KENW Liq Sweep 17This indicator is designed to alert on potential liquidity sweep events:

- In uptrends, it tracks Sell-Side Liquidity (SSL) by marking swing lows that occur during negative MACD histogram periods. It generates a long entry alert when price makes a lower low in SSL (i.e., the most recent SSL level is below the prior one), suggesting a sweep of sell-side liquidity before a potential bullish continuation.

- In downtrends, it tracks Buy-Side Liquidity (BSL) by marking swing highs that occur during positive MACD histogram periods. It generates a short entry alert when price makes a higher high in BSL (i.e., the most recent BSL level is above the prior one), indicating a sweep of buy-side liquidity before a potential bearish continuation.

在脚本中搜索"sweep"

Wick Sweep EntriesWick Sweep Entry designed by Finweal Finance (Indicator Originator : Prajyot Mahajan) :

This Indicator is specially designed for Nifty, Sensex and Banknifty Options Buying. This works well on Expiry Days.

Setup Timeframe : 5m and 1m.

Entry Criteria :

For Long/CE :

Wait for Sweep of 5m Candle Low with next 5m Candle but you do not wait for the next 5 minute candle to close, you enter directly whenever any 1 minute candle of next 5minute candle to close above the low of previous 5m Candle.

For Short/PE :

Wait for Sweep of 5m Candle High with next 5m Candle but you do not wait for the next 5 minute candle to close, you enter directly whenever any 1 minute candle of next 5minute candle to close below the High of previous 5m Candle.

Key notes :

1. As this is the Scalping High Frequency Strategy, it is to be used for scalping purpose only. You might have losses too so to avoid the noise in the market, i suggest you to use this strategy in the first 45 minutes to 1 hour of Indian Markets as this is a volatility Strategy.

2. Although Nifty and Banknifty are independent indices, they still show some reactions with each other, so if you spot a long entry on BNF and Short Entry on nifty then you will avoid taking the trade, you will take the trade only if there is a tandem activity or At least the other index is not showing opposite signal.

3. If target is not hit and you spot another entry, you will avoid taking the new entry.

The Indicator will automatically spot/plot the entry signal, all you need to do is enter as soon as 1minute candle closes either below prior 5 minute candle High for Short/PE or closes above 5minute low for Long/CE.

For Targets :

You Can Target recent minor pull back, FVG, or Order blocks.

Remember : This is a scalping strategy so don't hold trade for more than 4/5 1minute Candles

TJR asia session sweep//@version=5

strategy("TJR asia session sweep", "TJR Asia Sweep", overlay=true, max_lines_count=500, max_labels_count=500)

// Input settings

show_asian = input.bool(true, "Show Asian Session", group="Visual Settings")

show_london = input.bool(true, "Show London Session", group="Visual Settings")

show_swing_points = input.bool(true, "Show Asian Swing Points", group="Visual Settings")

show_market_structure = input.bool(true, "Show Market Structure", group="Visual Settings")

show_bos = input.bool(true, "Show Break of Structure", group="Visual Settings")

// Session Time Settings

asian_start_hour_input = input.int(22, "Asian Session Start Hour", minval=0, maxval=23, group="Session Times")

asian_end_hour_input = input.int(3, "Asian Session End Hour", minval=0, maxval=23, group="Session Times")

london_start_hour_input = input.int(3, "London Session Start Hour", minval=0, maxval=23, group="Session Times")

london_end_hour_input = input.int(8, "London Session End Hour", minval=0, maxval=23, group="Session Times")

session_timezone = input.string("America/New_York", "Session Timezone", options= , group="Session Times")

// Risk Management Settings

use_atr_sl = input.bool(false, "Use ATR Multiplier for Stop Loss", group="Risk Management")

atr_length = input.int(14, "ATR Length", minval=1, maxval=50, group="Risk Management")

atr_multiplier = input.float(2.0, "ATR Multiplier for Stop Loss", minval=0.5, maxval=10.0, group="Risk Management")

force_london_close = input.bool(true, "Force Close at London Session End", group="Risk Management")

cutoff_minutes = input.int(60, "Minutes Before Session End to Stop New Trades", minval=0, maxval=300, group="Risk Management")

// Position Sizing Settings

position_sizing_method = input.string("USD Risk", "Position Sizing Method", options= , group="Position Sizing")

usd_risk_per_trade = input.float(100.0, "USD Risk Per Trade", minval=1.0, maxval=10000.0, group="Position Sizing")

fixed_contracts = input.float(1.0, "Fixed Number of Contracts", minval=0.01, maxval=1000.0, step=0.01, group="Position Sizing")

// Color settings

asian_color = input.color(color.red, "Asian Session Color")

london_color = input.color(color.blue, "London Session Color")

swing_high_color = input.color(color.orange, "Swing High Color")

swing_low_color = input.color(color.lime, "Swing Low Color")

bullish_structure_color = input.color(color.green, "Bullish Structure Color")

bearish_structure_color = input.color(color.red, "Bearish Structure Color")

bos_color = input.color(color.orange, "Break of Structure Color")

// Line settings

line_width = input.int(2, "Line Width", minval=1, maxval=5)

// ATR calculation for stop loss

atr = ta.atr(atr_length)

// Position size calculation function

calculate_position_size(entry_price, stop_loss_price) =>

var float position_size = na

if position_sizing_method == "Fixed Contracts"

position_size := fixed_contracts

else // USD Risk method

stop_distance = math.abs(entry_price - stop_loss_price)

if stop_distance > 0

// Calculate position size based on USD risk per trade

// For forex: position_size = risk_amount / (stop_distance * point_value)

// For most forex pairs, point value = 1 (since we're dealing with price differences directly)

position_size := usd_risk_per_trade / stop_distance

else

position_size := fixed_contracts // Fallback to fixed contracts if stop distance is 0

position_size

// Session time definitions (using input variables)

asian_start_hour = asian_start_hour_input

asian_end_hour = asian_end_hour_input

london_start_hour = london_start_hour_input

london_end_hour = london_end_hour_input

// Get current hour using selected timezone

current_hour = hour(time, session_timezone)

// Previous hour for transition detection

prev_hour = hour(time , session_timezone)

// Session transition detection

asian_start = current_hour == asian_start_hour and prev_hour != asian_start_hour

asian_end = current_hour == asian_end_hour and prev_hour != asian_end_hour

london_start = current_hour == london_start_hour and prev_hour != london_start_hour

london_end = current_hour == london_end_hour and prev_hour != london_end_hour

// Session activity detection

asian_active = (current_hour >= asian_start_hour) or (current_hour < asian_end_hour)

london_active = (current_hour >= london_start_hour) and (current_hour < london_end_hour)

// Session boxes - keep previous sessions visible

var box asian_session_box = na

var box london_session_box = na

// Create Asian session box

if show_asian and asian_start

// Create new box at session start (previous box remains visible)

asian_session_box := box.new(bar_index, high, bar_index + 1, low,

border_color=asian_color, bgcolor=color.new(asian_color, 90),

border_width=2, border_style=line.style_solid)

// Pre-calculate session highs and lows for consistency

asian_session_length = asian_active and not na(asian_session_box) ? bar_index - box.get_left(asian_session_box) + 1 : 1

current_asian_high = ta.highest(high, asian_session_length)

current_asian_low = ta.lowest(low, asian_session_length)

// Update Asian session box continuously during session

if show_asian and asian_active and not na(asian_session_box)

box.set_right(asian_session_box, bar_index)

// Update box to contain session highs and lows

box.set_top(asian_session_box, current_asian_high)

box.set_bottom(asian_session_box, current_asian_low)

// Create London session box

if show_london and london_start

// Create new box at session start (previous box remains visible)

london_session_box := box.new(bar_index, high, bar_index + 1, low,

border_color=london_color, bgcolor=color.new(london_color, 90),

border_width=2, border_style=line.style_solid)

// Pre-calculate London session highs and lows for consistency

london_session_length = london_active and not na(london_session_box) ? bar_index - box.get_left(london_session_box) + 1 : 1

current_london_high = ta.highest(high, london_session_length)

current_london_low = ta.lowest(low, london_session_length)

// Update London session box continuously during session

if show_london and london_active and not na(london_session_box)

box.set_right(london_session_box, bar_index)

// Update box to contain session highs and lows

box.set_top(london_session_box, current_london_high)

box.set_bottom(london_session_box, current_london_low)

// Asian Session Swing Points Detection

var float asian_session_high = na

var float asian_session_low = na

var int asian_high_bar = na

var int asian_low_bar = na

// Asian Session Absolute High/Low for TP levels

var float asian_absolute_high = na

var float asian_absolute_low = na

var line asian_high_line = na

var line asian_low_line = na

var label asian_high_label = na

var label asian_low_label = na

var bool high_broken = false

var bool low_broken = false

// London Session High/Low tracking for stop loss

var float london_session_high = na

var float london_session_low = na

// Market structure tracking variables

var string breakout_direction = na // "bullish" or "bearish"

var float last_hh_level = na // Last Higher High level

var float last_hl_level = na // Last Higher Low level

var float last_ll_level = na // Last Lower Low level

var float last_lh_level = na // Last Lower High level

var int structure_count = 0

var string last_structure_type = na // "HH", "HL", "LL", "LH"

// Legacy variables for compatibility

var float last_swing_high = na

var float last_swing_low = na

var int last_high_bar = na

var int last_low_bar = na

// Market structure state tracking

var float pending_high = na

var float pending_low = na

var int pending_high_bar = na

var int pending_low_bar = na

var bool waiting_for_confirmation = false

// Break of Structure tracking variables

var float most_recent_hl = na

var float most_recent_lh = na

var int most_recent_hl_bar = na

var int most_recent_lh_bar = na

var bool bos_detected = false

// Trading variables

var bool trade_taken = false

// Trade visualization boxes (based on Casper strategy approach)

var box current_profit_box = na

var box current_sl_box = na

// Update swing points during Asian session

if asian_active and show_swing_points

// Always track absolute high/low for both TP levels and breakout detection

if na(asian_absolute_high) or high > asian_absolute_high

asian_absolute_high := high

if na(asian_absolute_low) or low < asian_absolute_low

asian_absolute_low := low

// Use absolute high/low for breakout levels (simplified logic)

if na(asian_session_high) or high > asian_session_high

asian_session_high := high

asian_high_bar := bar_index

if na(asian_session_low) or low < asian_session_low

asian_session_low := low

asian_low_bar := bar_index

// Track London session high/low for stop loss levels

if london_active

if na(london_session_high) or high > london_session_high

london_session_high := high

if na(london_session_low) or low < london_session_low

london_session_low := low

// Draw initial lines when Asian session ends

if asian_end and show_swing_points

if not na(asian_session_high) and not na(asian_high_bar)

// Draw extending line for high

asian_high_line := line.new(asian_high_bar, asian_session_high, bar_index + 200, asian_session_high,

color=swing_high_color, width=2, style=line.style_dashed, extend=extend.right)

asian_high_label := label.new(bar_index + 5, asian_session_high, "Asian High: " + str.tostring(asian_session_high, "#.####"), style=label.style_label_left, color=swing_high_color, textcolor=color.white, size=size.small)

if not na(asian_session_low) and not na(asian_low_bar)

// Draw extending line for low

asian_low_line := line.new(asian_low_bar, asian_session_low, bar_index + 200, asian_session_low,

color=swing_low_color, width=2, style=line.style_dashed, extend=extend.right)

asian_low_label := label.new(bar_index + 5, asian_session_low, "Asian Low: " + str.tostring(asian_session_low, "#.####"), style=label.style_label_left, color=swing_low_color, textcolor=color.white, size=size.small)

// Reset break flags for new session

high_broken := false

low_broken := false

// Check for breakouts during London session

if london_active and show_swing_points and not na(asian_session_high) and not na(asian_session_low)

// Check if Asian high is broken

if not high_broken and not low_broken and high > asian_session_high

high_broken := true

// Update high line to end at break point

if not na(asian_high_line)

line.set_x2(asian_high_line, bar_index)

line.set_extend(asian_high_line, extend.none)

// Remove the low line (first break wins)

if not na(asian_low_line)

line.delete(asian_low_line)

if not na(asian_low_label)

label.delete(asian_low_label)

// Add break marker

label.new(bar_index, asian_session_high * 1.001, "HIGH BREAK!",

style=label.style_label_down, color=color.red, textcolor=color.white, size=size.normal)

// Set breakout direction and initialize structure tracking

breakout_direction := "bullish"

last_swing_high := asian_session_high

last_swing_low := asian_session_low

last_high_bar := bar_index

structure_count := 0

// Check if Asian low is broken

if not low_broken and not high_broken and low < asian_session_low

low_broken := true

// Update low line to end at break point

if not na(asian_low_line)

line.set_x2(asian_low_line, bar_index)

line.set_extend(asian_low_line, extend.none)

// Remove the high line (first break wins)

if not na(asian_high_line)

line.delete(asian_high_line)

if not na(asian_high_label)

label.delete(asian_high_label)

// Add break marker

label.new(bar_index, asian_session_low * 0.999, "LOW BREAK!",

style=label.style_label_up, color=color.red, textcolor=color.white, size=size.normal)

// Set breakout direction and initialize structure tracking

breakout_direction := "bearish"

last_swing_high := asian_session_high

last_swing_low := asian_session_low

last_low_bar := bar_index

structure_count := 0

// Stop extending lines when London session ends (if not already broken)

if london_end and show_swing_points

if not high_broken and not na(asian_high_line)

line.set_x2(asian_high_line, bar_index)

line.set_extend(asian_high_line, extend.none)

if not low_broken and not na(asian_low_line)

line.set_x2(asian_low_line, bar_index)

line.set_extend(asian_low_line, extend.none)

// Force close all trades at London session end (if enabled)

if london_end and force_london_close

if strategy.position_size != 0

// Extend boxes immediately before session close to prevent timing issues

if not na(current_profit_box)

// Ensure minimum 8 bars width or extend to current bar, whichever is longer

box_left = box.get_left(current_profit_box)

min_right = box_left + 8

final_right = math.max(min_right, bar_index)

box.set_right(current_profit_box, final_right)

current_profit_box := na // Clear reference after extending

if not na(current_sl_box)

// Ensure minimum 8 bars width or extend to current bar, whichever is longer

box_left = box.get_left(current_sl_box)

min_right = box_left + 8

final_right = math.max(min_right, bar_index)

box.set_right(current_sl_box, final_right)

current_sl_box := na // Clear reference after extending

strategy.close_all(comment="London Close")

trade_taken := false // Reset trade flag for next session

// Market structure detection after breakout (only during London session and before first BoS)

if show_market_structure and not na(breakout_direction) and london_active and not bos_detected

// Bullish structure tracking (HH, HL alternating)

if breakout_direction == "bullish"

// Check for Higher High pattern: Bullish candle followed by bearish candle

pattern_high = math.max(high , high)

prev_hh = na(last_hh_level) ? last_swing_high : last_hh_level

// HH Detection: Only if we expect HH next (no last structure or last was HL)

if (na(last_structure_type) or last_structure_type == "HL") and close > open and close < open and pattern_high > prev_hh and close > prev_hh

// Check consolidation

is_too_close = not na(last_high_bar) and (bar_index - last_high_bar) <= 4

should_create_hh = true

if is_too_close and structure_count > 0 and pattern_high <= last_hh_level

should_create_hh := false

if should_create_hh

structure_count := structure_count + 1

label.new(bar_index - 1, high + (high * 0.0003), "HH" + str.tostring(structure_count),

style=label.style_none, color=color.new(color.white, 100),

textcolor=color.white, size=size.small)

last_hh_level := pattern_high

last_swing_high := pattern_high

last_high_bar := bar_index

last_structure_type := "HH"

// HL Detection: Only if we expect HL next (last was HH)

pattern_low = math.min(low , low)

prev_hl = na(last_hl_level) ? last_swing_low : last_hl_level

if last_structure_type == "HH" and close < open and close > open and pattern_low > prev_hl and close > prev_hl

// Check consolidation

is_too_close = not na(last_low_bar) and (bar_index - last_low_bar) <= 4

should_create_hl = true

if is_too_close and pattern_low <= last_hl_level

should_create_hl := false

if should_create_hl

structure_count := structure_count + 1

label.new(bar_index - 1, low - (low * 0.0003), "HL" + str.tostring(structure_count),

style=label.style_none, color=color.new(color.white, 100),

textcolor=color.white, size=size.small)

last_hl_level := pattern_low

most_recent_hl := pattern_low // Update most recent HL for BoS detection

most_recent_hl_bar := bar_index - 1 // Store HL bar position

last_low_bar := bar_index

last_structure_type := "HL"

// Bearish structure tracking (LL, LH alternating)

if breakout_direction == "bearish"

// Check for Lower Low pattern: Bearish candle followed by bullish candle

pattern_low = math.min(low , low)

prev_ll = na(last_ll_level) ? last_swing_low : last_ll_level

// LL Detection: Only if we expect LL next (no last structure or last was LH)

if (na(last_structure_type) or last_structure_type == "LH") and close < open and close > open and pattern_low < prev_ll and close < prev_ll

// Check consolidation

is_too_close = not na(last_low_bar) and (bar_index - last_low_bar) <= 4

should_create_ll = true

if is_too_close and structure_count > 0 and pattern_low >= last_ll_level

should_create_ll := false

if should_create_ll

structure_count := structure_count + 1

label.new(bar_index - 1, low - (low * 0.0003), "LL" + str.tostring(structure_count),

style=label.style_none, color=color.new(color.white, 100),

textcolor=color.white, size=size.small)

last_ll_level := pattern_low

last_swing_low := pattern_low

last_low_bar := bar_index

last_structure_type := "LL"

// LH Detection: Only if we expect LH next (last was LL)

pattern_high = math.max(high , high)

prev_lh = na(last_lh_level) ? last_swing_high : last_lh_level

if last_structure_type == "LL" and close > open and close < open and pattern_high < prev_lh and close < prev_lh

// Check consolidation

is_too_close = not na(last_high_bar) and (bar_index - last_high_bar) <= 4

should_create_lh = true

if is_too_close and pattern_high >= last_lh_level

should_create_lh := false

if should_create_lh

structure_count := structure_count + 1

label.new(bar_index - 1, high + (high * 0.0003), "LH" + str.tostring(structure_count),

style=label.style_none, color=color.new(color.white, 100),

textcolor=color.white, size=size.small)

last_lh_level := pattern_high

most_recent_lh := pattern_high // Update most recent LH for BoS detection

most_recent_lh_bar := bar_index - 1 // Store LH bar position

last_high_bar := bar_index

last_structure_type := "LH"

// Check if we're within the cutoff period before London session end

current_minute = minute(time, session_timezone)

london_end_time_minutes = london_end_hour * 60 // Convert London end hour to minutes

current_time_minutes = current_hour * 60 + current_minute // Current time in minutes

// Calculate minutes remaining in London session

london_session_minutes_remaining = london_end_time_minutes - current_time_minutes

// Handle day rollover case (e.g., if london_end is 8:00 (480 min) and current is 23:30 (1410 min))

if london_session_minutes_remaining < 0

london_session_minutes_remaining := london_session_minutes_remaining + (24 * 60) // Add 24 hours in minutes

// Only allow trades if more than cutoff_minutes remaining in London session

allow_new_trades = london_session_minutes_remaining > cutoff_minutes

// Break of Structure (BoS) Detection and Trading Logic - Only first BoS per London session and outside cutoff period

if show_bos and london_active and show_market_structure and not bos_detected and not trade_taken and allow_new_trades

// Bullish BoS: Price closes below the most recent HL (after bullish breakout) - SELL SIGNAL

if breakout_direction == "bullish" and not na(most_recent_hl) and not na(most_recent_hl_bar)

// Check minimum distance requirement (at least 4 candles between BoS and HL)

if close < most_recent_hl and (bar_index - most_recent_hl_bar) >= 4

// Draw dotted line from HL position to BoS point

line.new(most_recent_hl_bar, most_recent_hl, bar_index, most_recent_hl,

color=bos_color, width=2, style=line.style_dotted, extend=extend.none)

// Calculate center position for BoS label

center_bar = math.round((most_recent_hl_bar + bar_index) / 2)

// Draw BoS label below the line for HL break

label.new(center_bar, most_recent_hl - (most_recent_hl * 0.0005), "BoS",

style=label.style_none, color=color.new(color.white, 100),

textcolor=bos_color, size=size.normal)

// SELL ENTRY

if not na(london_session_high) and not na(asian_absolute_low)

// Calculate stop loss based on settings

stop_loss_level = use_atr_sl ? close + (atr * atr_multiplier) : london_session_high

take_profit_level = asian_absolute_low

entry_price = close

// Calculate position size based on user settings

position_size = calculate_position_size(entry_price, stop_loss_level)

strategy.entry("SELL", strategy.short, qty=position_size, comment="BoS Sell")

strategy.exit("SELL EXIT", "SELL", stop=stop_loss_level, limit=take_profit_level, comment="SL/TP")

// Create trade visualization boxes (TradingView style) - minimum 8 bars width

// Blue profit zone box (from entry to take profit)

current_profit_box := box.new(left=bar_index, top=take_profit_level, right=bar_index + 8, bottom=entry_price,

bgcolor=color.new(color.blue, 70), border_width=0)

// Red stop loss zone box (from entry to stop loss)

current_sl_box := box.new(left=bar_index, top=entry_price, right=bar_index + 8, bottom=stop_loss_level,

bgcolor=color.new(color.red, 70), border_width=0)

trade_taken := true

bos_detected := true // Mark BoS as detected for this session

// Bearish BoS: Price closes above the most recent LH (after bearish breakout) - BUY SIGNAL

if breakout_direction == "bearish" and not na(most_recent_lh) and not na(most_recent_lh_bar)

// Check minimum distance requirement (at least 4 candles between BoS and LH)

if close > most_recent_lh and (bar_index - most_recent_lh_bar) >= 4

// Draw dotted line from LH position to BoS point

line.new(most_recent_lh_bar, most_recent_lh, bar_index, most_recent_lh,

color=bos_color, width=1, style=line.style_dotted, extend=extend.none)

// Calculate center position for BoS label

center_bar = math.round((most_recent_lh_bar + bar_index) / 2)

// Draw BoS label above the line for LH break

label.new(center_bar, most_recent_lh + (most_recent_lh * 0.0005), "BoS",

style=label.style_none, color=color.new(color.white, 100),

textcolor=bos_color, size=size.normal)

// BUY ENTRY

if not na(london_session_low) and not na(asian_absolute_high)

// Calculate stop loss based on settings

stop_loss_level = use_atr_sl ? close - (atr * atr_multiplier) : london_session_low

take_profit_level = asian_absolute_high

entry_price = close

// Calculate position size based on user settings

position_size = calculate_position_size(entry_price, stop_loss_level)

strategy.entry("BUY", strategy.long, qty=position_size, comment="BoS Buy")

strategy.exit("BUY EXIT", "BUY", stop=stop_loss_level, limit=take_profit_level, comment="SL/TP")

// Create trade visualization boxes (TradingView style) - minimum 8 bars width

// Blue profit zone box (from entry to take profit)

current_profit_box := box.new(left=bar_index, top=entry_price, right=bar_index + 8, bottom=take_profit_level,

bgcolor=color.new(color.blue, 70), border_width=0)

// Red stop loss zone box (from entry to stop loss)

current_sl_box := box.new(left=bar_index, top=stop_loss_level, right=bar_index + 8, bottom=entry_price,

bgcolor=color.new(color.red, 70), border_width=0)

trade_taken := true

bos_detected := true // Mark BoS as detected for this session

// Position close detection for extending boxes (based on Casper strategy)

if barstate.isconfirmed and strategy.position_size == 0 and strategy.position_size != 0

// Extend trade visualization boxes to exact exit point when position closes

if not na(current_profit_box)

// Ensure minimum 8 bars width or extend to current bar, whichever is longer

box_left = box.get_left(current_profit_box)

min_right = box_left + 8

final_right = math.max(min_right, bar_index)

box.set_right(current_profit_box, final_right)

current_profit_box := na // Clear reference after extending

if not na(current_sl_box)

// Ensure minimum 8 bars width or extend to current bar, whichever is longer

box_left = box.get_left(current_sl_box)

min_right = box_left + 8

final_right = math.max(min_right, bar_index)

box.set_right(current_sl_box, final_right)

current_sl_box := na // Clear reference after extending

// Backup safety check - extend boxes if position is closed but boxes still active

if not na(current_profit_box) and strategy.position_size == 0

box_left = box.get_left(current_profit_box)

min_right = box_left + 8

final_right = math.max(min_right, bar_index)

box.set_right(current_profit_box, final_right)

current_profit_box := na

if not na(current_sl_box) and strategy.position_size == 0

box_left = box.get_left(current_sl_box)

min_right = box_left + 8

final_right = math.max(min_right, bar_index)

box.set_right(current_sl_box, final_right)

current_sl_box := na

// Reset everything when new Asian session starts

if asian_start and show_swing_points

asian_session_high := na

asian_session_low := na

asian_high_bar := na

asian_low_bar := na

// Reset absolute levels

asian_absolute_high := na

asian_absolute_low := na

asian_high_line := na

asian_low_line := na

asian_high_label := na

asian_low_label := na

high_broken := false

low_broken := false

// Reset London session levels

london_session_high := na

london_session_low := na

// Reset market structure tracking

breakout_direction := na

last_hh_level := na

last_hl_level := na

last_ll_level := na

last_lh_level := na

last_swing_high := na

last_swing_low := na

last_high_bar := na

last_low_bar := na

structure_count := 0

last_structure_type := na

pending_high := na

pending_low := na

pending_high_bar := na

pending_low_bar := na

waiting_for_confirmation := false

// Reset BoS tracking

most_recent_hl := na

most_recent_lh := na

most_recent_hl_bar := na

most_recent_lh_bar := na

bos_detected := false

// Reset trading

trade_taken := false

// Reset current trade boxes

current_profit_box := na

current_sl_box := na

// Debug info (optional)

show_debug = input.bool(false, "Show Debug Info")

if show_debug

var table debug_table = table.new(position.top_right, 2, 3, bgcolor=color.white, border_width=1)

if barstate.islast

table.cell(debug_table, 0, 0, "Current Hour:", text_color=color.black)

table.cell(debug_table, 1, 0, str.tostring(current_hour), text_color=color.black)

table.cell(debug_table, 0, 1, "Asian Active:", text_color=color.black)

table.cell(debug_table, 1, 1, str.tostring((current_hour >= asian_start_hour) or (current_hour < asian_end_hour)), text_color=color.black)

table.cell(debug_table, 0, 2, "London Active:", text_color=color.black)

table.cell(debug_table, 1, 2, str.tostring((current_hour >= london_start_hour) and (current_hour < london_end_hour)), text_color=color.black)

Swing High/Low Levels (Auto Remove)Plots untapped swing high and low levels from higher timeframes. Used for liquidity sweep strategy. Cluster of swing levels are a magnet for price to return to and reverse. Indicator gives option for candle body or wick for sweep to remove lines.

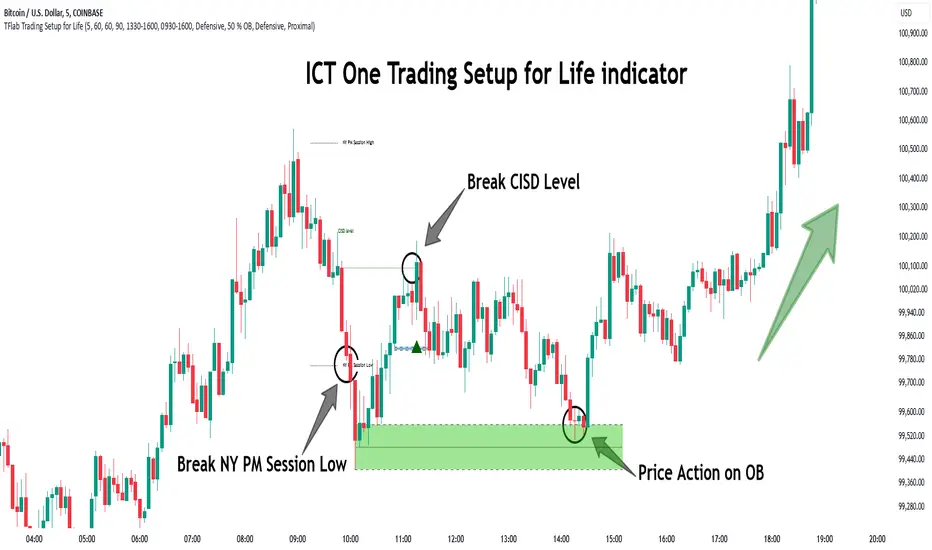

One Trading Setup for Life ICT [TradingFinder] Sweep Session FVG🔵 Introduction

ICT One Trading Setup for Life is a trading strategy based on liquidity and market structure shifts, utilizing the PM Session Sweep to determine price direction. In this strategy, the market first forms a price range during the PM Session (from 13:30 to 16:00 EST), which includes the highest high (PM Session High) and lowest low (PM Session Low).

In the next session, the price first touches one of these levels to trigger a Liquidity Hunt before confirming its trend by breaking the Change in State of Delivery (CISD) Level. After this confirmation, the price retraces toward a Fair Value Gap (FVG) or Order Block (OB), which serve as the best entry points in alignment with liquidity.

In financial markets, liquidity is the primary driver of price movement, and major market participants such as institutional investors and banks are constantly seeking liquidity at key levels. This process, known as Liquidity Hunt or Liquidity Sweep, occurs when the price reaches an area with a high concentration of orders, absorbs liquidity, and then reverses direction.

In this setup, the PM Session range acts as a trading framework, where its highs and lows function as key liquidity zones that influence the next session’s price movement. After the New York market opens at 9:30 EST, the price initially breaks one of these levels to capture liquidity.

However, for a trend shift to be confirmed, the CISD Level must be broken.

Once the CISD Level is breached, the price retraces toward an FVG or OB, which serve as optimal trade entry points.

Bullish Setup :

Bearish Setup :

🔵 How to Use

In this strategy, the PM Session range is first identified, which includes the highest high (PM Session High) and lowest low (PM Session Low) between 13:30 and 16:00 EST. In the following session, the price touches one of these levels for a Liquidity Hunt, followed by a break of the Change in State of Delivery (CISD) Level. The price then retraces toward a Fair Value Gap (FVG) or Order Block (OB), creating a trading opportunity.

This process can occur in two scenarios : bearish and bullish setups.

🟣 Bullish Setup

In a bullish scenario, the PM Session High and PM Session Low are identified. In the following session, the price first breaks the PM Session Low, absorbing liquidity. This process results in a Fake Breakout to the downside, misleading retail traders into taking short positions.

After the Liquidity Hunt, the CISD Level is broken, confirming a trend reversal. The price then retraces toward an FVG or OB, offering an optimal long entry opportunity.

The initial take-profit target is the PM Session High, but if higher timeframe liquidity levels exist, extended targets can be set.

The stop-loss should be placed below the Fake Breakout low or the first candle of the FVG.

🟣 Bearish Setup

In a bearish scenario, the market first defines its PM Session High and PM Session Low. In the next session, the price initially breaks the PM Session High, triggering a Liquidity Hunt. This movement often causes a Fake Breakout, misleading retail traders into taking incorrect positions.

After absorbing liquidity, the CISD Level breaks, indicating a shift in market structure. The price then retraces toward an FVG or OB, offering the best short entry opportunity.

The initial take-profit target is the PM Session Low, but if additional liquidity exists on higher timeframes, lower targets can be considered.

The stop-loss should be placed above the Fake Breakout high or the first candle of the FVG.

🔵 Setting

CISD Bar Back Check : The Bar Back Check option enables traders to specify the number of past candles checked for identifying the CISD Level, enhancing CISD Level accuracy on the chart.

Order Block Validity : The number of candles that determine the validity of an Order Block.

FVG Validity : The duration for which a Fair Value Gap remains valid.

CISD Level Validity : The duration for which a CISD Level remains valid after being broken.

New York PM Session : Defines the PM Session range from 13:30 to 16:00 EST.

New York AM Session : Defines the AM Session range from 9:30 to 16:00 EST.

Refine Order Block : Enables finer adjustments to Order Block levels for more accurate price responses.

Mitigation Level OB : Allows users to set specific reaction points within an Order Block, including: Proximal: Closest level to the current price. 50% OB: Midpoint of the Order Block. Distal: Farthest level from the current price.

FVG Filter : The Judas Swing indicator includes a filter for Fair Value Gap (FVG), allowing different filtering based on FVG width: FVG Filter Type: Can be set to "Very Aggressive," "Aggressive," "Defensive," or "Very Defensive." Higher defensiveness narrows the FVG width, focusing on narrower gaps.

Mitigation Level FVG : Like the Order Block, you can set price reaction levels for FVG with options such as Proximal, 50% OB, and Distal.

Demand Order Block : Enables or disables bullish Order Block.

Supply Order Block : Enables or disables bearish Order Blocks.

Demand FVG : Enables or disables bullish FVG.

Supply FVG : Enables or disables bearish FVGs.

Show All CISD : Enables or disables the display of all CISD Levels.

Show High CISD : Enables or disables high CISD levels.

Show Low CISD : Enables or disables low CISD levels.

🔵 Conclusion

The ICT One Trading Setup for Life is a liquidity-based strategy that leverages market structure shifts and precise entry points to identify high-probability trade opportunities. By focusing on PM Session High and PM Session Low, this setup first captures liquidity at these levels and then confirms trend shifts with a break of the Change in State of Delivery (CISD) Level.

Entering a trade after a retracement to an FVG or OB allows traders to position themselves at optimal liquidity levels, ensuring high reward-to-risk trades. When used in conjunction with higher timeframe bias, order flow, and liquidity analysis, this strategy can become one of the most effective trading methods within the ICT Concept framework.

Successful execution of this setup requires risk management, patience, and a deep understanding of liquidity dynamics. Traders can enhance their confidence in this strategy by conducting extensive backtesting and analyzing past market data to optimize their approach for different assets.

Liquidity Sweep Indicator (Signal-based SL + BE/TP)I created a more advanced version of my Liquidity Sweep Indicator. Open source, but I dont recommend to create a TV-strategy from the code because you should combine it with price action an chart analysis! Have fun :)

Session Sweep + Retrace (London + NY) - FixedORB Strategy with confluence. This sets out the 5 min session sweep from London and NY, and highlights a test back into the order zone with fib retracement.

BTC LL->HH Liquidity Sweep / BOS / Retest / 4H Bias v6_8BTC LL->HH Liquidity Sweep / BOS / Retest / 4H Bias v6_8

Liquidity Sweep Breakout - LSBLiquidity Sweep Breakout - LSB

A professional session-based breakout system designed for OANDA:USDJPY and other JPY pairs.

Not guesswork, but precision - built on detailed observation of institutional moves to capture clear trade direction daily.

Master the Market’s Daily Bank Flow.

---

Strategy Detail:

I discovered this strategy after carefully studying how Japanese banks influence the forex market during their daily settlement period. Banks are some of the biggest players in the financial world, and when they adjust or settle their accounts in the morning, it often creates a push in the market. From years of observation, I noticed a consistent pattern, once banks finish their settlements, the market usually continues moving in the same direction that was formed right after those actions. This daily banking flow often sets the tone for the entire trading session, especially for JPY pairs like USDJPY.

To capture this move, I built the indicator so that it follows the bank-driven trend with clear rules for entries, stop-loss (SL), and take-profit (TP). The system is designed with professional risk management in mind. By default, it assumes a $10,000 account size, risks only 1% of that balance per trade, and targets a 1:1.5 reward-to-risk ratio. This means for every $100 risked, the potential profit is $150. Such controlled risk makes the system safer and more sustainable for long-term traders. At the same time, users are not limited to this setup, they can adjust the account balance in the settings, and the indicator will automatically recalculate the lot size and risk levels based on their own capital. This ensures the strategy works for small accounts and larger accounts alike.

🌍 Why It Works

Fundamentally driven: Based on **daily Japanese banking settlement flows**.

Session-specific precision: Targets the exact window when USDJPY liquidity reshapes.

Risk-managed: Always calculates lot size based on account and risk preferences.

Automatable: With webhook + MT5 EA, it can be fully hands-free.

---

✅ Recommended

Pair: USDJPY (best observed behavior).

Timeframe: 3-Minute chart.

Platform: TradingView Premium (for webhooks).

Execution: MT5 via EA.

---

🔎 Strategy Concept

The Tokyo Magic Breakout (TMB) is built on years of session observation and the unique daily rhythm of the Japanese banking system.

Every morning between 5:50 AM – 6:10 AM PKT (09:50 – 10:10 JST), Japanese banks perform daily reconciliation and settlement. This often sets the tone for the USDJPY direction of the day.

This strategy isolates that critical moment of liquidity adjustment and waits for a clean breakout confirmation. Instead of chasing noise, it executes only when price action is aligned with the Tokyo market’s hidden flows.

---

🕒 Timing Logic

Session Start: 5:00 AM PKT (Tokyo market open range).

Magic Candle: The 5:54 AM PKT candle is marked as the reference “breakout selector.”

Checkpoints: First confirmation at 6:30 AM PKT, then every 15 minutes until 8:30 AM PKT.

* If price stays inside the magic range → wait.

* If a breakout happens but the candle wick touches the range → wait for the next checkpoint.

* If by 8:30 AM PKT no clean breakout occurs → the day is marked as No Trade Day (NTD).

👉 Recommended timeframe: 3-Minute chart (3M) for precise signals.

---

📈 Trade Execution

Entry: Clean break above/below the magic candle’s range.

Stop-Loss: Opposite side of the Tokyo session high/low.

Take-Profit: Calculated by Reward\:Risk ratio (default 1.5:1).

Lot Size: Auto-calculated based on your risk model:

* Fixed Dollar

* % of Equity

* Conservative (minimum of both).

Visuals include:

✅ Entry/SL/TP lines

✅ Shaded risk (red) and reward (green) zones

✅ Trade labels (Buy/Sell with lot size & levels)

✅ TP/SL hit markers

---

🔔 Alerts & Automation (AutoTMB)

This strategy is fully automation-ready with EA + MT5:

1. Enable alerts in TMB settings.

2. Insert your PineConnector License Key.

3. Configure your risk management preferences.

4. Create a TradingView alert → in the message box simply type:

Pine Script®

{{alert_message}}

and set the EA webhook.

Now, every breakout trade (with exact entry, SL, TP, and lot size) is sent instantly.

👉 On your MT5:

* Install the EA.

* Use the same license key.

* Run it on a VPS or local MT5 terminal.

You now have a hands-free trading system: AutoTMB.

Current Hourly Open Liquidity with Sweep DetectionStatistics indicate that if the current hourly candle reaches the high or low of the previous hourly candle, there is a strong likelihood that the price will return to the current hour's open, depending on how quickly the previous hour's high or low was swept. If the sweep occurs within the first 20 minutes, there is a 75% chance the current hour's open will be reached; if it takes between 21 and 40 minutes, the probability decreases to 50%; and if it takes longer than 41 minutes, the chance drops to 25%.

These statistics can help identify manipulation on the hourly timeframe and guide trade decisions accordingly. For instance, if the previous hourly high is taken within the first 20 minutes but the current hour's open is not reached, it may be wise to avoid long positions until it happens or consider short positions in the direction of the open liquidity, using your existing entry rules and risk management.

The indicator highlights the current hour's open with a line and label to visually represent that liquidity pool, adjusting the line's color based on whether and when the previous hour's high or low was tapped. Once the open is reached, the indicator can, depending on settings, remove the line and label from the chart (this is enabled by default) since the liquidity pool is no longer relevant, preventing chart clutter.

All colors, line widths, label text sizes, and colors can be customized.

AMD Liquidity Sweep with AlertsAMD Liquidity Sweep with Alerts

Identify key liquidity levels from the Asian trading session with visual markers and alerts.

📌 Key Features:

Asia Session Detection

Customizable start/end hours (0-23) to match your trading timezone

Automatically calculates session high/low

Smart Swing Level Identification

Finds the closest significant swing high ≥ Asia high

Finds the closest significant swing low ≤ Asia low

Adjustable pivot sensitivity (# of left/right bars)

Professional Visuals

Dashed reference lines extending into the future

Blue-highlighted key levels

Clean label formatting with precise price levels

Trading Alerts

Price-cross alerts for liquidity breaks

Visual markers (triangles) when levels are breached

Separate alerts for buy-side/sell-side liquidity

Customization Options

Toggle intermediate swing highlights

Adjust label sizes

💡 Trading Applications:

Institutional Levels: Identify zones where Asian session liquidity pools exist

Breakout Trading: Get alerted when price breaches Asian session ranges

S/R Flip Zones: Watch how price reacts at these key reference levels

London/NY Open: Use Asian levels for early European session trades

🔧 How to Use:

Set your preferred Asia session hours

Adjust pivot sensitivity (default 1 bar works for most timeframes)

Enable alerts for breakouts if desired

Watch for reactions at the plotted levels

Session Breakout/Sweep with alertsThis indicator is based on popular London breakout strategy. but as I noticed that it don't work good with breakouts so I made it to be used as reversal entries as well. By default the timing is set for asian session but you can change it according to your need.

Use as breakout

Use as liquidity sweep

Note:

On some pairs the timing changes automatically (I don't know why), if you face this issue , go to settings and set the timing accordingly and save it as templet so that you don't have to change it every time you load the chart with timing issue.

I hope you guys find it useful. Do share your though and feedback in comments.

HTF Liquidity Levels█ OVERVIEW

The indicator introduces a new representation of the previous days, weeks, and months highs & lows ( DWM HL ) with a focus on untapped levels.

█ CONCEPTS

Untapped Levels

It is popularly known that the liquidity is located behind swing points or beyond higher time frames highs/lows (in a sense, an intraday swing point is a day high/low). These key areas are said "liquid" because of the accumulation of resting orders, mainly in the form of stop-loss orders. And this more significantly on higher time frames which have more time for stacking orders. As the result, the indicator aims to keep track of untapped levels that have their liquidity states intact.

Liquidity Pools

Once a liquidity level identified, or better, a cluster of liquidity levels work as magnets for the market. The price is more likely to make its way towards heavier pockets of liquidity, by proximity (the closest liquidity pool), and by difficulty (path with less obstacles). This phenomenon is referred as liquidity run, raid, purge, grab, hunt, sweep, you name it. Consequently, the indicator can help you frame a directional bias during your trading session.

█ NOTES

Drawings

Once a level is tapped, it is highlighted. At the end of each day, all tapped levels are cleared.

SL Hunter Tracker SL Hunter Tracker

coded by Bogdan Vaida

SL Hunter Tracker is a meticulous hunter that tracks SL hunters.

First it plots the fractals on the chart, then it draws lines from them

to the last wick that touched that height. You can add sweep alerts, once

per bar close, so that you get notified when a wick was touched.

Tested on: EURUSD 30'

0DTE Watchlist0DTE Watchlist – Intraday Momentum Scanner

This script is a real-time multi-symbol intraday watchlist designed for 0DTE options and high-conviction day trades. It continuously scans up to 10 large-cap symbols for clean Opening Range Breakout (ORB) continuation setups using structure, VWAP alignment, and controlled risk parameters.

The indicator automatically:

Defines the Opening Range (customizable minutes after the open)

Detects bullish and bearish structure (higher highs/lows or lower lows/highs)

Confirms momentum with ORB breaks, retests, and liquidity sweeps

Applies an optional VWAP filter to avoid low-quality trades

Calculates ATR-based stop loss, TP1, and TP2 levels

Manages trades with break-even logic, cooldown periods, and session resets

All signals are displayed in a clean table dashboard, showing:

Current trade status (Call / Put / In Trade / Cooldown / Closed)

Live price, entry, stop loss, TP1, TP2

ORB high and low levels per symbol

How to use:

Add your preferred large-cap symbols (SPY, NVDA, META, etc.)

Use a 1–5 min chart for 0DTE scalping

Wait for the table to show “BUY CALL” or “BUY PUT”

Execute via your options platform and manage risk using the provided levels

Avoid trades during cooldown or outside regular market hours

This tool is optimized for clean trend days, institutional momentum, and continuation moves—not chop or mean-reversion noise.

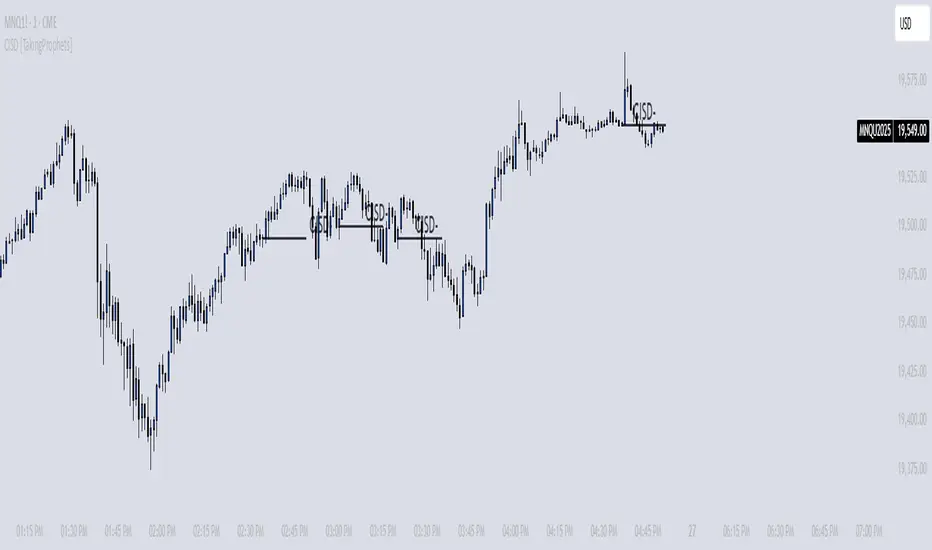

CISD [TakingProphets]🧠 Indicator Purpose:

The "CISD - Change in State of Delivery" is a precision tool designed for traders utilizing ICT (Inner Circle Trader) conecpets. It detects critical shifts in delivery conditions after liquidity sweeps — helping you spot true smart money activity and optimal trade opportunities. This script is especially valuable for traders applying liquidity concepts, displacement recognition, and market structure shifts at both intraday and swing levels.

🌟 What Makes This Indicator Unique:

Unlike basic trend-following or scalping tools, CISD operates through a two-phase smart money logic:

Liquidity Sweep Detection (sweeping Buyside or Sellside Liquidity).

State of Delivery Change Identification (through bearish or bullish displacement after the sweep).

It intelligently tracks candle sequences and only signals a CISD event after true displacement — offering a much deeper context than ordinary indicators.

⚙️ How the Indicator Works:

Swing Point Detection: Identifies recent pivot highs/lows to map Buyside Liquidity (BSL) and Sellside Liquidity (SSL) zones.

Liquidity Sweeps: Watches for price breaches of these liquidity points to detect institutional stop hunts.

Sequence Recognition: Finds series of same-direction candles before sweeps to mark institutional accumulation/distribution.

Change of Delivery Confirmation: Confirms CISD only after significant displacement moves price against the initial candle sequence.

Visual Markings: Automatically plots CISD lines and optional labels, customizable in color, style, and size.

🎯 How to Use It:

Identify Liquidity Sweeps: Watch for CISD levels plotted after a liquidity sweep event.

Plan Entries: Look for retracements into CISD lines for high-probability entries.

Manage Risk: Use CISD levels to refine your stop-loss and profit-taking zones.

Best Application:

After stop hunts during Killzones (London Open, New York AM).

As part of the Flow State Model: identify higher timeframe PD Arrays ➔ wait for lower timeframe CISD confirmation.

🔎 Underlying Concepts:

Liquidity Pools: Highs and lows cluster stop orders, attracting institutional sweeps.

Displacement: Powerful price moves post-sweep confirm smart money involvement.

Market Structure: CISD frequently precedes major Change of Character (CHoCH) or Break of Structure (BOS) shifts.

🎨 Customization Options:

Adjustable line color, width, and style (solid, dashed, dotted).

Optional label display with customizable color and sizing.

Line extension settings to keep CISD zones visible for future reference.

✅ Recommended for:

Traders studying ICT Smart Money Concepts.

Intraday scalpers and higher timeframe swing traders.

Traders who want to improve entries around liquidity sweeps and institutional displacement moves.

🚀 Bonus Tip:

For maximum confluence, pair this with the HTF POI, ICT Liquidity Levels, and HTF Market Structure indicators available at TakingProphets.com! 🔥

2022 Model ICT Entry Strategy [TradingFinder] One Setup For Life🔵 Introduction

The ICT 2022 model, introduced by Michael Huddleston, is an advanced trading strategy rooted in liquidity and price imbalance, where time and price serve as the core elements. This ICT 2022 trading strategy is an algorithmic approach designed to analyze liquidity and imbalances in the market. It incorporates concepts such as Fair Value Gap (FVG), Liquidity Sweep, and Market Structure Shift (MSS) to help traders identify liquidity movements and structural changes in the market, enabling them to determine optimal entry and exit points for their trades.

This Full ICT Day Trading Model empowers traders to pinpoint the Previous Day High/Low as well as the highs and lows of critical sessions like the London and New York sessions. These levels act as Liquidity Zones, which are frequently swept prior to a market structure shift (MSS) or a retracement to areas such as Optimal Trade Entry (OTE).

Bullish :

Bearish :

🔵 How to Use

The ICT 2022 model is a sophisticated trading strategy that focuses on identifying key liquidity levels and price movements. It operates based on two main principles. In the first phase, the price approaches liquidity zones and sweeps critical levels such as the previous day’s high or low and key session levels.

This movement is known as a Liquidity Sweep. In the second phase, following the sweep, the price retraces to areas like the FVG (Fair Value Gap), creating ideal entry points for trades. Below is a detailed explanation of how to apply this strategy in bullish and bearish setups.

🟣 Bullish ICT 2022 Model Setup

To use the ICT 2022 model in a bullish setup, start by identifying the Previous Day High/Low or key session levels, such as those of the London or New York sessions. In a bullish setup, the price usually moves downward first, sweeping the Liquidity Low. This move, known as a Liquidity Sweep, reflects the collection of buy orders by major market participants.

After the liquidity sweep, the price should shift market structure and start moving upward; this shift, referred to as Market Structure Shift (MSS), signals the beginning of an upward trend. Following MSS, areas like FVG, located within the Discount Zone, are identified. At this stage, the trader waits for the price to retrace to these zones. Once the price returns, a long trade is executed.

Finally, the stop-loss should be set below the liquidity low to manage risk, while the take-profit target is usually placed above the previous day’s high or other identified liquidity levels. This structure enables traders to take advantage of the upward price movement after the liquidity sweep.

🟣 Bearish ICT 2022 Model Setup

To identify a bearish setup in the ICT 2022 model, begin by marking the Previous Day High/Low or key session levels, such as the London or New York sessions. In this scenario, the price typically moves upward first, sweeping the Liquidity High. This move, known as a Liquidity Sweep, signifies the collection of sell orders by key market players.

After the liquidity sweep, the price should shift market structure downward. This movement, called the Market Structure Shift (MSS), indicates the start of a downtrend. Following MSS, areas such as FVG, found within the Premium Zone, are identified. At this stage, the trader waits for the price to retrace to these areas. Once the price revisits these zones, a short trade is executed.

In this setup, the stop-loss should be placed above the liquidity high to control risk, while the take-profit target is typically set below the previous day’s low or another defined liquidity level. This approach allows traders to capitalize on the downward price movement following the liquidity sweep.

🔵 Settings

Swing period : You can set the swing detection period.

Max Swing Back Method : It is in two modes "All" and "Custom". If it is in "All" mode, it will check all swings, and if it is in "Custom" mode, it will check the swings to the extent you determine.

Max Swing Back : You can set the number of swings that will go back for checking.

FVG Length : Default is 120 Bar.

MSS Length : Default is 80 Bar.

FVG Filter : This refines the number of identified FVG areas based on a specified algorithm to focus on higher quality signals and reduce noise.

Types of FVG filters :

Very Aggressive Filter: Adds a condition where, for an upward FVG, the last candle's highest price must exceed the middle candle's highest price, and for a downward FVG, the last candle's lowest price must be lower than the middle candle's lowest price. This minimally filters out FVGs.

Aggressive Filter: Builds on the Very Aggressive mode by ensuring the middle candle is not too small, filtering out more FVGs.

Defensive Filter: Adds criteria regarding the size and structure of the middle candle, requiring it to have a substantial body and specific polarity conditions, filtering out a significant number of FVGs.

Very Defensive Filter: Further refines filtering by ensuring the first and third candles are not small-bodied doji candles, retaining only the highest quality signals.

🔵 Conclusion

The ICT 2022 model is a comprehensive and advanced trading strategy designed around key concepts such as liquidity, price imbalance, and market structure shifts (MSS). By focusing on the sweep of critical levels such as the previous day’s high/low and important trading sessions like London and New York, this strategy enables traders to predict market movements with greater precision.

The use of tools like FVG in this model helps traders fine-tune their entry and exit points and take advantage of bullish and bearish trends after liquidity sweeps. Moreover, combining this strategy with precise timing during key trading sessions allows traders to minimize risk and maximize returns.

In conclusion, the ICT 2022 model emphasizes the importance of time and liquidity, making it a powerful tool for both professional and novice traders. By applying the principles of this model, you can make more informed trading decisions and seize opportunities in financial markets more effectively.

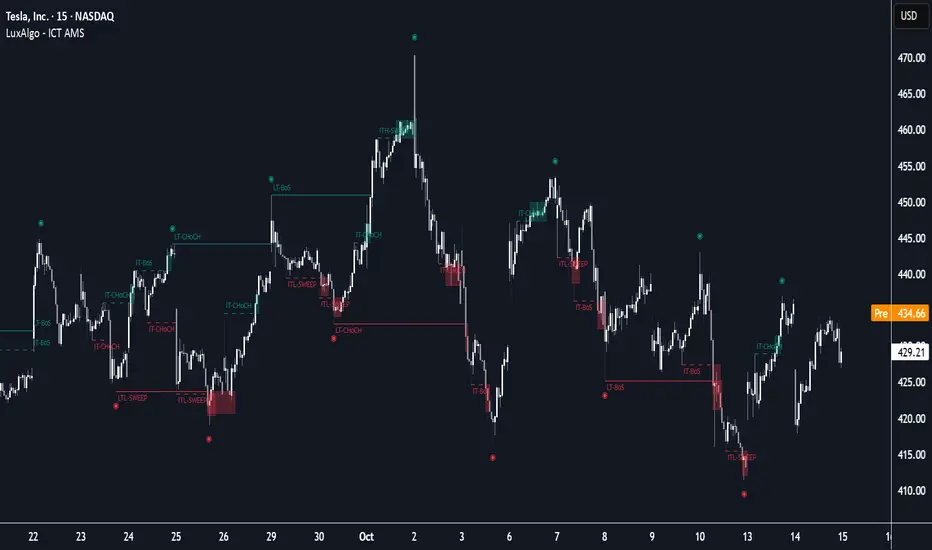

ICT Anchored Market Structures with Validation [LuxAlgo]The ICT Anchored Market Structures with Validation indicator is an advanced iteration of the original Pure-Price-Action-Structures tool, designed for price action traders.

It systematically tracks and validates key price action structures, distinguishing between true structural shifts/breaks and short-term sweeps to enhance trend and reversal analysis. The indicator automatically highlights structural points, confirms breakouts, identifies sweeps, and provides clear visual cues for short-term, intermediate-term, and long-term market structures.

A distinctive feature of this indicator is its exclusive reliance on price patterns. It does not depend on any user-defined input, ensuring that its analysis remains robust, objective, and uninfluenced by user bias, making it an effective tool for understanding market dynamics.

🔶 USAGE

Market structure is a cornerstone of price action analysis. This script automatically detects real-time market structures across short-term, intermediate-term, and long-term levels, simplifying trend analysis for traders. It assists in identifying both trend reversals and continuations with greater clarity.

Market structure shifts and breaks help traders identify changes in trend direction. A shift signals a potential reversal, often occurring when a swing high or low is breached, suggesting a transition in trend. A break, on the other hand, confirms the continuation of an established trend, reinforcing the current direction. Recognizing these shifts and breaks allows traders to anticipate price movement with greater accuracy.

It’s important to note that while a CHoCH may signal a potential trend reversal and a BoS suggests a continuation of the prevailing trend, neither guarantees a complete reversal or continuation. In some cases, CHoCH and BoS levels may act as liquidity zones or areas of consolidation rather than indicating a clear shift or continuation in market direction. The indicator’s validation component helps confirm whether the detected CHoCH and BoS are true breakouts or merely liquidity sweeps.

🔶 DETAILS

🔹 Market Structures

Market structures are derived from price action analysis, focusing on identifying key levels and patterns in the market. Swing point detection, a fundamental concept in ICT trading methodologies and teachings, plays a central role in this approach.

Swing points are automatically identified based exclusively on market movements, without requiring any user-defined input.

🔹 Utilizing Swing Points

Swing points are not identified in real-time as they form. Short-term swing points may appear with a delay of up to one bar, while the identification of intermediate and long-term swing points is entirely dependent on subsequent market movements. Importantly, this detection process is not influenced by any user-defined input, relying solely on pure price action. As a result, swing points are generally not intended for real-time trading scenarios.

Instead, traders often analyze historical swing points to understand market trends and identify potential entry and exit opportunities. By examining swing highs and lows, traders can:

Recognize Trends: Swing highs and lows provide insight into trend direction. Higher swing highs and higher swing lows signify an uptrend, while lower swing highs and lower swing lows indicate a downtrend.

Identify Support and Resistance Levels: Swing highs often act as resistance levels, referred to as Buyside Liquidity Levels in ICT terminology, while swing lows function as support levels, also known as Sellside Liquidity Levels. Traders can leverage these levels to plan their trade entries and exits.

Spot Reversal Patterns: Swing points can form key reversal patterns, such as double tops or bottoms, head and shoulders, and triangles. Recognizing these patterns can indicate potential trend reversals, enabling traders to adjust their strategies effectively.

Set Stop Loss and Take Profit Levels: In ICT teachings, swing levels represent price points with expected clusters of buy or sell orders. Traders can target these liquidity levels/pools for position accumulation or distribution, using swing points to define stop loss and take profit levels in their trades.

Overall, swing points provide valuable information about market dynamics and can assist traders in making more informed trading decisions.

🔹 Logic of Validation

The validation process in this script determines whether a detected market structure shift or break represents a confirmed breakout or a sweep.

The breakout is confirmed when the close price is significantly outside the deviation range of the last detected structural price. This deviation range is defined by the 17-period Average True Range (ATR), which creates a buffer around the detected market structure shift or break.

A sweep occurs when the price breaches the structural level within the deviation range but does not confirm a breakout. In this case, the label is updated to 'SWEEP.'

A visual box is created to represent the price range where the breakout or sweep occurs. If the validation process continues, the box is updated. This box visually highlights the price range involved in a sweep, helping traders identify liquidity events on the chart.

🔶 SETTINGS

The settings for Short-Term, Intermediate-Term, and Long-Term Structures are organized into groups, allowing users to customize swing points, market structures, and visual styles for each.

🔹 Structures

Swings and Size: Enables or disables the display of swing highs and lows, assigns icons to represent the structures, and adjusts the size of the icons.

Market Structures: Toggles the visibility of market structure lines.

Market Structure Validation: Enable or disable validation to distinguish true breakouts from liquidity sweeps.

Market Structure Labels: Displays or hides labels indicating the type of market structure.

Line Style and Width: Allows customization of the style and width of the lines representing market structures.

Swing and Line Colors: Provides options to adjust the colors of swing icons, market structure lines, and labels for better visualization.

🔶 RELATED SCRIPTS

Pure-Price-Action-Structures.

Market-Structures-(Intrabar).

Daytrade Forex Scalper TwinPulse Auction Timer IndicatorWhat this indicator is

TwinPulse Auction Timer is a multi component execution aid designed for liquid markets. It looks for two families of opportunities

Breakouts that leave a compression area after a fresh sweep

Reversals that trigger after a sweep with strong wick polarity

It does not try to predict future prices. It measures present auction conditions with transparent rules and shows you when those conditions align. You get a simple table that says LONG SHORT or WAIT, optional session shading, clean entry and exit level visuals, and alerts you can wire to your workflow.

Why it is different

Most tools show a single signal. TwinPulse combines several independent signals into an Edge Score that you can tune. The components are

• Pulse. A signed measure of wick asymmetry with candle body direction

• Compression. Current true range compared with an average range

• Sweep timer. Bars elapsed since the most recent sweep of a prior high or low

• Bias. Direction of a higher timeframe candle

• Regime. Efficiency ratio and the relation of micro to macro volatility

• Location. Distance from the daily anchored VWAP

• Session. London and New York filter by time windows

Each component is visible in the inputs and in the table so you can understand why a suggestion appears. The script uses request.security() with lookahead off in all calls so it does not peek into the future. Shapes may move while a bar is open since price is still forming. They stop moving when the bar closes.

What you will see on the chart

• L and S shapes on entry bars

• An Exit shape at the price where a stop or the runner target would have been hit

• Four horizontal lines while a trade is active

Entry

Stop

TP1 at one R

TP2 at the runner target expressed in R

• Labels anchored to each line so you can instantly read Entry SL TP1 and TP2 with current values

• Optional shading during your session windows

• Optional daily VWAP line

The table in the top right shows

Action LONG SHORT IN LONG IN SHORT or WAIT

Session ON or OFF

Bias UP DOWN or FLAT

Pulse value

Compression value

Edge L percent and Edge S percent

How it works in detail

Pulse

For each bar the script measures up wick minus down wick divided by range and multiplies that by the sign of the candle body. The result is averaged with pulse_len. Positive numbers indicate aggressive buying. Negative numbers indicate aggressive selling. You control the minimum absolute value with pulse_thr.

Compression

Compression is the ratio of current range to an average range. You can choose the range basis. HL SMA uses simple high minus low smoothed by range_len. ATR uses classic True Range smoothed by atr_len. Values below comp_thr indicate a coil.

Sweeps and the timer

A sweep occurs when price trades beyond the highest high or lowest low seen in the previous sweep_len bars. A strict sweep requires a close back inside that prior range. The timer measures how many bars have elapsed since the last sweep. Breakout setups require the timer to exceed timer_thr.

Bias on a confirmation timeframe

A higher timeframe candle is read with confirm_tf. If close is above open bias is UP. If close is below open bias is DOWN. This keeps breakouts aligned with the prevailing drift.

Regime filters

Efficiency ratio measures the straight line change over the sum of absolute bar to bar changes over er_len. It rises in trendy conditions and falls in noise. Minimum efficiency is controlled by er_min.

Micro to macro volatility ratio compares a short lookback average range with a longer lookback average range using your chosen basis. For breakouts you usually want micro volatility to be near or above macro hence mvr_min. For reversals you often want micro volatility that is not overheated relative to macro hence mvr_max_rev.

VWAP distance gate

Daily anchored VWAP is rebuilt from the open of each session. The script computes the absolute distance from VWAP in units of your average range and requires that distance to exceed vwap_dist_thr when use_vwap_gate is true. This keeps entries away from the mean.

Edge Score

Each gate contributes a weight that you control. The script sums weights of the satisfied gates and divides by the sum of all weights to produce an Edge percent for long and an Edge percent for short. You can then require a minimum Edge percent using edge_min_pct. This turns the indicator into a step by step checklist that you can tune to your taste.

Using the indicator step by step

Choose markets and timeframes

The logic is designed for liquid instruments. Major currency pairs, index futures and cash index CFDs, and the most liquid crypto pairs work well. On intraday use one to fifteen minutes for signals and fifteen to sixty minutes for confirmation. On swing use one hour to one day for signals and one day for confirmation.

Decide on entry mode

Breakouts require a compression area and a sweep timer. Reversals require a strict sweep and a strong pulse. If you are unsure leave the default which allows both.

Pick a range basis

For FX and crypto HL SMA is often stable. For indices and single name equities with gaps ATR can adapt better. If results look too reactive increase the window. If results are too slow reduce it.

Tune regime filters

If you trade trend continuation raise er_min and mvr_min. If you trade counter rotation lower them and rely on the reversal path with the strict sweep condition.

Set the VWAP gate

Enabling it helps you avoid entries at the mean. Push the threshold higher on range bound days. Reduce it in strong trend days.

Table driven decision

Watch Action and the Edge percents. If the script says WAIT you can read Pulse and Compression to see what is missing. Often the best trades appear when both Edge percents are well separated and your session switch is ON.

Use the visuals

When a suggestion triggers you will see entry stop and targets. You can mirror the levels in your own workflow or use alerts.

Consider bar close

Signals are computed in real time. For a strict process you can wait until the bar closes to reduce noise.

Inputs explained with quick guidance

Setup

Signal TF chooses where the logic is computed. Leave blank to use the chart.

Confirm TF sets the higher timeframe for bias.

Session filter restricts signals to the London and New York windows you specify.

Invert flips long and short. It is useful on inverse instruments.

Logic options

Entry mode allows Breakouts Reversals or Both.

Average range basis selects HL SMA or ATR.

ATR length is used when ATR is selected.

Pulse source can be Regular OHLC or Heikin Ashi. Heikin Ashi smooths noisy series, but the script still runs on regular bars and you should publish and use it on standard candles to respect the platform guidance.

Core numeric settings

Sweep lookback controls the size of the liquidity pool targeted by the sweep condition.

Pulse window smooths the wick polarity measure.

Average range window controls your base range when you use HL SMA.

Pulse threshold sets the minimum polarity required.

Compression threshold sets the maximum current range relative to average to consider the market coiled.

Expansion timer bars sets how much time has passed since the last sweep before you allow a breakout.

Regime filters

Efficiency ratio length and minimum value keep you out of aimless drift.

Micro and Macro range lengths feed the micro to macro ratio.

Minimum micro to macro for breakouts and maximum micro to macro for reversals steer the two entry families.

VWAP gate and distance threshold keep you away from the mean.

Levels and trade management visuals

Runner target in R sets TP2 as a multiple of initial risk.

Stop distance as average range multiple sets initial risk size for the visuals.

Move stop to entry after one R touch turns on break even logic once price has traveled one risk unit.

Trail buffer as R fraction uses the last sweep as an anchor and keeps a dynamic stop at a chosen fraction of R beyond it.

Cooldown after exit prevents immediate re entries.

Edge Score

Weights for pulse compression timer bias efficiency ratio micro to macro VWAP gate and session let you align the checklist with your style.

Minimum Edge percent to suggest applies a final filter to LONG or SHORT suggestions.

UI

Table and markers switch the compact dashboard and the shapes.

TP and SL lines and labels draw and name each level.

TP1 partial label percent is printed in the TP1 label for clarity.

Session shading helps with focus.

Daily VWAP line is optional.

Alerts

The script provides alerts for Long Short Exit and for Edge percent crossing the threshold on either side. Use them to drive notifications or to sync with webhooks and your broker integration. Alerts trigger in real time and will repaint during a bar. For conservative use trigger on bar close.

Recommended presets

Intraday trend continuation

Confirm TF fifteen minutes

Entry mode Breakouts

Range basis HL SMA

Pulse threshold near 0.10

Compression threshold near 0.60

Timer around 18

Minimum efficiency ratio near 0.20

Minimum micro to macro near 1.00

VWAP gate enabled with distance near 0.35

Edge minimum 50 or higher

Intraday mean reversion at sweeps

Entry mode Reversals

Pulse source Regular OHLC

Compression threshold can be a little higher

Maximum micro to macro near 1.60

Efficiency ratio minimum lower near 0.12

VWAP gate enabled

Edge minimum 40 to 60

Swing trend continuation

Signal TF one hour

Confirm TF one day

Range basis ATR

ATR length around 14

Average range window 20 to 30

Efficiency ratio minimum near 0.18

Micro to macro windows 12 and 60

Edge minimum 50 to 70

These are starting points only. Your instrument and timeframe will require small adjustments.

Limitations and honest warnings

No indicator is perfect. TwinPulse will mark attractive conditions that do not always lead to profitable trades. During economic releases or very thin liquidity the assumptions behind compression and sweeps may fail. In strong gap environments the HL SMA basis may lag while ATR may overreact. Heikin Ashi pulse can help in choppy markets but it will lag during sharp reversals. Session times use the exchange time of your chart. If you switch symbol or exchange verify the windows.

Edge percent is not a probability of profit. It is the fraction of satisfied gates with your chosen weights. Two traders can set different weights and see different Edge readings on the same bar. That is the design. The score is a guide that helps you act with discipline.

This indicator does not place orders or manage real risk. The lines and labels show a model entry a model stop and two model targets built from the average range at entry and from recent swing points. Use them as references and not as hard rules. Always test on historical data and demo first. Past results do not guarantee anything in the future.

Credits and originality

All code in this publication is original and written for this indicator. The concept of the efficiency ratio originates from Perry Kaufman. The use of a daily anchored volume weighted average price is a standard industry tool. The specific combination of pulse from wick polarity strict sweep timing compression and the tunable Edge Score is unique to this script at the time of publication. If you reuse parts of the open source code in your own work remember to credit the author and contribute meaningful improvements.

How to read the table at a glance

Action reflects your current state.

IN LONG or IN SHORT appears while a trade is active.

LONG or SHORT appears when conditions for entry are met and the Edge threshold is satisfied.

WAIT appears when at least one gate is missing.

Session shows ON during your chosen windows.

Bias shows the color of the confirmation candle.

Pulse is the smoothed polarity number.

Comp shows current range divided by the average range. Values below one mean compression.

Edge L percent and Edge S percent show the long and short checklists as percents.

Final thoughts

Markets move because orders accumulate at certain prices and at certain times. The indicator tries to measure two things that often matter at those turning points. One is the existence of a hidden imbalance revealed by wick polarity and by sweeps of prior extremes. The other is the presence of energy stored in a coil that can release in the direction of a drift. Neither force guarantees profit. Together they can improve your selection and your timing.