio of the last element to the preceding approaches the Golden ratio (1.618033...), a well-known metallic ratio theoretically observed in many natural and synthetic systems. Many traders believe that the Fibonacci sequence and the Golden ratio carry significance in the financial markets.

Fibonacci retracements and extensions

Fibonacci retracements and extensions are extremely popular in technical analysis. They are created by connecting two extreme points, typically pivot points, by a trend line and multiplying the range between them by the ratios of steps in the Fibonacci sequence, or more precisely, powers of the Golden Ratio, to produce estimated levels of support and resistance. The ratios used for retracement multipliers are typically the Golden ratio raised to the power of 0, -0.5, -1, -2, and -3, or 1, 0.786, 0.618, 0.382, and 0.236, respectively. It is also common to see traders use a retracement ratio of 0.5. The ratios used for extension multipliers are typically the Golden ratio raised to the power of 0.5, 1, 2, and 3, or 1.272, 1.618, 2.618, and 4.236, respectively. Traders often combine these retracement and extension ratios with others they deem significant for a more personalized output.

Zig Zag

Zig Zag is a popular indicator that filters out minor price fluctuations to denoise data and emphasize trends. Traders commonly use Zig Zag for trend confirmation, identifying potential support and resistance, and pattern detection. It is formed by identifying significant local high and low points in alternating order and connecting them with straight lines, omitting all other data points from their output. There are several ways to calculate the Zig Zag's data points and the conditions by which its direction changes. This script uses the highest and lowest values over a specified length to estimate the locations of pivots. The Zig Zag reverses its direction when a new high or low emerges in the opposite direction. Additionally, enabling the "Detect additional pivots" option in the script settings will locate extra pivots when the number of bars in which no new pivot occurs exceeds the Zig Zag length.

Visible Fibonacci

This script uses the chart's visible bars to calculate and display an automated Fibonacci retracement tool with extreme points based on either of two calculation methods:

• Visible Chart Range: This method uses the highest and lowest points from the visible chart range for Fibonacci level calculation.

• Visible Zig Zag: This method uses historical pivots from a Zig Zag indicator for level calculation. The "nth Last Pivot" input in the script settings controls how many pivots back from the last visible one will be used to calculate the Fibonacci levels.

As traders pan and zoom on their charts, the script dynamically recalculates its values explicitly using the bars within the visible range.

Note that levels drawn outside the range between the high and low points may affect the scale of the chart. To prevent this, select the "Scale price chart only" option in the chart settings.

█ FOR Pine Script™ CODERS

• This script utilizes functions from the VisibleChart library by our resident PineCoders . The library exploits the chart.left_visible_bar_time and chart.right_visible_bar_time variables, which return the opening time of the leftmost and rightmost bars on the chart. They are only two of many new built-ins in the `chart.*` namespace. See this blog post for more information, or look them up by typing "chart." in the Pine Script™ Reference Manual .

• This script's architecture utilizes user-defined types (UDTs) to create custom objects which are the equivalent of variables containing multiple parts, each able to hold independent values of different types . The recently added feature was announced in this blog post.

Look first. Then leap.

Seasonal tendency: week-on-week % change and 10yr Averages-shows week-on-week % change, and 10yr averages of these % changes

-scan across the 10yr averages to get a good idea of the seasonality of an asset

-best used on commodities with strong seasonal tendencies (Gold, Wheat, Coffee, Lean hogs etc)

-works only on daily timeframe

-by default it will compare SMA(length) in the following way, BTC: Sunday cf previous Sunday | ES/Gold: Monday cf previous Monday

-for most assets, 5 daily bars in a week (SMA(5)) => that's the default. For BTC can change this to 7.

~~inputs:

-change input year to show any previous decade of asset's history; the table will display over that year on the chart

-choose expression for Average of % change week on week: SMA, ohlc4, vwma, vwap (default SMA)

-choose number of daily bars in a week (i.e. SMA length)

-change label sizes/colors

~~notes:

-When applied to current year: will print the 10yr average for previous weeks in the year; 9yr average for future weeks in the year

-drawings and SMA plot on the above chart are just to show visually how the week's average is calculated, and how this lines up with the label

-current week of year will highlight in large font orange by default

-the first 2 weeks of the year are omitted because of a bug i can't figure out, which throws out bad numbers.

-cannot print all the values for each of previous 10yrs; 'code too long' error. Could likely do this via using matrices but would require a rewrite

17th Dec 2022

@twingall

[blackcat] L3 YACD38Level 3

Background

"3/8 moving average" golden cross enters, and dead cross exits.

Function

This set of methods is an improved moving average usage - "38 moving average usage", we need to use three moving averages:

3-day, 8-day and 21-day moving averages.

Why is it the 3-day, 8-day, and 21-day moving averages? Most of my friends may not be clear. 3, 8, and 21 are all Fibonacci numbers, also known as the golden section numbers. The Fibonacci number is a basic pattern of nature, which exists in all things. If you don’t understand it, you can go to a certain degree to understand it. In short, it is a very magical existence.

Keep in mind the principle of only doing uptrends and not downtrends. Then we have to use our 21-day moving average skillfully. The 21-day moving average happens to be the average price line for one month. We take it as the decision-making line. When the decision-making line goes down or goes flat, we mainly wait and see; , the operation success rate is higher!

Let's directly share the technical points of "38 moving average usage":

1. Entry point: the 3-day line crosses the 8-day line to form a golden cross, or both the 3-day and 8-day line cross the 21-day moving average; the position of the golden cross must be above the 21-day moving average, and it is invalid if it is below;

2. Basis for holding shares: After entering the market, the moving averages are arranged in a long position, and the K-line rises along the 3-day and 8-day moving averages, hold it patiently, and sell for whatever reason you buy!

3. Exit point: When the 3-day moving average crosses the 8-day moving average to form a dead cross, or the 3-day and 8-day moving averages break below the 21-day moving average, then decisively leave the market;

Note: "38 moving average usage" only needs to refer to the moving average, and the other most reference quantities can be changed. As long as the above conditions are met, you can boldly intervene, and after the intervention, you will rise to the top! Don't underestimate the usage of this set of moving averages, carefully comprehend and memorize them by heart, and be able to achieve the unity of knowledge and action, and you will be able to stand up and be the master from now on!

Remarks

Feedbacks are appreciated.

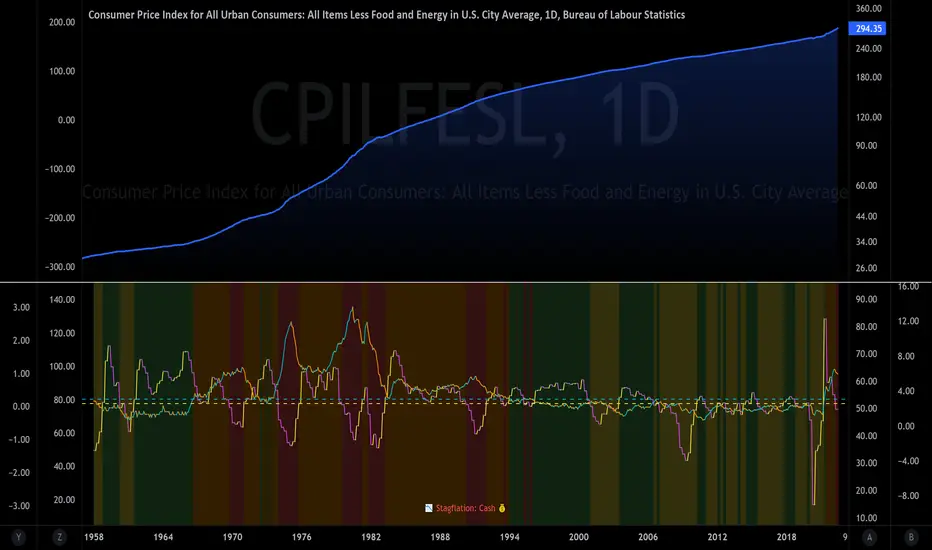

The Investment ClockThe Investment Clock was most likely introduced to the general public in a research paper distributed by Merrill Lynch. It’s a simple yet useful framework for understanding the various stages of the US economic cycle and which asset classes perform best in each stage.

The Investment Clock splits the business cycle into four phases, where each phase is comprised of the orientation of growth and inflation relative to their sustainable levels:

Reflation phase (6:01 to 8:59): Growth is sluggish and inflation is low. This phase occurs during the heart of a bear market. The economy is plagued by excess capacity and falling demand. This keeps commodity prices low and pulls down inflation. The yield curve steepens as the central bank lowers short-term rates in an attempt to stimulate growth and inflation. Bonds are the best asset class in this phase.

Recovery phase (9:01 to 11:59): The central bank’s easing takes effect and begins driving growth to above the trend rate. Though growth picks up, inflation remains low because there’s still excess capacity. Rising growth and low inflation are the Goldilocks phase of every cycle. Stocks are the best asset class in this phase.

Overheat phase(12:01 to 2:59): Productivity growth slows and the GDP gap closes causing the economy to bump up against supply constraints. This causes inflation to rise. Rising inflation spurs the central banks to hike rates. As a result, the yield curve begins flattening. With high growth and high inflation, stocks still perform but not as well as in recovery. Volatility returns as bond yields rise and stocks compete with higher yields for capital flows. In this phase, commodities are the best asset class.

Stagflation phase (3:01 to 5:59): GDP growth slows but inflation remains high (sidenote: most bear markets are preceded by a 100%+ increase in the price of oil which drives inflation up and causes central banks to tighten). Productivity dives and a wage-price spiral develops as companies raise prices to protect compressing margins. This goes on until there’s a steep rise in unemployment which breaks the cycle. Central banks keep rates high until they reign in inflation. This causes the yield curve to invert. During this phase, cash is the best asset.

Additional notes from Merrill Lynch:

Cyclicality: When growth is accelerating (12 o'clock), Stocks and Commodities do well. Cyclical sectors like Tech or Steel outperform. When growth is slowing (6 o'clock), Bonds, Cash, and defensives outperform.

Duration: When inflation is falling (9 o'clock), discount rates drop and financial assets do well. Investors pay up for long duration Growth stocks. When inflation is rising (3 o'clock), real assets like Commodities and Cash do best. Pricing power is plentiful and short-duration Value stocks outperform.

Interest Rate-Sensitives: Banks and Consumer Discretionary stocks are interest-rate sensitive “early cycle” performers, doing best in Reflation and Recovery when central banks are easing and growth is starting to recover.

Asset Plays: Some sectors are linked to the performance of an underlying asset. Insurance stocks and Investment Banks are often bond or equity price sensitive, doing well in the Reflation or Recovery phases. Mining stocks are metal price-sensitive, doing well during an Overheat.

About the indicator:

This indicator suggests iShares ETFs for sector rotation analysis. There are likely other ETFs to consider which have lower fees and are outperforming their sector peers.

You may get errors if your chart is set to a different timeframe & ticker other than 1d for symbol/tickers GDPC1 or CPILFESL.

Investment Clock settings are based on a "sustainable level" of growth and inflation, which are each slightly subjective depending on the economist and probably have changed since the last time this indicator was updated. Hence, the sustainable levels are customizable in the settings. When I was formally educated I was trained to use average CPI of 3.1% for financial planning purposes, the default for the indicator is 2.5%, and the Medium article backtested and optimized a 2% sustainable inflation rate. Again, user-defined sustainable growth and rates are slightly subjective and will affect results.

I have not been trained or even had much experience with MetaTrader code, which is how this indicator was originally coded. See the original Medium article that inspired this indicator if you want to audit & compare code.

Hover over info panel for detailed information.

Features: Advanced info panel that performs Investment Clock analysis and offers additional hover info such as sector rotation suggestions. Customizable sustainable levels, growth input, and inflation input. Phase background coloring.

⚠ DISCLAIMER: Not financial advice. Not a trading system. DYOR. I am not affiliated with Medium, Macro Ops, iShares, or Merrill Lynch.

About the Author: I am a patent-holding inventor, a futures trader, a hobby PineScripter, and a former FINRA Registered Representative.

10yr, 20yr, 30yr Averages: Month/Month % Change; SeasonalityCalculates 10yr, 20yr and 30yr averages for month/month % change

~shows seasonal tendencies in assets (best in commodities). In above chart: August is a seasonally bullish month for Gold: All the averages agree. And January is the most seasonally bullish month.

~averages represent current month/previous month. i.e. Jan22 average % change represents whole of jan22 / whole of dec21

~designed for daily timeframe only: I found calling monthly data too buggy to work with, and I thought weekly basis may be less precise (though it would certainly reduce calculation time!)

~choose input year, and see the previous 10yrs of monthly % change readings, and previous 10yrs Average, 20yr Average, 30yr Average for the respective month. Labels table is always anchored to input year.

~user inputs: colors | label sizes | decimal places | source expression for averages | year | show/hide various sections

~multi-yr averges always print, i.e if only 10yrs history => 10yr Av = 20yr Av = 30yr Av. 'History Available' label helps here.

Based on my previously publised script: "Month/Month Percentage % Change, Historical; Seasonal Tendency"

Publishing this as seperate indicator because:

~significantly slower to load (around 13 seconds)

~non-premium users may not have the historical bars available to use 20yr or 30yr averages =>> prefer the lite/speedier version

~~tips~~

~after loading, touch the new right scale; then can drag the table as you like and seperate it from price chart

##Debugging/tweaking##

Comment-in the block at the end:

~test/verifify specific array elements elements.

~see the script calculation/load time

~~other ideas ~~

~could tweak the array.slice values in lines 313 - 355 to show the last 3 consecutive 10yr averages instead (i.e. change 0, 10 | 0,20 | 0, 30 to 0, 10 | 10, 20 | 20,30)

~add 40yr average by adding another block to each of the array functions, and tweaking the respective labels after line 313 (though this would likely add another 5 seconds to the load time)

~use alternative method for getting obtaining multi-year values from individual month elements. I used array.avg. You could try array.median, array.mode, array.variance, array.max, array.min (lines 313-355)

MACD XDThis indicator is based on the classic MACD indicator, and with the following additional features:

1. Another set of MACD and signal lines (green and orange) is added for analyzing a bigger trend in a higher time frame. The default set of MACD and signal lines (red and blue) are used for the smaller trend (current time frame).

2. Small upward and downward triangles are added to mark the golden and death crosses of MACD and signal lines: Blue and red triangles (buy and sell signals) - golden and death crosses of MACD and signal lines for the smaller trend (current time frame), green and orange triangles (buy and sell signals) - golden and death crosses of MACD and signal lines for the bigger trend (a higher time frame).

3. The total areas of histograms above and below the MACD zero axis are calculated and shown by the numbers next to the histogram. This information can be used to analyze the top and bottom divergences of the smaller trend (current time frame).

4. A line connecting peaks of adjacent positive or negative histograms is drawn when top and bottom divergences occur, which indicates a potential trend reversal.

This indicator can be used in the following way: after a golden cross occurs in the bigger trend (green arrow), a death cross in the smaller trend (red arrow) may lead to a potential long entry at the pull back of the bigger up trend; after a death cross occurs in the bigger trend (orange arrow), a golden cross in the smaller trend (blue arrow) may lead to a potential short entry at the pull back of the bigger down trend. Note that in general, golden crosses occur when MACD and signal lines are above the zero axis means a higher high will be made, and death crosses occur when MACD and signal lines are below the zero axis means a lower low will be made. On the contrary, golden crosses occurring below the zero axis or death crosses occurring above the zero axis may only lead to a potential pull back in a trend.

本指标基于经典的MACD指标,适合与缠论指标结合使用:

1. 加入第二组MACD线和信号线,适用于辅助判断缠论中的线段背离。

2. 加入计算直方图(红绿柱子)面积的部分,有助于判断缠论中的笔背离。

3. 标注出两组MACD线与信号线的金叉死叉,以及用特殊颜色表示零轴上方金叉和零轴下方死叉的情况。

4. 用直线标注出顶底背离发生的情况,利于准确分辨和判断。

Trendlines Boll Ichi S1 by GammaprodI. How to use this indicator :

------------------------------

I.1. Set your teadingview theme to dark theme.

I.2. Gammaprod indicator is valid for forex, stock and but more valid for crypto.

I.3. Use three timeframe for more validation (choose between those, that fit to your trading style) :

- Timeframe 1m, 5m, and 15m for Scalping

- Timeframe 30m, 1h and 4h for Intraday

- Timeframe 4h, 1D and 1W for Swing Trading

I.4 Always use THREE INDICATORS FROM GAMMAPROD, those three indicators is back to back each other, by the way, I only made those three indicators only (for now) :

- Trendlines Boll Ichi S1 by Gammaprod

- MACD Volume S2 by Gammaprod

- Stoch RSI Divs Zone S2 by Gammaprod

============================================================================

II. How to setting :

--------------------

II.1. Trendlines Boll Ichi Crypto by Gammaprod

II.1.A. Support and Resistance

- Well if you familiar with this indicator you can add it, but recommended for Timeframe 30m or more

II.1.B. Trendlines Primary or Trendlines Secondary

- Timeframe 1m you DON'T NEED Trendlines Primary or Trendlines Secondary

- Timeframe 5m you DON'T NEED Trendlines Secondary, but you CAN ADD Trendlines Primary if you fell it helpful (for me, it is helpful to find where the candles start or the end trend or a consolidation or where the candles will surpass a resistance or a support).

- Timeframe 15m you DON'T NEED Trendlines Secondary, DEFENITELY add Trendlines Primary it will help to find where the candles stop or a consolidation or where the candles will surpass a resistance or a support).

- Timeframe 30m or more, DEFENITELY NEED BOTH Trendlines Primary and Secondary Trendlines, it will help to find where the candle stop or consolidation or where the candle will surpass a resistance or support).

II.1.C. Bollinger, Ichimoku Cloud and Lagging Span

- Please DON'T CHANGE IT at all, it's really helpful to know when and where to make an entry decesion or a trend or a consolidation, if you don't understand how to read it, you better to learn it first (on "how to read" section and "How to OPEN position" the section below)

II.2. Stoch RSI Divs Zone Crypto by Gammaprod (DON'T CHANGE IT)

II.3. MACD Volume Crypto by Gammaprod (DON'T CHANGE IT)

============================================================================

III. How to read :

------------------

III.1. Sell or Buy Priority :

III.1.A. Sell Priority

- Color background on macd and stoch rsi is pink or purple sell is the priority, (if you're not sure to buy, just wait until the best moment to sell)

III.1.B. Buy Priority

- Color background on macd and stoch rsi Teal or light green buy is the priority, (if you're not sure to sell, just wait until the best moment to buy)

III.1.C. Indecision / Golden Moment

- Color background on stoch rsi yellow is indecision / golden moment of reversal pattern (wait until it formed background only on Stoch RSI), please be careful at this moment.

III.2. Trend / Consolidation :

III.2.A. BULLISH trend

- When Stoch RSI and MACD have teal or light green background that's means BULLISH trend, better to confirm by the candle is above green cloud and lagging span (red line) is also above the candle.

III.2.B. BEARISH trend

- When Stoch RSI and MACD have the Pink or purple background that's means BEARISH trend, better to confirm by the candle is above purple cloud and lagging span (red line) is also below the candle.

III.2.C. CONSOLIDATION

- When Stoch RSI have the mix background that's means CONSOLIDATION, better to confirm by the candle is in or near to green / purple cloud and lagging span (red line) is also on the candle.

III.3. Special Mark

III.3.A. Ideal Bullish :

- Near line 20 and green / teal background = When Stoch RSI have the char R / H on lime color label, that's means divergence or hidden divergence for buy position, if you not see this label that's means just a standard confirmation for buy

III.3.B. Not an Ideal Bullish :

- Near line 80 and green / teal background = if this happens make sure you know what happen, it could be a false signal or bullish continual pattern

III.3.C. Ideal Bearish :

- Near line 80 and pink / purple background = When Stoch RSI have the char R / H on lime color label, that's means divergence or hidden divergence for buy position, if you not see this label that's means just a standard confirmation for sell position.

III.3.D. Not an Ideal Bearish:

- Near line 20 and pink / purple background = if this happens make sure you know what happen, it could be a false signal or bearish continual pattern

III.3.E. The Beginning of Reversal (from BEARISH to BULLISH) :

- When Stoch RSI line shaping GREEN position is near 20.

- MACD lines still PINK, position lines is UNDER the HISTOGRAM, but the HISTOGRAM start to SHAPE FALL PINK (light pink) and the BACKGROUND still PINK / PURPLE.

- Position CANDLES NEAR BLUE line, NEAR PURPLE CLOUD, and lagging span (red line) STILL ON the area candle. (it used to be confirmed with the golden moment).

III.3.F. The Beginning of Reversal (from BULLISH to BEARISH) :

- When Stoch RSI line shaping PINK position is near 80.

- MACD lines still GREEN, position lines is ABOVE the HISTOGRAM, but the HISTOGRAM start to SHAPE FALL GREEN (light green) and the BACKGROUND still TEAL / GREEN.

- Position CANDLES NEAR WHITE line, NEAR TEAL CLOUD, and lagging span (red line) STILL ON the area candle. (it used to be confirmed with the golden moment).

III.3.G. False Signals, or It could be a Golden Moment (better to see it on TF 15 or bigger):

- Near line 20 or 80 and yellow background = When Stoch RSI have the char R / H on color label, that's means divergence or hidden divergence for buy / sell position, if you not see this label that's means just a standard confirmation for buy / sell depends on where the Stoch RSI line if near 20 that's means buy, near 80 means sell

============================================================================

IV. How to OPEN position:

-------------------------

IV.1. Bullish

IV.1.A. Trendlines Boll Ichi S1 by Gammaprod

- The candles above the green cloud.

- Lagging span (red line) above the candles.

- then open buy near yellow line (the first option) / blue line (the second option) (always confirm the position with two other indicators below).

IV.1.B. MACD Volume S2 by Gammaprod

- Teal or Green background.

- The lines is shaped or shaping green.

- Better if at the green histogram.

IV.1.C. Stoch RSI Divs Zone S3 by Gammaprod

- Teal or Green background.

- The lines is shaping green.

- Better if on the bottom (at a range 20).

IV.2. Bearish

IV.2.A. Trendlines Boll Ichi S1 by Gammaprod

- The candles below the purple cloud.

- Lagging span (red line) below the candles.

- then open buy near yellow line (the first option) / white line (the second option) (always confirm the position with two other indicators below).

IV.2.B. MACD Volume S2 by Gammaprod

- Pink or purple background.

- The lines are shaped or shaping green.

- Better if at the pink histogram.

IV.2.C. Stoch RSI Divs Zone S3 by Gammaprod

- Pink or purple background.

- The lines are shaping pink.

- Better if the line on the top (at a range 80).

IV.3. Consolidation

IV.3.A. Trendlines Boll Ichi S1 by Gammaprod

- The candles on the cloud (green or purple).

- Lagging span (red line) on the candles.

- then open buy near the white or blue line (always confirm the position with two other indicators below).

IV.3.B. MACD Volume S2 by Gammaprod

- Changing the background.

- The line is near the middle line.

- Have small Histogram.

IV.3.C. Stoch RSI Divs Zone S3 by Gammaprod

- Mix background specially on a timeframe 15m or more.

- The line move fast up and down.

- Better if on the bottom or the top of the lines (at a range 20 or 80).

============================================================================

>> The secret ingredient is comparing the timeframe :

The example scalping (Timeframe 1m, 5m and 15m)

- TF 1m is for making an open position.

- TF 5m is for making a judgement of the trend market.

- TF 15m is to confirm that judgement from TF 5m, be careful if it not similar then it used to be a consolidation or the beginning of the reversal.

There's a lot a way to open the position than above information that i gave it to you, but consider there are a limit chars on this column, I hope it will help your trading and make a more profit on it.

MACD Volume S2 By Gammaprod>> How to use this indicator :

1. Set your teadingview theme to dark theme.

2. My indicator is valid for forex, stock and but more valid for crypto.

3. Use three timeframe for more validation (choose between those, that fit to your trading style) :

- Timeframe 1m, 5m, and 15m for Scalping

- Timeframe 30m, 1h and 4h for Intraday

- Timeframe 4h, 1D and 1W for Swing Trading

4 . Always use THREE INDICATORS FROM GAMMAPROD, those three indicators is back to back each other, by the way, I only made those three indicators only (for now) :

- Trendlines Boll Ichi Crypto by Gammaprod

- Stoch RSI Divs Zone Crypto by Gammaprod

- MACD Volume Crypto by Gammaprod

>> How to setting :

1. Trendlines Boll Ichi Crypto by Gammaprod

A. Support and Resistence

- Well if you familiar with this indicator you can add it, but recommended for Timeframe 30m or more

B. Trendlines Primary or Trendlines Secondary

- Timeframe 1m you DON'T NEED Trendlines Primary or Trendlines Secondary

- Timeframe 5m you DON'T NEED Trendlines Secondary, but you CAN ADD Trendlines Primary if you fell it helpful (for me, it is helpful to find where the candles start or the end trend or a consolidation or where the candles will surpass a resistance or a support).

- Timeframe 15m you DON'T NEED Trendlines Secondary, DEFENITELY add Trendlines Primary it will help to find where the candles stop or a consolidation or where the candles will surpass a resistance or a support).

- Timeframe 30m or more, DEFENITELY NEED BOTH Trendlines Primary and Secondary Trendlines, it will help to find where the candle stop or consolidation or where the candle will surpass a resistance or support).

C. Bolinger, Ichimoku Cloud and Lagging Span

- Please DON'T CHANGE IT at all, it's really helpful to know when and where to make an entry decesion or a trend or a consolidation, if you don't understand how to read it, you better to learn it first (on "how to read" section and "How to OPEN position" the section below)

2. Stoch RSI Divs Zone Crypto by Gammaprod (DON'T CHANGE IT)

3. MACD Volume Crypto by Gammaprod (DON'T CHANGE IT)

>> How to read :

1. Sell or Buy Priority :

A. Buy Priority

- Color background on macd and stoch rsi is pink or purple sell is the priority, (if you're not sure to buy, just wait until the best moment to sell)

B. Buy Priority

- Color background on macd and stoch rsi Teal or light green buy is the priority, (if you're not sure to sell, just wait until the best moment to buy)

C. Indecision / Golden Moment

- Color background on stoch rsi yellow is indecision / golden moment of reversal pattern (wait until it formed background only on Stoch RSI), please becareful at this moment.

2. Trend / Consolidation :

A. BULLISH trend

- When Stoch RSI and MACD have teal or light green background that's means BULLISH trend, better to confirm by the candle is above green cloud and lagging span (red line) is also above the candle.

B. BEARISH trend

- When Stoch RSI and MACD have the Pink or purple background that's means BEARISH trend, better to confirm by the candle is above purple cloud and lagging span (red line) is also below the candle.

C. CONSOLIDATION

- When Stoch RSI have the mix background that's means CONSOLIDATION, better to confirm by the candle is in or near to green / purple cloud and lagging span (red line) is also on the candle.

3. Special Mark

A. Ideal Bullish :

- Near line 20 and green / teal background = When Stoch RSI have the char R / H on lime color label, that's means divergence or hidden divergence for buy position, if you not see this label that's means just a standard confirmation for buy

B. Not an Ideal Bullish :

- Near line 80 and green / teal background = if this happens make sure you know what happen, it could be a false signal or bullish continual pattern

C. Ideal Bearish :

- Near line 80 and pink / purple background = When Stoch RSI have the char R / H on lime color label, that's means divergence or hidden divergence for buy position, if you not see this label that's means just a standard confirmation for sell position.

D. Not an Ideal Bearish:

- Near line 20 and pink / purple background = if this happens make sure you know what happen, it could be a false signal or bearish continual pattern

E. The Beginning of Reversal (from BEARISH to BULLISH) :

- When Stoch RSI line shaping GREEN position is near 20.

- MACD lines still PINK, position lines is UNDER the HISTOGRAM, but the HISTOGRAM start to SHAPE FALL PINK (light pink) and the BACKGROUND still PINK / PURPLE.

- Position CANDLES NEAR BLUE line, NEAR PURPLE CLOUD, and lagging span (red line) STILL ON the area candle. (it used to be confirmed with the golden moment).

F. The Beginning of Reversal (from BULLISH to BEARISH) :

- When Stoch RSI line shaping PINK position is near 80.

- MACD lines still GREEN, position lines is ABOVE the HISTOGRAM, but the HISTOGRAM start to SHAPE FALL GREEN (light green) and the BACKGROUND still TEAL / GREEN.

- Position CANDLES NEAR WHITE line, NEAR TEAL CLOUD, and lagging span (red line) STILL ON the area candle. (it used to be confirmed with the golden moment).

G. False Signals, or It could be a Golden Moment (better to see it on TF 15 or bigger):

- Near line 20 or 80 and yellow background = When Stoch RSI have the char R / H on color label, that's means divergence or hidden divergence for buy / sell position, if you not see this label that's means just a standard confirmation for buy / sell depends on where the Stoch RSI line if near 20 that's means buy, near 80 means sell

>> How to OPEN position:

A. Bullish

1. Trendlines Boll Ichi Crypto by Gammaprod

- The candles above the green cloud.

- Lagging span (red line) above the candles.

- then open buy near yellow line (the first option) / blue line (the second option) (always confirm the position with two other indicators below).

2. Stoch RSI Divs Zone Crypto by Gammaprod

- Teal or Green background.

- The lines is shaping green.

- Better if on the bottom (at a range 20).

3. MACD Volume Crypto by Gammaprod

- Teal or Green background.

- The lines is shaped or shaping green.

- Better if at the green histogram.

B. Bearish

1. Trendlines Boll Ichi Crypto by Gammaprod

- The candles below the purple cloud.

- Lagging span (red line) below the candles.

- then open buy near yellow line (the first option) / white line (the second option) (always confirm the position with two other indicators below).

2. Stoch RSI Divs Zone Crypto by Gammaprod

- Pink or purple background.

- The lines are shaping pink.

- Better if the line on the top (at a range 80).

3. MACD Volume Crypto by Gammaprod

- Pink or purple background.

- The lines are shaped or shaping green.

- Better if at the pink histogram.

C. Consolidation

1. Trendlines Boll Ichi Crypto by Gammaprod

- The candles on the cloud (green or purple).

- Lagging span (red line) on the candles.

- then open buy near the white or blue line (always confirm the position with two other indicators below).

2. Stoch RSI Divs Zone Crypto by Gammaprod

- Mix background specially on a timeframe 15m or more.

- The line move fast up and down.

- Better if on the bottom or the top of the lines (at a range 20 or 80).

3. MACD Volume Crypto by Gammaprod

- Changing the background.

- The line is near the middle line.

- Have small Histogram.

>> The secret ingridient is comparing the timeframe :

The example scalping (Timeframe 1m, 5m and 15m)

- TF 1m is for making an open position.

- TF 5m is for making a judgement of the trend market.

- TF 15m is to confirm that judgement from TF 5m, be careful if it not similar then it used to be a consolidation or the beginning of the reversal.

There's a lot a way to open the position than above information that i gave it to you, but consider there are a limit char on this column, I hope it will help your trading and make a more profit on it.

Stoch RSI, Div, Zone S3 by Gammaprod>> How to use this indicator :

1. Set your teadingview theme to dark theme.

2. My indicator is valid for forex, stock and but more valid for crypto.

3. Use three timeframe for more validation (choose between those, that fit to your trading style) :

- Timeframe 1m, 5m, and 15m for Scalping

- Timeframe 30m, 1h and 4h for Intraday

- Timeframe 4h, 1D and 1W for Swing Trading

4 . Always use THREE INDICATORS FROM GAMMAPROD, those three indicators is back to back each other, by the way, I only made those three indicators only (for now) :

- Trendlines Boll Ichi Crypto by Gammaprod

- Stoch RSI Divs Zone Crypto by Gammaprod

- MACD Volume Crypto by Gammaprod

>> How to setting :

1. Trendlines Boll Ichi Crypto by Gammaprod

A. Support and Resistence

- Well if you familiar with this indicator you can add it, but recommended for Timeframe 30m or more

B. Trendlines Primary or Trendlines Secondary

- Timeframe 1m you DON'T NEED Trendlines Primary or Trendlines Secondary

- Timeframe 5m you DON'T NEED Trendlines Secondary, but you CAN ADD Trendlines Primary if you fell it helpful (for me, it is helpful to find where the candles start or the end trend or a consolidation or where the candles will surpass a resistance or a support).

- Timeframe 15m you DON'T NEED Trendlines Secondary, DEFENITELY add Trendlines Primary it will help to find where the candles stop or a consolidation or where the candles will surpass a resistance or a support).

- Timeframe 30m or more, DEFENITELY NEED BOTH Trendlines Primary and Secondary Trendlines, it will help to find where the candle stop or consolidation or where the candle will surpass a resistance or support).

C. Bolinger, Ichimoku Cloud and Lagging Span

- Please DON'T CHANGE IT at all, it's really helpful to know when and where to make an entry decesion or a trend or a consolidation, if you don't understand how to read it, you better to learn it first (on "how to read" section and "How to OPEN position" the section below)

2. Stoch RSI Divs Zone Crypto by Gammaprod (DON'T CHANGE IT)

3. MACD Volume Crypto by Gammaprod (DON'T CHANGE IT)

>> How to read :

1. Sell or Buy Priority :

A. Buy Priority

- Color background on macd and stoch rsi is pink or purple sell is the priority, (if you're not sure to buy, just wait until the best moment to sell)

B. Buy Priority

- Color background on macd and stoch rsi Teal or light green buy is the priority, (if you're not sure to sell, just wait until the best moment to buy)

C. Indecision / Golden Moment

- Color background on stoch rsi yellow is indecision / golden moment of reversal pattern (wait until it formed background only on Stoch RSI), please becareful at this moment.

2. Trend / Consolidation :

A. BULLISH trend

- When Stoch RSI and MACD have teal or light green background that's means BULLISH trend, better to confirm by the candle is above green cloud and lagging span (red line) is also above the candle.

B. BEARISH trend

- When Stoch RSI and MACD have the Pink or purple background that's means BEARISH trend, better to confirm by the candle is above purple cloud and lagging span (red line) is also below the candle.

C. CONSOLIDATION

- When Stoch RSI have the mix background that's means CONSOLIDATION, better to confirm by the candle is in or near to green / purple cloud and lagging span (red line) is also on the candle.

3. Special Mark

A. Ideal Bullish :

- Near line 20 and green / teal background = When Stoch RSI have the char R / H on lime color label, that's means divergence or hidden divergence for buy position, if you not see this label that's means just a standard confirmation for buy

B. Not an Ideal Bullish :

- Near line 80 and green / teal background = if this happens make sure you know what happen, it could be a false signal or bullish continual pattern

C. Ideal Bearish :

- Near line 80 and pink / purple background = When Stoch RSI have the char R / H on lime color label, that's means divergence or hidden divergence for buy position, if you not see this label that's means just a standard confirmation for sell position.

D. Not an Ideal Bearish:

- Near line 20 and pink / purple background = if this happens make sure you know what happen, it could be a false signal or bearish continual pattern

E. The Beginning of Reversal (from BEARISH to BULLISH) :

- When Stoch RSI line shaping GREEN position is near 20.

- MACD lines still PINK, position lines is UNDER the HISTOGRAM, but the HISTOGRAM start to SHAPE FALL PINK (light pink) and the BACKGROUND still PINK / PURPLE.

- Position CANDLES NEAR BLUE line, NEAR PURPLE CLOUD, and lagging span (red line) STILL ON the area candle. (it used to be confirmed with the golden moment).

F. The Beginning of Reversal (from BULLISH to BEARISH) :

- When Stoch RSI line shaping PINK position is near 80.

- MACD lines still GREEN, position lines is ABOVE the HISTOGRAM, but the HISTOGRAM start to SHAPE FALL GREEN (light green) and the BACKGROUND still TEAL / GREEN.

- Position CANDLES NEAR WHITE line, NEAR TEAL CLOUD, and lagging span (red line) STILL ON the area candle. (it used to be confirmed with the golden moment).

G. False Signals, or It could be a Golden Moment (better to see it on TF 15 or bigger):

- Near line 20 or 80 and yellow background = When Stoch RSI have the char R / H on color label, that's means divergence or hidden divergence for buy / sell position, if you not see this label that's means just a standard confirmation for buy / sell depends on where the Stoch RSI line if near 20 that's means buy, near 80 means sell

>> How to OPEN position:

A. Bullish

1. Trendlines Boll Ichi Crypto by Gammaprod

- The candles above the green cloud.

- Lagging span (red line) above the candles.

- then open buy near yellow line (the first option) / blue line (the second option) (always confirm the position with two other indicators below).

2. Stoch RSI Divs Zone Crypto by Gammaprod

- Teal or Green background.

- The lines is shaping green.

- Better if on the bottom (at a range 20).

3. MACD Volume Crypto by Gammaprod

- Teal or Green background.

- The lines is shaped or shaping green.

- Better if at the green histogram.

B. Bearish

1. Trendlines Boll Ichi Crypto by Gammaprod

- The candles below the purple cloud.

- Lagging span (red line) below the candles.

- then open buy near yellow line (the first option) / white line (the second option) (always confirm the position with two other indicators below).

2. Stoch RSI Divs Zone Crypto by Gammaprod

- Pink or purple background.

- The lines are shaping pink.

- Better if the line on the top (at a range 80).

3. MACD Volume Crypto by Gammaprod

- Pink or purple background.

- The lines are shaped or shaping green.

- Better if at the pink histogram.

C. Consolidation

1. Trendlines Boll Ichi Crypto by Gammaprod

- The candles on the cloud (green or purple).

- Lagging span (red line) on the candles.

- then open buy near the white or blue line (always confirm the position with two other indicators below).

2. Stoch RSI Divs Zone Crypto by Gammaprod

- Mix background specially on a timeframe 15m or more.

- The line move fast up and down.

- Better if on the bottom or the top of the lines (at a range 20 or 80).

3. MACD Volume Crypto by Gammaprod

- Changing the background.

- The line is near the middle line.

- Have small Histogram.

>> The secret ingridient is comparing the timeframe :

The example scalping (Timeframe 1m, 5m and 15m)

- TF 1m is for making an open position.

- TF 5m is for making a judgement of the trend market.

- TF 15m is to confirm that judgement from TF 5m, be careful if it not similar then it used to be a consolidation or the beginning of the reversal.

There's a lot a way to open the position than above information that i gave it to you, but consider there are a limit char on this column, I hope it will help your trading and make a more profit on it.

[blackcat] L2 Hann Ehanced DMILevel: 2

Background

Among the many indicators, it can be said that DMI is the only "super turning" indicator. This indicator can alone send out risk warning signals when extreme market conditions occur in the stock market, helping us to solve some problems.

If we can operate according to the instructions of DMI, firstly, we can avoid the mistake of buying stocks at the head. Secondly, in the process of falling fear of the market, we can follow the direction signal sent by DMI and catch every time on the way down. Opportunity to rebound to unwind.

If you look at the diagram of the DMI, you will think it is very complicated, because there are four lines in its diagram, and they are intertwined, and it is difficult to distinguish the complex signals in it. But don't worry about its complex structure, we will fully dissect this indicator.

Function

These four lines are: PDI, MDI, ADX and ADXR. The scale of the table is from 0-100, which means from very weak to very strong. The PDI curve and MDI curve on some software are called +DI curve and -DI curve , all have the same meaning.

PDI: Represents the position of multiple parties in the market.

In market movements, the higher the PDI, the stronger the current market. On the contrary, it is a weak market. The A-share market is easy to go to extremes. Therefore, we can see that in the past A-share market, the PDI sometimes fell to near zero, and at this time, it often indicated that a rebound and uptrend was about to start.

MDI: Represents the position of the bears in the market.

In the market movement, the higher the MDI goes, the weaker the current market is, and vice versa, it is a strong market. Before a big bull market comes, we can see the MDI drop to a position close to zero, and at this time, the bears in the market have no power to fight back.

The relationship between PDI and MDI:

In the operation of the market, PDI and MDI are intertwined with each other. If the PDI is above the MDI, the market at this time is a strong market. The MDI is above the PDI, which is a bear market. The closer the distance between the two, the market is in a stalemate of consolidation. On the contrary, the further apart the two lines are, the more obvious the unilateral nature of the market is, whether it is a bull market or a bear market. The so-called unilateral market means that there is no midway adjustment when it rises, and there is no rebound correction when it falls.

ADX: Fast steering pullback.

The difference between ADX and other analysis indicators is that whether it is rising or falling, as long as there is a unilateral market, it runs upwards, not like other indicators, the strong market runs upwards and the weak market runs downwards.

The thread is almost entwined with PDI and MDI in general market movement, which makes no sense at this time. However, once the market breaks out of the market and starts to go to extremes, whether the market is rising or falling, ADX will start to run upwards. At this time, ADX has a clear meaning, because DMI has begun to issue early warning of impending turn!

ADXR: slow pull back.

This line is matched to ADX and is a moving average of ADX values. When ADX goes up, ADXR goes up with it, just slower.

When a round of rapid decline ends, it usually needs to be corrected by a rebound, and ADX will take the lead in turning up. Once it crosses with ADXR, it is regarded as an effective breakthrough.

Numerical division. I set an input threshold for HEDMI, and users can set the optimal threshold to buy and sell according to different TFs.

When PDI crosses the threshold, no matter how strong the bull market is, we must beware of risks from happening at any time.

In order to distinguish more clearly, I slightly modified the formula of the system, and when this happens, the indicator will issue a green warning label, so as to avoid risks in time.

Comprehensive use of four lines:

If the four lines in the steering indicator DMI are intertwined below 50, it usually means that the market is in a state of mild consolidation at this time. The DMI indicator at this time is useless because it does not generate a strong pullback force. Don't worry about an unexpected turnaround in the market. As for the consolidation, it's not a turnaround, it's a breakout.

When PDI and MDI gradually separate, at this time, ADX and ADXR will also rise. At this time, the DIM that is usually messy like twine will be clearly separated. When rising, PDI rises along with ADX and ADXR, while MDI sinks weakly. On the contrary, when the market starts to fall, MDI will rise along with ADX and ADXR, and PDI will sink helplessly. At this time, the DMI will be like a "tiger's mouth", gradually opening its bloody mouth. The bigger the opening, the more lethal the bite.

Here comes a tactic, or technical trend, called double hooves, that is, PDI and MDI split, ADX and ADXR upward to produce golden forks, PDI and MDI are like the double front hooves of a horse, ADX and ADXR The golden fork is like the rear hooves of a steed ready to take off, and this trend of the four lines is like the four legs of a steed that is about to run.

If you think it is too complicated to look at DMI like this, then I can tell you the easiest way to judge, that is, just look at the PDI line. When the PDI line falls below 10, boldly buy the dip, because it is a dip, so you need to calculate the rebound At this time, combined with the golden section theory I often talk about, you can easily find the selling point by making the golden section of the downward trend for the previous trend.

This kind of bottom-hunting method uses the golden section theory, and basically there will be no losses. Remember that one thing is not to be greedy and strictly enforce discipline. This is bottom-hunting, and advancing with both hooves is chasing up. The two styles are different, and the operation styles are different. You also need to explore more in actual combat. Any kind of trick, if you practice it proficiently, it is a unique trick.

Remark

Hanning Window Enhanced DMI

Free and Open Source Indicator

Auto Phivots PP S/R Log /Lin V2 [DM]Greetings, I cover version two since the code has had great changes.

This script has two time frames with a separate symbol from the main window.

Alerts for the two different configurable time frames.

Van use for a big ranges or small and Log Scales.

The colors, extensions, thickness, style of the lines and the labels are completely configurable.

With a few small adjustments it can be used in a separate window with another symbol

Enjoy BigfOOts

Pythagorean Means of Moving AveragesDESCRIPTION

Pythagorean Means of Moving Averages

1. Calculates a set of moving averages for high, low, close, open and typical prices, each at multiple periods.

Period values follow the Fibonacci sequence.

The "short" set includes moving average having the following periods: 5, 8, 13, 21, 34, 55, 89, 144, 233, 377.

The "mid" set includes moving average having the following periods: 5, 8, 13, 21, 34, 55, 89, 144, 233, 377, 610, 987, 1597.

The "long" set includes moving average having the following periods: 5, 8, 13, 21, 34, 55, 89, 144, 233, 377, 610, 987, 1597, 2584, 4181.

2. User selects the type of moving average: SMA, EMA, HMA, RMA, WMA, VWMA.

3. Calculates the mean of each set of moving averages.

4. User selects the type of mean to be calculated: 1) arithmetic, 2) geometric, 3) harmonic, 4) quadratic, 5) cubic. Multiple mean calculations may be displayed simultaneously, allowing for comparison.

5. Plots the mean for high, low, close, open, and typical prices.

6. User selects which plots to display: 1) high and low prices, 2) close prices, 3) open prices, and/or 4) typical prices.

7. Calculates and plots a vertical deviation from an origin mean--the mean from which the deviation is measured.

8. Deviation = origin mean x a x b^(x/y)/c.

9. User selects the deviation origin mean: 1) high and low prices plot, 2) close prices plot, or 3) typical prices plot.

10. User defines deviation variables a, b, c, x and y.

Examples of deviation:

a) Percent of the mean = 1.414213562 = 2^(1/2) = Pythagoras's constant (default).

b) Percent of the mean = 0.7071067812 = = = sin 45˚ = cos 45˚.

11. Displaces the plots horizontally +/- by a user defined number of periods.

PURPOSE

1. Identify price trends and potential levels of support and resistance.

CREDITS

1. "Fibonacci Moving Average" by Sofien Kaabar: two plots, each an arithmetic mean of EMAs of 1) high prices and 2) low prices, with periods 5, 8, 13, 21, 34, 55, 89, 144, 233, 377, 610, 987, 1597, 2584, 4181.

2. "Solarized" color scheme by Ethan Schoonover.

vol_premiaThis script shows the volatility risk premium for several instruments. The premium is simply "IV30 - RV20". Although Tradingview doesn't provide options prices, CBOE publishes 30-day implied volatilities for many instruments (most of which are VIX variations). CBOE calculates these in a standard way, weighting at- and out-of-the-money IVs for options that expire in 30 days, on average. For realized volatility, I used the standard deviation of log returns. Since there are twenty trading periods in 30 calendar days, IV30 can be compared to RV20. The "premium" is the difference, which reflects market participants' expectation for how much upcoming volatility will over- or under-shoot recent volatility.

The script loads pretty slow since there are lots of symbols, so feel free to delete the ones you don't care about. Hopefully the code is straightforward enough. I won't list the meaning of every symbols here, since I might change them later, but you can type them into tradingview for data, and read about their volatility index on CBOE's website. Some of the more well-known ones are:

ES: S&P futures, which I prefer to the SPX index). Its implied volatility is VIX.

USO: the oil ETF representing WTI future prices. Its IV is OVX.

GDX: the gold miner's ETF, which is usually more volatile than gold. Its IV is VXGDX.

FXI: a china ETF, whose volatility is VXFXI.

And so on. In addition to the premium, the "percentile" column shows where this premium ranks among the previous 252 trading days. 100 = the highest premium, 0 = the lowest premium.

MathConstantsLibrary "MathConstants"

Mathematical Constants

E() The number e

Log2E() The number log (e)

Log10E() The number log (e)

Ln2() The number log (2)

Ln10() The number log (10)

LnPi() The number log (pi)

Ln2PiOver2() The number log (2*pi)/2

InvE() The number 1/e

SqrtE() The number sqrt(e)

Sqrt2() The number sqrt(2)

Sqrt3() The number sqrt(3)

Sqrt1Over2() The number sqrt(1/2) = 1/sqrt(2) = sqrt(2)/2

HalfSqrt3() The number sqrt(3)/2

Pi() The number pi

Pi2() The number pi*2

PiOver2() The number pi/2

Pi3Over2() The number pi*3/2

PiOver4() The number pi/4

SqrtPi() The number sqrt(pi)

Sqrt2Pi() The number sqrt(2pi)

SqrtPiOver2() The number sqrt(pi/2)

Sqrt2PiE() The number sqrt(2*pi*e)

LogSqrt2Pi() The number log(sqrt(2*pi))

LogSqrt2PiE() The number log(sqrt(2*pi*e))

LogTwoSqrtEOverPi() The number log(2 * sqrt(e / pi))

InvPi() The number 1/pi

TwoInvPi() The number 2/pi

InvSqrtPi() The number 1/sqrt(pi)

InvSqrt2Pi() The number 1/sqrt(2pi)

TwoInvSqrtPi() The number 2/sqrt(pi)

TwoSqrtEOverPi() The number 2 * sqrt(e / pi)

Degree() The number (pi)/180 - factor to convert from Degree (deg) to Radians (rad).

Grad() The number (pi)/200 - factor to convert from NewGrad (grad) to Radians (rad).

PowerDecibel() The number ln(10)/20 - factor to convert from Power Decibel (dB) to Neper (Np). Use this version when the Decibel represent a power gain but the compared values are not powers (e.g. amplitude, current, voltage).

NeutralDecibel() The number ln(10)/10 - factor to convert from Neutral Decibel (dB) to Neper (Np). Use this version when either both or neither of the Decibel and the compared values represent powers.

Catalan() The Catalan constant

Sum(k=0 -> inf){ (-1)^k/(2*k + 1)2 }

EulerMascheroni() The Euler-Mascheroni constant

lim(n -> inf){ Sum(k=1 -> n) { 1/k - log(n) } }

GoldenRatio() The number (1+sqrt(5))/2, also known as the golden ratio

Glaisher() The Glaisher constant

e^(1/12 - Zeta(-1))

Khinchin() The Khinchin constant

prod(k=1 -> inf){1+1/(k*(k+2))^log(k,2)}

Long only EMA CROSS 8/50/200 BacktestImprove EMA CROSS 8/50/200 with adjustable Exit EMA Level, and can open trade only when above EMA200