Momentum Breakout Filter + ATR ZonesMomentum Breakout Filter + ATR Zones - User Guide

What This Indicator Does

This indicator helps you with your MACD + volume momentum strategy by:

Filtering out fake breakouts - Shows ⚠️ warnings when breakouts lack confirmation

Showing clear entry signals - 🚀 LONG and 🔻 SHORT labels when all conditions align

Automatic stop loss & profit targets - Based on ATR (Average True Range)

Visual trend confirmation - Background color + EMA alignment

Signal Types

🚀 LONG Entry Signal (Green Label)

Appears when ALL conditions met:

✅ MACD crosses above signal line

✅ Volume > 1.5× average

✅ Price > EMA 9 > EMA 21 > EMA 200 (bullish trend)

✅ Price closes above recent 20-bar high

🔻 SHORT Entry Signal (Red Label)

Appears when ALL conditions met:

✅ MACD crosses below signal line

✅ Volume > 1.5× average

✅ Price < EMA 9 < EMA 21 < EMA 200 (bearish trend)

✅ Price closes below recent 20-bar low

⚠️ FAKE Breakout Warning (Orange Label)

Appears when price breaks high/low BUT lacks confirmation:

❌ Low volume (below 1.5× average), OR

❌ Wick break only (didn't close through level), OR

❌ MACD not aligned with direction

Hover over the warning label to see what's missing!

ATR Stop Loss & Targets

When you get a signal, colored lines automatically appear:

Long Position

Red solid line = Stop Loss (Entry - 1.5×ATR)

Green dashed lines = Profit Targets:

Target 1: Entry + 2×ATR

Target 2: Entry + 3×ATR

Target 3: Entry + 4×ATR

Short Position

Red solid line = Stop Loss (Entry + 1.5×ATR)

Green dashed lines = Profit Targets:

Target 1: Entry - 2×ATR

Target 2: Entry - 3×ATR

Target 3: Entry - 4×ATR

The lines move with each bar until you exit the position.

Chart Elements

Moving Averages

Blue line = EMA 9 (fast)

Orange line = EMA 21 (medium)

White line = EMA 200 (trend filter)

Volume

Yellow bars = High volume (above threshold)

Gray bars = Normal volume

Background Color

Light green = Bullish trend (all EMAs aligned up)

Light red = Bearish trend (all EMAs aligned down)

No color = Neutral/mixed

MACD (Bottom Pane)

Green/Red columns = MACD Histogram

Blue line = MACD Line

Orange line = Signal Line

Info Dashboard (Bottom Right)

ItemWhat It ShowsVolumeCurrent volume vs average (✓ HIGH or ✗ Low)MACDDirection (BULLISH or BEARISH)TrendEMA alignment (BULL, BEAR, or NEUTRAL)ATRCurrent ATR value in dollarsPositionCurrent position (LONG, SHORT, or NONE)R:RRisk-to-Reward ratio (shows when in position)

How To Use It

Basic Workflow

Wait for setup

Watch for MACD to approach signal line

Volume should be building

Price should be near EMA structure

Get confirmation

Wait for 🚀 LONG or 🔻 SHORT label

Check dashboard shows "✓ HIGH" volume

Verify trend is aligned (green or red background)

Enter the trade

Enter when signal appears

Note your stop loss (red line)

Note your targets (green dashed lines)

Manage the trade

Exit at first target for partial profit

Move stop to breakeven

Trail remaining position

What To Avoid

❌ Don't trade when you see:

⚠️ FAKE labels (wait for confirmation)

Neutral background (no clear trend)

"✗ Low" volume in dashboard

MACD and Trend not aligned

Settings You Can Adjust

Volume Sensitivity

High Volume Threshold: Default 1.5×

Increase to 2.0× for cleaner signals (fewer trades)

Decrease to 1.2× for more signals (more trades)

Fake Breakout Filters

You can toggle these ON/OFF:

Volume Confirmation: Requires high volume

Close Through: Requires candle close, not just wick

MACD Alignment: Requires MACD direction match

Tip: Turn all three ON for highest quality signals

ATR Stop/Target Multipliers

Default settings (conservative):

Stop Loss: 1.5×ATR

Target 1: 2×ATR (1.33:1 R:R)

Target 2: 3×ATR (2:1 R:R)

Target 3: 4×ATR (2.67:1 R:R)

Aggressive traders might use:

Stop Loss: 1.0×ATR

Target 1: 2×ATR (2:1 R:R)

Target 2: 4×ATR (4:1 R:R)

Conservative traders might use:

Stop Loss: 2.0×ATR

Target 1: 3×ATR (1.5:1 R:R)

Target 2: 5×ATR (2.5:1 R:R)

Example Trade Scenarios

Scenario 1: Perfect Long Setup ✅

Stock consolidating near EMA 21

MACD curling up toward signal line

Volume bar turns yellow (high volume)

🚀 LONG label appears

Red stop line and green target lines appear

Result: High probability trade

Scenario 2: Fake Breakout Avoided ✅

Price breaks above resistance

Volume is normal (gray bar)

⚠️ FAKE label appears (hover shows "Low volume")

No entry signal

Price falls back below breakout level

Result: Avoided losing trade

Scenario 3: Premature Entry ❌

MACD crosses up

Volume is high

BUT trend is NEUTRAL (no background color)

No signal appears (trend filter blocks it)

Result: Avoided choppy/sideways market

Quick Reference

Entry Checklist

🚀 or 🔻 label on chart

Dashboard shows "✓ HIGH" volume

Dashboard shows aligned MACD + Trend

Colored background (green or red)

ATR lines visible

No ⚠️ FAKE warning

Exit Strategy

Target 1 (2×ATR): Take 50% profit, move stop to breakeven

Target 2 (3×ATR): Take 25% profit, trail stop

Target 3 (4×ATR): Take remaining profit or trail aggressively

Stop Loss: Exit entire position if hit

Alerts

Set up these alerts:

Long Entry: Fires when 🚀 LONG signal appears

Short Entry: Fires when 🔻 SHORT signal appears

Fake Breakout Warning: Fires when ⚠️ appears (optional)

Tips for Success

Use on 5-minute charts for day trading momentum plays

Only trade high volume stocks ($5-20 range works best)

Wait for full confirmation - don't jump early

Respect the stop loss - it's calculated based on volatility

Scale out at targets - don't hold for home runs

Avoid trading first 15 minutes - let market settle

Best during 10am-11am and 2pm-3pm - peak momentum times

Common Questions

Q: Why didn't I get a signal even though MACD crossed?

A: All conditions must be met - check dashboard for what's missing (likely volume or trend alignment)

Q: Can I use this on any timeframe?

A: Yes, but it's designed for 5-15 minute charts. On daily charts, adjust ATR multipliers higher.

Q: The stop loss seems too tight, can I widen it?

A: Yes, increase "Stop Loss (×ATR)" from 1.5 to 2.0 or 2.5 in settings.

Q: I keep seeing FAKE warnings but price keeps going - what gives?

A: The filter is conservative. You can disable some filters in settings, but expect more false signals.

Q: Can I use this for swing trading?

A: Yes, but use larger timeframes (1H or 4H) and adjust ATR multipliers up (3× for stops, 6-9× for targets).

在脚本中搜索"stop loss"

Multi-Timeframe Trend Indicator with Signals═══════════════════════════════════════════════════════════════

Multi-Timeframe Trend Indicator with Signals

by Zakaria Safri

═══════════════════════════════════════════════════════════════

⚠️ IMPORTANT DISCLAIMERS:

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

• This indicator may REPAINT on unconfirmed bars

• Signals appear in real-time but may change or disappear

• FOR EDUCATIONAL PURPOSES ONLY - NOT FINANCIAL ADVICE

• Past performance does not guarantee future results

• Always do your own research and use proper risk management

• The Risk Management feature is VISUAL ONLY - does not execute trades

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📊 OVERVIEW:

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

This indicator combines multiple technical analysis tools to help identify

potential trend directions and entry/exit points across different timeframes.

It uses SuperTrend, EMAs, ADX, RSI, and Keltner Channels to generate signals.

🎯 KEY FEATURES:

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📍 SIGNAL TYPES:

• All Signals: Shows all SuperTrend crossovers

• Filtered Signals: Additional EMA filter for potentially higher quality signals

• Signals use barstate.isconfirmed to reduce (but not eliminate) repainting

📈 TREND ANALYSIS:

• Trend Ribbon: 8 EMAs creating a visual trend direction indicator

• Trend Cloud: EMA 150/250 cloud for long-term trend context

• Chaos Trend Line: Dynamic support/resistance trend line

• Multi-timeframe dashboard showing trend across 8 timeframes (3m to Daily)

📊 TECHNICAL INDICATORS:

• Keltner Channels: Dynamic price channels

• RSI Background: Visual overbought/oversold zones

• Candlestick Coloring: Three modes (CleanScalper/Trend Ribbon/Moving Average)

• ADX-based trend strength analysis for MTF dashboard

🎯 VISUAL TOOLS:

• Order Blocks: Supply/demand zones (optional)

• Channel Breakouts: Pivot-based support/resistance levels

• Reversal Signals: RSI-based potential reversal indicators

• Visual TP/SL Lines: For reference only - does NOT execute trades

📊 DASHBOARD:

• Real-time multi-timeframe trend analysis

• Volatility indicator (Very Low to Very High)

• Current RSI value with color coding

• Customizable position and size

⚙️ SETTINGS:

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

MAIN SETTINGS:

• Sensitivity: Controls signal frequency (lower = more signals)

• Signal Type: Choose between All Signals or Filtered Signals

• Factor: ATR multiplier for SuperTrend calculation

TREND SETTINGS:

• Toggle Trend Ribbon, Trend Cloud, Chaos Trend, Order Blocks

• Moving Average: Customizable EMA (default 200)

ADVANCED SETTINGS:

• Candlestick coloring with 3 different modes

• Overbought/Oversold background coloring

• Channel breakout levels

• Show/hide signals

RISK MANAGEMENT (VISUAL ONLY):

• ⚠️ Does NOT execute trades automatically

• Shows potential Take Profit levels (TP1, TP2, TP3)

• Shows potential Stop Loss level

• Adjustable TP strength multiplier

• For educational reference only

📖 HOW TO USE:

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

1. SIGNAL INTERPRETATION:

• "Buy" signals appear below candles when conditions are met

• "Sell" signals appear above candles when conditions are met

• Wait for bar close confirmation to avoid repainting

• Use multiple timeframes for confluence

2. TREND CONFIRMATION:

• Check the multi-timeframe dashboard for trend alignment

• Use Trend Ribbon for visual trend direction

• Trend Cloud shows longer-term market bias

• Green candles = potential uptrend, Red = potential downtrend

3. ENTRY/EXIT STRATEGY:

• Combine signals with other analysis tools

• Check volatility status before entering trades

• Use support/resistance levels for confirmation

• The visual TP/SL lines are for planning only

4. RISK MANAGEMENT:

• Always use stop losses (indicator shows suggested levels only)

• Position size according to your risk tolerance

• Never risk more than you can afford to lose

• The indicator does NOT manage trades automatically

⚠️ LIMITATIONS & RISKS:

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

REPAINTING:

• Signals may appear and disappear on unconfirmed bars

• Always wait for bar close before taking action

• Historical performance may look better than real-time results

FALSE SIGNALS:

• No indicator is 100% accurate

• Signals can fail in ranging/choppy markets

• Use additional confirmation methods

• Consider market context and fundamentals

VISUAL TP/SL:

• Lines are for reference/planning only

• Does NOT place or manage actual trades

• You must manually set your own stop losses

• TP levels are calculated estimates, not guarantees

🔧 TECHNICAL DETAILS:

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

• Version: Pine Script v5

• Overlay: Yes (displays on main chart)

• Anti-repaint measures: Uses barstate.isconfirmed on signals

• Security function: Uses lookahead protection for higher timeframes

• Dynamic requests: Enabled for MTF analysis

• Max labels: 500

📚 COMPONENTS EXPLAINED:

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

SUPERTREND:

• Core signal generator using ATR-based bands

• Crossovers indicate potential trend changes

• Adjustable via Sensitivity and Factor inputs

EMA FILTER:

• Uses 200 EMA as trend filter (customizable)

• Filtered signals require price above/below EMA

• Helps reduce false signals in ranging markets

ADX TREND QUALITY:

• Measures trend strength across timeframes

• Used in multi-timeframe dashboard

• Shows Bullish/Bearish/Neutral states

KELTNER CHANNELS:

• Multiple bands showing volatility zones

• Color-coded based on RSI levels

• Helps identify overbought/oversold conditions

ORDER BLOCKS:

• Identifies supply/demand zones

• Based on price structure and pivots

• Can extend to the right for projection

💡 BEST PRACTICES:

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

✓ Use multiple timeframe confirmation

✓ Wait for bar close before acting on signals

✓ Combine with support/resistance analysis

✓ Check overall market conditions

✓ Use proper risk management (1-2% per trade)

✓ Backtest on your specific market/timeframe

✓ Paper trade before using real money

✓ Keep a trading journal

✓ Adjust settings to your trading style

✗ Don't rely solely on this indicator

✗ Don't ignore risk management

✗ Don't trade on unconfirmed signals

✗ Don't overtrade every signal

✗ Don't use without understanding how it works

✗ Don't expect the TP/SL feature to trade for you

📞 SUPPORT & UPDATES:

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Creator: Zakaria Safri

Version: 4.3 (Compliance Update)

For questions or feedback, please use TradingView's comment section.

⚖️ FINAL DISCLAIMER:

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

This indicator is provided for EDUCATIONAL and INFORMATIONAL purposes only.

It is NOT financial advice, investment advice, or a recommendation to buy/sell.

Trading involves substantial risk of loss. Past performance, whether actual or

indicated by historical tests of strategies, is not indicative of future results.

The creator assumes NO responsibility for your trading results. You are solely

responsible for your own investment decisions and due diligence.

Always consult with a qualified financial advisor before making investment decisions.

By using this indicator, you acknowledge and accept these risks and limitations.

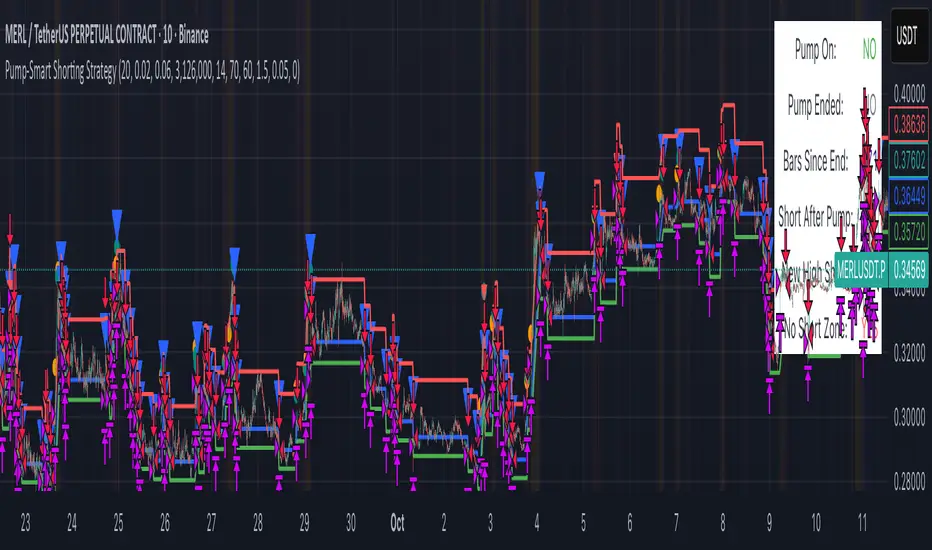

Pump-Smart Shorting StrategyThis strategy is built to keep your portfolio hedged as much as possible while maximizing profitability. Shorts are opened after pumps cool off and on new highs (when safe), and closed quickly during strong upward moves or if stop loss/profit targets are hit. It uses visual overlays to clearly show when hedging is on, off, or blocked due to momentum, ensuring you’re protected in most market conditions but never short against the pump. Fast re-entry keeps the hedge active with minimal downtime.

Pump Detection:

RSI (Relative Strength Index): Calculated over a custom period (default 14 bars). If RSI rises above a threshold (default 70), the strategy considers the market to be in a pump (strong upward momentum).

Volume Spike: The current volume is compared to a 20-bar simple moving average of volume. If it exceeds the average by 1.5× and price increases at least 5% in one bar, pump conditions are triggered.

Price Jump: Measured by (close - close ) / close . A single-bar change > 5% helps confirm rapid momentum.

Pump Zone (No Short): If any of these conditions is true, an orange or red background is shown and shorts are blocked.

Cooldown and Re-Entry:

Cooldown Detection: After the pump ends, RSI must fall below a set value (default ≤ 60), and either volume returns towards average or price momentum is less than half the original spike (oneBarUp <= pctUp/2).

barsWait Parameter: You can specify a waiting period after cooldown before a short is allowed.

Short Entry After Pump/Cooldown: When these cooldown conditions are met, and no short is active, a blue background is shown and a short position is opened at the next signal.

New High Entry:

Lookback New High: If the current high is greater than the highest high in the last N bars (default 20), and pump is NOT active, a short can be opened.

Take Profit (TP) & Stop Loss (SL):

Take Profit: Short is closed if price falls to a threshold below the entry (minProfitPerc, default 2%).

Stop Loss: Short is closed if price rises to a threshold above the entry (stopLossPerc, default 6%).

Preemptive Exit:

Any time a pump is detected while a short position is open, the strategy closes the short immediately to avoid losses.

Visual Feedback:

Orange Background: Market is pumping, do not short.

Red Background: Other conditions block shorts (cooldown or waiting).

Blue Background: Shorts allowed.

Triangles/Circles: Mark entries, pump start/end, for clear trading signals.

VMS Momentum Trend Matrix Indicator [09.00 to 23.30]VMS Momentum Trend Matrix Indicator - Detailed Explanation

🎯 Overview & Core Philosophy

This is a multi-dimensional trading and a multi-confirmation system that combines 4 independent analytical approaches into one unified framework. The indicator operates on the principle of "consensus trading" - where signals are only considered reliable when multiple systems confirm each other. The system is designed for 9:00 AM to 23:30 PM trading sessions (Indian Market) with dynamic support/resistance levels.

Five Pillars of Analysis:

1. Trend Matrix – Multiple indicator voting system

2. Momentum Suite – Multiple Hybrid oscillator

3. Volume Analysis - Buy/sell pressure quantification

4. Key Level Identification - Dynamic support/resistance

5. EMA Trend: Indicates the overall long-term direction.

📊 DASHBOARD INTERPRETATION - ROW BY ROW

ROW 1: Indicator Name and Cell background colour changes with Trend Matrix

ROW 2: EMA ANALYSIS (It analyses independently and does not combine this analysis with the Combined Analysis and Trading View. Background Colour on price chart is based on this)

Purpose: Long-term trend identification using Exponential Moving Averages

What to Watch:

• Major Trend: Overall market direction (Bullish/Bearish/Neutral)

• Bullish Condition: All EMAs aligned upward

• Bearish Condition: All EMAs aligned downward

• Neutral: Mixed alignment

Trading Significance:

• Trading Condition: Current bias based on EMA alignment

• Bullish Market: Focus on LONG positions only

• Bearish Market: Focus on SHORT positions only

• Neutral Market: Wait for clearer direction

ROW 3-4: KEY LEVELS

Purpose: Dynamic support and resistance identification

Levels to Monitor:

• VMS Line-1 (Support): Dynamic Support for long positions

• VMS Line-2 (Resistance): Dynamic Resistance for short positions

• Up/Down: Daily base levels from opening price calculations

• Up: Daily support level based on opening price

• Down: Daily resistance level based on opening price

How Levels Work:

• Wait for Line-1 and 2 Crossing

• In the Upward movement, Line-1 will move with the price, and Line-2 will be moved as a straight line

• In the Downward movement, Line-2 will move with the price, and Line-2 will be moved as a straight line

• Provide clear entry/exit points

• If the price is between these levels, it is mostly a sideways market. After the Upward movement, if the price crosses Line-1 and other bearish conditions are supported, a short position can be taken. And in the Downward movement, it is the reverse condition.

• If the price is above the up level, it can be considered as bullish and below as bearish

ROW 5-6: VOLUME ANALYSIS

Purpose: Measure buying vs selling pressure

Key Metrics:

• Total Buy Volume: Cumulative buying pressure

• Total Sell Volume: Cumulative selling pressure

• Bullish Candles: Number of up-candles in session

• Bearish Candles: Number of down-candles in session

Interpretation:

• Buy Volume > Sell Volume: Bullish sentiment

• Sell Volume > Buy Volume: Bearish sentiment

• Bullish Candles Dominating: Upward momentum

• Bearish Candles Dominating: Downward momentum

ROW 7-8: MOMENTUM SUITE (Background colour of Oscillator is based on this)

Purpose: Short-term momentum strength and direction

Critical Components:

• Direction: Current momentum (BULLISH/BEARISH)

• Strength: 0-100% strength measurement

• Bullish Height: Positive momentum magnitude

• Bearish Height: Negative momentum magnitude

Strength Classification:

• 80-100%: Very Strong - High conviction trades

• 60-80%: Strong - Good trading opportunities

• 40-60%: Moderate - Caution advised

• 20-40%: Weak - Avoid trading

• 0-20%: Very Weak - No trade zone

ROW 9-11: TREND MATRIX

Purpose: Consensus from Multiple technical indicators

Matrix Scoring:

• Bullish Signals: Number voting UP

• Bearish Signals: Number voting DOWN

• Neutral Signals: Non-committed indicators

• Net Score: Bullish - Bearish signals

Trend Classification:

• Strong Uptrend: Net Score ≥ +5

• Uptrend: Net Score +1 to +4

• Neutral: Net Score = 0

• Downtrend: Net Score -1 to -4

• Strong Downtrend: Net Score ≤ -5

ROW 12: COMBINED ANALYSIS

Purpose: Final integrated signal from all systems

Bias Levels:

• STRONG BULLISH: All systems aligned upward

• BULLISH: Majority systems upward

• NEUTRAL: Mixed or weak signals

• BEARISH: Majority systems downward

• STRONG BEARISH: All systems aligned downward

Confidence Score: 0-100% reliability measurement

ROW 13: TRADING VIEW

Purpose: Clear action recommendations

Possible Actions:

• STRONG LONG: High conviction buy signal

• MODERATE LONG: Medium conviction buy signal

• WAIT FOR CONFIRMATION: No clear signal

• MODERATE SHORT: Medium conviction sell signal

• STRONG SHORT: High conviction sell signal

🎯 COMPLETE TRADING RULES

BUY ENTRY CONDITIONS (All Must Be True)

Primary Conditions:

1. Combined Bias: BULLISH or STRONG BULLISH

2. Trading Action: MODERATE LONG or STRONG LONG

3. Momentum Strength: ≥ 40% (≥60% for STRONG LONG)

4. Trend Matrix: Net Score ≥ +3

5. EMA Trend: Bullish or Neutral

Confirmation Conditions:

6. Price Position: Above VMS Line-1 AND Base Up

7. Volume Confirmation: Buy Volume > Sell Volume

8. Bullish Candles: More bullish than bearish candles

Risk Management:

9. Stop Loss: Below VMS Line-1 OR Base Down (whichever is lower)

10. Position Size: Based on confidence score (higher score = larger position)

11. Take Profit: When Combined Bias turns "NEUTRAL" or momentum strength drops below 20%

12. Exit Signal: Trading Action shows "WAIT FOR CONFIRMATION"

SELL/SHORT ENTRY CONDITIONS (All Must Be True)

Primary Conditions:

1. Combined Bias: BEARISH or STRONG BEARISH

2. Trading Action: MODERATE SHORT or STRONG SHORT

3. Momentum Strength: ≥ 40% (≥60% for STRONG SHORT)

4. Bearish Signals: ≥ 12 in Trend Matrix

5. Trend Matrix: Net Score ≤ -3

6. EMA Trend: Bearish or Neutral

Confirmation Conditions:

6. Price Position: Below VMS Line-2 AND Base Down

7. Volume Confirmation: Sell Volume > Buy Volume

8. Bearish Candles: More bearish than bullish candles

Risk Management:

9. Stop Loss: Above VMS Line-2 OR Base Up (whichever is higher)

10. Position Size: Based on confidence score

11. Take Profit: When Combined Bias turns "NEUTRAL" or momentum strength drops below 20%

12. Exit Signal: Trading Action shows "WAIT FOR CONFIRMATION"

⏰ ENTRY/EXIT TIMING

Best Entry Times:

• 9:30-11:00 AM: Early session momentum established

• 12:30-16:30 AM: Mid-session confirmation

• 21:30-23:00 PM: closing session momentum shifts

Avoid Trading:

• First 15 minutes: Excessive volatility

• 12:00-18:00 PM: Low liquidity period

• After 22:00 PM: Session closing volatility

Exit Triggers:

Profit Taking:

• Target 1: 1:1 Risk-Reward (exit 50% position)

• Target 2: 1.5:1 Risk-Reward (exit remaining 50%)

• Trailing Stop: Move stop to breakeven after Target 1

Stop Loss Triggers:

• Price crosses opposite VMS line

• Combined Bias changes to NEUTRAL

• Momentum Strength drops below 20%

• Volume confirmation reverses

•

Emergency Exit:

• Trend Matrix Net Score reverses direction

• 6-EMA trend changes direction

• Key support/resistance breaks against position

📈 TRADING SCENARIOS

Scenario 1: STRONG BULLISH SETUP

- Combined Bias: STRONG BULLISH

- Trading Action: STRONG LONG

- Momentum Strength: 75%

- Trend Matrix: Net Score +8

- Price: Above VMS Line-1 and Base Up

- Volume: Strong buy volume dominance

ACTION: Enter LONG with full position size

STOP LOSS: Below VMS Line-1

TARGET: 1.5:1 Risk-Reward ratio

Scenario 2: MODERATE BEARISH SETUP

- Combined Bias: BEARISH

- Trading Action: MODERATE SHORT

- Momentum Strength: 55%

- Trend Matrix: Net Score -4

- Price: Below VMS Line-2 but above Base Down

- Volume: Moderate sell volume dominance

ACTION: Enter SHORT with half position size

STOP LOSS: Above VMS Line-2

TARGET: 1:1 Risk-Reward ratio

Scenario 3: NEUTRAL/WAIT SETUP

- Combined Bias: NEUTRAL

- Trading Action: WAIT FOR CONFIRMATION

- Momentum Strength: 35%

- Trend Matrix: Net Score 0

- Mixed volume signals

ACTION: NO TRADE - Wait for clearer signals

________________________________________

⚠️ RISK MANAGEMENT RULES

Position Sizing:

• STRONG Signals (80-100% confidence): 100% normal position

• MODERATE Signals (60-79% confidence): 50-75% position

• WEAK Signals (40-59% confidence): 25% position or avoid

• VERY WEAK (<40% confidence): NO TRADE

Daily Loss Limits:

• Maximum 2% capital loss per day

• Maximum 3 consecutive losing trades

• Stop trading after the daily limit is reached

Trade Management:

• Never move the stop loss against a position

• Take partial profits at predetermined levels

• Never average down losing positions

• Respect all exit signals immediately

________________________________________

🔄 SIGNAL CONFIRMATION PROCESS

Step 1: Trend Direction

Check EMA alignment and Combined Bias

Step 2: Momentum Strength

Verify Momentum Strength ≥ 40% and direction matches trend

Step 3: Volume Confirmation

Confirm volume supports the direction

Step 4: Matrix Consensus

Ensure Trend Matrix agrees (Net Score ≥ |3|)

Step 5: Price Position

Verify price is on the correct side of key levels

Step 6: Entry Execution

Enter on a pullback to support/resistance with a stop loss

________________________________________

This system works best when you wait for all conditions to align. Patience is key - only trade when all systems confirm the same direction with adequate strength. The multiple confirmation layers significantly increase the probability of success but reduce trading frequency.

Cnagda Pure Price ActionCnagda Pure Price Action (CPPA) indicator is a pure price action-based system designed to provide traders with real-time, dynamic analysis of the market. It automatically identifies key candles, support and resistance zones, and potential buy/sell signals by combining price, volume, and multiple popular trend indicators.

How Price Action & Volume Analysis Works

Silver Zone – Logic, Reason, and Trade Planning

Logic & Visualization:

The Silver Zone is created when the closing price is the lowest in the chosen window and volume is the highest in that window.

Visually, a large silver-colored box/rectangle appears on the chart.

Thick horizontal lines (top and bottom) are drawn at the high and low of that candle/bar, extending to the right.

Reasoning:

This combination typically occurs at strong “accumulation” or support areas:

Sellers push the price down to the lowest point, but aggressive buyers step in with high volume, absorbing supply.

Indicates potential exhaustion of selling and likely shift in market control to buyers.

How to Plan Trades Using Silver Zone:

Watch if price returns to the Silver Zone in the future: It often acts as powerful support.

Bullish entries (buys) can be planned when price tests or slightly pierces this zone, especially if new buy signals occur (like yellow/green candle labels).

Place your stop-loss below the bottom line of the Silver Zone.

Target: Look for the nearest resistance or opposing zone, or use indicator’s bullish label as confirmation.

Extra Tip:

Multiple touches of the Silver Zone reinforce its importance, but if price closes deeply below it with high volume, that’s a caution signal—support may be breaking.

Black Zone – Logic, Reason, and Trade Planning (as CPPA):

Logic & Visualization:

The Black Zone is created when the closing price is the highest in the chosen window and volume is the lowest in that window.

Visually, a large black-colored box/rectangle appears on the chart, along with thick horizontal lines at the top (high) and bottom (low) of the candle, extending to the right.

Reasoning:

This combination signals a strong “distribution” or resistance area:

Buyers push the price up to a local high, but low volume means there is not much follow-through or conviction in the move.

Often marks exhaustion where uptrend may pause or reverse, as sellers can soon step in.

How to Plan Trades Using Black Zone:

If price revisits the Black Zone in the future, it often acts as major resistance.

Bearish entries (sells) are considered when price is near, testing, or slightly above the Black Zone—especially if new sell signals appear (like blue/red candle labels).

Place your stop-loss just above the top line of the Black Zone.

Target: Nearest support zone (such as a Silver Zone) or next indicator’s bearish label.

Extra Tip:

Multiple touches of the Black Zone make it stronger, but if price closes far above with rising volume, be cautious—resistance might be breaking.

Support Line – Logic, Reason, and Trade Planning (as Cppa):

Logic & Visualization:

The Support Line is a dynamically drawn dashed line (usually blue) that marks key price levels where the market has previously shown significant buying interest.

The line is generated whenever a candle forms a high price with high volume (orange logic).

The script checks for historical pivot lows, past support zones, and even higher timeframe (HTF) supports, and then extends a blue dashed line from that price level to the right, labeling it (sometimes as “Prev Support Orange, HTF”).

Reasoning:

This line helps you visually identify where demand has been strong enough to hold price from falling further—essentially a floor in the market used by professional traders.

If price approaches or re-tests this line, there’s a good chance buyers will defend it again.

How to Plan Trades Using Support Line:

Watch for price to approach the Support Line during down moves. If you see a bullish candlestick pattern, buy labels (yellow/green), or other indicators aligning, this can be a high-probability entry zone.

Great for planning stop-loss for long trades: place stops just below this line.

Target: Next resistance zone, Black Zone, or the top of the last swing.

Extra Tip:

Multiple confirmations (support line + Silver Zone + bullish label) provide powerful entry signals.

If price closes strongly below the Support Line with volume, be cautious—support may be breaking, and a trend reversal or deeper correction could follow.

Resistance Line – Logic, Reason, and Trade Planning (from CPPA):

Logic & Visualization:

The Resistance Line is a dynamically drawn dashed line (usually purple or red) that identifies price levels where the market has previously faced significant selling pressure.

This line is created when a candle reaches a high price combined with high volume (orange logic), or from a historical pivot high/resistance,

The script also tracks higher timeframe (HTF) resistance lines, labeled as “Prev Resistance Orange, HTF,” and extends these dashed lines to the right across the chart.

Reasoning:

Resistance Lines are visual markers of “supply zones,” where buyers previously failed, and sellers took control.

If the price returns to this line later, sellers may get active again to defend this level, halting the uptrend.

How to Plan Trades Using Resistance Line:

Watch for price to approach the Resistance Line during up moves. If you see bearish candlestick patterns, sell labels (blue/red), or bearish indicator confirmation, this becomes a strong shorting opportunity.

Perfect for placing stop-loss in short trades—put your stop just above the Resistance Line.

Target: Next support zone (Silver Zone) or bottom of the last swing.

If the price breaks above with high volume, avoid shorting—resistance may be failing.

Extra Tip:

Multiple resistances (Resistance Line + Black Zone + bearish label) make short signals stronger.

Choppy movement around this line often signals indecision; wait for a clear rejection before entering trades.

Bullish / Bearish Label – Logic, Reason, and Trade Planning:

Logic & Visualization:

The indicator constantly calculates a "Bull Score" and a "Bear Score" based on several factors:

Trend direction from price slope

Confirmation by popular indicators (RSI, ADX, SAR, CMF, OBV, CCI, Bollinger Bands, TWAP)

Adaptive scoring (higher score for each bullish/bearish condition met)

If Bull Score > Bear Score, the chart displays a green "BULLISH" label (usually below the bar).

If Bear Score > Bull Score, the chart displays a red "BEARISH" label (usually above the bar).

If neither dominates, a "NEUTRAL" label appears.

Reasoning:

The labels summarize complex price action and indicator analysis into a simple, actionable sentiment cue:

Bullish: Majority of conditions indicate buying strength; trend is up.

Bearish: Majority signals show selling pressure; trend is down.

How to Use in Trade Planning:

Use the Bullish label as confirmation to enter or hold long (buy) positions, especially if near support/Silver Zone.

Use the Bearish label to enter/hold short (sell) positions, especially if near resistance/Black Zone.

For best results, combine with candle color, volume analysis, or other labels (yellow/green for buys, blue/red for sells).

Avoid trading against these labels unless you have strong confluence from zones/support levels.

Yellow Label (Buy Signal) – Logic, Reason & Trade Planning:

Logic & Visualization:

The yellow label appears below a candle (label.style_label_up, yloc.belowbar) and marks a potential buy signal.

Script conditions:

The candle must be a “yellow candle” (which means it’s at the local lowest close, not a high, with normal volume).

Volume is decreasing for 2 consecutive candles (current volume < previous volume, previous volume < second previous).

When these conditions are met, a yellow label is plotted below the candle.

Reasoning:

This scenario often marks the end of selling pressure and start of possible accumulation—buyers may be stepping in as sellers exhaust.

Decreasing volume during a local price low means selling is slowing, possibly hinting at a reversal.

How to Trade Using Yellow Label:

Entry: Consider buying at/just above the yellow-labeled candle’s close.

Stop-loss: A bit below the candle’s low (or Silver Zone line, if present).

Target: Next resistance level, Black Zone, or chart’s bullish label.

Extra Tip:

If the yellow label is found at/near a Silver Zone or Support Line, and trend is “Bullish,” the setup gets even stronger.

Avoid trading if overall indicator shows “Bearish.”

Green Label (Buy with Increasing Volume) – Logic, Reason & Trade Planning:

Logic & Visualization:

The green label is plotted below a candle (label.style_label_up, yloc.belowbar) and marks a strong buy signal.

Script conditions:

The candle must be a “yellow candle” (at the local lowest close, normal volume).

Volume is increasing for 2 consecutive candles (current volume > previous volume, previous volume > second previous).

When these conditions are met, a green label is plotted below the candle.

Reasoning:

This scenario signals that buyers are stepping in aggressively at a local price low—the end of a downtrend with strong, rising activity.

Increasing volume at a price low is a classic sign of accumulation, where institutions or large players may be buying.

How to Trade Using Green Label:

Entry: Consider buying at/just above the green-labeled candle’s close for a momentum-based reversal.

Stop-loss: Slightly below the candle’s low, or the Silver Zone/support line if present.

Target: Nearest resistance zone/Black Zone, indicator’s bullish label, or next swing high.

Extra Tip:

If the green label is near other supports (Silver Zone, Support Line), the setup is extra strong.

Use confirmation from Bullish labels or trend signals for best results.

Green label setups are suitable for quick, high momentum trades due to increasing volume

Blue Label (Sell Signal on Decreasing Volume) – Logic, Reason & Trade Planning:

Logic & Visualization:

The blue label is plotted above a candle (label.style_label_down, yloc.abovebar) as a potential sell signal.

Script conditions:

The candle is a “blue candle” (local highest close, but not also lowest, and volume is neither highest nor lowest).

Volume is decreasing over 2 consecutive candles (current volume < previous, previous < two ago).

When these match, a blue label appears above the candle.

Reasoning:

This typically signals buyer exhaustion at a local high: price has gone up, but volume is dropping, suggesting big players may not be buying any more at these levels.

The trend is losing strength, and a reversal or pullback is likely.

How to Trade Using Blue Label:

Entry: Look to sell at/just below the candle with the blue label.

Stop-loss: Just above the candle’s high (or above the Black Zone/resistance if present).

Target: Nearest support, Silver Zone, or a swing low.

Extra Tip:

Blue label signals are stronger if they appear near Black Zones or Resistance Lines, or when the general market label is "Bearish."

As with buy setups, always check for confirmation from trend or volume before trading aggressively.

Blue Label (Sell Signal on Decreasing Volume) – Logic, Reason & Trade Planning:

Logic & Visualization:

The blue label is plotted above a candle (label.style_label_down, yloc.abovebar) as a potential sell signal.

Script conditions:

The candle is a “blue candle” (local highest close, but not also lowest, and volume is neither highest nor lowest).

Volume is decreasing over 2 consecutive candles (current volume < previous, previous < two ago).

When these match, a blue label appears above the candle.

Reasoning:

This typically signals buyer exhaustion at a local high: price has gone up, but volume is dropping, suggesting big players may not be buying any more at these levels.

The trend is losing strength, and a reversal or pullback is likely.

How to Trade Using Blue Label:

Entry: Look to sell at/just below the candle with the blue label.

Stop-loss: Just above the candle’s high (or above the Black Zone/resistance if present).

Target: Nearest support, Silver Zone, or a swing low.

Extra Tip:

Blue label signals are stronger if they appear near Black Zones or Resistance Lines, or when the general market label is "Bearish."

As with buy setups, always check for confirmation from trend or volume before trading aggressively.

Here’s a summary of all key chart labels, zones, and trading logic of your Price Action script:

Silver Zone: Powerful support zone. Created at lowest close + highest volume. Best for buy entries near its lines.

Black Zone: Strong resistance zone. Created at highest close + lowest volume. Ideal for short trades near its levels.

Support Line: Blue dashed line at historical demand; buyers defend here. Look for bullish setups when price approaches.

Resistance Line: Purple/red dashed line at supply; sellers defend here. Great for bearish setups when price nears.

Bullish/Bearish Labels: Summarize trend direction using price action + multiple indicator confirmations. Plan buys, holds on bullish; sells, shorts on bearish.

Yellow Label: Buy signal on decreasing volume and local price low. Entry above candle, stop below, target next resistance.

Green Label: Strong buy on increasing volume at a price low. Entry for momentum trade, stop below, target next zone.

Blue Label: Sell signal on dropping volume and local price high. Entry below candle, stop above, target next support.

Best Practices:

Always combine zone/label signals for higher probability trades.

Use stop-loss near zones/lines for risk management.

Prefer trading in the trend direction (bullish/bearish label agrees with your entry).

if Any Question, Suggestion Feel free to ask

Disclaimer:

All information provided by this indicator is for educational and analysis purposes only, and should not be considered financial advice.

VMS Momentum Trend Matrix Indicator [09.15 to 15.30]VMS Momentum Trend Matrix Indicator - Detailed Explanation

🎯 Overview & Core Philosophy

This is a multi-dimensional trading and a multi-confirmation system that combines 4 independent analytical approaches into one unified framework. The indicator operates on the principle of "consensus trading" - where signals are only considered reliable when multiple systems confirm each other. The system is designed for 9:15 AM to 3:30 PM trading sessions (Indian Market) with dynamic support/resistance levels.

Five Pillars of Analysis:

1. Trend Matrix – Multiple indicator voting system

2. Momentum Suite – Multiple Hybrid oscillator

3. Volume Analysis - Buy/sell pressure quantification

4. Key Level Identification - Dynamic support/resistance

5. EMA Trend: Indicates the overall long-term direction.

📊 DASHBOARD INTERPRETATION - ROW BY ROW

ROW 1: Indicator Name and Cell background colour changes with Trend Matrix

ROW 2: EMA ANALYSIS (It analyses independently and does not combine this analysis with the Combined Analysis and Trading View. Background Colour on price chart is based on this)

Purpose: Long-term trend identification using Exponential Moving Averages

What to Watch:

• Major Trend: Overall market direction (Bullish/Bearish/Neutral)

• Bullish Condition: All EMAs aligned upward

• Bearish Condition: All EMAs aligned downward

• Neutral: Mixed alignment

Trading Significance:

• Trading Condition: Current bias based on EMA alignment

• Bullish Market: Focus on LONG positions only

• Bearish Market: Focus on SHORT positions only

• Neutral Market: Wait for clearer direction

ROW 3-4: KEY LEVELS

Purpose: Dynamic support and resistance identification

Levels to Monitor:

• VMS Line-1 (Support): Dynamic Support for long positions

• VMS Line-2 (Resistance): Dynamic Resistance for short positions

• Up/Down: Daily base levels from opening price calculations

• Up: Daily support level based on opening price

• Down: Daily resistance level based on opening price

How Levels Work:

• Wait for Line-1 and 2 Crossing

• In the Upward movement, Line-1 will move with the price, and Line-2 will be moved as a straight line

• In the Downward movement, Line-2 will move with the price, and Line-2 will be moved as a straight line

• Provide clear entry/exit points

• If the price is between these levels, it is mostly a sideways market. After the Upward movement, if the price crosses Line-1 and other bearish conditions are supported, a short position can be taken. And in the Downward movement, it is the reverse condition.

• If the price is above the up level, it can be considered as bullish and below as bearish

ROW 5-6: VOLUME ANALYSIS

Purpose: Measure buying vs selling pressure

Key Metrics:

• Total Buy Volume: Cumulative buying pressure

• Total Sell Volume: Cumulative selling pressure

• Bullish Candles: Number of up-candles in session

• Bearish Candles: Number of down-candles in session

Interpretation:

• Buy Volume > Sell Volume: Bullish sentiment

• Sell Volume > Buy Volume: Bearish sentiment

• Bullish Candles Dominating: Upward momentum

• Bearish Candles Dominating: Downward momentum

ROW 7-8: MOMENTUM SUITE (Background colour of Oscillator is based on this)

Purpose: Short-term momentum strength and direction

Critical Components:

• Direction: Current momentum (BULLISH/BEARISH)

• Strength: 0-100% strength measurement

• Bullish Height: Positive momentum magnitude

• Bearish Height: Negative momentum magnitude

Strength Classification:

• 80-100%: Very Strong - High conviction trades

• 60-80%: Strong - Good trading opportunities

• 40-60%: Moderate - Caution advised

• 20-40%: Weak - Avoid trading

• 0-20%: Very Weak - No trade zone

ROW 9-11: TREND MATRIX

Purpose: Consensus from Multiple technical indicators

Matrix Scoring:

• Bullish Signals: Number voting UP

• Bearish Signals: Number voting DOWN

• Neutral Signals: Non-committed indicators

• Net Score: Bullish - Bearish signals

Trend Classification:

• Strong Uptrend: Net Score ≥ +5

• Uptrend: Net Score +1 to +4

• Neutral: Net Score = 0

• Downtrend: Net Score -1 to -4

• Strong Downtrend: Net Score ≤ -5

ROW 12: COMBINED ANALYSIS

Purpose: Final integrated signal from all systems

Bias Levels:

• STRONG BULLISH: All systems aligned upward

• BULLISH: Majority systems upward

• NEUTRAL: Mixed or weak signals

• BEARISH: Majority systems downward

• STRONG BEARISH: All systems aligned downward

Confidence Score: 0-100% reliability measurement

ROW 13: TRADING VIEW

Purpose: Clear action recommendations

Possible Actions:

• STRONG LONG: High conviction buy signal

• MODERATE LONG: Medium conviction buy signal

• WAIT FOR CONFIRMATION: No clear signal

• MODERATE SHORT: Medium conviction sell signal

• STRONG SHORT: High conviction sell signal

🎯 COMPLETE TRADING RULES

BUY ENTRY CONDITIONS (All Must Be True)

Primary Conditions:

1. Combined Bias: BULLISH or STRONG BULLISH

2. Trading Action: MODERATE LONG or STRONG LONG

3. Momentum Strength: ≥ 40% (≥60% for STRONG LONG)

4. Trend Matrix: Net Score ≥ +3

5. 6-EMA Trend: Bullish or Neutral

Confirmation Conditions:

6. Price Position: Above VMS Line-1 AND Base Up

7. Volume Confirmation: Buy Volume > Sell Volume

8. Bullish Candles: More bullish than bearish candles

Risk Management:

9. Stop Loss: Below VMS Line-1 OR Base Down (whichever is lower)

10. Position Size: Based on confidence score (higher score = larger position)

11. Take Profit: When Combined Bias turns "NEUTRAL" or momentum strength drops below 20%

12. Exit Signal: Trading Action shows "WAIT FOR CONFIRMATION"

SELL/SHORT ENTRY CONDITIONS (All Must Be True)

Primary Conditions:

1. Combined Bias: BEARISH or STRONG BEARISH

2. Trading Action: MODERATE SHORT or STRONG SHORT

3. Momentum Strength: ≥ 40% (≥60% for STRONG SHORT)

4. Bearish Signals: ≥ 12 in Trend Matrix

5. Trend Matrix: Net Score ≤ -3

6. EMA Trend: Bearish or Neutral

Confirmation Conditions:

6. Price Position: Below VMS Line-2 AND Base Down

7. Volume Confirmation: Sell Volume > Buy Volume

8. Bearish Candles: More bearish than bullish candles

Risk Management:

9. Stop Loss: Above VMS Line-2 OR Base Up (whichever is higher)

10. Position Size: Based on confidence score

11. Take Profit: When Combined Bias turns "NEUTRAL" or momentum strength drops below 20%

12. Exit Signal: Trading Action shows "WAIT FOR CONFIRMATION"

⏰ ENTRY/EXIT TIMING

Best Entry Times:

• 9:30-10:00 AM: Early session momentum established

• 11:00-11:30 AM: Mid-session confirmation

• 1:30-2:00 PM: Afternoon momentum shifts

Avoid Trading:

• First 15 minutes: Excessive volatility

• 12:00-1:00 PM: Low liquidity period

• After 3:00 PM: Session closing volatility

Exit Triggers:

Profit Taking:

• Target 1: 1:1 Risk-Reward (exit 50% position)

• Target 2: 1.5:1 Risk-Reward (exit remaining 50%)

• Trailing Stop: Move stop to breakeven after Target 1

Stop Loss Triggers:

• Price crosses opposite VMS line

• Combined Bias changes to NEUTRAL

• Momentum Strength drops below 20%

• Volume confirmation reverses

•

Emergency Exit:

• Trend Matrix Net Score reverses direction

• 6-EMA trend changes direction

• Key support/resistance breaks against position

📈 TRADING SCENARIOS

Scenario 1: STRONG BULLISH SETUP

- Combined Bias: STRONG BULLISH

- Trading Action: STRONG LONG

- Momentum Strength: 75%

- Trend Matrix: Net Score +8

- Price: Above VMS Line-1 and Base Up

- Volume: Strong buy volume dominance

ACTION: Enter LONG with full position size

STOP LOSS: Below VMS Line-1

TARGET: 1.5:1 Risk-Reward ratio

Scenario 2: MODERATE BEARISH SETUP

- Combined Bias: BEARISH

- Trading Action: MODERATE SHORT

- Momentum Strength: 55%

- Trend Matrix: Net Score -4

- Price: Below VMS Line-2 but above Base Down

- Volume: Moderate sell volume dominance

ACTION: Enter SHORT with half position size

STOP LOSS: Above VMS Line-2

TARGET: 1:1 Risk-Reward ratio

Scenario 3: NEUTRAL/WAIT SETUP

- Combined Bias: NEUTRAL

- Trading Action: WAIT FOR CONFIRMATION

- Momentum Strength: 35%

- Trend Matrix: Net Score 0

- Mixed volume signals

ACTION: NO TRADE - Wait for clearer signals

________________________________________

⚠️ RISK MANAGEMENT RULES

Position Sizing:

• STRONG Signals (80-100% confidence): 100% normal position

• MODERATE Signals (60-79% confidence): 50-75% position

• WEAK Signals (40-59% confidence): 25% position or avoid

• VERY WEAK (<40% confidence): NO TRADE

Daily Loss Limits:

• Maximum 2% capital loss per day

• Maximum 3 consecutive losing trades

• Stop trading after the daily limit is reached

Trade Management:

• Never move the stop loss against a position

• Take partial profits at predetermined levels

• Never average down losing positions

• Respect all exit signals immediately

________________________________________

🔄 SIGNAL CONFIRMATION PROCESS

Step 1: Trend Direction

Check EMA alignment and Combined Bias

Step 2: Momentum Strength

Verify Momentum Strength ≥ 40% and direction matches trend

Step 3: Volume Confirmation

Confirm volume supports the direction

Step 4: Matrix Consensus

Ensure Trend Matrix agrees (Net Score ≥ |3|)

Step 5: Price Position

Verify price is on the correct side of key levels

Step 6: Entry Execution

Enter on a pullback to support/resistance with a stop loss

________________________________________

This system works best when you wait for all conditions to align. Patience is key - only trade when all systems confirm the same direction with adequate strength. The multiple confirmation layers significantly increase the probability of success but reduce trading frequency.

AVGO Advanced Day Trading Strategy📈 Overview

The AVGO Advanced Day Trading Strategy is a comprehensive, multi-timeframe trading system designed for active day traders seeking consistent performance with robust risk management. Originally optimized for AVGO (Broadcom), this strategy adapts well to other liquid stocks and can be customized for various trading styles.

🎯 Key Features

Multiple Entry Methods

EMA Crossover: Classic trend-following signals using fast (9) and medium (16) EMAs

MACD + RSI Confluence: Momentum-based entries combining MACD crossovers with RSI positioning

Price Momentum: Consecutive price action patterns with EMA and RSI confirmation

Hybrid System: Advanced multi-trigger approach combining all methodologies

Advanced Technical Arsenal

When enabled, the strategy analyzes 8+ additional indicators for confluence:

Volume Price Trend (VPT): Measures volume-weighted price momentum

On-Balance Volume (OBV): Tracks cumulative volume flow

Accumulation/Distribution Line: Identifies institutional money flow

Williams %R: Momentum oscillator for entry timing

Rate of Change Suite: Multi-timeframe momentum analysis (5, 14, 18 periods)

Commodity Channel Index (CCI): Cyclical turning points

Average Directional Index (ADX): Trend strength measurement

Parabolic SAR: Dynamic support/resistance levels

🛡️ Risk Management System

Position Sizing

Risk-based position sizing (default 1% per trade)

Maximum position limits (default 25% of equity)

Daily loss limits with automatic position closure

Multiple Profit Targets

Target 1: 1.5% gain (50% position exit)

Target 2: 2.5% gain (30% position exit)

Target 3: 3.6% gain (20% position exit)

Configurable exit percentages and target levels

Stop Loss Protection

ATR-based or percentage-based stop losses

Optional trailing stops

Dynamic stop adjustment based on market volatility

📊 Technical Specifications

Primary Indicators

EMAs: 9 (Fast), 16 (Medium), 50 (Long)

VWAP: Volume-weighted average price filter

RSI: 6-period momentum oscillator

MACD: 8/13/5 configuration for faster signals

Volume Confirmation

Volume filter requiring 1.6x average volume

19-period volume moving average baseline

Optional volume confirmation bypass

Market Structure Analysis

Bollinger Bands (20-period, 2.0 multiplier)

Squeeze detection for breakout opportunities

Fractal and pivot point analysis

⏰ Trading Hours & Filters

Time Management

Configurable trading hours (default: 9:30 AM - 3:30 PM EST)

Weekend and holiday filtering

Session-based trade management

Market Condition Filters

Trend alignment requirements

VWAP positioning filters

Volatility-based entry conditions

📱 Visual Features

Information Dashboard

Real-time display of:

Current entry method and signals

Bullish/bearish signal counts

RSI and MACD status

Trend direction and strength

Position status and P&L

Volume and time filter status

Chart Visualization

EMA plots with customizable colors

Entry signal markers

Target and stop level lines

Background color coding for trends

Optional Bollinger Bands and SAR display

🔔 Alert System

Entry Alerts

Customizable alerts for long and short entries

Method-specific alert messages

Signal confluence notifications

Advanced Alerts

Strong confluence threshold alerts

Custom alert messages with signal counts

Risk management alerts

⚙️ Customization Options

Strategy Parameters

Enable/disable long or short trades

Adjustable risk parameters

Multiple entry method selection

Advanced indicator on/off toggle

Visual Customization

Color schemes for all indicators

Dashboard position and size options

Show/hide various chart elements

Background color preferences

📋 Default Settings

Initial Capital: $100,000

Commission: 0.1%

Default Position Size: 10% of equity

Risk Per Trade: 1.0%

RSI Length: 6 periods

MACD: 8/13/5 configuration

Stop Loss: 1.1% or ATR-based

🎯 Best Use Cases

Day Trading: Designed for intraday opportunities

Swing Trading: Adaptable for longer-term positions

Momentum Trading: Excellent for trending markets

Risk-Conscious Trading: Built-in risk management protocols

⚠️ Important Notes

Paper Trading Recommended: Test thoroughly before live trading

Market Conditions: Performance varies with market volatility

Customization: Adjust parameters based on your risk tolerance

Educational Purpose: Use as a learning tool and customize for your needs

🏆 Performance Features

Detailed performance metrics

Trade-by-trade analysis capability

Customizable risk/reward ratios

Comprehensive backtesting support

This strategy is for educational purposes. Past performance does not guarantee future results. Always practice proper risk management and consider your financial situation before trading.

Liquidity SweeperStrategy Overview

This Pine Script implements a Liquidity Sweep Trading Strategy, a sophisticated approach that capitalizes on market manipulation tactics commonly used by institutional traders. The strategy identifies when price "sweeps" above recent swing highs or below swing lows to trigger stop losses and grab liquidity, then quickly reverses direction - creating high-probability trading opportunities.

Core Concept: What is a Liquidity Sweep?

A liquidity sweep occurs when:

Price breaks above a swing high (or below a swing low) to trigger retail stop losses

Institutional players absorb this liquidity at favorable prices

Price quickly reverses back into the previous range

This creates a "fake breakout" or "stop hunt" pattern

The strategy exploits these manipulative moves by entering trades in the direction of the reversal.

How the Strategy Works

1. Swing Point Detection

Uses a lookback period (default: 20 bars) to identify significant swing highs and lows

Employs proper pivot point detection using ta.highestbars() and ta.lowestbars()

Only considers confirmed swing points (not just recent highs/lows)

2. Liquidity Sweep Identification

High Sweep (Short Setup):

Price moves above the last swing high (triggering buy stops)

Same bar closes back below the swing high (showing rejection)

Low Sweep (Long Setup):

Price moves below the last swing low (triggering sell stops)

Same bar closes back above the swing low (showing support)

3. Confirmation Process

Requires price to stay within the swept range for a specified number of bars (default: 3)

This confirms the sweep was genuine and not just normal volatility

Prevents false signals and improves trade quality

4. Entry Logic

Long Entries: Triggered after confirmed low sweeps

Short Entries: Triggered after confirmed high sweeps

5. Risk Management

Stop Loss: Placed at a multiple of ATR (default: 1.5x) from entry price

Take Profit: Risk/Reward ratio based (default: 2:1)

Position Sizing: 10% of equity per trade (configurable)

Red X-crosses: High sweeps detected

Green X-crosses: Low sweeps detected

Red triangles (down): Short entry signals

Green triangles (up): Long entry signals

Horizontal lines: Current swing high/low levels

Info label: Shows last detected swing levels

Optimal Conditions:

Timeframes: 1H, 4H, and Daily work best

Market Conditions: Ranging and trending markets both suitable

Volatility: Moderate to high volatility preferred

Session Times: Most effective during active trading sessions

Strengths:

✅ Exploits institutional manipulation tactics

✅ Clear entry/exit rules with defined risk

✅ Works across multiple asset classes

✅ Includes proper confirmation to reduce false signals

✅ Visual clarity for manual verification

✅ Reasonable risk/reward parameters

Limitations:

⚠️ Requires patience - not a high-frequency strategy

⚠️ Market dependent - fewer signals in low volatility periods

⚠️ Needs sufficient lookback data for swing identification

⚠️ May have drawdown periods during strong trending moves

⚠️ Requires understanding of market structure concepts

Best Practices for Users

Optimization Tips:

Adjust lookback period based on timeframe (shorter for lower TFs)

Test different confirmation periods for your market

Consider market session times when backtesting

Use alongside volume analysis for additional confirmation

Risk Management:

Never risk more than 2-3% per trade of total capital

Consider reducing position size during high-impact news

Monitor correlation if trading multiple pairs simultaneously

Use additional filters (trend, support/resistance) for confluence

Backtesting Recommendations:

Test on at least 6 months of historical data

Include different market conditions (trending, ranging, volatile)

Consider transaction costs and slippage in results

Forward test on demo before live implementation

Expected Results

Based on typical liquidity sweep strategy performance:

Disclaimer

This strategy is based on market structure analysis and institutional trading behavior patterns. Past performance doesn't guarantee future results. Users should:

Thoroughly backtest before live trading

Start with small position sizes

Understand the underlying concepts before implementation

Consider combining with other analysis methods

Always use proper risk management

The strategy works best when traders understand the psychological and structural elements of liquidity sweeps rather than just following signals blindly.

5m Exit AlertsThese can help a lot with Daytrading if you don't have a price target in mind when there's no clear resistance / support nearby, and you don't trust the market enough to hold it as a swing trade.

Keep in mind that its main purpose is to give you a "warning" that it might be good to look at your screen, instead of guaranteeing you "now is the best time to exit". You won't reach high winning stats by blindly following this alert.

"A Exit LONG":

(I'm using letters instead of numbers for all Exit alerts to make sure I don't accidentally confuse Enter and Exit alerts).

There are 4 conditions that might trigger it. The reasons show up in the exit alert message (unfortunately only as a number, since alert messages can't have "dynamic text" in TradingView), and can also be displayed as symbols in the chart (see image above - make sure to enable "Show Signals" in the indicator settings first though).

Here are the conditions sorted from best to worst:

Technical reversal: Bearish Hammer candle with Volume > 2 * avg volume (of last 30 candles), when 5m candle closed. Reversal very likely. This is usually the best time to take your gains for the rest of the day.

EMA 3/8 cross: standard 5m EMA 3/8 cross, indicating a trend reversal, or at least a pullback. Can also be helpful to detect double tops / double bottoms.

Trailing Stop Loss: Crossed below 30m EMA 8, 5m candle closed. This is a "fallback" alert in case EMA 3 was already below EMA 8 before you set up the alert. It's not unlikely that the stock might go further down to VWAP, so depending on the chart and market this might be a good opportunity to save the gains you have left.

"Final" Stop Loss: Crossed below VWAP. Usually not a good sign. If you entered around VWAP your losses shouldn't be big yet, but if you plan on holding the stock the Daily chart and market outlook should better be quite convincing, and you wouldn't have needed to use this alert in the first place.

Keep in mind these work of course best if you picked a "good" stock: clear movement, tidy price action, high volume. Otherwise alerts are more likely to be triggered redundantly.

Always consider how the market and stock looks like, then decide whether to exit or not! Usually it makes sense to wait a bit to see f. e. whether the stock bounces off the 30m EMA 8, and it's just a pullback.

"B Enter SHORT":

Similar, but for shorts...

"C 1m Scalp LONG" + "D 1m Scalp SHORT":

Simple Scalping alert for EMA 3/8 cross on a 1m chart - but without needing to use a 1m chart to set it up!

Unfortunately it's not as accurate as manually setting this alert up on a 1m chart. It might be an advantage though that it sometimes is triggered 1-2 min later, since this means there are less redundant triggerings.

It can be useful esp. on high momentum trades, but I honestly haven't used it in a looong while.

"X Candle Close":

same as in 5m Entry indicator: triggered when 5m candle is confirmed

"Z Trend Change: UP" + "Z Trend Change: DOWN":

This one is meant to be used only on SPY: It alerts you when SPY is changing its trending direction, which might mean entering or closing existing trades.

I have therefore set it up to never end (by setting it to "Once Per Bar Close" in the alert settings).

It's based on DMI positive or negative being > 25. I had it based on VWAP at the beginning, but there were days where it was triggered every 5 minutes...

More infos: www.reddit.com

Trend MasterOverview

The Strategy is a trend-following trading system designed for forex, stocks, or other markets on TradingView. It uses pivot points to identify support and resistance levels, combined with a 200-period Exponential Moving Average (EMA) to filter trades. The strategy enters long or short positions based on trend reversals during specific trading sessions (London or New York). It incorporates robust risk management, including position sizing based on risk percentage or fixed amount, trailing stop-losses, breakeven moves, and weekly/monthly profit/loss limits to prevent overtrading.

This script is ideal for traders who want a semi-automated approach with visual aids like colored session backgrounds, support/resistance lines, and a performance dashboard. It supports backtesting from a custom start date and can limit trades to one per session for discipline. Alerts are built-in for entries, exits, and stop-loss adjustments, making it compatible with automated trading bots.

Key Benefits:

Trend Reversal Detection: Spots higher highs/lows and lower highs/lows to confirm trend changes.

Session Filtering: Trades only during high-liquidity sessions to avoid choppy markets.

Risk Control: Automatically calculates position sizes to risk only a set percentage or dollar amount per trade.

Performance Tracking: Displays a table of weekly or monthly P&L (profit and loss) with color-coded heatmaps for easy review.

Customizable: Adjust trade direction, risk levels, take-profit ratios, and more via inputs.

The strategy uses a 1:1.2 risk-reward ratio by default but can be tweaked.

How It Works

Trend Identification:

The script calculates pivot highs and lows using left (4) and right (2) bars to detect swing points.

It identifies patterns like Higher Highs (HH), Higher Lows (HL), Lower Highs (LH), and Lower Lows (LL) to determine the trend direction (uptrend if above resistance, downtrend if below support).

Support (green dotted lines) and resistance (red dotted lines) are drawn dynamically and update on trend changes.

Bars are colored blue (uptrend) or black (downtrend) for visual clarity.

Entry Signals:

Long Entry: Price closes above the 200 EMA, trend shifts from down to up (e.g., breaking resistance), during an active session (London or NY), and no trade has been taken that session (if enabled).

Short Entry: Price closes below the 200 EMA, trend shifts from up to down (e.g., breaking support), during an active session, and no prior trade that session.

Trades can be restricted to "Long Only," "Short Only," or "Both."

Entries are filtered by a start date (e.g., from January 2022) and optional month-specific testing.

Position Sizing and Risk:

Risk per trade: Either a fixed dollar amount (e.g., $500) or percentage of equity (e.g., 1%).

Quantity is calculated as: Risk Amount / (Entry Price - Stop-Loss Price).

This ensures you never risk more than intended, regardless of market volatility.

Stop-Loss (SL) and Take-Profit (TP):

SL for Longs: Set below the recent support level, adjustable by a "reduce value" (e.g., tighten by 0-90%) and gap (e.g., add a buffer).

SL for Shorts: Set above the recent resistance level, with similar adjustments.

TP: Based on risk-reward ratio (default 1.2:1), so if SL is 100 pips away, TP is 120 pips in profit.

Visual boxes show SL (red) and TP (green) on the chart for the next 4 bars after entry.

Trade Management:

Trailing SL: Automatically moves SL to the new support (longs) or resistance (shorts) if it tightens the stop without increasing risk.

Breakeven Move: If enabled, SL moves to entry price once profit reaches a set ratio of initial risk (default 1:1). For example, if risk was 1%, SL moves to breakeven at 1% profit.

One Trade Per Session: Prevents multiple entries in the same London or NY session to avoid overtrading.

Sessions include optional weekend inclusion and are highlighted (blue for London, green for NY).

Risk Limits (Weekly/Monthly):

Monitors P&L for the current week or month.

Stops trading if losses hit a limit (e.g., -3%) or profits reach a target (e.g., +7%).

Resets at the start of each new week/month.

Alerts notify when limits are hit.

Exits:

Trades exit at TP, SL, or manually via alerts.

No time-based exits; relies on price action.

Performance Dashboard:

A customizable table (position, size, colors) shows P&L percentages for each week/month in a grid.

Rows = Years, Columns = Weeks (1-52) or Months (1-12).

Color scaling: Green for profits (darker for bigger wins), red for losses (darker for bigger losses).

Yearly totals in the last column.

Helps visualize strategy performance over time without manual calculations.

Input Parameters Explained

Here's a breakdown of the main inputs for easy customization:

Trade Direction: "Both" (default), "Long Only," or "Short Only" – Controls allowed trade types.

Test Only Selected Month: If true, backtests only the specified month from the start year.

Start Year/Month: Sets the backtest start date (default: Jan 2022).

Include Weekends: If true, sessions can include weekends (rarely useful for forex).

Only One Trade Per Session: Limits to one entry per London/NY session (default: true).

Risk Management Time Frame: "Weekly" or "Monthly" – For P&L limits.

Enable Limits: Toggle weekly/monthly stop trading on loss/profit thresholds.

Loss Limit (%)/Profit Target (%): Stops trading if P&L hits these (e.g., -3% loss or +7% profit).

London/New York Session: Enable/disable, with time ranges (e.g., London: 0800-1300 UTC).

Left/Right Bars: For pivot detection (default: 4 left, 2 right) – Higher values smooth signals.

Support/Resistance: Toggle lines, colors, style, width.

Change Bar Color: Colors bars based on trend.

TP RR: Take-profit risk-reward (default: 1.2).

Stoploss Reduce Value: Tightens SL (negative values widen it, 0-0.9 range).

Stoploss Gap: Adds a buffer to SL (e.g., 0.1% away from support).

Move to Breakeven: Enables SL move to entry at a profit ratio (default: true, 1:1).

Use Risk Amount $: If true, risks fixed $ (e.g., 500); else, % of equity (default: 1%).

EMA 3: The slow EMA period (default: 200) for trend filter.

Performance Display: Toggle table, location (e.g., Bottom Right), size, colors, scaling for heatmaps.

Setup and Usage Tips

Add to Chart: Copy the script into TradingView's Pine Editor, compile, and add to your chart.

Backtesting: Use the Strategy Tester tab. Adjust inputs and test on historical data.

Live Trading: Connect alerts to a broker or bot (e.g., via webhook). The script sends JSON-formatted alerts for entry, exit, SL moves, and limits.

Best Markets: Works well on crypto pairs like SOLUSD or RUNEUSD on 4H timeframes.

Risk Warning: This is not financial advice. Always use demo accounts first. Past performance doesn't guarantee future results. Commission is set to 0.05% by default – adjust for your broker.

Customization: Experiment with EMA length or RR ratio for your style.

- Trading Bot – Dynamic RSI (Professional) - Robot Strategy -1. General Concept and Philosophy

This strategy was designed for systematic traders and work especially well on short timeframes (1 to 5 minutes), who seek to capture trend reversal movements with a high degree of confirmation. The goal is not to follow the trend, but to identify precise entry points in oversold or overbought zones, and then to exit the position dynamically to adapt to changing market conditions.

The originality of Trading Bot Dynamic RSI lies not in a single indicator, but in the intelligent fusion of several concepts:

Dynamic RSI bands for both entries and exits .

A triple confirmation filter to secure trade entries.

A fully parameterizable design ready for automation .

2. Originality at the Core of the Strategy: Key Features

Dynamic Exits on RSI Bands: This is a main original feature of this script. Unlike traditional strategies that use fixed Take-Profits and Stop-Losses, this one uses an exit RSI band, calculated with parameters independent of the entry ones. This allows the strategy to:

Adapt to Volatility: In a volatile market, the exit band will move further away, allowing for the capture of larger moves. In a ranging market, it will tighten to secure smaller gains.

Optimize Profits: The exit occurs when momentum genuinely fades, not at an arbitrary price level, thus maximizing the potential of each trade.

Triple Confirmation Filter for Precise Entries: To avoid false signals, each entry is validated by the convergence of three distinct conditions:

The base signal is generated when the price reaches an overbought or oversold zone, materialized by an RSI band calculated directly on the chart.

The WaveTrend oscillator must also be in an extreme zone, confirming that the short-term momentum is ready for a reversal.

Finally, the StochRSI must validate that the RSI itself is in an overbought or oversold condition, adding an extra layer of security.

"Automation Ready" Design: The strategy was developed with automation in mind.

Customizable Alert Messages: All messages for entries and exits (Long/Short) can be formatted to be compatible with automated trade execution platforms.

Precise Capital Management: The position size calculation can be set as a fixed amount (e.g., 100 USDT), a percentage of the total capital, or of the available capital, and includes leverage. These parameters are crucial for a trading bot.

3. Detailed Operation

Entry Logic: A position is opened only if the following three conditions are met:

The market price touches (or closes below/above) the entry RSI band (lower for a buy, upper for a sell).

The WaveTrend indicator is in the oversold zone (for a buy) or overbought zone (for a sell).

The Stochastic RSI indicator is also in the oversold zone (for a buy) or overbought zone (for a sell).

The order is placed as a limit order on the RSI band, allowing for execution at the best possible price.

Exit Logic: The primary exit is dynamic.

For a Long position, the trade is closed when the price reaches the upper exit RSI band.

For a Short position, the trade is closed when the price reaches the lower exit RSI band.

Optionally, a percentage-based Stop-Loss and Take-Profit can be activated for more traditional risk management, although the dynamic exit is the recommended default mechanism.

4. Ease of Use and Customization

Despite its internal complexity, the strategy is designed to be user-friendly :

Clear Settings Panel: Parameters are grouped by function (Long Entry, Long Exit, Quantity, etc.), and each option comes with an explanatory tooltip.

Integrated Display: All key information (performance, current settings) is displayed in clean and discreet tables directly on the chart, allowing you to see at a glance how the strategy is configured.