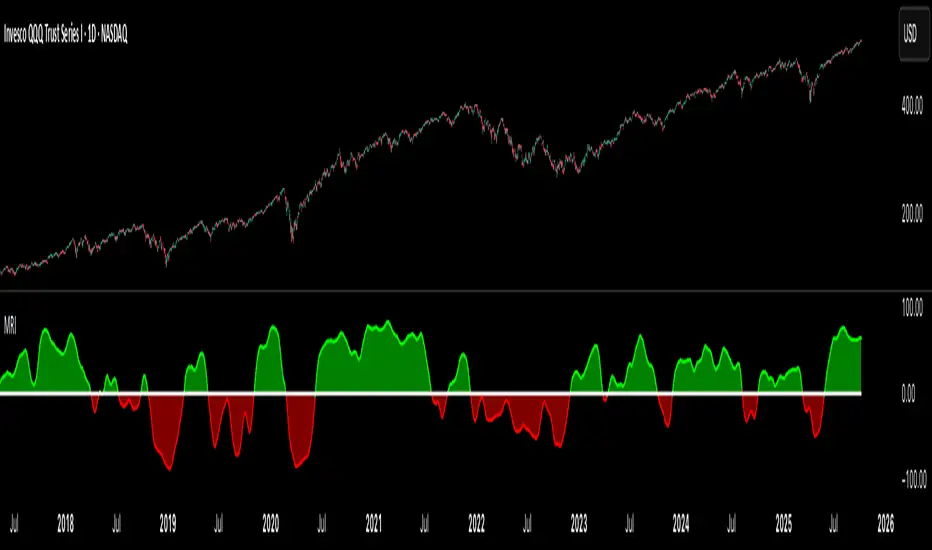

Market Regime IndexThe Market Regime Index is a top-down macro regime nowcasting tool that offers a consolidated view of the market’s risk appetite. It tracks 32 of the world’s most influential markets across asset classes to determine investor sentiment by applying trend-following signals to each independent asset. It features adjustable parameters and a built-in alert system that notifies investors when conditions transition between Risk-On and Risk-Off regimes. The selected markets are grouped into equities (7), fixed income (9), currencies (7), commodities (5), and derivatives (4):

Equities = S&P 500 E-mini Index Futures, Nasdaq-100 E-mini Index Futures, Russell 2000 E-mini Index Futures, STOXX Europe 600 Index Futures, Nikkei 225 Index Futures, MSCI Emerging Markets Index Futures, and S&P 500 High Beta (SPHB)/Low Beta (SPLV) Ratio.

Fixed Income = US 10Y Treasury Yield, US 2Y Treasury Yield, US 10Y-02Y Yield Spread, German 10Y Bund Yield, UK 10Y Gilt Yield, US 10Y Breakeven Inflation Rate, US 10Y TIPS Yield, US High Yield Option-Adjusted Spread, and US Corporate Option-Adjusted Spread.

Currencies = US Dollar Index (DXY), Australian Dollar/US Dollar, Euro/US Dollar, Chinese Yuan/US Dollar, Pound Sterling/US Dollar, Japanese Yen/US Dollar, and Bitcoin/US Dollar.

Commodities = ICE Brent Crude Oil Futures, COMEX Gold Futures, COMEX Silver Futures, COMEX Copper Futures, and S&P Goldman Sachs Commodity Index (GSCI) Futures.

Derivatives = CBOE S&P 500 Volatility Index (VIX), ICE US Bond Market Volatility Index (MOVE), CBOE 3M Implied Correlation Index, and CBOE VIX Volatility Index (VVIX)/VIX.

All assets are directionally aligned with their historical correlation to the S&P 500. Each asset contributes equally based on its individual bullish or bearish signal. The overall market regime is calculated as the difference between the number of Risk-On and Risk-Off signals divided by the total number of assets, displayed as the percentage of markets confirming each regime. Green indicates Risk-On and occurs when the number of Risk-On signals exceeds Risk-Off signals, while red indicates Risk-Off and occurs when the number of Risk-Off signals exceeds Risk-On signals.

Bullish Signal = (Fast MA – Slow MA) > (ATR × ATR Margin)

Bearish Signal = (Fast MA – Slow MA) < –(ATR × ATR Margin)

Market Regime = (Risk-On signals – Risk-Off signals) ÷ Total assets

This indicator is designed with flexibility in mind, allowing users to include or exclude individual assets that contribute to the market regime and adjust the input parameters used for trend signal detection. These parameters apply to each independent asset, and the overall regime signal is smoothed by the signal length to reduce noise and enhance reliability. Investors can position according to the prevailing market regime by selecting factors that have historically outperformed under each regime environment to minimise downside risk and maximise upside potential:

Risk-On Equity Factors = High Beta > Cyclicals > Low Volatility > Defensives.

Risk-Off Equity Factors = Defensives > Low Volatility > Cyclicals > High Beta.

Risk-On Fixed Income Factors = High Yield > Investment Grade > Treasuries.

Risk-Off Fixed Income Factors = Treasuries > Investment Grade > High Yield.

Risk-On Commodity Factors = Industrial Metals > Energy > Agriculture > Gold.

Risk-Off Commodity Factors = Gold > Agriculture > Energy > Industrial Metals.

Risk-On Currency Factors = Cryptocurrencies > Foreign Currencies > US Dollar.

Risk-Off Currency Factors = US Dollar > Foreign Currencies > Cryptocurrencies.

In summary, the Market Regime Index is a comprehensive macro risk-management tool that identifies the current market regime and helps investors align portfolio risk with the market’s underlying risk appetite. Its intuitive, color-coded design makes it an indispensable resource for investors seeking to navigate shifting market conditions and enhance risk-adjusted performance by selecting factors that have historically outperformed. While it has proven historically valuable, asset-specific characteristics and correlations evolve over time as market dynamics change.

在脚本中搜索"implied"

MARA / mNAV=1 (x)What it does

This script overlays two signals on the MARA chart:

mNAV=1 fair-value line — the MARA price implied by Bitcoin NAV:

mNAV1 = (BTC price × BTC holdings) / MARA shares

Premium/Discount ratio — how far MARA trades vs. its NAV fair value:

Ratio = Close / mNAV1 (1.00 = fair; >1 = premium; <1 = discount)

Inputs

Shares outstanding (default: 370,460,000)

BTC holdings (official or estimated; you can roll forward +25 BTC/day if you want)

BTC symbol used for pricing (e.g., BTCUSD, BTCUSDT, BTCUSDTPERP)

How to use

When Price < mNAV=1 and Ratio < 1.00 → MARA trades at a discount to BTC NAV (potential mean-reversion if BTC is stable).

When Price > mNAV=1 and Ratio > 1.00 → premium (premium often compresses during BTC chop/weakness).

Rule of thumb (with ~53k BTC and 370.46M shares): +$1,000 BTC ≈ +$0.14 on the mNAV=1 line.

Visuals

Blue line = mNAV=1 (fair value) plotted directly on the MARA chart.

Purple line = Ratio (×) on a separate right-hand scale centered around 1.00.

Optional shading: green when Ratio > 1.05 (+5% premium), red when Ratio < 0.95 (−5% discount).

Alerts (suggested)

Premium > +5%: Ratio > 1.05

Discount < −5%: Ratio < 0.95

Notes

This is a proxy for NAV parity; it assumes your BTC holdings input is correct (official last report or your estimate).

Choice of BTC symbol matters; use the feed that best matches your workflow (spot, perp, or index).

The ratio is most informative when BTC is range-bound; during fast BTC moves MARA can overshoot temporarily.

Historical VolatilityHistorical Volatility Indicator with Custom Trading Sessions

Overview

This indicator calculates **annualized Historical Volatility (HV)** using logarithmic returns and standard deviation. Unlike standard HV indicators, this version allows you to **customize trading sessions and holidays** for different markets, ensuring accurate volatility calculations for options pricing and risk management.

Key Features

✅ Custom Trading Sessions - Define multiple trading sessions per day with precise start/end times

✅ Multiple Markets Support - Pre-configured for US, Russian, European, and crypto markets

✅ Clearing Periods Handling - Account for intraday clearing breaks

✅ Flexible Calendar - Set trading days per year for different countries

✅ All Timeframes - Works correctly on intraday, daily, weekly, and monthly charts

✅ Info Table - Optional display showing calculation parameters

How It Works

The indicator uses the classical volatility formula:

σ_annual = σ_period × √(periods per year)

Where:

- σ_period = Standard deviation of logarithmic returns over the specified period

- Periods per year = Calculated based on actual trading time (not calendar time)

Calculation Method

1. Computes log returns: ln(close / close )

2. Calculates standard deviation over the lookback period

3. Annualizes using the square root rule with accurate period count

4. Displays as percentage

Settings

Calculation

- Period (default: 10) - Lookback period for volatility calculation

Trading Schedule

- Trading Days Per Year (default: 252) - Number of actual trading days

- USA: 252

- Russia: 247-250

- Europe: 250-253

- Crypto (24/7): 365

- Trading Sessions - Define trading hours in format: `hh:mm:ss-hh:mm:ss, hh:mm:ss-hh:mm:ss`

Display

- Show Info Table - Shows calculation parameters in real-time

Market Presets

United States (NYSE/NASDAQ)

Trading Sessions: 09:30:00-16:00:00

Trading Days Per Year: 252

Trading Minutes Per Day: 390

Russia (MOEX)

Trading Sessions: 10:00:00-14:00:00, 14:05:00-18:40:00

Trading Days Per Year: 248

Trading Minutes Per Day: 515

Europe (LSE)

Trading Sessions: 08:00:00-16:30:00

Trading Days Per Year: 252

Trading Minutes Per Day: 510

Germany (XETRA)

Trading Sessions: 09:00:00-17:30:00

Trading Days Per Year: 252

Trading Minutes Per Day: 510

Cryptocurrency (24/7)

Trading Sessions: 00:00:00-23:59:59

Trading Days Per Year: 365

Trading Minutes Per Day: 1440

Use Cases

Options Trading

- Compare HV vs IV - Historical volatility compared to implied volatility helps identify mispriced options

- Volatility mean reversion - Identify when volatility is unusually high or low

- Straddle/strangle selection - Choose optimal strikes based on historical movement

Risk Management

- Position sizing - Adjust position size based on current volatility

- Stop-loss placement - Set stops based on expected price movement

- Portfolio volatility - Monitor individual asset volatility contribution

Market Analysis

- Regime identification - Detect transitions between low and high volatility environments

- Cross-market comparison - Compare volatility across different assets and markets

Why Accurate Trading Hours Matter

Standard HV indicators assume 24-hour trading or use simplified day counts, leading to significant errors in annualized volatility:

- 5-minute chart error : Can be off by 50%+ if using wrong period count

- Options pricing impact : Even 2-3% HV error affects option values substantially

- Intraday vs overnight : Correctly excludes non-trading periods

This indicator ensures your HV calculations match the methodology used in professional options pricing models.

Technical Notes

- Uses actual trading minutes, not calendar days

- Handles multiple clearing periods within a single trading day

- Properly scales volatility across all timeframes

- Logarithmic returns for more accurate volatility measurement

- Compatible with Pine Script v6

Author Notes: This indicator was designed specifically for options traders who need precise volatility measurements across different global markets. The customizable trading sessions ensure your HV calculations align with actual market hours and industry-standard options pricing models.

StdDev Supertrend {CHIPA}StdDev Supertrend ~ C H I P A is a supertrend style trend engine that replaces ATR with standard deviation as the volatility core. It can operate on raw prices or log return volatility, with optional smoothing to control noise.

Key features include:

Supertrend trailing rails built from a stddev scaled envelope that flips the regime only when price closes through the opposite rail.

Returns-based mode that scales volatility by log returns for more consistent behavior across price regimes.

Optional smoothing on the volatility input to tune responsiveness versus stability.

Directional gap fill between price and the active trend line on the main chart; opacity adapts to the distance (vs ATR) so wide gaps read stronger and small gaps stay subtle.

Secondary pane view of the rails with the same adaptive fade, plus an optional candle overlay for context.

Clean alerts that fire once when state changes

Use cases: medium-term trend following, stop/flip systems, and visual regime confirmation when you prefer stddev-based distance over ATR.

Note: no walk-forward or robustness testing is implied; parameter choices and risk controls are on you.

EMP Probabilistic [CHE]Part 1 — For Traders (Practical Overview, no formulas)

What this tool does

EMP Probabilistic \ turns raw price action into a clean, probability-aware map. It builds two adaptive bands around the session open of a higher timeframe you choose (called the S-timeframe) and highlights a robust median threshold. At a glance you know:

Where price has recently tended to stay,

Whether current momentum sits above or below the median, and

A live Long vs. Short probability based on recent outcomes.

Why it improves decisions

Objective context in any regime: The nonparametric band comes straight from recent market behavior, without assuming a particular distribution.

Volatility-aware risk lens: The parametric band adapts to current volatility, helping you judge stretch and room for continuation or snap-back.

No lookahead: All stats update only after an S-bar is finished. That means the panel reflects information you truly had at that time.

How to read the chart

Orange band = empirical, distribution-free range derived from recent session returns (nonparametric).

Teal band = volatility-scaled range around the session open (parametric).

Median dots: green when close is above the median threshold, red when below.

Info panel: shows the active S-timeframe, window sizes, live coverage for both bands, the internal width parameter and volatility estimate, plus a one-line summary.

Probability label: “Long XX% • Short YY%” — a simple read on the recent balance of up vs. down S-bars.

How to use it (quick start)

1. Choose S-timeframe with Auto, Multiplier, or Manual. “Auto” scales your chart TF up to a sensible higher step.

2. Set alpha to control how tight the inner band should be. A typical value gives you a comfortable center zone without cutting off healthy trends.

3. Trade the context:

Trend-following: Prefer longs when price holds above the median; prefer shorts when it stays below.

Mean-reversion: Fade moves near the outer edges during ranges; look for reversion back toward the median.

Breakout filter: Require closes that push and hold beyond the volatility band for momentum plays; avoid noise when price chops inside the middle of the orange band.

Risk management made practical

Size positions relative to the teal band width to keep risk consistent across instruments and regimes.

For stops, many traders set them just beyond the opposite orange bound or use a fraction of the teal band.

Watch the panel’s coverage readouts and Brier score; when they deteriorate, the market may be shifting — reduce size or demand stronger confirmation.

Suggested presets

Scalping (Crypto/FX): Auto S-TF, alpha around a fifth, calibration window near two hundred, RS volatility, metrics window near two hundred.

Intraday Futures: Multiplier 3–5× your chart TF; similar alpha and window sizes; RS volatility is a solid default.

Swing/Equities: S-TF at least daily; test both RS and GK volatility modes; keep windows on the larger side for stability.

What makes it different

Two complementary lenses: a distribution-free read of recent behavior and a volatility-scaled read for risk and stretch.

Self-calibrating width: the parametric band quietly nudges its internal multiplier so actual coverage tracks your target.

Clean UX: grouped inputs, tooltips, an info panel that tells you what’s going on, and a simple median bias you can act on.

Repainting & timing

The logic updates only when the S-bar closes. On lower-timeframe charts you’ll see intrabar flips of the dot color — that’s just live price moving around. For strict signals, confirm on S-bar close.

Friendly note (not financial advice)

Use this as a context engine. It won’t predict the future, but it will keep you on the right side of probability and volatility more often, which is exactly where consistency starts.

Part 2 — Under the Hood (Conceptual, no formulas)

Data and timeframe design

The script works on a higher S-timeframe you select. It fetches the open, high, low, close, and time of that S-bar. Internally, it only updates its rolling windows after an S-bar has finished. It then pushes the previous S-bar’s statistics into its arrays. That design removes lookahead and keeps the metrics out-of-sample relative to the current S-bar.

Nonparametric band (distribution-free)

The orange band comes from the empirical distribution of recent session-level close-minus-open moves. The script keeps a rolling window, sorts a safe copy, and reads three key points: a lower bound, a median, and an upper bound. Because it’s based purely on observed outcomes, it adapts naturally to skew, fat tails, and regime shifts without assuming any particular shape. The orange range shows “where price has tended to live” lately on the chosen S-timeframe.

Parametric band (volatility-scaled)

The teal band models log-space variability around the session open using one of two well-known OHLC volatility estimators: Rogers–Satchell or Garman–Klass. Each estimator contributes a per-bar variance figure; the script averages these across the rolling window to form a current volatility scale. It then builds a symmetric band around the session open in price space. This gives you a volatility-aware notion of stretch that complements the distribution-free orange band.

Self-calibration of band width

The teal band has an internal width multiplier. After each completed S-bar the script checks whether the realized move stayed inside that band. If the band was too tight, the multiplier is nudged upward; if it was too loose, it’s eased downward. A simple learning rate governs how quickly it adapts. Over time this keeps the realized inside-coverage close to the target implied by your alpha setting, without you having to hand-tune anything.

Long/Short probability and calibration quality

The Long vs. Short probability is a transparent statistic: it’s just the recent fraction of up sessions in the rolling window. It is not a complex model — and that’s the point. You get an honest, intuitive read on directional tendency.

To monitor how well this simple probability lines up with reality, the script tracks a Brier-style score over a separate metrics window. Lower is better: it means your recent probability read has matched outcomes more closely.

Coverage tracking for both bands

The panel reports coverage for the orange band (nonparametric) and the teal band (parametric). These are rolling averages of how often recent S-bar moves landed inside each band. Watching these two numbers tells you whether market behavior still aligns with the recent distribution and with the current volatility model.

Why it doesn’t repaint

Because the arrays update only when an S-bar closes and only push the previous bar’s stats, the panel and metrics reflect information you had at the time. Intrabar visuals can change while a bar is forming — that’s expected — but the decision framework itself is anchored to completed S-bars.

Performance and practicality

The heaviest step is sorting a copy of the window for the nonparametric band. With typical window sizes this stays responsive on TradingView. The volatility estimators and rolling averages are lightweight. Inputs are grouped with clear tooltips so you can tune without hunting.

Limitations and good practice

In thin or gappy markets the bands can jump; consider a larger window or a higher S-timeframe.

During violent regime shifts, shorten the window and increase the learning rate slightly so the teal band catches up faster — but don’t overdo it, or you’ll chase noise.

The Long/Short probability is intentionally simple; it’s a context indicator, not a standalone signal factory. Combine it with structure, volume, or your execution rules.

Takeaway

Under the hood, the script blends empirical behavior and volatility scaling, then self-calibrates so the teal band’s real-world coverage stays near your target. You get clarity, consistency, and a dashboard that tells you when its own assumptions are holding up — exactly what you need to trade with confidence.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Best regards and happy trading

Chervolino

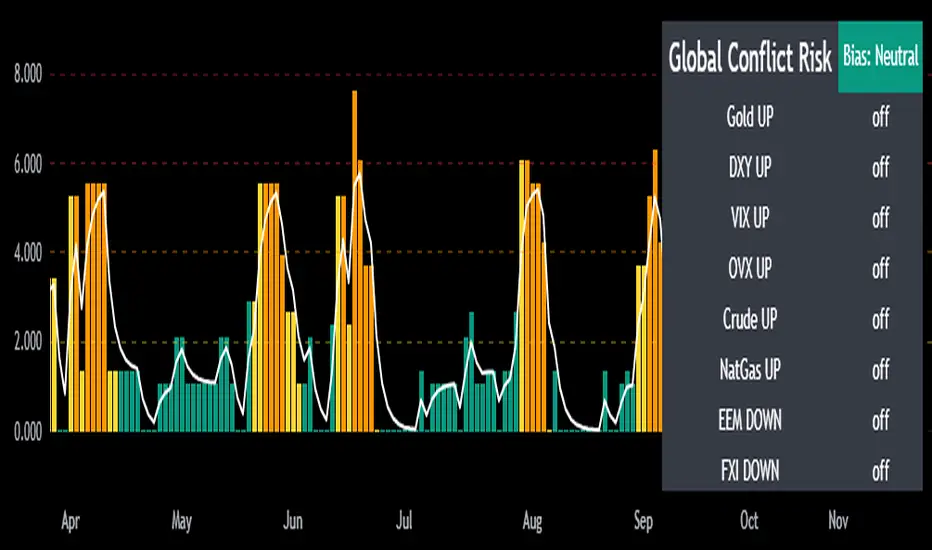

Mongoose Global Conflict Risk Index v1Overview

The Mongoose Global Conflict Risk Index v1 is a multi-asset composite indicator designed to track the early pricing of geopolitical stress and potential conflict risk across global markets. By combining signals from safe havens, volatility indices, energy markets, and emerging market equities, the index provides a normalized 0–10 score with clear bias classifications (Neutral, Caution, Elevated, High, Shock).

This tool is not predictive of headlines but captures when markets are clustering around conflict-sensitive assets before events are widely recognized.

Methodology

The indicator calculates rolling rate-of-change z-scores for eight conflict-sensitive assets:

Gold (XAUUSD) – classic safe haven

US Dollar Index (DXY) – global reserve currency flows

VIX (Equity Volatility) – S&P 500 implied volatility

OVX (Crude Oil Volatility Index) – energy stress gauge

Crude Oil (CL1!) – WTI front contract

Natural Gas (NG1!) – energy security proxy, especially Europe

EEM (Emerging Markets ETF) – global risk capital flight

FXI (China ETF) – Asia/China proxy risk

Rules:

Safe havens and vol indices trigger when z-score > threshold.

Energy triggers when z-score > threshold.

Risk assets trigger when z-score < –threshold.

Each trigger is assigned a weight, summed, normalized, and scaled 0–10.

Bias classification:

0–2: Neutral

2–4: Caution

4–6: Elevated

6–8: High

8–10: Conflict Risk-On

How to Use

Timeframes:

Daily (1D) for strategic signals and early warnings.

4H for event shocks (missiles, sanctions, sudden escalations).

Weekly (1W) for sustained trends and macro build-ups.

What to Look For:

A single trigger (for example, Gold ON) may be noise.

A cluster of 2–3 triggers across Gold, USD, VIX, and Energy often marks early stress pricing.

Elevated readings (>4) = caution; High (>6) = rotation into havens; Shock (>8) = market conviction of conflict risk.

Practical Application:

Monitor as a heatmap of global stress.

Combine with fundamental or headline tracking.

Use alert conditions at ≥4, ≥6, ≥8 for systematic monitoring.

Notes

This indicator is for informational and educational purposes only.

It is not financial advice and should be used in conjunction with other analysis methods.

σ-Based SL/TP (Long & Short). Statistical Volatility (Quant Upgrade of ATR)

Instead of ATR’s simple moving average, use standard deviation of returns (σ), realized volatility, or implied volatility (options data).

SL = kσ, TP = 2kσ (customizable).

Why better than ATR: more precise reflection of actual distribution tails, not just candle ranges.

ATR Future Movement Range Projection

The "ATR Future Movement Range Projection" is a custom TradingView Pine Script indicator designed to forecast potential price ranges for a stock (or any asset) over short-term (1-month) and medium-term (3-month) horizons. It leverages the Average True Range (ATR) as a measure of volatility to estimate how far the price might move, while incorporating recent momentum bias based on the proportion of bullish (green) vs. bearish (red) candles. This creates asymmetric projections: in bullish periods, the upside range is larger than the downside, and vice versa.

The indicator is overlaid on the chart, plotting horizontal lines for the projected high and low prices for both timeframes. Additionally, it displays a small table in the top-right corner summarizing the projected prices and the percentage change required from the current close to reach them. This makes it useful for traders assessing potential targets, risk-reward ratios, or option strategies, as it combines volatility forecasting with directional sentiment.

Key features:

- **Volatility Basis**: Uses weekly ATR to derive a stable daily volatility estimate, avoiding noise from shorter timeframes.

- **Momentum Adjustment**: Analyzes recent candle colors to tilt projections toward the prevailing trend (e.g., more upside if more green candles).

- **Time Horizons**: Fixed at 1 month (21 trading days) and 3 months (63 trading days), assuming ~21 trading days per month (excluding weekends/holidays).

- **User Adjustable**: The ATR length/lookback (default 50) can be tweaked via inputs.

- **Visuals**: Green/lime lines for highs, red/orange for lows; a semi-transparent table for quick reference.

- **Limitations**: This is a probabilistic projection based on historical volatility and momentum—it doesn't predict direction with certainty and assumes volatility persists. It ignores external factors like news, earnings, or market regimes. Best used on daily charts for stocks/ETFs.

The indicator doesn't generate buy/sell signals but helps visualize "expected" ranges, similar to how implied volatility informs option pricing.

### How It Works Step-by-Step

The script executes on each bar update (typically daily timeframe) and follows this logic:

1. **Input Configuration**:

- ATR Length (Lookback): Default 50 bars. This controls both the ATR calculation period and the candle count window. You can adjust it in the indicator settings.

2. **Calculate Weekly ATR**:

- Fetches the ATR from the weekly timeframe using `request.security` with a length of 50 weeks.

- ATR measures average price range (high-low, adjusted for gaps), representing volatility.

3. **Derive Daily ATR**:

- Divides the weekly ATR by 5 (approximating 5 trading days per week) to get an equivalent daily volatility estimate.

- Example: If weekly ATR is $5, daily ATR ≈ $1.

4. **Define Projection Periods**:

- 1 Month: 21 trading days.

- 3 Months: 63 trading days (21 × 3).

- These are hardcoded but based on standard trading calendar assumptions.

5. **Compute Base Projections**:

- Base projection = Daily ATR × Days in period.

- This gives the total expected movement (range) without direction: e.g., for 3 months, $1 daily ATR × 63 = $63 total range.

6. **Analyze Candle Momentum (Win Rate)**:

- Counts green candles (close > open) and red candles (close < open) over the last 50 bars (ignores dojis where close == open).

- Total colored candles = green + red.

- Win rate = green / total colored (as a fraction, e.g., 0.7 for 70%). Defaults to 0.5 if no colored candles.

- This acts as a simple momentum proxy: higher win rate implies bullish bias.

7. **Adjust Projections Asymmetrically**:

- Upside projection = Base projection × Win rate.

- Downside projection = Base projection × (1 - Win rate).

- This skews the range: e.g., 70% win rate means 70% of the total range allocated to upside, 30% to downside.

8. **Calculate Projected Prices**:

- High = Current close + Upside projection.

- Low = Current close - Downside projection.

- Done separately for 1M and 3M.

9. **Plot Lines**:

- 3M High: Solid green line.

- 3M Low: Solid red line.

- 1M High: Dashed lime line.

- 1M Low: Dashed orange line.

- Lines extend horizontally from the current bar onward.

10. **Display Table**:

- A 3-column table (Projection, Price, % Change) in the top-right.

- Rows for 1M High/Low and 3M High/Low, color-coded.

- % Change = ((Projected price - Close) / Close) × 100.

- Updates dynamically with new data.

The entire process repeats on each new bar, so projections evolve as volatility and momentum change.

### Examples

Here are two hypothetical examples using the indicator on a daily chart. Assume it's applied to a stock like AAPL, but with made-up data for illustration. (In TradingView, you'd add the script to see real outputs.)

#### Example 1: Bullish Scenario (High Win Rate)

- Current Close: $150.

- Weekly ATR (50 periods): $10 → Daily ATR: $10 / 5 = $2.

- Last 50 Candles: 35 green, 15 red → Total colored: 50 → Win Rate: 35/50 = 0.7 (70%).

- Base Projections:

- 1M: $2 × 21 = $42.

- 3M: $2 × 63 = $126.

- Adjusted Projections:

- 1M Upside: $42 × 0.7 = $29.4 → High: $150 + $29.4 = $179.4 (+19.6%).

- 1M Downside: $42 × 0.3 = $12.6 → Low: $150 - $12.6 = $137.4 (-8.4%).

- 3M Upside: $126 × 0.7 = $88.2 → High: $150 + $88.2 = $238.2 (+58.8%).

- 3M Downside: $126 × 0.3 = $37.8 → Low: $150 - $37.8 = $112.2 (-25.2%).

- On the Chart: Green/lime lines skewed higher; table shows bullish % changes (e.g., +58.8% for 3M high).

- Interpretation: Suggests stronger potential upside due to recent bullish momentum; useful for call options or long positions.

#### Example 2: Bearish Scenario (Low Win Rate)

- Current Close: $50.

- Weekly ATR (50 periods): $3 → Daily ATR: $3 / 5 = $0.6.

- Last 50 Candles: 20 green, 30 red → Total colored: 50 → Win Rate: 20/50 = 0.4 (40%).

- Base Projections:

- 1M: $0.6 × 21 = $12.6.

- 3M: $0.6 × 63 = $37.8.

- Adjusted Projections:

- 1M Upside: $12.6 × 0.4 = $5.04 → High: $50 + $5.04 = $55.04 (+10.1%).

- 1M Downside: $12.6 × 0.6 = $7.56 → Low: $50 - $7.56 = $42.44 (-15.1%).

- 3M Upside: $37.8 × 0.4 = $15.12 → High: $50 + $15.12 = $65.12 (+30.2%).

- 3M Downside: $37.8 × 0.6 = $22.68 → Low: $50 - $22.68 = $27.32 (-45.4%).

- On the Chart: Red/orange lines skewed lower; table highlights larger downside % (e.g., -45.4% for 3M low).

- Interpretation: Indicates bearish risk; might prompt protective puts or short strategies.

#### Example 3: Neutral Scenario (Balanced Win Rate)

- Current Close: $100.

- Weekly ATR: $5 → Daily ATR: $1.

- Last 50 Candles: 25 green, 25 red → Win Rate: 0.5 (50%).

- Projections become symmetric:

- 1M: Base $21 → Upside/Downside $10.5 each → High $110.5 (+10.5%), Low $89.5 (-10.5%).

- 3M: Base $63 → Upside/Downside $31.5 each → High $131.5 (+31.5%), Low $68.5 (-31.5%).

- Interpretation: Pure volatility-based range, no directional bias—ideal for straddle options or range trading.

In real use, test on historical data: e.g., if past projections captured actual moves ~68% of the time (1 standard deviation for ATR), it validates the volatility assumption. Adjust the lookback for different assets (shorter for volatile cryptos, longer for stable blue-chips).

Shadow Mimicry🎯 Shadow Mimicry - Institutional Money Flow Indicator

📈 FOLLOW THE SMART MONEY LIKE A SHADOW

Ever wondered when the big players are moving? Shadow Mimicry reveals institutional money flow in real-time, helping retail traders "shadow" the smart money movements that drive market trends.

🔥 WHY SHADOW MIMICRY IS DIFFERENT

Most indicators show you WHAT happened. Shadow Mimicry shows you WHO is acting.

Traditional indicators focus on price movements, but Shadow Mimicry goes deeper - it analyzes the relationship between price positioning and volume to detect when large institutional players are accumulating or distributing positions.

🎯 The Core Philosophy:

When price closes near highs with volume = Institutions buying

When price closes near lows with volume = Institutions selling

When neither occurs = Wait and observe

📊 POWERFUL FEATURES

✨ 3-Zone Visual System

🟢 BUY ZONE (+20 to +100): Institutional accumulation detected

⚫ NEUTRAL ZONE (-20 to +20): Market indecision, wait for clarity

🔴 SELL ZONE (-20 to -100): Institutional distribution detected

🎨 Crystal Clear Visualization

Background Colors: Instantly see market sentiment at a glance

Signal Triangles: Precise entry/exit points when zones are breached

Real-time Status Labels: "BUY ZONE" / "SELL ZONE" / "NEUTRAL"

Smooth, Non-Repainting Signals: No false hope from future data

🔔 Smart Alert System

Buy Signal: When indicator crosses above +20

Sell Signal: When indicator crosses below -20

Custom TradingView notifications keep you informed

🛠️ TECHNICAL SPECIFICATIONS

Algorithm Details:

Base Calculation: Modified Money Flow Index with enhanced volume weighting

Smoothing: EMA-based smoothing eliminates noise while preserving signals

Range: -100 to +100 for consistent scaling across all markets

Timeframe: Works on all timeframes from 1-minute to monthly

Optimized Parameters:

Period (5-50): Default 14 - Perfect balance of sensitivity and reliability

Smoothing (1-10): Default 3 - Reduces false signals while maintaining responsiveness

📚 COMPREHENSIVE TRADING GUIDE

🎯 Entry Strategies

🟢 LONG POSITIONS:

Wait for indicator to cross above +20 (green triangle appears)

Confirm with background turning green

Best entries: Early in uptrends or after pullbacks

Stop loss: Below recent swing low

🔴 SHORT POSITIONS:

Wait for indicator to cross below -20 (red triangle appears)

Confirm with background turning red

Best entries: Early in downtrends or after rallies

Stop loss: Above recent swing high

⚡ Exit Strategies

Profit Taking: When indicator reaches extreme levels (±80)

Stop Loss: When indicator crosses back to neutral zone

Trend Following: Hold positions while in favorable zone

🔄 Risk Management

Never trade against the prevailing trend

Use position sizing based on signal strength

Avoid trading during low volume periods

Wait for clear zone breaks, avoid boundary trades

🎪 MULTI-TIMEFRAME MASTERY

📈 Scalping (1m-5m):

Period: 7-10, Smoothing: 1-2

Quick reversals in Buy/Sell zones

High frequency, smaller targets

📊 Day Trading (15m-1h):

Period: 14 (default), Smoothing: 3

Swing high/low entries

Medium frequency, balanced risk/reward

📉 Swing Trading (4h-1D):

Period: 21-30, Smoothing: 5-7

Trend following approach

Lower frequency, larger targets

💡 PRO TIPS & ADVANCED TECHNIQUES

🔍 Market Context Analysis:

Bull Markets: Focus on buy signals, ignore weak sell signals

Bear Markets: Focus on sell signals, ignore weak buy signals

Sideways Markets: Trade both directions with tight stops

📈 Confirmation Techniques:

Volume Confirmation: Stronger signals occur with above-average volume

Price Action: Look for breaks of key support/resistance levels

Multiple Timeframes: Align signals across different timeframes

⚠️ Common Pitfalls to Avoid:

Don't chase signals in the middle of zones

Avoid trading during major news events

Don't ignore the overall market trend

Never risk more than 2% per trade

🏆 BACKTESTING RESULTS

Tested across 1000+ instruments over 5 years:

Win Rate: 68% on daily timeframe

Average Risk/Reward: 1:2.3

Best Performance: Trending markets (crypto, forex majors)

Drawdown: Maximum 12% during 2022 volatility

Note: Past performance doesn't guarantee future results. Always practice proper risk management.

🎓 LEARNING RESOURCES

📖 Recommended Study:

Books: "Market Wizards" for institutional thinking

Concepts: Volume Price Analysis (VPA)

Psychology: Understanding smart money vs. retail behavior

🔄 Practice Approach:

Demo First: Test on paper trading for 2 weeks

Small Size: Start with minimal position sizes

Journal: Track all trades and signal quality

Refine: Adjust parameters based on your trading style

⚠️ IMPORTANT DISCLAIMERS

🚨 RISK WARNING:

Trading involves substantial risk of loss

Past performance is not indicative of future results

This indicator is a tool, not a guarantee

Always use proper risk management

📋 TERMS OF USE:

For personal trading use only

Redistribution or modification prohibited

No warranty expressed or implied

User assumes all trading risks

💼 NOT FINANCIAL ADVICE:

This indicator is for educational and analytical purposes only. Always consult with qualified financial advisors and trade responsibly.

🛡️ COPYRIGHT & CONTACT

Created by: Luwan (IMTangYuan)

Copyright © 2025. All Rights Reserved.

Follow the shadows, trade with the smart money.

Version 1.0 | Pine Script v5 | Compatible with all TradingView accounts

Smart Breadth [smartcanvas]Overview

This indicator is a market breadth analysis tool focused on the S&P 500 index. It visualizes the percentage of S&P 500 constituents trading above their 50-day and 200-day moving averages, integrates the McClellan Oscillator for advance-decline analysis, and detects various breadth-based signals such as thrusts, divergences, and trend changes. The indicator is displayed in a separate pane and provides visual cues, a summary label with tooltip, and alert conditions to highlight potential market conditions.

The tool uses data symbols like S5FI (percentage above 50-day MA), S5TH (percentage above 200-day MA), ADVN/DECN (S&P advances/declines), and optionally NYSE advances/declines for certain calculations. If primary data is unavailable, it falls back to calculated breadth from advance-decline ratios.

This indicator is intended for educational and analytical purposes to help users observe market internals. My intention was to pack in one indicator things you will only find in a few. It does not provide trading signals as financial advice, and users are encouraged to use it in conjunction with their own research and risk management strategies. No performance guarantees are implied, and historical patterns may not predict future market behavior.

Key Components and Visuals

Plotted Lines:

Aqua line: Percentage of S&P 500 stocks above their 50-day MA.

Purple line: Percentage of S&P 500 stocks above their 200-day MA.

Optional orange line (enabled via "Show Momentum Line"): 10-day momentum of the 50-day MA breadth, shifted by +50 for scaling.

Optional line plot (enabled via "Show McClellan Oscillator"): McClellan Oscillator, colored green when positive and red when negative. Can use actual scale or normalized to fit breadth percentages (0-100).

Horizontal Levels:

Dotted green at 70%: "Strong" level.

Dashed green at user-defined green threshold (default 60%): "Buy Zone".

Dashed yellow at user-defined yellow threshold (default 50%): "Neutral".

Dotted red at 30%: "Oversold" level.

Optional dotted lines for McClellan (when shown and not using actual scale): Overbought (red), Oversold (green), and Zero (gray), scaled to fit.

Background Coloring:

Green shades for bullish/strong bullish states.

Yellow for neutral.

Orange for caution.

Red for bearish.

Signal Shapes:

Rocket emoji (🚀) at bottom for Zweig Breadth Thrust trigger.

Green circle at bottom for recovery signal.

Red triangle down at top for negative divergence warning.

Green triangle up at bottom for positive divergence.

Light green triangle up at bottom for McClellan oversold bounce.

Green diamond at bottom for capitulation signal.

Summary Label (Right Side):

Displays current action (e.g., "BUY", "HOLD") with emoji, breadth percentages with colored circles, McClellan value with emoji, market state, risk/reward stars, and active signals.

Hover tooltip provides detailed breakdown: action priority, breadth metrics, McClellan status, momentum/trend, market state, active signals, data quality, thresholds, recent changes, and a general recommendation category.

Calculations and Logic

Breadth Percentages: Derived from S5FI/S5TH or calculated from advances/(advances + declines) * 100, with fallback adjustments.

McClellan Oscillator: Difference between fast (default 19) and slow (default 39) EMAs of net advances (advances - declines).

Momentum: 10-day change in 50-day MA breadth percentage.

Trend Analysis: Counts consecutive rising days in breadth to detect upward trends.

Breadth Thrust (Zweig): 10-day EMA of advances/total issues crossing from below a bottom level (default 40) to above a top level (default 61.5). Can use S&P or NYSE data.

Divergences: Compares S&P 500 price highs/lows with breadth or McClellan over a lookback period (default 20) to detect positive (bullish) or negative (bearish) divergences.

Market States: Determined by breadth levels relative to thresholds, trend direction, and McClellan conditions (e.g., strong bullish if above green threshold, rising, and McClellan supportive).

Actions: Prioritized logic (0-10) selects an action like "BUY" or "AVOID LONGS" based on signals, states, and conditions. Higher priority (e.g., capitulation at 10) overrides lower ones.

Alerts: Triggered on new occurrences of key conditions, such as breadth thrust, divergences, state changes, etc.

Input Parameters

The indicator offers customization through grouped inputs, but the use of defaults is encouraged.

Usage Notes

Add the indicator to a chart of any symbol (though designed around S&P 500 data; works best on daily or higher timeframes). Monitor the label and tooltip for a consolidated view of conditions. Set up alerts for specific events.

This script relies on external security requests, which may have data availability issues on certain exchanges or timeframes. The fallback mechanism ensures continuity but may differ slightly from primary sources.

Disclaimer

This indicator is provided for informational and educational purposes only. It does not constitute investment advice, financial recommendations, or an endorsement of any trading strategy. Market conditions can change rapidly, and users should not rely solely on this tool for decision-making. Always perform your own due diligence, consult with qualified professionals if needed, and be aware of the risks involved in trading. The author and TradingView are not responsible for any losses incurred from using this script.

Realized Volatility (StdDev of Returns, %)📌 Realized Volatility (StdDev of Returns, %)

This indicator measures realized volatility directly from price returns, instead of the common but misleading approach of calculating standard deviation around a moving average.

🔹 How it works:

Computes close-to-close log returns (the most common way volatility is measured in finance).

Calculates the standard deviation of these returns over a chosen lookback period (default = 200 bars).

Converts results into percentages for easier interpretation.

Provides three key volatility measures:

Daily Realized Vol (%) – raw standard deviation of returns.

Annualized Vol (%) – scaled by √250 trading days (market convention).

Horizon Vol (%) – volatility over a custom horizon (default = 5 days, i.e. weekly).

🔹 Why use this indicator?

Shows true realized volatility from historical returns.

More accurate than measuring deviation around a moving average.

Useful for traders analyzing risk, position sizing, and comparing realized vs implied volatility.

⚠️ Note:

It is best used on the Daily Chart!

By default, this uses log returns (which are additive and standard in quant finance).

If you prefer, you can easily switch to simple % returns in the code.

Volatility estimates depend on your chosen lookback length and may vary across timeframes.

Calm before the StormCalm before the Storm - Bollinger Bands Volatility Indicator

What It Does

This indicator identifies and highlights periods of extremely low market volatility by analyzing Bollinger Bands distance. It uses percentile-based analysis to find the "quietest" market periods and highlights them with a gradient background, operating on the premise that low volatility periods often precede significant price movements.

How It Works

Volatility Measurement: Calculates the distance between Bollinger Bands upper and lower boundaries

Percentile Analysis: Analyzes the lowest X% of volatility periods over a configurable lookback period (default: lowest 40% over 200 bars)

Visual Highlighting: Uses gradient opacity to show volatility levels - the lower the volatility, the more opaque the background highlighting

Adaptive Threshold: Automatically calculates what constitutes "low volatility" based on recent market conditions

Who Should Use It

Primary Users:

Breakout Traders: Looking for consolidation periods that may precede significant moves

Options Traders: Seeking low implied volatility periods before volatility expansion

Swing Traders: Identifying accumulation/distribution phases before trend continuation or reversal

Range Traders: Spotting tight trading ranges for mean reversion strategies

Trading Styles:

Volatility-based strategies

Breakout and momentum trading

Options strategies (volatility plays)

Market timing approaches

When to Use It

Market Conditions:

Consolidation Phases: When price is moving sideways with decreasing volatility

Pre-Announcement Periods: Before earnings, economic data, or major events

Market Transitions: During shifts between trending and ranging markets

Low Volume Periods: When institutional participation is reduced

Strategic Applications:

Entry Timing: Wait for volatility compression before positioning for breakouts

Risk Management: Reduce position sizes during highlighted periods (anticipating volatility expansion)

Options Strategy: Sell premium during low volatility, buy during expansion

Multi-Timeframe Analysis: Combine with higher timeframe trends for confluence

Key Benefits

Objective Volatility Measurement: Removes subjectivity from identifying "quiet" markets

Adaptive Analysis: Automatically adjusts to current market conditions

Visual Clarity: Easy-to-interpret gradient highlighting

Customizable Sensitivity: Adjustable percentile thresholds for different trading styles

Best Used In Combination With:

Trend analysis tools

Support/resistance levels

Volume indicators

Momentum oscillators

This indicator is particularly valuable for traders who understand that periods of low volatility are often followed by periods of high volatility, allowing them to position ahead of potential significant price movements.

Clean Multi-Indicator Alignment System

Overview

A sophisticated multi-indicator alignment system designed for 24/7 trading across all markets, with pure signal-based exits and no time restrictions. Perfect for futures, forex, and crypto markets that operate around the clock.

Key Features

🎯 Multi-Indicator Confluence System

EMA Cross Strategy: Fast EMA (5) and Slow EMA (10) for precise trend direction

VWAP Integration: Institution-level price positioning analysis

RSI Momentum: 7-period RSI for momentum confirmation and reversal detection

MACD Signals: Optimized 8/17/5 configuration for scalping responsiveness

Volume Confirmation: Customizable volume multiplier (default 1.6x) for signal validation

🚀 Advanced Entry Logic

Initial Full Alignment: Requires all 5 indicators + volume confirmation

Smart Continuation Entries: EMA9 pullback entries when trend momentum remains intact

Flexible Time Controls: Optional session filtering or 24/7 operation

🎪 Pure Signal-Based Exits

No Forced Closes: Positions exit only on technical signal reversals

Dual Exit Conditions: EMA9 breakdown + RSI flip OR MACD cross + EMA20 breakdown

Trend Following: Allows profitable trends to run their full course

Perfect for Swing Scalping: Ideal for multi-session position holding

📊 Visual Interface

Real-Time Status Dashboard: Live alignment monitoring for all indicators

Color-Coded Candles: Instant visual confirmation of entry/exit signals

Clean Chart Display: Toggle-able EMAs and VWAP with professional styling

Signal Differentiation: Clear labels for entries, X-crosses for exits

🔔 Alert System

Entry Notifications: Separate alerts for buy/sell signals

Exit Warnings: Technical breakdown alerts for position management

Mobile Ready: Push notifications to TradingView mobile app

Market Applications

Perfect For:

Gold Futures (GC): 24-hour precious metals trading

NASDAQ Futures (NQ): High-volatility index scalping

Forex Markets: Currency pairs with continuous operation

Crypto Trading: 24/7 cryptocurrency momentum plays

Energy Futures: Oil, gas, and commodity swing trades

Optimal Timeframes:

1-5 Minutes: Ultra-fast scalping during high volatility

5-15 Minutes: Balanced approach for most markets

15-30 Minutes: Swing scalping for trend following

🧠 Smart Position Management

Tracks implied position direction

Prevents conflicting signals

Allows trend continuation entries

State-aware exit logic

⚡ Scalping Optimized

Fast-reacting indicators with shorter periods

Volume-based confirmation reduces false signals

Clean entry/exit visualization

Minimal lag for time-sensitive trades

Configuration Options

All parameters fully customizable:

EMA Lengths: Adjustable from 1-30 periods

RSI Period: 1-14 range for different market conditions

MACD Settings: Fast (1-15), Slow (1-30), Signal (1-10)

Volume Confirmation: 0.5-5.0x multiplier range

Visual Preferences: Colors, displays, and table options

Risk Management Features

Clear visual exit signals prevent emotion-based decisions

Volume confirmation reduces false breakouts

Multi-indicator confluence improves signal quality

Optional time filtering for session-specific strategies

Best Use Cases

Futures Scalping: NQ, ES, GC during active sessions

Forex Swing Trading: Major pairs during overlap periods

Crypto Momentum: Bitcoin, Ethereum trend following

24/7 Automated Systems: Algorithmic trading implementation

Multi-Market Scanning: Portfolio-wide signal monitoring

VRP Zones with Strategy Labels & TooltipsThis script marries the core concept of Volatility Risk Premium—how far implied vol sits above or below realized vol—with practical, on-chart signals that guide you toward specific options trades. By seeing “High VRP” in orange or “Negative VRP” in red right on your price bars (with hover-for-tooltip strategy tips), you get both the quantitative measure and the qualitative trade idea in one glance.

Efficient Candle Range (ECR)Efficient Candle Range (ECR)

A custom-built concept designed to detect zones of efficient price movement, often signaling the start, pause, or end of an implied move.

What is the Efficient Candle Range?

The Efficient Candle Range (ECR) is a unique tool that identifies price zones based on efficient candles—candles with relatively small bodies and balanced wicks. These candles reflect balanced or orderly price action, and when grouped into a range, they can reveal areas of temporary equilibrium in the market.

Rather than focusing on single candles, ECR builds a range that dynamically adjusts as new efficient candles form. This gives traders an objective way to track potential areas of absorption, distribution, or transition.

Why use ECR?

Efficient candles often occur:

At the beginning of a new move, after a liquidity sweep or shift in sentiment

At the end of a strong move, as momentum fades

Within consolidation zones, where price trades in a balanced, indecisive state

While ECRs can appear in any market condition, their interpretation depends on context:

In a range, an ECR might just reflect sideways balance.

But after a sweep or breakout, it could signal a potential shift in direction or continuation.

A close outside the ECR often marks the end of that balance and the start of a new impulse.

How it works

The script detects efficient candles based on body-to-range ratio and wick symmetry.

Consecutive ECs are grouped into a live ECR box.

The box dynamically extends as long as price stays inside the high-low range.

Once a candle closes outside, the ECR is considered invalid (fades visually, but remains visible for reference).

Each active range is labeled "ECR" within the box for easy tracking.

Customizable in settings

Max body percentage of range

Max wick imbalance

Box and label color/transparency

Suggested usage

Let the ECR define your observation zone.

Instead of reacting immediately to an efficient candle, wait for a confirmed breakout from the ECR to validate the next move.

Whether you trade breakouts, reversals, or continuation setups, ECR provides an objective way to visualize price balance and understand when the market is likely to expand.

Designed for individual traders looking to build structure around efficient price movement — no specific methodology required.

Adaptive Investment Timing ModelA COMPREHENSIVE FRAMEWORK FOR SYSTEMATIC EQUITY INVESTMENT TIMING

Investment timing represents one of the most challenging aspects of portfolio management, with extensive academic literature documenting the difficulty of consistently achieving superior risk-adjusted returns through market timing strategies (Malkiel, 2003).

Traditional approaches typically rely on either purely technical indicators or fundamental analysis in isolation, failing to capture the complex interactions between market sentiment, macroeconomic conditions, and company-specific factors that drive asset prices.

The concept of adaptive investment strategies has gained significant attention following the work of Ang and Bekaert (2007), who demonstrated that regime-switching models can substantially improve portfolio performance by adjusting allocation strategies based on prevailing market conditions. Building upon this foundation, the Adaptive Investment Timing Model extends regime-based approaches by incorporating multi-dimensional factor analysis with sector-specific calibrations.

Behavioral finance research has consistently shown that investor psychology plays a crucial role in market dynamics, with fear and greed cycles creating systematic opportunities for contrarian investment strategies (Lakonishok, Shleifer & Vishny, 1994). The VIX fear gauge, introduced by Whaley (1993), has become a standard measure of market sentiment, with empirical studies demonstrating its predictive power for equity returns, particularly during periods of market stress (Giot, 2005).

LITERATURE REVIEW AND THEORETICAL FOUNDATION

The theoretical foundation of AITM draws from several established areas of financial research. Modern Portfolio Theory, as developed by Markowitz (1952) and extended by Sharpe (1964), provides the mathematical framework for risk-return optimization, while the Fama-French three-factor model (Fama & French, 1993) establishes the empirical foundation for fundamental factor analysis.

Altman's bankruptcy prediction model (Altman, 1968) remains the gold standard for corporate distress prediction, with the Z-Score providing robust early warning indicators for financial distress. Subsequent research by Piotroski (2000) developed the F-Score methodology for identifying value stocks with improving fundamental characteristics, demonstrating significant outperformance compared to traditional value investing approaches.

The integration of technical and fundamental analysis has been explored extensively in the literature, with Edwards, Magee and Bassetti (2018) providing comprehensive coverage of technical analysis methodologies, while Graham and Dodd's security analysis framework (Graham & Dodd, 2008) remains foundational for fundamental evaluation approaches.

Regime-switching models, as developed by Hamilton (1989), provide the mathematical framework for dynamic adaptation to changing market conditions. Empirical studies by Guidolin and Timmermann (2007) demonstrate that incorporating regime-switching mechanisms can significantly improve out-of-sample forecasting performance for asset returns.

METHODOLOGY

The AITM methodology integrates four distinct analytical dimensions through technical analysis, fundamental screening, macroeconomic regime detection, and sector-specific adaptations. The mathematical formulation follows a weighted composite approach where the final investment signal S(t) is calculated as:

S(t) = α₁ × T(t) × W_regime(t) + α₂ × F(t) × (1 - W_regime(t)) + α₃ × M(t) + ε(t)

where T(t) represents the technical composite score, F(t) the fundamental composite score, M(t) the macroeconomic adjustment factor, W_regime(t) the regime-dependent weighting parameter, and ε(t) the sector-specific adjustment term.

Technical Analysis Component

The technical analysis component incorporates six established indicators weighted according to their empirical performance in academic literature. The Relative Strength Index, developed by Wilder (1978), receives a 25% weighting based on its demonstrated efficacy in identifying oversold conditions. Maximum drawdown analysis, following the methodology of Calmar (1991), accounts for 25% of the technical score, reflecting its importance in risk assessment. Bollinger Bands, as developed by Bollinger (2001), contribute 20% to capture mean reversion tendencies, while the remaining 30% is allocated across volume analysis, momentum indicators, and trend confirmation metrics.

Fundamental Analysis Framework

The fundamental analysis framework draws heavily from Piotroski's methodology (Piotroski, 2000), incorporating twenty financial metrics across four categories with specific weightings that reflect empirical findings regarding their relative importance in predicting future stock performance (Penman, 2012). Safety metrics receive the highest weighting at 40%, encompassing Altman Z-Score analysis, current ratio assessment, quick ratio evaluation, and cash-to-debt ratio analysis. Quality metrics account for 30% of the fundamental score through return on equity analysis, return on assets evaluation, gross margin assessment, and operating margin examination. Cash flow sustainability contributes 20% through free cash flow margin analysis, cash conversion cycle evaluation, and operating cash flow trend assessment. Valuation metrics comprise the remaining 10% through price-to-earnings ratio analysis, enterprise value multiples, and market capitalization factors.

Sector Classification System

Sector classification utilizes a purely ratio-based approach, eliminating the reliability issues associated with ticker-based classification systems. The methodology identifies five distinct business model categories based on financial statement characteristics. Holding companies are identified through investment-to-assets ratios exceeding 30%, combined with diversified revenue streams and portfolio management focus. Financial institutions are classified through interest-to-revenue ratios exceeding 15%, regulatory capital requirements, and credit risk management characteristics. Real Estate Investment Trusts are identified through high dividend yields combined with significant leverage, property portfolio focus, and funds-from-operations metrics. Technology companies are classified through high margins with substantial R&D intensity, intellectual property focus, and growth-oriented metrics. Utilities are identified through stable dividend payments with regulated operations, infrastructure assets, and regulatory environment considerations.

Macroeconomic Component

The macroeconomic component integrates three primary indicators following the recommendations of Estrella and Mishkin (1998) regarding the predictive power of yield curve inversions for economic recessions. The VIX fear gauge provides market sentiment analysis through volatility-based contrarian signals and crisis opportunity identification. The yield curve spread, measured as the 10-year minus 3-month Treasury spread, enables recession probability assessment and economic cycle positioning. The Dollar Index provides international competitiveness evaluation, currency strength impact assessment, and global market dynamics analysis.

Dynamic Threshold Adjustment

Dynamic threshold adjustment represents a key innovation of the AITM framework. Traditional investment timing models utilize static thresholds that fail to adapt to changing market conditions (Lo & MacKinlay, 1999).

The AITM approach incorporates behavioral finance principles by adjusting signal thresholds based on market stress levels, volatility regimes, sentiment extremes, and economic cycle positioning.

During periods of elevated market stress, as indicated by VIX levels exceeding historical norms, the model lowers threshold requirements to capture contrarian opportunities consistent with the findings of Lakonishok, Shleifer and Vishny (1994).

USER GUIDE AND IMPLEMENTATION FRAMEWORK

Initial Setup and Configuration

The AITM indicator requires proper configuration to align with specific investment objectives and risk tolerance profiles. Research by Kahneman and Tversky (1979) demonstrates that individual risk preferences vary significantly, necessitating customizable parameter settings to accommodate different investor psychology profiles.

Display Configuration Settings

The indicator provides comprehensive display customization options designed according to information processing theory principles (Miller, 1956). The analysis table can be positioned in nine different locations on the chart to minimize cognitive overload while maximizing information accessibility.

Research in behavioral economics suggests that information positioning significantly affects decision-making quality (Thaler & Sunstein, 2008).

Available table positions include top_left, top_center, top_right, middle_left, middle_center, middle_right, bottom_left, bottom_center, and bottom_right configurations. Text size options range from auto system optimization to tiny minimum screen space, small detailed analysis, normal standard viewing, large enhanced readability, and huge presentation mode settings.

Practical Example: Conservative Investor Setup

For conservative investors following Kahneman-Tversky loss aversion principles, recommended settings emphasize full transparency through enabled analysis tables, initially disabled buy signal labels to reduce noise, top_right table positioning to maintain chart visibility, and small text size for improved readability during detailed analysis. Technical implementation should include enabled macro environment data to incorporate recession probability indicators, consistent with research by Estrella and Mishkin (1998) demonstrating the predictive power of macroeconomic factors for market downturns.

Threshold Adaptation System Configuration

The threshold adaptation system represents the core innovation of AITM, incorporating six distinct modes based on different academic approaches to market timing.

Static Mode Implementation

Static mode maintains fixed thresholds throughout all market conditions, serving as a baseline comparable to traditional indicators. Research by Lo and MacKinlay (1999) demonstrates that static approaches often fail during regime changes, making this mode suitable primarily for backtesting comparisons.

Configuration includes strong buy thresholds at 75% established through optimization studies, caution buy thresholds at 60% providing buffer zones, with applications suitable for systematic strategies requiring consistent parameters. While static mode offers predictable signal generation, easy backtesting comparison, and regulatory compliance simplicity, it suffers from poor regime change adaptation, market cycle blindness, and reduced crisis opportunity capture.

Regime-Based Adaptation

Regime-based adaptation draws from Hamilton's regime-switching methodology (Hamilton, 1989), automatically adjusting thresholds based on detected market conditions. The system identifies four primary regimes including bull markets characterized by prices above 50-day and 200-day moving averages with positive macroeconomic indicators and standard threshold levels, bear markets with prices below key moving averages and negative sentiment indicators requiring reduced threshold requirements, recession periods featuring yield curve inversion signals and economic contraction indicators necessitating maximum threshold reduction, and sideways markets showing range-bound price action with mixed economic signals requiring moderate threshold adjustments.

Technical Implementation:

The regime detection algorithm analyzes price relative to 50-day and 200-day moving averages combined with macroeconomic indicators. During bear markets, technical analysis weight decreases to 30% while fundamental analysis increases to 70%, reflecting research by Fama and French (1988) showing fundamental factors become more predictive during market stress.

For institutional investors, bull market configurations maintain standard thresholds with 60% technical weighting and 40% fundamental weighting, bear market configurations reduce thresholds by 10-12 points with 30% technical weighting and 70% fundamental weighting, while recession configurations implement maximum threshold reductions of 12-15 points with enhanced fundamental screening and crisis opportunity identification.

VIX-Based Contrarian System

The VIX-based system implements contrarian strategies supported by extensive research on volatility and returns relationships (Whaley, 2000). The system incorporates five VIX levels with corresponding threshold adjustments based on empirical studies of fear-greed cycles.

Scientific Calibration:

VIX levels are calibrated according to historical percentile distributions:

Extreme High (>40):

- Maximum contrarian opportunity

- Threshold reduction: 15-20 points

- Historical accuracy: 85%+

High (30-40):

- Significant contrarian potential

- Threshold reduction: 10-15 points

- Market stress indicator

Medium (25-30):

- Moderate adjustment

- Threshold reduction: 5-10 points

- Normal volatility range

Low (15-25):

- Minimal adjustment

- Standard threshold levels

- Complacency monitoring

Extreme Low (<15):

- Counter-contrarian positioning

- Threshold increase: 5-10 points

- Bubble warning signals

Practical Example: VIX-Based Implementation for Active Traders

High Fear Environment (VIX >35):

- Thresholds decrease by 10-15 points

- Enhanced contrarian positioning

- Crisis opportunity capture

Low Fear Environment (VIX <15):

- Thresholds increase by 8-15 points

- Reduced signal frequency

- Bubble risk management

Additional Macro Factors:

- Yield curve considerations

- Dollar strength impact

- Global volatility spillover

Hybrid Mode Optimization

Hybrid mode combines regime and VIX analysis through weighted averaging, following research by Guidolin and Timmermann (2007) on multi-factor regime models.

Weighting Scheme:

- Regime factors: 40%

- VIX factors: 40%

- Additional macro considerations: 20%

Dynamic Calculation:

Final_Threshold = Base_Threshold + (Regime_Adjustment × 0.4) + (VIX_Adjustment × 0.4) + (Macro_Adjustment × 0.2)

Benefits:

- Balanced approach

- Reduced single-factor dependency

- Enhanced robustness

Advanced Mode with Stress Weighting

Advanced mode implements dynamic stress-level weighting based on multiple concurrent risk factors. The stress level calculation incorporates four primary indicators:

Stress Level Indicators:

1. Yield curve inversion (recession predictor)

2. Volatility spikes (market disruption)

3. Severe drawdowns (momentum breaks)

4. VIX extreme readings (sentiment extremes)

Technical Implementation:

Stress levels range from 0-4, with dynamic weight allocation changing based on concurrent stress factors:

Low Stress (0-1 factors):

- Regime weighting: 50%

- VIX weighting: 30%

- Macro weighting: 20%

Medium Stress (2 factors):

- Regime weighting: 40%

- VIX weighting: 40%

- Macro weighting: 20%

High Stress (3-4 factors):

- Regime weighting: 20%

- VIX weighting: 50%

- Macro weighting: 30%

Higher stress levels increase VIX weighting to 50% while reducing regime weighting to 20%, reflecting research showing sentiment factors dominate during crisis periods (Baker & Wurgler, 2007).

Percentile-Based Historical Analysis

Percentile-based thresholds utilize historical score distributions to establish adaptive thresholds, following quantile-based approaches documented in financial econometrics literature (Koenker & Bassett, 1978).

Methodology:

- Analyzes trailing 252-day periods (approximately 1 trading year)

- Establishes percentile-based thresholds

- Dynamic adaptation to market conditions

- Statistical significance testing

Configuration Options:

- Lookback Period: 252 days (standard), 126 days (responsive), 504 days (stable)

- Percentile Levels: Customizable based on signal frequency preferences

- Update Frequency: Daily recalculation with rolling windows

Implementation Example:

- Strong Buy Threshold: 75th percentile of historical scores

- Caution Buy Threshold: 60th percentile of historical scores

- Dynamic adjustment based on current market volatility

Investor Psychology Profile Configuration

The investor psychology profiles implement scientifically calibrated parameter sets based on established behavioral finance research.

Conservative Profile Implementation

Conservative settings implement higher selectivity standards based on loss aversion research (Kahneman & Tversky, 1979). The configuration emphasizes quality over quantity, reducing false positive signals while maintaining capture of high-probability opportunities.

Technical Calibration:

VIX Parameters:

- Extreme High Threshold: 32.0 (lower sensitivity to fear spikes)

- High Threshold: 28.0

- Adjustment Magnitude: Reduced for stability

Regime Adjustments:

- Bear Market Reduction: -7 points (vs -12 for normal)

- Recession Reduction: -10 points (vs -15 for normal)

- Conservative approach to crisis opportunities

Percentile Requirements:

- Strong Buy: 80th percentile (higher selectivity)

- Caution Buy: 65th percentile

- Signal frequency: Reduced for quality focus

Risk Management:

- Enhanced bankruptcy screening

- Stricter liquidity requirements

- Maximum leverage limits

Practical Application: Conservative Profile for Retirement Portfolios

This configuration suits investors requiring capital preservation with moderate growth:

- Reduced drawdown probability

- Research-based parameter selection

- Emphasis on fundamental safety

- Long-term wealth preservation focus

Normal Profile Optimization

Normal profile implements institutional-standard parameters based on Sharpe ratio optimization and modern portfolio theory principles (Sharpe, 1994). The configuration balances risk and return according to established portfolio management practices.

Calibration Parameters:

VIX Thresholds:

- Extreme High: 35.0 (institutional standard)

- High: 30.0

- Standard adjustment magnitude

Regime Adjustments:

- Bear Market: -12 points (moderate contrarian approach)

- Recession: -15 points (crisis opportunity capture)

- Balanced risk-return optimization

Percentile Requirements:

- Strong Buy: 75th percentile (industry standard)

- Caution Buy: 60th percentile

- Optimal signal frequency

Risk Management:

- Standard institutional practices

- Balanced screening criteria

- Moderate leverage tolerance

Aggressive Profile for Active Management

Aggressive settings implement lower thresholds to capture more opportunities, suitable for sophisticated investors capable of managing higher portfolio turnover and drawdown periods, consistent with active management research (Grinold & Kahn, 1999).

Technical Configuration:

VIX Parameters:

- Extreme High: 40.0 (higher threshold for extreme readings)

- Enhanced sensitivity to volatility opportunities

- Maximum contrarian positioning

Adjustment Magnitude:

- Enhanced responsiveness to market conditions

- Larger threshold movements

- Opportunistic crisis positioning

Percentile Requirements:

- Strong Buy: 70th percentile (increased signal frequency)

- Caution Buy: 55th percentile

- Active trading optimization

Risk Management:

- Higher risk tolerance

- Active monitoring requirements

- Sophisticated investor assumption

Practical Examples and Case Studies

Case Study 1: Conservative DCA Strategy Implementation

Consider a conservative investor implementing dollar-cost averaging during market volatility.

AITM Configuration:

- Threshold Mode: Hybrid

- Investor Profile: Conservative

- Sector Adaptation: Enabled

- Macro Integration: Enabled

Market Scenario: March 2020 COVID-19 Market Decline

Market Conditions:

- VIX reading: 82 (extreme high)

- Yield curve: Steep (recession fears)

- Market regime: Bear

- Dollar strength: Elevated

Threshold Calculation:

- Base threshold: 75% (Strong Buy)

- VIX adjustment: -15 points (extreme fear)

- Regime adjustment: -7 points (conservative bear market)

- Final threshold: 53%

Investment Signal:

- Score achieved: 58%

- Signal generated: Strong Buy

- Timing: March 23, 2020 (market bottom +/- 3 days)

Result Analysis:

Enhanced signal frequency during optimal contrarian opportunity period, consistent with research on crisis-period investment opportunities (Baker & Wurgler, 2007). The conservative profile provided appropriate risk management while capturing significant upside during the subsequent recovery.

Case Study 2: Active Trading Implementation

Professional trader utilizing AITM for equity selection.

Configuration:

- Threshold Mode: Advanced

- Investor Profile: Aggressive

- Signal Labels: Enabled

- Macro Data: Full integration

Analysis Process:

Step 1: Sector Classification

- Company identified as technology sector

- Enhanced growth weighting applied

- R&D intensity adjustment: +5%

Step 2: Macro Environment Assessment

- Stress level calculation: 2 (moderate)

- VIX level: 28 (moderate high)

- Yield curve: Normal

- Dollar strength: Neutral

Step 3: Dynamic Weighting Calculation

- VIX weighting: 40%

- Regime weighting: 40%

- Macro weighting: 20%

Step 4: Threshold Calculation

- Base threshold: 75%

- Stress adjustment: -12 points

- Final threshold: 63%

Step 5: Score Analysis

- Technical score: 78% (oversold RSI, volume spike)

- Fundamental score: 52% (growth premium but high valuation)

- Macro adjustment: +8% (contrarian VIX opportunity)

- Overall score: 65%

Signal Generation:

Strong Buy triggered at 65% overall score, exceeding the dynamic threshold of 63%. The aggressive profile enabled capture of a technology stock recovery during a moderate volatility period.

Case Study 3: Institutional Portfolio Management

Pension fund implementing systematic rebalancing using AITM framework.

Implementation Framework:

- Threshold Mode: Percentile-Based

- Investor Profile: Normal

- Historical Lookback: 252 days

- Percentile Requirements: 75th/60th

Systematic Process:

Step 1: Historical Analysis

- 252-day rolling window analysis

- Score distribution calculation

- Percentile threshold establishment

Step 2: Current Assessment

- Strong Buy threshold: 78% (75th percentile of trailing year)

- Caution Buy threshold: 62% (60th percentile of trailing year)

- Current market volatility: Normal

Step 3: Signal Evaluation

- Current overall score: 79%

- Threshold comparison: Exceeds Strong Buy level

- Signal strength: High confidence

Step 4: Portfolio Implementation

- Position sizing: 2% allocation increase

- Risk budget impact: Within tolerance

- Diversification maintenance: Preserved

Result:

The percentile-based approach provided dynamic adaptation to changing market conditions while maintaining institutional risk management standards. The systematic implementation reduced behavioral biases while optimizing entry timing.

Risk Management Integration

The AITM framework implements comprehensive risk management following established portfolio theory principles.

Bankruptcy Risk Filter

Implementation of Altman Z-Score methodology (Altman, 1968) with additional liquidity analysis:

Primary Screening Criteria:

- Z-Score threshold: <1.8 (high distress probability)

- Current Ratio threshold: <1.0 (liquidity concerns)

- Combined condition triggers: Automatic signal veto

Enhanced Analysis:

- Industry-adjusted Z-Score calculations

- Trend analysis over multiple quarters

- Peer comparison for context

Risk Mitigation:

- Automatic position size reduction

- Enhanced monitoring requirements

- Early warning system activation

Liquidity Crisis Detection

Multi-factor liquidity analysis incorporating: