Dashboard — Vol & PriceDashboard for traders

Indicator Description

1. Prev Day High

What it shows: the previous trading day's high.

Why it shows: a resistance level. Many traders watch to see if the price will hold above or below this level. A breakout can signal buying strength.

2. Prev Day Low

What it shows: the previous day's low.

Why it shows: a support level. If the price breaks downwards, it signals weakness and a possible continuation of the decline.

3. Today

What it shows:

The difference between the current price and yesterday's close (in absolute values and as a percentage).

Color: green for an increase, red for a decrease.

Why it shows: immediately shows how strong a gap or movement is today relative to yesterday. This is an indicator of current momentum.

4. ADR, % (Average Daily Range)

What it shows: Average daily range (High – Low), expressed as a percentage of the closing price, for the selected period (default 7 days).

Why it's useful: To understand the "normal" volatility of an instrument. For example, if the ADR is 3%, then a 1% move is small, while a 6% move is very large.

5. ATR (Average True Range)

What it shows: Average fluctuation range (including gaps), in absolute points, for the specified period (default 7 days).

Why it's useful: A classic volatility indicator. Useful for setting stops, calculating position sizes, and identifying "noise" movements.

6. ATR (Today), %

What it shows: How much the current movement today (from yesterday's close to the current price) represents in % of the average ATR.

Why it shows: Shows whether the instrument has "played out" its average range. If the value is already >100%, there is a high probability that the movement will begin to slow.

7. Vol (Today)

What it shows:

Current trading volume for the day (in millions/billions).

Comparison with yesterday as a percentage (for example: 77.32M (-52.78%)).

Color: green if the volume is higher than yesterday; red if lower.

Why it shows:Quickly shows whether the market is active today. Volume = fuel for price movement.

8. Avg Vol (20d)

What it shows: Average daily volume over the last 20 trading days.

Why it's useful:"normal" activity level. It's a convenient backdrop for assessing today's turnover.

9. Rel. Vol (Today), % (Relative Volume)

What it shows: Deviation of the current volume from the average (20 days).

Formula: `(today / average - 1)` * 100`.

+30% = volume 30% above average, -40% = 40% below average.

Color: green for +, red for –.

Why it's useful:A key indicator for a trader. If RelVol > 100% (green), the market is "charged," and the movement is more significant. If low, activity is weak and movements are less reliable.

10. Normalized RS (Relative Strength)

What it shows: the relative strength of a stock to a selected benchmark (e.g., SPY), normalized by the period (default 7 days).

100 = same result as the market.

> 100 = the stock is stronger than the index.

<100 = weaker than the index.

Why it's needed: filtering ideas. Strong stocks rise faster when the market rises, weak stocks fall more sharply. This helps trade in the direction of the trend and select the best candidates.

In summary:

Prev High / Low — key support and resistance levels.

Today — an instant understanding of the current momentum.

ADR and ATR — volatility and potential movement.

ATR (Today) — how much the instrument has already "run."

Vol + Rel.Vol — activity and confirmation of the movement's strength.

RS — selecting strong/weak leaders against the market.

在脚本中搜索"spy"

SMC ORB vs Pre-Market SPY/IWMStacks institutional confluences such as Smart Money Concepts, Inner Circle Trading, volatility, and structure.

Plots Premarket high/low and 15 minute Opening range

Plots the first sweep of Premarket high/low and any subsequent orb breaks

Local Hurst Slope [Dynamic Regime]1. HOW THE INDICATOR WORKS (Math → Market Edge)Step

Math

Market Intuition

1. Log-Returns

r_t = log(P_t / P_{t-1})

Removes scale, makes series stationary

2. R/S per τ

R = max(cum_dev) - min(cum_dev)

S = stdev(segment)

Measures memory strength over window τ

3. H(τ) = log(R/S) / log(τ)

Di Matteo (2007)

H > 0.5 → Trend memory

H < 0.5 → Mean-reversion

4. Slope = dH/d(log τ)

Linear regression of H vs log(τ)

Slope > 0.12 → Trend accelerating

Slope < -0.08 → Reversion emerging

LEADING EDGE: The slope changes 3–20 bars BEFORE price confirms

→ You enter before the crowd, exit before the trap

Slope > +0.12 + Strong Trend = Bullish = Long

Slope +0.05 to +0.12 = Weak Trend = Cautious = Hold/Trail

Slope -0.05 to +0.05 = Random = No Edge

Slope-0.08 to -0.05 = Weak Reversion = Bearish setup = Prepare Short

Slope < -0.08 = Strong Reversion = Bearish= Short

PRO TIPS

Only trade in direction of 200-day SMA

Filters false signals

Avoid trading 3 days before/after earnings

Volatility kills edge

Use on ETFs (SPY, QQQ)

Cleaner than single stocks

Combine with RSI(14)

RSI < 30 + Hurst short = nuclear reversal

Volume Area 80 Rule Pro - Adaptive RTHSummary in one paragraph

Adaptive value area 80 percent rule for index futures large cap equities liquid crypto and major FX on intraday timeframes. It focuses activity only when multiple context gates align. It is original because the classic prior day value area traverse is fused with a daily regime classifier that remaps the operating parameters in real time.

Scope and intent

• Markets. ES NQ SPY QQQ large cap equities BTC ETH major FX pairs and other liquid RTH instruments

• Timeframes. One minute to one hour with daily regime context

• Default demo used in the publication. ES1 on five minutes

• Purpose. Trade only the balanced days where the 80 percent traverse has edge while standing aside or tightening rules during trend or shock

Originality and usefulness

• Unique fusion. Prior day value area logic plus a rolling daily regime classifier using percentile ranks of realized volatility and ADX. The regime remaps hold time end of window stop buffer and value area coverage on each session

• Failure mode addressed. False starts during strong trend or shock sessions and weak traverses during quiet grind

• Testability. All gates are visible in Inputs and debug flags can be plotted so users can verify why a suggestion appears

• Portable yardstick. The regime uses ATR divided by close and ADX percent ranks which behave consistently across symbols

Method overview in plain language

The script builds the prior session profile during regular trading hours. At the first regular bar it freezes yesterday value area low value area high and point of control. It then evaluates the current session open location the first thirty minute volume rank the open gap rank and an opening drive test. In parallel a daily series classifies context into Calm Balance Trend or Shock from rolling percentile ranks of realized volatility and ADX. The classifier scales the rules. Calm uses longer holds and a slightly wider value area. Trend and Shock shorten the window reduce holds and enlarge stop buffers.

Base measures

• Range basis. True Range smoothed over a configurable length on both the daily and intraday series

• Return basis. Not required. ATR over close is the unit for regime strength

Components

• Prior Value Area Engine. Builds yesterday value area low value area high and point of control from a binned volume profile with automatic TPO fallback and minimum integrity guards

• Opening Location. Detects whether the session opens above the prior value area or below it

• Inside Hold Counter. Counts consecutive bars that hold inside the value area after a re entry

• Volume Gate. Percentile of the first thirty minutes volume over a rolling sample

• Gap Gate. Percentile rank of the regular session open gap over a rolling sample

• Drive Gate. Opening drive check using a multiple of intraday ATR

• Regime Classifier. Percentile ranks of daily ATR over close and daily ADX classify Calm Balance Trend Shock and remap parameters

• Session windows optional. Windows follow the chart exchange time

Fusion rule

Minimum satisfied gates approach. A re entry must hold inside the value area for a regime scaled number of bars while the volume gap and drive gates allow the setup. The regime simultaneously scales value area coverage end minute time stop and stop buffer.

Signal rule

• Long suggestion appears when price opens below yesterday value area then re enters and holds for the required bars while all gates allow the setup

• Short suggestion appears when price opens above yesterday value area then re enters and holds for the required bars while all gates allow the setup

• WAIT shows implicitly when any required gate is missing

• Exit labels mark target touch stop touch or a time based close

Inputs with guidance

Setup

• Signal timeframe. Uses the chart by default

• Session windows optional. Start and end minutes inside regular trading hours

• Invert direction is not used. The logic is symmetric

Logic

• Hold bars inside value area. Typical range 3 to 12. Raising it reduces trades and favors better traverses. Lowering it increases frequency and risk of false starts

• Earliest minute since RTH open and Latest minute since RTH open. Typical range 0 to 390. Reducing the latest minute cuts late session trades

• Time stop bars after entry. Typical range 6 to 30. Larger values give setups more room

Filters

• Value area coverage. Typical range 0.70 to 0.85. Higher coverage narrows the traverse but accepts fewer days

• Bin size in ticks. Typical range 1 to 8. Larger bins stabilize noisy profiles

• Stop buffer ticks beyond edge. Typical range 2 to 20. Larger buffers survive noise

• First thirty minute volume percentile. Typical range 0.30 to 0.70. Higher values require more active opens

• Gap filter percentile. Typical range 0.70 to 0.95. Lower values block more gap days

• Opening drive multiple and bars. Higher multiple or longer bars block strong directional opens

Adaptivity

• Lookback days for regime ranks. Typical 150 to 500

• Calm RV percentile. Typical 25 to 45

• Trend ADX percentile. Typical 55 to 75

• Shock RV percentile. Typical 75 to 90

• End minute ratio in Trend and Shock. Typical 0.5 to 0.8

• Hold and Time stop scales per regime. Use values near one to keep behavior close to static settings

Realism and responsible publication

• No performance claims. Past results never guarantee future outcomes

• Shapes can move while a bar forms and settle on close

• Sessions use the chart exchange time

Honest limitations and failure modes

• Economic releases and thin liquidity can break the balance premise

• Gap heavy symbols may work better with stronger gap filters and a True Range focus

• Very quiet regimes reduce signal contrast. Consider longer windows or higher thresholds

Legal

Education and research only. Not investment advice. Test in simulation before any live use.

Daniel.Yer Volume Breakout Signal🧠 Summary – Daniel.Yer Volume Breakout Signal

The indicator only works on time frames of minutes.

An indicator that detects high-volume breakouts after the market opens and highlights potential entry zones.

Based on sampling the opening volume window and comparing it to the session’s volume peak.

Visually marks preparation areas (colored background) and plots BUY/SELL triangles for confirmation candles.

Includes real-time alert conditions for leading tickers: SPY, AAPL, MSFT, META, AMD, TSLA, NVDA, PLTR, GOOG, and AMZN.

Optimized for day trading — provides actionable alerts even when the user is offline.

Grizzly Brahman · PRO SCALPERGrizzly Brahman TMAX 4 is a fourth-generation Trend-Momentum-Adaptive Crossover system built to identify true intraday direction and volatility alignment before price acceleration begins.

It combines adaptive moving-average bands, momentum filtration, and trend-fill logic to produce crystal-clear long/short zones directly on the chart.

Preset Modes

“Aggressive / Balanced / Disciplined” presets optimize responsiveness for scalping, intra-day, or swing conditions.

Session Shading & ORB Levels

Optional overlays for Opening Range Breakout, Pre-Market High/Low, and Previous Day High/Low to frame liquidity targets.

Heikin Ashi Compatibility

Optimized to read momentum flow cleanly on Heikin Ashi charts for false-breakout filtering.

Momentum Bands

Adaptive outer bands act as over-extension or “take-profit” zones — similar to ATR channels but smoothed for consistency.

How to Use

Identify Trend Zone — watch for color fill change and TMA alignment.

Enter on Marker Confirmation — green triangle = long momentum confirm, red triangle = short.

Manage Risk around outer TMA/ATR band touches or when color intensity fades.

Combine with GB Set-Up & Confirmation (lower pane) for dual-signal entry validation.

NSR Dynamic Channel - HTF + ReversionNSR Dynamic Channel – HTF Volatility + Reversion

(Beginner-friendly, pro-grade, non-repainting)

The NSR Dynamic Channel builds an adaptive volatility envelope that compares current price action to a statistically-derived “expected” range pulled from a user-selected higher timeframe (HTF).

Is this just another keltner variation?

In short: Keltner reacts. NSR anticipates.

Keltner says “price moved a lot.”

NSR says “this move is abnormal compared to the last 2 days on a higher timeframe — and here’s the probability it snaps back.”

The channel is not a simple multiple of recent ATR or standard deviation; instead it:

Samples HTF volatility over a rolling window (default: last 2 days on the chosen HTF).

Expected Range

HTF Volatility Spread = StDev of 1-bar ATR on the HTF

Scales this HTF range to the current chart’s volatility using a compression ratio :

compRatio = SMA(High-Low over lookback) / Expected Range

This makes the channel tighten in low-vol regimes and widen in high-vol regimes .

Centers the channel on a composite mean ( AVGMEAN ) calculated from:

Smoothed Adaptive Averages of the current timeframe close

SMA of close over the user-defined lookback ( Slow )

The three means are averaged to reduce lag and noise.

Draws two layers :

HTF Expected Channel (gray fill) = PAMEAN ± expectedD

Dynamic Expected Band (inner gray) = HTF Expected Range

Adds a fast 2σ envelope around AVGMEAN using the standard deviation of close over the lookback period.

Core Calculations (Conceptual Overview)

HTF Baseline → ATR on user HTF → SMA & StDev over a defined number of days

Compression Ratio → Normalizes current range to HTF “normal” volatility

Expected Band Width → Expected Range × CompressionRatio

Bias Detection → % change of composite mean over 2 bars → “bullish” / “bearish” filter

Overextension % → Position of price within the expected band (0–100%)

How to Use It (3 Steps)

Apply to any chart – defaults work on futures (NQ/ES), stocks (SPY), crypto (BTC), forex, etc.

Price is outside both the fast 2σ envelope and the HTF-scaled expected band

Expect some sort of reversion

Enable alerts – two built-in conditions:

NSR Exit Long – bullish bias + high crosses upper expected edge

NSR Exit Short – bearish bias + low crosses lower expected edge

Optional toggles :

Show 2σ Price Range → fast overextension lines

Expected Channel → HTF-based gray fill

Mean → MEAN centerline

Why It Works

Context-aware : Uses HTF “normal” volatility as anchor

Adaptive : Shrinks in consolidation, expands in breakouts

Filtered signals : Only triggers when both statistical layers agree

Non-repainting : All calculations use confirmed bars

Happy trading!

nsrgroup

Relative Rotation - RRG JdK RS-Ratio & RS-MomentumThis indicator calculates the JdK RS-Ratio and RS-Momentum, which form the basis of Relative Rotation Graphs (RRG). It compares the performance of any asset against a benchmark (default: SPY) to identify the current RRG quadrant: LEADING, WEAKENING, LAGGING, or IMPROVING.

The RS-Ratio (red line) and RS-Momentum (green line) are plotted around a baseline of 100. The background color indicates the current quadrant, and an optional feature allows coloring chart candles based on the RRG phase.

Alerts can be configured to notify when the asset transitions between quadrants, helping traders identify rotational shifts in relative strength.

Sector Relative StrengthThis indicator measures a stock's Real Relative Strength against its sector benchmark, helping you identify stocks that are outperforming or underperforming their sector peers.

The concept is based on the Real Relative Strength methodology popularized by the r/realdaytrading community.

Unlike traditional relative strength calculations that simply compare price ratios, this indicator uses a more sophisticated approach that accounts for volatility through ATR (Average True Range), providing a normalized view of true relative performance.

Key Features

Automatic Sector Detection

Automatically detects your stock's sector using TradingView's built-in sector classification

Maps to the appropriate SPDR Sector ETF (XLK, XLF, XLV, XLY, XLP, XLI, XLE, XLU, XLB, XLC)

Supports all 20 TradingView sectors

Sector ETF Mappings

The indicator automatically compares your stock against:

Technology: XLK (Technology Services, Electronic Technology)

Financials: XLF (Finance sector)

Healthcare: XLV (Health Technology, Health Services)

Consumer Discretionary: XLY (Retail Trade, Consumer Services, Consumer Durables)

Consumer Staples: XLP (Consumer Non-Durables)

Industrials: XLI (Producer Manufacturing, Industrial Services, Transportation, Commercial Services)

Energy: XLE (Energy Minerals)

Utilities: XLU

Materials: XLB (Non-Energy Minerals, Process Industries)

Communications: XLC

Default: SPY (for Miscellaneous or unclassified sectors)

Customizable Settings

Comparison Mode: Choose between automatic sector comparison or custom symbol

Length: Adjustable lookback period (default: 12)

Smoothing: Apply moving average to reduce noise (default: 3)

Visual Clarity

Green line: Stock is outperforming its sector

Red line: Stock is underperforming its sector

Zero baseline: Clear reference point for performance

Clean info box: Shows which ETF you're comparing against

How It Works

The indicator calculates relative strength using the following methodology:

Rolling Price Change: Measures the price movement over the specified length for both the stock and its sector ETF

ATR Normalization: Uses Average True Range to normalize for volatility differences

Power Index: Calculates the sector's strength relative to its volatility

Real Relative Strength: Compares the stock's performance against the sector's power index

Smoothing: Applies a moving average to reduce single-candle spikes

Formula:

Power Index = (Sector Price Change) / (Sector ATR)

RRS = (Stock Price Change - Power Index × Stock ATR) / Stock ATR

Smoothed RRS = SMA(RRS, Smoothing Length)

(FTD) Follow-Through Day SignalFollow-Through Day (FTD) Signal

This indicator detects potential Follow-Through Days (FTDs) — a concept popularized by William O’Neil — to help identify possible market trend confirmations.

A Follow-Through Day occurs when an index shows strong upside action on higher volume several days after a market low, suggesting institutional buying rather than short covering.

How it works:

The indicator checks for a session where the price gains a defined minimum percentage from the prior close (default: 1.2% or more).

Volume must be greater than the previous day’s volume.

The rally must occur at least three days after a recent low, determined by the lookback period (default: 20 days).

Additional safeguards require that recent bars are not making new lows and that the bar three days prior either closed positive or was not at a new low — filtering out false signals from oversold bounces.

When all conditions are met, a blue up arrow is plotted beneath the bar, and an optional “FTD” label appears if enabled.

Inputs:

Min % Gain from Previous Close (%): Sets the minimum daily percentage gain to qualify as a Follow-Through Day.

Lookback Period for Lowest Low Checks: Defines how many bars back to search for a recent market low (default: 20).

Show Signal Label: Toggles the on-chart “FTD” label display.

Usage:

This indicator is intended for use on daily charts of major market indexes — such as the Nasdaq Composite (symbol: IXIC) or broad index ETFs including QQQ, SPY, and DIA — where Follow-Through Day signals are most relevant for confirming potential trend reversals.

Rolling Correlation vs Another Symbol (SPY Default)This indicator visualizes the rolling correlation between the current chart symbol and another selected asset, helping traders understand how closely the two move together over time.

It calculates the Pearson correlation coefficient over a user-defined period (default 22 bars) and plots it as a color-coded line:

• Green line → positive correlation (move in the same direction)

• Red line → negative correlation (move in opposite directions)

• A gray dashed line marks the zero level (no correlation).

The background highlights periods of strong relationship:

• Light green when correlation > +0.7 (strong positive)

• Light red when correlation < –0.7 (strong negative)

Use this tool to quickly spot diversification opportunities, confirm hedges, or understand how assets interact during different market regimes.

Multi-Anchor VWAP Deviation Dashboard Overview

Multi-Anchor VWAP Deviation Dashboard (Optimized Global) is an overlay indicator that computes up to five user-defined Anchored Volume Weighted Average Prices (AVWAPs) from custom timestamps, plotting their lines and displaying real-time percentage deviations from the current close. It enables precise analysis of price positioning relative to key events (e.g., earnings, news) or periods (e.g., weekly opens), with a compact dashboard for quick scans. Optimized for performance, it uses manual iterative calculations to handle dynamic anchor changes without repainting.

Core Mechanics

The indicator focuses on efficient AVWAP computation and deviation tracking:

Anchor Configuration: Five independent anchors, each with a name, UTC timestamp (e.g., "01 Oct 2025 00:00" for monthly open), show toggle, and color. Timestamps define the calculation start—e.g., AVWAP1 from "20 Oct 2025" onward.

AVWAP Calculation: For each enabled anchor, it identifies the first bar at/after the timestamp as the reset point, then iteratively accumulates (price * volume) / total volume from there. Uses HLC3 source (customizable); handles input changes by resetting sums on new anchors.

Deviation Metric: For each AVWAP, computes % deviation = ((close - AVWAP) / AVWAP) * 100—positive = above (potential resistance), negative = below (support).

Visuals: Plots lines (linewidth 1–2, user colors); dashboard (2 columns, 6 rows) shows names (anchor-colored if enabled) and deviations (green >0%, red <0%, gray N/A), positioned user-selectable with text sizing. Updates on last bar for efficiency.

This setup scales deviations across volatilities, aiding multi-period bias assessment.

Why This Adds Value & Originality

Standard VWAPs limit to session anchors (daily/weekly); deviation tools often lack multiples. This isn't a simple mashup: Manual iterative AVWAP (no built-in ta.vwap reliance) ensures dynamic resets on timestamp tweaks—e.g., shift "Event" to FOMC date without recalc lag. The 5-anchor flexibility (arbitrary UTC times) + centralized dashboard (colored deviations at a glance) creates a "global timeline scanner" unique to event-driven trading, unlike rigid multi-VWAP scripts. It streamlines what requires 5 separate indicators, with % normalization for cross-asset comparison (e.g., SPY vs. BTC).

How to Use

Setup: Overlay on chart. Configure anchors (e.g., Anchor1: "Weekly Open" at next Monday 00:00 UTC; enable/show 2–3 for focus). Set source (HLC3 default), position (Top Right), text size (Small).

Interpret Dashboard:

Left Column: Anchor names (e.g., "Monthly Open" in orange).

Right Column: Deviations (e.g., "+1.25%" green = above, bullish exhaustion?).

Scan for confluence (e.g., all >+2% = overbought).

Trading:

Lines: Price near AVWAP = mean reversion; breaks = momentum.

Example: -0.8% below "Event" anchor post-earnings → potential bounce buy.

Use on 1H–D; adjust timestamps via calendar.

Tips: Enable 1–3 anchors to avoid clutter; test on historical events.

Limitations & Disclaimer

AVWAPs reset on anchor bars, potentially lagging mid-period; deviations are % only (add ATR for absolute). Table updates on close (no intrabar). Timestamps must be UTC/future-proof. No alerts/exits—integrate manually. Not advice; backtest deviations on your assets. Past ≠ future. Comments for ideas.

J.P. Morgan Efficiente 5 IndexJ.P. MORGAN EFFICIENTE 5 INDEX REPLICATION

Walk into any retail trading forum and you'll find the same scene playing out thousands of times a day: traders huddled over their screens, drawing trendlines on candlestick charts, hunting for the perfect entry signal, convinced that the next RSI crossover will unlock the path to financial freedom. Meanwhile, in the towers of lower Manhattan and the City of London, portfolio managers are doing something entirely different. They're not drawing lines. They're not hunting patterns. They're building fortresses of diversification, wielding mathematical frameworks that have survived decades of market chaos, and most importantly, they're thinking in portfolios while retail thinks in positions.

This divide is not just philosophical. It's structural, mathematical, and ultimately, profitable. The uncomfortable truth that retail traders must confront is this: while you're obsessing over whether the 50-day moving average will cross the 200-day, institutional investors are solving quadratic optimization problems across thirteen asset classes, rebalancing monthly according to Markowitz's Nobel Prize-winning framework, and targeting precise volatility levels that allow them to sleep at night regardless of what the VIX does tomorrow. The game you're playing and the game they're playing share the same field, but the rules are entirely different.

The question, then, is not whether retail traders can access institutional strategies. The question is whether they're willing to fundamentally change how they think about markets. Are you ready to stop painting lines and start building portfolios?

THE INSTITUTIONAL FRAMEWORK: HOW THE PROFESSIONALS ACTUALLY THINK

When Harry Markowitz published "Portfolio Selection" in The Journal of Finance in 1952, he fundamentally altered how sophisticated investors approach markets. His insight was deceptively simple: returns alone mean nothing. Risk-adjusted returns mean everything. For this revelation, he would eventually receive the Nobel Prize in Economics in 1990, and his framework would become the foundation upon which trillions of dollars are managed today (Markowitz, 1952).

Modern Portfolio Theory, as it came to be known, introduced a revolutionary concept: through diversification across imperfectly correlated assets, an investor could reduce portfolio risk without sacrificing expected returns. This wasn't about finding the single best asset. It was about constructing the optimal combination of assets. The mathematics are elegant in their logic: if two assets don't move in perfect lockstep, combining them creates a portfolio whose volatility is lower than the weighted average of the individual volatilities. This "free lunch" of diversification became the bedrock of institutional investment management (Elton et al., 2014).

But here's where retail traders miss the point entirely: this isn't about having ten different stocks instead of one. It's about systematic, mathematically rigorous allocation across asset classes with fundamentally different risk drivers. When equity markets crash, high-quality government bonds often rally. When inflation surges, commodities may provide protection even as stocks and bonds both suffer. When emerging markets are in vogue, developed markets may lag. The professional investor doesn't predict which scenario will unfold. Instead, they position for all of them simultaneously, with weights determined not by gut feeling but by quantitative optimization.

This is what J.P. Morgan Asset Management embedded into their Efficiente Index series. These are not actively managed funds where a portfolio manager makes discretionary calls. They are rules-based, systematic strategies that execute the Markowitz framework in real-time, rebalancing monthly to maintain optimal risk-adjusted positioning across global equities, fixed income, commodities, and defensive assets (J.P. Morgan Asset Management, 2016).

THE EFFICIENTE 5 STRATEGY: DECONSTRUCTING INSTITUTIONAL METHODOLOGY

The Efficiente 5 Index, specifically, targets a 5% annualized volatility. Let that sink in for a moment. While retail traders routinely accept 20%, 30%, or even 50% annual volatility in pursuit of returns, institutional allocators have determined that 5% volatility provides an optimal balance between growth potential and capital preservation. This isn't timidity. It's mathematics. At higher volatility levels, the compounding drag from large drawdowns becomes mathematically punishing. A 50% loss requires a 100% gain just to break even. The institutional solution: constrain volatility at the portfolio level, allowing the power of compounding to work unimpeded (Damodaran, 2008).

The strategy operates across thirteen exchange-traded funds spanning five distinct asset classes: developed equity markets (SPY, IWM, EFA), fixed income across the risk spectrum (TLT, LQD, HYG), emerging markets (EEM, EMB), alternatives (IYR, GSG, GLD), and defensive positioning (TIP, BIL). These aren't arbitrary choices. Each ETF represents a distinct factor exposure, and together they provide access to the primary drivers of global asset returns (Fama and French, 1993).

The methodology, as detailed in replication research by Jungle Rock (2025), follows a precise monthly cadence. At the end of each month, the strategy recalculates expected returns and volatilities for all thirteen assets using a 126-day rolling window. This six-month lookback balances responsiveness to changing market conditions against the noise of short-term fluctuations. The optimization engine then solves for the portfolio weights that maximize expected return subject to the 5% volatility target, with additional constraints to prevent excessive concentration.

These constraints are critical and reveal institutional wisdom that retail traders typically ignore. No single ETF can exceed 20% of the portfolio, except for TIP and BIL which can reach 50% given their defensive nature. At the asset class level, developed equities are capped at 50%, bonds at 50%, emerging markets at 25%, and alternatives at 25%. These aren't arbitrary limits. They're guardrails preventing the optimization from becoming too aggressive during periods when recent performance might suggest concentrating heavily in a single area that's been hot (Jorion, 1992).

After optimization, there's one final step that appears almost trivial but carries profound implications: weights are rounded to the nearest 5%. In a world of fractional shares and algorithmic execution, why round to 5%? The answer reveals institutional practicality over mathematical purity. A portfolio weight of 13.7% and 15.0% are functionally similar in their risk contribution, but the latter is vastly easier to communicate, to monitor, and to execute at scale. When you're managing billions, parsimony matters.

WHY THIS MATTERS FOR RETAIL: THE GAP BETWEEN APPROACH AND EXECUTION

Here's the uncomfortable reality: most retail traders are playing a different game entirely, and they don't even realize it. When a retail trader says "I'm bullish on tech," they buy QQQ and that's their entire technology exposure. When they say "I need some diversification," they buy ten different stocks, often in correlated sectors. This isn't diversification in the Markowitzian sense. It's concentration with extra steps.

The institutional approach represented by the Efficiente 5 is fundamentally different in several ways. First, it's systematic. Emotions don't drive the allocation. The mathematics do. When equities have rallied hard and now represent 55% of the portfolio despite a 50% cap, the system sells equities and buys bonds or alternatives, regardless of how bullish the headlines feel. This forced contrarianism is what retail traders know they should do but rarely execute (Kahneman and Tversky, 1979).

Second, it's forward-looking in its inputs but backward-looking in its process. The strategy doesn't try to predict the next crisis or the next boom. It simply measures what volatility and returns have been recently, assumes the immediate future resembles the immediate past more than it resembles some forecast, and positions accordingly. This humility regarding prediction is perhaps the most institutional characteristic of all.

Third, and most critically, it treats the portfolio as a single organism. Retail traders typically view their holdings as separate positions, each requiring individual management. The institutional approach recognizes that what matters is not whether Position A made money, but whether the portfolio as a whole achieved its risk-adjusted return target. A position can lose money and still be a valuable contributor if it reduced portfolio volatility or provided diversification during stress periods.

THE MATHEMATICAL FOUNDATION: MEAN-VARIANCE OPTIMIZATION IN PRACTICE

At its core, the Efficiente 5 strategy solves a constrained optimization problem each month. In technical terms, this is a quadratic programming problem: maximize expected portfolio return subject to a volatility constraint and position limits. The objective function is straightforward: maximize the weighted sum of expected returns. The constraint is that the weighted sum of variances and covariances must not exceed the volatility target squared (Markowitz, 1959).

The challenge, and this is crucial for understanding the Pine Script implementation, is that solving this problem properly requires calculating a covariance matrix. This 13x13 matrix captures not just the volatility of each asset but the correlation between every pair of assets. Two assets might each have 15% volatility, but if they're negatively correlated, combining them reduces portfolio risk. If they're positively correlated, it doesn't. The covariance matrix encodes these relationships.

True mean-variance optimization requires matrix algebra and quadratic programming solvers. Pine Script, by design, lacks these capabilities. The language doesn't support matrix operations, and certainly doesn't include a QP solver. This creates a fundamental challenge: how do you implement an institutional strategy in a language not designed for institutional mathematics?

The solution implemented here uses a pragmatic approximation. Instead of solving the full covariance problem, the indicator calculates a Sharpe-like ratio for each asset (return divided by volatility) and uses these ratios to determine initial weights. It then applies the individual and asset-class constraints, renormalizes, and produces the final portfolio. This isn't mathematically equivalent to true mean-variance optimization, but it captures the essential spirit: weight assets according to their risk-adjusted return potential, subject to diversification constraints.

For retail implementation, this approximation is likely sufficient. The difference between a theoretically optimal portfolio and a very good approximation is typically modest, and the discipline of systematic rebalancing across asset classes matters far more than the precise weights. Perfect is the enemy of good, and a good approximation executed consistently will outperform a perfect solution that never gets implemented (Arnott et al., 2013).

RETURNS, RISKS, AND THE POWER OF COMPOUNDING

The Efficiente 5 Index has, historically, delivered on its promise of 5% volatility with respectable returns. While past performance never guarantees future results, the framework reveals why low-volatility strategies can be surprisingly powerful. Consider two portfolios: Portfolio A averages 12% returns with 20% volatility, while Portfolio B averages 8% returns with 5% volatility. Which performs better over time?

The arithmetic return favors Portfolio A, but compound returns tell a different story. Portfolio A will experience occasional 20-30% drawdowns. Portfolio B rarely draws down more than 10%. Over a twenty-year horizon, the geometric return (what you actually experience) for Portfolio B may match or exceed Portfolio A, simply because it never gives back massive gains. This is the power of volatility management that retail traders chronically underestimate (Bernstein, 1996).

Moreover, low volatility enables behavioral advantages. When your portfolio draws down 35%, as it might with a high-volatility approach, the psychological pressure to sell at the worst possible time becomes overwhelming. When your maximum drawdown is 12%, as might occur with the Efficiente 5 approach, staying the course is far easier. Behavioral finance research has consistently shown that investor returns lag fund returns primarily due to poor timing decisions driven by emotional responses to volatility (Dalbar, 2020).

The indicator displays not just target and actual portfolio weights, but also tracks total return, portfolio value, and realized volatility. This isn't just data. It's feedback. Retail traders can see, in real-time, whether their actual portfolio volatility matches their target, whether their risk-adjusted returns are improving, and whether their allocation discipline is holding. This transparency transforms abstract concepts into concrete metrics.

WHAT RETAIL TRADERS MUST LEARN: THE MINDSET SHIFT

The path from retail to institutional thinking requires three fundamental shifts. First, stop thinking in positions and start thinking in portfolios. Your question should never be "Should I buy this stock?" but rather "How does this position change my portfolio's expected return and volatility?" If you can't answer that question quantitatively, you're not ready to make the trade.

Second, embrace systematic rebalancing even when it feels wrong. Perhaps especially when it feels wrong. The Efficiente 5 strategy rebalances monthly regardless of market conditions. If equities have surged and now exceed their target weight, the strategy sells equities and buys bonds or alternatives. Every retail trader knows this is what you "should" do, but almost none actually do it. The institutional edge isn't in having better information. It's in having better discipline (Swensen, 2009).

Third, accept that volatility is not your friend. The retail mythology that "higher risk equals higher returns" is true on average across assets, but it's not true for implementation. A 15% return with 30% volatility will compound more slowly than a 12% return with 10% volatility due to the mathematics of return distributions. Institutions figured this out decades ago. Retail is still learning.

The Efficiente 5 replication indicator provides a bridge. It won't solve the problem of prediction no indicator can. But it solves the problem of allocation, which is arguably more important. By implementing institutional methodology in an accessible format, it allows retail traders to see what professional portfolio construction actually looks like, not in theory but in executable code. The the colorful lines that retail traders love to draw, don't disappear. They simply become less central to the process. The portfolio becomes central instead.

IMPLEMENTATION CONSIDERATIONS AND PRACTICAL REALITY

Running this indicator on TradingView provides a dynamic view of how institutional allocation would evolve over time. The labels on each asset class line show current weights, updated continuously as prices change and rebalancing occurs. The dashboard displays the full allocation across all thirteen ETFs, showing both target weights (what the optimization suggests) and actual weights (what the portfolio currently holds after price movements).

Several key insights emerge from watching this process unfold. First, the strategy is not static. Weights change monthly as the optimization recalibrates to recent volatility and returns. What worked last month may not be optimal this month. Second, the strategy is not market-timing. It doesn't try to predict whether stocks will rise or fall. It simply measures recent behavior and positions accordingly. If volatility has risen, the strategy shifts toward defensive assets. If correlations have changed, the diversification benefits adjust.

Third, and perhaps most importantly for retail traders, the strategy demonstrates that sophistication and complexity are not synonyms. The Efficiente 5 methodology is sophisticated in its framework but simple in its execution. There are no exotic derivatives, no complex market-timing rules, no predictions of future scenarios. Just systematic optimization, monthly rebalancing, and discipline. This simplicity is a feature, not a bug.

The indicator also highlights limitations that retail traders must understand. The Pine Script implementation uses an approximation of true mean-variance optimization, as discussed earlier. Transaction costs are not modeled. Slippage is ignored. Tax implications are not considered. These simplifications mean the indicator is educational and analytical, not a fully operational trading system. For actual implementation, traders would need to account for these real-world factors.

Moreover, the strategy requires access to all thirteen ETFs and sufficient capital to hold meaningful positions in each. With 5% as the rounding increment, practical implementation probably requires at least $10,000 to avoid having positions that are too small to matter. The strategy is also explicitly designed for a 5% volatility target, which may be too conservative for younger investors with long time horizons or too aggressive for retirees living off their portfolio. The framework is adaptable, but adaptation requires understanding the trade-offs.

CAN RETAIL TRULY COMPETE WITH INSTITUTIONS?

The honest answer is nuanced. Retail traders will never have the same resources as institutions. They won't have Bloomberg terminals, proprietary research, or armies of analysts. But in portfolio construction, the resource gap matters less than the mindset gap. The mathematics of Markowitz are available to everyone. ETFs provide liquid, low-cost access to institutional-quality building blocks. Computing power is essentially free. The barriers are not technological or financial. They're conceptual.

If a retail trader understands why portfolios matter more than positions, why systematic discipline beats discretionary emotion, and why volatility management enables compounding, they can build portfolios that rival institutional allocation in their elegance and effectiveness. Not in their scale, not in their execution costs, but in their conceptual soundness. The Efficiente 5 framework proves this is possible.

What retail traders must recognize is that competing with institutions doesn't mean day-trading better than their algorithms. It means portfolio-building better than their average client. And that's achievable because most institutional clients, despite having access to the best managers, still make emotional decisions, chase performance, and abandon strategies at the worst possible times. The retail edge isn't in outsmarting professionals. It's in out-disciplining amateurs who happen to have more money.

The J.P. Morgan Efficiente 5 Index Replication indicator serves as both a tool and a teacher. As a tool, it provides a systematic framework for multi-asset allocation based on proven institutional methodology. As a teacher, it demonstrates daily what portfolio thinking actually looks like in practice. The colorful lines remain on the chart, but they're no longer the focus. The portfolio is the focus. The risk-adjusted return is the focus. The systematic discipline is the focus.

Stop painting lines. Start building portfolios. The institutions have been doing it for seventy years. It's time retail caught up.

REFERENCES

Arnott, R. D., Hsu, J., & Moore, P. (2013). Fundamental Indexation. Financial Analysts Journal, 61(2), 83-99.

Bernstein, W. J. (1996). The Intelligent Asset Allocator. New York: McGraw-Hill.

Dalbar, Inc. (2020). Quantitative Analysis of Investor Behavior. Boston: Dalbar.

Damodaran, A. (2008). Strategic Risk Taking: A Framework for Risk Management. Upper Saddle River: Pearson Education.

Elton, E. J., Gruber, M. J., Brown, S. J., & Goetzmann, W. N. (2014). Modern Portfolio Theory and Investment Analysis (9th ed.). Hoboken: John Wiley & Sons.

Fama, E. F., & French, K. R. (1993). Common risk factors in the returns on stocks and bonds. Journal of Financial Economics, 33(1), 3-56.

Jorion, P. (1992). Portfolio optimization in practice. Financial Analysts Journal, 48(1), 68-74.

J.P. Morgan Asset Management. (2016). Guide to the Markets. New York: J.P. Morgan.

Jungle Rock. (2025). Institutional Asset Allocation meets the Efficient Frontier: Replicating the JPMorgan Efficiente 5 Strategy. Working Paper.

Kahneman, D., & Tversky, A. (1979). Prospect Theory: An Analysis of Decision under Risk. Econometrica, 47(2), 263-291.

Markowitz, H. (1952). Portfolio Selection. The Journal of Finance, 7(1), 77-91.

Markowitz, H. (1959). Portfolio Selection: Efficient Diversification of Investments. New York: John Wiley & Sons.

Swensen, D. F. (2009). Pioneering Portfolio Management: An Unconventional Approach to Institutional Investment. New York: Free Press.

S&P Trading System with PivotsThe S&P Trading System with Pivots is a TradingView indicator designed for the 30-minute SPX chart to guide SPY options trading. It uses a trend-following strategy with:

10 SMA and 50 SMA: Plots a 10-period (blue) and 50-period (red) Simple Moving Average. A bullish crossover (10 SMA > 50 SMA) signals a potential buy (green triangle below bar), while a bearish crossunder (10 SMA < 50 SMA) signals a sell or exit (red triangle above bar).

Trend Bias: Colors the background green (bullish) or red (bearish) based on SMA positions.

Pivot Points: Marks recent highs (orange circles) and lows (purple circles) as potential resistance and support levels, using a 5-bar lookback period.

Trend Catch STFR - whipsaw Reduced### Summary of the Setup

This trading system combines **SuperTrend** (a trend-following indicator based on ATR for dynamic support/resistance), **Range Filter** (a smoothed median of the last 100 candles to identify price position relative to a baseline), and filters using **VIX Proxy** (a volatility measure: (14-period ATR / 14-period SMA of Close) × 100) and **ADX** (Average Directional Index for trend strength). It's designed for trend trading with volatility safeguards.

- **Entries**: Triggered only in "tradeable" markets (VIX Proxy ≥ 15 OR ADX ≥ 20) when SuperTrend aligns with direction (green for long, red for short), price crosses the Range Filter median accordingly, and you're not already in that position.

- **Exits**: Purely price-based—exit when SuperTrend flips or price crosses back over the Range Filter median. No forced exits from low volatility/trend.

- **No Trade Zone**: Blocks new entries if both VIX Proxy < 15 AND ADX < 20, but doesn't affect open positions.

- **Overall Goal**: Enter trends with confirmed strength/volatility, ride them via price action, and avoid ranging/choppy markets for new trades.

This creates a filtered trend-following strategy that prioritizes quality entries while letting winners run.

### Advantages

- **Reduces Noise in Entries**: The VIX Proxy and ADX filters ensure trades only in volatile or strongly trending conditions, avoiding low-momentum periods that often lead to false signals.

- **Lets Winners Run**: Exits based solely on price reversal (SuperTrend or Range Filter) allow positions to stay open during temporary lulls in volatility/trend, potentially capturing longer moves.

- **Simple and Balanced**: Combines trend (SuperTrend/ADX), range (Filter), and volatility (VIX Proxy) without overcomplicating—easy to backtest and adapt to assets like stocks, forex, or crypto.

- **Adaptable to Markets**: The "OR" logic for VIX/ADX provides flexibility (e.g., enters volatile sideways markets if ADX is low, or steady trends if VIX is low).

- **Risk Control**: Implicitly limits exposure by blocking entries in calm markets, which can preserve capital during uncertainty.

### Disadvantages

- **Whipsaws in Choppy Markets**: As you noted, SuperTrend can flip frequently in ranging conditions, leading to quick entries/exits and small losses, especially if the Range Filter isn't smoothing enough noise.

- **Missed Opportunities**: Strict filters (e.g., requiring VIX ≥ 15 or ADX ≥ 20) might skip early-stage trends or low-volatility grinds, reducing trade frequency and potential profits in quiet bull/bear markets.

- **Lagging Exits**: Relying only on price flips means you might hold losing trades longer if volatility drops without a clear reversal, increasing drawdowns.

- **Parameter Sensitivity**: Values like VIX 15, ADX 20, or Range Filter's 100-candle lookback need tuning per asset/timeframe; poor choices could amplify whipsaws or over-filter.

- **No Built-in Risk Management**: Lacks explicit stops/targets, so it relies on user-added rules (e.g., ATR-based stops), which could lead to oversized losses if not implemented.

### How to Use It

This system can be implemented in platforms like TradingView (via Pine Script), Python (e.g., with TA-Lib or Pandas), or MT4/5. Here's a step-by-step guide, assuming TradingView for simplicity—adapt as needed. (If coding in Python, use libraries like pandas_ta for indicators.)

1. **Set Up Indicators**:

- Add SuperTrend (default: ATR period 10, multiplier 3—adjust as suggested in prior tweaks).

- Create Range Filter: Use a 100-period SMA of (high + low)/2, smoothed (e.g., via EMA if desired).

- Calculate VIX Proxy: Custom script for (ATR(14) / SMA(close, 14)) * 100.

- Add ADX (period 14, standard).

2. **Define Rules in Code/Script**:

- **Long Entry**: If SuperTrend direction < 0 (green), close > RangeFilterMedian, (VIX Proxy ≥ 15 OR ADX ≥ 20), and not already long—buy on bar close.

- **Short Entry**: If SuperTrend direction > 0 (red), close < RangeFilterMedian, (VIX Proxy ≥ 15 OR ADX ≥ 20), and not already short—sell short.

- **Exit Long**: If in long and (SuperTrend > 0 OR close < RangeFilterMedian)—sell.

- **Exit Short**: If in short and (SuperTrend < 0 OR close > RangeFilterMedian)—cover.

- Monitor No Trade Zone visually (e.g., plot yellow background when VIX < 15 AND ADX < 20).

3. **Backtest and Optimize**:

- Use historical data on your asset (e.g., SPY on 1H chart).

- Test metrics: Win rate, profit factor, max drawdown. Adjust thresholds (e.g., ADX to 25) to reduce whipsaws.

- Forward-test on demo account to validate.

4. **Live Trading**:

- Apply to a chart, set alerts for entries/exits.

- Add risk rules: Position size 1-2% of capital, stop-loss at SuperTrend line.

- Monitor manually or automate via bots—avoid overtrading; use on trending assets.

For the adjustments I suggested earlier (e.g., ADX 25, 2-bar confirmation), integrate them into entries only—test one at a time to isolate improvements. If whipsaws persist, combine 2-3 tweaks.

Risk-On / Risk-Off CompositeReal-time Risk-On / Risk-Off Composite from your four ratios:

SPY / TLT (equities vs long bonds)

HYG / LQD (high-yield vs IG credit)

HG / GOLD (copper vs gold)

BTC / GOLD (speculative vs defensive)

It:

normalizes each ratio with a z-score (so they’re comparable),

lets you weight them,

plots a composite line + histogram (up = risk-on, down = risk-off),

shows a small heat-table for each sub-signal,

and includes alert conditions for Risk-On / Risk-Off flips.

Luxy Adaptive MA Cloud - Trend Strength & Signal Tracker V2Luxy Adaptive MA Cloud - Professional Trend Strength & Signal Tracker

Next-generation moving average cloud indicator combining ultra-smooth gradient visualization with intelligent momentum detection. Built for traders who demand clarity, precision, and actionable insights.

═══════════════════════════════════════════════

WHAT MAKES THIS INDICATOR SPECIAL?

═══════════════════════════════════════════════

Unlike traditional MA indicators that show static lines, Luxy Adaptive MA Cloud creates a living, breathing visualization of market momentum. Here's what sets it apart:

Exponential Gradient Technology

This isn't just a simple fill between two lines. It's a professionally engineered gradient system with 26 precision layers using exponential density distribution. The result? An organic, cloud-like appearance where the center is dramatically darker (15% transparency - where crossovers and price action occur), while edges fade gracefully (75% transparency). Think of it as a visual "heat map" of trend strength.

Dynamic Momentum Intelligence

Most MA clouds only show structure (which MA is on top). This indicator shows momentum strength in real-time through four intelligent states:

- 🟢 Bright Green = Explosive bullish momentum (both MAs rising strongly)

- 🔵 Blue = Weakening bullish (structure intact, but momentum fading)

- 🟠 Orange = Caution zone (bearish structure forming, weak momentum)

- 🔴 Deep Red = Strong bearish momentum (both MAs falling)

The cloud literally tells you when trends are accelerating or losing steam.

Conditional Performance Architecture

Every calculation is optimized for speed. Disable a feature? It stops calculating entirely—not just hidden, but not computed . The 26-layer gradient only renders when enabled. Toggle signals off? Those crossover checks don't run. This makes it one of the most efficient cloud indicators available, even with its advanced visual system.

Zero Repaint Guarantee

All signals and momentum states are based on confirmed bar data only . What you see in historical data is exactly what you would have seen trading live. No lookahead bias. No repainting tricks. No signals that "magically" appear perfect in hindsight. If a signal shows in history, it would have triggered in real-time at that exact moment.

Educational by Design

Every single input includes comprehensive tooltips with:

- Clear explanations of what each parameter does

- Practical examples of when to use different settings

- Recommended configurations for scalping, day trading, and swing trading

- Real-world trading impact ("This affects entry timing" vs "This is visual only")

You're not just getting an indicator—you're learning how to use it effectively .

═══════════════════════════════════════════════

THE GRADIENT CLOUD - TECHNICAL DETAILS

═══════════════════════════════════════════════

Architecture:

26 precision layers for silk-smooth transitions

Exponential density curve - layers packed tightly near center (where crossovers happen), spread wider at edges

75%-15% transparency range - center is highly opaque (15%), edges fade gracefully (75%)

V-Gradient design - emphasizes the action zone between Fast and Medium MAs

The Four Momentum States:

🟢 GREEN - Strong Bullish

Fast MA above Medium MA

Both MAs rising with momentum > 0.02%

Action: Enter/hold LONG positions, strong uptrend confirmed

🔵 BLUE - Weak Bullish

Fast MA above Medium MA

Weak or flat momentum

Action: Caution - bullish structure but losing strength, consider trailing stops

🟠 ORANGE - Weak Bearish

Medium MA above Fast MA

Weak or flat momentum

Action: Warning - bearish structure developing, consider exits

🔴 RED - Strong Bearish

Medium MA above Fast MA

Both MAs falling with momentum < -0.02%

Action: Enter/hold SHORT positions, strong downtrend confirmed

Smooth Transitions: The momentum score is smoothed using an 8-bar EMA to eliminate noise and prevent whipsaws. You see the true trend , not every minor fluctuation.

═══════════════════════════════════════════════

FLEXIBLE MOVING AVERAGE SYSTEM

═══════════════════════════════════════════════

Three Customizable MAs:

Fast MA (default: EMA 10) - Reacts quickly to price changes, defines short-term momentum

Medium MA (default: EMA 20) - Balances responsiveness with stability, core trend reference

Slow MA (default: SMA 200, optional) - Long-term trend filter, major support/resistance

Six MA Types Available:

EMA - Exponential; faster response, ideal for momentum and day trading

SMA - Simple; smooth and stable, best for swing trading and trend following

WMA - Weighted; middle ground between EMA and SMA

VWMA - Volume-weighted; reflects market participation, useful for liquid markets

RMA - Wilder's smoothing; used in RSI/ADX, excellent for trend filters

HMA - Hull; extremely responsive with minimal lag, aggressive option

Recommended Settings by Trading Style:

Scalping (1m-5m):

Fast: EMA(5-8)

Medium: EMA(10-15)

Slow: Not needed or EMA(50)

Day Trading (5m-1h):

Fast: EMA(10-12)

Medium: EMA(20-21)

Slow: SMA(200) for bias

Swing Trading (4h-1D):

Fast: EMA(10-20)

Medium: EMA(34-50)

Slow: SMA(200)

Pro Tip: Start with Fast < Medium < Slow lengths. The gradient works best when there's clear separation between Fast and Medium MAs.

═══════════════════════════════════════════════

CROSSOVER SIGNALS - CLEAN & RELIABLE

═══════════════════════════════════════════════

Golden Cross ⬆ LONG Signal

Fast MA crosses above Medium MA

Classic bullish reversal or trend continuation signal

Most reliable when accompanied by GREEN cloud (strong momentum)

Death Cross ⬇ SHORT Signal

Fast MA crosses below Medium MA

Classic bearish reversal or trend continuation signal

Most reliable when accompanied by RED cloud (strong momentum)

Signal Intelligence:

Anti-spam filter - Minimum 5 bars between signals prevents noise

Clean labels - Placed precisely at crossover points

Alert-ready - Built-in ALERTS for automated trading systems

No repainting - Signals based on confirmed bars only

Signal Quality Assessment:

High-Quality Entry:

Golden Cross + GREEN cloud + Price above both MAs

= Strong bullish setup ✓

Low-Quality Entry (skip or wait):

Golden Cross + ORANGE cloud + Choppy price action

= Weak bullish setup, likely whipsaw ✗

═══════════════════════════════════════════════

REAL-TIME INFO PANEL

═══════════════════════════════════════════════

An at-a-glance dashboard showing:

Trend Strength Indicator:

Visual display of current momentum state

Color-coded header matching cloud color

Instant recognition of market bias

MA Distance Table:

Shows percentage distance of price from each enabled MA:

Green rows : Price ABOVE MA (bullish)

Red rows : Price BELOW MA (bearish)

Gray rows : Price AT MA (rare, decision point)

Distance Interpretation:

+2% to +5%: Healthy uptrend

+5% to +10%: Getting extended, caution

+10%+: Overextended, expect pullback

-2% to -5%: Testing support

-5% to -10%: Oversold zone

-10%+: Deep correction or downtrend

Customization:

4 corner positions

5 font sizes (Tiny to Huge)

Toggle visibility on/off

═══════════════════════════════════════════════

HOW TO USE - PRACTICAL TRADING GUIDE

═══════════════════════════════════════════════

STRATEGY 1: Trend Following

Identify trend : Wait for GREEN (bullish) or RED (bearish) cloud

Enter on signal : Golden Cross in GREEN cloud = LONG, Death Cross in RED cloud = SHORT

Hold position : While cloud maintains color

Exit signals :

• Cloud turns ORANGE/BLUE = momentum weakening, tighten stops

• Opposite crossover = close position

• Cloud turns opposite color = full reversal

STRATEGY 2: Pullback Entries

Confirm trend : GREEN cloud established (bullish bias)

Wait for pullback : Price touches or crosses below Fast MA

Enter when : Price rebounds back above Fast MA with cloud still GREEN

Stop loss : Below Medium MA or recent swing low

Target : Previous high or when cloud weakens

STRATEGY 3: Momentum Confirmation

Your setup triggers : (e.g., chart pattern, support/resistance)

Check cloud color :

• GREEN = proceed with LONG

• RED = proceed with SHORT

• BLUE/ORANGE = skip or reduce size

Use gradient as confluence : Not as primary signal, but as momentum filter

Risk Management Tips:

Never enter against the cloud color (don't LONG in RED cloud)

Reduce position size during BLUE/ORANGE (transition periods)

Place stops beyond Medium MA for swing trades

Use Slow MA (200) as final trend filter - don't SHORT above it in uptrends

═══════════════════════════════════════════════

PERFORMANCE & OPTIMIZATION

═══════════════════════════════════════════════

Tested On:

Crypto: BTC, ETH, major altcoins

Stocks: SPY, AAPL, TSLA, QQQ

Forex: EUR/USD, GBP/USD, USD/JPY

Indices: S&P 500, NASDAQ, DJI

═══════════════════════════════════════════════

TRANSPARENCY & RELIABILITY

═══════════════════════════════════════════════

Educational Focus:

Detailed tooltips on every input

Clear documentation of methodology

Practical examples in descriptions

Teaches you why , not just what

Open Logic:

Momentum calculation: (Fast slope + Medium slope) / 2

Smoothing: 8-bar EMA to reduce noise

Thresholds: ±0.02% for strong momentum classification

Everything is transparent and explainable

═══════════════════════════════════════════════

COMPLETE FEATURE LIST

═══════════════════════════════════════════════

Visual Components:

26-layer exponential gradient cloud

3 customizable moving average lines

Golden Cross / Death Cross labels

Real-time info panel with trend strength

MA distance table

Calculation Features:

6 MA types (EMA, SMA, WMA, VWMA, RMA, HMA)

Momentum-based cloud coloring

Smoothed trend strength scoring

Conditional performance optimization

Customization Options:

All MA lengths adjustable

All colors customizable (when gradient disabled)

Panel position (4 corners)

Font sizes (5 options)

Toggle any feature on/off

Signal Features:

Anti-spam filter (configurable gap)

Clean, non-overlapping labels

Built-in alert conditions

No repainting guarantee

═══════════════════════════════════════════════

IMPORTANT DISCLAIMERS

═══════════════════════════════════════════════

This indicator is for educational and informational purposes only

Not financial advice - always do your own research

Past performance does not guarantee future results

Use proper risk management - never risk more than you can afford to lose

Test on paper/demo accounts before using with real money

Combine with other analysis methods - no single indicator is perfect

Works best in trending markets; less effective in choppy/sideways conditions

Signals may perform differently in different timeframes and market conditions

The indicator uses historical data for MA calculations - allow sufficient lookback period

═══════════════════════════════════════════════

CREDITS & TECHNICAL INFO

═══════════════════════════════════════════════

Version: 2.0

Release: October 2025

Special Thanks:

TradingView community for feedback and testing

Pine Script documentation for technical reference

═══════════════════════════════════════════════

SUPPORT & UPDATES

═══════════════════════════════════════════════

Found a bug? Comment below with:

Ticker symbol

Timeframe

Screenshot if possible

Steps to reproduce

Feature requests? I'm always looking to improve! Share your ideas in the comments.

Questions? Check the tooltips first (hover over any input) - most answers are there. If still stuck, ask in comments.

═══════════════════════════════════════════════

Happy Trading!

Remember: The best indicator is the one you understand and use consistently. Take time to learn how the cloud behaves in different market conditions. Practice on paper before going live. Trade smart, manage risk, and may the trends be with you! 🚀

Whales buy & sell🐋 Whales on Wall Street — Buy & Sell Signal Indicator

The Whales on Wall Street Signal Indicator is a precision-built trading tool designed to simplify your decision-making and give you real-time clarity in the market.

It automatically identifies high-probability reversal zones, momentum shifts, and trend confirmations — marking exact Buy (green) and Sell (red) signals based on price action, volume confirmation, and momentum strength.

Built for day traders and scalpers, this indicator eliminates the guesswork by combining multiple technical confluences such as:

EMA & RSI alignment for trend direction

Smart volume spikes for institutional activity

Volatility filters to reduce false signals

Dynamic alerts for entries and exits in real time

Whether you’re trading SPY, QQQ, NVDA, or Tesla, this indicator adapts to any ticker and timeframe — giving you crystal-clear entries, cleaner exits, and the confidence to trade like a whale.

Risk ModuleThis indicator provides a visual reference for position sizing and approximate stop and target placement. It supports trade planning by calculating equalized risk per trade and maintaining consistent exposure across different markets.

For more information about the concept, see the post Position Sizing and Risk Management .

Fixed Fractional Risk

The indicator calculates the number of shares that can be traded to maintain consistent monetary risk. The formula is based on the distance between the current price and stop reference, adjusting position size proportionally. A closer stop results in a larger position size, while a wider stop results in a smaller one.

Position Size = (Account Size × Risk %) ÷ (Entry Price – Stop Price)

Stop and Target

Stop placement is derived from volatility using the Average True Range (ATR). The target is plotted as a multiple of the stop distance, defining the risk-to-reward relationship in R units.

Stop = Price ± ATR × Multiplier

Target = Price ± (R × Risk Distance)

Chart Elements

The stop and target levels are plotted above and below the current price, with the stop marked by a red dot and the target by a green dot. The information table displayed on the chart shows the number of shares to trade, stop level, and target level.

Setup and Configuration

This configuration only needs to be set once, but can be adjusted later if preferred.

1. Start by setting the account size and risk percentage per trade to define the monetary amount risked on each trade. These values form the basis for position size calculation.

2. Set the ATR multiplier to determine stop distance, common values range between 1 and 3 ATR. Lower values place stops closer to price, increasing sensitivity but risking short-term noise. Higher values widen the stop, which reduces noise impact but extends time in risk.

3. Set the R-multiple to determine target distance relative to the stop. A value of 1 represents a 1:1 risk-to-reward relationship. Lower values reduce potential reward but tend to increase win rate, whereas higher values increase potential reward but tend to reduce win rate. The selection depends on system characteristics and trade expectancy.

When the parameters are defined, the indicator displays the stop, target, and calculated position size on the chart. All that remains is to enter the trade with the number of shares shown in the table and place bracket orders at the plotted stop and target levels.

Settings Overview

Account Size / Risk %: Defines account capital and per-trade exposure.

ATR Multiplier: Adjusts stop distance relative to volatility.

R Multiple: Sets target distance relative to stop (risk-reward ratio).

Position: Choose Long or Short direction.

Table Position: Controls information table placement and scale.

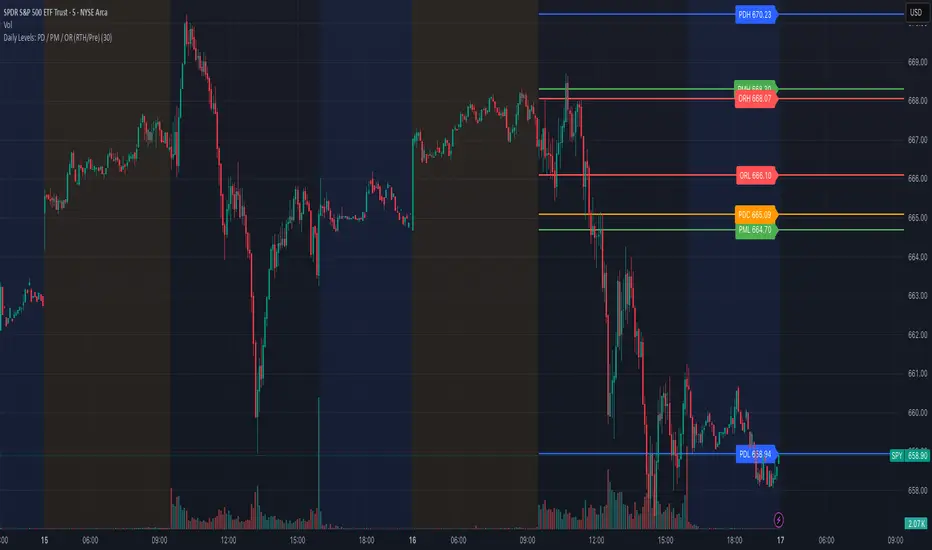

Daily Levels: PD / PM / OR (RTH/Pre)# Daily Levels: PD / PM / OR (RTH/Pre)

## Overview

This indicator displays key intraday support and resistance levels for US equity markets, specifically designed for traders who use Previous Day, Pre-Market, and Opening Range levels in their trading strategy.

## Key Features

**Seven Critical Levels Displayed:**

- **PDH (Previous Day High)** - Blue line: The highest price from yesterday's regular trading hours (9:30 AM - 4:00 PM ET)

- **PDL (Previous Day Low)** - Blue line: The lowest price from yesterday's regular trading hours

- **PDC (Previous Day Close)** - Orange line: The closing price from yesterday's regular trading hours

- **PMH (Pre-Market High)** - Yellow line: The highest price during today's pre-market session (4:00 AM - 9:30 AM ET)

- **PML (Pre-Market Low)** - Yellow line: The lowest price during today's pre-market session

- **ORH (Opening Range High)** - Red line: The highest price during the first 30 minutes of trading (9:30 AM - 10:00 AM ET)

- **ORL (Opening Range Low)** - Red line: The lowest price during the first 30 minutes of trading

## How It Works

**At 9:30 AM ET (Market Open):**

- PDH, PDL, PDC levels appear (from previous day's RTH)

- PMH, PML levels appear (from today's pre-market session)

- All lines begin at the 9:30 AM bar and extend right

**At 10:00 AM ET (Opening Range Close):**

- ORH, ORL levels appear (from today's first 30 minutes)

- Lines begin at the 9:30 AM bar and extend right

**Level Persistence:**

- All levels remain visible until the next trading day at 9:30 AM ET

- Levels reset daily for the new trading session

## Use Cases

**Day Trading:**

- Identify key support and resistance zones before placing trades

- Use PDH/PDL as potential profit targets or stop loss areas

- Monitor price reaction at pre-market levels for early trading signals

- Trade breakouts or rejections at opening range levels

**Swing Trading:**

- Assess daily momentum by observing breaks above/below previous day levels

- Use multiple timeframes while maintaining consistent reference points

**Market Structure:**

- Quickly identify if the market is trading above or below key levels

- Recognize accumulation/distribution patterns around these zones

## Technical Details

- **Timezone:** All times referenced are US Eastern Time (America/New_York)

- **Session Windows:**

- Pre-Market: 4:00 AM - 9:30 AM ET

- Regular Trading Hours: 9:30 AM - 4:00 PM ET

- Opening Range: 9:30 AM - 10:00 AM ET

- **Timeframe Agnostic:** Works on any chart timeframe

- **Visual Clarity:** Color-coded lines and labels for easy identification

## Color Scheme

- **Blue:** Previous Day levels (PDH, PDL)

- **Orange:** Previous Day Close (PDC)

- **Yellow:** Pre-Market levels (PMH, PML)

- **Red:** Opening Range levels (ORH, ORL)

## Best Practices

1. Use on US equity indices (SPY, QQQ, ES, NQ) and liquid US stocks

2. Combine with volume analysis for confirmation

3. Pay attention to how price reacts at these levels (bounce vs. break)

4. Most effective during the first 2 hours of trading when volatility is highest

5. Consider the market context (trending vs. ranging) when interpreting these levels

## Note

This indicator is specifically designed for US market hours. Results may vary when applied to international markets or instruments with different trading sessions.

Put Credit Spread System V.1A simple put credit spread system for my nephew, who likes trading. Intended for SPY, QQQ, SLV, GLD, etc if on an uptrend.

CUBE's V17CUBE’s V15.1 — Sparkles ⚡ + Cubes 🟨 + Smart/LC 🟫 + Golden ✨ (multi-signal scalper & trend helper)

CUBE’s V15.1 is a multi-module toolkit for intraday momentum and quick-scalp decision making. It blends a trend engine, VWAP/EMA50 band logic, CRT + Volume pair detection, weighted divergence, OBV-MACD regime flips, and “Sparkles” presets—then fuses them into readable Cube labels and higher-conviction Golden combos.

What it prints (signal taxonomy)

🟨 Cube ++ Incoming — pre-signal when price enters VWAP/EMA50 “yellow” bands with trend alignment.

🟨 Cube’s Buy ++ / Sell ++ — the “plus-plus” confirmations after CRT context; gated to avoid spam.

🟫 Last Chance → 🟫 Last Chance ++ — RSI + divergence-weighted follow-through (waits for a tiny UT flip).

🟪 Smart Cube — post-Cube, waits for KC(1.2) location + OBV presence + divergence stack (more selective).

✨ Golden (Sparkles + Cube) — objective confluence labels that require Sparkles (preset wins) plus a Cube event inside a short window. Comes in Golden-2 (2+ sparkles in 3 bars) and Golden-1 (tight 0–1 bar proximity).

Each label automatically shows “(Quick Scalp)” when price is inside the careful bands, so you know when to downshift risk.

The engines (under the hood)

Trend: Pivot-Point SuperTrend (PPST 2/10/3) drives bullish/bearish context (invertible).

Bands: 5-minute VWAP + EMA50 zones with symbol-aware tolerances (majors/ETFs/crypto/megacaps tuned).

CRT + Volume Spike Pair: detects recent hammer/shooter + volume conditions and uses them to gate higher tiers.

Weighted Divergence: RSI / Stoch (weighted) / CCI / MOM / OBV (weighted) / CMF / MFI (and more) with CRT-recency gates to keep it relevant.

UT micro-flips: tiny ATR trail crosses used to “arm” Last Chance ++ entries.

OBV-MACD regime: structural flips for the Super7 and Smart Cube filters.

Super7 Sparkles: five presets (4/8/15/24/40 bars) that score 9 modules; you can show compact ✨ icons or 9/9 text.

Quick start (60 seconds)

Add to a 1–5m chart of your instrument.

Leave defaults on; optionally toggle “Sparkle Settings” (the presets are already on).

Watch for:

✨ Golden Buy/Sell → higher-quality scalp setups.

🟨 Cube’s Buy/Sell ++ → momentum continuation outside the yellow bands.

🟪 Smart Cube → selective continuation after a Cube with KC/OBV/div confluence.

Use the built-in alerts (see list below) to automate.

Inputs & customization highlights

Invert Trend Logic — flips bull/bear interpretation (useful in range regimes).

Reference TF label anchoring — place labels using a reference timeframe; optional “(tf)” tag.

Careful (Quick-Scalp) palettes — swap label colors when inside bands; hide/show quick-scalp labels per mode.

Duplicate filters — suppress Cube repeats within a window.

Session tools — optional 6:00 PM 5m “reset” box (purple) and 9:30 AM 1m NY Open box (yellow).

Backgrounds — optional ST(10,1) 0.5–0.7 ATR ribbons for context.

Presets — five Sparkle presets with per-side alternation and wipe logic.

Alerts (names as they appear in TradingView)

⬜ Cube’s Buy / Sell (or 🟨 Incoming if trend is inverted)

🟨 CUBE’S BUY ++ / CUBE’S SELL ++ (or “Cube’s … ++” if inverted)

🟫 Buy Last Chance / 🟫 Incoming (Sell Last Chance)

🟫 Cube’s Last Chance Buy ++ / Cube’s Last Chance Sell

🟪 Smart Cube’s Buy / Smart Cube’s Sell

🔔 ALL Cube Alerts (one catch-all)

✨ G✨lden Buy/Sell (Sparkles+Cube) and G✨lden-1/2 variants

Tip: Set close-bar alerts for most signals; if you want early heads-up, allow “once per bar” but expect more noise.

Reading the labels

“(Quick Scalp)” suffix = price inside the VWAP/EMA50 careful bands; tighten targets/size.

Some labels include indicator names + a weighted count (e.g., “Hist RSI MOM 3”) to hint at divergence depth.

Star ⭐ near a label means a CRT+VOL pair was detected within the recent window.

Golden text shows the most recent cube subtype (“Cube ++”, “Smart Cube”, etc.) that satisfied the window rule.

Recommended markets & timeframes

Built-in tuning for: NQ/ES/RTY/YM, GC/CL, XAU/XAG, FX majors, BTC/ETH/SOL, SPY/QQQ/IWM/DIA, and mega-caps (AAPL, MSFT, NVDA, etc.).

Best experience on 1m–5m for intraday. Works on higher TFs but is designed around the 5-minute VWAP/EMA50 backbone.

Best practices

Confluence over single prints: Use ✨ Golden or 🟪 Smart Cube + trend + structure.

Location matters: Prefer signals near session boxes, prior day H/L, and liquidity pools.

Risk first: Size down in (Quick Scalp) zones and during lunch hours/illiquid sessions.

Avoid double-counting: The script already suppresses blatant duplicates—don’t force extra alerts.

Repainting & transparency