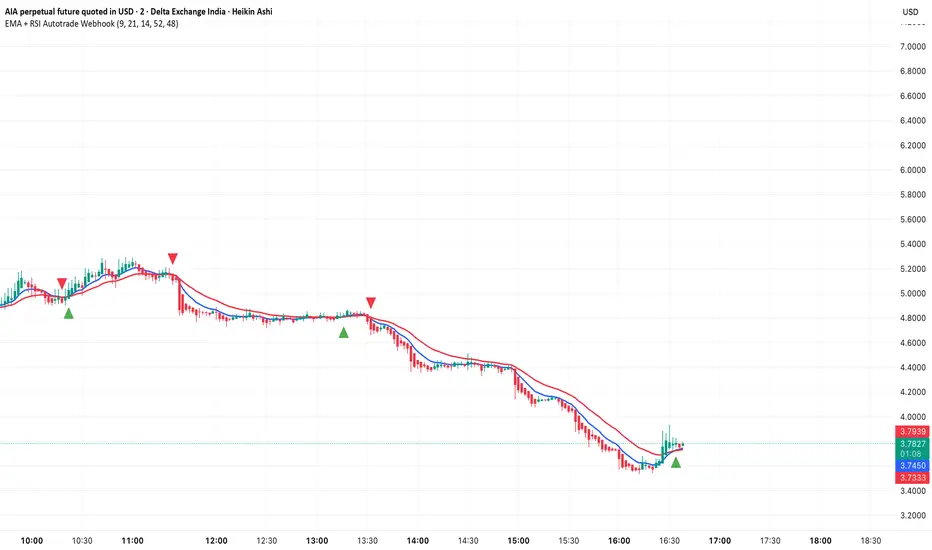

EMA + RSI Autotrade Webhook - VarunOverview

The EMA + RSI Autotrade Webhook is a powerful trend-following indicator designed for automated crypto futures trading. This indicator combines the reliability of Exponential Moving Average (EMA) crossovers with RSI momentum filtering to generate high-probability buy and sell signals optimized for webhook integration with crypto exchanges like Delta Exchange, Binance Futures, and Bybit.Key Features

Simple & Effective: Uses proven EMA 9/21 crossover strategy

RSI Momentum Filter: Eliminates low-probability trades in ranging markets

Webhook Ready: Two clean alerts (LONG Entry, SHORT Entry) for seamless automation

Exchange Compatible: Works with Delta Exchange, 3Commas, Alertatron, and other webhook platforms

Zero Lag Signals: Real-time alerts on crossover confirmation

Visual Clarity: Clean chart markers for easy signal identification

How It Works

Entry Signals:

LONG Entry: Triggers when EMA 9 crosses above EMA 21 AND RSI is above 52 (bullish momentum confirmed)

SHORT Entry: Triggers when EMA 9 crosses under EMA 21 AND RSI is below 48 (bearish momentum confirmed)

Technical Components:

Fast EMA: 9-period (tracks short-term price action)

Slow EMA: 21-period (identifies primary trend)

RSI: 14-period (confirms momentum strength)

RSI Long Threshold: 52 (filters weak bullish signals)

RSI Short Threshold: 48 (filters weak bearish signals)

Best Use Cases

Crypto Futures Trading: Bitcoin, Ethereum, Altcoin perpetual contracts

Automated Trading Bots: Integration with Delta Exchange webhooks, TradingView alerts

Timeframes: Optimized for 15-minute charts (works on 5min-1H)

Markets: Trending crypto markets with clear directional moves

Risk Management: Best used with 1-2% stop loss per trade (managed externally)

Webhook Automation Setup

Add indicator to your TradingView chart

Create alerts for "LONG Entry" and "SHORT Entry"

Configure webhook URL from your exchange (Delta Exchange, Binance, etc.)

Use alert message: Entry LONG {{ticker}} @ {{close}} or Entry SHORT {{ticker}} @ {{close}}

Exchange automatically reverses positions on opposite signals

Advantages

✅ No manual trading required - fully automated

✅ Eliminates emotional trading decisions

✅ Catches trending moves early with EMA crossovers

✅ RSI filter reduces whipsaws in choppy markets

✅ Works 24/7 without monitoring

✅ Simple two-alert system (easy to manage)

✅ Compatible with multiple exchanges via webhooksStrategy Philosophy

This indicator follows a trend-following with momentum confirmation approach. By waiting for both EMA crossover AND RSI confirmation, it ensures you're entering trades with genuine momentum behind them, not just random price noise. The tight RSI thresholds (52/48) keep you aligned with the prevailing trend.Recommended Settings

Timeframe: 15-minute (primary), 5-minute (scalping), 1-hour (swing)

Markets: BTC/USDT, ETH/USDT, high-liquidity altcoin perpetuals

Position Sizing: 100% capital per signal (exchange manages reversals)

Stop Loss: 2% (managed via exchange or external bot)

Leverage: 1-2x for conservative approach, up to 5x for aggressive

Important Notes

⚠️ This indicator generates entry signals only - position reversals are handled automatically by your exchange

⚠️ Always backtest on historical data before live trading

⚠️ Use proper risk management and position sizing

⚠️ Best performance in trending markets; may generate false signals in tight ranges

⚠️ Requires TradingView Premium or higher for webhook functionalityTags

cryptocurrency futures automated-trading ema-crossover rsi webhook delta-exchange tradingview-alerts trend-following momentum bitcoin ethereum crypto-bot algo-trading 15-minute-strategy

Pine Script®指标