Intraday Combo Strategy HHStochastic RSI Momentum/Reversal quickly identifies overbought/oversold zones

MACD Momentum/Trend confirms a trend reversal, a late but powerful signal

Supertrend Trend Tracking provides clear and concise buy/sell signals

Bollinger Bands Volatility shows price deviation during breakouts/squeezes

ADX Trend Strength measures trend strength to filter out false signals

在脚本中搜索"adx"

DVPOOverview

The DVPO (Dynamic Volume Profile Oscillator) Strategy is a comprehensive and highly customizable trading tool designed for precision and control. It is built around a unique, volume-driven oscillator that identifies potential market entries by analyzing the relationship between price, volume, and volatility.

This strategy is not just another signal generator; it's a complete framework that includes dynamic entry logic, adaptive risk management (ATR Stop Loss and R:R-based Take Profit), and a powerful dashboard of 10+ optional confirmation filters to help you tailor the strategy to your specific instrument, timeframe, and trading style.

The Core Concept: The DVPO Oscillator

The heart of this strategy is the DVPO oscillator. Unlike standard oscillators like RSI or Stochastics, the DVPO's primary goal is to quantify how far the current price has deviated from its recent volume-weighted "fair value."

Here’s how it works conceptually:

Micro Volume Profile: The indicator first analyzes a recent period of bars (defined by Lookback Period) to build a mini-profile of price and volume.

Volume-Weighted Mean: From this profile, it calculates a volume-weighted average price (VWAP) and the average deviation from that mean. This establishes the central point of value for the recent period.

Deviation Measurement: The oscillator's value is derived from how far the current price is from this calculated mean, scaled by the observed price deviation and a user-defined Sensitivity. A value above the midline suggests the price is trading at a premium, while a value below suggests it's at a discount.

Adaptive Volatility Zones: Instead of using fixed overbought/oversold levels (e.g., 70/30), the DVPO calculates dynamic upper and lower zones using the standard deviation of the oscillator itself. These zones expand and contract based on recent market volatility.

An entry signal is triggered not just when the oscillator is "overbought" or "oversold," but when it breaks out of these adaptive volatility zones, signaling that a statistically significant price movement is underway.

📈 Long Entry Condition : The oscillator crosses above the dynamic upper zone.

📉 Short Entry Condition : The oscillator crosses below the dynamic lower zone.

Integrated Risk & Trade Management

A signal is useless without proper risk management. This strategy has professional-grade risk management built directly into its logic.

Stop Loss (ATR-Based): The Stop Loss is not a fixed percentage. It is calculated using the Average True Range (ATR), allowing it to adapt automatically to the market's current volatility. In volatile periods, the stop will be wider; in quiet periods, it will be tighter.

Take Profit (Risk/Reward Ratio): The Take Profit level is calculated based on a user-defined Risk/Reward Ratio. If you set a ratio of 2.0, the Take Profit target will be placed at twice the distance of the Stop Loss from your entry price.

Dynamic Position Sizing: The strategy can automatically calculate the trade quantity for you. It determines the position size based on your specified Capital Size and the % Risk Per Trade you are willing to accept, ensuring disciplined risk control on every trade.

The Filter Dashboard : Enhance Your Signal Quality

To help reduce false signals and adapt to different market conditions, the strategy includes a comprehensive dashboard of optional confirmation filters. An entry signal will only be executed if it aligns with all the filters you have activated.

Trend & Momentum Filters :

T3, VMA, & VWAP Trend Filters: Utilize a suite of advanced moving averages (T3, Variable Moving Average, and a session-based VWAP) to ensure your trades are aligned with the dominant trend.

ADX Filter: Confirms that the market has sufficient directional strength for a trend-following trade, helping to avoid entries during choppy conditions.

Kaufman Efficiency Filter: Uses the Kaufman Efficiency Ratio to measure market noise. It only allows trades when the market is trending efficiently.

Volume & Market State Filters :

Volume Flow (VFI): A sophisticated volume-based filter that confirms whether volume is supporting the price move.

TDFI (Trader's Dynamic Index): A market state indicator designed to identify when the market is primed for a strong, directional move.

Flat Market Detector: A unique filter that identifies and avoids trading in sideways or ranging markets where trend strategies typically underperform.

Trade Condition Filters :

Min TP / Max SL %: Filter out trades where the risk/reward profile doesn't meet your minimum requirements (e.g., ignore a trade if the ATR-based stop loss is more than 10% away from the price).

Session Filters: Allows you to enable or disable trading on specific days of the week and to set a Cooldown Period (a set number of bars to wait after a trade closes before looking for a new entry).

How To Use This Strategy

Start with the Core: Begin by configuring the DVPO Oscillator settings (Lookback Period, Sensitivity, Zone Width) and your Risk Management parameters (ATR Multiplier, RR Ratio, % Risk Per Trade). These form the foundation of the strategy.

Backtest and Observe: Use TradingView's Strategy Tester to see how the core signals perform on your chosen asset and timeframe.

Layer Filters Intelligently: Enable the confirmation filters one by one and re-run your backtest. Observe how each filter impacts performance (e.g., does the T3 filter increase profitability but reduce the number of trades?). The goal is to find the optimal balance between signal quality and frequency.

Visualize and Analyze: Use the Show Risk/Reward Area option to plot your entry, stop loss, and take profit levels directly on the chart for every trade, providing a clear visual representation of your trade plan.

Disclaimer: This strategy is provided for educational and analytical purposes only. Past performance is not indicative of future results. All trading involves risk, and you should conduct your own thorough backtesting and analysis before deploying any strategy in a live market.

TrendMaster Pro 2.3 with Alerts

Hello friends,

A member of the community approached me and asked me how to write an indicator that would achieve a particular set of goals involving comprehensive trend analysis, risk management, and session-based trading controls. Here is one example method of how to create such a system:

Core Strategy Components

Multi-Moving Average System - Uses configurable MA types (EMA, SMA, SMMA) with short-term (9) and long-term (21) periods for primary signal generation through crossovers

Higher Timeframe Trend Filter - Optional trend confirmation using a separate MA (default 50-period) to ensure trades align with broader market direction

Band Power Indicator - Dynamic high/low bands calculated using different MA types to identify price channels and volatility zones

Advanced Signal Filtering

Bollinger Bands Volatility Filter - Prevents trading during low-volatility ranging markets by requiring sufficient band width

RSI Momentum Filter - Uses customizable thresholds (55 for longs, 45 for shorts) to confirm momentum direction

MACD Trend Confirmation - Ensures MACD line position relative to signal line aligns with trade direction

Stochastic Oscillator - Adds momentum confirmation with overbought/oversold levels

ADX Strength Filter - Only allows trades when trend strength exceeds 25 threshold

Session-Based Trading Management

Four Trading Sessions - Asia (18:00-00:00), London (00:00-08:00), NY AM (08:00-13:00), NY PM (13:00-18:00)

Individual Session Limits - Separate maximum trade counts for each session (default 5 per session)

Automatic Session Closure - All positions close at specified market close time

Risk Management Features

Multiple Stop Loss Options - Percentage-based, MA cross, or band-based SL methods

Risk/Reward Ratio - Configurable TP levels based on SL distance (default 1:2)

Auto-Risk Calculation - Dynamic position sizing based on dollar risk limits ($150-$250 range)

Daily Limits - Stop trading after reaching specified TP or SL counts per day

Support & Resistance System

Multiple Pivot Types - Traditional, Fibonacci, Woodie, Classic, DM, and Camarilla calculations

Flexible Timeframes - Auto-adjusting or manual timeframe selection for S/R levels

Historical Levels - Configurable number of past S/R levels to display

Visual Customization - Individual color and display settings for each S/R level

Additional Features

Alert System - Customizable buy/sell alert messages with once-per-bar frequency

Visual Trade Management - Color-coded entry, SL, and TP levels with fill areas

Session Highlighting - Optional background colors for different trading sessions

Comprehensive Filtering - All signals must pass through multiple confirmation layers before execution

This approach demonstrates how to build a professional-grade trading system that combines multiple technical analysis methods with robust risk management and session-based controls, suitable for algorithmic trading across different market sessions.

Good luck and stay safe!

Hybrid: RSI + Breakout + DashboardHybrid RSI + Breakout Strategy

Adaptive trading system that switches modes based on market regime:

Ranging: Buys when RSI < 30 and sells when RSI > 70.

Trending: Enters momentum breakouts only in the direction of the 200-EMA bias, with ADX confirming trend strength.

Risk Management: Trailing stop locks profits and caps drawdown.

Optimized for BTC, ETH, and SOL on 1 h–1 D charts; back-tested from 2017 onward. Educational use only—run your own tests before deploying live funds.

Dskyz (DAFE) AI Adaptive Regime - Beginners VersionDskyz (DAFE) AI Adaptive Regime - Pro: Revolutionizing Trading for All

Introduction

In the fast-paced world of financial markets, traders need tools that can keep up with ever-changing conditions while remaining accessible. The Dskyz (DAFE) AI Adaptive Regime - Pro is a groundbreaking TradingView strategy that delivers advanced, AI-driven trading capabilities to everyday traders. Available on TradingView (TradingView Scripts), this Pine Script strategy combines sophisticated market analysis with user-friendly features, making it a standout choice for both novice and experienced traders.

Core Functionality

The strategy is built to adapt to different market regimes—trending, ranging, volatile, or quiet—using a robust set of technical indicators, including:

Moving Averages (MA): Fast and slow EMAs to detect trend direction.

Average True Range (ATR): For dynamic stop-loss and volatility assessment.

Relative Strength Index (RSI) and MACD: Multi-timeframe confirmation of momentum and trend.

Average Directional Index (ADX): To identify trending markets.

Bollinger Bands: For assessing volatility and range conditions.

Candlestick Patterns: Recognizes patterns like bullish engulfing, hammer, and double bottoms, confirmed by volume spikes.

It generates buy and sell signals based on a scoring system that weighs these indicators, ensuring trades align with the current market environment. The strategy also includes dynamic risk management with ATR-based stops and trailing stops, as well as performance tracking to optimize future trades.

What Sets It Apart

The Dskyz (DAFE) AI Adaptive Regime - Pro distinguishes itself from other TradingView strategies through several unique features, which we compare to common alternatives below:

| Feature | Dskyz (DAFE) | Typical TradingView Strategies|

|---------|-------------|------------------------------------------------------------|

| Regime Detection | Automatically identifies and adapts to **four** market regimes | Often static or limited to trend/range detection |

| Multi‑Timeframe Analysis | Uses higher‑timeframe RSI/MACD for confirmation | Rarely incorporates multi‑timeframe data |

| Pattern Recognition | Detects candlestick patterns **with volume confirmation** | Limited or no pattern recognition |

| Dynamic Risk Management | ATR‑based stops and trailing stops | Often uses fixed stops or basic risk rules |

| Performance Tracking | Adjusts thresholds based on past performance | Typically static parameters |

| Beginner‑Friendly Presets | Aggressive, Conservative, Optimized profiles | Requires manual parameter tuning |

| Visual Cues | Color‑coded backgrounds for regimes | Basic or no visual aids |

The Dskyz strategy’s ability to integrate regime detection, multi-timeframe analysis, and user-friendly presets makes it uniquely versatile and accessible, addressing the needs of everyday traders who want professional-grade tools without the complexity.

-Key Features and Benefits

[Why It’s Ideal for Everyday Traders

⚡The Dskyz (DAFE) AI Adaptive Regime - Pro democratizes advanced trading by offering professional-grade tools in an accessible package. Unlike many TradingView strategies that require deep technical knowledge or fail in changing market conditions, this strategy simplifies complex analysis while maintaining robustness. Its presets and visual aids make it easy for beginners to start, while its adaptive features and performance tracking appeal to advanced traders seeking an edge.

🔄Limitations and Considerations

Market Dependency: Performance varies by market and timeframe. Backtesting is essential to ensure compatibility with your trading style.

Learning Curve: While presets simplify use, understanding regimes and indicators enhances effectiveness.

No Guaranteed Profits: Like all strategies, success depends on market conditions and proper execution. The Reddit discussion highlights skepticism about TradingView strategies’ universal success (Reddit Discussion).

Instrument Specificity: Optimized for futures (e.g., ES, NQ) due to fixed tick values. Test on other instruments like stocks or forex to verify compatibility.

📌Conclusion

The Dskyz (DAFE) AI Adaptive Regime - Pro is a revolutionary TradingView strategy that empowers everyday traders with advanced, AI-driven tools. Its ability to adapt to market regimes, confirm signals across timeframes, and manage risk dynamically. sets it apart from typical strategies. By offering beginner-friendly presets and visual cues, it makes sophisticated trading accessible without sacrificing power. Whether you’re a novice looking to trade smarter or a pro seeking a competitive edge, this strategy is your ticket to mastering the markets. Add it to your chart, backtest it, and join the elite traders leveraging AI to dominate. Trade like a boss today! 🚀

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

-Dskyz

DI+/- Cross Strategy with ATR SL and 2% TPDI+/- Cross Strategy with ATR Stop Loss and 2% Take Profit

📝 Script Description for Publishing:

This strategy is based on the directional movement of the market using the Average Directional Index (ADX) components — DI+ and DI- — to generate entry signals, with clearly defined risk and reward targets using ATR-based Stop Loss and Fixed Percentage Take Profit.

🔍 How it works:

Buy Signal: When DI+ crosses above 40, signaling strong bullish momentum.

Sell Signal: When DI- crosses above 40, indicating strong bearish momentum.

Stop Loss: Dynamically calculated using ATR × 1.5, to account for market volatility.

Take Profit: Fixed at 2% above/below the entry price, for consistent reward targeting.

🧠 Why it’s useful:

Combines momentum breakout logic with volatility-based risk management.

Works well on trending assets, especially when combined with higher timeframe filters.

Clean BUY and SELL visual labels make it easy to interpret and backtest.

✅ Tips for Use:

Use on assets with clear trends (e.g., major forex pairs, trending stocks, crypto).

Best on 30m – 4H timeframes, but can be customized.

Consider combining with other filters (e.g., EMA trend direction or Bollinger Bands) for even better accuracy.

Market Trend Levels Non-Repainting [BigBeluga X PineIndicators]This strategy is based on the Market Trend Levels Detector developed by BigBeluga. Full credit for the concept and original indicator goes to BigBeluga.

The Market Trend Levels Detector Strategy is a non-repainting trend-following strategy that identifies market trend shifts using two Exponential Moving Averages (EMA). It also detects key price levels and allows traders to apply multiple filters to refine trade entries and exits.

This strategy is designed for trend trading and enables traders to:

Identify trend direction based on EMA crossovers.

Detect significant market levels using labeled trend lines.

Use multiple filter conditions to improve trade accuracy.

Avoid false signals through non-repainting calculations.

How the Market Trend Levels Detector Strategy Works

1. Core Trend Detection Using EMA Crossovers

The strategy detects trend shifts using two EMAs:

Fast EMA (default: 12 periods) – Reacts quickly to price movements.

Slow EMA (default: 25 periods) – Provides a smoother trend confirmation.

A bullish crossover (Fast EMA crosses above Slow EMA) signals an uptrend , while a bearish crossover (Fast EMA crosses below Slow EMA) signals a downtrend .

2. Market Level Detection & Visualization

Each time an EMA crossover occurs, a trend level line is drawn:

Bullish crossover → A green line is drawn at the low of the crossover candle.

Bearish crossover → A purple line is drawn at the high of the crossover candle.

Lines can be extended to act as support and resistance zones for future price action.

Additionally, a small label (●) appears at each crossover to mark the event on the chart.

3. Trade Entry & Exit Conditions

The strategy allows users to choose between three trading modes:

Long Only – Only enters long trades.

Short Only – Only enters short trades.

Long & Short – Trades in both directions.

Entry Conditions

Long Entry:

A bullish EMA crossover occurs.

The trade direction setting allows long trades.

Filter conditions (if enabled) confirm a valid long signal.

Short Entry:

A bearish EMA crossover occurs.

The trade direction setting allows short trades.

Filter conditions (if enabled) confirm a valid short signal.

Exit Conditions

Long Exit:

A bearish EMA crossover occurs.

Exit filters (if enabled) indicate an invalid long position.

Short Exit:

A bullish EMA crossover occurs.

Exit filters (if enabled) indicate an invalid short position.

Additional Trade Filters

To improve trade accuracy, the strategy allows traders to apply up to 7 additional filters:

RSI Filter: Only trades when RSI confirms a valid trend.

MACD Filter: Ensures MACD histogram supports the trade direction.

Stochastic Filter: Requires %K line to be above/below threshold values.

Bollinger Bands Filter: Confirms price position relative to the middle BB line.

ADX Filter: Ensures the trend strength is above a set threshold.

CCI Filter: Requires CCI to indicate momentum in the right direction.

Williams %R Filter: Ensures price momentum supports the trade.

Filters can be enabled or disabled individually based on trader preference.

Dynamic Level Extension Feature

The strategy provides an optional feature to extend trend lines until price interacts with them again:

Bullish support lines extend until price revisits them.

Bearish resistance lines extend until price revisits them.

If price breaks a line, the line turns into a dotted style , indicating it has been breached.

This helps traders identify key levels where trend shifts previously occurred, providing useful support and resistance insights.

Customization Options

The strategy includes several adjustable settings :

Trade Direction: Choose between Long Only, Short Only, or Long & Short.

Trend Lengths: Adjust the Fast & Slow EMA lengths.

Market Level Extension: Decide whether to extend support/resistance lines.

Filters for Trade Confirmation: Enable/disable individual filters.

Color Settings: Customize line colors for bullish and bearish trend shifts.

Maximum Displayed Lines: Limit the number of drawn support/resistance lines.

Considerations & Limitations

Trend Lag: As with any EMA-based strategy, signals may be slightly delayed compared to price action.

Sideways Markets: This strategy works best in trending conditions; frequent crossovers in sideways markets can produce false signals.

Filter Usage: Enabling multiple filters may reduce trade frequency, but can also improve trade quality.

Line Overlap: If many crossovers occur in a short period, the chart may become cluttered with multiple trend levels. Adjusting the "Display Last" setting can help.

Conclusion

The Market Trend Levels Detector Strategy is a non-repainting trend-following system that combines EMA crossovers, market level detection, and customizable filters to improve trade accuracy.

By identifying trend shifts and key price levels, this strategy can be used for:

Trend Confirmation – Using EMA crossovers and filters to confirm trend direction.

Support & Resistance Trading – Identifying dynamic levels where price reacts.

Momentum-Based Trading – Combining EMA crossovers with additional momentum filters.

This strategy is fully customizable and can be adapted to different trading styles, timeframes, and market conditions.

Full credit for the original concept and indicator goes to BigBeluga.

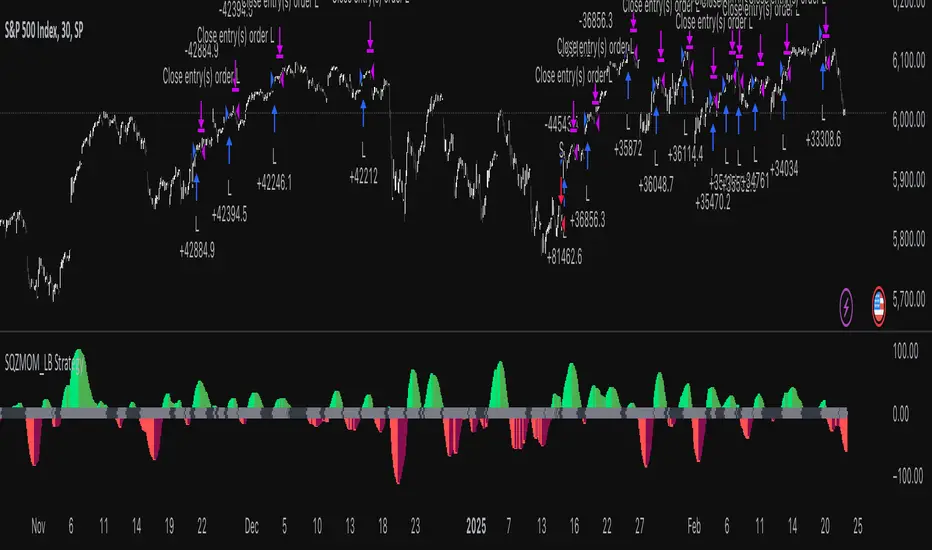

Squeeze Momentum Indicator Strategy [LazyBear + PineIndicators]The Squeeze Momentum Indicator Strategy (SQZMOM_LB Strategy) is an automated trading strategy based on the Squeeze Momentum Indicator developed by LazyBear, which itself is a modification of John Carter's "TTM Squeeze" concept from his book Mastering the Trade (Chapter 11). This strategy is designed to identify low-volatility phases in the market, which often precede explosive price movements, and to enter trades in the direction of the prevailing momentum.

Concept & Indicator Breakdown

The strategy employs a combination of Bollinger Bands (BB) and Keltner Channels (KC) to detect market squeezes:

Squeeze Condition:

When Bollinger Bands are inside the Keltner Channels (Black Crosses), volatility is low, signaling a potential upcoming price breakout.

When Bollinger Bands move outside Keltner Channels (Gray Crosses), the squeeze is released, indicating an expansion in volatility.

Momentum Calculation:

A linear regression-based momentum value is used instead of traditional momentum indicators.

The momentum histogram is color-coded to show strength and direction:

Lime/Green: Increasing bullish momentum

Red/Maroon: Increasing bearish momentum

Signal Colors:

Black: Market is in a squeeze (low volatility).

Gray: Squeeze is released, and volatility is expanding.

Blue: No squeeze condition is present.

Strategy Logic

The script uses historical volatility conditions and momentum trends to generate buy/sell signals and manage positions.

1. Entry Conditions

Long Position (Buy)

The squeeze just released (Gray Cross after Black Cross).

The momentum value is increasing and positive.

The momentum is at a local low compared to the past 100 bars.

The price is above the 100-period EMA.

The closing price is higher than the previous close.

Short Position (Sell)

The squeeze just released (Gray Cross after Black Cross).

The momentum value is decreasing and negative.

The momentum is at a local high compared to the past 100 bars.

The price is below the 100-period EMA.

The closing price is lower than the previous close.

2. Exit Conditions

Long Exit:

The momentum value starts decreasing (momentum lower than previous bar).

Short Exit:

The momentum value starts increasing (momentum higher than previous bar).

Position Sizing

Position size is dynamically adjusted based on 8% of strategy equity, divided by the current closing price, ensuring risk-adjusted trade sizes.

How to Use This Strategy

Apply on Suitable Markets:

Best for stocks, indices, and forex pairs with momentum-driven price action.

Works on multiple timeframes but is most effective on higher timeframes (1H, 4H, Daily).

Confirm Entries with Additional Indicators:

The author recommends ADX or WaveTrend to refine entries and avoid false signals.

Risk Management:

Since the strategy dynamically sizes positions, it's advised to use stop-losses or risk-based exits to avoid excessive drawdowns.

Final Thoughts

The Squeeze Momentum Indicator Strategy provides a systematic approach to trading volatility expansions, leveraging the classic TTM Squeeze principles with a unique linear regression-based momentum calculation. Originally inspired by John Carter’s method, LazyBear's version and this strategy offer a refined, adaptable tool for traders looking to capitalize on market momentum shifts.

Arpeet MACDOverview

This strategy is based on the zero-lag version of the MACD (Moving Average Convergence Divergence) indicator, which captures short-term trends by quickly responding to price changes, enabling high-frequency trading. The strategy uses two moving averages with different periods (fast and slow lines) to construct the MACD indicator and introduces a zero-lag algorithm to eliminate the delay between the indicator and the price, improving the timeliness of signals. Additionally, the crossover of the signal line and the MACD line is used as buy and sell signals, and alerts are set up to help traders seize trading opportunities in a timely manner.

Strategy Principle

Calculate the EMA (Exponential Moving Average) or SMA (Simple Moving Average) of the fast line (default 12 periods) and slow line (default 26 periods).

Use the zero-lag algorithm to double-smooth the fast and slow lines, eliminating the delay between the indicator and the price.

The MACD line is formed by the difference between the zero-lag fast line and the zero-lag slow line.

The signal line is formed by the EMA (default 9 periods) or SMA of the MACD line.

The MACD histogram is formed by the difference between the MACD line and the signal line, with blue representing positive values and red representing negative values.

When the MACD line crosses the signal line from below and the crossover point is below the zero axis, a buy signal (blue dot) is generated.

When the MACD line crosses the signal line from above and the crossover point is above the zero axis, a sell signal (red dot) is generated.

The strategy automatically places orders based on the buy and sell signals and triggers corresponding alerts.

Advantage Analysis

The zero-lag algorithm effectively eliminates the delay between the indicator and the price, improving the timeliness and accuracy of signals.

The design of dual moving averages can better capture market trends and adapt to different market environments.

The MACD histogram intuitively reflects the comparison of bullish and bearish forces, assisting in trading decisions.

The automatic order placement and alert functions make it convenient for traders to seize trading opportunities in a timely manner, improving trading efficiency.

Risk Analysis

In volatile markets, frequent crossover signals may lead to overtrading and losses.

Improper parameter settings may cause signal distortion and affect strategy performance.

The strategy relies on historical data for calculations and has poor adaptability to sudden events and black swan events.

Optimization Direction

Introduce trend confirmation indicators, such as ADX, to filter out false signals in volatile markets.

Optimize parameters to find the best combination of fast and slow line periods and signal line periods, improving strategy stability.

Combine other technical indicators or fundamental factors to construct a multi-factor model, improving risk-adjusted returns of the strategy.

Introduce stop-loss and take-profit mechanisms to control single-trade risk.

Summary

The MACD Dual Crossover Zero Lag Trading Strategy achieves high-frequency trading by quickly responding to price changes and capturing short-term trends. The zero-lag algorithm and dual moving average design improve the timeliness and accuracy of signals. The strategy has certain advantages, such as intuitive signals and convenient operation, but also faces risks such as overtrading and parameter sensitivity. In the future, the strategy can be optimized by introducing trend confirmation indicators, parameter optimization, multi-factor models, etc., to improve the robustness and profitability of the strategy.

Candle Emotion Index (CEI) StrategyThe Candle Emotion Index (CEI) Strategy is an innovative sentiment-based trading approach designed to help traders identify and capitalize on market psychology. By analyzing candlestick patterns and combining them into a unified metric, the CEI Strategy provides clear entry and exit signals while dynamically managing risk. This strategy is ideal for traders looking to leverage market sentiment to identify high-probability trading opportunities.

How It Works

The CEI Strategy is built around three core oscillators that reflect key emotional states in the market:

Indecision Oscillator . Measures market uncertainty using patterns like Doji and Spinning Tops. High values indicate hesitation, signaling potential turning points.

Fear Oscillator . Tracks bearish sentiment through patterns like Shooting Star, Hanging Man, and Bearish Engulfing. Helps identify moments of intense selling pressure.

Greed Oscillator . Detects bullish sentiment using patterns like Marubozu, Hammer, Bullish Engulfing, and Three White Soldiers. Highlights periods of strong buying interest.

These oscillators are averaged into the Candle Emotion Index (CEI):

CEI = (Indecision + Fear + Greed) / 3

This single value quantifies overall market sentiment and drives the strategy’s trading decisions.

Key Features

Sentiment-Based Trading Signals . Long Entry: Triggered when the CEI crosses above a lower threshold (e.g., 0.1), indicating increasing bullish sentiment. Short Entry: Triggered when the CEI crosses above a higher threshold (e.g., 0.2), signaling rising bearish sentiment.

Volume Confirmation . Trades are validated only if volume exceeds a user-defined multiplier of the average volume over the lookback period. This ensures entries are backed by significant market activity.

Break-Even Recovery Mechanism . If a trade moves into a loss, the strategy attempts to recover to break-even instead of immediately exiting at a loss. This feature provides flexibility, allowing the market to recover while maintaining disciplined risk management.

Dynamic Risk Management . Maximum Holding Period: Trades are closed after a user-defined number of candles to avoid overexposure to prolonged uncertainty. Profit-Taking Conditions: Positions are exited when favorable price moves are confirmed by increased volume, locking in gains. Loss Threshold: Trades are exited early if the price moves unfavorably beyond a set percentage of the entry price, limiting potential losses.

Cooldown Period . After a trade is closed, a cooldown period prevents immediate re-entry, reducing overtrading and improving signal quality.

Why Use This Strategy?

The CEI Strategy combines advanced sentiment analysis with robust trade management, making it a powerful tool for traders seeking to understand market psychology and identify high-probability setups. Its unique features, such as the break-even recovery mechanism and volume confirmation, add an extra layer of discipline and reliability to trading decisions.

Best Practices

Combine with Other Indicators . Use trend-following tools (e.g., moving averages, ADX) and momentum oscillators (e.g., RSI, MACD) to confirm signals.

Align with Key Levels . Incorporate support and resistance levels for refined entries and exits.

Multi-Market Compatibility . Apply this strategy to forex, crypto, stocks, or any asset class with strong volume and price action.

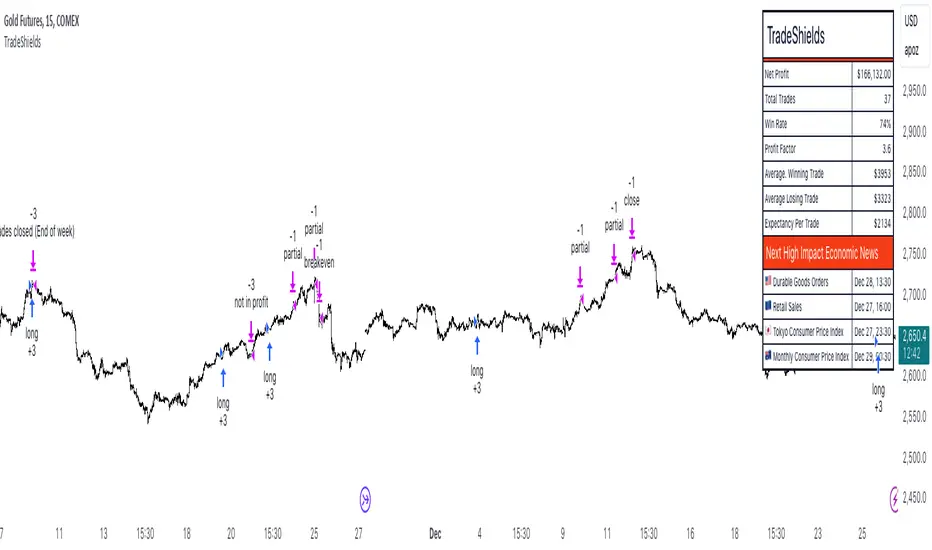

TradeShields Strategy Builder🛡 WHAT IS TRADESHIELDS?

This no-code strategy builder is designed for traders on TradingView, offering an intuitive platform to create, backtest, and automate trading strategies. While identifying signals is often straightforward, the real challenge in trading lies in managing risk and knowing when not to trade. It equips users with advanced tools to address this challenge, promoting disciplined decision-making and structured trading practices.

This is not just a collection of indicators but a comprehensive toolkit that helps identify high-quality opportunities while placing risk management at the core of every strategy. By integrating customizable filters, robust controls, and automation capabilities, it empowers traders to align their strategies with their unique objectives and risk tolerance.

_____________________________________

🛡 THE GOAL: SHIELD YOUR STRATEGY

The mission is simple: to shield your strategy from bad trades . Whether you're a seasoned trader or just starting, the hardest part of trading isn’t finding signals—it’s avoiding trades that can harm your account. This framework prioritizes quality over quantity , helping filter out suboptimal setups and encouraging disciplined execution.

With tools to manage risk, avoid overtrading, and adapt to changing market conditions, it protects your strategy against impulsive decisions and market volatility.

_____________________________________

🛡 HOW TO USE IT

1. Apply Higher Timeframe Filters

Begin by analyzing broader market trends using tools like the 200 EMA, Ichimoku Cloud, or Supertrend on higher timeframes (e.g., daily or 4-hour charts).

- Example: Ensure the price is above the 200 EMA on the daily chart for long trades or below it for short trades.

2. Identify the Appropriate Entry Signal

Choose an entry signal that aligns with your model and the asset you're trading. Options include:

Supertrend changes for trend reversals.

Bollinger Band touches for mean-reversion trades.

RSI strength/weakness for overbought or oversold conditions.

Breakouts of key levels (e.g., daily or weekly highs/lows) for momentum trades.

MACD and TSI flips.

3. Determine Take-Profit and Stop-Loss Levels

Set clear exit strategies to protect your capital and lock in profits:

Use single, dual, or triple take-profit levels based on percentages or price levels.

Choose a stop-loss type, such as fixed percentage, ATR-based, or trailing stops.

Optionally, set breakeven adjustments after hitting your first take-profit target.

4. Apply Risk Management Filters

Incorporate risk controls to ensure disciplined execution:

Limit the number of trades per day, week, or month to avoid overtrading.

Use time-based filters to trade during specific sessions or custom windows.

Avoid trading around high-impact news events with region-specific filters.

5. Automate and Execute

Leverage the advanced automation features to streamline execution. Alerts are tailored specifically for each supported platform, ensuring seamless integration with tools like PineConnector, 3Commas, Zapier, and more.

_____________________________________

🛡 CORE FOCUS: RISK MANAGEMENT, AUTOMATION, AND DISCIPLINED TRADING

This builder emphasizes quality over quantity, encouraging traders to approach markets with structure and control. Its innovative tools for risk management and automation help optimize performance while reducing effort, fostering consistency and long-term success.

_____________________________________

🛡 KEY FEATURES

General Settings

Theme Customization : Light and dark themes for a tailored interface.

Timezone Adjustment : Align session times and news schedules with your local timezone.

Position Sizing : Define lot sizes to manage risk effectively.

Directional Control : Choose between long-only, short-only, or both directions for trading.

Time Filters

Day-of-Week Selection : Enable or disable trading on specific days.

Session-Based Trading : Restrict trades to major market sessions (Asia, London, New York) or custom windows.

Custom Time Windows : Precisely control the timeframes for trade execution.

Risk Management Tools

Trade Limits : Maximum trades per day, week, or month to avoid overtrading.

Automatic Trade Closures : End-of-session, end-of-day, or end-of-week options.

Duration-Based Filters : Close trades if take-profit isn’t reached within a set timeframe or if they remain unprofitable beyond a specific duration.

Stop-Loss and Take-Profit Options : Fixed percentage or ATR-based stop-losses, single/dual/triple take-profit levels, and breakeven stop adjustments.

Economic News Filters

Region-Specific Filters : Exclude trades around major news events in regions like the USA, UK, Europe, Asia, or Oceania.

News Avoidance Windows : Pause trades before and after high-impact events or automatically close trades ahead of scheduled news releases.

Higher Timeframe Filters

Multi-Timeframe Tools : Leverage EMAs, Supertrend, or Ichimoku Cloud on higher timeframes (Daily, 4-hour, etc.) for trend alignment.

Chart Timeframe Filters

Precision Filtering : Apply EMA or ADX-based conditions to refine trade setups on current chart timeframes.

Entry Signals

Customizable Options : Choose from signals like Supertrend, Bollinger Bands, RSI, MACD, Ichimoku Cloud, or EMA pullbacks.

Indicator Parameter Overrides : Fine-tune default settings for specific signals.

Exit Settings

Flexible Take-Profit Targets : Single, dual, or triple targets. Exit at significant levels like daily/weekly highs or lows.

Stop-Loss Variability : Fixed, ATR-based, or trailing stop-loss options.

Alerts and Automation

Third-Party Integrations : Seamlessly connect with platforms like PineConnector, 3Commas, Zapier, and Capitalise.ai.

Precision-Formatted Alerts : Alerts are tailored specifically for each platform, ensuring seamless execution. For example:

- PineConnector alerts include risk-per-trade parameters.

- 3Commas alerts contain bot-specific configurations.

_____________________________________

🛡 PUBLISHED CHART SETTINGS: 15m COMEX:GC1!

Time Filters : Trades are enabled from Tuesday to Friday, as Mondays often lack sufficient data coming off the weekend, and weekends are excluded due to market closures. Custom time sessions are turned off by default, allowing trades throughout the day.

Risk Filters : Risk is tightly controlled by limiting trades to a maximum of 2 per day and enabling a mechanism to close trades if they remain open too long and are unprofitable. Weekly trade closures ensure that no positions are carried over unnecessarily.

Economic News Filters : By default, trades are allowed during economic news periods, giving traders flexibility to decide how to handle volatility manually. It is recommended to enable these filters if you are creating strategies on lower timeframes.

Higher Timeframe Filters : The setup incorporates confluence from higher timeframe indicators. For example, the 200 EMA on the daily timeframe is used to establish trend direction, while the Ichimoku cloud on the 30-minute timeframe adds additional confirmation.

Entry Signals : The strategy triggers trades based on changes in the Supertrend indicator.

Exit Settings : Trades are configured to take partial profits at three levels (1%, 2%, and 3%) and use a fixed stop loss of 2%. Stops are moved to breakeven after reaching the first take profit level.

_____________________________________

🛡 WHY CHOOSE THIS STRATEGY BUILDER?

This tool transforms trading from reactive to proactive, focusing on risk management and automation as the foundation of every strategy. By helping users avoid unnecessary trades, implement robust controls, and automate execution, it fosters disciplined trading.

Bollinger Breakout Strategy with Direction Control [4H crypto]Bollinger Breakout Strategy with Direction Control - User Guide

This strategy leverages Bollinger Bands, RSI, and directional filters to identify potential breakout trading opportunities. It is designed for traders looking to capitalize on significant price movements while maintaining control over trade direction (long, short, or both). Here’s how to use this strategy effectively:

How the Strategy Works

Indicators Used:

Bollinger Bands:

A volatility-based indicator with an upper and lower band around a simple moving average (SMA). The bands expand or contract based on market volatility.

RSI (Relative Strength Index):

Measures momentum to determine overbought or oversold conditions. In this strategy, RSI is used to confirm breakout strength.

Trade Direction Control:

You can select whether to trade:

Long only: Buy positions.

Short only: Sell positions.

Both: Trade in both directions depending on conditions.

Breakout Conditions:

Long Trade:

The price closes above the upper Bollinger Band.

RSI is above the midline (50), confirming upward momentum.

The "Trade Direction" setting allows either "Long" or "Both."

Short Trade:

The price closes below the lower Bollinger Band.

RSI is below the midline (50), confirming downward momentum.

The "Trade Direction" setting allows either "Short" or "Both."

Risk Management:

Stop-Loss:

Long trades: Set at 2% below the entry price.

Short trades: Set at 2% above the entry price.

Take-Profit:

Calculated using a Risk/Reward Ratio (default is 2:1).

Adjust this in the strategy settings.

Inputs and Customization

Key Parameters:

Bollinger Bands Length: Default is 20. Adjust based on the desired sensitivity.

Multiplier: Default is 2.0. Higher values widen the bands; lower values narrow them.

RSI Length: Default is 14, which is standard for RSI.

Risk/Reward Ratio: Default is 2.0. Increase for more aggressive profit targets, decrease for conservative exits.

Trade Direction:

Options: "Long," "Short," or "Both."

Example: Set to "Long" in a bullish market to focus only on buy trades.

How to Use This Strategy

Adding the Strategy:

Paste the script into TradingView’s Pine Editor and add it to your chart.

Setting Parameters:

Adjust the Bollinger Band settings, RSI, and Risk/Reward Ratio to fit the asset and timeframe you're trading.

Analyzing Signals:

Green line (Upper Band): Signals breakout potential for long trades.

Red line (Lower Band): Signals breakout potential for short trades.

Blue line (Basis): Central Bollinger Band (SMA), helpful for understanding price trends.

Testing the Strategy:

Use the Strategy Tester in TradingView to backtest performance on your chosen asset and timeframe.

Optimizing for Assets:

Forex pairs, cryptocurrencies (like BTC), or stocks with high volatility are ideal for this strategy.

Works best on higher timeframes like 4H or Daily.

Best Practices

Combine with Volume: Confirm breakouts with increased volume for higher reliability.

Avoid Sideways Markets: Use additional trend filters (like ADX) to avoid trades in low-volatility conditions.

Optimize Parameters: Regularly adjust the Bollinger Bands multiplier and RSI settings to match the asset's behavior.

By utilizing this strategy, you can effectively trade breakouts while maintaining flexibility in trade direction. Adjust the parameters to match your trading style and market conditions for optimal results!

FlowHello, everyone,

Recently I found a useful indicator for the short-term minute-level trading called Liquidity Sweeps. This is a technical indicator that studies the resistance and support levels of candle patterns.

The strategy takes into account the following market factors:

Lql -> resistance formed by a rapid rise or support formed by a rapid rise

Sweep Area -> potential entry point

The inspiration of this strategy comes mostly from Liquidity Sweeps (LuxAlgo), but I have also optimized it based on my own trading experience.

What are the differences from the original strategy?

The Only Outbreaks & Retest option has been removed, and the formation of Wicks is enough to prevent conflicting signals.

The P&L ratio of the strategy has been set, which allows more combinations of the appropriate strategy parameters to match different characteristics of trading pairs.

Signals

1. Enter the trade when three consecutive bars are formed in the Wicks block (resistance or support) and set the stop-loss/stop-profit

2. The condition is not met when three bars are formed in the Wicks block, and the Wicks index is reset when the price returns.

Risk Management

1. Use the P&L ratio, plus appropriate ATR volatility to prevent false breakouts.

2. When the signal is reversed.

3. The strategy is suitable for the short-term level, not for the trend market.

Now, for the inexperienced reader, a series of knowledge. ATR: Like Boolean channel and ADX, Average True Rage is an indicator used to measure price volatility. But unlike these two indicators, it can reflect the price volatility more accurately because of the factors such as gaps added in its calculation process. For this reason, it is called "true" volatility.

Sincerely,

Special thanks to @LuxAlgo for sharing.

SOFEX High-End Indicators + BacktestingBINANCE:BTCUSDT.P BINANCE:ETHUSDT.P

Introducing the first publicly available suite of indicators for Bitcoin and Ethereum by Sofex - the High-End Indicators & Backtesting System.

🔬 Trading Philosophy

The High-End Indicators & Backtesting system offers both trend-following and mean-reversal algorithms to provide traders with a deep insight into the highly volatile cryptocurrency markets, known for their market noise and vulnerability to manipulation.

With these factors in mind, our indicators are designed to sidestep most potentially false signals. This is facilitated further by the "middle-ground" time frame (1 Hour) we use. Our focus is on the two largest cryptocurrencies: Bitcoin and Ethereum , which provide high liquidity, necessary for reliable trading.

Therefore, we recommend using our suite on these markets.

The backtesting version of the Sofex High-End Indicators includes mainly trend-following indicators. This is because our trading vision is that volatility in cryptocurrency markets is a tool that should be used carefully, and many times avoided. Furthermore, mean-reversal trading can lead to short-term profits, but we have found it less than ideal for long-term trading.

The script does not aim to make a lot of trades, or to always remain in a position and switch from long to short. Many times there is no direction and the market is in "random walk mode", and chasing trades is futile.

Based on our experience, it is preferable if traders remain neutral the majority of the time and only enter trades that can be exited in the foreseeable future. Trading just for the sake of it ultimately leads to loss in the long-run.

Expectations of performance should be realistic.

We also focus on a balanced take-profit to stop-loss ratio. In the default set-up of the script, that is a 2% : 2% (1:1) ratio. A relatively low stop loss and take profit build onto our idea that positions should be exited promptly. There are many options to edit these values, including enabling trailing take profit and stop loss. Traders can also completely turn off TP and SL levels, and rely on opposing signals to exit and enter new trades.

Extreme scenarios can happen on the cryptocurrency markets, and disabling stop-loss levels completely is not recommended. The position size should be monitored since all of it is at risk with no stop-loss.

We take pride in presenting this comprehensive suite of trading indicators, designed for both manual and automated use. Although automated use leads to increased efficiency, traders are free to incorporate any of our indicators into their own manual trading strategy.

⚙️ Indicators

By default, all indicators are enabled for both Long and Short trades.

Extreme Trend Breakouts

The Extreme Trend Breakouts indicator seeks to follow breakouts of support and resistance levels, while also accounting for the unfortunate fact that false signals can be generated on these levels. The indicator combines trend-breakout strategies with various other volatility and direction measurements. It works best in the beginning of trends.

Underpinning this indicator are renowned Perry Kaufman's Adaptive Moving Averages (PKAMA) alongside our proprietary adaptive moving averages. These dynamic indicators adjust their parameters based on recent price movements, attempting to catch trends while maintaining consistent performance in the long run.

In addition, our modification of the TTM Squeeze indicator further enhances the Extreme Trend Breakouts indicator, making it more responsive, especially during the initial stages of trends and filtering of "flat" markets.

High-Volatility Trend Follower

The High-Volatility Trend Follower indicator is based around the logic of evading market conditions where volatility is low (choppy markets) and aggressively following confirmed trends. The indicator works best during strong trends, however, it has the downside of entering trades at trend tops or bottoms.

This indicator also leverages our proprietary adaptive moving averages to identify and follow high-volatility trends effectively. Furthermore, it uses the Average Directional Index, Aroon Oscillator, ATR and a modified version of VWAP, to categorize trends into weak or strong ones. The VWAP indicator is used to identify the monetary (volume) inflow into a given trend, further helping to avoid short-term manipulations.

Low-Volatility Reversal

The Low-Volatility Reversal aims at plugging the holes that trend-following indicators ignore. It specifically looks for choppy markets. Using proven concepts such as Relative Strength Index and volume measurements, among others, this indicator finds local tops and bottoms with good accuracy. It works best in choppy markets with low to medium volatility. It has a downside that all reversals have, losing trades at the end of choppy markets and in the beginning of big trends.

This indicator, like the others, employs PKAMA in conjunction with our proprietary adaptive moving averages, and an Average PSAR indicator to seek out "sideways" markets. Furthermore, Bollinger Bands with an adaptive basis line is used, with the idea of trading against the short-term trends by looking at big deviations in price movement. The above mentioned indicators attempt to catch local tops and bottoms in markets.

Adaptive Trend Convergence

The Adaptive Trend Convergence aims at following trends while avoiding entering positions at local bottoms and tops. It does so by comparing a number of adaptive moving averages and looking for convergence among them. Adaptive filtering techniques for avoiding choppy markets are also used.

This indicator utilizes our proprietary adaptive moving averages, and an Average Price Range indicator to identify trend convergence and divergence effectively, preventing false signals during volatile market phases. It also makes use of Bollinger Bands with an adaptive moving average basis line and price-action adjusted deviation. Contrasting to the Low-Volatility Reversal condition described above, the Bollinger Bands used here attempt to follow breakouts outside of the lower and upper bands.

Double-Filtered Channel Breakouts

The Double-Filtered Channel Breakouts indicator is made out of adaptive channel-identifying indicators. The indicator then follows trends that significantly diverge from the established channels. This aims at following extreme trends, where rapid, continuous movements in either direction occur. This indicator works best in very strong trends and follows them relentlessly. However, these strong trends can end in strong reversals, and the indicator can be stopped out on the last trade.

Our Double-Filtered Channel Breakouts indicator is built on a foundation of adaptive channel indicators. We've harnessed the power of Keltner Channels and Bollinger Band Channels, with a similar approach used in the Adaptive Trend Convergence indicator. The basis and upper/lower bands of the channels do not rely on fixed deviation parameters, rather on adaptive ones, based on price action and volatility. This combination seeks to identify and follows extreme trends.

Direction Tracker

The Direction Tracker indicator is made out of a central slower, adaptive moving average that clearly recognizes global, long-term trends. Combined with direction and range indicators, among others, this indicator excels at finding the long-term trend and ignoring temporary pullbacks in the opposite direction. It works best at the beginning and middle of long and strong trends. It can fail at the end of trends and on very strong historical resistance lines (where sharp reversals are common).

Our Direction Tracker indicator integrates an adaptive SuperTrend indicator into its core, alongside our proprietary adaptive moving averages, to accurately identify and track long-term trends while mitigating temporary pullbacks. Furthermore, it uses Average True Range, ADX and other volatility indicators to attempt to catch unusual moves on the market early-on.

📟 Parameters Menu

To offer traders flexibility, our system comes with a comprehensive parameter menu:

Preset Selection : Choose between Bitcoin or Ethereum presets to tailor the indicators to your preferred cryptocurrency market.

Global Signal Direction: Set the global signal direction as Long, Short, or Both, depending on your trading strategy.

Global Sensitivity Parameter : Adjust the system's sensitivity to adapt to different trend-following conditions, particularly beneficial during higher-strength trends.

Source of Signals : Toggle individual indicators on or off according to your preference. By default, all indicators are enabled. Customize the indicators to trade Long, Short, or Both, aligning them with your desired market exposure.

Confirmation of Signals : Set the minimum number of confirmed signals on the same bar, ensuring signals are generated only when specific confirmation criteria are met. The default value is one, and it can be adjusted for both Long and Short signals.

Exit of Signals : You have options regarding Take-Profit (TP) and Stop-Loss (SL) levels. Enable TP/SL levels to exit trades at predetermined levels, or disable them to rely on direction changes for exits. Be aware that removing stop losses can introduce additional risk, and position sizing should be carefully monitored.

By enabling Trailing TP/SL, the system switches to a trailing approach, allowing you to:

- Place an initial customizable SL.

- Specify a level (%) for the Trailing SL to become active.

- When the activation level is reached, the system moves the trailing stop by a given Offset (%).

Additionally, you can enable exit at break-even, where the system places an exit order when the trail activation level is reached, accounting for fees and slippage.

Alert Messages : Define the fields for alert messages based on specific conditions. You can set up alerts to receive email, SMS, and in-app notifications. If you use webhooks for alerts, exercise caution, as these alerts can potentially execute trades without human supervision.

Backtesting : Default backtesting parameters are set to provide realistic backtesting performance:

- 0.04% Commission per trade (for both entries and exits)

- 3 ticks Slippage (highly dependent on exchange)

- Initial capital of $1000

- Order size of $1000

While the order size is equal to the initial capital, the script employs a 2% stop-loss order to limit losses and attempts to prevent risky trades from creating big losses. The order size is a set dollar value, so that the backtesting performance is linear, instead of using % of capital which may result in unrealistic backtesting performance.

Risk Disclaimer

Please be aware that backtesting results, while valuable for statistical overview, do not guarantee future performance in any way. Cryptocurrency markets are inherently volatile and risky. Always trade responsibly and do not risk more than you can afford to lose.

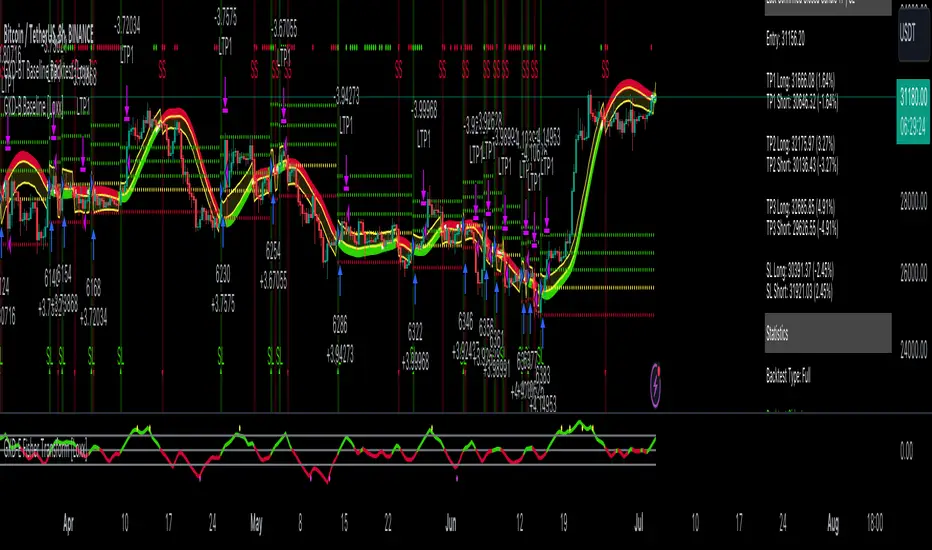

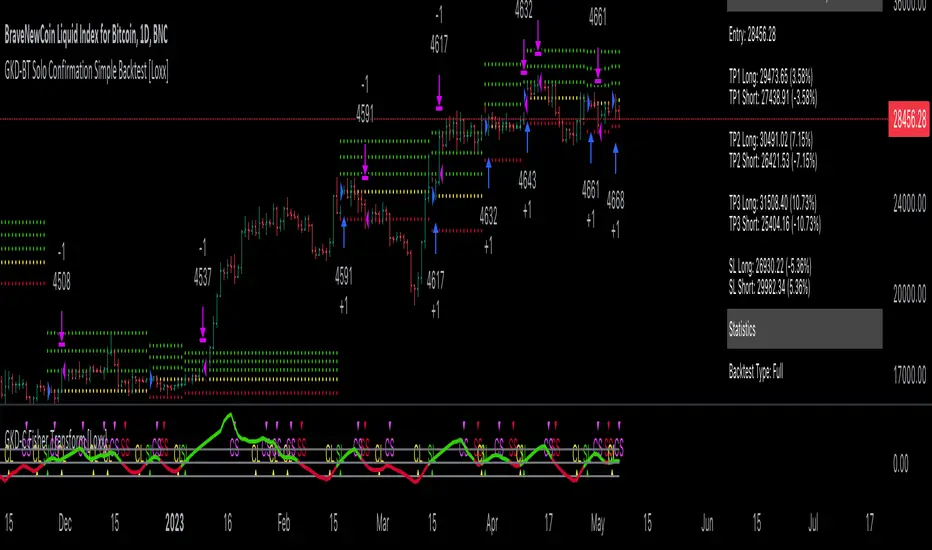

GKD-BT Baseline Backtest [Loxx]The Giga Kaleidoscope GKD-BT Baseline Backtest is a backtesting module included in Loxx's "Giga Kaleidoscope Modularized Trading System."

█ GKD-BT Baseline Backtest

The GKD-BT Baseline Backtest allows traders to backtest the Regular and Stepped baselines used in the GKD trading system. This module includes 65+ moving averages and 15+ types of volatility to choose from.

Additionally, this backtest module provides the option to test the GKD-B indicator with 1 to 3 take profits and 1 stop loss. The Trading backtest allows for the use of 1 to 3 take profits, while the Full backtest is limited to 1 take profit. The Trading backtest also offers the capability to apply a trailing take profit.

In terms of the percentage of trade removed at each take profit, this backtest module has the following hardcoded values:

Take profit 1: 50% of the trade is removed

Take profit 2: 25% of the trade is removed

Take profit 3: 25% of the trade is removed

Stop loss: 100% of the trade is removed

After each take profit is achieved, the stop loss level is adjusted. When take profit 1 is reached, the stop loss is moved to the entry point. Similarly, when take profit 2 is reached, the stop loss is shifted to take profit 1. The trailing take profit feature comes into play after take profit 2 or take profit 3, depending on the number of take profits selected in the settings. The trailing take profit is always activated on the final take profit when 2 or more take profits are chosen.

The backtest also offers the capability to restrict by a specific date range, allowing for simulated forward testing based on past data. Additionally, users have the option to display or hide a trading panel that provides relevant information about the backtest, statistics, and the current trade. It is also possible to activate alerts and toggle sections of the trading panel on or off. On the chart, historical take profit and stop loss levels are represented by horizontal lines overlaid for reference.

This backtest also includes an optional GKD-E Exit indicator that can be used to test early exits.

The GKD system utilizes volatility-based take profits and stop losses. Each take profit and stop loss is calculated as a multiple of volatility. You can change the values of the multipliers in the settings as well.

To utilize this strategy, follow these steps:

1. (Required) Import the value "Input into NEW GKD-BT Backtest" from the GKD-B Baseline indicator into the GKD-BT Baseline Backtest field "Import GKD-B Baseline"

2. (Optional) Import the value "Input into NEW GKD-BT Backtest" from the GKD-E Exit indicator into the GKD-BT Baseline Backtest field "Import GKD-E Exit". You can toggle the Exit on or off using the "Activate GKD-E Exit" option.

Baselines that are compatible with this backtest module:

GKD-B Baseline

GKD-B Stepped Baseline

Volatility Types Included

17 types of volatility are included in this indicator

Close-to-Close

Parkinson

Garman-Klass

Rogers-Satchell

Yang-Zhang

Garman-Klass-Yang-Zhang

Exponential Weighted Moving Average

Standard Deviation of Log Returns

Pseudo GARCH(2,2)

Average True Range

True Range Double

Standard Deviation

Adaptive Deviation

Median Absolute Deviation

Efficiency-Ratio Adaptive ATR

Mean Absolute Deviation

Static Percent

█ Giga Kaleidoscope Modularized Trading System

Core components of an NNFX algorithmic trading strategy

The NNFX algorithm is built on the principles of trend, momentum, and volatility. There are six core components in the NNFX trading algorithm:

1. Volatility - price volatility; e.g., Average True Range, True Range Double, Close-to-Close, etc.

2. Baseline - a moving average to identify price trend

3. Confirmation 1 - a technical indicator used to identify trends

4. Confirmation 2 - a technical indicator used to identify trends

5. Continuation - a technical indicator used to identify trends

6. Volatility/Volume - a technical indicator used to identify volatility/volume breakouts/breakdown

7. Exit - a technical indicator used to determine when a trend is exhausted

8. Metamorphosis - a technical indicator that produces a compound signal from the combination of other GKD indicators*

*(not part of the NNFX algorithm)

What is Volatility in the NNFX trading system?

In the NNFX (No Nonsense Forex) trading system, ATR (Average True Range) is typically used to measure the volatility of an asset. It is used as a part of the system to help determine the appropriate stop loss and take profit levels for a trade. ATR is calculated by taking the average of the true range values over a specified period.

True range is calculated as the maximum of the following values:

-Current high minus the current low

-Absolute value of the current high minus the previous close

-Absolute value of the current low minus the previous close

ATR is a dynamic indicator that changes with changes in volatility. As volatility increases, the value of ATR increases, and as volatility decreases, the value of ATR decreases. By using ATR in NNFX system, traders can adjust their stop loss and take profit levels according to the volatility of the asset being traded. This helps to ensure that the trade is given enough room to move, while also minimizing potential losses.

Other types of volatility include True Range Double (TRD), Close-to-Close, and Garman-Klass

What is a Baseline indicator?

The baseline is essentially a moving average, and is used to determine the overall direction of the market.

The baseline in the NNFX system is used to filter out trades that are not in line with the long-term trend of the market. The baseline is plotted on the chart along with other indicators, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR).

Trades are only taken when the price is in the same direction as the baseline. For example, if the baseline is sloping upwards, only long trades are taken, and if the baseline is sloping downwards, only short trades are taken. This approach helps to ensure that trades are in line with the overall trend of the market, and reduces the risk of entering trades that are likely to fail.

By using a baseline in the NNFX system, traders can have a clear reference point for determining the overall trend of the market, and can make more informed trading decisions. The baseline helps to filter out noise and false signals, and ensures that trades are taken in the direction of the long-term trend.

What is a Confirmation indicator?

Confirmation indicators are technical indicators that are used to confirm the signals generated by primary indicators. Primary indicators are the core indicators used in the NNFX system, such as the Average True Range (ATR), the Moving Average (MA), and the Relative Strength Index (RSI).

The purpose of the confirmation indicators is to reduce false signals and improve the accuracy of the trading system. They are designed to confirm the signals generated by the primary indicators by providing additional information about the strength and direction of the trend.

Some examples of confirmation indicators that may be used in the NNFX system include the Bollinger Bands, the MACD (Moving Average Convergence Divergence), and the MACD Oscillator. These indicators can provide information about the volatility, momentum, and trend strength of the market, and can be used to confirm the signals generated by the primary indicators.

In the NNFX system, confirmation indicators are used in combination with primary indicators and other filters to create a trading system that is robust and reliable. By using multiple indicators to confirm trading signals, the system aims to reduce the risk of false signals and improve the overall profitability of the trades.

What is a Continuation indicator?

In the NNFX (No Nonsense Forex) trading system, a continuation indicator is a technical indicator that is used to confirm a current trend and predict that the trend is likely to continue in the same direction. A continuation indicator is typically used in conjunction with other indicators in the system, such as a baseline indicator, to provide a comprehensive trading strategy.

What is a Volatility/Volume indicator?

Volume indicators, such as the On Balance Volume (OBV), the Chaikin Money Flow (CMF), or the Volume Price Trend (VPT), are used to measure the amount of buying and selling activity in a market. They are based on the trading volume of the market, and can provide information about the strength of the trend. In the NNFX system, volume indicators are used to confirm trading signals generated by the Moving Average and the Relative Strength Index. Volatility indicators include Average Direction Index, Waddah Attar, and Volatility Ratio. In the NNFX trading system, volatility is a proxy for volume and vice versa.

By using volume indicators as confirmation tools, the NNFX trading system aims to reduce the risk of false signals and improve the overall profitability of trades. These indicators can provide additional information about the market that is not captured by the primary indicators, and can help traders to make more informed trading decisions. In addition, volume indicators can be used to identify potential changes in market trends and to confirm the strength of price movements.

What is an Exit indicator?

The exit indicator is used in conjunction with other indicators in the system, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR), to provide a comprehensive trading strategy.

The exit indicator in the NNFX system can be any technical indicator that is deemed effective at identifying optimal exit points. Examples of exit indicators that are commonly used include the Parabolic SAR, the Average Directional Index (ADX), and the Chandelier Exit.

The purpose of the exit indicator is to identify when a trend is likely to reverse or when the market conditions have changed, signaling the need to exit a trade. By using an exit indicator, traders can manage their risk and prevent significant losses.

In the NNFX system, the exit indicator is used in conjunction with a stop loss and a take profit order to maximize profits and minimize losses. The stop loss order is used to limit the amount of loss that can be incurred if the trade goes against the trader, while the take profit order is used to lock in profits when the trade is moving in the trader's favor.

Overall, the use of an exit indicator in the NNFX trading system is an important component of a comprehensive trading strategy. It allows traders to manage their risk effectively and improve the profitability of their trades by exiting at the right time.

What is an Metamorphosis indicator?

The concept of a metamorphosis indicator involves the integration of two or more GKD indicators to generate a compound signal. This is achieved by evaluating the accuracy of each indicator and selecting the signal from the indicator with the highest accuracy. As an illustration, let's consider a scenario where we calculate the accuracy of 10 indicators and choose the signal from the indicator that demonstrates the highest accuracy.

The resulting output from the metamorphosis indicator can then be utilized in a GKD-BT backtest by occupying a slot that aligns with the purpose of the metamorphosis indicator. The slot can be a GKD-B, GKD-C, or GKD-E slot, depending on the specific requirements and objectives of the indicator. This allows for seamless integration and utilization of the compound signal within the GKD-BT framework.

How does Loxx's GKD (Giga Kaleidoscope Modularized Trading System) implement the NNFX algorithm outlined above?

Loxx's GKD v2.0 system has five types of modules (indicators/strategies). These modules are:

1. GKD-BT - Backtesting module (Volatility, Number 1 in the NNFX algorithm)

2. GKD-B - Baseline module (Baseline and Volatility/Volume, Numbers 1 and 2 in the NNFX algorithm)

3. GKD-C - Confirmation 1/2 and Continuation module (Confirmation 1/2 and Continuation, Numbers 3, 4, and 5 in the NNFX algorithm)

4. GKD-V - Volatility/Volume module (Confirmation 1/2, Number 6 in the NNFX algorithm)

5. GKD-E - Exit module (Exit, Number 7 in the NNFX algorithm)

6. GKD-M - Metamorphosis module (Metamorphosis, Number 8 in the NNFX algorithm, but not part of the NNFX algorithm)

(additional module types will added in future releases)

Each module interacts with every module by passing data to A backtest module wherein the various components of the GKD system are combined to create a trading signal.

That is, the Baseline indicator passes its data to Volatility/Volume. The Volatility/Volume indicator passes its values to the Confirmation 1 indicator. The Confirmation 1 indicator passes its values to the Confirmation 2 indicator. The Confirmation 2 indicator passes its values to the Continuation indicator. The Continuation indicator passes its values to the Exit indicator, and finally, the Exit indicator passes its values to the Backtest strategy.

This chaining of indicators requires that each module conform to Loxx's GKD protocol, therefore allowing for the testing of every possible combination of technical indicators that make up the six components of the NNFX algorithm.

What does the application of the GKD trading system look like?

Example trading system:

Backtest: GKD-BT Baseline Backtest as shown on the chart above

Baseline: Hull Moving Average as shown on the chart above

Volatility/Volume: Hurst Exponent

Confirmation 1: Sherif's HiLo

Confirmation 2: uf2018

Continuation: Coppock Curve

Exit: Fisher Transform as shown on the chart above

Metamorphosis: Baseline Optimizer

Each GKD indicator is denoted with a module identifier of either: GKD-BT, GKD-B, GKD-C, GKD-V, GKD-M, or GKD-E. This allows traders to understand to which module each indicator belongs and where each indicator fits into the GKD system.

█ Giga Kaleidoscope Modularized Trading System Signals

Standard Entry

1. GKD-C Confirmation gives signal

2. Baseline agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Volatility/Volume agrees

1-Candle Standard Entry

1a. GKD-C Confirmation gives signal

2a. Baseline agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

Next Candle

1b. Price retraced

2b. Baseline agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Baseline Entry

1. GKD-B Baseline gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Volatility/Volume agrees

7. Confirmation 1 signal was less than 'Maximum Allowable PSBC Bars Back' prior

1-Candle Baseline Entry

1a. GKD-B Baseline gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSBC Bars Back' prior

Next Candle

1b. Price retraced

2b. Baseline agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Volatility/Volume Entry

1. GKD-V Volatility/Volume gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Baseline agrees

7. Confirmation 1 signal was less than 7 candles prior

1-Candle Volatility/Volume Entry

1a. GKD-V Volatility/Volume gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSVVC Bars Back' prior

Next Candle

1b. Price retraced

2b. Volatility/Volume agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Baseline agrees

Confirmation 2 Entry

1. GKD-C Confirmation 2 gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Volatility/Volume agrees

6. Baseline agrees

7. Confirmation 1 signal was less than 7 candles prior

1-Candle Confirmation 2 Entry

1a. GKD-C Confirmation 2 gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSC2C Bars Back' prior

Next Candle

1b. Price retraced

2b. Confirmation 2 agrees

3b. Confirmation 1 agrees

4b. Volatility/Volume agrees

5b. Baseline agrees

PullBack Entry

1a. GKD-B Baseline gives signal

2a. Confirmation 1 agrees

3a. Price is beyond 1.0x Volatility of Baseline

Next Candle

1b. Price inside Goldie Locks Zone Minimum

2b. Price inside Goldie Locks Zone Maximum

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Continuation Entry

1. Standard Entry, 1-Candle Standard Entry, Baseline Entry, 1-Candle Baseline Entry, Volatility/Volume Entry, 1-Candle Volatility/Volume Entry, Confirmation 2 Entry, 1-Candle Confirmation 2 Entry, or Pullback entry triggered previously

2. Baseline hasn't crossed since entry signal trigger

4. Confirmation 1 agrees

5. Baseline agrees

6. Confirmation 2 agrees

GKD-BT Giga Confirmation Stack Backtest [Loxx]Giga Kaleidoscope GKD-BT Giga Confirmation Stack Backtest is a Backtesting module included in Loxx's "Giga Kaleidoscope Modularized Trading System".

█ GKD-BT Giga Confirmation Stack Backtest

The Giga Confirmation Stack Backtest module allows users to perform backtesting on Long and Short signals from the confluence between GKD-C Confirmation 1 and GKD-C Confirmation 2 indicators. This module encompasses two types of backtests: Trading and Full. The Trading backtest permits users to evaluate individual trades, whether Long or Short, one at a time. Conversely, the Full backtest allows users to analyze either Longs or Shorts separately by toggling between them in the settings, enabling the examination of results for each signal type. The Trading backtest emulates actual trading conditions, while the Full backtest assesses all signals, regardless of being Long or Short.

Additionally, this backtest module provides the option to test using indicators with 1 to 3 take profits and 1 stop loss. The Trading backtest allows for the use of 1 to 3 take profits, while the Full backtest is limited to 1 take profit. The Trading backtest also offers the capability to apply a trailing take profit.

In terms of the percentage of trade removed at each take profit, this backtest module has the following hardcoded values:

Take profit 1: 50% of the trade is removed.

Take profit 2: 25% of the trade is removed.

Take profit 3: 25% of the trade is removed.

Stop loss: 100% of the trade is removed.

After each take profit is achieved, the stop loss level is adjusted. When take profit 1 is reached, the stop loss is moved to the entry point. Similarly, when take profit 2 is reached, the stop loss is shifted to take profit 1. The trailing take profit feature comes into play after take profit 2 or take profit 3, depending on the number of take profits selected in the settings. The trailing take profit is always activated on the final take profit when 2 or more take profits are chosen.

The backtest module also offers the capability to restrict by a specific date range, allowing for simulated forward testing based on past data. Additionally, users have the option to display or hide a trading panel that provides relevant information about the backtest, statistics, and the current trade. It is also possible to activate alerts and toggle sections of the trading panel on or off. On the chart, historical take profit and stop loss levels are represented by horizontal lines overlaid for reference.

To utilize this strategy, follow these steps:

1. Adjust the "Confirmation Type" in the GKD-C Confirmation 1 Indicator to "GKD New."