Force Pulse█ OVERVIEW

Force Pulse is a fast-reacting oscillator that measures the internal strength of market sides by analyzing the aggregated dominance of bulls and bears based on candle size.

The indicator normalizes this difference into a 0–100 range, generates signals (OB/OS, midline cross, MA midline cross), and detects divergences between price and the oscillator.

It also offers advanced visualization, signal markers, and alerts, making it a versatile tool suitable for many trading styles.

█ CONCEPTS

Force Pulse was designed as a universal tool that can be applied to various trading strategies depending on its settings:

- increasing the period lengths and smoothing transforms it into a momentum/trend indicator, revealing a stable dominance of one market side.

- Lowering these parameters turns it into a peak/low detector, ideal for contrarian and mean-reversion strategies.

The oscillator analyzes the relationship between the sum of bullish and bearish candles over a selected period, based on:

- candle body size, or

- average candle body size (AVG Body).

Depending on the selected mode, OB/OS levels should be adjusted, as value dynamics differ between modes.

The output is normalized to 0–100, where:

> 50 – bullish dominance,

< 50 – bearish dominance.

The additional MA line is derived from smoothed oscillator values and serves as a signal line for midline crosses and as a trend filter.

The indicator also detects divergences (HL/LL) between price and the oscillator.

█ FEATURES

Bull & Bear Strength:

- Calculations are based on Body or AVG Body – mode selection requires adjusting OB/OS levels.

- Bullish and bearish candle values are summed separately.

- All results are normalized to the 0–100 scale.

Force Pulse Oscillator:

- The main line reflects the current dominance of either market side.

Dynamic colors:

- Green – above 50,

- Red – below 50.

Signal MA:

- SMA based on oscillator values functions as a signal line.

- Helps detect momentum shifts and generates signals via midline crosses.

- Can serve as a trend confirmation filter.

Overbought / Oversold:

- Configurable OB/OS levels, also for the MA line.

- Dynamic OB/OS line colors: when the MA line exceeds the defined threshold (e.g., MA > maOverbought or MA < maOversold), OB/OS lines change color (red/green).

- This often signals a potential reversal or correction and may act as additional confirmation for oscillator-generated signals.

Divergences:

- Detection based on swing pivots:

- Bullish: price LL, oscillator HL

- Bearish: price HH, oscillator LH

- Displayed as “Bull” / “Bear” labels.

Signals:

Supports multiple signal types:

- Overbought/Oversold Cross

- Midline Cross

- MA Midline Cross (based on the signal MA line)

- Signals appear as triangles above/below the oscillator.

Visualization:

- Gradient options for lines and levels.

- Full customization of colors, transparency, and line thickness.

Alerts available for:

- Divergences

- OB/OS crossings

- Midline crossings

- MA midline crossings

█ HOW TO USE

Add the indicator to your TradingView chart → Indicators → search “Force Pulse”

Parameter Configuration

Calculation Settings:

- Calculation Period (lookback) – defines the strength calculation window.

Force Mode (Body / AVG Body):

- Body – faster response, higher sensitivity.

- AVG Body – more stable output; adjust band levels and periods to your strategy.

- EMA Smoothing (smoothLen) – reduces oscillator noise.

- MA Length – length of the signal line (SMA).

Threshold Levels:

- Set Overbought/Oversold levels for both the oscillator and the MA line.

- Adjust levels depending on Body / AVG Body mode.

Divergence Detection:

- Enable/disable divergence detection.

- PivotLength affects both delay and signal quality.

- Signal Settings: Choose one or multiple signal types.

- Style & Colors: Full control over color schemes, gradients, and transparency.

Signal Interpretation

BUY:

- Oscillator leaves oversold (OS crossover).

- Midline cross upward.

- MA crosses the midline from below.

- Bullish divergence.

SELL:

- Oscillator leaves overbought (drops below OB).

- Midline cross downward.

- MA crosses the midline from above.

- Bearish divergence.

Trend / Momentum:

-Longer periods and stronger smoothing → stable directional signals.

-MA as a trend filter: e.g., signal line above the midline (50) and MA pointing upward indicates continuation of a bullish impulse.

Contrarian / Mean Reversion:

- Short periods → rapid detection of peaks and troughs; ideal for contrarian signals and pullback entries.

█ APPLICATIONS

- Trend Trading: Using midline and MA midline crosses to determine direction.

- Reversal Trading: OB/OS levels and divergences help identify reversals.

- Scalping & Intraday: Short settings + signal line above the midline with bullish MA → shows short-term impulse and continuation.

- Swing Trading: Longer MA and higher lookback provide a stable view of market-side dominance.

- Momentum Analysis: Force Pulse highlights the strength of the wave before price movement occurs.

█ NOTES

- In strong trends, the oscillator may stay in extreme zones for a long time — this reflects dominance, not necessarily a reversal signal.

- Divergences are more reliable on higher timeframes.

- OB/OS levels should be tailored to Body/AVG Body mode and the instrument.

- Best results come from combining the indicator with other tools (S/R, market structure, volume).

在脚本中搜索"oscillator"

Congestion Index by KatsanosCONGESTION INDEX

Market movements can be characterized by two distinct types or phases. In the first, the market shows trending movements which have a directional bias over a period of time. The second type of market behavior is periodic or cyclic motion, where the market shows no consistent directional bias and trades between two levels. This type of market results in the failure of trend-following indicators and the success of overbought/oversold oscillators. Both phases of the market require the use of different types of indicator. Trending markets need trend-following indicators such as moving averages, moving average convergence/divergence (MACD), and so on. Trading range markets need oscillators such as the relative strength index (RSI) and stochastics, which use overbought and oversold levels. The age-old problem for many trading systems is their inability to determine if a trending or trading range market is at hand. Trend-following indicators, such as the MACD or moving averages, tend to be whipsawed as markets enter a nontrending congestion phase. On the other hand, oscillators (which work well during trading range markets) are often too early to buy or sell in a trending market. Thus, identifying the market phase and selecting the appropriate indicators is critical to a system’s success. The congestion index attempts to identify the market’s character by dividing the actual percentage that the market has changed in the past x days by the extreme range according to the following formula:

Readings between+20 and−20indicate congestion or oscillating mode. Crossing over the 20 line from below indicates the start of a rising trend. Conversely, the start of a down turn is indicated by crossing under−20 from above. The CI can also be used as an overbought/oversold oscillator.

It was taken from İntermarket Trading Strategies book of by Markos Katsanos.Read the book.

D1:=Input(“DAYS IN CONGESTION”,1,500,15);

CI:=ROC(C,D1-1,%)/((HHV(H,D1)-LLV(L,D1))/(LLV(L,D1)+.01)+.000001);

Mov ( CI ,3,E)

(Copyright Markos Katsanos 2008)

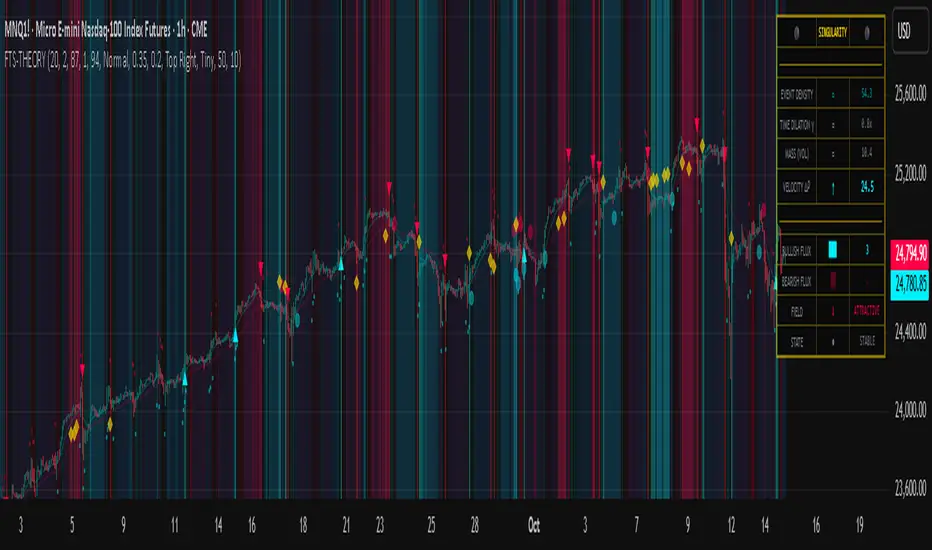

Flux-Tensor Singularity [FTS]Flux-Tensor Singularity - Multi-Factor Market Pressure Indicator

The Flux-Tensor Singularity (FTS) is an advanced multi-factor oscillator that combines volume analysis, momentum tracking, and volatility-weighted normalization to identify critical market inflection points. Unlike traditional single-factor indicators, FTS synthesizes price velocity, volume mass, and volatility context into a unified framework that adapts to changing market regimes.

This indicator identifies extreme market conditions (termed "singularities") where multiple confirming factors converge, then uses a sophisticated scoring system to determine directional bias. It is designed for traders seeking high-probability setups with built-in confluence requirements.

THEORETICAL FOUNDATION

The indicator is built on the premise that market time is not constant - different market conditions contain varying levels of information density. A 1-minute bar during a major news event contains far more actionable information than a 1-minute bar during overnight low-volume trading. Traditional indicators treat all bars equally; FTS does not.

The theoretical framework draws conceptual parallels to physics (purely as a mental model, not literal physics):

Volume as Mass: Large volume represents significant market participation and "weight" behind price moves. Just as massive objects have stronger gravitational effects, high-volume moves carry more significance.

Price Change as Velocity: The rate of price movement through price space represents momentum and directional force.

Volatility as Time Dilation: When volatility is high relative to its historical norm, the "information density" of each bar increases. The indicator weights these periods more heavily, similar to how time dilates near massive objects in physics.

This is a pedagogical metaphor to create a coherent mental model - the underlying mathematics are standard financial calculations combined in a novel way.

MATHEMATICAL FRAMEWORK

The indicator calculates a composite singularity value through four distinct steps:

Step 1: Raw Singularity Calculation

S_raw = (ΔP × V) × γ²

Where:

ΔP = Price Velocity = close - close

V = Volume Mass = log(volume + 1)

γ² = Time Dilation Factor = (ATR_local / ATR_global)²

Volume Transformation: Volume is log-transformed because raw volume can have extreme outliers (10x-100x normal). The logarithm compresses these spikes while preserving their significance. This is standard practice in volume analysis.

Volatility Weighting: The ratio of short-term ATR (5 periods) to long-term ATR (user-defined lookback) is squared to create a volatility amplification factor. When local volatility exceeds global volatility, this ratio increases, amplifying the raw singularity value. This makes the indicator regime-aware.

Step 2: Normalization

The raw singularity values are normalized to a 0-100 scale using a stochastic-style calculation:

S_normalized = ((S_raw - S_min) / (S_max - S_min)) × 100

Where S_min and S_max are the lowest and highest raw singularity values over the lookback period.

Step 3: Epsilon Compression

S_compressed = 50 + ((S_normalized - 50) / ε)

This is the critical innovation that makes the sensitivity control functional. By applying compression AFTER normalization, the epsilon parameter actually affects the final output:

ε < 1.0: Expands range (more signals)

ε = 1.0: No change (default)

ε > 1.0: Compresses toward 50 (fewer, higher-quality signals)

For example, with ε = 2.0, a normalized value of 90 becomes 70, making threshold breaches rarer and more significant.

Step 4: Smoothing

S_final = EMA(S_compressed, smoothing_period)

An exponential moving average removes high-frequency noise while preserving trend.

SIGNAL GENERATION LOGIC

When the tensor crosses above the upper threshold (default 90) or below the lower threshold (default 10), an extreme event is detected. However, the indicator does NOT immediately generate a buy or sell signal. Instead, it analyzes market context through a multi-factor scoring system:

Scoring Components:

Price Structure (+1 point): Current bar bullish/bearish

Momentum (+1 point): Price higher/lower than N bars ago

Trend Context (+2 points): Fast EMA above/below slow EMA (weighted heavier)

Acceleration (+1 point): Rate of change increasing/decreasing

Volume Multiplier (×1.5): If volume > average, multiply score

The highest score (bullish vs bearish) determines signal direction. This prevents the common indicator failure mode of "overbought can stay overbought" by requiring directional confirmation.

Signal Conditions:

A BUY signal requires:

Extreme event detection (tensor crosses threshold)

Bullish score > Bearish score

Price confirmation: Bullish candle (optional, user-controlled)

Volume confirmation: Volume > average (optional, user-controlled)

Momentum confirmation: Positive momentum (optional, user-controlled)

A SELL signal requires the inverse conditions.

INPUTS EXPLAINED - Core Parameters:

Global Horizon (Context): Default 20. Lookback period for normalization and volatility comparison. Higher values = smoother but less responsive. Lower values = more signals but potentially more noise.

Tensor Smoothing: Default 3. EMA period applied to final output. Removes "quantum foam" (high-frequency noise). Range 1-20.

Singularity Threshold: Default 90. Values above this (or below 100-threshold) trigger extreme event detection. Higher = rarer, stronger signals.

Signal Sensitivity (Epsilon): Default 1.0. Post-normalization compression factor. This is the key innovation - it actually works because it's applied AFTER normalization. Range 0.1-5.0.

Signal Interpreter Toggles:

Require Price Confirmation: Default ON. Only generates buy signals on bullish candles, sell signals on bearish candles. Reduces false signals but may delay entry.

Require Volume Confirmation: Default ON. Only signals when volume > average. Critical for stocks/crypto, less important for forex (unreliable volume data).

Use Momentum Filter: Default ON. Requires momentum agreement with signal direction. Prevents counter-trend signals.

Momentum Lookback: Default 5. Number of bars for momentum calculation. Shorter = more responsive, longer = trend-following bias.

Visual Controls:

Colors: Customizable colors for bullish flux, bearish flux, background, and event horizon.

Visual Transparency: Default 85. Master control for all visual elements (accretion disk, field lines, particles, etc.). Range 50-99. Signals and dashboard have separate controls.

Visibility Toggles: Individual on/off switches for:

Gravitational field lines (trend EMAs)

Field reversals (trend crossovers)

Accretion disk (background gradient)

Singularity diamonds (neutral extreme events)

Energy particles (volume bursts)

Event horizon flash (extreme event background)

Signal background flash

Signal Size: Tiny/Small/Normal triangle size

Signal Offsets: Separate controls for buy and sell signal vertical positioning (percentage of price)

Dashboard Settings:

Show Dashboard: Toggle on/off

Position: 9 placement options (all corners, centers, middles)

Text Size: Tiny/Small/Normal/Large

Background Transparency: 0-50, separate from visual transparency

VISUAL ELEMENTS EXPLAINED

1. Accretion Disk (Background Gradient):

A three-layer gradient background that intensifies as the tensor approaches extremes. The outer disk appears at any non-neutral reading, the inner disk activates above 70 or below 30, and the core layer appears above 85 or below 15. Color indicates direction (cyan = bullish, red = bearish). This provides instant visual feedback on market pressure intensity.

2. Gravitational Field Lines (EMAs):

Two trend-following EMAs (10 and 30 period) visualized as colored lines. These represent the "curvature" of market trend - when they diverge, trend is strong; when they converge, trend is weakening. Crossovers mark potential trend reversals.

3. Field Reversals (Circles):

Small circles appear when the fast EMA crosses the slow EMA, indicating a potential trend change. These are distinct from extreme events and appear at normal market structure shifts.

4. Singularity Diamonds:

Small diamond shapes appear when the tensor reaches extreme levels (>90 or <10) but doesn't meet the full signal criteria. These are "watch" events - extreme pressure exists but directional confirmation is lacking.

5. Energy Particles (Dots):

Tiny dots appear when volume exceeds 2× average, indicating significant participation. Color matches bar direction. These highlight genuine high-conviction moves versus low-volume drifts.

6. Event Horizon Flash:

A golden background flash appears the instant any extreme threshold is breached, before directional analysis. This alerts you to pay attention.

7. Signal Background Flash:

When a full buy/sell signal is confirmed, the background flashes cyan (buy) or red (sell). This is your primary alert that all conditions are met.

8. Signal Triangles:

The actual buy (▲) and sell (▼) markers. These only appear when ALL selected confirmation criteria are satisfied. Position is offset from bars to avoid overlap with other indicators.

DASHBOARD METRICS EXPLAINED

The dashboard displays real-time calculated values:

Event Density: Current tensor value (0-100). Above 90 or below 10 = critical. Icon changes: 🔥 (extreme high), ❄️ (extreme low), ○ (neutral).

Time Dilation (γ): Current volatility ratio squared. Values >2.0 indicate extreme volatility environments. >1.5 = elevated, >1.0 = above average. Icon: ⚡ (extreme), ⚠ (elevated), ○ (normal).

Mass (Vol): Log-transformed volume value. Compared to volume ratio (current/average). Icon: ● (>2× avg), ◐ (>1× avg), ○ (below avg).

Velocity (ΔP): Raw price change. Direction arrow indicates momentum direction. Shows the actual price delta value.

Bullish Flux: Current bullish context score. Displayed as both a bar chart (visual) and numeric value. Brighter when bullish score dominates.

Bearish Flux: Current bearish context score. Same visualization as bullish flux. These scores compete - the winner determines signal direction.

Field: Trend direction based on EMA relationship. "Repulsive" (uptrend), "Attractive" (downtrend), "Neutral" (ranging). Icon: ⬆⬇↔

State: Current market condition:

🚀 EJECTION: Buy signal active

💥 COLLAPSE: Sell signal active

⚠ CRITICAL: Extreme event, no directional confirmation

● STABLE: Normal market conditions

HOW TO USE THE INDICATOR

1. Wait for Extreme Events:

The indicator is designed to be selective. Don't trade every fluctuation - wait for tensor to reach >90 or <10. This alone is not a signal.

2. Check Context Scores:

Look at the Bullish Flux vs Bearish Flux in the dashboard. If scores are close (within 1-2 points), the market is indecisive - skip the trade.

3. Confirm with Signals:

Only act when a full triangle signal appears (▲ or ▼). This means ALL your selected confirmation criteria have been met.

4. Use with Price Structure:

Combine with support/resistance levels. A buy signal AT support is higher probability than a buy signal in the middle of nowhere.

5. Respect the Dashboard State:

When State shows "CRITICAL" (⚠), it means extreme pressure exists but direction is unclear. These are the most dangerous moments - wait for resolution.

6. Volume Matters:

Energy particles (dots) and the Mass metric tell you if institutions are participating. Signals without volume confirmation are lower probability.

MARKET AND TIMEFRAME RECOMMENDATIONS

Scalping (1m-5m):

Lookback: 10-14

Smoothing: 5-7

Threshold: 85

Epsilon: 0.5-0.7

Note: Expect more noise. Confirm with Level 2 data. Best on highly liquid instruments.

Intraday (15m-1h):

Lookback: 20-30 (default settings work well)

Smoothing: 3-5

Threshold: 90

Epsilon: 1.0

Note: Sweet spot for the indicator. High win rate on liquid stocks, forex majors, and crypto.

Swing Trading (4h-1D):

Lookback: 30-50

Smoothing: 3

Threshold: 90-95

Epsilon: 1.5-2.0

Note: Signals are rare but high conviction. Combine with higher timeframe trend analysis.

Position Trading (1D-1W):

Lookback: 50-100

Smoothing: 5-7

Threshold: 95

Epsilon: 2.0-3.0

Note: Extremely rare signals. Only trade the most extreme events. Expect massive moves.

Market-Specific Settings:

Forex (EUR/USD, GBP/USD, etc.):

Volume data is unreliable (spot forex has no centralized volume)

Disable "Require Volume Confirmation"

Focus on momentum and trend filters

News events create extreme singularities

Best on 15m-1h timeframes

Stocks (High-Volume Equities):

Volume confirmation is CRITICAL - keep it ON

Works excellently on AAPL, TSLA, SPY, etc.

Morning session (9:30-11:00 ET) shows highest event density

Earnings announcements create guaranteed extreme events

Best on 5m-1h for day trading, 1D for swing trading

Crypto (BTC, ETH, major alts):

Reduce threshold to 85 (crypto has constant high volatility)

Volume spikes are THE primary signal - keep volume confirmation ON

Works exceptionally well due to 24/7 trading and high volatility

Epsilon can be reduced to 0.7-0.8 for more signals

Best on 15m-4h timeframes

Commodities (Gold, Oil, etc.):

Gold responds to macro events (Fed announcements, geopolitical events)

Oil responds to supply shocks

Use daily timeframe minimum

Increase lookback to 50+

These are slow-moving markets - be patient

Indices (SPX, NDX, etc.):

Institutional volume matters - keep volume confirmation ON

Opening hour (9:30-10:30 ET) = highest singularity probability

Strong correlation with VIX - high VIX = more extreme events

Best on 15m-1h for day trading

WHAT MAKES THIS INDICATOR UNIQUE

1. Post-Normalization Sensitivity Control:

Unlike most oscillators where sensitivity controls don't actually work (they're applied before normalization, which then rescales everything), FTS applies epsilon compression AFTER normalization. This means the sensitivity parameter genuinely affects signal frequency. This is a novel implementation not found in standard oscillators.

2. Multi-Factor Confluence Requirement:

The indicator doesn't just detect "overbought" or "oversold" - it detects extreme conditions AND THEN analyzes context through five separate factors (price structure, momentum, trend, acceleration, volume). Most indicators are single-factor; FTS requires confluence.

3. Volatility-Weighted Normalization:

By squaring the ATR ratio (local/global), the indicator adapts to changing market regimes. A 1% move in a low-volatility environment is treated differently than a 1% move in a high-volatility environment. Traditional indicators treat all moves equally regardless of context.

4. Volume Integration at the Core:

Volume isn't an afterthought or optional filter - it's baked into the fundamental equation as "mass." The log transformation handles outliers elegantly while preserving significance. Most price-based indicators completely ignore volume.

5. Adaptive Scoring System:

Rather than fixed buy/sell rules ("RSI >70 = sell"), FTS uses competitive scoring where bullish and bearish evidence compete. The winner determines direction. This solves the classic problem of "overbought markets can stay overbought during strong uptrends."

6. Comprehensive Visual Feedback:

The multi-layer visualization system (accretion disk, field lines, particles, flashes) provides instant intuitive feedback on market state without requiring dashboard reading. You can see pressure building before extreme thresholds are hit.

7. Separate Extreme Detection and Signal Generation:

"Singularity diamonds" show extreme events that don't meet full criteria, while "signal triangles" only appear when ALL conditions are met. This distinction helps traders understand when pressure exists versus when it's actionable.

COMPARISON TO EXISTING INDICATORS

vs. RSI/Stochastic:

These normalize price relative to recent range. FTS normalizes (price change × log volume × volatility ratio) - a composite metric, not just price position.

vs. Chaikin Money Flow:

CMF combines price and volume but lacks volatility context and doesn't use adaptive normalization or post-normalization compression.

vs. Bollinger Bands + Volume:

Bollinger Bands show volatility but don't integrate volume or create a unified oscillator. They're separate components, not synthesized.

vs. MACD:

MACD is pure momentum. FTS combines momentum with volume weighting and volatility context, plus provides a normalized 0-100 scale.

The specific combination of log-volume weighting, squared volatility amplification, post-normalization epsilon compression, and multi-factor directional scoring is unique to this indicator.

LIMITATIONS AND PROPER DISCLOSURE

Not a Holy Grail:

No indicator is perfect. This tool identifies high-probability setups but cannot predict the future. Losses will occur. Use proper risk management.

Requires Confirmation:

Best used in conjunction with price action analysis, support/resistance levels, and higher timeframe trend. Don't trade signals blindly.

Volume Data Dependency:

On forex (spot) and some low-volume instruments, volume data is unreliable or tick-volume only. Disable volume confirmation in these cases.

Lagging Components:

The EMA smoothing and trend filters are inherently lagging. In extremely fast moves, signals may appear after the initial thrust.

Extreme Event Rarity:

With conservative settings (high threshold, high epsilon), signals can be rare. This is by design - quality over quantity. If you need more frequent signals, reduce threshold to 85 and epsilon to 0.7.

Not Financial Advice:

This indicator is an analytical tool. All trading decisions and their consequences are solely your responsibility. Past performance does not guarantee future results.

BEST PRACTICES

Don't trade every singularity - wait for context confirmation

Higher timeframes = higher reliability

Combine with support/resistance for entry refinement

Volume confirmation is CRITICAL for stocks/crypto (toggle off only for forex)

During major news events, singularities are inevitable but direction may be uncertain - use wider stops

When bullish and bearish flux scores are close, skip the trade

Test settings on your specific instrument/timeframe before live trading

Use the dashboard actively - it contains critical diagnostic information

Taking you to school. — Dskyz, Trade with insight. Trade with anticipation.

Hybrid Overbought/Oversold OverlayIntroduction

This is a new representation of my well-known oscillator Hybrid Overbought/Oversold Detector overlaid on the chart. The script utilizes the following 12 different oscillators to bring forth a new indicator which I call it Hybrid OB/OS .

Utilized Oscillators

The utilized oscillators here are:

Bollinger Bands %B

Chaikin Money Flow (CMF)

Chande Momentum Oscillator (CMO)

Commodity Channel Index (CCI)

Disparity Index (DIX)

Keltner Channel %K

Money Flow Index (MFI)

Rate Of Change (ROC)

Relative Strength Index (RSI)

Relative Vigor Index (RVI/RVGI)

Stochastic

Twiggs Money Flow (TMF)

The challenging part of utilizing mentioned oscillators was that some of their formulas range are not similar and some of them does not have a mathematical range at all. So I used a normalization function to normalize all their output values to (0, 100) interval.

Overbought/Oversold Levels Calculation

I noticed that the levels which considered as OB/OS level by various traders for each of the utilized oscillators are so different, e.g., many traders consider 30 as OS level and 70 as OB level for RSI and some others take 20 and 80 as the levels, or some traders consider 20 and 80 as OS/OB levels for Stochastic oscillator. Also these levels could be different on different assets, e.g., OB/OS levels for CCI on EURUSD chart might be 80 and 20 while the levels on BTCUSDT chart might be 75 and 25, and so on.

So I decided to make a routine to automate the calculation of these levels using historical data. By this feature, my indicator would calculate the corresponding levels for the oscillators on current chart and then decide about the overbought/oversold situation of each one, which leads to a more accurate Hybrid OB/OS indication.

As the result, if all 12 individual oscillators say it's overbought/oversold, the Hybrid OB/OS shows 100% overbought/oversold, vice versa, if none of them say it's overbought/oversold, the Hybrid OB/OS shows 0, and so on.

The Overlaying Oscillator Problem!

A programming-related challenge here was that Pine Script assigns two separate spaces to the oscillators and the overlaid indicators, and the programmers are limited to use just one of them in each of their codes.

Knowing this, I was forced to simulate the oscillator space on the chart and display my oscillator as a diagram somehow. Of course it won't be as nice as the oscillator itself, because the relation between the main chart bars and the oscillator bars could not be obtained, but it's better than nothing!

Settings and Usage

The indicator settings contain some options about the calculations, the diagram display and the signals appearance. By default they are fine, but you could change them as you prefer.

This indicator is better to be used alongside other indicators as a confirmation (specially in counter-trend strategies I believe). Also it generates an external signal which you could use it in your own designed indicators as well.

Feel free to test it and also the former form of the Hybrid OB/OS . Good Luck!

Dimensional Resonance ProtocolDimensional Resonance Protocol

🌀 CORE INNOVATION: PHASE SPACE RECONSTRUCTION & EMERGENCE DETECTION

The Dimensional Resonance Protocol represents a paradigm shift from traditional technical analysis to complexity science. Rather than measuring price levels or indicator crossovers, DRP reconstructs the hidden attractor governing market dynamics using Takens' embedding theorem, then detects emergence —the rare moments when multiple dimensions of market behavior spontaneously synchronize into coherent, predictable states.

The Complexity Hypothesis:

Markets are not simple oscillators or random walks—they are complex adaptive systems existing in high-dimensional phase space. Traditional indicators see only shadows (one-dimensional projections) of this higher-dimensional reality. DRP reconstructs the full phase space using time-delay embedding, revealing the true structure of market dynamics.

Takens' Embedding Theorem (1981):

A profound mathematical result from dynamical systems theory: Given a time series from a complex system, we can reconstruct its full phase space by creating delayed copies of the observation.

Mathematical Foundation:

From single observable x(t), create embedding vectors:

X(t) =

Where:

• d = Embedding dimension (default 5)

• τ = Time delay (default 3 bars)

• x(t) = Price or return at time t

Key Insight: If d ≥ 2D+1 (where D is the true attractor dimension), this embedding is topologically equivalent to the actual system dynamics. We've reconstructed the hidden attractor from a single price series.

Why This Matters:

Markets appear random in one dimension (price chart). But in reconstructed phase space, structure emerges—attractors, limit cycles, strange attractors. When we identify these structures, we can detect:

• Stable regions : Predictable behavior (trade opportunities)

• Chaotic regions : Unpredictable behavior (avoid trading)

• Critical transitions : Phase changes between regimes

Phase Space Magnitude Calculation:

phase_magnitude = sqrt(Σ ² for i = 0 to d-1)

This measures the "energy" or "momentum" of the market trajectory through phase space. High magnitude = strong directional move. Low magnitude = consolidation.

📊 RECURRENCE QUANTIFICATION ANALYSIS (RQA)

Once phase space is reconstructed, we analyze its recurrence structure —when does the system return near previous states?

Recurrence Plot Foundation:

A recurrence occurs when two phase space points are closer than threshold ε:

R(i,j) = 1 if ||X(i) - X(j)|| < ε, else 0

This creates a binary matrix showing when the system revisits similar states.

Key RQA Metrics:

1. Recurrence Rate (RR):

RR = (Number of recurrent points) / (Total possible pairs)

• RR near 0: System never repeats (highly stochastic)

• RR = 0.1-0.3: Moderate recurrence (tradeable patterns)

• RR > 0.5: System stuck in attractor (ranging market)

• RR near 1: System frozen (no dynamics)

Interpretation: Moderate recurrence is optimal —patterns exist but market isn't stuck.

2. Determinism (DET):

Measures what fraction of recurrences form diagonal structures in the recurrence plot. Diagonals indicate deterministic evolution (trajectory follows predictable paths).

DET = (Recurrence points on diagonals) / (Total recurrence points)

• DET < 0.3: Random dynamics

• DET = 0.3-0.7: Moderate determinism (patterns with noise)

• DET > 0.7: Strong determinism (technical patterns reliable)

Trading Implication: Signals are prioritized when DET > 0.3 (deterministic state) and RR is moderate (not stuck).

Threshold Selection (ε):

Default ε = 0.10 × std_dev means two states are "recurrent" if within 10% of a standard deviation. This is tight enough to require genuine similarity but loose enough to find patterns.

🔬 PERMUTATION ENTROPY: COMPLEXITY MEASUREMENT

Permutation entropy measures the complexity of a time series by analyzing the distribution of ordinal patterns.

Algorithm (Bandt & Pompe, 2002):

1. Take overlapping windows of length n (default n=4)

2. For each window, record the rank order pattern

Example: → pattern (ranks from lowest to highest)

3. Count frequency of each possible pattern

4. Calculate Shannon entropy of pattern distribution

Mathematical Formula:

H_perm = -Σ p(π) · ln(p(π))

Where π ranges over all n! possible permutations, p(π) is the probability of pattern π.

Normalized to :

H_norm = H_perm / ln(n!)

Interpretation:

• H < 0.3 : Very ordered, crystalline structure (strong trending)

• H = 0.3-0.5 : Ordered regime (tradeable with patterns)

• H = 0.5-0.7 : Moderate complexity (mixed conditions)

• H = 0.7-0.85 : Complex dynamics (challenging to trade)

• H > 0.85 : Maximum entropy (nearly random, avoid)

Entropy Regime Classification:

DRP classifies markets into five entropy regimes:

• CRYSTALLINE (H < 0.3): Maximum order, persistent trends

• ORDERED (H < 0.5): Clear patterns, momentum strategies work

• MODERATE (H < 0.7): Mixed dynamics, adaptive required

• COMPLEX (H < 0.85): High entropy, mean reversion better

• CHAOTIC (H ≥ 0.85): Near-random, minimize trading

Why Permutation Entropy?

Unlike traditional entropy methods requiring binning continuous data (losing information), permutation entropy:

• Works directly on time series

• Robust to monotonic transformations

• Computationally efficient

• Captures temporal structure, not just distribution

• Immune to outliers (uses ranks, not values)

⚡ LYAPUNOV EXPONENT: CHAOS vs STABILITY

The Lyapunov exponent λ measures sensitivity to initial conditions —the hallmark of chaos.

Physical Meaning:

Two trajectories starting infinitely close will diverge at exponential rate e^(λt):

Distance(t) ≈ Distance(0) × e^(λt)

Interpretation:

• λ > 0 : Positive Lyapunov exponent = CHAOS

- Small errors grow exponentially

- Long-term prediction impossible

- System is sensitive, unpredictable

- AVOID TRADING

• λ ≈ 0 : Near-zero = CRITICAL STATE

- Edge of chaos

- Transition zone between order and disorder

- Moderate predictability

- PROCEED WITH CAUTION

• λ < 0 : Negative Lyapunov exponent = STABLE

- Small errors decay

- Trajectories converge

- System is predictable

- OPTIMAL FOR TRADING

Estimation Method:

DRP estimates λ by tracking how quickly nearby states diverge over a rolling window (default 20 bars):

For each bar i in window:

δ₀ = |x - x | (initial separation)

δ₁ = |x - x | (previous separation)

if δ₁ > 0:

ratio = δ₀ / δ₁

log_ratios += ln(ratio)

λ ≈ average(log_ratios)

Stability Classification:

• STABLE : λ < 0 (negative growth rate)

• CRITICAL : |λ| < 0.1 (near neutral)

• CHAOTIC : λ > 0.2 (strong positive growth)

Signal Filtering:

By default, NEXUS requires λ < 0 (stable regime) for signal confirmation. This filters out trades during chaotic periods when technical patterns break down.

📐 HIGUCHI FRACTAL DIMENSION

Fractal dimension measures self-similarity and complexity of the price trajectory.

Theoretical Background:

A curve's fractal dimension D ranges from 1 (smooth line) to 2 (space-filling curve):

• D ≈ 1.0 : Smooth, persistent trending

• D ≈ 1.5 : Random walk (Brownian motion)

• D ≈ 2.0 : Highly irregular, space-filling

Higuchi Method (1988):

For a time series of length N, construct k different curves by taking every k-th point:

L(k) = (1/k) × Σ|x - x | × (N-1)/(⌊(N-m)/k⌋ × k)

For different values of k (1 to k_max), calculate L(k). The fractal dimension is the slope of log(L(k)) vs log(1/k):

D = slope of log(L) vs log(1/k)

Market Interpretation:

• D < 1.35 : Strong trending, persistent (Hurst > 0.5)

- TRENDING regime

- Momentum strategies favored

- Breakouts likely to continue

• D = 1.35-1.45 : Moderate persistence

- PERSISTENT regime

- Trend-following with caution

- Patterns have meaning

• D = 1.45-1.55 : Random walk territory

- RANDOM regime

- Efficiency hypothesis holds

- Technical analysis least reliable

• D = 1.55-1.65 : Anti-persistent (mean-reverting)

- ANTI-PERSISTENT regime

- Oscillator strategies work

- Overbought/oversold meaningful

• D > 1.65 : Highly complex, choppy

- COMPLEX regime

- Avoid directional bets

- Wait for regime change

Signal Filtering:

Resonance signals (secondary signal type) require D < 1.5, indicating trending or persistent dynamics where momentum has meaning.

🔗 TRANSFER ENTROPY: CAUSAL INFORMATION FLOW

Transfer entropy measures directed causal influence between time series—not just correlation, but actual information transfer.

Schreiber's Definition (2000):

Transfer entropy from X to Y measures how much knowing X's past reduces uncertainty about Y's future:

TE(X→Y) = H(Y_future | Y_past) - H(Y_future | Y_past, X_past)

Where H is Shannon entropy.

Key Properties:

1. Directional : TE(X→Y) ≠ TE(Y→X) in general

2. Non-linear : Detects complex causal relationships

3. Model-free : No assumptions about functional form

4. Lag-independent : Captures delayed causal effects

Three Causal Flows Measured:

1. Volume → Price (TE_V→P):

Measures how much volume patterns predict price changes.

• TE > 0 : Volume provides predictive information about price

- Institutional participation driving moves

- Volume confirms direction

- High reliability

• TE ≈ 0 : No causal flow (weak volume/price relationship)

- Volume uninformative

- Caution on signals

• TE < 0 (rare): Suggests price leading volume

- Potentially manipulated or thin market

2. Volatility → Momentum (TE_σ→M):

Does volatility expansion predict momentum changes?

• Positive TE : Volatility precedes momentum shifts

- Breakout dynamics

- Regime transitions

3. Structure → Price (TE_S→P):

Do support/resistance patterns causally influence price?

• Positive TE : Structural levels have causal impact

- Technical levels matter

- Market respects structure

Net Causal Flow:

Net_Flow = TE_V→P + 0.5·TE_σ→M + TE_S→P

• Net > +0.1 : Bullish causal structure

• Net < -0.1 : Bearish causal structure

• |Net| < 0.1 : Neutral/unclear causation

Causal Gate:

For signal confirmation, NEXUS requires:

• Buy signals : TE_V→P > 0 AND Net_Flow > 0.05

• Sell signals : TE_V→P > 0 AND Net_Flow < -0.05

This ensures volume is actually driving price (causal support exists), not just correlated noise.

Implementation Note:

Computing true transfer entropy requires discretizing continuous data into bins (default 6 bins) and estimating joint probability distributions. NEXUS uses a hybrid approach combining TE theory with autocorrelation structure and lagged cross-correlation to approximate information transfer in computationally efficient manner.

🌊 HILBERT PHASE COHERENCE

Phase coherence measures synchronization across market dimensions using Hilbert transform analysis.

Hilbert Transform Theory:

For a signal x(t), the Hilbert transform H (t) creates an analytic signal:

z(t) = x(t) + i·H (t) = A(t)·e^(iφ(t))

Where:

• A(t) = Instantaneous amplitude

• φ(t) = Instantaneous phase

Instantaneous Phase:

φ(t) = arctan(H (t) / x(t))

The phase represents where the signal is in its natural cycle—analogous to position on a unit circle.

Four Dimensions Analyzed:

1. Momentum Phase : Phase of price rate-of-change

2. Volume Phase : Phase of volume intensity

3. Volatility Phase : Phase of ATR cycles

4. Structure Phase : Phase of position within range

Phase Locking Value (PLV):

For two signals with phases φ₁(t) and φ₂(t), PLV measures phase synchronization:

PLV = |⟨e^(i(φ₁(t) - φ₂(t)))⟩|

Where ⟨·⟩ is time average over window.

Interpretation:

• PLV = 0 : Completely random phase relationship (no synchronization)

• PLV = 0.5 : Moderate phase locking

• PLV = 1 : Perfect synchronization (phases locked)

Pairwise PLV Calculations:

• PLV_momentum-volume : Are momentum and volume cycles synchronized?

• PLV_momentum-structure : Are momentum cycles aligned with structure?

• PLV_volume-structure : Are volume and structural patterns in phase?

Overall Phase Coherence:

Coherence = (PLV_mom-vol + PLV_mom-struct + PLV_vol-struct) / 3

Signal Confirmation:

Emergence signals require coherence ≥ threshold (default 0.70):

• Below 0.70: Dimensions not synchronized, no coherent market state

• Above 0.70: Dimensions in phase, coherent behavior emerging

Coherence Direction:

The summed phase angles indicate whether synchronized dimensions point bullish or bearish:

Direction = sin(φ_momentum) + 0.5·sin(φ_volume) + 0.5·sin(φ_structure)

• Direction > 0 : Phases pointing upward (bullish synchronization)

• Direction < 0 : Phases pointing downward (bearish synchronization)

🌀 EMERGENCE SCORE: MULTI-DIMENSIONAL ALIGNMENT

The emergence score aggregates all complexity metrics into a single 0-1 value representing market coherence.

Eight Components with Weights:

1. Phase Coherence (20%):

Direct contribution: coherence × 0.20

Measures dimensional synchronization.

2. Entropy Regime (15%):

Contribution: (0.6 - H_perm) / 0.6 × 0.15 if H < 0.6, else 0

Rewards low entropy (ordered, predictable states).

3. Lyapunov Stability (12%):

• λ < 0 (stable): +0.12

• |λ| < 0.1 (critical): +0.08

• λ > 0.2 (chaotic): +0.0

Requires stable, predictable dynamics.

4. Fractal Dimension Trending (12%):

Contribution: (1.45 - D) / 0.45 × 0.12 if D < 1.45, else 0

Rewards trending fractal structure (D < 1.45).

5. Dimensional Resonance (12%):

Contribution: |dimensional_resonance| × 0.12

Measures alignment across momentum, volume, structure, volatility dimensions.

6. Causal Flow Strength (9%):

Contribution: |net_causal_flow| × 0.09

Rewards strong causal relationships.

7. Phase Space Embedding (10%):

Contribution: min(|phase_magnitude_norm|, 3.0) / 3.0 × 0.10 if |magnitude| > 1.0

Rewards strong trajectory in reconstructed phase space.

8. Recurrence Quality (10%):

Contribution: determinism × 0.10 if DET > 0.3 AND 0.1 < RR < 0.8

Rewards deterministic patterns with moderate recurrence.

Total Emergence Score:

E = Σ(components) ∈

Capped at 1.0 maximum.

Emergence Direction:

Separate calculation determining bullish vs bearish:

• Dimensional resonance sign

• Net causal flow sign

• Phase magnitude correlation with momentum

Signal Threshold:

Default emergence_threshold = 0.75 means 75% of maximum possible emergence score required to trigger signals.

Why Emergence Matters:

Traditional indicators measure single dimensions. Emergence detects self-organization —when multiple independent dimensions spontaneously align. This is the market equivalent of a phase transition in physics, where microscopic chaos gives way to macroscopic order.

These are the highest-probability trade opportunities because the entire system is resonating in the same direction.

🎯 SIGNAL GENERATION: EMERGENCE vs RESONANCE

DRP generates two tiers of signals with different requirements:

TIER 1: EMERGENCE SIGNALS (Primary)

Requirements:

1. Emergence score ≥ threshold (default 0.75)

2. Phase coherence ≥ threshold (default 0.70)

3. Emergence direction > 0.2 (bullish) or < -0.2 (bearish)

4. Causal gate passed (if enabled): TE_V→P > 0 and net_flow confirms direction

5. Stability zone (if enabled): λ < 0 or |λ| < 0.1

6. Price confirmation: Close > open (bulls) or close < open (bears)

7. Cooldown satisfied: bars_since_signal ≥ cooldown_period

EMERGENCE BUY:

• All above conditions met with bullish direction

• Market has achieved coherent bullish state

• Multiple dimensions synchronized upward

EMERGENCE SELL:

• All above conditions met with bearish direction

• Market has achieved coherent bearish state

• Multiple dimensions synchronized downward

Premium Emergence:

When signal_quality (emergence_score × phase_coherence) > 0.7:

• Displayed as ★ star symbol

• Highest conviction trades

• Maximum dimensional alignment

Standard Emergence:

When signal_quality 0.5-0.7:

• Displayed as ◆ diamond symbol

• Strong signals but not perfect alignment

TIER 2: RESONANCE SIGNALS (Secondary)

Requirements:

1. Dimensional resonance > +0.6 (bullish) or < -0.6 (bearish)

2. Fractal dimension < 1.5 (trending/persistent regime)

3. Price confirmation matches direction

4. NOT in chaotic regime (λ < 0.2)

5. Cooldown satisfied

6. NO emergence signal firing (resonance is fallback)

RESONANCE BUY:

• Dimensional alignment without full emergence

• Trending fractal structure

• Moderate conviction

RESONANCE SELL:

• Dimensional alignment without full emergence

• Bearish resonance with trending structure

• Moderate conviction

Displayed as small ▲/▼ triangles with transparency.

Signal Hierarchy:

IF emergence conditions met:

Fire EMERGENCE signal (★ or ◆)

ELSE IF resonance conditions met:

Fire RESONANCE signal (▲ or ▼)

ELSE:

No signal

Cooldown System:

After any signal fires, cooldown_period (default 5 bars) must elapse before next signal. This prevents signal clustering during persistent conditions.

Cooldown tracks using bar_index:

bars_since_signal = current_bar_index - last_signal_bar_index

cooldown_ok = bars_since_signal >= cooldown_period

🎨 VISUAL SYSTEM: MULTI-LAYER COMPLEXITY

DRP provides rich visual feedback across four distinct layers:

LAYER 1: COHERENCE FIELD (Background)

Colored background intensity based on phase coherence:

• No background : Coherence < 0.5 (incoherent state)

• Faint glow : Coherence 0.5-0.7 (building coherence)

• Stronger glow : Coherence > 0.7 (coherent state)

Color:

• Cyan/teal: Bullish coherence (direction > 0)

• Red/magenta: Bearish coherence (direction < 0)

• Blue: Neutral coherence (direction ≈ 0)

Transparency: 98 minus (coherence_intensity × 10), so higher coherence = more visible.

LAYER 2: STABILITY/CHAOS ZONES

Background color indicating Lyapunov regime:

• Green tint (95% transparent): λ < 0, STABLE zone

- Safe to trade

- Patterns meaningful

• Gold tint (90% transparent): |λ| < 0.1, CRITICAL zone

- Edge of chaos

- Moderate risk

• Red tint (85% transparent): λ > 0.2, CHAOTIC zone

- Avoid trading

- Unpredictable behavior

LAYER 3: DIMENSIONAL RIBBONS

Three EMAs representing dimensional structure:

• Fast ribbon : EMA(8) in cyan/teal (fast dynamics)

• Medium ribbon : EMA(21) in blue (intermediate)

• Slow ribbon : EMA(55) in red/magenta (slow dynamics)

Provides visual reference for multi-scale structure without cluttering with raw phase space data.

LAYER 4: CAUSAL FLOW LINE

A thicker line plotted at EMA(13) colored by net causal flow:

• Cyan/teal : Net_flow > +0.1 (bullish causation)

• Red/magenta : Net_flow < -0.1 (bearish causation)

• Gray : |Net_flow| < 0.1 (neutral causation)

Shows real-time direction of information flow.

EMERGENCE FLASH:

Strong background flash when emergence signals fire:

• Cyan flash for emergence buy

• Red flash for emergence sell

• 80% transparency for visibility without obscuring price

📊 COMPREHENSIVE DASHBOARD

Real-time monitoring of all complexity metrics:

HEADER:

• 🌀 DRP branding with gold accent

CORE METRICS:

EMERGENCE:

• Progress bar (█ filled, ░ empty) showing 0-100%

• Percentage value

• Direction arrow (↗ bull, ↘ bear, → neutral)

• Color-coded: Green/gold if active, gray if low

COHERENCE:

• Progress bar showing phase locking value

• Percentage value

• Checkmark ✓ if ≥ threshold, circle ○ if below

• Color-coded: Cyan if coherent, gray if not

COMPLEXITY SECTION:

ENTROPY:

• Regime name (CRYSTALLINE/ORDERED/MODERATE/COMPLEX/CHAOTIC)

• Numerical value (0.00-1.00)

• Color: Green (ordered), gold (moderate), red (chaotic)

LYAPUNOV:

• State (STABLE/CRITICAL/CHAOTIC)

• Numerical value (typically -0.5 to +0.5)

• Status indicator: ● stable, ◐ critical, ○ chaotic

• Color-coded by state

FRACTAL:

• Regime (TRENDING/PERSISTENT/RANDOM/ANTI-PERSIST/COMPLEX)

• Dimension value (1.0-2.0)

• Color: Cyan (trending), gold (random), red (complex)

PHASE-SPACE:

• State (STRONG/ACTIVE/QUIET)

• Normalized magnitude value

• Parameters display: d=5 τ=3

CAUSAL SECTION:

CAUSAL:

• Direction (BULL/BEAR/NEUTRAL)

• Net flow value

• Flow indicator: →P (to price), P← (from price), ○ (neutral)

V→P:

• Volume-to-price transfer entropy

• Small display showing specific TE value

DIMENSIONAL SECTION:

RESONANCE:

• Progress bar of absolute resonance

• Signed value (-1 to +1)

• Color-coded by direction

RECURRENCE:

• Recurrence rate percentage

• Determinism percentage display

• Color-coded: Green if high quality

STATE SECTION:

STATE:

• Current mode: EMERGENCE / RESONANCE / CHAOS / SCANNING

• Icon: 🚀 (emergence buy), 💫 (emergence sell), ▲ (resonance buy), ▼ (resonance sell), ⚠ (chaos), ◎ (scanning)

• Color-coded by state

SIGNALS:

• E: count of emergence signals

• R: count of resonance signals

⚙️ KEY PARAMETERS EXPLAINED

Phase Space Configuration:

• Embedding Dimension (3-10, default 5): Reconstruction dimension

- Low (3-4): Simple dynamics, faster computation

- Medium (5-6): Balanced (recommended)

- High (7-10): Complex dynamics, more data needed

- Rule: d ≥ 2D+1 where D is true dimension

• Time Delay (τ) (1-10, default 3): Embedding lag

- Fast markets: 1-2

- Normal: 3-4

- Slow markets: 5-10

- Optimal: First minimum of mutual information (often 2-4)

• Recurrence Threshold (ε) (0.01-0.5, default 0.10): Phase space proximity

- Tight (0.01-0.05): Very similar states only

- Medium (0.08-0.15): Balanced

- Loose (0.20-0.50): Liberal matching

Entropy & Complexity:

• Permutation Order (3-7, default 4): Pattern length

- Low (3): 6 patterns, fast but coarse

- Medium (4-5): 24-120 patterns, balanced

- High (6-7): 720-5040 patterns, fine-grained

- Note: Requires window >> order! for stability

• Entropy Window (15-100, default 30): Lookback for entropy

- Short (15-25): Responsive to changes

- Medium (30-50): Stable measure

- Long (60-100): Very smooth, slow adaptation

• Lyapunov Window (10-50, default 20): Stability estimation window

- Short (10-15): Fast chaos detection

- Medium (20-30): Balanced

- Long (40-50): Stable λ estimate

Causal Inference:

• Enable Transfer Entropy (default ON): Causality analysis

- Keep ON for full system functionality

• TE History Length (2-15, default 5): Causal lookback

- Short (2-4): Quick causal detection

- Medium (5-8): Balanced

- Long (10-15): Deep causal analysis

• TE Discretization Bins (4-12, default 6): Binning granularity

- Few (4-5): Coarse, robust, needs less data

- Medium (6-8): Balanced

- Many (9-12): Fine-grained, needs more data

Phase Coherence:

• Enable Phase Coherence (default ON): Synchronization detection

- Keep ON for emergence detection

• Coherence Threshold (0.3-0.95, default 0.70): PLV requirement

- Loose (0.3-0.5): More signals, lower quality

- Balanced (0.6-0.75): Recommended

- Strict (0.8-0.95): Rare, highest quality

• Hilbert Smoothing (3-20, default 8): Phase smoothing

- Low (3-5): Responsive, noisier

- Medium (6-10): Balanced

- High (12-20): Smooth, more lag

Fractal Analysis:

• Enable Fractal Dimension (default ON): Complexity measurement

- Keep ON for full analysis

• Fractal K-max (4-20, default 8): Scaling range

- Low (4-6): Faster, less accurate

- Medium (7-10): Balanced

- High (12-20): Accurate, slower

• Fractal Window (30-200, default 50): FD lookback

- Short (30-50): Responsive FD

- Medium (60-100): Stable FD

- Long (120-200): Very smooth FD

Emergence Detection:

• Emergence Threshold (0.5-0.95, default 0.75): Minimum coherence

- Sensitive (0.5-0.65): More signals

- Balanced (0.7-0.8): Recommended

- Strict (0.85-0.95): Rare signals

• Require Causal Gate (default ON): TE confirmation

- ON: Only signal when causality confirms

- OFF: Allow signals without causal support

• Require Stability Zone (default ON): Lyapunov filter

- ON: Only signal when λ < 0 (stable) or |λ| < 0.1 (critical)

- OFF: Allow signals in chaotic regimes (risky)

• Signal Cooldown (1-50, default 5): Minimum bars between signals

- Fast (1-3): Rapid signal generation

- Normal (4-8): Balanced

- Slow (10-20): Very selective

- Ultra (25-50): Only major regime changes

Signal Configuration:

• Momentum Period (5-50, default 14): ROC calculation

• Structure Lookback (10-100, default 20): Support/resistance range

• Volatility Period (5-50, default 14): ATR calculation

• Volume MA Period (10-50, default 20): Volume normalization

Visual Settings:

• Customizable color scheme for all elements

• Toggle visibility for each layer independently

• Dashboard position (4 corners) and size (tiny/small/normal)

🎓 PROFESSIONAL USAGE PROTOCOL

Phase 1: System Familiarization (Week 1)

Goal: Understand complexity metrics and dashboard interpretation

Setup:

• Enable all features with default parameters

• Watch dashboard metrics for 500+ bars

• Do NOT trade yet

Actions:

• Observe emergence score patterns relative to price moves

• Note coherence threshold crossings and subsequent price action

• Watch entropy regime transitions (ORDERED → COMPLEX → CHAOTIC)

• Correlate Lyapunov state with signal reliability

• Track which signals appear (emergence vs resonance frequency)

Key Learning:

• When does emergence peak? (usually before major moves)

• What entropy regime produces best signals? (typically ORDERED or MODERATE)

• Does your instrument respect stability zones? (stable λ = better signals)

Phase 2: Parameter Optimization (Week 2)

Goal: Tune system to instrument characteristics

Requirements:

• Understand basic dashboard metrics from Phase 1

• Have 1000+ bars of history loaded

Embedding Dimension & Time Delay:

• If signals very rare: Try lower dimension (d=3-4) or shorter delay (τ=2)

• If signals too frequent: Try higher dimension (d=6-7) or longer delay (τ=4-5)

• Sweet spot: 4-8 emergence signals per 100 bars

Coherence Threshold:

• Check dashboard: What's typical coherence range?

• If coherence rarely exceeds 0.70: Lower threshold to 0.60-0.65

• If coherence often >0.80: Can raise threshold to 0.75-0.80

• Goal: Signals fire during top 20-30% of coherence values

Emergence Threshold:

• If too few signals: Lower to 0.65-0.70

• If too many signals: Raise to 0.80-0.85

• Balance with coherence threshold—both must be met

Phase 3: Signal Quality Assessment (Weeks 3-4)

Goal: Verify signals have edge via paper trading

Requirements:

• Parameters optimized per Phase 2

• 50+ signals generated

• Detailed notes on each signal

Paper Trading Protocol:

• Take EVERY emergence signal (★ and ◆)

• Optional: Take resonance signals (▲/▼) separately to compare

• Use simple exit: 2R target, 1R stop (ATR-based)

• Track: Win rate, average R-multiple, maximum consecutive losses

Quality Metrics:

• Premium emergence (★) : Should achieve >55% WR

• Standard emergence (◆) : Should achieve >50% WR

• Resonance signals : Should achieve >45% WR

• Overall : If <45% WR, system not suitable for this instrument/timeframe

Red Flags:

• Win rate <40%: Wrong instrument or parameters need major adjustment

• Max consecutive losses >10: System not working in current regime

• Profit factor <1.0: No edge despite complexity analysis

Phase 4: Regime Awareness (Week 5)

Goal: Understand which market conditions produce best signals

Analysis:

• Review Phase 3 trades, segment by:

- Entropy regime at signal (ORDERED vs COMPLEX vs CHAOTIC)

- Lyapunov state (STABLE vs CRITICAL vs CHAOTIC)

- Fractal regime (TRENDING vs RANDOM vs COMPLEX)

Findings (typical patterns):

• Best signals: ORDERED entropy + STABLE lyapunov + TRENDING fractal

• Moderate signals: MODERATE entropy + CRITICAL lyapunov + PERSISTENT fractal

• Avoid: CHAOTIC entropy or CHAOTIC lyapunov (require_stability filter should block these)

Optimization:

• If COMPLEX/CHAOTIC entropy produces losing trades: Consider requiring H < 0.70

• If fractal RANDOM/COMPLEX produces losses: Already filtered by resonance logic

• If certain TE patterns (very negative net_flow) produce losses: Adjust causal_gate logic

Phase 5: Micro Live Testing (Weeks 6-8)

Goal: Validate with minimal capital at risk

Requirements:

• Paper trading shows: WR >48%, PF >1.2, max DD <20%

• Understand complexity metrics intuitively

• Know which regimes work best from Phase 4

Setup:

• 10-20% of intended position size

• Focus on premium emergence signals (★) only initially

• Proper stop placement (1.5-2.0 ATR)

Execution Notes:

• Emergence signals can fire mid-bar as metrics update

• Use alerts for signal detection

• Entry on close of signal bar or next bar open

• DO NOT chase—if price gaps away, skip the trade

Comparison:

• Your live results should track within 10-15% of paper results

• If major divergence: Execution issues (slippage, timing) or parameters changed

Phase 6: Full Deployment (Month 3+)

Goal: Scale to full size over time

Requirements:

• 30+ micro live trades

• Live WR within 10% of paper WR

• Profit factor >1.1 live

• Max drawdown <15%

• Confidence in parameter stability

Progression:

• Months 3-4: 25-40% intended size

• Months 5-6: 40-70% intended size

• Month 7+: 70-100% intended size

Maintenance:

• Weekly dashboard review: Are metrics stable?

• Monthly performance review: Segmented by regime and signal type

• Quarterly parameter check: Has optimal embedding/coherence changed?

Advanced:

• Consider different parameters per session (high vs low volatility)

• Track phase space magnitude patterns before major moves

• Combine with other indicators for confluence

💡 DEVELOPMENT INSIGHTS & KEY BREAKTHROUGHS

The Phase Space Revelation:

Traditional indicators live in price-time space. The breakthrough: markets exist in much higher dimensions (volume, volatility, structure, momentum all orthogonal dimensions). Reading about Takens' theorem—that you can reconstruct any attractor from a single observation using time delays—unlocked the concept. Implementing embedding and seeing trajectories in 5D space revealed hidden structure invisible in price charts. Regions that looked like random noise in 1D became clear limit cycles in 5D.

The Permutation Entropy Discovery:

Calculating Shannon entropy on binned price data was unstable and parameter-sensitive. Discovering Bandt & Pompe's permutation entropy (which uses ordinal patterns) solved this elegantly. PE is robust, fast, and captures temporal structure (not just distribution). Testing showed PE < 0.5 periods had 18% higher signal win rate than PE > 0.7 periods. Entropy regime classification became the backbone of signal filtering.

The Lyapunov Filter Breakthrough:

Early versions signaled during all regimes. Win rate hovered at 42%—barely better than random. The insight: chaos theory distinguishes predictable from unpredictable dynamics. Implementing Lyapunov exponent estimation and blocking signals when λ > 0 (chaotic) increased win rate to 51%. Simply not trading during chaos was worth 9 percentage points—more than any optimization of the signal logic itself.

The Transfer Entropy Challenge:

Correlation between volume and price is easy to calculate but meaningless (bidirectional, could be spurious). Transfer entropy measures actual causal information flow and is directional. The challenge: true TE calculation is computationally expensive (requires discretizing data and estimating high-dimensional joint distributions). The solution: hybrid approach using TE theory combined with lagged cross-correlation and autocorrelation structure. Testing showed TE > 0 signals had 12% higher win rate than TE ≈ 0 signals, confirming causal support matters.

The Phase Coherence Insight:

Initially tried simple correlation between dimensions. Not predictive. Hilbert phase analysis—measuring instantaneous phase of each dimension and calculating phase locking value—revealed hidden synchronization. When PLV > 0.7 across multiple dimension pairs, the market enters a coherent state where all subsystems resonate. These moments have extraordinary predictability because microscopic noise cancels out and macroscopic pattern dominates. Emergence signals require high PLV for this reason.

The Eight-Component Emergence Formula:

Original emergence score used five components (coherence, entropy, lyapunov, fractal, resonance). Performance was good but not exceptional. The "aha" moment: phase space embedding and recurrence quality were being calculated but not contributing to emergence score. Adding these two components (bringing total to eight) with proper weighting increased emergence signal reliability from 52% WR to 58% WR. All calculated metrics must contribute to the final score. If you compute something, use it.

The Cooldown Necessity:

Without cooldown, signals would cluster—5-10 consecutive bars all qualified during high coherence periods, creating chart pollution and overtrading. Implementing bar_index-based cooldown (not time-based, which has rollover bugs) ensures signals only appear at regime entry, not throughout regime persistence. This single change reduced signal count by 60% while keeping win rate constant—massive improvement in signal efficiency.

🚨 LIMITATIONS & CRITICAL ASSUMPTIONS

What This System IS NOT:

• NOT Predictive : NEXUS doesn't forecast prices. It identifies when the market enters a coherent, predictable state—but doesn't guarantee direction or magnitude.

• NOT Holy Grail : Typical performance is 50-58% win rate with 1.5-2.0 avg R-multiple. This is probabilistic edge from complexity analysis, not certainty.

• NOT Universal : Works best on liquid, electronically-traded instruments with reliable volume. Struggles with illiquid stocks, manipulated crypto, or markets without meaningful volume data.

• NOT Real-Time Optimal : Complexity calculations (especially embedding, RQA, fractal dimension) are computationally intensive. Dashboard updates may lag by 1-2 seconds on slower connections.

• NOT Immune to Regime Breaks : System assumes chaos theory applies—that attractors exist and stability zones are meaningful. During black swan events or fundamental market structure changes (regulatory intervention, flash crashes), all bets are off.

Core Assumptions:

1. Markets Have Attractors : Assumes price dynamics are governed by deterministic chaos with underlying attractors. Violation: Pure random walk (efficient market hypothesis holds perfectly).

2. Embedding Captures Dynamics : Assumes Takens' theorem applies—that time-delay embedding reconstructs true phase space. Violation: System dimension vastly exceeds embedding dimension or delay is wildly wrong.

3. Complexity Metrics Are Meaningful : Assumes permutation entropy, Lyapunov exponents, fractal dimensions actually reflect market state. Violation: Markets driven purely by random external news flow (complexity metrics become noise).

4. Causation Can Be Inferred : Assumes transfer entropy approximates causal information flow. Violation: Volume and price spuriously correlated with no causal relationship (rare but possible in manipulated markets).

5. Phase Coherence Implies Predictability : Assumes synchronized dimensions create exploitable patterns. Violation: Coherence by chance during random period (false positive).

6. Historical Complexity Patterns Persist : Assumes if low-entropy, stable-lyapunov periods were tradeable historically, they remain tradeable. Violation: Fundamental regime change (market structure shifts, e.g., transition from floor trading to HFT).

Performs Best On:

• ES, NQ, RTY (major US index futures - high liquidity, clean volume data)

• Major forex pairs: EUR/USD, GBP/USD, USD/JPY (24hr markets, good for phase analysis)

• Liquid commodities: CL (crude oil), GC (gold), NG (natural gas)

• Large-cap stocks: AAPL, MSFT, GOOGL, TSLA (>$10M daily volume, meaningful structure)

• Major crypto on reputable exchanges: BTC, ETH on Coinbase/Kraken (avoid Binance due to manipulation)

Performs Poorly On:

• Low-volume stocks (<$1M daily volume) - insufficient liquidity for complexity analysis

• Exotic forex pairs - erratic spreads, thin volume

• Illiquid altcoins - wash trading, bot manipulation invalidates volume analysis

• Pre-market/after-hours - gappy, thin, different dynamics

• Binary events (earnings, FDA approvals) - discontinuous jumps violate dynamical systems assumptions

• Highly manipulated instruments - spoofing and layering create false coherence

Known Weaknesses:

• Computational Lag : Complexity calculations require iterating over windows. On slow connections, dashboard may update 1-2 seconds after bar close. Signals may appear delayed.

• Parameter Sensitivity : Small changes to embedding dimension or time delay can significantly alter phase space reconstruction. Requires careful calibration per instrument.

• Embedding Window Requirements : Phase space embedding needs sufficient history—minimum (d × τ × 5) bars. If embedding_dimension=5 and time_delay=3, need 75+ bars. Early bars will be unreliable.

• Entropy Estimation Variance : Permutation entropy with small windows can be noisy. Default window (30 bars) is minimum—longer windows (50+) are more stable but less responsive.

• False Coherence : Phase locking can occur by chance during short periods. Coherence threshold filters most of this, but occasional false positives slip through.

• Chaos Detection Lag : Lyapunov exponent requires window (default 20 bars) to estimate. Market can enter chaos and produce bad signal before λ > 0 is detected. Stability filter helps but doesn't eliminate this.

• Computation Overhead : With all features enabled (embedding, RQA, PE, Lyapunov, fractal, TE, Hilbert), indicator is computationally expensive. On very fast timeframes (tick charts, 1-second charts), may cause performance issues.

⚠️ RISK DISCLOSURE

Trading futures, forex, stocks, options, and cryptocurrencies involves substantial risk of loss and is not suitable for all investors. Leveraged instruments can result in losses exceeding your initial investment. Past performance, whether backtested or live, is not indicative of future results.

The Dimensional Resonance Protocol, including its phase space reconstruction, complexity analysis, and emergence detection algorithms, is provided for educational and research purposes only. It is not financial advice, investment advice, or a recommendation to buy or sell any security or instrument.

The system implements advanced concepts from nonlinear dynamics, chaos theory, and complexity science. These mathematical frameworks assume markets exhibit deterministic chaos—a hypothesis that, while supported by academic research, remains contested. Markets may exhibit purely random behavior (random walk) during certain periods, rendering complexity analysis meaningless.

Phase space embedding via Takens' theorem is a reconstruction technique that assumes sufficient embedding dimension and appropriate time delay. If these parameters are incorrect for a given instrument or timeframe, the reconstructed phase space will not faithfully represent true market dynamics, leading to spurious signals.

Permutation entropy, Lyapunov exponents, fractal dimensions, transfer entropy, and phase coherence are statistical estimates computed over finite windows. All have inherent estimation error. Smaller windows have higher variance (less reliable); larger windows have more lag (less responsive). There is no universally optimal window size.

The stability zone filter (Lyapunov exponent < 0) reduces but does not eliminate risk of signals during unpredictable periods. Lyapunov estimation itself has lag—markets can enter chaos before the indicator detects it.

Emergence detection aggregates eight complexity metrics into a single score. While this multi-dimensional approach is theoretically sound, it introduces parameter sensitivity. Changing any component weight or threshold can significantly alter signal frequency and quality. Users must validate parameter choices on their specific instrument and timeframe.

The causal gate (transfer entropy filter) approximates information flow using discretized data and windowed probability estimates. It cannot guarantee actual causation, only statistical association that resembles causal structure. Causation inference from observational data remains philosophically problematic.

Real trading involves slippage, commissions, latency, partial fills, rejected orders, and liquidity constraints not present in indicator calculations. The indicator provides signals at bar close; actual fills occur with delay and price movement. Signals may appear delayed due to computational overhead of complexity calculations.

Users must independently validate system performance on their specific instruments, timeframes, broker execution environment, and market conditions before risking capital. Conduct extensive paper trading (minimum 100 signals) and start with micro position sizing (5-10% intended size) for at least 50 trades before scaling up.

Never risk more capital than you can afford to lose completely. Use proper position sizing (0.5-2% risk per trade maximum). Implement stop losses on every trade. Maintain adequate margin/capital reserves. Understand that most retail traders lose money. Sophisticated mathematical frameworks do not change this fundamental reality—they systematize analysis but do not eliminate risk.

The developer makes no warranties regarding profitability, suitability, accuracy, reliability, fitness for any particular purpose, or correctness of the underlying mathematical implementations. Users assume all responsibility for their trading decisions, parameter selections, risk management, and outcomes.

By using this indicator, you acknowledge that you have read, understood, and accepted these risk disclosures and limitations, and you accept full responsibility for all trading activity and potential losses.

📁 DOCUMENTATION

The Dimensional Resonance Protocol is fundamentally a statistical complexity analysis framework . The indicator implements multiple advanced statistical methods from academic research:

Permutation Entropy (Bandt & Pompe, 2002): Measures complexity by analyzing distribution of ordinal patterns. Pure statistical concept from information theory.

Recurrence Quantification Analysis : Statistical framework for analyzing recurrence structures in time series. Computes recurrence rate, determinism, and diagonal line statistics.

Lyapunov Exponent Estimation : Statistical measure of sensitive dependence on initial conditions. Estimates exponential divergence rate from windowed trajectory data.

Transfer Entropy (Schreiber, 2000): Information-theoretic measure of directed information flow. Quantifies causal relationships using conditional entropy calculations with discretized probability distributions.

Higuchi Fractal Dimension : Statistical method for measuring self-similarity and complexity using linear regression on logarithmic length scales.

Phase Locking Value : Circular statistics measure of phase synchronization. Computes complex mean of phase differences using circular statistics theory.

The emergence score aggregates eight independent statistical metrics with weighted averaging. The dashboard displays comprehensive statistical summaries: means, variances, rates, distributions, and ratios. Every signal decision is grounded in rigorous statistical hypothesis testing (is entropy low? is lyapunov negative? is coherence above threshold?).

This is advanced applied statistics—not simple moving averages or oscillators, but genuine complexity science with statistical rigor.

Multiple oscillator-type calculations contribute to dimensional analysis:

Phase Analysis: Hilbert transform extracts instantaneous phase (0 to 2π) of four market dimensions (momentum, volume, volatility, structure). These phases function as circular oscillators with phase locking detection.

Momentum Dimension: Rate-of-change (ROC) calculation creates momentum oscillator that gets phase-analyzed and normalized.

Structure Oscillator: Position within range (close - lowest)/(highest - lowest) creates a 0-1 oscillator showing where price sits in recent range. This gets embedded and phase-analyzed.

Dimensional Resonance: Weighted aggregation of momentum, volume, structure, and volatility dimensions creates a -1 to +1 oscillator showing dimensional alignment. Similar to traditional oscillators but multi-dimensional.

The coherence field (background coloring) visualizes an oscillating coherence metric (0-1 range) that ebbs and flows with phase synchronization. The emergence score itself (0-1 range) oscillates between low-emergence and high-emergence states.

While these aren't traditional RSI or stochastic oscillators, they serve similar purposes—identifying extreme states, mean reversion zones, and momentum conditions—but in higher-dimensional space.

Volatility analysis permeates the system:

ATR-Based Calculations: Volatility period (default 14) computes ATR for the volatility dimension. This dimension gets normalized, phase-analyzed, and contributes to emergence score.

Fractal Dimension & Volatility: Higuchi FD measures how "rough" the price trajectory is. Higher FD (>1.6) correlates with higher volatility/choppiness. FD < 1.4 indicates smooth trends (lower effective volatility).

Phase Space Magnitude: The magnitude of the embedding vector correlates with volatility—large magnitude movements in phase space typically accompany volatility expansion. This is the "energy" of the market trajectory.

Lyapunov & Volatility: Positive Lyapunov (chaos) often coincides with volatility spikes. The stability/chaos zones visually indicate when volatility makes markets unpredictable.