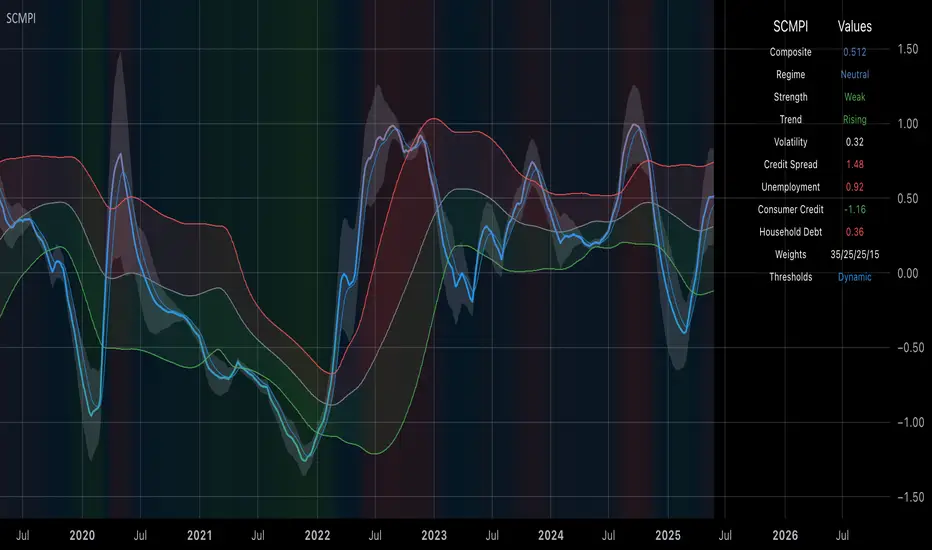

Systemic Credit Market Pressure IndexSystemic Credit Market Pressure Index (SCMPI): A Composite Indicator for Credit Cycle Analysis

The Systemic Credit Market Pressure Index (SCMPI) represents a novel composite indicator designed to quantify systemic stress within credit markets through the integration of multiple macroeconomic variables. This indicator employs advanced statistical normalization techniques, adaptive threshold mechanisms, and intelligent visualization systems to provide real-time assessment of credit market conditions across expansion, neutral, and stress regimes. The methodology combines credit spread analysis, labor market indicators, consumer credit conditions, and household debt metrics into a unified framework for systemic risk assessment, featuring dynamic Bollinger Band-style thresholds and theme-adaptive visualization capabilities.

## 1. Introduction

Credit cycles represent fundamental drivers of economic fluctuations, with their dynamics significantly influencing financial stability and macroeconomic outcomes (Bernanke, Gertler & Gilchrist, 1999). The identification and measurement of credit market stress has become increasingly critical following the 2008 financial crisis, which highlighted the need for comprehensive early warning systems (Adrian & Brunnermeier, 2016). Traditional single-variable approaches often fail to capture the multidimensional nature of credit market dynamics, necessitating the development of composite indicators that integrate multiple information sources.

The SCMPI addresses this gap by constructing a weighted composite index that synthesizes four key dimensions of credit market conditions: corporate credit spreads, labor market stress, consumer credit accessibility, and household leverage ratios. This approach aligns with the theoretical framework established by Minsky (1986) regarding financial instability hypothesis and builds upon empirical work by Gilchrist & Zakrajšek (2012) on credit market sentiment.

## 2. Theoretical Framework

### 2.1 Credit Cycle Theory

The theoretical foundation of the SCMPI rests on the credit cycle literature, which posits that credit availability fluctuates in predictable patterns that amplify business cycle dynamics (Kiyotaki & Moore, 1997). During expansion phases, credit becomes increasingly available as risk perceptions decline and collateral values rise. Conversely, stress phases are characterized by credit contraction, elevated risk premiums, and deteriorating borrower conditions.

The indicator incorporates Kindleberger's (1978) framework of financial crises, which identifies key stages in credit cycles: displacement, boom, euphoria, profit-taking, and panic. By monitoring multiple variables simultaneously, the SCMPI aims to capture transitions between these phases before they become apparent in individual metrics.

### 2.2 Systemic Risk Measurement

Systemic risk, defined as the risk of collapse of an entire financial system or entire market (Kaufman & Scott, 2003), requires measurement approaches that capture interconnectedness and spillover effects. The SCMPI follows the methodology established by Bisias et al. (2012) in constructing composite measures that aggregate individual risk indicators into system-wide assessments.

The index employs the concept of "financial stress" as defined by Illing & Liu (2006), encompassing increased uncertainty about fundamental asset values, increased uncertainty about other investors' behavior, increased flight to quality, and increased flight to liquidity.

## 3. Methodology

### 3.1 Component Variables

The SCMPI integrates four primary components, each representing distinct aspects of credit market conditions:

#### 3.1.1 Credit Spreads (BAA-10Y Treasury)

Corporate credit spreads serve as the primary indicator of credit market stress, reflecting risk premiums demanded by investors for corporate debt relative to risk-free government securities (Gilchrist & Zakrajšek, 2012). The BAA-10Y spread specifically captures investment-grade corporate credit conditions, providing insight into broad credit market sentiment.

#### 3.1.2 Unemployment Rate

Labor market conditions directly influence credit quality through their impact on borrower repayment capacity (Bernanke & Gertler, 1995). Rising unemployment typically precedes credit deterioration, making it a valuable leading indicator for credit stress.

#### 3.1.3 Consumer Credit Rates

Consumer credit accessibility reflects the transmission of monetary policy and credit market conditions to household borrowing (Mishkin, 1995). Elevated consumer credit rates indicate tightening credit conditions and reduced credit availability for households.

#### 3.1.4 Household Debt Service Ratio

Household leverage ratios capture the debt burden relative to income, providing insight into household financial stress and potential credit losses (Mian & Sufi, 2014). High debt service ratios indicate vulnerable household sectors that may contribute to credit market instability.

### 3.2 Statistical Methodology

#### 3.2.1 Z-Score Normalization

Each component variable undergoes robust z-score normalization to ensure comparability across different scales and units:

Z_i,t = (X_i,t - μ_i) / σ_i

Where X_i,t represents the value of variable i at time t, μ_i is the historical mean, and σ_i is the historical standard deviation. The normalization period employs a rolling 252-day window to capture annual cyclical patterns while maintaining sensitivity to regime changes.

#### 3.2.2 Adaptive Smoothing

To reduce noise while preserving signal quality, the indicator employs exponential moving average (EMA) smoothing with adaptive parameters:

EMA_t = α × Z_t + (1-α) × EMA_{t-1}

Where α = 2/(n+1) and n represents the smoothing period (default: 63 days).

#### 3.2.3 Weighted Aggregation

The composite index combines normalized components using theoretically motivated weights:

SCMPI_t = w_1×Z_spread,t + w_2×Z_unemployment,t + w_3×Z_consumer,t + w_4×Z_debt,t

Default weights reflect the relative importance of each component based on empirical literature: credit spreads (35%), unemployment (25%), consumer credit (25%), and household debt (15%).

### 3.3 Dynamic Threshold Mechanism

Unlike static threshold approaches, the SCMPI employs adaptive Bollinger Band-style thresholds that automatically adjust to changing market volatility and conditions (Bollinger, 2001):

Expansion Threshold = μ_SCMPI - k × σ_SCMPI

Stress Threshold = μ_SCMPI + k × σ_SCMPI

Neutral Line = μ_SCMPI

Where μ_SCMPI and σ_SCMPI represent the rolling mean and standard deviation of the composite index calculated over a configurable period (default: 126 days), and k is the threshold multiplier (default: 1.0). This approach ensures that thresholds remain relevant across different market regimes and volatility environments, providing more robust regime classification than fixed thresholds.

### 3.4 Visualization and User Interface

The SCMPI incorporates advanced visualization capabilities designed for professional trading environments:

#### 3.4.1 Adaptive Theme System

The indicator features an intelligent dual-theme system that automatically optimizes colors and transparency levels for both dark and bright chart backgrounds. This ensures optimal readability across different trading platforms and user preferences.

#### 3.4.2 Customizable Visual Elements

Users can customize all visual aspects including:

- Color Schemes: Automatic theme adaptation with optional custom color overrides

- Line Styles: Configurable widths for main index, trend lines, and threshold boundaries

- Transparency Optimization: Automatic adjustment based on selected theme for optimal contrast

- Dynamic Zones: Color-coded regime areas with adaptive transparency

#### 3.4.3 Professional Data Table

A comprehensive 13-row data table provides real-time component analysis including:

- Composite index value and regime classification

- Individual component z-scores with color-coded stress indicators

- Trend direction and signal strength assessment

- Dynamic threshold status and volatility metrics

- Component weight distribution for transparency

## 4. Regime Classification

The SCMPI classifies credit market conditions into three distinct regimes:

### 4.1 Expansion Regime (SCMPI < Expansion Threshold)

Characterized by favorable credit conditions, low risk premiums, and accommodative lending standards. This regime typically corresponds to economic expansion phases with low default rates and increasing credit availability.

### 4.2 Neutral Regime (Expansion Threshold ≤ SCMPI ≤ Stress Threshold)

Represents balanced credit market conditions with moderate risk premiums and stable lending standards. This regime indicates neither significant stress nor excessive exuberance in credit markets.

### 4.3 Stress Regime (SCMPI > Stress Threshold)

Indicates elevated credit market stress with high risk premiums, tightening lending standards, and deteriorating borrower conditions. This regime often precedes or coincides with economic contractions and financial market volatility.

## 5. Technical Implementation and Features

### 5.1 Alert System

The SCMPI includes a comprehensive alert framework with seven distinct conditions:

- Regime Transitions: Expansion, Neutral, and Stress phase entries

- Extreme Conditions: Values exceeding ±2.0 standard deviations

- Trend Reversals: Directional changes in the underlying trend component

### 5.2 Performance Optimization

The indicator employs several optimization techniques:

- Efficient Calculations: Pre-computed statistical measures to minimize computational overhead

- Memory Management: Optimized variable declarations for real-time performance

- Error Handling: Robust data validation and fallback mechanisms for missing data

## 6. Empirical Validation

### 6.1 Historical Performance

Backtesting analysis demonstrates the SCMPI's ability to identify major credit stress episodes, including:

- The 2008 Financial Crisis

- The 2020 COVID-19 pandemic market disruption

- Various regional banking crises

- European sovereign debt crisis (2010-2012)

### 6.2 Leading Indicator Properties

The composite nature and dynamic threshold system of the SCMPI provides enhanced leading indicator properties, typically signaling regime changes 1-3 months before they become apparent in individual components or market indices. The adaptive threshold mechanism reduces false signals during high-volatility periods while maintaining sensitivity during regime transitions.

## 7. Applications and Limitations

### 7.1 Applications

- Risk Management: Portfolio managers can use SCMPI signals to adjust credit exposure and risk positioning

- Academic Research: Researchers can employ the index for credit cycle analysis and systemic risk studies

- Trading Systems: The comprehensive alert system enables automated trading strategy implementation

- Financial Education: The transparent methodology and visual design facilitate understanding of credit market dynamics

### 7.2 Limitations

- Data Dependency: The indicator relies on timely and accurate macroeconomic data from FRED sources

- Regime Persistence: Dynamic thresholds may exhibit brief lag during extremely rapid regime transitions

- Model Risk: Component weights and parameters require periodic recalibration based on evolving market structures

- Computational Requirements: Real-time calculations may require adequate processing power for optimal performance

## References

Adrian, T. & Brunnermeier, M.K. (2016). CoVaR. *American Economic Review*, 106(7), 1705-1741.

Bernanke, B. & Gertler, M. (1995). Inside the black box: the credit channel of monetary policy transmission. *Journal of Economic Perspectives*, 9(4), 27-48.

Bernanke, B., Gertler, M. & Gilchrist, S. (1999). The financial accelerator in a quantitative business cycle framework. *Handbook of Macroeconomics*, 1, 1341-1393.

Bisias, D., Flood, M., Lo, A.W. & Valavanis, S. (2012). A survey of systemic risk analytics. *Annual Review of Financial Economics*, 4(1), 255-296.

Bollinger, J. (2001). *Bollinger on Bollinger Bands*. McGraw-Hill Education.

Gilchrist, S. & Zakrajšek, E. (2012). Credit spreads and business cycle fluctuations. *American Economic Review*, 102(4), 1692-1720.

Illing, M. & Liu, Y. (2006). Measuring financial stress in a developed country: An application to Canada. *Journal of Financial Stability*, 2(3), 243-265.

Kaufman, G.G. & Scott, K.E. (2003). What is systemic risk, and do bank regulators retard or contribute to it? *The Independent Review*, 7(3), 371-391.

Kindleberger, C.P. (1978). *Manias, Panics and Crashes: A History of Financial Crises*. Basic Books.

Kiyotaki, N. & Moore, J. (1997). Credit cycles. *Journal of Political Economy*, 105(2), 211-248.

Mian, A. & Sufi, A. (2014). What explains the 2007–2009 drop in employment? *Econometrica*, 82(6), 2197-2223.

Minsky, H.P. (1986). *Stabilizing an Unstable Economy*. Yale University Press.

Mishkin, F.S. (1995). Symposium on the monetary transmission mechanism. *Journal of Economic Perspectives*, 9(4), 3-10.

在脚本中搜索"demand"

BTC Markup/Markdown Zones by Koenigsegg📈 BTC Markup/Markdown Zones

A handcrafted indicator designed to mark Bitcoin's most critical High Time Frame (HTF) structure shifts. This tool overlays true institutional-level Markup and Markdown Zones, selected manually after deep market review. Whether you're testing strategies or actively trading, this tool gives you the bigger picture at all times.

🔍 Key Features:

✅ HTF Markup & Markdown Zones

Every zone is manually selected — no indicators, no repainting. Just raw market history and real structure.

✅ Two Display Modes

• Background Zones — soft overlays with low opacity for visual context — with the option to increase opacity manually if desired.

• Start Candle Highlight — sharply highlighted candle marking the final pivot before a macro reversal.

✅ Custom Color Controls (Style Tab)

All visual styling lives in the Style tab, with clearly labeled fields:

• Markup Zone

• Markdown Zone

• Start Candle Highlight Markup

• Start Candle Highlight Markdown

✅ Minimal Input Section

Just one toggle: display mode. Everything else is kept clean and intuitive.

🧠 Purpose:

This script is made for any timeframe:

• Zoom into lower timeframes to know whether you're trading inside a Markup or Markdown

• Use it during strategy testing for true structural awareness

📅 Handpicked Macro Turning Points:

Each zone originates from a manually confirmed candle — the last meaningful candle before a shift in control between bulls and bears:

• FRI 19 AUG 2011 12PM – MARK DOWN

• THU 20 OCT 2011 12AM – MARK UP

• WED 10 APR 2013 12PM – MARK DOWN

• FRI 12 APR 2013 12PM – MARK UP

• SAT 30 NOV 2013 12AM – MARK DOWN

• WED 14 JAN 2015 12PM – MARK UP

• SUN 17 DEC 2017 12PM – MARK DOWN

• SAT 15 DEC 2018 12PM – MARK UP

• WED 14 APR 2021 4AM – MARK DOWN

• TUE 22 JUN 2021 12PM – MARK UP

• WED 10 NOV 2021 12PM – MARK DOWN

• MON 21 NOV 2022 8PM – MARK UP

• THU 14 MAR 2024 4AM – MARK DOWN

• MON 5 AUG 2024 12PM – MARK UP

• MON 20 JAN 2025 4AM – MARK DOWN

💡 Zones are manually updated by me after each new confirmed Markup or Markdown.

🧬 Fractal Structure for MTF Systems

Price is fractal — meaning the same principles of structure repeat across all timeframes. In Version 2, this tool evolves by introducing manually selected sub-zones inside each High Time Frame (HTF) Markup or Markdown. These sub-zones reflect Medium Timeframe (MTF) structure shifts, offering precision for traders who operate on both intraday and swing levels.

This makes the indicator ideal for low timeframe (LTF) Markup/Markdown awareness — whether you're managing 15m entries or building multi-timeframe confluence systems.

No auto-zones. No guesswork. Just clean, intentional structure division within the broader trend, handpicked for maximum clarity and edge.

💡 Pro Tip:

When price is inside a Markup Zone, shorting becomes riskier — you're trading against a macro bullish structure.

When inside a Markdown Zone, longing becomes riskier — you're fighting against confirmed bearish momentum.

Use this tool to stay aligned with the broader move, especially when zoomed into smaller timeframes or managing entries/exits during intraday setups.

📈 Markup Phase – Bullish Sentiment

Definition: A period where price makes higher highs and higher lows — the uptrend is in full force.

Why sentiment is bullish:

- Institutions and smart money are already positioned long.

- Public/institutional demand drives prices up.

- Momentum is supported by positive news, breakouts, and FOMO.

- Higher highs confirm buyers are in control.

📉 Markdown Phase – Bearish Sentiment

Definition: A period where price makes lower lows and lower highs — clear downtrend.

Why sentiment is bearish:

- Distribution has already occurred, and supply outweighs demand.

- Smart money is short or sidelined, waiting for deeper prices.

- Panic selling or trend-following traders add downside momentum.

- Lower lows confirm sellers are in control.

❌ Trading Against the Trend — Consequences:

-Reduced Probability of Success

-You’re fighting the dominant flow. Most participants are pushing in the opposite direction.

-Drawdowns & Stop-Outs

-Countertrend trades often get wicked or flushed before any meaningful move, especially without structure-based entries.

-Low Risk-Reward Ratio

-Trends offer sustained moves. Countertrend trades may have small take-profit zones or chop.

-Mental Drain & Doubt

-Fighting momentum causes anxiety, second-guessing, and emotional reactions.

-Missed Opportunities

-Focusing on fighting the trend makes you blind to the high-probability setups with the trend.

-Increased Transaction Costs

-More stop-outs and re-entries mean more fees, more friction.

-FOMO from Watching the Trend Run

-Entering countertrend means you might watch the trend explode without you.

-Confirmation Bias & Stubbornness

-Countertrend traders often look for reasons to justify staying in the wrong direction — leading to bigger losses.

🧠 Summary

In markup = bulls dominate → you swim with the current.

In markdown = bears dominate → going long is like pushing a rock uphill.

Trading with the trend is not just safer, it's smarter. The edge lives in momentum — not ego.

⚠️ Disclaimer

This indicator is for educational and analytical use only. It is not financial advice and should not be relied on for decision-making without personal analysis.

This is not a predictive tool. No indicator can forecast upcoming price movements.

What you see here is based purely on past market behavior — specifically, historical tops and bottoms that marked the start of confirmed reversals.

This script does not know where the next reversal begins, nor can it determine where a new Markup or Markdown starts or ends. It is designed to provide context, not prediction.

Always trade with responsibility and perform your own due diligence.

Wyckoff Accumulation Distribution Wyckoff Accumulation & Distribution Indicator (RSI-Based)

This Pine Script is a technical analysis indicator built around the Wyckoff Method, designed to detect accumulation and distribution phases using RSI (Relative Strength Index) and pivot points. It automatically marks key structural turning points on the chart and highlights relevant zones with colored boxes.

What Does It Do?

Draws accumulation and distribution boxes based on RSI behavior.

Automatically detects Wyckoff structural signals:

SC (Selling Climax)

AR (Automatic Rally)

ST (Secondary Test)

BC (Buying Climax)

DAR (Automatic Reaction)

DST (Secondary Test - Distribution)

Identifies trend transitions by detecting sideways RSI movement.

Attempts to detect spring and UTAD-like deviations based on RSI reversals.

Uses RSI extremes in conjunction with pivot points to generate Wyckoff signals.

How Does It Work?

RSI Zone: It identifies sideways markets when RSI stays within ±20 of the 50 level (this range is configurable).

Pivot Points: It detects pivot highs/lows that sync with RSI values (pivotLen is adjustable).

Trend Box Drawing:

When RSI exits the sideways zone, the script draws a gray box between the highest high and lowest low within that range.

If RSI breaks upward, the box becomes green (Accumulation); if downward, it becomes red (Distribution).

Wyckoff Structural Points:

SC/BC: Detected when a pivot occurs with RSI below/above a threshold.

AR/DAR: The next opposite pivot after SC or BC.

ST/DST: The next same-direction pivot after AR or DAR.

How to Use It

Works best on 4H or daily charts for more reliable signals. Shorter timeframes may generate noise.

Primarily used for interpreting RSI structures through the lens of Wyckoff methodology.

Box colors help quickly identify market phase:

Green box: Likely Accumulation

Red box: Likely Distribution

Triangular markers show key signals:

SC, AR, ST: Accumulation points

BC, DAR, DST: Distribution points

Use these signals alongside price action to manually interpret Wyckoff phases.

image.binance.vision

image.binance.vision

What Is the Wyckoff Method?

The Wyckoff Method, developed in the 1930s by Richard Wyckoff, is a market analysis approach that focuses on supply and demand dynamics behind price movements.

Wyckoff’s 5 Phases:

Accumulation: Smart money gradually buying at low prices.

Markup: Price begins trending upwards.

Distribution: Smart money selling to retail traders.

Markdown: Downtrend begins as supply outweighs demand.

Re-accumulation / Re-distribution: Trend-continuation phases with consolidations.

This indicator is specifically designed to detect phase 1 (Accumulation) and phase 3 (Distribution).

Extra Notes

Repainting is minimal, as pivots are confirmed using historical candles.

Labels use plotshape for a clean, minimalist visual style.

Other Wyckoff events (like SOS, LPS, UT, UTAD) could be added in future updates.

This script does not generate buy/sell signals; it is meant for structural interpretation.

Order blocksHi all!

This indicator will show you found order blocks that can be used as supply or demand. It's my take on trying to create good order blocks and I hope it makes sense.

First off I suggest to verify the current trend before using an order block. This can be done in a variety of ways, one way could be to use my other script "Market structure" () which I use and suggest.

You can configure the indicator to behave differently depending on settings. These are the settings available:

• The order blocks created can be found in any higher timeframe defined in "Timeframe"

• The number of active order blocks are defined in "Count". If an order block is found the earliest order block will be replaced

• You can choose the type of order blocks that are found ("Bullish", "Bearish " or "Both") in "Type"

• The old order blocks can be kept if "Keep history" is checked

• Order blocks that are found are not removed when mitigated (entered) but when a new one appears. They can be removed when they are broken by price if "Remove broken zones" are checked

There is also a setting section called "Requirements" that defines what is required for an order block to be created. These are the settings:

• "Take out"

Check this if you want the base of the order block (the candle where the zone is drawn from (high and low)) to have to take out the previous candle (be higher or lower depending if the order block is bullish or bearish).

• "Consecutive rising/falling"

Each following candle in the reaction (the 3 reaction candles) needs to reach higher or lower (depending on bullish or bearish). Check this if you want that to be true.

• "Reaction"

Some sort of reaction is needed from the 3 candles creating the order block. This reaction is based on the value of the Average True Length (ATR) of length 14. You can here define a factor of the value from the ATR that these 3 candles needs to move in price. A higher need for a reaction (higher factor of the ATR) will create lesser zones. You can also choose to show this limit with the checkbox.

• "Fair Value Gap"

The reaction needs to create a gap (imbalance) in price. This gap is known as a "Fair Value Gap" and is created when the last candle's wick does not meet with the base candle's wick. Check this if you want this to be needed.

After these settings you can also choose the colors of the created zones. The ones that are active (called "Zones"), the ones that are replaced ("Replaced zones") and the ones that are broken ("Broken zones") (if this is enabled in "Remove broken zones").

I'm using my library "Touched" to be able to show you labels when the order blocks have a retest, false breakout and breakout. These labels can be hidden if you disable the labels under the style tab in the indicator settings.

The concept of order blocks is widely used among traders and can provide you with good supply or demand zones. I hope that this indicator makes sense.

My todo-list has a few things, but top of that list is adding alerts for zone interactions or creations. Please feel free to say what you want to be coded!

The order blocks in the publication chart are found in weekly timeframe but are shown on the daily timeframe. Other than that the image shows you zones from the default settings (which are based on the daily timeframe).

Best of luck trading!

Balance of Power [Pinescriptlabs]Balance of Power Indicator ⚖️

The Balance of Power Indicator is a visual tool that illustrates the power dynamics between buyers and sellers by analyzing recent price action. Instead of providing direct buy or sell signals, this indicator shows how the tilt of a symbolic scale reflects the relative strength of both parties. The calculation is based on the difference between the current closing price and the closing price from a specific number of periods (defined by the user), adjusted for market volatility measured by the ATR (Average True Range).

Tilt Value Interpretation:

• Positive Tilt (0 to 1) 📈:

o A tilt value close to 1 indicates significant control by buyers. The current price is well above the average adjusted for recent volatility. Practically, a tilt in the range of 0.50 to 1 suggests buyers are pushing the price above the average volatility, signaling a strong bullish trend.

•

o

• Negative Tilt (-1 to 0) 📉:

o A tilt value close to -1 indicates significant control by sellers. The current price has dropped notably compared to the average adjusted for recent volatility. A tilt in the range of -0.50 to -1 suggests sellers are dominating, with the price falling below the average volatility, reflecting a strong bearish trend.

o

Neutral:

Indicator Sensitivity:

The number of periods analyzed affects the sensitivity of the indicator:

• Shorter Periods: Make the indicator respond more quickly to price changes.

• Longer Periods: Smooth out the tilt, providing a more stable view of market forces.

Visualizing Relative Power:

The balance not only shows the general direction of power between buyers and sellers but also the intensity of this pressure. By adding more small balances, the indicator visually represents greater strength in the corresponding direction. Thus, the Balance of Power provides an overview of the balance between supply and demand, and allows for a visual assessment of the magnitude of that pressure based on the scale’s tilt.

Español

Indicador de Balance de Poder ⚖️

El Indicador de Balance de Poder es una herramienta visual que ilustra la dinámica de poder entre compradores y vendedores mediante el análisis de la acción reciente del precio. En lugar de proporcionar señales directas de compra o venta, este indicador muestra cómo la inclinación de una balanza simbólica refleja la fuerza relativa de ambas partes. El cálculo se basa en la diferencia entre el precio de cierre actual y el precio de cierre de un número específico de períodos (definidos por el usuario), ajustado por la volatilidad del mercado medida por el ATR (Average True Range).

#### **Interpretación del Valor de Tilt(inclinación):**

- Tilt Positivo (0 a 1) 📈:

- Un valor de inclinación cercano a **1** indica un control significativo por parte de los compradores. El precio actual está muy por encima del promedio ajustado por la volatilidad reciente. En términos prácticos, un tilt en el rango de **0.50 a 1** sugiere que los compradores están impulsando el precio por encima de la volatilidad promedio, señalando una fuerte tendencia alcista.

- **Tilt Negativo (-1 a 0) 📉:**

- Un valor de inclinación cercano a **-1** indica un control significativo por parte de los vendedores. El precio actual ha caído notablemente en comparación con el promedio ajustado por la volatilidad reciente. Un tilt en el rango de **-0.50 a -1** sugiere que los vendedores están dominando, con el precio cayendo por debajo de la volatilidad promedio, reflejando una fuerte tendencia bajista.

- **Neutral:**

**Sensibilidad del Indicador:**

El número de períodos analizados afecta la sensibilidad del indicador:

- **Períodos más cortos:** Hacen que el indicador responda más rápidamente a los cambios en el precio.

- **Períodos más largos:** Suavizan la inclinación, proporcionando una visión más estable de las fuerzas del mercado.

#### **Visualización del Poder Relativo:**

La balanza no solo muestra la dirección general del poder entre compradores y vendedores, sino también la intensidad de esta presión. Al agregar más pequeñas balanzas, el indicador representa visualmente una mayor fuerza en la dirección correspondiente. Así, el **Balance de Poder** proporciona una visión general del equilibrio entre oferta y demanda y permite una evaluación visual de la magnitud de esa presión basada en la inclinación de la balanza.

Swing Pivots [UkutaLabs]█ OVERVIEW

The Swing Pivots indicator uses relevant price-action information to identify key levels of Support and Resistance. Traders will be able to use current day Swing Pivots as well as mirror higher time frame Swing Pivots to gain a stronger understanding of overall market strength and key levels.

The aim of this script is to improve the users trading experience by offering a versatile toolkit that can be used in a wide variety of trading strategies to help simplify the complexities of the market.

█ USAGE

Throughout the trading day, the script will automatically identify key High and Low levels in the market based on currently relevant price action information, giving users potentially strong support and resistance levels which serve to guide the trader throughout the complexities in the market.

The script will also Identify powerful Order Blocks which are clusters of orders executed at a specific price level which represent an imbalance between supply and demand. By identifying Order Blocks, the script can indicate valuable supply and demand zones which help signal potential market turning points for the trader.

Furthermore, the script allows the user to mirror higher time frame Swing Pivots onto lower time frame charts to gain a stronger understanding of overall market strength and key levels on multiple time frames from a single chart.

█ SETTINGS

Configuration

Pivot Strength: Determines the sensitivity of the pivot calculation. A higher strength will result in less pivots being drawn, and a lower strength will result in more pivots being drawn.

Current Time frame

• Display: Determines whether or not Swing Pivots from the current time frame will be drawn on the chart.

5 Minute (Higher Time Frame)

• Display: Determines whether or not Swing Pivots from the 5 minute time frame will be drawn on the chart.

15 Minute (Higher Time Frame)

• Display: Determines whether or not Swing Pivots from the 15 minute time frame will be drawn on the chart.

30 Minute (Higher Time Frame)

• Display: Determines whether or not Swing Pivots from the 30 minute time frame will be drawn on the chart.

1 Hour (Higher Time Frame)

• Display: Determines whether or not Swing Pivots from the 1 hour time frame will be drawn on the chart.

4 Hour (Higher Time Frame)

• Display: Determines whether or not Swing Pivots from the 4 hour time frame will be drawn on the chart.

Daily (Higher Time Frame)

• Display: Determines whether or not Swing Pivots from the daily time frame will be drawn on the chart.

Double FVG-BPR [QuantVue]The Double FVG BPR Indicator is a versatile tool that helps traders identify potential support and resistance levels through the concept of balanced price ranges.

A Balanced Price Range (BPR) is a zone on a price chart where the market has found equilibrium after a period of price imbalance.

It is identified by detecting a Fair Value Gap (FVG) in one direction, followed by an overlapping Fair Value Gap in the opposite direction.

Components of a Balanced Price Range

Fair Value Gap (FVG): A FVG occurs when there is a rapid price movement, creating a gap in the price chart where minimal trading occurs. This gap represents an imbalance between supply and demand.

Bullish FVG: A bullish FVG is identified when the low of a candle is higher than the high of a candle two periods ago, and the close of the previous candle is higher than the high of that same period.

Bearish FVG: A bearish FVG is identified when the high of a candle is lower than the low of a candle two periods ago, and the close of the previous candle is lower than the low of that same period.

Overlapping Fair Value Gap: For a BPR to be formed, an initial FVG must be followed by an overlapping FVG in the opposite direction. This creates a balanced zone where the price has moved up (or down) quickly and then moved down (or up) with similar intensity, suggesting a temporary equilibrium.

The area between the high and low points of these overlapping FVGs forms the BPR. This zone represents a temporary market equilibrium where supply and demand have balanced out after a period of significant price movement in both directions.

How to Use

Support and Resistance Levels: The upper and lower boundaries of the BPR act as dynamic support and resistance levels. Traders can use these levels to place buy and sell orders, anticipating that the price may find support or face resistance within these zones.

Trend Reversal and Continuation: The BPR can signal potential trend reversals or continuations.

If the price moves back into the BPR after a breakout, it may indicate a reversal. Conversely, if the price breaks out of the BPR with strong momentum, it may signal a trend continuation.

Support and Resistance Breakouts By RICHIESupport and resistance are fundamental concepts in technical analysis used to identify price levels on charts that act as barriers, preventing the price of an asset from getting pushed in a certain direction. Here’s a detailed description of each and how breakout strategies are typically used:

Support

Support is a price level where a downtrend can be expected to pause due to a concentration of demand. As the price of an asset drops, it hits a level where buyers tend to step in, causing the price to rebound.

Support Level Identification: Support levels are identified by looking at historical data where prices have repeatedly fallen to a certain level but have then rebounded.

Strength of Support: The more times an asset price hits a support level without breaking below it, the stronger that support level is considered to be.

Resistance

Resistance is a price level where an uptrend can be expected to pause due to a concentration of selling interest. As the price of an asset increases, it hits a level where sellers tend to step in, causing the price to drop.

Resistance Level Identification: Resistance levels are identified by looking at historical data where prices have repeatedly risen to a certain level but have then fallen back.

Strength of Resistance: The more times an asset price hits a resistance level without breaking above it, the stronger that resistance level is considered to be.

Breakouts

A breakout occurs when the price moves above a resistance level or below a support level with increased volume. Breakouts can be significant because they suggest a change in supply and demand dynamics, often leading to strong price movements.

Breakout Above Resistance: Indicates a bullish market sentiment. Traders often interpret this as a sign to enter a long position (buy).

Breakout Below Support: Indicates a bearish market sentiment. Traders often interpret this as a sign to enter a short position (sell).

Breakout Trading Strategies

Confirmation: Wait for a candle to close beyond the support or resistance level to confirm the breakout.

Volume: Increased volume on a breakout adds credibility, suggesting that the price move is supported by strong buying or selling interest.

Retest: Sometimes, after a breakout, the price will return to the breakout level to test it as a new support or resistance. This retest offers another entry point.

Stop-Loss: Place stop-loss orders just below the resistance (for long positions) or above the support (for short positions) to limit potential losses in case of a false breakout.

Take-Profit: Identify target levels for taking profits. These can be set based on previous support/resistance levels or using tools like Fibonacci retracements.

MOST + Moving Average ScreenerScreener version of Anıl Özekşi's Moving Stop Loss (MOST) Indicator:

USERS MAY SCREEN MOST WITH 11 DIFFERENT TYPES OF MOVING AVERAGES + THEY CAN ALSO SCREEN SIGNALS WITH THAT 11 MOVING AVERAGES INSTEAD OF USING MOST LINE.

Adjustable Moving Average Types:

SMA : Simple Moving Average

EMA : Exponential Moving Average

WMA : Weighted Moving Average

DEMA : Double Exponential Moving Average

TMA : Triangular Moving Average

VAR : Variable Index Dynamic Moving Average aka VIDYA

WWMA : Welles Wilder's Moving Average

ZLEMA : Zero Lag Exponential Moving Average

TSF : True Strength Force

HULL : Hull Moving Average

TILL : Tillson T3 Moving Average

About Screener Panel:

Users can explore 20 different and user-defined tickers, which can be changed from the SETTINGS (shares, crypto, commodities...) on this screener version.

The screener panel shows up right after the bars on the right side of the chart.

-In this screener version of MOST, users can define the number of demanded tickers (symbols) from 1 to 20 by checking the relevant boxes on the settings tab.

-All selected tickers can be screened in different timeframes.

-Also, different timeframes of the same Ticker can be screened.

IMPORTANT NOTICE:

Screener shows the results in 3 different logic:

1st LOGIC (Default Settings):

BUY AND SELL SIGNALS of MOST and MOVING AVERAGE LINE

Most Buy Signal: Moving Average Crosses ABOVE the MOST LINE

Most Sel Signal: Moving Average Crosses BELOW the MOST LINE

Tickers seen in green are the ones that are in an uptrend, according to MOST.

The ones that appear in red are those in the SELL signal, in a downtrend.

The numbers before each Ticker indicate how many bars passed after MOST's last BUY or SELL signal.

For example, according to the indicator, when BTCUSDT appears (3) in GREEN, Bitcoin switched to a BUY signal 3 bars ago.

2nd LOGIC (Moving Average & Price Flips Screener Mode):

This mode can only be activated by checking the 'Activate Moving Average Screening Mode' box on the settings menu.

MOST line will be disappeared after checking the box.

Buy Signal: When the Selected Price crosses ABOVE the selected Moving Average.

Sell Signal: When the Selected Price crosses BELOW the selected Moving Average.

Tickers seen in green are the ones that are in an uptrend, according to Moving Average & Price Flips.

The ones that appear in red are those in the SELL signal, in a downtrend.

The numbers before each Ticker indicate how many bars passed after the last BUY or SELL signal of Moving Average & Price Flips.

For example, according to the indicator, when BTCUSDT appears (3) in GREEN, Bitcoin switched to a BUY signal 3 bars ago.

3rd LOGIC (Moving Average Color Change Screener Mode):

Both 'Activate Moving Average Screening Mode' and 'Activate Moving Average Color Change Screening Mode' boxes must be checked in the settings tab.

Moving Average Line will turn out into two colors.

Green color means the moving average value is greater than the previous bar's value.

Red color means the moving average value is smaller than the previous bar's value.

Buy Signal: After the Selected Moving Average turns GREEN from red.

Sell Signal: After the Selected Moving Average turns RED from green.

-Screener shows the information about the color changes of the selected Moving Average with default settings.

If this option is preferred, users are advised to enlarge the length to have better signals.

Tickers seen in green are the ones that are in an uptrend, according to Moving Average Color.

The ones that appear in red are those in the SELL signal, in a downtrend.

The numbers before each Ticker indicate how many bars passed after the last BUY or SELL signal of Moving Average Color Change.

For example, according to the indicator, when BTCUSDT appears (3) in GREEN, Bitcoin switched to a BUY signal 3 bars ago.

Tillson T3 Moving Average - ScreenerScreener version of Tillson T3 Moving Average:

The T3 Moving Average generally produces entry signals similar to other moving averages and, thus, is mainly traded in the same manner. Here are several assumptions:

Suppose the price action is above the T3 Moving Average, and the indicator is upward. In that case, we have a bullish trend and should only enter long trades (advisable for novice/intermediate traders). If the price is below the T3 Moving Average and edging lower, we have a bearish trend and should limit entries to short.

About Screener Panel:

Users can explore 20 different and user-defined tickers, which can be changed from the SETTINGS (shares, crypto, commodities...) on this screener version.

The screener panel shows up right after the bars on the right side of the chart.

Tickers seen in green are the ones that are in an uptrend, according to T3.

The ones that appear in red are those in the SELL signal, in a downtrend.

The numbers in front of each Ticker indicate how many bars passed after the last BUY or SELL signal of T3.

For example, according to the indicator, when BTCUSDT appears (3) in GREEN, Bitcoin switched to a BUY signal 3 bars ago.

-In this screener version of Tillson T3 Moving Average, users can define the number of demanded tickers (symbols) from 1 to 20 by checking the relevant boxes on the settings tab.

-All selected tickers can be screened in different timeframes.

-Also, different timeframes of the same Ticker can be screened.

IMPORTANT NOTICE:

Screener shows the results in 2 different logic:

-Screener shows the information about the color changes of the T3 Moving Average with default settings.

-Users can check the "Change Screener to show T3 & Price Flips" button to activate the screener giving information about price flips.

If this option is preferred, users are advised to enlarge the length to have better signals.

MavilimW ScreenerScreener version of MavilimW Moving Average :

Short-Term Examples (by decreasing 3 and 5 default values to have trading signals from color changes)

BUY when MavilimW turns blue from red.

SELL when MavW turns red from blue.

Long-Term Examples (with Default values 3 and 5)

BUY when the price crosses over the MavilimW line

SELL when the price crosses below the MavW line

MavilimW can also define significant SUPPORT and RESISTANCE levels in every period with its default values 3 and 5.

Screener Panel:

You can explore 20 different and user-defined tickers, which can be changed from the SETTINGS (shares, crypto, commodities...) on this screener version.

The screener panel shows up right after the bars on the right side of the chart.

Tickers seen in green are the ones that are in an uptrend, according to MavilimW.

The ones that appear in red are those in the SELL signal, in a downtrend.

The numbers in front of each Ticker indicate how many bars passed after the last BUY or SELL signal of MavW.

For example, according to the indicator, when BTCUSDT appears (3) in GREEN, Bitcoin switched to a BUY signal 3 bars ago.

-In this screener version of MavilimW, users can define the number of demanded tickers (symbols) from 1 to 20 by checking the relevant boxes on the settings tab.

-All selected tickers can be screened in different timeframes.

-Also, different timeframes of the same Ticker can be screened.

IMPORTANT NOTICE:

-Screener shows the information about the color changes of MavilimW Moving Average with default settings (as explained in the Short-Term Example section).

-Users can check the "Change Screener to show MavilimW & Price Flips" button to activate the screener as explained in the Short-Term Example section. Then the screener will give information about price flips.

Crypto Flow Index (CFI) - RS vs BTC/ETH ---

Crypto Flow Index, CFI

Crypto Flow Index, CFI, measures relative strength between an asset and Bitcoin or Ethereum.

You use CFI to judge whether capital favors your asset or the benchmark.

CFI does not give entry or exit signals.

You use CFI as a bias and context tool.

---

What CFI measures

Relative strength money flow on the BASE/BTC or BASE/ETH pair.

Volume weighted pressure, not price alone.

Momentum blended into flow to smooth rotations.

Optional USD trend filter using fast and slow EMAs.

---

How to read CFI

Above 50 means relative strength favors the asset.

Below 50 means relative strength favors BTC or ETH.

Rising CFI shows strengthening relative demand.

Falling CFI shows weakening relative demand.

---

Histogram

Green bars show positive relative flow.

Red bars show negative relative flow.

Larger bars signal stronger pressure.

---

Bias ribbon

Green ribbon shows bullish relative bias.

Red ribbon shows bearish relative bias.

Gray ribbon shows transition or balance.

---

How to use CFI

Favor long trades when CFI stays above 50.

Avoid longs when price rises but CFI falls.

Spot rotations before price reacts.

Combine with structure, entries, and risk rules.

---

Important limits

CFI compares assets only to BTC or ETH.

CFI does not represent the entire crypto market.

USD price and relative strength often diverge.

---

Core question CFI answers

Is your asset gaining or losing strength versus Bitcoin or Ethereum.

---

Adaptive Z-Score Oscillator [QuantAlgo]🟢 Overview

The Adaptive Z-Score Oscillator transforms price action into statistical significance measurements by calculating how many standard deviations the current price deviates from its moving average baseline, then dynamically adjusting threshold levels based on historical distribution patterns. Unlike traditional oscillators that rely on fixed overbought/oversold levels, this indicator employs percentile-based adaptive thresholds that automatically calibrate to changing market volatility regimes and statistical characteristics. By offering both adaptive and fixed threshold modes alongside multiple moving average types and customizable smoothing, the indicator provides traders and investors with a robust framework for identifying extreme price deviations, mean reversion opportunities, and underlying trend conditions through the visualization of price behavior within a statistical distribution context.

🟢 How It Works

The indicator begins by establishing a dynamic baseline using a user-selected moving average type applied to closing prices over the specified length period, then calculates the standard deviation to measure price dispersion:

basis = ma(close, length, maType)

stdev = ta.stdev(close, length)

The core Z-Score calculation quantifies how many standard deviations the current price sits above or below the moving average basis, creating a normalized oscillator that facilitates cross-asset and cross-timeframe comparisons:

zScore = stdev != 0 ? (close - basis) / stdev : 0

smoothedZ = ma(zScore, smooth, maType)

The adaptive threshold mechanism employs percentile calculations over a historical lookback period to determine statistically significant extreme zones. Rather than using fixed levels like ±2.0, the indicator identifies where a specified percentage of historical Z-Score readings have fallen, automatically adjusting to market regime changes:

upperThreshold = adaptive ? ta.percentile_linear_interpolation(smoothedZ, percentilePeriod, upperPercentile) : fixedUpper

lowerThreshold = adaptive ? ta.percentile_linear_interpolation(smoothedZ, percentilePeriod, lowerPercentile) : fixedLower

The visualization architecture creates a four-tier coloring system that distinguishes between extreme conditions (beyond the adaptive thresholds) and moderate conditions (between the midpoint and threshold levels), providing visual gradation of statistical significance through opacity variations and immediate recognition of distribution extremes.

🟢 How to Use This Indicator

▶ Overbought and Oversold Identification:

The indicator identifies potential overbought conditions when the smoothed Z-Score crosses above the upper threshold, indicating that price has deviated to a statistically extreme level above its mean. Conversely, oversold conditions emerge when the Z-Score crosses below the lower threshold, signaling statistically significant downward deviation. In adaptive mode (default), these thresholds automatically adjust to the asset's historical behavior, i.e., during high volatility periods, the thresholds expand to accommodate wider price swings, while during low volatility regimes, they contract to capture smaller deviations as significant. This dynamic calibration reduce false signals that plague fixed-level oscillators when market character shifts between volatile and ranging conditions.

▶ Mean Reversion Trading Applications:

The Z-Score framework excels at identifying mean reversion opportunities by highlighting when price has stretched too far from its statistical equilibrium. When the oscillator reaches extreme bearish levels (below the lower threshold with deep red coloring), it suggests price has become statistically oversold and may snap back toward the mean, presenting potential long entry opportunities for mean reversion traders. Symmetrically, extreme bullish readings (above the upper threshold with bright green coloring) indicate potential short opportunities or long exit points as price becomes statistically overbought. The moderate zones (lighter colors between midpoint and threshold) serve as early warning areas where traders can prepare for potential reversals, while exits from extreme zones (crossing back inside the thresholds) often provide confirmation that mean reversion is underway.

▶ Trend and Distribution Analysis:

Beyond discrete overbought/oversold signals, the histogram's color pattern and shape reveal the underlying trend structure and distribution characteristics. Sustained periods where the Z-Score oscillates primarily in positive territory (green bars) indicate a bullish trend where price consistently trades above its moving average baseline, even if not reaching extreme levels. Conversely, predominant negative readings (red bars) suggest bearish trend conditions. The distribution shape itself provides insight into market behavior, e.g., a narrow, centered distribution clustering near zero indicates tight ranging conditions with price respecting the mean, while a wide distribution with frequent extreme readings reveals volatile trending or choppy conditions. Asymmetric distributions skewed heavily toward one side demonstrate persistent directional bias, whereas balanced distributions suggest equilibrium between bulls and bears.

▶ Built-in Alerts:

Seven alert conditions enable automated monitoring of statistical extremes and trend transitions. Enter Overbought and Enter Oversold alerts trigger when the Z-Score crosses into extreme zones, providing early warnings of potential reversal setups. Exit Overbought and Exit Oversold alerts signal when price begins reverting from extremes, offering confirmation that mean reversion has initiated. Zero Cross Up and Zero Cross Down alerts identify transitions through the neutral line, indicating shifts between above-mean and below-mean price action that can signal trend changes. The Extreme Zone Entry alert fires on any extreme threshold penetration regardless of direction, allowing unified monitoring of both overbought and oversold opportunities.

▶ Color Customization:

Six visual themes (Classic, Aqua, Cosmic, Ember, Neon, plus Custom) accommodate different chart backgrounds and aesthetic preferences, ensuring optimal contrast and readability across trading platforms. The bar transparency control (0-90%) allows fine-tuning of visual prominence, with minimal transparency creating bold, attention-grabbing bars for primary analysis, while higher transparency values produce subtle background context when using the oscillator alongside other indicators. The extreme and moderate zone coloring system uses automatic opacity variation to create instant visual hierarchy, with darkest colors highlight the most statistically significant deviations demanding immediate attention, while lighter shades mark developing conditions that warrant monitoring but may not yet justify action. Optional candle coloring extends the Z-Score color scheme directly to the price candles on the main chart, enabling traders to instantly recognize statistical extremes and trend conditions without needing to reference the oscillator panel, creating a unified visual experience where both price action and statistical analysis share the same color language.

Session Open Range, Breakout & Trap Framework - TrendPredator OBSession Open Range, Breakout & Trap Framework — TrendPredator Open Box

Stacey Burke’s trading approach combines concepts from George Douglas Taylor, Tony Crabel, Steve Mauro, and Robert Schabacker. His framework focuses on reading price behaviour across daily templates and identifying how markets move through recurring cycles of expansion, contraction, and reversal. While effective, much of this analysis requires real-time interpretation of session-based behaviour, which can be demanding for traders working on lower intraday timeframes.

The TrendPredator indicators formalize parts of this methodology by introducing mechanical rules for multi-timeframe bias tracking and session structure analysis. They aim to present the key elements of the system—bias, breakouts, fakeouts, and range behaviour—in a consistent and objective way that reduces discretionary interpretation.

The Open Box indicator focuses specifically on the opening behaviour of major trading sessions. It builds on principles found in classical Open Range Breakout (ORB) techniques described by Tony Crabel, where a defined time window around the session open forms a structural reference range. Price behaviour relative to this range—breaking out, failing back inside, or expanding—can highlight developing session bias, potential trap formation, and directional conviction.

This indicator applies these concepts throughout the major equity sessions. It automatically maps the session’s initial range (“Open Box”) and tracks how price interacts with it as liquidity and volatility increase. It also incorporates related structural references such as:

* the first-hour high and low of the futures session

* the exact session open level

* an anchored VWAP starting at the session open

* automated expansion levels projected from the Open Box

In combination, these components provide a unified view of early session activity, including breakout attempts, fakeouts, VWAP reactions, and liquidity targeting. The Open Box offers a structured lens for observing how price transitions through the major sessions (Asia → London → New York) and how these behaviours relate to higher-timeframe bias defined in the broader TrendPredator framework.

Core Features

Open Box (Session Structure)

The indicator defines an initial session range beginning at the selected session open. This “Open Box” represents a fixed time window—commonly the first 30 minutes, or any user-defined duration—that serves as a structural reference for analysing early session behaviour.

The range highlights whether price remains inside the box, breaks out, or rejects the boundaries, providing a consistent foundation for interpreting early directional tendencies and recognising breakout, continuation, or fakeout characteristics.

How it works:

* At the session open, the indicator calculates the high and low over the specified time window.

* This range is plotted as the initial structure of the session.

* Price behaviour at the boundaries can illustrate emerging bias or potential trap formation.

* An optional secondary range (e.g., 15-minute high/low) can be enabled to capture early volatility with additional precision.

Inputs / Options:

* Session specifications (Tokyo, London, New York)

* Open Box start and end times (e.g., equity open + first 30 minutes, or any custom length)

* Open Box colour and label settings

* Formatting options for Open Box high and low lines

* Optional secondary range per session (e.g., 15-minute high/low)

* Forward extension of Open Box high/low lines

* Number of historic Open Boxes to display

Session VWAPs

The indicator plots VWAPs for each major trading session—Asia, London, and New York—anchored to their respective session opens. These session-specific VWAPs assist in tracking how value develops through the day and how price interacts with session-based volume distributions.

How it works:

* At each session open, a VWAP is anchored to the open price.

* The VWAP updates throughout the session as new volume and price data arrive.

* Deviations above or below the VWAP may indicate balance, imbalance, or directional control.

* Viewed together, session VWAPs help identify transitions in value across sessions.

Inputs / Options:

* Enable or disable VWAP per session

* Adjustable anchor and end times (optionally to end of day)

* Line styling and label settings

* Number of historic VWAPs to draw

First Hour High/Low Extensions

The indicator marks the high and low formed during the first hour of each session. These reference points often function as early control levels and provide context for assessing whether the session is establishing bias, consolidating, or exhibiting reversal behaviour.

How it works:

* After the session starts, the indicator records the highest and lowest prices during the first hour.

* These levels are plotted and extended across the session.

* They provide a visual reference for observing reactions, targets, or rejection zones.

Inputs / Options:

* Enable or disable for each session

* Line style, colour, and label visibility

* Number of historic sessions displayed

EQO Levels (Equity Open)

The indicator plots the opening price of each configured session. These “Equity Open” levels represent short-term reference points that can attract price early in the session.

Once the level is revisited after the Open Box has formed, it is automatically cut to avoid clutter. If not revisited, the line remains as an untested reference, similar to a naked point of control.

How it works:

* At session open, the open price is recorded.

* The level is plotted as a local reference.

* If price interacts with the level after the Open Box completes, the line is cut.

* Untested EQOs extend forward until interacted with.

Inputs / Options:

* Enable/disable per session

* Line style and label settings

* Optional extension into the next day

* Option for cutting vs. hiding on revisit

* Number of historic sessions displayed

OB Range Expansions (Automatic)

Range expansions are calculated from the height of the Open Box. These levels provide structured reference zones for identifying potential continuation or exhaustion areas within a session.

How it works:

* After the Open Box is formed, multiples of the range (e.g., 1×, 2×, 3×) are projected.

* These expansion levels are plotted above and below the range.

* Price reactions near these areas can illustrate continuation, hesitation, or potential reversal.

Inputs / Options:

* Enable or disable per session

* Select number of multiples

* Line style, colour, and label settings

* Extension length into the session

Stacey Burke 12-Candle Window Marker

The indicator can highlight the 12-candle window often referenced in Stacey Burke’s session methodology. This window represents the key active period of each session where breakout attempts, volatility shifts, and reversal signatures often occur.

How it works:

* A configurable window (default 12 candles) is highlighted from each session open.

* This window acts as a guide for observing active session behaviour.

* It remains visible throughout the session for structural context.

Inputs / Options:

* Enable/disable per session

* Configurable window duration (default: 3 hours)

* Colour and transparency controls

Concept and Integration

The Open Box is built around the same multi-timeframe logic that underpins the broader TrendPredator framework.

While higher-timeframe tools track bias and setups across the H8–D–W–M levels, the Open Box focuses on the H1–M30 domain to define session structure and observe how early intraday behaviour aligns with higher-timeframe conditions.

The indicator integrates with the TrendPredator FO (Breakout, Fakeout & Trend Switch Detector), which highlights microstructure signals on lower timeframes (M15/M5). Together they form a layered workflow:

* Higher timeframes: context, bias, and developing setups

* TrendPredator OB: intraday and intra-session structure

* TrendPredator FO: microstructure confirmation (e.g., FOL/FOH, switches)

This alignment provides a structured way to observe how daily directional context interacts with intraday behaviour.

See the public open source indicator TP FO here (click on it for access):

Practical Application

Before Session Open

* Review previous session Open Box, Open level, and VWAPs

* Assess how higher-timeframe bias aligns with potential intraday continuation or reversal

* Note untested EQO levels or VWAPs that may function as liquidity attractors

During Session Open

* Observe behaviour around the first-hour high/low and higher-timeframe reference levels

* Monitor how the M15 and 30-minute ranges close

* Track reactions relative to the session open level and the session VWAP

After the Open Box completes

* Assess price interaction with Open Box boundaries and first-hour levels

* Use microstructure signals (e.g., FOH/FOL, switches) for potential confirmation

* Refer to expansion levels as reference zones for management or target setting

After Session

* Review how price behaved relative to the Open Box, EQO levels, VWAPs, and expansion zones

* Analyse breakout attempts, fakeouts, and whether intraday structure aligned with the broader daily move

Example Workflow and Trade

1. Higher-timeframe analysis signals a Daily Fakeout Low Continuation (bullish context).

2. The New York session forms an Open Box; price breaks above and holds above the first-hour high.

3. A Fakeout Low + Switch Bar appears on M5 (via FO), after retesting the session VWAP triggering the entry.

4. 1x expansion level serves as reference targets for take profit.

Relation to the TrendPredator Ecosystem

The Open Box is part of the TrendPredator Indicator Family, designed to apply multi-timeframe logic consistently across:

* higher-timeframe context and setups

* intraday and session structure (OB)

* microstructure confirmation (FO)

Together, these modules offer a unified structure for analysing how daily and intraday cycles interact.

Disclaimer

This indicator is for educational purposes only and does not guarantee profits.

It does not provide buy or sell signals but highlights structural and behavioural areas for analysis.

Users are solely responsible for their trading decisions and outcomes.

Martingale Strategy Simulator [BackQuant]Martingale Strategy Simulator

Purpose

This indicator lets you study how a martingale-style position sizing rule interacts with a simple long or short trading signal. It computes an equity curve from bar-to-bar returns, adapts position size after losing streaks, caps exposure at a user limit, and summarizes risk with portfolio metrics. An optional Monte Carlo module projects possible future equity paths from your realized daily returns.

What a martingale is

A martingale sizing rule increases stake after losses and resets after a win. In its classical form from gambling, you double the bet after each loss so that a single win recovers all prior losses plus one unit of profit. In markets there is no fixed “even-money” payout and returns are multiplicative, so an exact recovery guarantee does not exist. The core idea is unchanged:

Lose one leg → increase next position size

Lose again → increase again

Win → reset to the base size

The expectation of your strategy still depends on the signal’s edge. Sizing does not create positive expectancy on its own. A martingale raises variance and tail risk by concentrating more capital as a losing streak develops.

What it plots

Equity – simulated portfolio equity including compounding

Buy & Hold – equity from holding the chart symbol for context

Optional helpers – last trade outcome, current streak length, current allocation fraction

Optional diagnostics – daily portfolio return, rolling drawdown, metrics table

Optional Monte Carlo probability cone – p5, p16, p50, p84, p95 aggregate bands

Model assumptions

Bar-close execution with no slippage or commissions

Shorting allowed and frictionless

No margin interest, borrow fees, or position limits

No intrabar moves or gaps within a bar (returns are close-to-close)

Sizing applies to equity fraction only and is capped by your setting

All results are hypothetical and for education only.

How the simulator applies it

1) Directional signal

You pick a simple directional rule that produces +1 for long or −1 for short each bar. Options include 100 HMA slope, RSI above or below 50, EMA or SMA crosses, CCI and other oscillators, ATR move, BB basis, and more. The stance is evaluated bar by bar. When the stance flips, the current trade ends and the next one starts.

2) Sizing after losses and wins

Position size is a fraction of equity:

Initial allocation – the starting fraction, for example 0.15 means 15 percent of equity

Increase after loss – multiply the next allocation by your factor after a losing leg, for example 2.00 to double

Reset after win – return to the initial allocation

Max allocation cap – hard ceiling to prevent runaway growth

At a high level the size after k consecutive losses is

alloc(k) = min( cap , base × factor^k ) .

In practice the simulator changes size only when a leg ends and its PnL is known.

3) Equity update

Let r_t = close_t / close_{t-1} − 1 be the symbol’s bar return, d_{t−1} ∈ {+1, −1} the prior bar stance, and a_{t−1} the prior bar allocation fraction. The simulator compounds:

eq_t = eq_{t−1} × (1 + a_{t−1} × d_{t−1} × r_t) .

This is bar-based and avoids intrabar lookahead. Costs, slippage, and borrowing costs are not modeled.

Why traders experiment with martingale sizing

Mean-reversion contexts – if the signal often snaps back after a string of losses, adding size near the tail of a move can pull the average entry closer to the turn

Behavioral or microstructure edges – some rules have modest edge but frequent small whipsaws; size escalation may shorten time-to-recovery when the edge manifests

Exploration and stress testing – studying the relationship between streaks, caps, and drawdowns is instructive even if you do not deploy martingale sizing live

Why martingale is dangerous

Martingale concentrates capital when the strategy is performing worst. The main risks are structural, not cosmetic:

Loss streaks are inevitable – even with a 55 percent win rate you should expect multi-loss runs. The probability of at least one k-loss streak in N trades rises quickly with N.

Size explodes geometrically – with factor 2.0 and base 10 percent, the sequence is 10, 20, 40, 80, 100 (capped) after five losses. Without a strict cap, required size becomes infeasible.

No fixed payout – in gambling, one win at even odds resets PnL. In markets, there is no guaranteed bounce nor fixed profit multiple. Trends can extend and gaps can skip levels.

Correlation of losses – losses cluster in trends and in volatility bursts. A martingale tends to be largest just when volatility is highest.

Margin and liquidity constraints – leverage limits, margin calls, position limits, and widening spreads can force liquidation before a mean reversion occurs.

Fat tails and regime shifts – assumptions of independent, Gaussian returns can understate tail risk. Structural breaks can keep the signal wrong for much longer than expected.

The simulator exposes these dynamics in the equity curve, Max Drawdown, VaR and CVaR, and via Monte Carlo sketches of forward uncertainty.

Interpreting losing streaks with numbers

A rough intuition: if your per-trade win probability is p and loss probability is q=1−p , the chance of a specific run of k consecutive losses is q^k . Over many trades, the chance that at least one k-loss run occurs grows with the number of opportunities. As a sanity check:

If p=0.55 , then q=0.45 . A 6-loss run has probability q^6 ≈ 0.008 on any six-trade window. Across hundreds of trades, a 6 to 8-loss run is not rare.

If your size factor is 1.5 and your base is 10 percent, after 8 losses the requested size is 10% × 1.5^8 ≈ 25.6% . With factor 2.0 it would try to be 10% × 2^8 = 256% but your cap will stop it. The equity curve will still wear the compounded drawdown from the sequence that led to the cap.

This is why the cap setting is central. It does not remove tail risk, but it prevents the sizing rule from demanding impossible positions

Note: The p and q math is illustrative. In live data the win rate and distribution can drift over time, so real streaks can be longer or shorter than the simple q^k intuition suggests..

Using the simulator productively

Parameter studies

Start with conservative settings. Increase one element at a time and watch how the equity, Max Drawdown, and CVaR respond.

Initial allocation – lower base reduces volatility and drawdowns across the board

Increase factor – set modestly above 1.0 if you want the effect at all; doubling is aggressive

Max cap – the most important brake; many users keep it between 20 and 50 percent

Signal selection

Keep sizing fixed and rotate signals to see how streak patterns differ. Trend-following signals tend to produce long wrong-way streaks in choppy ranges. Mean-reversion signals do the opposite. Martingale sizing interacts very differently with each.

Diagnostics to watch

Use the built-in metrics to quantify risk:

Max Drawdown – worst peak-to-trough equity loss

Sharpe and Sortino – volatility and downside-adjusted return

VaR 95 percent and CVaR – tail risk measures from the realized distribution

Alpha and Beta – relationship to your chosen benchmark

If you would like to check out the original performance metrics script with multiple assets with a better explanation on all metrics please see

Monte Carlo exploration

When enabled, the forecast draws many synthetic paths from your realized daily returns:

Choose a horizon and a number of runs

Review the bands: p5 to p95 for a wide risk envelope; p16 to p84 for a narrower range; p50 as the median path

Use the table to read the expected return over the horizon and the tail outcomes

Remember it is a sketch based on your recent distribution, not a predictor

Concrete examples

Example A: Modest martingale

Base 10 percent, factor 1.25, cap 40 percent, RSI>50 signal. You will see small escalations on 2 to 4 loss runs and frequent resets. The equity curve usually remains smooth unless the signal enters a prolonged wrong-way regime. Max DD may rise moderately versus fixed sizing.

Example B: Aggressive martingale

Base 15 percent, factor 2.0, cap 60 percent, EMA cross signal. The curve can look stellar during favorable regimes, then a single extended streak pushes allocation to the cap, and a few more losses drive deep drawdown. CVaR and Max DD jump sharply. This is a textbook case of high tail risk.

Strengths

Bar-by-bar, transparent computation of equity from stance and size

Explicit handling of wins, losses, streaks, and caps

Portable signal inputs so you can A–B test ideas quickly

Risk diagnostics and forward uncertainty visualization in one place

Example, Rolling Max Drawdown

Limitations and important notes

Martingale sizing can escalate drawdowns rapidly. The cap limits position size but not the possibility of extended adverse runs.

No commissions, slippage, margin interest, borrow costs, or liquidity limits are modeled.

Signals are evaluated on closes. Real execution and fills will differ.

Monte Carlo assumes independent draws from your recent return distribution. Markets often have serial correlation, fat tails, and regime changes.

All results are hypothetical. Use this as an educational tool, not a production risk engine.

Practical tips

Prefer gentle factors such as 1.1 to 1.3. Doubling is usually excessive outside of toy examples.

Keep a strict cap. Many users cap between 20 and 40 percent of equity per leg.

Stress test with different start dates and subperiods. Long flat or trending regimes are where martingale weaknesses appear.

Compare to an anti-martingale (increase after wins, cut after losses) to understand the other side of the trade-off.

If you deploy sizing live, add external guardrails such as a daily loss cut, volatility filters, and a global max drawdown stop.

Settings recap

Backtest start date and initial capital

Initial allocation, increase-after-loss factor, max allocation cap

Signal source selector

Trading days per year and risk-free rate

Benchmark symbol for Alpha and Beta

UI toggles for equity, buy and hold, labels, metrics, PnL, and drawdown

Monte Carlo controls for enable, runs, horizon, and result table

Final thoughts

A martingale is not a free lunch. It is a way to tilt capital allocation toward losing streaks. If the signal has a real edge and mean reversion is common, careful and capped escalation can reduce time-to-recovery. If the signal lacks edge or regimes shift, the same rule can magnify losses at the worst possible moment. This simulator makes those trade-offs visible so you can calibrate parameters, understand tail risk, and decide whether the approach belongs anywhere in your research workflow.

Information-Geometric Market DynamicsInformation-Geometric Market Dynamics

The Information Field: A Geometric Approach to Market Dynamics

By: DskyzInvestments

Foreword: Beyond the Shadows on the Wall

If you have traded for any length of time, you know " the feeling ." It is the frustration of a perfect setup that fails, the whipsaw that stops you out just before the real move, the nagging sense that the chart is telling you only half the story. For decades, technical analysis has relied on interpreting the shadows—the patterns left behind by price. We draw lines on these shadows, apply indicators to them, and hope they reveal the future.

But what if we could stop looking at the shadows and, instead, analyze the object casting them?

This script introduces a new paradigm for market analysis: Information-Geometric Market Dynamics (IGMD) . The core premise of IGMD is that the price chart is merely a one-dimensional projection of a much richer, higher-dimensional reality—an " information field " generated by the collective actions and beliefs of all market participants.