Superior-Range Bound Renko - Alerts - 11-29-25 - Signal LynxSuperior-Range Bound Renko – Alerts Edition with Advanced Risk Management Template

Signal Lynx | Free Scripts supporting Automation for the Night-Shift Nation 🌙

1. Overview

This is the Alerts & Indicator Edition of Superior-Range Bound Renko (RBR).

The Strategy version is built for backtesting inside TradingView.

This Alerts version is built for automation: it emits clean, discrete alert events that you can route into webhooks, bots, or relay engines (including your own Signal Lynx-style infrastructure).

Under the hood, this script contains the same core engine as the strategy:

Adaptive Range Bounding based on volatility

Renko Brick Emulation on standard candles

A stack of Laguerre Filters for impulse detection

K-Means-style Adaptive SuperTrend for trend confirmation

The full Signal Lynx Risk Management Engine (state machine, layered exits, AATS, RSIS, etc.)

The difference is in what we output:

Instead of placing historical trades, this version:

Plots the entry and RM signals in a separate pane (overlay = false)

Exposes alertconditions for:

Long Entry

Short Entry

Close Long

Close Short

TP1, TP2, TP3 hits (Staged Take Profit)

This makes it ideal as the signal source for automated execution via TradingView Alerts + Webhooks.

2. Quick Action Guide (TL;DR)

Best Timeframe:

4H and above. This is a swing-trading / position-trading style engine, not a micro-scalper.

Best Assets:

Volatile but structured markets, e.g.:

BTC, ETH, XAUUSD (Gold), GBPJPY, and similar high-volatility majors or indices.

Script Type:

indicator() – Alerts & Visualization Only

No built-in order placement

All “orders” are emitted as alerts for your external bot or manual handling

Strategy Type:

Volatility-Adaptive Trend Following + Impulse Detection

using Renko-like structure and multi-layer Laguerre filters.

Repainting:

Designed to be non-repainting on closed candles.

The underlying Risk Management engine is built around previous-bar data (close , high , low ) for execution-critical logic.

Intrabar values can move while the bar is forming (normal for any advanced signal), but once a bar closes, the alert logic is stable.

Recommended Alert Settings:

Condition: one of the built-in signals (see section 3.B)

Options: “Once Per Bar Close” is strongly recommended for automation

Message: JSON, CSV, or simple tokens – whatever your webhook / relay expects

3. Detailed Report: How the Alerts Edition Works

A. Relationship to the Strategy Version

The Alerts Edition shares the same internal logic as the strategy version:

Same Adaptive Lookback and volatility normalization

Same Range and Close Range construction

Same Renko Brick Emulator and directional memory (renkoDir)

Same Fib structures, Laguerre stack, K-Means SuperTrend, and Baseline signals (B1, B2)

Same Risk Management Engine and layered exits

In the strategy script, these signals are wired into strategy.entry, strategy.exit, and strategy.close.

In the alerts script:

We still compute the final entry/exit signals (Fin, CloseEmAll, TakeProfit1Plot, etc.)

Instead of placing trades, we:

Plot them for visual inspection

Expose them via alertcondition(...) so that TradingView can fire alerts.

This ensures that:

If you use the same settings on the same symbol/timeframe, the Alerts Edition and Strategy Edition agree on where entries and exits occur.

(Subject only to normal intrabar vs. bar-close differences.)

B. Signals & Alert Conditions

The alerts script focuses on discrete, automation-friendly events.

Internally, the main signals are:

Fin – Final entry decision from the RM engine

CloseEmAll – RM-driven “hard close” signal (for full-position exits)

TakeProfit1Plot / 2Plot / 3Plot – One-time event markers when each TP stage is hit

On the chart (in the separate indicator pane), you get:

plot(Fin) – where:

+2 = Long Entry event

-2 = Short Entry event

plot(CloseEmAll) – where:

+1 = “Close Long” event

-1 = “Close Short” event

plot(TP1/TP2/TP3) (if Staged TP is enabled) – integer tags for TP hits:

+1 / +2 / +3 = TP1 / TP2 / TP3 for Longs

-1 / -2 / -3 = TP1 / TP2 / TP3 for Shorts

The corresponding alertconditions are:

Long Entry

alertcondition(Fin == 2, title="Long Entry", message="Long Entry Triggered")

Fire this to open/scale a long position in your bot.

Short Entry

alertcondition(Fin == -2, title="Short Entry", message="Short Entry Triggered")

Fire this to open/scale a short position.

Close Long

alertcondition(CloseEmAll == 1, title="Close Long", message="Close Long Triggered")

Fire this to fully exit a long position.

Close Short

alertcondition(CloseEmAll == -1, title="Close Short", message="Close Short Triggered")

Fire this to fully exit a short position.

TP 1 Hit

alertcondition(TakeProfit1Plot != 0, title="TP 1 Hit", message="TP 1 Level Reached")

First staged take profit hit (either long or short). Your bot can interpret the direction based on position state or message tags.

TP 2 Hit

alertcondition(TakeProfit2Plot != 0, title="TP 2 Hit", message="TP 2 Level Reached")

TP 3 Hit

alertcondition(TakeProfit3Plot != 0, title="TP 3 Hit", message="TP 3 Level Reached")

Together, these give you a complete trade lifecycle:

Open Long / Short

Optionally scale out via TP1/TP2/TP3

Close remaining via Close Long / Close Short

All while the Risk Management Engine enforces the same logic as the strategy version.

C. Using This Script for Automation

This Alerts Edition is designed for:

Webhook-based bots

Execution relays (e.g., your own Lynx-Relay-style engine)

Dedicated external trade managers

Typical setup flow:

Add the script to your chart

Same symbol, timeframe, and settings you use in the Strategy Edition backtests.

Configure Inputs:

Longs / Shorts enabled

Risk Management toggles (SL, TS, Staged TP, AATS, RSIS)

Weekend filter (if you do not want weekend trades)

RBR-specific knobs (Adaptive Lookback, Brick type, ATR vs Standard Brick, etc.)

Create Alerts for Each Event Type You Need:

Long Entry

Short Entry

Close Long

Close Short

TP1 / TP2 / TP3 (optional, if your bot handles partial closes)

For each:

Condition: the corresponding alertcondition

Option: “Once Per Bar Close” is strongly recommended

Message:

You can use structured JSON or a simple token set like:

{"side":"long","event":"entry","symbol":"{{ticker}}","time":"{{timenow}}"}

or a simpler text for manual trading like:

LONG ENTRY | {{ticker}} | {{interval}}

Wire Up Your Bot / Relay:

Point TradingView’s webhook URL to your execution engine

Parse the messages and map them into:

Exchange

Symbol

Side (long/short)

Action (open/close/partial)

Size and risk model (this script does not position-size for you; it only signals when, not how much.)

Because the alerts come from a non-repainting, RM-backed engine that you’ve already validated via the Strategy Edition, you get a much cleaner automation pipeline.

D. Repainting Protection (Alerts Edition)

The same protections as the Strategy Edition apply here:

Execution-critical logic (trailing stop, TP triggers, SL, RM state changes) uses previous bar OHLC:

open , high , low , close

No security() with lookahead or future-bar dependencies.

This means:

Alerts are designed to fire on states that would have been visible at bar close, not on hypothetical “future history.”

Important practical note:

Intrabar: While a bar is forming, internal conditions can oscillate.

Bar Close: With “Once Per Bar Close” alerts, the fired signal corresponds to the final state of the engine for that candle, matching your Strategy Edition expectations.

4. For Developers & Modders

You can treat this Alerts script as an ”RM + Alert Framework” and inject any signal logic you want.

Where to plug in:

Find the section:

// BASELINE & SIGNAL GENERATION

You’ll see how B1 and B2 are built from the RBR stack and then combined:

baseSig = B2

altSig = B1

finalSig = sigSwap ? baseSig : altSig

To use your own logic:

Replace or wrap the code that sets baseSig / altSig with your own conditions:

e.g., RSI, MACD, Heikin Ashi filters, candle patterns, volume filters, etc.

Make sure your final decision is still:

2 → Long / Buy signal

-2 → Short / Sell signal

0 → No trade

finalSig is then passed into the RM engine and eventually becomes Fin, which:

Drives the Long/Short Entry alerts

Interacts with the RM state machine to integrate properly with AATS, SL, TS, TP, etc.

Because this script already exposes alertconditions for key lifecycle events, you don’t need to re-wire alerts each time — just ensure your logic feeds into finalSig correctly.

This lets you use the Signal Lynx Risk Management Engine + Alerts wrapper as a drop-in chassis for your own strategies.

5. About Signal Lynx

Automation for the Night-Shift Nation 🌙

Signal Lynx builds tools and templates that help traders move from:

“I have an indicator” → “I have a structured, automatable strategy with real risk management.”

This Superior-Range Bound Renko – Alerts Edition is the automation-focused companion to the Strategy Edition. It’s designed for:

Traders who backtest with the Strategy version

Then deploy live signals with this Alerts version via webhooks or bots

While relying on the same non-repainting, RM-driven logic

We release this code under the Mozilla Public License 2.0 (MPL-2.0) to support the Pine community with:

Transparent, inspectable logic

A reusable Risk Management template

A reference implementation of advanced adaptive logic + alerts

If you are exploring full-stack automation (TradingView → Webhooks → Exchange / VPS), keep Signal Lynx in your search.

License: Mozilla Public License 2.0 (Open Source).

If you build improvements or helpful variants, please consider sharing them back with the community.

在脚本中搜索"tradingview+筹码结构"

Etherium CME gaps multi-timeframe auto finderThis indicator is a powerful tool that automatically detects and visualizes price gaps (Gaps) in the Ethereum CME futures market across multiple timeframes and also provides alert functionality. Price gaps occur when the futures market is inactive for a certain period, often acting as potential support or resistance zones.

What is an Ethereum CME Gap?

CME (Chicago Mercantile Exchange) is one of the largest derivatives exchanges globally. The Ethereum CME futures market is closed on weekends and certain holidays. When the market reopens, a price difference may occur between the previous closing price and the new opening price, referred to as a "CME Gap."

Key Features of the Indicator

Multi-timeframe gap detection: Detects and displays gaps across 5m, 15m, 30m, 1h, 4h, 1d timeframes simultaneously.

Customizable CME Symbol: You can specify Ethereum CME futures symbols, such as ETH1!.

Two gap price display methods:

CME_price: Displays the gap based on the actual price levels in the CME futures market.

Chart_price: Adjusts the gap to match the price levels on the chart being viewed (e.g., spot market). This helps visualize the impact of futures gaps on the spot market.

Visual customization:

Individual color settings for bullish/bearish gap boxes for each timeframe.

Adjust the extension (display length) of gap boxes in bars.

Configure label display, position, text size, background, and text color.

Highlight significant gaps: Emphasize gaps above a specified percentage with a unique color and border thickness.

Alert functionality: Receive notifications when a gap is detected, with options to enable alerts only for specific timeframes.

Why CME Gaps Matter

Traders often consider CME gaps as significant price zones.

Gap Fill: Historical data shows that many gaps tend to get "filled" over time, meaning the price returns to the gap area, reaching the start or end point of the gap.

Support/Resistance: Unfilled gaps can serve as potential support (Bullish Gap) or resistance (Bearish Gap) zones.

Bullish Gap: Occurs when the current opening price is higher than the previous closing price. Typically leaves an unfilled gap below (previous high), which can act as potential support.

Bearish Gap: Occurs when the current opening price is lower than the previous closing price. Typically leaves an unfilled gap above (previous low), which can act as potential resistance.

How to Use the Indicator

Add Indicator on TradingView: Click the "Indicators" button on the TradingView chart.

Find the indicator in "My Scripts" or "Invite-Only Scripts" and add it to the chart.

Adjust Settings: Once the indicator is added, click the settings (gear) icon to adjust inputs.

CME Symbol (ETH): ETH1! is typically the default symbol for Ethereum CME futures. Confirm based on your broker or data feed.

Min gap %: Set the minimum gap size in percentage; smaller gaps will not be displayed.

Select Exchanges to Display gap price: Choose between "CME_price" or "Chart_price." For viewing futures gaps on a spot chart, "Chart_price" is recommended.

Show Xm/h/d gap boxes: Select which timeframe gap boxes to display.

Color, Extension, Label settings: Customize the visual aspects of gap boxes and labels.

Highlight gap % (>=): Set the minimum percentage for highlighting significant gaps.

Enable Alerts: Choose whether to receive alerts when a gap is detected.

Alert Timeframe: Select whether alerts apply to all timeframes or specific ones only.

Chart Analysis

Once the indicator is applied, gap boxes for the selected timeframes appear on the chart.

Green shades indicate Bullish Gaps, and red shades indicate Bearish Gaps (default green can be customized, and bearish gap color can be set separately).

Highlighted gaps may carry higher significance and should be monitored carefully.

Potential trading opportunities can be explored when the price approaches or attempts to fill a gap.

Usage Strategies (Examples)

Support/Resistance Confirmation: The lower boundary of a bullish gap can act as potential support, while the upper boundary of a bearish gap can act as potential resistance. Observe for reversals or breakouts when price reaches these areas.

Retracement Trading: Trade when the price returns to fill a gap after leaving it through a sharp move up or down.

Multi-timeframe Analysis: Gaps overlapping across multiple timeframes can form stronger support/resistance zones.

Considerations

* "Gap Filled" Condition: The indicator does not draw a gap if it determines that the gap has already been filled by the current bar’s low (bullish gap) or high (bearish gap).

* Tool Only: This indicator is a gap detection tool and should not be used alone for trading decisions. Always combine with other technical analysis tools and your trading strategy.

* Past Data ≠ Future Guarantee: Historical gap fill trends do not guarantee future occurrences.

This indicator allows effective tracking of Ethereum CME futures gaps and provides valuable insights for enhancing your trading strategy.

Range Oscillator Strategy + Stoch Confirm🔹 Short summary

This is a free, educational long-only strategy built on top of the public “Range Oscillator” by Zeiierman (used under CC BY-NC-SA 4.0), combined with a Stochastic timing filter, an EMA-based exit filter and an optional risk-management layer (SL/TP and R-multiple exits). It is NOT financial advice and it is NOT a magic money machine. It’s a structured framework to study how range-expansion + momentum + trend slope can be combined into one rule-based system, often with intentionally RARE trades.

────────────────────────

0. Legal / risk disclaimer

────────────────────────

• This script is FREE and public. I do not charge any fee for it.

• It is for EDUCATIONAL PURPOSES ONLY.

• It is NOT financial advice and does NOT guarantee profits.

• Backtest results can be very different from live results.

• Markets change over time; past performance is NOT indicative of future performance.

• You are fully responsible for your own trades and risk.

Please DO NOT use this script with money you cannot afford to lose. Always start in a demo / paper trading environment and make sure you understand what the logic does before you risk any capital.

────────────────────────

1. About default settings and risk (very important)

────────────────────────

The script is configured with the following defaults in the `strategy()` declaration:

• `initial_capital = 10000`

→ This is only an EXAMPLE account size.

• `default_qty_type = strategy.percent_of_equity`

• `default_qty_value = 100`

→ This means 100% of equity per trade in the default properties.

→ This is AGGRESSIVE and should be treated as a STRESS TEST of the logic, not as a realistic way to trade.

TradingView’s House Rules recommend risking only a small part of equity per trade (often 1–2%, max 5–10% in most cases). To align with these recommendations and to get more realistic backtest results, I STRONGLY RECOMMEND you to:

1. Open **Strategy Settings → Properties**.

2. Set:

• Order size: **Percent of equity**

• Order size (percent): e.g. **1–2%** per trade

3. Make sure **commission** and **slippage** match your own broker conditions.

• By default this script uses `commission_value = 0.1` (0.1%) and `slippage = 3`, which are reasonable example values for many crypto markets.

If you choose to run the strategy with 100% of equity per trade, please treat it ONLY as a stress-test of the logic. It is NOT a sustainable risk model for live trading.

────────────────────────

2. What this strategy tries to do (conceptual overview)

────────────────────────

This is a LONG-ONLY strategy designed to explore the combination of:

1. **Range Oscillator (Zeiierman-based)**

- Measures how far price has moved away from an adaptive mean.

- Uses an ATR-based range to normalize deviation.

- High positive oscillator values indicate strong price expansion away from the mean in a bullish direction.

2. **Stochastic as a timing filter**

- A classic Stochastic (%K and %D) is used.

- The logic requires %K to be below a user-defined level and then crossing above %D.

- This is intended to catch moments when momentum turns up again, rather than chasing every extreme.

3. **EMA Exit Filter (trend slope)**

- An EMA with configurable length (default 70) is calculated.

- The slope of the EMA is monitored: when the slope turns negative while in a long position, and the filter is enabled, it triggers an exit condition.

- This acts as a trend-protection exit: if the medium-term trend starts to weaken, the strategy exits even if the oscillator has not yet fully reverted.

4. **Optional risk-management layer**

- Percentage-based Stop Loss and Take Profit (SL/TP).

- Risk/Reward (R-multiple) exit based on the distance from entry to SL.

- Implemented as OCO orders that work *on top* of the logical exits.

The goal is not to create a “holy grail” system but to serve as a transparent, configurable framework for studying how these concepts behave together on different markets and timeframes.

────────────────────────

3. Components and how they work together

────────────────────────

(1) Range Oscillator (based on “Range Oscillator (Zeiierman)”)

• The script computes a weighted mean price and then measures how far price deviates from that mean.

• Deviation is normalized by an ATR-based range and expressed as an oscillator.

• When the oscillator is above the **entry threshold** (default 100), it signals a strong move away from the mean in the bullish direction.

• When it later drops below the **exit threshold** (default 30), it can trigger an exit (if enabled).

(2) Stochastic confirmation

• Classic Stochastic (%K and %D) is calculated.

• An entry requires:

- %K to be below a user-defined “Cross Level”, and

- then %K to cross above %D.

• This is a momentum confirmation: the strategy tries to enter when momentum turns up from a pullback rather than at any random point.

(3) EMA Exit Filter

• The EMA length is configurable via `emaLength` (default 70).

• The script monitors the EMA slope: it computes the relative change between the current EMA and the previous EMA.

• If the slope turns negative while the strategy holds a long position and the filter is enabled, it triggers an exit condition.

• This is meant to help protect profits or cut losses when the medium-term trend starts to roll over, even if the oscillator conditions are not (yet) signalling exit.

(4) Risk management (optional)

• Stop Loss (SL) and Take Profit (TP):

- Defined as percentages relative to average entry price.

- Both are disabled by default, but you can enable them in the Inputs.

• Risk/Reward Exit:

- Uses the distance from entry to SL to project a profit target at a configurable R-multiple.

- Also optional and disabled by default.

These exits are implemented as `strategy.exit()` OCO orders and can close trades independently of oscillator/EMA conditions if hit first.

────────────────────────

4. Entry & Exit logic (high level)

────────────────────────

A) Time filter

• You can choose a **Start Year** in the Inputs.

• Only candles between the selected start date and 31 Dec 2069 are used for backtesting (`timeCondition`).

• This prevents accidental use of tiny cherry-picked windows and makes tests more honest.

B) Entry condition (long-only)

A long entry is allowed when ALL the following are true:

1. `timeCondition` is true (inside the backtest window).

2. If `useOscEntry` is true:

- Range Oscillator value must be above `entryLevel`.

3. If `useStochEntry` is true:

- Stochastic condition (`stochCondition`) must be true:

- %K < `crossLevel`, then %K crosses above %D.

If these filters agree, the strategy calls `strategy.entry("Long", strategy.long)`.

C) Exit condition (logical exits)

A position can be closed when:

1. `timeCondition` is true AND a long position is open, AND

2. At least one of the following is true:

- If `useOscExit` is true: Oscillator is below `exitLevel`.

- If `useMagicExit` (EMA Exit Filter) is true: EMA slope is negative (`isDown = true`).

In that case, `strategy.close("Long")` is called.

D) Risk-management exits

While a position is open:

• If SL or TP is enabled:

- `strategy.exit("Long Risk", ...)` places an OCO stop/limit order based on the SL/TP percentages.

• If Risk/Reward exit is enabled:

- `strategy.exit("RR Exit", ...)` places an OCO order using a projected R-multiple (`rrMult`) of the SL distance.

These risk-based exits can trigger before the logical oscillator/EMA exits if price hits those levels.

────────────────────────

5. Recommended backtest configuration (to avoid misleading results)

────────────────────────

To align with TradingView House Rules and avoid misleading backtests:

1. **Initial capital**

- 10 000 (or any value you personally want to work with).

2. **Order size**

- Type: **Percent of equity**

- Size: **1–2%** per trade is a reasonable starting point.

- Avoid risking more than 5–10% per trade if you want results that could be sustainable in practice.

3. **Commission & slippage**

- Commission: around 0.1% if that matches your broker.

- Slippage: a few ticks (e.g. 3) to account for real fills.

4. **Timeframe & markets**

- Volatile symbols (e.g. crypto like BTCUSDT, or major indices).

- Timeframes: 1H / 4H / **1D (Daily)** are typical starting points.

- I strongly recommend trying the strategy on **different timeframes**, for example 1D, to see how the behaviour changes between intraday and higher timeframes.

5. **No “caution warning”**

- Make sure your chosen symbol + timeframe + settings do not trigger TradingView’s caution messages.

- If you see warnings (e.g. “too few trades”), adjust timeframe/symbol or the backtest period.

────────────────────────

5a. About low trade count and rare signals

────────────────────────

This strategy is intentionally designed to trade RARELY:

• It is **long-only**.

• It uses strict filters (Range Oscillator threshold + Stochastic confirmation + optional EMA Exit Filter).

• On higher timeframes (especially **1D / Daily**) this can result in a **low total number of trades**, sometimes WELL BELOW 100 trades over the whole backtest.

TradingView’s House Rules mention 100+ trades as a guideline for more robust statistics. In this specific case:

• The **low trade count is a conscious design choice**, not an attempt to cherry-pick a tiny, ultra-profitable window.

• The goal is to study a **small number of high-conviction long entries** on higher timeframes, not to generate frequent intraday signals.

• Because of the low trade count, results should NOT be interpreted as statistically strong or “proven” – they are only one sample of how this logic would have behaved on past data.

Please keep this in mind when you look at the equity curve and performance metrics. A beautiful curve with only a handful of trades is still just a small sample.

────────────────────────

6. How to use this strategy (step-by-step)

────────────────────────

1. Add the script to your chart.

2. Open the **Inputs** tab:

- Set the backtest start year.

- Decide whether to use Oscillator-based entry/exit, Stochastic confirmation, and EMA Exit Filter.

- Optionally enable SL, TP, and Risk/Reward exits.

3. Open the **Properties** tab:

- Set a realistic account size if you want.

- Set order size to a realistic % of equity (e.g. 1–2%).

- Confirm that commission and slippage are realistic for your broker.

4. Run the backtest:

- Look at Net Profit, Max Drawdown, number of trades, and equity curve.

- Remember that a low trade count means the statistics are not very strong.

5. Experiment:

- Tweak thresholds (`entryLevel`, `exitLevel`), Stochastic settings, EMA length, and risk params.

- See how the metrics and trade frequency change.

6. Forward-test:

- Before using any idea in live trading, forward-test on a demo account and observe behaviour in real time.

────────────────────────

7. Originality and usefulness (why this is more than a mashup)

────────────────────────

This script is not intended to be a random visual mashup of indicators. It is designed as a coherent, testable strategy with clear roles for each component:

• Range Oscillator:

- Handles mean vs. range-expansion states via an adaptive, ATR-normalized metric.

• Stochastic:

- Acts as a timing filter to avoid entering purely on extremes and instead waits for momentum to turn.

• EMA Exit Filter:

- Trend-slope-based safety net to exit when the medium-term direction changes against the position.

• Risk module:

- Provides practical, rule-based exits: SL, TP, and R-multiple exit, which are useful for structuring risk even if you modify the core logic.

It aims to give traders a ready-made **framework to study and modify**, not a black box or “signals” product.

────────────────────────

8. Limitations and good practices

────────────────────────

• No single strategy works on all markets or in all regimes.

• This script is long-only; it does not short the market.

• Performance can degrade when market structure changes.

• Overfitting (curve fitting) is a real risk if you endlessly tweak parameters to maximise historical profit.

Good practices:

- Test on multiple symbols and timeframes.

- Focus on stability and drawdown, not only on how high the profit line goes.

- View this as a learning tool and a basis for your own research.

────────────────────────

9. Licensing and credits

────────────────────────

• Core oscillator idea & base code:

- “Range Oscillator (Zeiierman)”

- © Zeiierman, licensed under CC BY-NC-SA 4.0.

• Strategy logic, Stochastic confirmation, EMA Exit Filter, and risk-management layer:

- Modifications by jokiniemi.

Please respect both the original license and TradingView House Rules if you fork or republish any part of this script.

────────────────────────

10. No payments / no vendor pitch

────────────────────────

• This script is completely FREE to use on TradingView.

• There is no paid subscription, no external payment link, and no private signals group attached to it.

• If you have questions, please use TradingView’s comment system or private messages instead of expecting financial advice.

Use this script as a tool to learn, experiment, and build your own understanding of markets.

────────────────────────

11. Example backtest settings used in screenshots

────────────────────────

To avoid any confusion about how the results shown in screenshots were produced, here is one concrete example configuration:

• Symbol: BTCUSDT (or similar major BTC pair)

• Timeframe: 1D (Daily)

• Backtest period: from 2018 to the most recent data

• Initial capital: 10 000

• Order size type: Percent of equity

• Order size: 2% per trade

• Commission: 0.1%

• Slippage: 3 ticks

• Risk settings: Stop Loss and Take Profit disabled by default, Risk/Reward exit disabled by default

• Filters: Range Oscillator entry/exit enabled, Stochastic confirmation enabled, EMA Exit Filter enabled

If you change any of these settings (symbol, timeframe, risk per trade, commission, slippage, filters, etc.), your results will look different. Please always adapt the configuration to your own risk tolerance, market, and trading style.

MTF EMA Trading SystemHere's a comprehensive description and usage guide for publishing your MTF EMA Trading System indicator on TradingView:

MTF EMA Trading System - Pro Edition

📊 Indicator Overview

The MTF EMA Trading System is an advanced multi-timeframe exponential moving average indicator designed for traders seeking high-probability setups with multiple confirmations. Unlike simple EMA crossover systems, this indicator combines trend alignment, momentum, volume analysis, and previous day confluence to generate reliable long and short signals with optimal risk-reward ratios.

✨ Key Features

1. Multi-Timeframe EMA Analysis

Configure 5 independent EMAs (default: 9, 21, 50, 100, 200)

Each EMA can pull data from ANY timeframe (5m, 15m, 1H, 4H, 1D, etc.)

Color-coded lines with customizable widths

End-of-line labels showing EMA period and timeframe (e.g., "EMA200 ")

Perfect for analyzing higher timeframe trends on lower timeframe charts

2. Advanced Signal Generation (Beyond Simple Crosses)

The system requires MULTIPLE confirmations before generating a signal:

LONG Signals Require:

✅ Price action trigger (EMA cross, bounce from key EMA, or pullback setup)

✅ Bullish EMA alignment (EMAs in proper ascending order)

✅ Volume spike confirmation (configurable threshold)

✅ RSI momentum confirmation (bullish but not overbought)

✅ Sufficient EMA separation (avoids choppy/whipsaw conditions)

✅ Price above previous day's low (confluence with support)

SHORT Signals Require:

✅ Price action trigger (EMA cross, rejection from key EMA, or pullback setup)

✅ Bearish EMA alignment (EMAs in proper descending order)

✅ Volume spike confirmation

✅ RSI momentum confirmation (bearish but not oversold)

✅ Sufficient EMA separation

✅ Price below previous day's high (confluence with resistance)

3. Real-Time Dashboard

Displays critical market conditions at a glance:

Overall trend direction (Bullish/Bearish/Neutral)

Price position relative to all EMAs

Volume status (spike or normal)

RSI momentum reading

EMA confluence strength

EMA separation quality

Current ATR value

Previous day high/low levels

Current signal status (LONG/SHORT/WAIT)

Risk-reward ratio

4. Clean Visual Design

Large, clear trade signal markers (green triangles for LONG, red triangles for SHORT)

No chart clutter - only essential information displayed

Customizable signal sizes

Professional color-coded dashboard

5. Built-In Risk Management

ATR-based calculations for stop loss placement

1:2 risk-reward ratio by default

All levels displayed in dashboard for easy reference

🎯 How to Use This Indicator

Step 1: Initial Setup

Add the indicator to your TradingView chart

Configure your preferred timeframes for each EMA:

EMA 9: Leave blank (uses chart timeframe) - Fast reaction to price

EMA 21: Leave blank or set to 15m - Key pivot level

EMA 50: Set to 1H - Intermediate trend

EMA 100: Set to 4H - Major trend filter

EMA 200: Set to 1D - Overall market bias

Adjust signal settings based on your trading style:

Conservative: Keep all confirmations enabled

Aggressive: Disable volume or momentum requirements

Scalping: Reduce min EMA separation to 0.2-0.3%

Step 2: Reading the Dashboard

Before taking any trade, check the dashboard:

Trend: Only take LONG signals in bullish trends, SHORT signals in bearish trends

Position: Confirm price is on the correct side of EMAs

Volume: Green spike = strong confirmation

RSI: Avoid extremes (>70 or <30)

Confluence: "Strong" = high probability setup

Separation: "Good" = trending market, avoid "Low" separation

Step 3: Trade Entry

For LONG Trades:

Wait for green triangle to appear below price

Verify dashboard shows:

Bullish or Neutral trend

Volume spike (preferred)

RSI between 50-70

Good separation

Enter at market or on next bar

Set stop loss at: Entry - (ATR × 2)

Set target at: Entry + (ATR × 4)

For SHORT Trades:

Wait for red triangle to appear above price

Verify dashboard shows:

Bearish or Neutral trend

Volume spike (preferred)

RSI between 30-50

Good separation

Enter at market or on next bar

Set stop loss at: Entry + (ATR × 2)

Set target at: Entry - (ATR × 4)

Step 4: Trade Management

Use the ATR values from dashboard for position sizing

Trail stops using the fastest EMA (EMA 9) as price moves in your favor

Exit partial position at 1:1 risk-reward, let remainder run to target

Exit immediately if dashboard trend changes against your position

💡 Best Practices

Timeframe Recommendations:

Scalping: 1m-5m chart with 5m, 15m, 1H, 4H, 1D EMAs

Day Trading: 5m-15m chart with 15m, 1H, 4H, 1D EMAs

Swing Trading: 1H-4H chart with 4H, 1D, 1W EMAs

Position Trading: 1D chart with 1D, 1W, 1M EMAs

Market Conditions:

Best in: Trending markets with clear direction

Avoid: Tight consolidation, low volume periods, major news events

Filter trades: Only take signals aligned with higher timeframe trend

Risk Management:

Never risk more than 1-2% per trade

Use ATR from dashboard to calculate position size

Respect the stop loss levels

Don't force trades when dashboard shows weak conditions

⚙️ Customization Options

EMA Settings (for each of 5 EMAs):

Length (period)

Timeframe (multi-timeframe capability)

Color

Line width

Show/hide toggle

Signal Settings:

Volume confirmation (on/off)

Volume spike threshold (1.0-3.0x)

Momentum confirmation (on/off)

RSI overbought/oversold levels

Minimum EMA separation percentage

ATR period and stop multiplier

Display Settings:

Show/hide EMA labels

Show/hide trade signals

Signal marker size (tiny/small/normal/large)

Show/hide dashboard

🔔 Alert Setup

The indicator includes 4 alert conditions:

LONG Signal - Fires when all long confirmations are met

SHORT Signal - Fires when all short confirmations are met

Bullish Setup - Early warning when trend aligns bullish with volume

Bearish Setup - Early warning when trend aligns bearish with volume

To set up alerts:

Right-click on chart → Add Alert

Select "MTF EMA Trading System"

Choose your desired alert condition

Configure notification method (popup, email, SMS, webhook)

📈 Performance Tips

Increase Win Rate:

Only trade in direction of higher timeframe trend

Wait for volume spike confirmation

Avoid trades during first 30 minutes and last 15 minutes of session

Skip trades when separation is "Low"

Reduce False Signals:

Increase minimum EMA separation to 0.7-1.0%

Enable all confirmation requirements

Only trade when confluence shows "Strong"

Combine with support/resistance levels

Optimize for Your Market:

Stocks: Use 9, 21, 50, 100, 200 EMAs

Forex: Consider 8, 13, 21, 55, 89 EMAs (Fibonacci)

Crypto: May need wider ATR multiplier (2.5-3.0x) for volatility

⚠️ Important Notes

This indicator is designed to reduce false signals by requiring multiple confirmations

No indicator is 100% accurate - always use proper risk management

Backtesting recommended before live trading

Market conditions change - adjust settings as needed

Works best in liquid markets with clear price action

🎓 Conclusion

The MTF EMA Trading System transforms simple moving average analysis into a sophisticated, multi-confirmation trading strategy. By combining trend alignment, momentum, volume, and confluence, it helps traders identify high-probability setups while filtering out noise and false signals. The clean interface and comprehensive dashboard make it suitable for both beginners and experienced traders across all markets and timeframes.

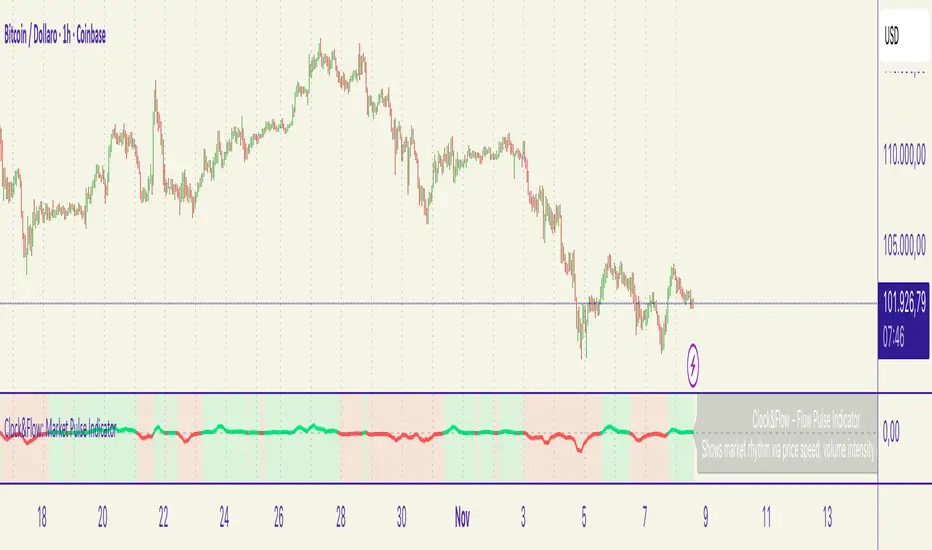

Clock&Flow – Market Pulse IndicatorClock&Flow – Market Pulse Indicator

1) General Purpose

The Market Pulse Indicator is designed to visualize the strength and direction of market flow in a clear, intuitive way.

Unlike common volume or momentum indicators, it blends three essential dimensions — price velocity, normalized volume, and volatility (ATR) — to highlight when market pressure is truly meaningful.

It helps identify genuine liquidity inflows/outflows, potential exhaustion zones, and moments of compression or expansion within the price structure.

2) Data Sources

All data is directly taken from the current chart’s feed on TradingView:

Price (close): to measure relative price change.

Volume: to detect the intensity of market participation (normalized to average).

ATR (Average True Range): to evaluate volatility relative to price levels.

No external data or off-platform sources are used.

3) Logic and Calculation Steps

Price Velocity: calculates the percentage change between the current close and the close N bars ago.

priceChange = (close - close ) / close

Normalized Volume: compares current volume to its moving average over the same period.

volNorm = volume / sma(volume, length)

Normalized Volatility: ATR divided by price to adjust for instrument scale.

atrNorm = atr(length) / close

Combination : multiplies the three components into one raw value that represents market pulse intensity.

rawPulse = priceChange * volNorm * (1 + atrNorm)

Smoothing: a moving average (smoothLen) is applied to create a cleaner and more readable oscillator line.

flowPulse = sma(rawPulse * multiplier, smoothLen)

4) Parameters (Default Settings)

length (20): analysis period for price change, volume, and ATR.

smoothLen (5): smoothing factor; higher values reduce noise.

multiplier (100): scales the output for readability; adjust to fit chart scale.

5) How to Read the Indicator

Market Pulse > 0 (green): net inflow of liquidity; buying pressure dominates.

Market Pulse < 0 (red): net outflow of liquidity; selling pressure dominates.

Near 0: neutral phase; market balance or consolidation.

Sudden peaks: strong bursts of flow — often coincide with news releases or session overlaps.

Confirmations: use as a second-level filter before entering trades or to confirm momentum behind a breakout.

6) Divergences

Divergences between price and Market Pulse are key signals of weakening flow strength:

Bullish divergence: price forms lower lows while Market Pulse forms higher lows → selling pressure is fading; potential reversal or bounce.

Bearish divergence: price forms higher highs while Market Pulse fails to confirm → buying momentum is losing strength; potential correction ahead.

For reliability, look for divergences on higher timeframes (H4, Daily).

On lower timeframes, treat them as early warnings.

7) Typical Use Cases

Breakout confirmation: price breaks resistance with a rising Market Pulse → confirms genuine participation.

False signal filter: price breaks a level but Market Pulse remains flat/negative → likely fake breakout.

Pullback entry: after a breakout, wait for a short retracement and a new positive pulse → safer entry point.

Exit signal: if you’re long and Market Pulse suddenly turns negative with strong volume → consider partial exit or tighter stops.

8) Recommended Timeframes

Intraday / Scalping: 5–30 min charts with length 10–14, smoothLen 3–5.

Swing trading: 1h–4h charts with length 20–50.

Position trading: Daily charts with larger length (50–100) for smoother data.

Always optimize parameters to the specific asset — there are no universal settings.

9) Limitations

This indicator is not a trading system — it’s a decision-support tool.

Results depend on the quality of the volume data available for the symbol.

Performance and sensitivity are influenced by length, smoothing, and multiplier values — always test before live trading.

Use alongside sound risk and money management.

10) Disclaimer

This script is provided for educational purposes only and does not constitute financial advice.

Trading and investing involve significant risk, including the potential loss of capital.

Always test indicators in simulation environments and make independent decisions based on your own analysis and risk tolerance.

Italiano

1) Scopo generale

Flow Pulse è un oscillatore pensato per visualizzare la forza e la direzione del flusso di mercato in modo immediato. Non è un semplice indicatore di volume né una copia di RSI/MACD: combina tre dimensioni fondamentali — variazione di prezzo, volume normalizzato e volatilità — per mettere in evidenza i momenti in cui la pressione dei partecipanti è realmente significativa.

È ideale per identificare: entrate guidate da flussi reali, potenziali esaurimenti, momenti di compressione/espansione del movimento e segnali di conferma per breakout o rimbalzi.

2) Dati utilizzati

L’indicatore usa esclusivamente dati disponibili sulla piattaforma TradingView del grafico corrente:

price (close) — per calcolare la variazione percentuale del prezzo;

volume per misurare l’intensità degli scambi (normalizzato su media);

ATR (Average True Range) — per normalizzare la volatilità rispetto al prezzo;

Tutti i feed (prezzo e volume) sono quelli forniti dall’exchange/fornitore dati collegato al simbolo sul grafico.

3) Logica e passaggi di calcolo

Velocità del prezzo: calcolo della variazione percentuale tra la chiusura corrente e la chiusura N barre fa:

priceChange = (close - close ) / close

— misura la direzione e magnitudine del movimento in termine relativo.

Volume normalizzato: rapporto tra il volume corrente e la media mobile semplice del volume su length barre:

volNorm = volume / sma(volume, length)

— evidenzia volumi anomali rispetto alla media.

Volatilità normalizzata (ATR): rapporto ATR/close per rendere la volatilità comparabile across price levels:

atrNorm = atr(length) / close

Combinazione: il prodotto di questi fattori (con un piccolo offset su ATR) genera un valore grezzo:

rawPulse = priceChange * volNorm * (1 + atrNorm)

— se priceChange e volNorm sono positivi e l’ATR è presente, il rawPulse sarà significativamente positivo.

Smoothing: media mobile semplice (SMA) applicata al rawPulse e moltiplicazione per un fattore scalare (multiplier) per portare il range su livelli leggibili:

flowPulse = sma(rawPulse * multiplier, smoothLen)

4) Parametri esposti (default consigliati)

length (periodo analisi) — default 20: influenza calcolo Δ% e media volumi; allunga la finestra storica.

smoothLen (smussamento) — default 5: smoothing del segnale per ridurre rumore.

multiplier — default 100: fattore di scala per rendere l’oscillatore più leggibile.

5) Interpretazione pratica dei valori

FlowPulse > 0 (verde): predominanza di flusso d’ingresso — pressione d’acquisto. Maggiore il valore, più forte la convinzione (volume + movimento + volatilità).

FlowPulse < 0 (rosso): predominanza di flusso in uscita — pressione di vendita.

Vicino a 0: assenza di flussi netti chiari; mercato piatto o bilanciato.

Picchi repentini: indicano accelerate di flusso — spesso coincidono con rotture, open/close session, news.

Sostegno al trade: usa FlowPulse come conferma prima di entrare su breakout o come avviso di attenzione su esaurimenti.

6) Divergenze (come leggerle)

Le divergenze tra prezzo e FlowPulse sono segnali importanti:

Divergenza rialzista (bullish divergence): prezzo fa nuovi minimi mentre FlowPulse non fa nuovi minimi (o forma minimo relativo più alto) → indica che la spinta di vendita non è supportata da volume/volatilità, possibile inversione/rimbalzo.

Divergenza ribassista (bearish divergence): prezzo fa nuovi massimi mentre FlowPulse non li conferma (o forma massimo relativo più basso) → la spinta d’acquisto è “debole”, possibile esaurimento e inversione.

Note pratiche: cercare divergenze su timeframe maggiori (H4, D) per maggiore attendibilità; sui timeframe minori prendere solo come early warning.

7) Esempi d’uso operativo

Conferma breakout: prezzo rompe resistenza + FlowPulse positivo e crescente → breakout più probabile e con volumi reali.

Filtro per falsi segnali: prezzo rompe ma FlowPulse è piatto/negativo → alto rischio di false breakout.

Entrata per pullback: dopo breakout, attendere un pullback con FlowPulse che torna positivo → ingresso più prudente.

Gestione delle uscite: se sei long e FlowPulse improvvisamente si inverte in negativo su volumi elevati → considerare riduzione posizione o stop.

8) Timeframe consigliati

Intraday / Scalping: M5–M30 con length ridotto (es. 10–14) e smoothLen piccolo.

Swing trading: H1–H4 con length 20–50.

Position trading: D1 con length maggiore per filtrare rumore.

Testa i parametri sul tuo asset e timeframe; nessun parametro è universale.

9) Limitazioni e avvertenze

L’indicatore non è un sistema di trading completo: è un tool di informazione e timing.

Dipende dalla qualità dei dati di volume del simbolo: su alcuni titoli/mercati (es. alcuni ETF, Forex su certi broker) il volume può essere parziale o non rappresentativo.

I valori di margine/multiplier e smoothing influenzano sensibilmente sensibilità e falsi segnali: backtest e ottimizzazione sono raccomandati.

Non usare il solo FlowPulse per entrare su leva elevata senza gestione del rischio12) Disclaimer da inserire

Disclaimer: Questo indicatore è fornito solo a scopo didattico e non costituisce consulenza finanziaria. L’uso comporta rischi: valuta sempre la gestione del rischio e testa su conto demo prima dell’applicazione in reale.

Close-Only Market StructureDYOR NFA

Function of the Close-Only Market Structure Script

The script is a custom indicator designed to display the market's structural trend based only on closing prices, ignoring price wicks (highs and lows) to focus on conviction.

pivotLengthInt Input: This user setting controls the sensitivity of the structure detection. It determines how many bars to look left and right to define a swing point (e.g., a setting of 5 means a bar's close must be the highest/lowest of the 5 preceding and 5 succeeding bars).

Swing Point Identification (SH/SL): It uses the ta.pivothigh() and ta.pivotlow() functions on the close price series to define Swing Highs (SH) and Swing Lows (SL).

Structure Tracking (structureType): It compares the most recent confirmed SH and SL against the immediately preceding ones (prevSH and prevSL) to classify the trend as one of the following four states:

HH (Higher High, Higher Low): Strong Uptrend

LL (Lower High, Lower Low): Strong Downtrend

HL/LH: Complex structure, consolidation, or reversal zones.

Structure Lines: It plots two continuous stepped lines (lastSH and lastSL) that hold the price of the most recent confirmed swing points, visually defining the current structure boundaries.

BOS Detection (Break of Structure): It identifies and plots a marker (BOS) when the current bar's close definitively breaks (closes above) the lastSH or closes below the lastSL, signaling a continuation of the trend or a major structural change.

Visual Confirmation:

Plots small SH/SL labels at the confirmed swing points.

Plots small HH/HL/LH/LL labels at the swing points to show the confirmed structural state.

Applies a light background color (green for bullish/ranging-up, red for bearish/ranging-down) for an at-a-glance view of the bias.

Alerts: It provides conditions for setting up notifications when a Bullish BOS or Bearish BOS occurs.

🚀 How to Use the Script

Open TradingView: Go to the chart where you want to apply the indicator.

Open Pine Editor: Click the Pine Editor tab at the bottom of the screen.

Paste and Save:

Copy the final, corrected Pine Script code.

Delete any existing code in the editor and paste the new code.

Click the Save button (or name the script) and then click Add to Chart.

Adjust Settings:

On the chart, hover over the indicator name ("Close-MS v6") and click the Gear Icon (Settings).

Pivot Lookback (L&R): Change this value to adjust sensitivity:

Smaller number (e.g., 3): More swings detected, structure changes faster, more noise.

Larger number (e.g., 10): Fewer swings detected, structure is more significant, less noise (recommended for higher timeframes).

Interpret the Chart:

The Red Stepped Line shows your current resistance (SH).

The Green Stepped Line shows your current support (SL).

Green Background: General bullish bias (making Higher Highs/Lows).

Red Background: General bearish bias (making Lower Highs/Lows).

BOS Triangle: Signals that the price has closed and validated a break of the previous structural high or low.

Set Alerts (Optional):

Click the Alert button (bell icon) on the TradingView toolbar.

Set the Condition to the indicator ("Close-MS v6").

Select the specific Alert Condition you want to monitor (e.g., "Bullish BOS" or "Bearish BOS").

4-Hour Range Scalping [v6.3]User Guide: 4-Hour Range Scalping Strategy

Hello! Here is the guide for the Pine Script strategy. Please read it carefully to get the best results.

📈 This script automates the "4-Hour Range Scalping Strategy" from the video.

The main idea is that the first four hours of a major trading day (like New York) set up a "trap zone." The strategy waits for the price to break out of this zone and then fail, giving us a signal that the breakout was false and the price is likely to reverse.

Here’s the simple logic:

Define the Range: It precisely calculates the highest high and lowest low during the first four hours of the selected trading session (e.g., 00:00 to 04:00 New York Time).

Wait for a Breakout: It then monitors the 5-minute chart for a price breakout where a candle fully closes outside of this established range.

Identify the Reversal: The trade trigger occurs when the price fails to continue its breakout and a subsequent 5-minute candle closes back inside the range. This signals a potential reversal or "failed breakout."

Execute the Trade:

]A Short (Sell) trade is triggered after a failed breakout above the range high.

A Long (Buy) trade is triggered after a failed breakout below the range low.

Manage the Risk: The Stop Loss is automatically placed at the peak (for shorts) or trough (for longs) of the breakout move, and the Take Profit is set to a default 2:1 Risk/Reward Ratio.

How to Use the Script (Step-by-Step) ⚙️

Follow these instructions to get it running perfectly.

1. Set Your Chart Timeframe This is the most important step. The strategy is designed to run on a 5-minute (5m) chart. Open your TradingView chart and make sure the timeframe is set to "5m".

2. Add the Script to Your Chart Open the Pine Editor tab at the bottom of TradingView, paste the entire script, and click the "Add to chart" button.

3. Configure the Settings On your chart, find the strategy's name (e.g., "4-Hour Range Scalping ") and click the gear icon ⚙️ to open its settings.

Trading Session: Choose the session for the range. New York is the default and the one from the video.

Risk/Reward Ratio: The default is 2.0, meaning your potential profit is twice your potential loss. You can adjust this to test other targets.

Backtesting Period: To see how the strategy performed on all historical data, go to the "Strategy Tester" panel, click its own gear icon ⚙️, and uncheck the boxes for "Start Date" and "End Date."

4. Understand the Visuals on Your Chart

Blue Background Area: This is the 4-hour calculation window. The script is identifying the day's high and low during this time. No trades will ever happen here.

Red Line (Range High): The highest price of the 4-hour window. This is the upper boundary of the "trap zone."

Green Line (Range Low): The lowest price of the 4-hour window. This is the lower boundary.

Green Triangle (▲): Shows where a Long (Buy) trade was entered.

Red Triangle (▼): Shows where a Short (Sell) trade was entered.

A Very Important Note on Timezones 🕒

This is critical for you in the Philippines (PHT).

The script is based on the New York session, which is 12 hours behind you. Your TradingView chart will still show your local time, but the script works on NY time in the background.

The New York "day" begins at 12:00 PM (Noon) your time.

The script's blue calculation window will be from 12:00 PM to 4:00 PM your local time.

The red and green range lines will appear on your chart only after 4:00 PM your time.

So, if you look at your chart in the morning or early afternoon, you will not see today's range yet. This is normal! The script is just waiting for the New York session to start.

How to Set Up Trade Alerts 🔔

You can have TradingView send you a notification whenever the script enters a trade.

Click the "Alert" button (looks like a clock) in the right-hand toolbar of TradingView.

In the "Condition" dropdown, select the name of the script (e.g., "4-Hour Range Scalping...").

You will then see two options: "Long Signal" and "Short Signal".

Select one (e.g., "Long Signal") and configure how you want to be notified (e.g., "Notify on app").

Click "Create". Repeat the process to create an alert for the other signal.

⚠️ Important Disclosure

For Educational and Research Purposes Only.

This script and all accompanying information are provided for educational and research purposes only. The strategy demonstrated is a technical concept and should not be misconstrued as financial, investment, legal, or tax advice.

Trading financial markets involves substantial risk and is not suitable for every investor. There is a possibility that you could sustain a loss of some or all of your initial investment. Therefore, you should not invest money that you cannot afford to lose.

Past performance is not indicative of future results. The backtesting results shown by this script are historical and do not guarantee future performance. Market conditions are constantly changing.

By using this script, you acknowledge that you are solely responsible for any and all trading decisions you make. You should conduct your own thorough research and, if necessary, seek advice from an independent financial advisor before making any investment decisions. The creators of this script assume no liability for any of your trading results.

Bollinger Band Screener [Pineify]Multi-Symbol Bollinger Band Screener Pineify – Advanced Multi-Timeframe Market Analysis

Unlock the power of rapid, multi-asset scanning with this original TradingView Pine Script. Expose trends, volatility, and reversals across your favorite tickers—all in a single, customizable dashboard.

Key Features

Screens up to 8 symbols simultaneously with individual controls.

Covers 4 distinct timeframes per symbol for robust, multi-timeframe analysis.

Integrates advanced Bollinger Band logic, adaptable with 11+ moving average types (SMA, EMA, RMA, HMA, WMA, VWMA, TMA, VAR, WWMA, ZLEMA, and TSF).

Visualizes precise state changes: Open/Parallel Uptrends & Downtrends, Consolidation, Breakouts, and more.

Highly interactive table view for instant signal interpretation and actionable alerts.

Flexible to any market: crypto, stocks, forex, indices, and commodities.

How It Works

For each chosen symbol and timeframe, the script calculates Bollinger Bands using your specified source, length, standard deviation, and moving average method.

Real-time state recognition assigns one of several states (Open Rising, Open Falling, Parallel Rising, Parallel Falling), painting the table with unique color codes.

State detection is rigorously defined: e.g., “Open Rising” is set when both bands and the basis rise, indicating strong up momentum.

All bands, signals, and strategies dynamically update as new bars print or user inputs change.

Trading Ideas and Insights

Identify volatility expansions and compressions instantly, spotting breakouts and breakdowns before they play out.

Spot multi-timeframe confluences—when trends align across several TFs, conviction increases for potential trades.

Trade reversals or continuations based on unique Bollinger Band patterns, such as squeeze-break or persistent parallel moves.

Harness this tool for scalping, swing trading, or systematic portfolio screens—your logic, your edge!

How Multiple Indicators Work Together

This screener’s core strength is its integration of multiple moving average types into Bollinger Band construction, not just standard SMA. Each average adapts the bands’ responsiveness to trend and noise, so traders can select the underlying logic that matches their market environment (e.g., HMA for fast moves or ZLEMA for smoothed lag). Overlaying 4 timeframes per symbol ensures trends, reversals, and volatility shifts never slip past your radar. When all MAs and bands synchronize across symbols and TFs, it becomes easy to separate real opportunity from market noise.

Unique Aspects

Perhaps the most flexible Bollinger Band screener for TradingView—choose from over 10 moving average methods.

Powerful multi-timeframe and multi-asset design, rare among Pine scripts.

Immediate visual clarity with color-coded table cells indicating band state—no need for guesswork or chart clutter.

Custom configuration for each asset and time slice to suit any trading style.

How to Use

Add the script to your TradingView chart.

Use the user-friendly input settings to specify up to 8 symbols and 4 timeframes each.

Customize the Bollinger Band parameters: source (price type), band length, standard deviation, and type of moving average.

Interpret the dashboard: Color codes and “state” abbreviations show you instantly which symbols and timeframes are trending, consolidating, or breaking out.

Take trades according to your strategy, using the screener as a confirmation or primary scan tool.

Customization

Fully customize: symbols, timeframes, source, band length, standard deviation multiplier, and moving average type.

Supports intricate watchlists—anything TradingView allows, this script tracks.

Adapt for cryptos, equities, forex, or derivatives by changing symbol inputs.

Conclusion

The Multi-Symbol Bollinger Band Screener “Pineify” is a comprehensive, SEO-optimized Pine Script tool to supercharge your market scanning, trend spotting, and decision-making on TradingView. Whether you trade crypto, stocks, or forex—its fast, intuitive, multi-timeframe dashboard gives you the informational edge to stay ahead of the market.

Try it now to streamline your trading workflow and see all the bands, all the trends, all the time!

Tunç ŞatıroğluTunç Şatıroğlu's Technical Analysis Suite

Description:

This comprehensive Pine Script indicator, inspired by the technical analysis teachings of Tunç Şatıroğlu, integrates six powerful TradingView indicators into a single, user-friendly suite for robust trend, momentum, and divergence analysis. Each component has been carefully selected and enhanced by beytun to improve functionality, performance, and visual clarity, aligning with Şatıroğlu's approach to technical analysis. The default configuration is meticulously set to match the exact settings of the individual indicators as used by Tunç Şatıroğlu in his training, ensuring authenticity and ease of use for followers of his methodology. Whether you're a beginner or an experienced trader, this suite provides a versatile toolkit for analyzing markets across multiple timeframes.

Included Indicators:

1. WaveTrend with Crosses (by LazyBear, modified): A momentum oscillator that identifies overbought/oversold conditions and trend reversals with clear buy/sell signals via crosses and bar color highlights.

2. Kaufman Adaptive Moving Average (KAMA) (by HPotter, modified): A dynamic moving average that adapts to market volatility, offering a smoother trend-following signal.

3. SuperTrend (by Alex Orekhov, modified): A trend-following indicator that plots dynamic support/resistance levels with buy/sell signals and optional wicks for enhanced accuracy.

4. Nadaraya-Watson Envelope (by LuxAlgo, modified): A non-linear envelope that highlights potential reversals with customizable repainting options for smoother outputs.

5. Divergence for Many Indicators v4 (by LonesomeTheBlue, modified): Detects regular and hidden divergences across multiple indicators (MACD, RSI, Stochastic, CCI, Momentum, OBV, VWMA, CMF, MFI, and more) for early reversal signals.

6. Ichimoku Cloud (TradingView built-in, modified): A multi-faceted indicator for trend direction, support/resistance, and momentum, with enhanced visuals for the Kumo Cloud.

Key Features:

- Authentic Default Settings : Pre-configured to mirror the exact parameters used by Tunç Şatıroğlu for each indicator, ensuring alignment with his proven technical analysis approach.

- Customizable Settings : Enable/disable individual indicators and fine-tune parameters to suit your trading style while retaining the option to revert to Şatıroğlu’s defaults.

- Enhanced User Experience : Modifications improve visual clarity, performance, and usability, with options like repainting smoothing for Nadaraya-Watson and adjustable Ichimoku projection periods.

- Multi-Timeframe Analysis : Combines trend-following, momentum, and divergence tools for a holistic view of market dynamics.

- Alert Conditions : Built-in alerts for SuperTrend direction changes, buy/sell signals, and divergence detections to keep you informed.

- Visual Clarity : Overlays (KAMA, SuperTrend, Nadaraya-Watson, Ichimoku) and pane-based indicators (WaveTrend, Divergences) are clearly distinguished, with customizable colors and styles.

Notes:

- The Nadaraya-Watson Envelope and Ichimoku Cloud may repaint in their default modes. Use the "Repainting Smoothing" option for Nadaraya-Watson or adjust Ichimoku settings to mitigate repainting if preferred.

- Published under the MIT License, with components licensed under GPL-3.0 (SuperTrend), CC BY-NC-SA 4.0 (Nadaraya-Watson), MPL 2.0 (Divergence), and TradingView's terms (Ichimoku Cloud).

Usage:

Add this indicator to your TradingView chart to leverage Tunç Şatıroğlu’s exact indicator configurations out of the box. Customize settings as needed to align with your strategy, and use the combined signals to identify trends, reversals, and divergences. Ideal for traders following Şatıroğlu’s methodologies or anyone seeking a powerful, all-in-one technical analysis tool.

Credits:

Original authors: LazyBear, HPotter, Alex Orekhov, LuxAlgo, LonesomeTheBlue, and TradingView.

Modifications and integration by beytun .

License:

Published under the MIT License, incorporating code under GPL-3.0, CC BY-NC-SA 4.0, MPL 2.0, and TradingView’s terms where applicable.

Multiplied and Divided Moving Average ### Multiplied and Divided Moving Average Indicator

**Description**:

The "Multiplied and Divided Moving Average" indicator is a customizable tool for TradingView users, designed to create dynamic bands around a user-selected moving average (MA). It calculates a moving average (SMA, EMA, WMA, VWMA, or RMA) and generates a user-defined number of lines above and below it by multiplying and dividing the MA by linearly spaced factors. These bands serve as potential support and resistance levels, aiding in trend identification, mean reversion strategies, or breakout detection. Optional Buy/Sell labels appear when the price crosses below the divided MAs (Buy) or above the multiplied MAs (Sell), providing clear visual cues for trading opportunities.

**Key Features**:

- **Flexible MA Types**: Choose from Simple (SMA), Exponential (EMA), Weighted (WMA), Volume-Weighted (VWMA), or Running (RMA) moving averages.

- **Customizable Bands**: Set the number of lines (0–10) above and below the MA, allowing tailored analysis for any market or timeframe.

- **Dynamic Factors**: Bands are created using factors that scale linearly from 1 to a user-defined maximum (default: 5.0), creating intuitive overbought/oversold zones.

- **Buy/Sell Signals**: Optional labels highlight potential entry (Buy) and exit (Sell) points when the price crosses the bands.

- **Clear Visuals**: The main MA is plotted in blue, with green (multiplied) and red (divided) lines using graduated transparency for easy differentiation.

**Inputs**:

- **MA Type**: Select the moving average type (default: SMA).

- **MA Length**: Set the MA period (default: 14).

- **Number of Lines Above/Below**: Choose how many bands to plot above and below the MA (default: 4, range: 0–10).

- **Max Factor**: Define the largest multiplier/divisor for the outermost bands (default: 5.0).

- **Source**: Select the price data for the MA (default: close).

- **Show Buy/Sell Labels**: Enable or disable Buy/Sell labels (default: true).

**How It Works**:

1. Calculates the chosen moving average based on user inputs.

2. Creates up to 10 lines above the MA (e.g., MA × 2, ×3, ×4, ×5 for `numLines=4`, `maxFactor=5`) and 10 below (e.g., MA ÷ 2, ÷3, ÷4, ÷5).

3. Plots the main MA in blue, multiplied lines in green, and divided lines in red, with transparency increasing for outer bands.

4. If enabled, displays "Buy" labels when the price crosses below any divided MA and "Sell" labels when it crosses above any multiplied MA, positioned at the outermost band.

**Use Cases**:

- **Trend Analysis**: Use the bands as dynamic support/resistance to confirm trend direction or reversals.

- **Mean Reversion**: Identify overbought (near multiplied MAs) or oversold (near divided MAs) conditions.

- **Breakout Trading**: Monitor price crossovers of the outermost bands for potential breakout signals.

- **Signal Confirmation**: Use Buy/Sell labels for swing trading or to complement other indicators.

**How to Use**:

1. Copy the script into TradingView’s Pine Editor.

2. Compile and apply it to your chart (e.g., stocks, forex, crypto).

3. Adjust inputs like `numLines`, `maxFactor`, or `maType` to fit your strategy.

4. Enable `Show Buy/Sell Labels` to visualize trading signals.

5. Test on various timeframes (e.g., 1H, 4H, 1D) and assets to optimize settings.

**Example Settings**:

- **Swing Trading**: Use `numLines=3`, `maxFactor=4`, `maType=EMA`, `maLength=20` on a 4-hour chart.

- **Intraday**: Try `numLines=2`, `maxFactor=3`, `maType=SMA`, `maLength=10` on a 15-minute chart.

**Notes**:

- **Performance**: Supports up to 20 bands (10 above, 10 below), staying within TradingView’s 64-plot limit.

- **False Signals**: In choppy markets, frequent crossovers may occur. Combine with trend filters (e.g., ADX, higher-timeframe MA) to reduce noise.

- **Enhancements**: Add alerts via TradingView’s alert system for Buy/Sell signals, or experiment with different `maxFactor` values for volatility.

**Limitations**:

- Bands are reactive, as they’re based on a moving average, so confirm signals with other indicators.

- High `numLines` values may clutter the chart; use 2–4 for clarity.

- Signals may lag in fast-moving markets due to the MA’s smoothing effect.

This indicator is perfect for traders seeking a customizable, visually clear tool to enhance technical analysis on TradingView. For support, feature requests (e.g., alerts, custom colors), or community discussion, visit TradingView’s forums or contact the script author.

Contract Interest Turnover T3 [T69]Overview

--------

Contract Interest Turnover (CIT) estimates how “churny” a crypto derivatives market is by comparing the amount traded in a bar to the base stock of outstanding contracts (open interest). It normalizes both Volume and Open Interest (OI) by Price (Close), then plots a Turnover Rate = (Volume/Close) ÷ (OI/Close) as colored columns. Higher values = faster contract recycling (strong momentum / hype potential).

Features

--------

- Auto-fetch OI: Pulls OI via request.security(_OI, …) when the exchange/symbol exposes an OI stream on TradingView.

- Price-normalized comparison: Converts both Volume and OI into comparable notional terms by dividing each by Close.

- Turnover columns with threshold: Color the columns green once Turnover ≥ your set threshold; gray otherwise.

- Status-line readouts: Displays normalized Volume and OI values for quick sanity checks.

- Crypto-aware timeframe: Uses chart TF for crypto; forces daily OI when not crypto to avoid noisy intraday pulls.

How to Use

----------

1. Add the script on a perpetual/futures symbol that has OI on TradingView (e.g., BTC perps where an _OI feed exists).

2. Watch the Turnover Rate bars: spikes above your threshold flag sessions where contracts are actively flipping.

3. Interpret spikes as a signal of movement or activity — it does not specify price direction, only that the market is engaged and contracts are being traded more intensely than usual.

Configuration

-------------

- Interest Turnover Threshold (default 1.0): colors columns green when Turnover ≥ threshold. Tune per market’s typical churn profile.

Under the Hood (Formulas & Logic)

---------------------------------

- Fetch OI

oiClose ← request.security(ticker.standard(syminfo.tickerid) + "_OI", timeframe, close) with ignore_invalid_symbol = true.

If none is found, the script throws a clear runtime error.

- Normalize to price

vol_norm = volume / close

oi_norm = oiClose / close

This converts both to a common notional basis so their ratio is meaningful even as price changes.

- Turnover Rate

turnover = vol_norm / oi_norm

Interpretation: fraction/multiples of the outstanding contract base traded in the bar. Color = green if turnover ≥ threshold.

Why Open Interest ≈ “Float” Proxy

---------------------------------

In stocks, float ≈ shares the public can trade. In derivatives, there are no “shares,” so Open Interest acts as the live stock of active contracts. It’s the best proxy for “what’s available in play” because it counts open positions that persist across bars. Using Volume ÷ OI mirrors stock float-turnover logic: how fast the tradable base is being recycled each period.

Why Normalize by Price

----------------------

Derivatives volume and OI may be reported in contracts, not notional value. One contract’s economic weight changes with price (especially on inverse contracts). Dividing both Volume and OI by Close:

- Puts them on a comparable notional footing.

- Prevents false spikes purely from price moves.

- Makes Turnover comparable across time even as price trends.

Advanced Tips

-------------

- Calibrate threshold: Start from the 80th–90th percentile of the last 60–90 bars of Turnover; set the threshold a touch below that to surface early heat.

- Add OI-delta: Layer an OI change histogram (current − prior) to separate new positioning from pure churn.

- Linear vs inverse: For linear (USDT-margined) contracts, the normalization still works and keeps visuals consistent; for inverse, it’s essential.

Limitations

-----------

- Data availability: Works only if your symbol exposes an _OI feed on TradingView; otherwise it errors out.

- Exchange conventions: Volume units differ by venue (contracts, coin, notional). Normalization mitigates, but cross-symbol comparisons still need caution.

- Intrabar gaps: OI is typically end-of-bar; rapid intrabar shifts won’t appear until the bar closes.

Notes

-----

- Designed primarily for crypto derivatives. For non-crypto, the script blanks OI to avoid misleading plots and uses a daily TF when needed.

Credit

------

- Concept & data: Built for TradingView data feeds.

- Acknowledgment: Credit to TradingView default indicator as requested.

- Source: This write-up reflects the logic present in your uploaded script.

Disclaimer

----------

Markets move; indicators simplify. Use with position sizing, hard stops, and catalyst awareness. The Turnover Rate flags activity, not direction.

Nifty50 Swing Trading Super Indicator# 🚀 Nifty50 Swing Trading Super Indicator - Complete Guide

**Created by:** Gaurav

**Date:** August 8, 2025

**Version:** 1.0 - Optimized for Indian Markets

---

## 📋 Table of Contents

1. (#quick-start-guide)

2. (#indicator-overview)

3. (#installation-instructions)

4. (#parameter-settings)

5. (#signal-interpretation)

6. (#trading-strategy)

7. (#risk-management)

8. (#optimization-tips)

9. (#troubleshooting)

---

## 🎯 Quick Start Guide

### What You Get

✅ **2 Complete Pine Script Indicators:**

- `swing_trading_super_indicator.pine` - Universal version for all markets

- `nifty_optimized_super_indicator.pine` - Specifically optimized for Nifty50 & Indian stocks

✅ **Key Features:**

- Multi-component signal confirmation system

- Optimized for daily and 3-hour timeframes

- Built-in risk management with dynamic stops and targets

- Real-time signal strength monitoring

- Gap analysis for Indian market characteristics

### Immediate Setup

1. Copy the Pine Script code from `nifty_optimized_super_indicator.pine`

2. Paste into TradingView Pine Editor

3. Add to chart on daily or 3-hour timeframe

4. Look for 🚀BUY and 🔻SELL signals

5. Use the information table for signal confirmation

---

## 🔍 Indicator Overview

### Core Components Integration

**🎯 Range Filter (35% Weight)**

- Primary trend identification using adaptive volatility filtering

- Optimized sampling period: 21 bars for Indian market volatility

- Enhanced range multiplier: 3.0 to handle market gaps

- Provides trend direction and strength measurement

**⚡ PMAX (30% Weight)**

- Volatility-adjusted trend confirmation using ATR-based calculations

- Dynamic multiplier adjustment based on market volatility

- 14-period ATR with 2.5 multiplier for swing trading sensitivity

- Offers trailing stop functionality

**🏗️ Support/Resistance (20% Weight)**

- Dynamic level identification using pivot point analysis

- Tighter channel width (3%) for precise Indian market levels

- Enhanced strength calculation with historical interaction weighting

- Provides entry/exit timing and breakout signals

**📊 EMA Alignment (15% Weight)**

- Multi-timeframe moving average confirmation

- Key EMAs: 9, 21, 50, 200 (popular in Indian markets)

- Hierarchical alignment scoring for trend strength

- Additional trend validation layer

### Advanced Features

**🌅 Gap Analysis**

- Automatic detection of significant price gaps (>2%)

- Gap strength measurement and impact on signals

- Specific optimization for Indian market overnight gaps