Difference over barsDescription:

One of my followers asked about an indicator that shows the difference between the open and a previous close and didn't find one so I wrote this one. This is similar to a momentum indicator except it offers more flexibility. While the standard momentum indicator calculates a difference between current close and a previous close (sometimes customizable to work on open, high or lows instead of close), this allows to mix and match between open, high, low and close. It also offers multiple kinds of moving averages.

Settings:

Current point of reference

Previous point of reference

Difference over how many bars?

How it works:

The indicator calculates the difference between the current point of reference and a previous (n-bars back) point of reference (where n is given by the "Difference over how many bars?").

How to use it:

find historical support lines like the 0.68 line in the cart above where in the past the indicator tends to bounce back; similarly find resistance lines like the -0.75 line in the chart (which servers as a resistance line both for the main indicator line and its moving average )

look for convergence between the price and the indicator; for example, if the price is going up and the indicator is going down a change in the price direction may be coming soon

look for the indicator crossing its moving average: moving up will signify an up trend and vice-versa

since the difference between the open and previous close (which is what the blue line in the chart shows) since to go up to 0.68 (the upper horizontal line) and down to -0.75 (the lower horizontal line) most of the time, one strategy, using options, is to to buy, right before the close of a trading day, a "long iron butterfly": buy-to-open (BTO) both a call and a put at the strike price and sell-to-open (STO) a call at a strike of around $0.68 more and sell to open a put at a strike of around $0.75 less. The STO legs should be for the next expiration and the BTO legs for the next expiration after that. This way the STO will decrease their time value faster than the BTO legs if the price stays flat (which plays to your advantage) and the BTO legs may make profit if the next day it opens away from the price at which the ticker closed the previous day (when the position was opened). The most profit is when it moves right up to one of the STO legs. This position would normally be closed next day at opening. The percentage of profit it makes is low compared to other strategies but also the percentage of the total cost at risk is also low which could potentially allow a trader to increase the lot and thus, in the end, the total profit amount may be comparable to other strategies.

Notes:

The indicator in the chart above comes with the standard options. For a more standard momentum indicator set both the current and previous reference point to the same OHLC value (such as "close").

The 0.68 and -0.75 levels are for open/close (current/previous point of reference) for ticker INTC. Obviously, other tickers will likely have other levels and you will have to find those yourself. If you use INTC but use other combination of current and previous reference points, they will have different levels as well.

在脚本中搜索"one一季度财报"

Percent Calculator (Return On Investment Target Price)First and foremost: I was inspired to publish my first script after reading some of the other member's scripts -a token of my appreciation and support, Thank You.

The percent calculator is a very simple and basic indicator to use, it''s function is to simply output the target price from either the close or ones trade-entry based on a desired percent return on investment (R.O.I.).

Say you want to profit 15% from your entry: simply plug in your entry value and the number 15 into the appropriate settings and the indicator displays what the target price should be (rounded to two decimal places).

The percent calculator also goes one step further by finding the average percent return on investment over a desired interval of time (the default is 20 candles) as well as allows one to adjust the size of the price move the average percent return on investment is being calculated for.

Say you want to find the average percent return on investment for a 3 candle swing over a 200 candle interval of time: simply plug the number 200 into the interval setting and the number 3 into the price-move setting and the indicator displays what the average 3 candle swing returns on investment.

Practical Application: comparing ones desired return on investment to the average return on investment can help determine how realistic ones goals are... it's unlikely to achieve 100% return on investment if the average is only around 10% (given the parameters one is working within) but on the other hand achieving 5% return on investment is highly likely.

SIMPLE MOVING AVG 10,20,50,100,200 with RESOLUTIONThis indicator is the best than all other sma indicators.Because in just one click you can change all the resolution /time frames for all the sma .

Multitime frame analysis can be done in just one click. just change the resolution to

15 min/30 min/1hr- if you intraday trader

1D- LONG TERM INVESTORS.

Multi-timeframe analysis (MTF) is a process in which traders can view the same ticker/indicator using a higher time frame than the chart’s, for example, displaying a daily moving average on a one-hour chart in just two clicks.

How to Use this to Buy Stocks ?

The technical indicator known as the Death cross occurs when the 50-day SMA crosses below the 200-day SMA => Bearish Signal.

An opposite indicator, known as the Golden cross, occurs when the 50-day SMA crosses above the 200-day SMA => Bullish Signal.

Crossovers are one of the main moving average strategies.

1st Strategy is the first type is a price crossover, which is when the price crosses above the sma => Buy signal

when the price crosses below the sma => Sell signal

2nd Strategy is to apply two moving averages to a chart: one longer and one shorter.

When the shorter-term MA (100) crosses above the longer-term MA (200), it's a buy signal, indicates trend is shifting up.

This is known as a "Golden cross."

Meanwhile, when the shorter-term MA (100) crosses below the longer-term MA (200), it's a sell signal, indicates trend is shifting down.

This is known as a "Dead/death cross."

The time frame or length you choose for a moving average, also called the "look back period," can play a big role in how effective it is.

An MA with a short time frame will react much quicker to price changes than an MA with a long look back period. In the figure below, the 20-day moving average more closely tracks the actual price than the 100-day moving average does.

A 20-day MA = more beneficial to a shorter-term trader, since it follows the price more closely.

A 100-day MA = more beneficial to a longer-term trader.

Moving averages work quite well in strong trending conditions but poorly in choppy or ranging conditions.

use this indicator along with Price action theory and not alone.

Moving average crossovers are a popular strategy for both entries and exits. MAs can also highlight areas of potential support or resistance

Happy Trading

Bitcoin Margin Call Envelopes [saraphig & alexgrover]Bitcoin is the most well known digital currency, and allow two parties to make a transaction without the need of a central entity, this is why cryptocurrencies are said to be decentralized, there is no central unit in the transaction network, this can be achieved thanks to cryptography. Bitcoin is also the most traded cryptocurrency and has the largest market capitalization, this make it one of the most liquid cryptocurrency.

There has been tons of academic research studying the profitability of Bitcoin as well as its role as a safe heaven asset, with all giving mixed conclusions, some says that Bitcoin is to risky to be considered as an hedging instrument while others highlight similarities between Bitcoin and gold thus showing evidence on the usefulness of Bitcoin acting as an hedging instrument. Yet Bitcoin seems to attract more short term speculative investors rather than other ones that would use Bitcoin as an hedging instrument.

Once introduced, cryptocurrencies where of course heavily analyzed by technical analyst, and technical indicators where used by retail as well as institutional investors in order to forecast the future trends of bitcoin. I never really liked the idea of designing indicators that specifically worked for only one type of market and ever less on only one symbol. Yet the user @saraphig posted in Feb 20 an indicator called " Margin Call MovingAverage " who calculate liquidation price by using a volume weighted moving average. It took my attention and we decided to work together on a relatively more complete version that would include resistances levels.

I believe the proposed indicator might result useful to some users, the code also show a way to restrict the use of an indicator to only one symbol (line 9 to 16).

The Indicator

The indicator only work on BTCUSD, if you use another symbol you should see the following message:

The indicator plot 6 extremities, with 3 upper (resistance) extremities and 3 lower (support) extremities, each one based on the isolated margin mode liquidation price formula:

UPlp = MA/Leverage × (Leverage+1-(Leverage*0.005))

for upper extremities and:

DNlp = MA × Leverage/(Leverage+1-(Leverage*0.005))

for lower extremities.

Length control the period of the moving averages, with higher values of length increasing the probability of the price crossing an extremity. The Leverage's settings control how far away their associated extremities are from the price, with lower values of Leverage making the extremity farther away from the price, Leverage 3 control Up3 and Dn3, Leverage 2 control Up2 and Dn2, Leverage 1 control Up1 and Dn1, @saraphig recommend values for Leverage of either : 25, 20, 15, 10 ,5.

You can select 3 different types of moving average, the default moving average is the volume weighted moving average (VWMA), you can also choose a simple moving average (SMA) and the Kaufman adaptive moving average (KAMA).

Based on my understanding (which could be wrong) the original indicator aim to highlight points where margin calls might have occurred, hence the name of the indicator.

If you want a more "DSP" like description then i would say that each extremity represent a low-pass filter with a passband greater than 1 for upper extremities and lower than 1 for lower extremities, unlike bands indicators made by adding/subtracting a volatility indicator from another moving average this allow to conserve the original shape of the moving average, the downside of it being the inability to show properly on different scales.

here length = 200, on a 1h tf, each extremities are able to detect short-terms tops and bottoms. The extremity become wider when using lower time-frames.

You would then need to increase the Leverages settings, i recommend a time frame of 1h.

Conclusion

I'am not comfortable enough to make a conclusion, as i don't know the indicator that well, however i liked the original indicator posted by @saraphig and was curious about the idea behind it, studying the effect of margin calls on market liquidity as well as making indicators based on it might result a source of inspiration for other traders.

A big thanks to @saraphig who shared a lot of information about the original indicator and allowed me to post this one. I don't exclude working with him/her in the future, i invite you to follow him/her:

www.tradingview.com

Thx for reading and have a nice weekend! :3

Extended Recursive Bands - Maximum Efficiency With Extra OptionsIntroducing A New Calculation For Efficient Bands Calculation !

Here it is ! The Recursive Bands Indicator, an indicator specially created to be extremely efficient, i think you already know that calculation time is extra important in algorithmic trading, and this is the principal motivation for the creation of the proposed indicator. Originally described in my paper "Pierrefeu, Alex (2019): Recursive Bands - A New Indicator For Technical Analysis" , the indicator framework has been widely used in my previous uploaded indicators, however it would have been a shame to not upload it, however user experience being a major concern for me, i decided to add extra options, which explain the term "extended".

On The Indicator Calculation

You can skip this part if it doesn't interest you. The calculation of the indicator is based on recursion, but i want to explain the mathematical formula described in the paper.

I've seen some users trying to remake it from the calculations, however there was always something weird, and i understand, mathematical notations are always a bit weird, even myself don't always write them correctly/understand them, however this one is relatively simple to understand.

First lets explain each elements of the calculation :

α = smoothing constant, or 2/(length+1)

max/min = maximum and minimum function, max return the greatest input value while min return the lowest one, for example :

max(4,2) = 4 while min(4,2) = 2

the "||" notation mean taking the absolute value, for example : |-1| = abs(-1) = 1

The calculation after the max/min function is called the correction factor, and is the core of the indicator. The last two variables are just here to provide an initial value for upper and lower, basically when we start our calculations we will assign the value of the closing price for upper and lower.

The motivation behind using a smoothing constant in range of (0,1) was to tell the reader that the indicator is easily made adaptive, this is what i did on my adaptive trailing stop indicator by using the efficiency ratio as smoothing variable, the user can use 1/length instead of the provided calculation for alpha.

If you interested on the indicator main logic, it is actually really simple, by using upper = max(price,upper) and lower = min(price,lower) we would get the maximum/minimum price value at time t , therefore upper can only be greater or equal than its precedent value, while lower can only be lower or equal than its precedent value, in order to fix that we subtract/sum upper/lower with a value, this allow the upper band to be lower than its precedent value and lower to be greater than its precedent value, this is the role of the correction factor.

The Indicator

The indicator display one upper and one lower band, every common usages applied to bands indicators such as support/resistance, breakout, trailing stop...etc, can also be applied to this one. length control how reactive the bands are, higher values of length will make the bands cross the price less often.

In order to provide more flexibility for the user i added the option to use various methods for the calculation of the indicator, therefore the indicator can use the average true range, standard deviation, average high-low range, and one totally exclusive method specially designed for this indicator.

Classic Method

This option make the indicator use its classical calculation, this is the most efficient method of all.

Atr Method (atr)

This method use the average true range as correction factor, notice that lower values of length can still produce wide band.

Standard Deviation Method (stdev)

This method use a biased estimate of the standard deviation as correction factor.

The method produce smoother bands that converge more slowly toward the price in comparison with the classic correction factor.

Average High-Low Range Method (ahlr)

This method use the average of the high-low range as correction factor, extremely similar to the average true range.

Rising Falling Volatility (rfv) Method

A new method created for this indicator, this correction factor use the absolute prices changes when price value is greater/lower than any length past values of the price, this allow to have more boxy shaped bands, work best with greater values of length.

The bands can be in contact with this method, a possible fix in the future.

Conclusion

The recursive band indicator is one of my greatest indicators in my opinion (i would love to have yours), as you can see the idea behind it is extremely simple and allow for a super efficient band indicator, which was the original motivation behind it, in order to provide more fun for the users i also added more option for the correction factor, this allow the user to be creative and not get stuck with the original calculation.

Like the trend step indicator family we have almost ended our series on the recursive band framework, 1 more trailing stop will be added in the future, and then we'll have more "boring" stuff until i find something cool again, it shouldn't be long ;)

Thanks for reading !

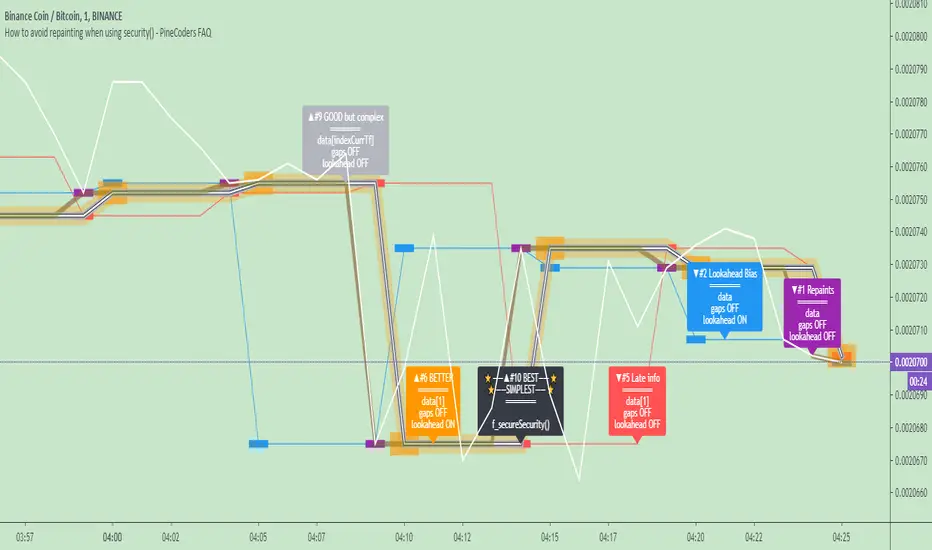

How to avoid repainting when using security() - PineCoders FAQNOTE

The non-repainting technique in this publication that relies on bar states is now deprecated, as we have identified inconsistencies that undermine its credibility as a universal solution. The outputs that use the technique are still available for reference in this publication. However, we do not endorse its usage. See this publication for more information about the current best practices for requesting HTF data and why they work.

This indicator shows how to avoid repainting when using the security() function to retrieve information from higher timeframes.

What do we mean by repainting?

Repainting is used to describe three different things, in what we’ve seen in TV members comments on indicators:

1. An indicator showing results that change during the realtime bar, whether the script is using the security() function or not, e.g., a Buy signal that goes on and then off, or a plot that changes values.

2. An indicator that uses future data not yet available on historical bars.

3. An indicator that uses a negative offset= parameter when plotting in order to plot information on past bars.

The repainting types we will be discussing here are the first two types, as the third one is intentional—sometimes even intentionally misleading when unscrupulous script writers want their strategy to look better than it is.

Let’s be clear about one thing: repainting is not caused by a bug ; it is caused by the different context between historical bars and the realtime bar, and script coders or users not taking the necessary precautions to prevent it.

Why should repainting be avoided?

Repainting matters because it affects the behavior of Pine scripts in the realtime bar, where the action happens and counts, because that is when traders (or our systems) take decisions where odds must be in our favor.

Repainting also matters because if you test a strategy on historical bars using only OHLC values, and then run that same code on the realtime bar with more than OHLC information, scripts not properly written or misconfigured alerts will alter the strategy’s behavior. At that point, you will not be running the same strategy you tested, and this invalidates your test results , which were run while not having the additional price information that is available in the realtime bar.

The realtime bar on your charts is only one bar, but it is a very important bar. Coding proper strategies and indicators on TV requires that you understand the variations in script behavior and how information available to the script varies between when the script is running on historical and realtime bars.

How does repainting occur?

Repainting happens because of something all traders instinctively crave: more information. Contrary to trader lure, more information is not always better. In the realtime bar, all TV indicators (a.k.a. studies ) execute every time price changes (i.e. every tick ). TV strategies will also behave the same way if they use the calc_on_every_tick = true parameter in their strategy() declaration statement (the parameter’s default value is false ). Pine coders must decide if they want their code to use the realtime price information as it comes in, or wait for the realtime bar to close before using the same OHLC values for that bar that would be used on historical bars.

Strategy modelers often assume that using realtime price information as it comes in the realtime bar will always improve their results. This is incorrect. More information does not necessarily improve performance because it almost always entails more noise. The extra information may or may not improve results; one cannot know until the code is run in realtime for enough time to provide data that can be analyzed and from which somewhat reliable conclusions can be derived. In any case, as was stated before, it is critical to understand that if your strategy is taking decisions on realtime tick data, you are NOT running the same strategy you tested on historical bars with OHLC values only.

How do we avoid repainting?

It comes down to using reliable information and properly configuring alerts, if you use them. Here are the main considerations:

1. If your code is using security() calls, use the syntax we propose to obtain reliable data from higher timeframes.

2. If your script is a strategy, do not use the calc_on_every_tick = true parameter unless your strategy uses previous bar information to calculate.

3. If your script is a study and is using current timeframe information that is compared to values obtained from a higher timeframe, even if you can rely on reliable higher timeframe information because you are correctly using the security() function, you still need to ensure the realtime bar’s information you use (a cross of current close over a higher timeframe MA, for example) is consistent with your backtest methodology, i.e. that your script calculates on the close of the realtime bar. If your system is using alerts, the simplest solution is to configure alerts to trigger Once Per Bar Close . If you are not using alerts, the best solution is to use information from the preceding bar. When using previous bar information, alerts can be configured to trigger Once Per Bar safely.

What does this indicator do?

It shows results for 9 different ways of using the security() function and illustrates the simplest and most effective way to avoid repainting, i.e. using security() as in the example above. To show the indicator’s lines the most clearly, price on the chart is shown with a black line rather than candlesticks. This indicator also shows how misusing security() produces repainting. All combinations of using a 0 or 1 offset to reference the series used in the security() , as well as all combinations of values for the gaps= and lookahead= parameters are shown.

The close in the call labeled “BEST” means that once security has reached the upper timeframe (1 day in our case), it will fetch the previous day’s value.

The gaps= parameter is not specified as it is off by default and that is what we need. This ensures that the value returned by security() will not contain na values on any of our chart’s bars.

The lookahead security() to use the last available value for the higher timeframe bar we are using (the previous day, in our case). This ensures that security() will return the value at the end of the higher timeframe, even if it has not occurred yet. In our case, this has no negative impact since we are requesting the previous day’s value, with has already closed.

The indicator’s Settings/Inputs allow you to set:

- The higher timeframe security() calls will use

- The source security() calls will use

- If you want identifying labels printed on the lines that have no gaps (the lines containing gaps are plotted using very thick lines that appear as horizontal blocks of one bar in length)

For the lines to be plotted, you need to be on a smaller timeframe than the one used for the security() calls.

Comments in the code explain what’s going on.

Look first. Then leap.

Triple Kijun Trend by SpiralmanIspired from "Oscars Simple Trend Ichimoku Kijun-sen" by CapnOscar

Script displays 3 kijun lines: one for current TF, second one emulates it for TF 4 times higher, third one for x16.

For example on 1H chart there will be 3 kijuns: one for 1H, second one for 4H (emulated), third one for 16H (emulated).

Kijuns change colors based on their position relative to price.

Kijun Sen

The base line, the slower EMA derivative, and a dynamic representation of the mean. With that said, the Kijun serves as both critical support and resistance levels for price. How does it work, and why would the Kijun be superior to commonly used moving average indicators? Fun fact: The Kijun dynamically equalizes itself to be the 50% retracement (or 0.5 Fibonacci level) of price for any given swing, and price will ALWAYS gravitate to the Kijun at some point regardless of how far above or below it is from it. By taking the median of price extremes, the Kijun accounts for volatility that other MAs or EMAs do not. A flat horizontal Kijun means that price extremes have not changed, and that the current trend losing momentum. Crypto-adjusted calculation: (highest high + lowest low) / 2 calculated over the last 60 periods.

Back to zero: Understanding seriestype: pine series basic example

time required: 10 minutes

level: medium (need to know the "array" data variable as a generic programming concept, basic Pine syntax)

tl;dr how variables and series work in Pine

Pine is an array/vector language. That's something that twists how it behaves, and how we have to think about it. A lot of misunderstandings come from forgetting this fact. This example tries to clear that concept.

First, you need to know what an array is, and how it works in a programmig language. Also, having javascript under your belt helps too. If you don't, google "javascript array basic tutorial" is your friend :)

So, in pine arrays are called "series". Every variable is an array with values for each candle in the chart. if we do:

myVar = true

this is not a constant. It is a series of values for each candle, { true, true,....., true }

In practice, the result is the same, but we can access each of the values in the series, like myVar{0}, myVar{7}, myVar{anyNumber}....

Again, it is not a constant, since you can access/modify the each value individually

so, lets show it:

plot (myVar, clolor = gray)

this plots an horizontal line of value 1 ( 1 is equal to true ) so it's all good.

On to a more usual series:

tipicalSeries = close > open ? true : false

plot(tipicalSeries, color= blue)

This gives the expected result, a tipical up and down line with values at 1 or 0. Naturally, "tipicalSeries" is an array, the "ups" and "downs" are all stored under the same variable, indexed by the candles.

In Pine, the ZERO position in the array is the last one, which corresponds to the last candle on the right. Say you have a chart with 12 candles. The close would be the closing value of what we intuitively think as first candle, the one on the left. then close ... and so on.... until close , the value of the "last" candle, the one on the right. It actually helps to start thinking of the positions backwards, counting down to zero, rocket launch style :)

And back to our series. The myVar will also be the same size, from myVar to myVar .

When we do some operation with them, something simple like

if ( myVar == tipicalSeries)

what is really happening is that internally, Pine is checking each of the indexes, as in myVar == tipicalSeries , myVar == tipicalSeries .... myVar == tipicalSeries

And we can store that stuff to check it. simply:

result = (myVar == tipicalSeries) ? true : false //yes, this is the same as tipicalSeries, but we're not in a boolean logic tut ;)

plot (result)

The reason we can plot the result is that it is an array, not a single value. The example indicator i provide shows a plot where the values are obtained from different places in the array, this line here:

mySeries3 = mySeries2 and mySeries1

this creates a series that is the result of the PREVIOUS values stored (the zero index is the one most at the right, or the "current" one), which here just causes a shift in the plotted line by one candle.

Go ahead, grab a copy of my code, try to change the indexes and see the results. Understanding this stuff is critical to go deeper into Pine :)

Third eye • StrategyThird eye • Strategy – User Guide

1. Idea & Concept

Third eye • Strategy combines three things into one system:

Ichimoku Cloud – to define market regime and support/resistance.

Moving Average (trend filter) – to trade only in the dominant direction.

CCI (Commodity Channel Index) – to generate precise entry signals on momentum breakouts.

The script is a strategy, not an indicator: it can backtest entries, exits, SL, TP and BreakEven logic automatically.

2. Indicators Used

2.1 Ichimoku

Standard Ichimoku settings (by default 9/26/52/26) are used:

Conversion Line (Tenkan-sen)

Base Line (Kijun-sen)

Leading Span A & B (Kumo Cloud)

Lagging Span is calculated but hidden from the chart (for visual simplicity).

From the cloud we derive:

kumoTop – top of the cloud under current price.

kumoBottom – bottom of the cloud under current price.

Flags:

is_above_kumo – price above the cloud.

is_below_kumo – price below the cloud.

is_in_kumo – price inside the cloud.

These conditions are used as trend / regime filters and for stop-loss & trailing stops.

2.2 Moving Average

You can optionally display and use a trend MA:

Types: SMA, EMA, DEMA, WMA

Length: configurable (default 200)

Source: default close

Filter idea:

If MA Direction Filter is ON:

When Close > MA → strategy allows only Long signals.

When Close < MA → strategy allows only Short signals.

The MA is plotted on the chart (if enabled).

2.3 CCI & Panel

The CCI (Commodity Channel Index) is used for entry timing:

CCI length and source are configurable (default length 20, source hlc3).

Two thresholds:

CCI Upper Threshold (Long) – default +100

CCI Lower Threshold (Short) – default –100

Signals:

Long signal:

CCI crosses up through the upper threshold

cci_val < upper_threshold and cci_val > upper_threshold

Short signal:

CCI crosses down through the lower threshold

cci_val > lower_threshold and cci_val < lower_threshold

There is a panel (table) in the bottom-right corner:

Shows current CCI value.

Shows filter status as colored dots:

Green = filter enabled and passed.

Red = filter enabled and blocking trades.

Gray = filter is disabled.

Filters shown in the panel:

Ichimoku Cloud filter (Long/Short)

Ichimoku Lines filter (Conversion/Base vs Cloud)

MA Direction filter

3. Filters & Trade Direction

All filters can be turned ON/OFF independently.

3.1 Ichimoku Cloud Filter

Purpose: trade only when price is clearly above or below the Kumo.

Long Cloud Filter (Use Ichimoku Cloud Filter) – when enabled:

Long trades only if close > cloud top.

Short Cloud Filter – when enabled:

Short trades only if close < cloud bottom.

If the cloud filter is disabled, this condition is ignored.

3.2 Ichimoku Lines Above/Below Cloud

Purpose: stronger trend confirmation: Ichimoku lines should also be on the “correct” side of the cloud.

Long Lines Filter:

Long allowed only if Conversion Line and Base Line are both above the cloud.

Short Lines Filter:

Short allowed only if both lines are below the cloud.

If this filter is OFF, the conditions are not checked.

3.3 MA Direction Filter

As described above:

When ON:

Close > MA → only Longs.

Close < MA → only Shorts.

4. Anti-Re-Entry Logic (Cloud Touch Reset)

The strategy uses internal flags to avoid continuous re-entries in the same direction without a reset.

Two flags:

allowLong

allowShort

After a Long entry, allowLong is set to false, allowShort to true.

After a Short entry, allowShort is set to false, allowLong to true.

Flags are reset when price touches the Kumo:

If Low goes into the cloud → allowLong = true

If High goes into the cloud → allowShort = true

If Close is inside the cloud → both allowLong and allowShort are set to true

There is a key option:

Wait Position Close Before Flag Reset

If ON: cloud touch will reset flags only when there is no open position.

If OFF: flags can be reset even while a trade is open.

This gives a kind of regime-based re-entry control: after a trend leg, you wait for a “cloud interaction” to allow new signals.

5. Risk Management

All risk management is handled inside the strategy.

5.1 Position Sizing

Order Size % of Equity – default 10%

The strategy calculates:

position_value = equity * (Order Size % / 100)

position_qty = position_value / close

So position size automatically adapts to your current equity.

5.2 Take Profit Modes

You can choose one of two TP modes:

Percent

Fibonacci

5.2.1 Percent Mode

Single Take Profit at X% from entry (default 2%).

For Long:

TP = entry_price * (1 + tp_pct / 100)

For Short:

TP = entry_price * (1 - tp_pct / 100)

One strategy.exit per side is used: "Long TP/SL" and "Short TP/SL".

5.2.2 Fibonacci Mode (2 partial TPs)

In this mode, TP levels are based on a virtual Fib-style extension between entry and stop-loss.

Inputs:

Fib TP1 Level (default 1.618)

Fib TP2 Level (default 2.5)

TP1 Share % (Fib) (default 50%)

TP2 share is automatically 100% - TP1 share.

Process for Long:

Compute a reference Stop (see SL section below) → sl_for_fib.

Compute distance: dist = entry_price - sl_for_fib.

TP levels:

TP1 = entry_price + dist * (Fib TP1 Level - 1)

TP2 = entry_price + dist * (Fib TP2 Level - 1)

For Short, the logic is mirrored.

Two exits are used:

TP1 – closes TP1 share % of position.

TP2 – closes remaining TP2 share %.

Same stop is used for both partial exits.

5.3 Stop-Loss Modes

You can choose one of three Stop Loss modes:

Stable – fixed % from entry.

Ichimoku – fixed level derived from the Kumo.

Ichimoku Trailing – dynamic SL following the cloud.

5.3.1 Stable SL

For Long:

SL = entry_price * (1 - Stable SL % / 100)

For Short:

SL = entry_price * (1 + Stable SL % / 100)

Used both for Percent TP mode and as reference for Fib TP if Kumo is not available.

5.3.2 Ichimoku SL (fixed, non-trailing)

At the time of a new trade:

For Long:

Base SL = cloud bottom minus small offset (%)

For Short:

Base SL = cloud top plus small offset (%)

The offset is configurable: Ichimoku SL Offset %.

Once computed, that SL level is fixed for this trade.

5.3.3 Ichimoku Trailing SL

Similar to Ichimoku SL, but recomputed each bar:

For Long:

SL = cloud bottom – offset

For Short:

SL = cloud top + offset

A red trailing SL line is drawn on the chart to visualize current stop level.

This trailing SL is also used as reference for BreakEven and for Fib TP distance.

6. BreakEven Logic (with BE Lines)

BreakEven is optional and supports two modes:

Percent

Fibonacci

Inputs:

Percent mode:

BE Trigger % (from entry) – move SL to BE when price goes this % in profit.

BE Offset % from entry – SL will be set to entry ± this offset.

Fibonacci mode:

BE Fib Level – Fib level at which BE will be activated (default 1.618, same style as TP).

BE Offset % from entry – how far from entry to place BE stop.

The logic:

Before BE is triggered, SL follows its normal mode (Stable/Ichimoku/Ichimoku Trailing).

When BE triggers:

For Long:

New SL = max(current SL, BE SL).

For Short:

New SL = min(current SL, BE SL).

This means BE will never loosen the stop – only tighten it.

When BE is activated, the strategy draws a violet horizontal line at the BreakEven level (once per trade).

BE state is cleared when the position is closed or when a new position is opened.

7. Entry & Exit Logic (Summary)

7.1 Long Entry

Conditions for a Long:

CCI signal:

CCI crosses up through the upper threshold.

Ichimoku Cloud Filter (optional):

If enabled → price must be above the Kumo.

Ichimoku Lines Filter (optional):

If enabled → Conversion Line and Base Line must be above the Kumo.

MA Direction Filter (optional):

If enabled → Close must be above the chosen MA.

Anti-re-entry flag:

allowLong must be true (cloud-based reset).

Position check:

Long entries are allowed when current position size ≤ 0 (so it can also reverse from short to long).

If all these conditions are true, the strategy sends:

strategy.entry("Long", strategy.long, qty = calculated_qty)

After entry:

allowLong = false

allowShort = true

7.2 Short Entry

Same structure, mirrored:

CCI signal:

CCI crosses down through the lower threshold.

Cloud filter: price must be below cloud (if enabled).

Lines filter: conversion & base must be below cloud (if enabled).

MA filter: Close must be below MA (if enabled).

allowShort must be true.

Position check: position size ≥ 0 (allows reversal from long to short).

Then:

strategy.entry("Short", strategy.short, qty = calculated_qty)

Flags update:

allowShort = false

allowLong = true

7.3 Exits

While in a position:

The strategy continuously recalculates SL (depending on chosen mode) and, in Percent mode, TP.

In Fib mode, fixed TP levels are computed at entry.

BreakEven may raise/tighten the SL if its conditions are met.

Exits are executed via strategy.exit:

Percent mode: one TP+SL exit per side.

Fib mode: two partial exits (TP1 and TP2) sharing the same SL.

At position open, the script also draws visual lines:

White line — entry price.

Green line(s) — TP level(s).

Red line — SL (if not using Ichimoku Trailing; with trailing, the red line is updated dynamically).

Maximum of 30 lines are kept to avoid clutter.

8. How to Use the Strategy

Choose market & timeframe

Works well on trending instruments. Try crypto, FX or indices on H1–H4, or intraday if you prefer more trades.

Adjust Ichimoku settings

Keep defaults (9/26/52/26) or adapt to your timeframe.

Configure Moving Average

Typical: EMA 200 as a trend filter.

Turn MA Direction Filter ON if you want to trade only with the main trend.

Set CCI thresholds

Default ±100 is classic.

Lower thresholds → more signals, higher noise.

Higher thresholds → fewer but stronger signals.

Enable/disable filters

Turn on Ichimoku Cloud and Ichimoku Lines if you want only “clean” trend trades.

Use Wait Position Close Before Flag Reset to control how often re-entries are allowed.

Choose TP & SL mode

Percent mode is simpler and easier to understand.

Fibonacci mode is more advanced: it aligns TP levels with the distance to stop, giving asymmetric RR setups (two partial TPs).

Choose Stable SL for fixed-risk trades, or Ichimoku / Ichimoku Trailing to tie stops to the cloud structure.

Set BreakEven

Enable BE if you want to lock in risk-free trades after a certain move.

Percent mode is straightforward; Fib mode keeps BreakEven in harmony with your Fib TP setup.

Run Backtest & Optimize

Press “Add to chart” → go to Strategy Tester.

Adjust parameters to your market and timeframe.

Look at equity curve, PF, drawdown, average trade, etc.

Live / Paper Trading

After you’re satisfied with backtest results, use the strategy to generate signals.

You can mirror entries/exits manually or connect them to alerts (if you build an alert-based execution layer).

Multivariate Kalman Filter🙏🏻 I see no1 ever posted an open source Multivariate Kalman filter on TV, so here it is, for you. Tested and mathematically correct implementation, with numerical safeties in place that do not affect the final results at all. That’s the main purpose of this drop, just to make the tool available here. Linear algebra everywhere, Neo would approve 4 sure.

...

Personally I haven't found any real use case of it for myself, aside from a very specific one I will explain later, but others usually do…

Almost every1 in the quant industry who uses Kalman is in fact misusing it, because by its real definition, it should be applied to Not the exact known values (e.g as real ticks provided by transparent audited regulated exchange), but “measurements” of those ‘with errors’.

If your measurements don’t have errors or you have real precise data, by its internal formulas Kalman will output the exact inputs. So most who use it come up with some imaginary errors of sorts, like from some kind of imaginary fair price etc. The important easy to miss point, the errors of your measurements have to be symmetric around its mean ‘ at least ’, if errors are biased, Kalman won’t provide.

For most tasks there are better tools, including other state space models , but still Multivariate Kalman is a very powerful instrument, you can make it do all kinds of stuff. Also as a state space model it can also provide confidence & prediction intervals without explicit calculations of dem.

...

In this script I included 2 example use cases, the first one is the classic tho perfectly working misuse, the second one is what I do with it:

One

Naive, estimates “hidden” adaptive moving regression endpoint. The result you can see on the chart above. You can imagine that your real datapoints are in fact non perfect measures of some hidden state, and by defining measurement noise and process noise, and by constructing the input matrixes in certain ways, you can express what that state should be.

Two

Upscaling tick lattice, aka modelling prices as if native tick size would’ve been lower. Kinda very specific task, mostly needed in HFT or just for analytical purposes. Some like ZN have huge tick sizes, they are traded a lot but barely do more than 20 ticks range in a session. The idea is to model raw data as AR2 process , learn the phi1 and phi2, make one point forecasts based on dem, and the process noise would be the variance of errors from these forecasts. The measurement noise here is legit, it’s quantization noise based on tick size, no need in olympic gold in mental gymnastics xd

^^ artificially upscaling ZN futures tick lattice

...

I really made it available there so You guys can take it and some crazy ish with it, just let state space models abduct your conciseness and never look back

∞

CoreMACDHTF [CHE]Library "CoreMACDHTF"

calc_macd_htf(src, preset_str, smooth_len)

Parameters:

src (float)

preset_str (simple string)

smooth_len (int)

is_hist_rising(src, preset_str, smooth_len)

Parameters:

src (float)

preset_str (simple string)

smooth_len (int)

hist_rising_01(src, preset_str, smooth_len)

Parameters:

src (float)

preset_str (simple string)

smooth_len (int)

CoreMACDHTF — Hardcoded HTF MACD Presets with Smoothed Histogram Regime Flags

Summary

CoreMACDHTF provides a reusable MACD engine that approximates higher-timeframe behavior by selecting hardcoded EMA lengths based on the current chart timeframe, then optionally smoothing the resulting histogram with a stateful filter. It is published as a Pine v6 library but intentionally includes a minimal demo plot so you can validate behavior directly on a chart. The primary exported outputs are MACD, signal, a smoothed histogram, and the resolved lengths plus a timeframe tag. In addition, it exposes a histogram rising condition so importing scripts can reuse the same regime logic instead of re-implementing it.

Motivation: Why this design?

Classic MACD settings are often tuned to one timeframe. When you apply the same parameters to very different chart intervals, the histogram can become either too noisy or too sluggish. This script addresses that by using a fixed mapping from the chart timeframe into a precomputed set of EMA lengths, aiming for more consistent “tempo” across intervals. A second problem is histogram micro-chop around turning points; the included smoother reduces short-run flips so regime-style conditions can be more stable for alerts and filters.

What’s different vs. standard approaches?

Reference baseline: a standard MACD using fixed fast, slow, and signal lengths on the current chart timeframe.

Architecture differences:

Automatic timeframe bucketing that selects a hardcoded length set for the chosen preset.

Two preset families: one labeled A with lengths three, ten, sixteen; one labeled B with lengths twelve, twenty-six, nine.

A custom, stateful histogram smoother intended to damp noisy transitions.

Library exports that return both signals and metadata, plus a dedicated “histogram rising” boolean.

Practical effect:

The MACD lengths change when the chart timeframe changes, so the oscillator’s responsiveness is not constant across intervals by design.

The rising-flag logic is based on the smoothed histogram, which typically reduces single-bar flip noise compared to using the raw histogram directly.

How it works (technical)

1. The script reads the chart timeframe and converts it into milliseconds using built-in timeframe helpers.

2. It assigns the timeframe into a bucket label, such as an intraday bucket or a daily-and-above bucket, using fixed thresholds.

3. It resolves a hardcoded fast, slow, and signal length triplet based on:

The selected preset family.

The bucket label.

In some cases, the current minute multiplier for finer mapping.

4. It computes fast and slow EMAs on the selected source and subtracts them to obtain MACD, then computes an EMA of MACD for the signal line.

5. The histogram is derived from the difference between MACD and signal, then passed through a custom smoother.

6. The smoother uses persistent internal state to carry forward its intermediate values from bar to bar. This is intentional and means the smoothing output depends on contiguous bar history.

7. The histogram rising flag compares the current smoothed histogram to its prior value. On the first comparable bar it defaults to “rising” to avoid a missing prior reference.

8. Exports:

A function that returns MACD, signal, smoothed histogram, the resolved lengths, and a text tag.

A function that returns the boolean rising state.

A function that returns a numeric one-or-zero series for direct plotting or downstream numeric logic.

HTF note: this is not a true higher-timeframe request. It does not fetch higher-timeframe candles. It approximates HTF feel by selecting different lengths on the current timeframe.

Parameter Guide

Source — Input price series used for EMA calculations — Default close — Trade-offs/Tips

Preset — Selects the hardcoded mapping family — Default preset A — Preset A is more reactive than preset B in typical use

Table Position — Anchor for an information table — Default top right — Present but not wired in the provided code (Unknown/Optional)

Table Size — Text size for the information table — Default normal — Present but not wired in the provided code (Unknown/Optional)

Dark Mode — Theme toggle for the table — Default enabled — Present but not wired in the provided code (Unknown/Optional)

Show Table — Visibility toggle for the table — Default enabled — Present but not wired in the provided code (Unknown/Optional)

Zero dead-band (epsilon) — Intended neutral band around zero for regime classification — Default zero — Present but not used in the provided code (Unknown/Optional)

Acceptance bars (n) — Intended debounce count for regime confirmation — Default three — Present but not used in the provided code (Unknown/Optional)

Smoothing length — Length controlling the histogram smoother’s responsiveness — Default nine — Smaller values react faster but can reintroduce flip noise

Reading & Interpretation

Smoothed histogram: use it as the momentum core. A positive value implies MACD is above signal, a negative value implies the opposite.

Histogram rising flag:

True means the smoothed histogram increased compared to the prior bar.

False means it did not increase compared to the prior bar.

Demo plot:

The included plot outputs one when rising is true and zero otherwise. It is a diagnostic-style signal line, not a scaled oscillator display.

Practical Workflows & Combinations

Trend following:

Use rising as a momentum confirmation filter after structural direction is established by higher highs and higher lows, or lower highs and lower lows.

Combine with a simple trend filter such as a higher-timeframe moving average from your main script (Unknown/Optional).

Exits and risk management:

If you use rising to stay in trends, consider exiting or reducing exposure when rising turns false for multiple consecutive bars rather than reacting to a single flip.

If you build alerts, evaluate on closed bars to avoid intra-bar flicker in live candles.

Multi-asset and multi-timeframe:

Because the mapping is hardcoded, validate on each asset class you trade. Volatility regimes differ and the perceived “equivalence” across timeframes is not guaranteed.

For consistent behavior, keep the smoothing length aligned across assets and adjust only when flip frequency becomes problematic.

Behavior, Constraints & Performance

Repaint and confirmation:

There is no forward-looking indexing. The logic uses current and prior values only.

Live-bar values can change until the bar closes, so rising can flicker intra-bar if you evaluate it in real time.

security and HTF:

No higher-timeframe candle requests are used. Length mapping is internal and deterministic per chart timeframe.

Resources:

No loops and no arrays in the core calculation path.

The smoother maintains persistent state, which is lightweight but means results depend on uninterrupted history.

Known limits:

Length mappings are fixed. If your chart timeframe is unusual, the bucket choice may not represent what you expect.

Several table and regime-related inputs are declared but not used in the provided code (Unknown/Optional).

The smoother is stateful; resetting chart history or changing symbol can alter early bars until state settles.

Sensible Defaults & Quick Tuning

S tarting point:

Preset A

Smoothing length nine

Source close

Tuning recipes:

Too many flips: increase smoothing length and evaluate rising only on closed bars.

Too sluggish: reduce smoothing length, but expect more short-run reversals.

Different timeframe feel after switching intervals: keep preset fixed and adjust smoothing length first before changing preset.

Want a clean plot signal: use the exported numeric rising series and apply your own display rules in the importing script.

What this indicator is—and isn’t

This is a momentum and regime utility layer built around a MACD-style backbone with hardcoded timeframe-dependent parameters and an optional smoother. It is not a complete trading system, not a risk model, and not predictive. Use it in context with market structure, execution rules, and risk controls.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Candle Patterns Ver.2When someone decided to start trading the first thing we learn is how to read and understand the candlesticks. This little "boxes" with sticks tell us how the market sentiment and they can be used to "predict" future moves. I put predict inside a quotation marks because I would say predict the market is almost an utopia and we all know the reason.

Anyway with a good understand in reading the candlesticks with other indicators(like momentum or even a MA) can give us some edge when analyzing an instrument.

Since we have a lot of candlesticks types I did some back test and figured out that for my strategy that three candlestick types works very well. I will briefly describe then.

Engulfing Bar

This type of candlestick shows us a potential reversal based on the previous bar.

A bullish Engulfing has the close higher than the open it works better if the previous one is a bearish bar(open higher than close) and it is at a Support level. The body of the Engulfing bar should "engulf" the full body of the previous bar. If all parameters(previous bearish bar at Support level after a downtrend move) this Engulfing will represents a reversal move. When I say reversal it could means a pullback reversal(if the past trend is downtrend) or if the previous downtrend is a pullback from a past uptrend. In any way the previous bearish followed by an bullish Engulfing in general leads for an upward move.

The same picture applies to a previous bullish bar followed by an bearish Engulfing bar that if appears at the Resistance level will lead to a downward move.

One thing that is worth to mention is in a downward(or upward) move we have a small bullish bar followed by a bullish Engulfing this situation may lead to a continuation, not reversal.

Pinbar Bar:

This is another candlestick type that represents possible reversal. The Pinbar candle show a small(or medium) size but the important part is the size of the stick. If the stick is the upper one and has the size of 2 times the size of the body, it is a bearish bars and it appears after an uptrend move it represents that the buyers are losing momentum so we can expect a reversal move. When this type of bar appears after a downward move, it is a bullish bars but the stick is the lower one and has the size of two times of the body it will represents a bullish reversal. In this picture this candle is called a "Hammer".

So based on that I develop an indicator that shows me these 2 bars types and makes easy to identify with the other indicator possible entries.

Please feel free for a constructive comments and hope it help any one whe trading. Candlestick are the fundamentals of Price action.

You all have a great trading new week.

Stochastic Ensembling of OutputsStochastic Ensembling of Outputs

🙏🏻 This is a simple tool/method that would solve naturally many well known problems:

“Price reversed 1 tick before the actual level, not executing my limit order”

“I consider intraday trend change by checking whether price is above/below VWAP, but is 1 tick enough? What to do, price is now whipsawing around vwap...”.

“I want to gradually accumulate a position around a chosen anchor. But where exactly should I put my orders? And I want to automate it ofc.“

“All these DSP adepts are telling you about some kind of noise in the markets… But how can I actually see it?”

The easy fix is to make things more analog less digital, by synthesizing numerous noise instances & adding it to any price-applied metric of yours. The ones who fw techno & psytrance, and other music, probably don’t need any more explanations. Then by checking not just 2 lines or 1 process against another one, you will be checking cloud vs cloud of lines, even allowing you to introduce proxies of probabilities. More crosses -> more confirmation to act.

How-to use:

The tool has 2 inputs: source and target:

Sources should always be the underlying process. If you apply the tool to price based metric, leave it hlcc4 unless you have a better one point estimate for each bar;

Target is your target, e.g if you want to apply it to VWAP, pick VWAP as target. You can thee on the chart above how trading activity recently never exactly touched VWAP, however noised instances of VWAP 'were' touched

The code is clean and written in modular form, you can simply copy paste it to any script of yours if you don't want to have multiple study-on-study script pairs.

^^ applied to prev days highs and lows

^^ applied to MBAD extensions and basis

^^ applied to input series itself

Here’s how it works, no ML, no “AI”, no 1k lines of code, just stats:

The problem with metrics, even if they are time aware like WMA, is that they still do not directly gain information about “changes” between datapoints. If we pick noise characteristics to match these changes, we’d effectively introduce this info into our ops.

^^ this screenshot represents 2 very different processes: a sine wave and white noise, see how the noise instances learned from each process differ significantly.

Changes can be represented as AR1 process . It’s dead simple, no PHD needed, it’s just how the current datapoint is related (or not) to the previous datapoint, no more than 1, and how this relationship holds/evolves over time. Unlike the mainstream approach like MLE, I estimate this relationship (phi parameter) via MoM but giving more weights to more recent datapoints via exponential smoothing over all the data available on your charts (so I encode temporal information), algocomplexity is O(1), lighting fast, just one pass. <- that gives phi , we’d use it as color for our noise generator

Then we just need to estimate noise amplitude ( gamma ) via checking what AR1 model actually thought vs the reality, variance of these innovations. Same via exponential smoothing, time aware, O(1), one pass, it’s all it does.

Then we generate white gaussian noise, and apply 2 estimated parameters (phi and gamma), and that’s all.

Omg, I think I just made my first real DSP script xd

Just like Monte Carlo for risk management, this is so simple and natural I can’t believe so many “pros” hide it and never talk about it in open access. Sharing it here on TradingView would’ve not done anything critical for em, but many would’ve benefited.

∞

TopBot [CHE] TopBot — Structure pivots with buffered acceptance and gradient trend visualization

Summary

TopBot detects swing structure from confirmed pivot highs and lows, derives support and resistance levels, and switches trend only after a buffered and accepted break. It renders labels for recent structure points, maintains dynamic support and resistance lines that freeze on contact, and colors candles using a gradient that reflects consecutive trend persistence. The gradient communicates strength without extra panels, while the buffered acceptance reduces fragile flips around key levels. Everything runs in the main chart for immediate context.

Motivation: Why this design?

Classical swing tools often flip on single-bar spikes and produce lines that extend forever without acknowledging when price invalidates them. This script addresses that by requiring a user-controlled buffer and a run of consecutive closes before changing trend, while also freezing lines once price interacts with them. The gradient color layer communicates regime persistence so users can quickly judge whether a move is maturing or just starting.

What’s different vs. standard approaches?

Baseline reference: Simple pivot labeling and unbuffered break-of-structure tools.

Architecture differences:

Buffered level testing using ticks, percent, or ATR.

Acceptance logic that requires multiple consecutive closes.

Synchronized structure labeling with a single Top and Bottom within the active set.

Progressive support and resistance management that freezes lines on first contact.

Gradient candle and wick coloring driven by consecutive trend counts with windowed normalization and gamma control.

Practical effect: Fewer whipsaw flips, clearer status of active levels, and visual feedback about trend persistence without a secondary pane.

How it works (technical)

The script confirms swing points using left and right bar pivots, then forms a current structure window to classify each pivot as higher high, lower high, higher low, or lower low. Recent labels are trimmed to a user cap, and a postprocess step ensures one highest and one lowest label while preserving side information for the others. Support updates on higher low events, resistance on lower high events. Trend flips only after the close has moved beyond the active level by a chosen buffer and this condition holds for a chosen number of consecutive bars. Lines for new levels extend to the right and freeze once price touches them. A running count of consecutive trend bars produces a strength score, which is normalized over a rolling window, shaped by gamma, and mapped to user-defined dark and neon colors for both up and down regimes. Wick coloring uses `plotcandle`; fallback bar coloring uses `barcolor`. No higher-timeframe data is requested. Signals confirm only after the right-bar lookback of the pivot function.

Parameter Guide

Left Bars / Right Bars (default five each): Pivot sensitivity. Larger values confirm later and reduce noise; smaller values respond faster with more noise.

Draw S/R Lines (default true): Enables support and resistance line creation and updates.

Support / Resistance Colors (lime, red): Line colors for each side.

Line Style (Solid, Dashed, Dotted; default Dotted) and Width (default three): Visual style of S/R lines.

Max Labels & Lines (default ten): Cap for objects to control clutter and resource usage.

Change Bar Color (default true), Up/Down colors (blue, black): Fallback bar coloring when gradients or wick coloring are disabled.

Show Neutral Candles (default false): Optional coloring when no trend is active.

Enable Gradient Bar Colors (default true): Turns on gradient body coloring from the strength score.

Enable Wick Coloring (default true): Colors wicks and borders using `plotcandle`.

Collection Period (default one hundred): Rolling window used to scale the strength score. Shorter windows react faster but vary more.

Gamma Bars / Gamma Plots (defaults zero point seven and zero point eight): Shapes perceived contrast of bar and wick gradients. Lower values brighten early; higher values compress until stronger runs appear.

Gradient Transparency / Wick Transparency (default zero): Visual transparency for bodies and wicks.

Up/Down Trend Dark and Neon Colors: Endpoints for gradient mapping in each regime.

Acceptance closes (n) (default two): Number of consecutive closes beyond a level required before trend flips. Larger values reduce false breaks but react later.

Break buffer (None, Ticks, Percent, ATR; default ATR) and Value (default zero point five) and ATR Len (default fourteen): Defines the safety margin beyond the level. ATR mode adapts to volatility; Percent and Ticks are static.

Reading & Interpretation

Labels: “Top” and “Bottom” mark the most extreme points in the active set; “LT” and “HB” indicate side labels for lower top and higher bottom.

Lines: New support or resistance is drawn when structure confirms. A line freezes once price touches it, signaling that the dynamic phase ended.

Trend: Internal state switches to up or down only after buffered acceptance.

Colors: Brighter neon tones indicate stronger and more persistent runs; darker tones suggest early or weakening runs. When gradients are off, fallback bar colors indicate trend sign.

Practical Workflows & Combinations

Trend following: Wait for a buffered and accepted break through the most recent level, then use gradient intensity to stage entries or scale-ins.

Structure-first filtering: Trade only in the direction of the last accepted trend while price remains above support or below resistance.

Exits and stops: Consider exiting on loss of gradient intensity combined with a return through the most recent structure level.

Multi-asset / Multi-timeframe: Works on liquid symbols across common timeframes. Use larger pivot bars and higher acceptance on lower timeframes. No built-in higher-timeframe aggregation is used.

Behavior, Constraints & Performance

Repaint/confirmation: Pivot confirmation waits for the right bar window; trend acceptance is based on closes and can change during a live bar. Final signals stabilize on bar close.

security/HTF: Not used. No cross-timeframe data.

Resources: Arrays and loops are used for labels, lines, and structure search up to a capped historical span. Object counts are clamped by user input and platform limits.

Known limits: Delayed confirmation at sharp turns due to pivot windows; rapid gaps can jump over buffers; gradient scaling depends on the chosen collection period.

Sensible Defaults & Quick Tuning

Start with the defaults: pivot windows at five, ATR buffer with value near one half, acceptance at two, collection period near one hundred, gamma near zero point seven to zero point eight.

Too many flips: increase acceptance, increase buffer value, or increase pivot windows.

Too sluggish: reduce acceptance, reduce buffer value, or reduce pivot windows.

Colors too flat: lower gamma or shorten the collection period.

Visual clutter: reduce the max labels and lines cap or disable wicks.

What this indicator is—and isn’t

This is a visualization and signal layer that encodes swing structure, level state, and regime persistence. It is not a complete trading system, not predictive, and does not manage orders. Use it with broader context such as higher timeframe structure, session behavior, and defined risk controls.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Acknowledgment

Thanks to LonesomeTheBlue for the fantastic and inspiring "Higher High Lower Low Strategy" .

Original script:

Credit for the original concept and implementation goes to the author; any adaptations or errors here are mine.

US/SPY- Financial Regime Index Swing Strategy Credits: concept inspired by EdgeTools Bloomberg Financial Conditions Index (Proxy)

Improvements: eight component basket, inverse volatility weights, winsorization option( statistical technique used to limit the influence of outliers in a dataset by replacing extreme values with less extreme ones, rather than removing them entirely), slope and price gates, exit guards, table and gradients.

Summary in one paragraph

A macro regime swing strategy for index ETFs, futures, FX majors, and large cap equities on daily calculation with optional lower time execution. It acts only when a composite Financial Conditions proxy plus slope and an optional price filter align. Originality comes from an eight component macro basket with inverse volatility weights and winsorized return z scores that produce a portable yardstick.

Scope and intent

Markets: SPY and peers, ES futures, ACWI, liquid FX majors, BTC, large cap equities.

Timeframes: calculation daily by default, trade on any chart.

Default demo: SPY on Daily.

Purpose: convert broad financial conditions into clear swing bias and exits.

Originality and usefulness

Unique fusion: return z scores for eight liquid proxies with inverse volatility weighting and optional winsorization, then slope and price gates.

Failure mode addressed: false starts in chop and early shorts during easy liquidity.

Testability: all knobs are inputs and the table shows components and weights.

Portable yardstick: z scores center at zero so thresholds transfer across symbols.

Method overview in plain language

Base measures

Return basis: natural log return over a configurable window, standardized to a z score. Winsorization optional to cap extremes.

Components

EQ US and EQ GLB measure equity tone.

CREDIT uses LQD over HYG. Higher credit quality outperformance is risk off so sign is flipped after z score.

RATES2Y uses two year yield, sign flipped.

SLOPE uses ten minus two year yield spread.

USD uses DXY, sign flipped.

VOL uses VIX, sign flipped.

LIQ uses BIL over SPY, sign flipped.

Each component is smoothed by the composite EMA.

Fusion rule

Weighted sum where weights are equal or inverse volatility with exponent gamma, normalized to percent so they sum to one.

Signal rule

Long when composite crosses up the long threshold and its slope is positive and price is above the SMA filter, or when composite is above the configured always long floor.

Short when composite crosses down the short threshold and its slope is negative and price is below the SMA filter.

Long exit on cross down of the long exit line or on a fresh short signal.

Short exit on cross up of the short exit line or on a fresh long signal, or when composite falls below the force short exit guard.

What you will see on the chart

Markers on suggestion bars: L for long, S for short, LX and SX for exits.

Reference lines at zero and soft regime bands at plus one and minus one.

Optional background gradient by regime intensity.

Compact table with component z, weight percent, and composite readout.

Table fields and quick reading guide

Component: EQ US, EQ GLB, CREDIT, RATES2Y, SLOPE, USD, VOL, LIQ.

Z: current standardized value, green for positive risk tone where applicable.

Weight: contribution percent after normalization.

Composite: current index value.

Reading tip: a broadly green Z column with slope positive often precedes better long context.

Inputs with guidance

Setup

Calc timeframe: default Daily. Leave blank to inherit chart.

Lookback: 50 to 1500. Larger length stabilizes regimes and delays turns.

EMA smoothing: 1 to 200. Higher smooths noise and delays signals.

Normalization

Winsorize z at ±3: caps extremes to reduce one off shocks.

Return window for equities: 5 to 260. Shorter reacts faster.

Weighting

Weight lookback: 20 to 520.

Weight mode: Equal or InvVol.

InvVol exponent gamma: 0.1 to 3. Higher compresses noisy components more.

Signals

Trade side: Long Short or Both.

Entry threshold long and short: portable z thresholds.

Exit line long and short: soft exits that give back less.

Slope lookback bars: 1 to 20.

Always long floor bfci ≥ X: macro easy mode keep long.

Force short exit when bfci < Y: macro stress guard.

Confirm

Use price trend filter and Price SMA length.

View

Glow line and Show component table.

Symbols

SPY ACWI HYG LQD VIX DXY US02Y US10Y BIL are defaults and can be changed.

Realism and responsible publication

No performance claims. Past is not future.

Shapes can move intrabar and settle on close.

Execution is on standard candles only.

Honest limitations and failure modes

Major economic releases and illiquid sessions can break assumptions.

Very quiet regimes reduce contrast. Use longer windows or higher thresholds.

Component proxies are ETFs and indexes and cannot match a proprietary FCI exactly.

Strategy notice

Orders are simulated on standard candles. All security calls use lookahead off. Nonstandard chart types are not supported for strategies.

Entries and exits

Long rule: bfci cross above long threshold with positive slope and optional price filter OR bfci above the always long floor.

Short rule: bfci cross below short threshold with negative slope and optional price filter.

Exit rules: long exit on bfci cross below long exit or on a short signal. Short exit on bfci cross above short exit or on a long signal or on force close guard.

Position sizing

Percent of equity by default. Keep target risk per trade low. One percent is a sensible starting point. For this example we used 3% of the total capital

Commisions

We used a 0.05% comission and 5 tick slippage

Legal

Education and research only. Not investment advice. Test in simulation first. Use realistic costs.

Cora Combined Suite v1 [JopAlgo]Cora Combined Suite v1 (CCSV1)

This is an 2 in 1 indicator (Overlay & Oscillator) the Cora Combined Suite v1 .

CCSV1 combines a price-pane Overlay for structure/trend with a compact Oscillator for timing/pressure. It’s designed to be clear, beginner-friendly, and largely automatic: you pick a profile (Scalp / Intraday / Swing), choose whether to run as Overlay or Oscillator, and CCSV1 tunes itself in the background.

What’s inside — at a glance

1) Overlay (price pane)

CoRa Wave: a smooth trend line based on a compound-ratio WMA (CRWMA).

Green when the slope rises (bull bias), Red when it falls (bear bias).

Asymmetric ATR Cloud around the CoRa Wave

Width expands more up when buyer pressure dominates and more down when seller pressure dominates.

Fill is intentionally light, so candlesticks remain readable.

Chop Guard (Range-Lock Gate)

When the cloud stays very narrow versus ATR (classic “dead water”), pullback alerts are muted to avoid noise.

Visuals don’t change—only the alerting logic goes quiet.

Typical Overlay reads

Trend: Follow the CoRa color; green favors long setups, red favors shorts.

Value: Pullbacks into/through the cloud in trend direction are higher-quality than chasing breaks far outside it.

Dominance: A visibly asymmetric cloud hints which side is funding the move (buyers vs sellers).

2) Oscillator (subpane or inline preview)

Stretch-Z (columns): how far price is from the CoRa mean (mean-reversion context), clipped to ±clip.

Near 0 = equilibrium; > +2 / < −2 = stretched/extended.

Slope-Z (line): z-score of CoRa’s slope (momentum of the trend line).

Crossing 0 upward = potential bullish impulse; downward = potential bearish impulse.

VPO (stepline): a normalized Volume-Pressure read (positive = buyers funding, negative = sellers).

Rendered as a clean stepline to emphasize state changes.

Event Bands ±2 (subpane): thin reference lines to spot extension/exhaustion zones fast.

Floor/Ceiling lines (optional): quiet boundaries so the panel doesn’t feel “bottomless.”

Inline vs Subpane

Inline (overlay): the oscillator auto-anchors and scales beneath price, so it never crushes the price scale.

Subpane (raw): move to a new pane for the classic ±clip view (with ±2 bands). Recommended for systematic use.

Why traders like it

Two in one: Structure on the chart, timing in the panel—built to complement each other.

Retail-first automation: Choose Scalp / Intraday / Swing and let CCSV1 auto-tune lengths, clips, and pressure windows.

Robust statistics: On fast, spiky markets/timeframes, it prefers outlier-resistant math automatically for steadier signals.

Optional HTF gate: You can require higher-timeframe agreement for oscillator alerts without changing visuals.

Quick start (simple playbook)

Run As

Overlay for structure: assess trend direction, where value is (the cloud), and whether chop guard is active.

Oscillator for timing: move to a subpane to see Stretch-Z, Slope-Z, VPO, and ±2 bands clearly.

Profile

Scalp (1–5m), Intraday (15–60m), or Swing (4H–1D). CCSV1 adjusts length/clip/pressure windows accordingly.

Overlay entries

Trade with CoRa color.

Prefer pullbacks into/through the cloud (trend direction).

If chop guard is active, wait; let the market “breathe” before engaging.

Oscillator timing

Look for Funded Flips: Slope-Z crossing 0 in the direction of VPO (i.e., momentum + funded pressure).