DTR Volume FVGDTR Volume FVG detects bullish and bearish Fair Value Gaps and shows how much volume occurred inside each gap. Instead of only drawing the imbalance, the indicator analyzes a lower timeframe and builds a small volume profile inside every FVG. This helps you understand which gaps are strong, weak, likely to hold, or likely to fill.

How It Works:

- The indicator finds FVGs using a lower timeframe (Auto mode or manual selection).

- Each FVG is drawn as a colored zone: green for bullish, purple for bearish.

- Inside the gap, the script shows volume distribution using horizontal boxes.

- The FVG extends forward in time until the gap is fully filled or invalidated.

- Once price closes through the gap, the zone is removed automatically.

How to Use:

- High volume inside the FVG suggests strong interest and possible support or resistance.

- Low volume suggests the gap may fill more easily.

- Bullish FVGs are used as retracement zones in uptrends.

- Bearish FVGs are used as retracement zones in downtrends.

- Use the Display option to hide the volume boxes if you want a cleaner chart.

Best For:

- Finding strong retracement zones

- Identifying which gaps matter

- Understanding how price and volume behaved during displacement

- Improving entries and stop placement with volume levels inside FVGs

This indicator gives a clearer view of which imbalances are important by combining FVG structure with real volume data.

在脚本中搜索"volume profile"

Hammer Model [#]Hammer Model - HTF Candle Entry Model

Overview

The Hammer Model is a sophisticated technical indicator that identifies high-probability reversal setups based on Higher Timeframe (HTF) candlestick wick rejection patterns. Unlike traditional hammer pattern indicators that simply flag candle formations, this system provides a complete trading framework with precise entry zones, stop loss placement, and multiple take profit targets calculated using statistical projections.

What Makes This Different

Proprietary Signal Filtering: This indicator uses a proprietary algorithm that analyzes multiple market structure conditions to filter out low-quality hammer patterns. Only the highest-probability setups are displayed, significantly reducing false signals compared to standard pattern recognition tools.

Dynamic Quadrant Mapping: Rather than basic support/resistance levels, the system divides each qualified hammer candle into three distinct zones (Upper Wick, Body, and Lower Wick), with precise .25, .5, and .75 subdivision levels for granular entry and exit planning.

Multi-Standard Deviation Projections: The indicator automatically calculates TP1 and TP2 targets based on the wick's range, along with optional 1-4 standard deviation extension levels for position scaling and profit maximization.

How It Works

Signal Generation @ Candle Close/New Candle Open

The indicator monitors your chart for HTF candles that meet specific criteria:

Bullish Hammer: Lower wick must be significantly larger than the body

Bearish Hammer: Upper wick must be significantly larger than the body

When both wicks qualify, the indicator selects the larger wick as the primary signal, depending on conditions set.

Visual Components

Bullish Setups:

SL: Stop loss level (below lower wick)

ENTRY: Entry zone (candle body range)

.25/.5/.25: Wick quadrant levels for scaling entries

TP1/TP2: First and second take profit targets

1-4STDV: Advanced/Long Range Targets

Bearish Setups:

SL: Stop loss level (above upper wick)

ENTRY: Entry zone (candle body range)

.25/.5/.25: Wick quadrant levels for scaling entries

TP1/TP2: First and second take profit targets

1-4STDV: Advanced/Long Range Targets

HTF Candle Overlay (Optional):

Displays the actual HTF candle that generated the signal

Shows Open, High, Low, and Close lines for context

Trading the Signals

For Bullish Hammers (Long):

Entry is @ HTF Candle Close / New HTF Candle Open (or wait for a .25-.5 wick retrace)

Place stop loss at or 1 tick below the SL level (lower wick low)

Target TP1 (1x wick range above) and TP2 (2x wick range above) and STDV

Use .25/.5/.25 levels to scale into positions or manage partial exits

For Bearish Hammers (Short):

Entry is @ HTF Candle Close / New HTF Candle Open (or wait for a .25-.5 wick retrace)

Place stop loss at or above the SL level (upper wick high)

Target TP1 (1x wick range below) and TP2 (2x wick range below) and STDV

Use .25/.5/.25 levels to scale into positions or manage partial exits

Key Settings

Hammer Model Conditions

Bullish/Bearish: Toggle which direction setups to display

1-2STDV / 3-4STDV: Show extended projection levels

HTF Liquidity Sweep: Filter for setups that swept previous HTF highs/lows (proprietary)

Wick Size: Require larger wick-to-body ratio (1.75x vs 1x)

Time Filters: Isolate setups during specific trading sessions (NY AM/PM, Asia, London)

Hourly Filters: Target setups that form during specific hour segments (useful for lower timeframes)

Display Options

Show Recent Hammer Models: Limit how many setups display on chart (default: 4)

Unlimited: Show all historical setups

Candle Quadrants: Toggle .25, .5, .25 subdivision lines

HTF Candle Overlay: Display the actual HTF candle that generated the signal

Timeframes

1min chart → 15min HTF (scalping)

5min chart → 1H HTF (day trading)

15min chart → 4H HTF (swing trading)

1H chart → Daily HTF (position trading)

The indicator automatically selects appropriate HTF pairs

Why Closed Source

This indicator is closed source to protect proprietary filtering algorithms that determine which hammer patterns qualify as valid signals. These filters analyze specific market structure conditions, liquidity dynamics, and statistical thresholds that have been developed through extensive backtesting, data logging over 1 years time, and represent the core intellectual property of this system. The filtering methodology is what separates this from basic pattern recognition tools and delivers higher-probability setups. To learn how to learn more about this system see Author Notes.

Best Practices

Confluence: Use this indicator alongside trend analysis, key support/resistance levels, or volume profiles

Risk Management: The SL levels provide clear invalidation points - always honor them

Scaling: Use the quadrant levels (.25/.5/.25) to scale into positions rather than entering full size at once

Session Filters: Enable time filters to focus on setups during high-liquidity sessions

Backtesting: Review historical signals on your preferred instruments to understand typical behavior and win rates

Notes

The indicator displays a table in the top-right showing the current chart timeframe and HTF being analyzed

Only charts with sufficient historical data will display all past signals

The "Unlimited" option may cause performance issues on very low timeframes with extensive history

Disclaimer: This indicator is a tool for technical analysis and risk management education and does not guarantee profitable trades. Always practice proper risk management and position sizing. Past performance does not indicate future results

Orderbook Table1. Indicator Name

Orderbook Table

This is an order book style trading volume map

that upgraded the price from my first script to label

2. One-line Introduction

A visual heatmap-style orderbook simulator that displays volume and delta clustering across price levels.

3. Overall Description

Orderbook Table is a powerful visual tool designed to replicate an on-chart approximation of a traditional order book.

It scans historical candles within a specified lookback window and accumulates traded volume into price "bins" or levels.

Each level is color-coded based on total volume and directional bias (delta), offering a layered view of where market interest was concentrated.

The indicator approximates order flow by analyzing each candle's directional volume, separating bullish and bearish volume.

With adjustable parameters such as level depth, price bin density, delta sensitivity, and opacity, it provides a highly customizable visualization.

Displayed directly on the chart, each level shows the volume at that price zone, along with a price label, offset to the right of the current bar.

Traders can use this tool to detect high liquidity zones, support/resistance clusters, and volume imbalances that may precede future price movements.

4. Key Benefits (Title + Description)

✅ On-Chart Volume Heatmap

Shows volume distribution across price levels in real-time directly on the price chart, creating a live “orderbook” view.

✅ Delta-Based Bias Coloring

Color changes based on net buying/selling pressure (delta), making aggressive demand/supply zones easy to spot.

✅ High Customizability

Users can adjust lookback bars, price bins, opacity levels, and delta usage to fit any market condition or asset class.

✅ Lightweight Simulation

Approximates orderbook depth using candle data without needing L2 feed access—works on all assets and timeframes.

✅ Clear Visual Anchoring

Volume quantities and price levels are offset to the right for easy viewing without cluttering the active chart area.

✅ Fast Market Context Recognition

Quickly identify price levels where volume concentrated historically, improving decision-making for entries/exits.

5. Indicator User Guide

📌 Basic Concept

Orderbook Table analyzes a configurable number of past bars and distributes traded volume into price "bins."

Each bin shows how much volume occurred around that price level, optionally adjusted for bullish/bearish candle direction.

⚙️ Settings Overview

Lookback Bars: Number of candles to scan for volume history

Levels (Total): Number of price levels to display around the current price

Price Bins: Granularity of price segmentation for volume distribution

Shift Right: How far to offset labels to the right of the current bar

Max/Min Opacity: Controls visual strength of volume coloring

Use Candle Delta Approx.: If enabled, colors the volume based on candle direction (green for up, red for down)

📈 Example Timing

Look for green clusters (bullish bias) below current price → possible strong demand zones

Price enters a high-volume level with previously aggressive buyers (green), suggesting support

📉 Example Timing

Red clusters (bearish bias) above current price can act as resistance or supply zones

Price stalling at a red-heavy volume band may indicate exhaustion or reversal opportunity

🧪 Recommended Use

Use as a support/resistance mapping tool in ranging and trending markets

Pair with candlestick analysis or momentum indicators for refined entry/exit points

Combine with VWAP or volume profile for multi-dimensional volume insight

🔒 Cautions

This is an approximation, not a true L2 orderbook—volume is based on historical candles, not actual limit order data

In low-volume markets or higher timeframes, bin granularity may be too coarse—adjust "Price Bins" accordingly

Delta calculation is based on open-close direction and does not reflect true buy/sell volume splits

Avoid overinterpreting low-opacity (light color) zones—they may indicate low interest rather than true resistance/support

+++

Wyckoff Accumulation/Distribution - Enhanced by ChakraWyckoff Accumulation/Distribution - Enhanced Indicator

Overview

An advanced Pine Script v6 indicator that detects Wyckoff accumulation and distribution patterns using RSI-based trend analysis, pivot detection, and volume confirmation. This enhanced version improves upon traditional Wyckoff indicators with cleaner code, English variable names, and additional market structure signals.

Key Features

Wyckoff Phase Detection

Accumulation Phase:

SC (Selling Climax): Bottom pivot with extreme bearish RSI and high volume

AR (Automatic Rally): First bounce after selling climax

ST (Secondary Test): Retest of lows without extreme RSI

SOS (Sign of Strength): Strong bullish breakout with volume confirmation ⭐ NEW

Distribution Phase:

BC (Buying Climax): Top pivot with extreme bullish RSI and high volume

DAR (Automatic Reaction): First drop after buying climax

DST (Distribution Secondary Test): Retest of highs

SOW (Sign of Weakness): Strong bearish breakdown with volume confirmation ⭐ NEW

Market Structure Events

Spring: False breakdown (RSI crosses above lower band) with background highlight

UTAD (Upthrust After Distribution): False breakout (RSI crosses below upper band) with background highlight

Visual Features

Range Boxes: Automatically draws consolidation ranges (gray) that change color on breakout:

🟢 Green = Accumulation (bullish breakout)

🔴 Red = Distribution (bearish breakout)

Pivot Markers: Orange triangles show regular (non-Wyckoff) pivot points

Bar Coloring: Lime bars for bullish trends, purple bars for bearish trends

Color-Coded Labels: All Wyckoff events clearly marked with descriptive text

Customizable Settings

RSI Settings:

RSI Length (default: 14)

Trend Sensitivity (default: 20) - Higher values = more sideways detection

Pivot Settings:

Pivot Length (default: 5) - Controls pivot point detection sensitivity

Display Options:

Toggle range boxes on/off

Toggle regular pivot markers

Toggle bar coloring by trend

Customize label text color

Advanced Detection:

Volume Confirmation toggle - Require high volume for climax events

Volume Threshold (default: 1.5x) - Adjustable volume multiplier

Alerts

8 comprehensive alert conditions:

Selling Climax (SC)

Buying Climax (BC)

Spring detection

UTAD detection

Sign of Strength (SOS)

Sign of Weakness (SOW)

Range Breakout

Improvements Over Original

✅ Pine Script v6 (latest version)

✅ English variable names (was Turkish)

✅ Fixed DAR label bug (was showing "AR")

✅ Added SOS (Sign of Strength) detection

✅ Added SOW (Sign of Weakness) detection

✅ Optional volume confirmation toggle

✅ Organized input groups for better UX

✅ Enhanced visual options

✅ Comprehensive alert system

✅ Cleaner, more maintainable code structure

Best Use Cases

Timeframes: Works on all timeframes; best on 4H, Daily, or Weekly

Markets: Stocks, Forex, Crypto, Indices

Trading Style: Swing trading, position trading, market structure analysis

Combine With: Support/Resistance, Volume Profile, Order Flow analysis

How It Works

The indicator uses RSI to identify market states (sideways, bullish, bearish) and combines this with pivot point detection and volume analysis to identify key Wyckoff events. When price is ranging (RSI between upper/lower bands), it draws a box. On breakout, the box color changes to indicate accumulation or distribution, helping traders identify smart money positioning.

Tips for Use

Lower Trend Sensitivity (10-15) for more signals in trending markets

Higher Trend Sensitivity (25-30) for clearer signals in choppy markets

Enable Volume Confirmation in high-volume markets (stocks, major crypto)

Disable Volume Confirmation in low-volume or forex markets

Watch for Spring/UTAD events within boxes for potential reversals

Version: 1.0

Pine Script: v6

Author: Chakrapani Chittabathina

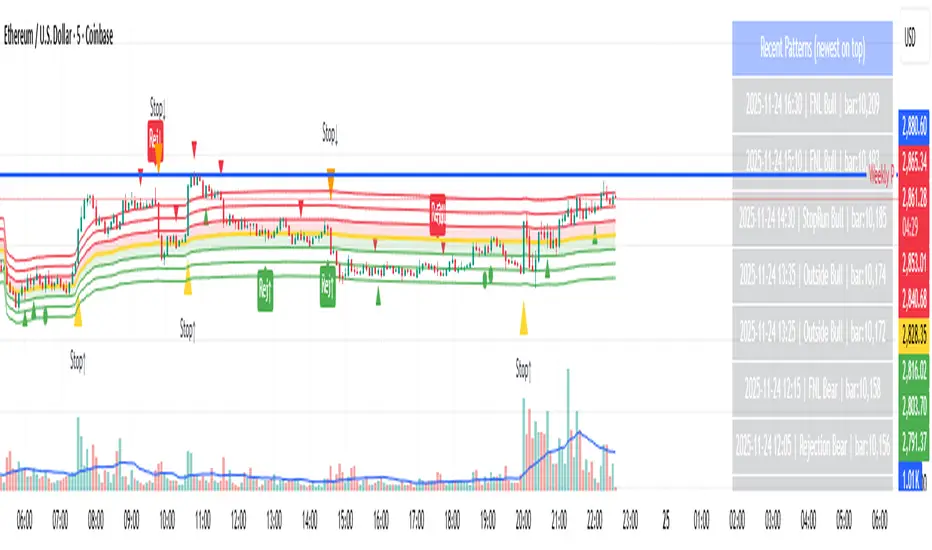

Day-Type Detector — Rejection / FNL / Outside / StopRun (Clean)Day-Type Detector — Rejection / FNL / Outside / Stop-Run (Clean Version)

This indicator identifies four high-impact candlestick day-types commonly used in professional price-action and auction-market trading: Rejection Days, Failed New Low (FNL) Days, Outside Days, and Stop-Run Days. These patterns often precede major directional moves, reversals, and absorption events, making them particularly valuable for swing traders, positional traders, and short-term discretionary traders.

The script is designed to work across all timeframes and is built around volatility-adjusted measurements using Average Daily Range (ADR) for accuracy and consistency.

What This Indicator Detects

1. Rejection Day (Bullish & Bearish)

A Rejection Day is a wide-range bar that rejects a previous extreme.

The indicator identifies rejection based on:

Range > ADR × threshold

Long lower wick (for bullish) or long upper wick (for bearish)

Close located in the strong zone of the day’s range

These conditions highlight areas where aggressive counter-orderflow entered the market.

2. Failed New Low (FNL) / Failed New High

An FNL day traps traders who attempted breakout selling or buying.

The indicator checks for:

A break beyond the previous session’s low or high

Immediate rejection back inside

Midpoint recapture conditions

ADR-normalized range requirements

These days often trigger powerful directional reversals.

3. Outside Day (Bullish & Bearish)

An Outside Day is a statistically significant expansion day that breaks both the previous high and low.

The script validates:

High > previous high and low < previous low

Range > ADR threshold

Close beyond prior session extreme to complete the rejection sequence

Outside Days often represent stop runs, shakeouts, or trend accelerations.

4. Stop-Run Day (Bullish & Bearish)

Stop-Run Days are aggressive volatility expansions and tend to be the largest ranges within short windows.

This detector identifies them using:

Range > ADR × multiplier

Close located near the extreme of the day (top for bullish, bottom for bearish)

Strong body relative to total range

Break above/below previous session extreme

These patterns indicate capitulation or forced liquidation and are often followed by continuation or sharp counter-rotation.

Key Features

✔ Historical Pattern Marking

All qualifying bars are marked on the chart using plotshape() in global scope, ensuring full historical visibility.

✔ Event Logging & Table Display

A table (top-right of the chart) displays the most recent pattern detections, including:

Timestamp

Pattern type

Bar index

This allows users to monitor and study past pattern occurrences without scanning the chart manually.

✔ ADR-Adjusted Detection

Volatility uncertainty is removed by anchoring all thresholds to ADR.

This ensures consistency across:

Different symbols

Different timeframes

Different market regimes

✔ Alerts Included

Alerts are preconfigured for:

Rejection Day Bull / Bear

FNL Bull / Bear

Outside Day Bull / Bear

Stop-Run Bull / Bear

This allows the user to receive real-time notifications when major day-type structures develop.

How to Use

Add the indicator to any timeframe chart.

Enable or disable:

Historical markers

History table

ADR diagnostics

Watch for shape markers or use alerts for real-time signals.

Use the history table to review recent occurrences.

Combine these day-types with:

Market structure levels

High/low volume nodes (LVNs)

Support/resistance zones

Trend context

These day-types are most effective when they occur near meaningful structural levels because they show where strong order-flow entered the market.

Best Practices

Use higher timeframes (1H–1D) for swing entries.

Confirm signals with market structure or volume profile.

Treat these day-types as context, not standalone signals.

Observe follow-through behavior in the next 1–3 bars after detection.

Credits

This script is based on concepts commonly seen in auction-market theory and professional price-action frameworks, such as Rejection Days, Failed New Lows, Outside Days, and Stop-Run behaviors.

All calculations and logic have been rebuilt from scratch to ensure clean, reliable, and optimized Pine Script v6 execution.

Tactical Deviation🎯 TACTICAL DEVIATION - Volume-Backed VWAP Deviation Analysis

What Makes This Different?

Unlike basic VWAP indicators, Tactical Deviation combines:

• Multi-timeframe VWAP deviation bands (Daily/Weekly/Monthly)

• Volume spike intelligence - signals only appear with volume confirmation

• Pivot reversal detection at deviation extremes

• Optional multi-VWAP confluence system

• Smart defaults for quality over quantity

This unique combination filters weak setups and identifies high-probability entries at extreme price deviations from fair value.

📊 DEFAULT SETTINGS (Ready to Use)

✅ Daily VWAP with ±2σ deviation bands

✅ Volume spike detection (1.5x average required)

✅ 2σ minimum deviation for signals

❌ Weekly/Monthly VWAPs (enable for multi-timeframe)

❌ Pivot reversal requirement (enable for stronger signals)

❌ Fill zones (optional visual enhancement)

Why: Daily VWAP is most relevant for intraday trading. 2σ bands catch meaningful moves. Volume spikes ensure conviction. Clean chart focuses on what matters.

🚀 HOW TO USE

BASIC USAGE:

• Green triangles (below bars) = Long signals at oversold deviations

• Red triangles (above bars) = Short signals at overbought deviations

SIGNAL QUALITY:

• Normal size, bright colors = Volume spike (best quality)

• Small size, lighter colors = Volume momentum

• Tiny size = No volume confirmation

DEVIATION ZONES:

• ±2σ = Extreme deviation (signals appear here)

• ±1σ to ±2σ = Extended but not extreme

• Within ±1σ = Normal range

TRADING APPROACHES:

Mean Reversion:

→ Enter when price reaches ±2σ with volume spike

→ Target: Return to VWAP or opposite band

→ Stop: Beyond extreme deviation

Trend Continuation:

→ Use bands to identify pullbacks

→ Enter pullback to VWAP in trending market

→ Volume confirms continuation

Reversal Trading:

→ Enable "Require Pivot Reversal" for stronger signals

→ Signals only when deviation + pivot reversal occur

→ Higher probability, fewer signals

⚙️ EXPLORE SETTINGS FOR FULL USE

VWAP SETTINGS:

• Show Weekly/Monthly VWAP = Multi-timeframe context

• Show ±1σ Bands = Normal deviation range

• Show ±3σ Bands = Extreme extremes (rare but powerful)

SIGNAL SETTINGS:

• Min Deviation: 1σ (more signals) | 2σ (default) | 3σ (fewer, extreme only)

• Require Pivot Reversal: OFF (default) | ON (stronger but fewer)

• Volume Spike Threshold: 1.5x (default) | 2.0x+ (major spikes) | 1.2x (more signals)

CONFLUENCE SETTINGS:

• Require Multi-VWAP Confluence: OFF (default) | ON (2+ VWAPs must agree)

• Min VWAPs: 2 (Daily + Weekly/Monthly) | 3 (all must agree)

VISUAL SETTINGS:

• Show Fill Zones = Shaded areas between bands

• Fill Opacity = Transparency adjustment

• Line Widths = Customize thickness

💡 PRO TIPS

1. Start with defaults, then enable features as you learn

2. Volume spike requirement filters weak moves - keep it enabled

3. Enable Weekly/Monthly VWAPs for higher timeframe context

4. Enable confluence for swing trading setups

5. Pivot reversals: ON for reversals, OFF for continuations

6. Check top-right info table for current deviation levels

🎨 VISUAL GUIDE

• Cyan Line = Daily VWAP (fair value)

• Cyan Bands = Daily deviation zones

• Orange Line = Weekly VWAP (if enabled)

• Purple Line = Monthly VWAP (if enabled)

• Green Triangle = Long signal (oversold)

• Red Triangle = Short signal (overbought)

⚠️ IMPORTANT

Educational purposes only. Always use proper risk management. Signals are based on statistical deviation, not guarantees. Volume confirmation improves quality but doesn't guarantee outcomes. Combine with your own analysis.

The unique combination of VWAP deviation analysis, volume profile confirmation, pivot identification, and multi-timeframe confluence in a single clean interface makes Tactical Deviation different from basic VWAP indicators.

Happy Trading! 📈

Chronos Reversal Labs - SPChronos Reversal Labs - Shadow Portfolio

Chronos Reversal Labs - Shadow Portfolio: combines reinforcement learning optimization with adaptive confluence detection through a shadow portfolio system. Unlike traditional indicator mashups that force traders to manually interpret conflicting signals, this system deploys 4 multi-armed bandit algorithms to automatically discover which of 5 specialized confluence strategies performs best in current market conditions, then validates those discoveries through parallel shadow portfolios that track virtual P&L for each strategy independently.

Core Innovation: Rather than relying on static indicator combinations, this system implements Thompson Sampling (Bayesian multi-armed bandits), contextual bandits (regime-specific learning), advanced chop zone detection (geometric pattern analysis), and historical pre-training to build a self-improving confluence detection engine. The shadow portfolio system runs 5 parallel virtual trading accounts—one per strategy—allowing the system to learn which confluence approach works best through actual position tracking with realistic exits.

Target Users: Intermediate to advanced traders seeking systematic reversal signals with mathematical rigor. Suitable for swing trading and day trading across stocks, forex, crypto, and futures on liquid instruments. Requires understanding of basic technical analysis and willingness to allow 50-100 bars for initial learning.

Why These Components Are Combined

The Fundamental Problem

No single confluence method works consistently across all market regimes. Kernel-based methods (entropy, DFA) excel during predictable phases but fail in chaos. Structure-based methods (harmonics, BOS) work during clear swings but fail in ranging conditions. Technical methods (RSI, MACD, divergence) provide reliable signals in trends but generate false signals during consolidation.

Traditional solutions force traders to either manually switch between methods (slow, error-prone) or interpret all signals simultaneously (cognitive overload). Both fail because they assume the trader knows which regime the market is in and which method works best.

The Solution: Meta-Learning Through Reinforcement Learning

This system solves the problem through automated strategy selection : Deploy 5 specialized confluence strategies designed for different market conditions, track their real-world performance through shadow portfolios, then use multi-armed bandit algorithms to automatically select the optimal strategy for the next trade.

Why Shadow Portfolios? Traditional bandit implementations use abstract "rewards." Shadow portfolios provide realistic performance measurement : Each strategy gets a virtual trading account with actual position tracking, stop-loss management, take-profit targets, and maximum holding periods. This creates risk-adjusted learning where strategies are evaluated on P&L, win rate, and drawdown—not arbitrary scores.

The Five Confluence Strategies

The system deploys 5 orthogonal strategies with different weighting schemes optimized for specific market conditions:

Strategy 1: Kernel-Dominant (Entropy/DFA focused, optimal in predictable markets)

Shannon Entropy weight × 2.5, DFA weight × 2.5

Detects low-entropy predictable patterns and DFA persistence/mean-reversion signals

Failure mode: High-entropy chaos (hedged by Technical-Dominant)

Strategy 2: Structure-Dominant (Harmonic/BOS focused, optimal in clear swing structures)

Harmonics weight × 2.5, Liquidity (S/R) weight × 2.0

Uses swing detection, break-of-structure, and support/resistance clustering

Failure mode: Range-bound markets (hedged by Balanced)

Strategy 3: Technical-Dominant (RSI/MACD/Divergence focused, optimal in established trends)

RSI weight × 2.0, MACD weight × 2.0, Trend weight × 2.0

Zero-lag RSI suite with 4 calculation methods, MACD analysis, divergence detection

Failure mode: Choppy/ranging markets (hedged by chop filter)

Strategy 4: Balanced (Equal weighting, optimal in unknown/transitional regimes)

All components weighted 1.2×

Baseline performance during regime uncertainty

Strategy 5: Regime-Adaptive (Dynamic weighting by detected market state)

Chop zones: Kernel × 2.0, Technical × 0.3

Bull/Bear trends: Trend × 1.5, DFA × 2.0

Ranging: Mean reversion × 1.5

Adapts explicitly to detected regime

Multi-Armed Bandit System: 4 Core Algorithms

What Is a Multi-Armed Bandit Problem?

Formal Definition: K arms (strategies), each with unknown reward distribution. Goal: Maximize cumulative reward while learning which arms are best. Challenge: Balance exploration (trying uncertain strategies) vs. exploitation (using known-best strategy).

Trading Application: Each confluence strategy is an "arm." After each trade, receive reward (P&L percentage). Bandits decide which strategy to trust for next signal.

The 4 Implemented Algorithms

1. Thompson Sampling (DEFAULT)

Category: Bayesian approach with probability distributions

How It Works: Model each strategy as Beta(α, β) where α = wins, β = losses. Sample from distributions, select highest sample.

Properties: Optimal regret O(K log T), automatic exploration-exploitation balance

When To Use: Best all-around choice, adaptive markets, long-term optimization

2. UCB1 (Upper Confidence Bound)

Category: Frequentist approach with confidence intervals

Formula: UCB_i = reward_mean_i + sqrt(2 × ln(total_pulls) / pulls_i)

Properties: Deterministic, interpretable, same optimal regret as Thompson

When To Use: Prefer deterministic behavior, stable markets

3. Epsilon-Greedy

Category: Simple baseline with random exploration

How It Works: With probability ε (0.15): random strategy. Else: best average reward.

Properties: Simple, fast initial learning

When To Use: Baseline comparison, short-term testing

4. Contextual Bandit

Category: Context-aware Thompson Sampling

Enhancement: Maintains separate alpha/beta for Bull/Bear/Ranging regimes

Learning: "Strategy 2: 60% win rate in Bull, 40% in Bear"

When To Use: After 100+ bars, clear regime shifts

Shadow Portfolio System

Why Shadow Portfolios?

Traditional bandits use abstract scores. Shadow portfolios provide realistic performance measurement through actual position simulation.

How It Works

Position Opening:

When strategy generates validated signal:

Opens virtual position for selected strategy

Records: entry price, direction, entry bar, RSI method

Optional: Open positions for ALL strategies simultaneously (faster learning)

Position Management (Every Bar):

Current P&L: pnl_pct = (close - entry) / entry × direction × 100

Exit if: pnl_pct <= -2.0% (stop-loss) OR pnl_pct >= +4.0% (take-profit) OR held ≥ 100 bars (time)

Position Closing:

Calculate final P&L percentage

Update strategy equity, track win rate, gross profit/loss, max drawdown

Calculate risk-adjusted reward:

text

base_reward = pnl_pct / 10.0

win_rate_bonus = (win_rate - 0.5) × 0.3

drawdown_penalty = -max_drawdown × 0.05

total_reward = sigmoid(base + bonus + penalty)

Update bandit algorithms with reward

Update RSI method bandit

Statistics Tracked Per Strategy:

Equity curve (starts at $10,000)

Win rate percentage

Max drawdown

Gross profit/loss

Current open position

This creates closed-loop learning : Strategies compete → Best performers selected → Bandits learn quality → System adapts automatically.

Historical Pre-Training System

The Problem with Live-Only Learning

Standard bandits start with zero knowledge and need 50-100 signals to stabilize. For weekly timeframe traders, this could take years.

The Solution: Historical Training

During Chart Load: System processes last 300-1000 bars (configurable) in "training mode":

Detect signals using Balanced strategy (consistent baseline)

For each signal, open virtual training positions for all 5 strategies

Track positions through historical bars using same exit logic (SL/TP/time)

Update bandit algorithms with historical outcomes

CRITICAL TRANSPARENCY: Signal detection does NOT look ahead—signals use only data available at entry bar. Exit tracking DOES look ahead (uses future bars for SL/TP), which is acceptable because:

✅ Entry decisions remain valid (no forward bias)

✅ Learning phase only (not affecting shown signals)

✅ Real-time mirrors training (identical exit logic)

Training Completion: Once chart reaches current bar, system transitions to live mode. Dashboard displays training vs. live statistics for comparison.

Benefit: System begins live trading with 100-500 historical trades worth of learning, enabling immediate intelligent strategy selection.

Advanced Chop Zone Detection Engine

The Innovation: Multi-Layer Geometric Chop Analysis

Traditional chop filters use simple volatility metrics (ATR thresholds) that can't distinguish between trending volatility (good for signals) and choppy volatility (bad for signals). This system implements three-layer geometric pattern analysis to precisely identify consolidation zones where reversal signals fail.

Layer 1: Micro-Structure Chop Detection

Method: Analyzes micro pivot points (5-bar left, 2-bar right) to detect geometric compression patterns.

Slope Analysis:

Calculates slope of pivot high trendline and pivot low trendline

Compression ratio: compression = slope_high - slope_low

Pattern Classification:

Converging slopes (compression < -0.05) → "Rising Wedge" or "Falling Wedge"

Flat slopes (|slope| < 0.05) → "Rectangle"

Parallel slopes (|compression| < 0.1) → "Channel"

Expanding slopes → "Expanding Range"

Chop Scoring:

Rectangle pattern: +15 points (highest chop)

Low average slope (<0.05): +15 points

Wedge patterns: +12 points

Flat structures: +10 points

Why This Works: Geometric patterns reveal market indecision. Rectangles and wedges create false breakouts that trap technical traders. By quantifying geometric compression, system detects these zones before signals fire.

Layer 2: Macro-Structure Chop Detection

Method: Tracks major swing highs/lows using ATR-based deviation threshold (default 2.0× ATR), projects channel boundaries forward.

Channel Position Calculation:

proj_high = last_swing_high + (swing_high_slope × bars_since)

proj_low = last_swing_low + (swing_low_slope × bars_since)

channel_width = proj_high - proj_low

position = (close - proj_low) / channel_width

Dead Zone Detection:

Middle 50% of channel (position 0.25-0.75) = low-conviction zone

Score increases as price approaches center (0.5)

Chop Scoring:

Price in dead zone: +15 points (scaled by centrality)

Narrow channel width (<3× ATR): +15 points

Channel width 3-5× ATR: +10 points

Why This Works: Price in middle of range has equal probability of moving either direction. Institutional traders avoid mid-range entries. By detecting "dead zones," system avoids low-probability setups.

Layer 3: Volume Chop Scoring

Method: Low volume indicates weak conviction—precursor to ranging behavior.

Scoring:

Volume < 0.5× average: +20 points

Volume 0.5-0.8× average: +15 points

Volume 0.8-1.0× average: +10 points

Overall Chop Intensity & Signal Filtering

Total Chop Calculation:

chop_intensity = micro_score + macro_score + (volume_score × volume_weight)

is_chop = chop_intensity >= 40

Signal Filtering (Three-Tier Approach):

1. Signal Blocking (Intensity > 70):

Extreme chop detected (e.g., tight rectangle + dead zone + low volume)

ALL signals blocked regardless of confluence

Chart displays red/orange background shading

2. Threshold Adjustment (Intensity 40-70):

Moderate chop detected

Confluence threshold increased: threshold += (chop_intensity / 50)

Only highest-quality signals pass

3. Strategy Weight Adjustment:

During Chop: Kernel-Dominant weight × 2.0 (entropy detects breakout precursors), Technical-Dominant weight × 0.3 (reduces false signals)

After Chop Exit: Weights revert to normal

Why This Three-Tier Approach Is Original: Most chop filters simply block all signals (loses breakout entries). This system adapts strategy selection during chop—allowing Kernel-Dominant (which excels at detecting low-entropy breakout precursors) to operate while suppressing Technical-Dominant (which generates false signals in consolidation). Result: System remains functional across full market regime spectrum.

Zero-Lag Filter Suite with Dynamic Volatility Scaling

Zero-Lag ADX (Trend Regime Detection)

Implementation: Applies ZLEMA to ADX components:

lag = (length - 1) / 2

zl_source = source + (source - source ) × strength

Dynamic Volatility Scaling (DVS):

Calculates volatility ratio: current_ATR / ATR_100period_avg

Adjusts ADX length dynamically: High vol → shorter length (faster), Low vol → longer length (smoother)

Regime Classification:

ADX > 25 with +DI > -DI = Bull Trend

ADX > 25 with -DI > +DI = Bear Trend

ADX < 25 = Ranging

Zero-Lag RSI Suite (4 Methods with Bandit Selection)

Method 1: Standard RSI - Traditional Wilder's RSI

Method 2: Ehlers Zero-Lag RSI

ema1 = ema(close, length)

ema2 = ema(ema1, length)

zl_close = close + (ema1 - ema2)

Method 3: ZLEMA RSI

lag = (length - 1) / 2

zl_close = close + (close - close )

Method 4: Kalman-Filtered RSI - Adaptive smoothing with process/measurement noise

RSI Method Bandit: Separate 4-arm bandit learns which calculation method produces best results. Updates independently after each trade.

Kalman Adaptive Filters

Fast Kalman: Low process noise → Responsive to genuine moves

Slow Kalman: Higher measurement noise → Filters noise

Application: Crossover logic for trend detection, acceleration analysis for momentum inflection

What Makes This Original

Innovation 1: Shadow Portfolio Validation

First TradingView script to implement parallel virtual portfolios for multi-armed bandit reward calculation. Instead of abstract scoring metrics, each strategy's performance is measured through realistic position tracking with stop-loss, take-profit, time-based exits, and risk-adjusted reward functions (P&L + win rate + drawdown). This provides orders-of-magnitude better reward signal quality for bandit learning than traditional score-based approaches.

Innovation 2: Three-Layer Geometric Chop Detection

Novel multi-scale geometric pattern analysis combining: (1) Micro-structure slope analysis with pattern classification (wedges, rectangles, channels), (2) Macro-structure channel projection with dead zone detection, (3) Volume confirmation. Unlike simple volatility filters, this system adapts strategy weights during chop —boosting Kernel-Dominant (breakout detection) while suppressing Technical-Dominant (false signal reduction)—allowing operation across full market regime spectrum without blind signal blocking.

Innovation 3: Historical Pre-Training System

Implements two-phase learning : Training phase (processes 300-1000 historical bars on chart load with proper state isolation) followed by live phase (real-time learning). Training positions tracked separately from live positions. System begins live trading with 100-500 trades worth of learned experience. Dashboard displays training vs. live performance for transparency.

Innovation 4: Contextual Multi-Armed Bandits with Regime-Specific Learning

Beyond standard bandits (global strategy quality), implements regime-specific alpha/beta parameters for Bull/Bear/Ranging contexts. System learns: "Strategy 2: 60% win rate in ranging markets, 45% in bull trends." Uses current regime's learned parameters for strategy selection, enabling regime-aware optimization.

Innovation 5: RSI Method Meta-Learning

Deploys 4 different RSI calculation methods (Standard, Ehlers ZL, ZLEMA, Kalman) with separate 4-arm bandit that learns which calculation works best. Updates RSI method bandit independently based on trade outcomes, allowing automatic adaptation to instrument characteristics.

Innovation 6: Dynamic Volatility Scaling (DVS)

Adjusts ALL lookback periods based on current ATR ratio vs. 100-period average. High volatility → shorter lengths (faster response). Low volatility → longer lengths (smoother signals). Applied system-wide to entropy, DFA, RSI, ADX, and Kalman filters for adaptive responsiveness.

How to Use: Practical Guide

Initial Setup (5 Minutes)

Theory Mode: Start with "BALANCED" (APEX for aggressive, CONSERVATIVE for defensive)

Enable RL: Toggle "Enable RL Auto-Optimization" to TRUE, select "Thompson Sampling"

Enable Confluence Modules: Divergence, Volume Analysis, Liquidity Mapping, RSI OB/OS, Trend Analysis, MACD (all recommended)

Enable Chop Filter: Toggle "Enable Chop Filter" to TRUE, sensitivity 1.0 (default)

Historical Training: Enable "Enable Historical Pre-Training", set 300-500 bars

Dashboard: Enable "Show Dashboard", position Top Right, size Large

Learning Phase (First 50-100 Bars)

Monitor Thompson Sampling Section:

Alpha/beta values should diverge from initial 1.0 after 20-30 trades

Expected win% should stabilize around 55-60% (excellent), >50% (acceptable)

"Pulls" column should show balanced exploration (not 100% one strategy)

Monitor Shadow Portfolios:

Equity curves should diverge (different strategies performing differently)

Win rate > 55% is strong

Max drawdown < 15% is healthy

Monitor Training vs Live (if enabled):

Delta difference < 10% indicates good generalization

Large negative delta suggests overfitting

Large positive delta suggests system adapting well

Optimization:

Too few signals: Lower "Base Confluence Threshold" to 2.5-3.0

Too many signals: Raise threshold to 4.0-4.5

One strategy dominates (>80%): Increase "Exploration Rate" to 0.20-0.25

Excessive chop blocking: Lower "Chop Sensitivity" to 0.7-0.8

Signal Interpretation

Dashboard Indicators:

"WAITING FOR SIGNAL": No confluence

"LONG ACTIVE ": Validated long entry

"SHORT ACTIVE ": Validated short entry

Chart Visuals:

Triangle markers: Entry signal (green = long, red = short)

Orange/red background: Chop zone

Lines: Support/resistance if enabled

Position Management

Entry: Enter on triangle marker, confirm direction matches dashboard, check confidence >60%

Stop-Loss: Entry ± 1.5× ATR or at structural swing point

Take-Profit:

TP1: Entry + 1.5R (take 50%, move SL to breakeven)

TP2: Entry + 3.0R (runner) or trail

Position Sizing:

Risk per trade = 1-2% of capital

Position size = (Account × Risk%) / (Entry - SL)

Recommended Settings by Instrument

Stocks (Large Cap): Balanced mode, Threshold 3.5, Thompson Sampling, Chop 1.0, 15min-1H, Training 300-500 bars

Forex Majors: Conservative-Balanced mode, Threshold 3.5-4.0, Thompson Sampling, Chop 0.8-1.0, 5min-30min, Training 400-600 bars

Cryptocurrency: Balanced-APEX mode, Threshold 3.0-3.5, Thompson Sampling, Chop 1.2-1.5, 15min-4H, Training 300-500 bars

Futures: Balanced mode, Threshold 3.5, UCB1 or Thompson, Chop 1.0, 5min-30min, Training 400-600 bars

Technical Approximations & Limitations

1. Thompson Sampling: Pseudo-Random Beta Distribution

Standard: Cryptographic RNG with true beta sampling

This Implementation: Box-Muller transform using market data as entropy source

Impact: Not cryptographically random but maintains exploration-exploitation balance. Sufficient for strategy selection.

2. Shadow Portfolio: Simplified Execution Model

Standard: Order book simulation with slippage, partial fills

This Implementation: Perfect fills at close price, no fees modeled

Impact: Real-world performance ~0.1-0.3% worse per trade due to execution costs.

3. Historical Training: Forward-Looking for Exits Only

Entry signals: Use only past data (causal, no bias)

Exit tracking: Uses future bars to determine SL/TP (forward-looking)

Impact: Acceptable because: (1) Entry logic remains valid, (2) Live trading mirrors training, (3) Improves learning quality. Training win rates reflect 8-bar evaluation window—live performance may differ if positions held longer.

4. Shannon Entropy & DFA: Simplified Calculations

Impact: 10-15% precision loss vs. academic implementations. Still captures predictability and persistence signals effectively.

General Limitations

No Predictive Guarantee: Past performance ≠ future results

Learning Period Required: Minimum 50-100 bars for stable statistics

Overfitting Risk: May not generalize to unprecedented conditions

Single-Instrument: No multi-asset correlation or sector context

Execution Assumptions: Degrades in illiquid markets (<100k volume), major news events, flash crashes

Risk Warnings & Disclaimers

No Guarantee of Profit: All trading involves substantial risk of loss. This indicator is a tool, not a guaranteed profit system.

System Failures: Software bugs possible despite testing. Use appropriate position sizing.

Market Regime Changes: Performance may degrade during extreme volatility (VIX >40), low liquidity periods, or fundamental regime shifts.

Broker-Specific Issues: Real-world execution includes slippage (0.1-0.5%), commissions, overnight financing costs, partial fills.

Forward-Looking Bias in Training: Historical training uses 8-bar forward window for exit evaluation. Dashboard "Training Win%" reflects this method. Real-time performance may differ.

Appropriate Use

This Indicator IS:

✅ Entry trigger system with confluence validation

✅ Risk management framework (automated SL/TP)

✅ Adaptive strategy selection engine

✅ Learning system that improves over time

This Indicator IS NOT:

❌ Complete trading strategy (requires position sizing, portfolio management)

❌ Replacement for due diligence

❌ Guaranteed profit generator

❌ Suitable for complete beginners

Recommended Complementary Analysis: Market context, volume profile, fundamental catalysts, higher timeframe alignment, support/resistance from other sources.

Conclusion

Chronos Reversal Labs V2.0 - Elite Edition synthesizes research from multi-armed bandit theory (Thompson Sampling, UCB, contextual bandits), market microstructure (geometric chop detection, zero-lag filters), and machine learning (shadow portfolio validation, historical pre-training, RSI method meta-learning).

Unlike typical indicator mashups, this system implements mathematically rigorous bandit algorithms with realistic performance validation, three-layer chop detection with adaptive strategy weighting, regime-specific learning, and full transparency on approximations and limitations.

The system is designed for intermediate to advanced traders who understand that no indicator is perfect, but through proper machine learning and realistic validation, we can build systems that improve over time and adapt to changing markets without manual intervention.

Use responsibly. Understand the limitations. Risk disclosure applies. Past performance does not guarantee future results.

Taking you to school. — Dskyz, Trade with insight. Trade with anticipation.

VWAP + Volume Spikes See Where Smart Money ExhaustsVolume tells the truth. VWAP tells the bias. This script shows both — live.

If you trade intraday momentum, reversals, or liquidity sweeps, this indicator is built for you.

It shows where volume spikes hit extreme levels, anchored around VWAP and its dynamic bands, so you can instantly spot capitulation or hidden absorption.

🎯 What This Indicator Does

✅ Plots VWAP — session-anchored, updates automatically

✅ Adds dynamic VWAP bands — standard deviation envelopes showing volatility context

✅ Highlights volume spikes — colored candles + background for abnormal prints

✅ Includes alerts — “Volume Spike”, “VWAP Cross”, or a combined alert with direction

✅ Clean visual design — instantly readable in fast markets

It’s your visual orderflow radar — whether you’re trading gold, indices, or small caps.

🔍 Why It Works

Institutions build and unwind positions around VWAP.

Retail often chases volume… this script shows you when that volume becomes too extreme.

A spike above VWAP near resistance? → Likely distribution.

A spike below VWAP near support? → Likely capitulation.

Combine volume exhaustion + VWAP context, and you’ll see market turning points form before most indicators react.

⚙️ Inputs You Can Tune

Bands lookback: adjusts how reactive the VWAP bands are

Band width (σ): set how tight or wide your deviation envelope is

Volume baseline length: controls how “abnormal” a spike must be

Spike threshold: multiplier vs. average volume

Toggle color-coding, bands, and labels

Default settings work well across 1m–15m intraday charts and 1h–4h swing frames.

💡 How Traders Use It

1️⃣ Fade Parabolics:

When a green spike candle pierces upper VWAP band on high volume → smart money unloading.

Look for rejection and short into VWAP.

2️⃣ Catch Capitulations:

When a red spike candle dumps below lower VWAP band → panic selling.

Watch for stabilization and long back to VWAP.

3️⃣ VWAP Rotation Plays:

Alerts for price crossing VWAP help you spot shift in intraday control.

Above VWAP = buyers in charge.

Below VWAP = sellers in charge.

🧠 Best Practices

Pair it with Volume Profile or Delta/Flow tools to confirm exhaustion.

Don’t chase — wait for spike confirmation + reversal candle.

Use it on liquid tickers (NASDAQ, SPY, GOLD, BTC, etc.).

Great for Dux-style small-cap shorts or index pullbacks.

🔔 Alerts Ready

Choose from:

Volume Spike (single-bar explosion)

VWAP Cross Up/Down (trend shift confirmation)

One Combined Alert (any signal, includes ticker, price, and volume)

Set once — get real-time push notifications, Telegram, or webhook signals.

📊 My Favorite Setups

US100 / NASDAQ: fade rallies above VWAP + spike

Gold / Silver: trade reversals from VWAP bands

Small caps: short back-side after volume climax

ES, DAX, Oil: scalp VWAP rotation with confluence

❤️ Support This Work

I release free and premium scripts weekly — combining smart money concepts, VWAP tools, and volume analytics.

👉 Follow me on TradingView for more indicators and setups.

👉 Comment “🔥” if you want me to post the multi-timeframe VWAP + Volume Pressure version next.

👉 Share this with your team — it helps the community grow.

Algorithm Predator - ML-liteAlgorithm Predator - ML-lite

This indicator combines four specialized trading agents with an adaptive multi-armed bandit selection system to identify high-probability trade setups. It is designed for swing and intraday traders who want systematic signal generation based on institutional order flow patterns , momentum exhaustion , liquidity dynamics , and statistical mean reversion .

Core Architecture

Why These Components Are Combined:

The script addresses a fundamental challenge in algorithmic trading: no single detection method works consistently across all market conditions. By deploying four independent agents and using reinforcement learning algorithms to select or blend their outputs, the system adapts to changing market regimes without manual intervention.

The Four Trading Agents

1. Spoofing Detector Agent 🎭

Detects iceberg orders through persistent volume at similar price levels over 5 bars

Identifies spoofing patterns via asymmetric wick analysis (wicks exceeding 60% of bar range with volume >1.8× average)

Monitors order clustering using simplified Hawkes process intensity tracking (exponential decay model)

Signal Logic: Contrarian—fades false breakouts caused by institutional manipulation

Best Markets: Consolidations, institutional trading windows, low-liquidity hours

2. Exhaustion Detector Agent ⚡

Calculates RSI divergence between price movement and momentum indicator over 5-bar window

Detects VWAP exhaustion (price at 2σ bands with declining volume)

Uses VPIN reversals (volume-based toxic flow dissipation) to identify momentum failure

Signal Logic: Counter-trend—enters when momentum extreme shows weakness

Best Markets: Trending markets reaching climax points, over-extended moves

3. Liquidity Void Detector Agent 💧

Measures Bollinger Band squeeze (width <60% of 50-period average)

Identifies stop hunts via 20-bar high/low penetration with immediate reversal and volume spike

Detects hidden liquidity absorption (volume >2× average with range <0.3× ATR)

Signal Logic: Breakout anticipation—enters after liquidity grab but before main move

Best Markets: Range-bound pre-breakout, volatility compression zones

4. Mean Reversion Agent 📊

Calculates price z-scores relative to 50-period SMA and standard deviation (triggers at ±2σ)

Implements Ornstein-Uhlenbeck process scoring (mean-reverting stochastic model)

Uses entropy analysis to detect algorithmic trading patterns (low entropy <0.25 = high predictability)

Signal Logic: Statistical reversion—enters when price deviates significantly from statistical equilibrium

Best Markets: Range-bound, low-volatility, algorithmically-dominated instruments

Adaptive Selection: Multi-Armed Bandit System

The script implements four reinforcement learning algorithms to dynamically select or blend agents based on performance:

Thompson Sampling (Default - Recommended):

Uses Bayesian inference with beta distributions (tracks alpha/beta parameters per agent)

Balances exploration (trying underused agents) vs. exploitation (using proven winners)

Each agent's win/loss history informs its selection probability

Lite Approximation: Uses pseudo-random sampling from price/volume noise instead of true random number generation

UCB1 (Upper Confidence Bound):

Calculates confidence intervals using: average_reward + sqrt(2 × ln(total_pulls) / agent_pulls)

Deterministic algorithm favoring agents with high uncertainty (potential upside)

More conservative than Thompson Sampling

Epsilon-Greedy:

Exploits best-performing agent (1-ε)% of the time

Explores randomly ε% of the time (default 10%, configurable 1-50%)

Simple, transparent, easily tuned via epsilon parameter

Gradient Bandit:

Uses softmax probability distribution over agent preference weights

Updates weights via gradient ascent based on rewards

Best for Blend mode where all agents contribute

Selection Modes:

Switch Mode: Uses only the selected agent's signal (clean, decisive)

Blend Mode: Combines all agents using exponentially weighted confidence scores controlled by temperature parameter (smooth, diversified)

Lock Agent Feature:

Optional manual override to force one specific agent

Useful after identifying which agent dominates your specific instrument

Only applies in Switch mode

Four choices: Spoofing Detector, Exhaustion Detector, Liquidity Void, Mean Reversion

Memory System

Dual-Layer Architecture:

Short-Term Memory: Stores last 20 trade outcomes per agent (configurable 10-50)

Long-Term Memory: Stores episode averages when short-term reaches transfer threshold (configurable 5-20 bars)

Memory Boost Mechanism: Recent performance modulates agent scores by up to ±20%

Episode Transfer: When an agent accumulates sufficient results, averages are condensed into long-term storage

Persistence: Manual restoration of learned parameters via input fields (alpha, beta, weights, microstructure thresholds)

How Memory Works:

Agent generates signal → outcome tracked after 8 bars (performance horizon)

Result stored in short-term memory (win = 1.0, loss = 0.0)

Short-term average influences agent's future scores (positive feedback loop)

After threshold met (default 10 results), episode averaged into long-term storage

Long-term patterns (weighted 30%) + short-term patterns (weighted 70%) = total memory boost

Market Microstructure Analysis

These advanced metrics quantify institutional order flow dynamics:

Order Flow Toxicity (Simplified VPIN):

Measures buy/sell volume imbalance over 20 bars: |buy_vol - sell_vol| / (buy_vol + sell_vol)

Detects informed trading activity (institutional players with non-public information)

Values >0.4 indicate "toxic flow" (informed traders active)

Lite Approximation: Uses simple open/close heuristic instead of tick-by-tick trade classification

Price Impact Analysis (Simplified Kyle's Lambda):

Measures market impact efficiency: |price_change_10| / sqrt(volume_sum_10)

Low values = large orders with minimal price impact ( stealth accumulation )

High values = retail-dominated moves with high slippage

Lite Approximation: Uses simplified denominator instead of regression-based signed order flow

Market Randomness (Entropy Analysis):

Counts unique price changes over 20 bars / 20

Measures market predictability

High entropy (>0.6) = human-driven, chaotic price action

Low entropy (<0.25) = algorithmic trading dominance (predictable patterns)

Lite Approximation: Simple ratio instead of true Shannon entropy H(X) = -Σ p(x)·log₂(p(x))

Order Clustering (Simplified Hawkes Process):

Tracks self-exciting event intensity (coordinated order activity)

Decays at 0.9× per bar, spikes +1.0 when volume >1.5× average

High intensity (>0.7) indicates clustering (potential spoofing/accumulation)

Lite Approximation: Simple exponential decay instead of full λ(t) = μ + Σ α·exp(-β(t-tᵢ)) with MLE

Signal Generation Process

Multi-Stage Validation:

Stage 1: Agent Scoring

Each agent calculates internal score based on its detection criteria

Scores must exceed agent-specific threshold (adjusted by sensitivity multiplier)

Agent outputs: Signal direction (+1/-1/0) and Confidence level (0.0-1.0)

Stage 2: Memory Boost

Agent scores multiplied by memory boost factor (0.8-1.2 based on recent performance)

Successful agents get amplified, failing agents get dampened

Stage 3: Bandit Selection/Blending

If Adaptive Mode ON:

Switch: Bandit selects single best agent, uses only its signal

Blend: All agents combined using softmax-weighted confidence scores

If Adaptive Mode OFF:

Traditional consensus voting with confidence-squared weighting

Signal fires when consensus exceeds threshold (default 70%)

Stage 4: Confirmation Filter

Raw signal must repeat for consecutive bars (default 3, configurable 2-4)

Minimum confidence threshold: 0.25 (25%) enforced regardless of mode

Trend alignment check: Long signals require trend_score ≥ -2, Short signals require trend_score ≤ 2

Stage 5: Cooldown Enforcement

Minimum bars between signals (default 10, configurable 5-15)

Prevents over-trading during choppy conditions

Stage 6: Performance Tracking

After 8 bars (performance horizon), signal outcome evaluated

Win = price moved in signal direction, Loss = price moved against

Results fed back into memory and bandit statistics

Trading Modes (Presets)

Pre-configured parameter sets:

Conservative: 85% consensus, 4 confirmations, 15-bar cooldown

Expected: 60-70% win rate, 3-8 signals/week

Best for: Swing trading, capital preservation, beginners

Balanced: 70% consensus, 3 confirmations, 10-bar cooldown

Expected: 55-65% win rate, 8-15 signals/week

Best for: Day trading, most traders, general use

Aggressive: 60% consensus, 2 confirmations, 5-bar cooldown

Expected: 50-58% win rate, 15-30 signals/week

Best for: Scalping, high-frequency trading, active management

Elite: 75% consensus, 3 confirmations, 12-bar cooldown

Expected: 58-68% win rate, 5-12 signals/week

Best for: Selective trading, high-conviction setups

Adaptive: 65% consensus, 2 confirmations, 8-bar cooldown

Expected: Varies based on learning

Best for: Experienced users leveraging bandit system

How to Use

1. Initial Setup (5 Minutes):

Select Trading Mode matching your style (start with Balanced)

Enable Adaptive Learning (recommended for automatic agent selection)

Choose Thompson Sampling algorithm (best all-around performance)

Keep Microstructure Metrics enabled for liquid instruments (>100k daily volume)

2. Agent Tuning (Optional):

Adjust Agent Sensitivity multipliers (0.5-2.0):

<0.8 = Highly selective (fewer signals, higher quality)

0.9-1.2 = Balanced (recommended starting point)

1.3 = Aggressive (more signals, lower individual quality)

Monitor dashboard for 20-30 signals to identify dominant agent

If one agent consistently outperforms, consider using Lock Agent feature

3. Bandit Configuration (Advanced):

Blend Temperature (0.1-2.0):

0.3 = Sharp decisions (best agent dominates)

0.5 = Balanced (default)

1.0+ = Smooth (equal weighting, democratic)

Memory Decay (0.8-0.99):

0.90 = Fast adaptation (volatile markets)

0.95 = Balanced (most instruments)

0.97+ = Long memory (stable trends)

4. Signal Interpretation:

Green triangle (▲): Long signal confirmed

Red triangle (▼): Short signal confirmed

Dashboard shows:

Active agent (highlighted row with ► marker)

Win rate per agent (green >60%, yellow 40-60%, red <40%)

Confidence bars (█████ = maximum confidence)

Memory size (short-term buffer count)

Colored zones display:

Entry level (current close)

Stop-loss (1.5× ATR)

Take-profit 1 (2.0× ATR)

Take-profit 2 (3.5× ATR)

5. Risk Management:

Never risk >1-2% per signal (use ATR-based stops)

Signals are entry triggers, not complete strategies

Combine with your own market context analysis

Consider fundamental catalysts and news events

Use "Confirming" status to prepare entries (not to enter early)

6. Memory Persistence (Optional):

After 50-100 trades, check Memory Export Panel

Record displayed alpha/beta/weight values for each agent

Record VPIN and Kyle threshold values

Enable "Restore From Memory" and input saved values to continue learning

Useful when switching timeframes or restarting indicator

Visual Components

On-Chart Elements:

Spectral Layers: EMA8 ± 0.5 ATR bands (dynamic support/resistance, colored by trend)

Energy Radiance: Multi-layer glow boxes at signal points (intensity scales with confidence, configurable 1-5 layers)

Probability Cones: Projected price paths with uncertainty wedges (15-bar projection, width = confidence × ATR)

Connection Lines: Links sequential signals (solid = same direction continuation, dotted = reversal)

Kill Zones: Risk/reward boxes showing entry, stop-loss, and dual take-profit targets

Signal Markers: Triangle up/down at validated entry points

Dashboard (Configurable Position & Size):

Regime Indicator: 4-level trend classification (Strong Bull/Bear, Weak Bull/Bear)

Mode Status: Shows active system (Adaptive Blend, Locked Agent, or Consensus)

Agent Performance Table: Real-time win%, confidence, and memory stats

Order Flow Metrics: Toxicity and impact indicators (when microstructure enabled)

Signal Status: Current state (Long/Short/Confirming/Waiting) with confirmation progress

Memory Panel (Configurable Position & Size):

Live Parameter Export: Alpha, beta, and weight values per agent

Adaptive Thresholds: Current VPIN sensitivity and Kyle threshold

Save Reminder: Visual indicator if parameters should be recorded

What Makes This Original

This script's originality lies in three key innovations:

1. Genuine Meta-Learning Framework:

Unlike traditional indicator mashups that simply display multiple signals, this implements authentic reinforcement learning (multi-armed bandits) to learn which detection method works best in current conditions. The Thompson Sampling implementation with beta distribution tracking (alpha for successes, beta for failures) is statistically rigorous and adapts continuously. This is not post-hoc optimization—it's real-time learning.

2. Episodic Memory Architecture with Transfer Learning:

The dual-layer memory system mimics human learning patterns:

Short-term memory captures recent performance (recency bias)

Long-term memory preserves historical patterns (experience)

Automatic transfer mechanism consolidates knowledge

Memory boost creates positive feedback loops (successful strategies become stronger)

This architecture allows the system to adapt without retraining , unlike static ML models that require batch updates.

3. Institutional Microstructure Integration:

Combines retail-focused technical analysis (RSI, Bollinger Bands, VWAP) with institutional-grade microstructure metrics (VPIN, Kyle's Lambda, Hawkes processes) typically found in academic finance literature and professional trading systems, not standard retail platforms. While simplified for Pine Script constraints, these metrics provide insight into informed vs. uninformed trading , a dimension entirely absent from traditional technical analysis.

Mashup Justification:

The four agents are combined specifically for risk diversification across failure modes:

Spoofing Detector: Prevents false breakout losses from manipulation

Exhaustion Detector: Prevents chasing extended trends into reversals

Liquidity Void: Exploits volatility compression (different regime than trending)

Mean Reversion: Provides mathematical anchoring when patterns fail

The bandit system ensures the optimal tool is automatically selected for each market situation, rather than requiring manual interpretation of conflicting signals.

Why "ML-lite"? Simplifications and Approximations

This is the "lite" version due to necessary simplifications for Pine Script execution:

1. Simplified VPIN Calculation:

Academic Implementation: True VPIN uses volume bucketing (fixed-volume bars) and tick-by-tick buy/sell classification via Lee-Ready algorithm or exchange-provided trade direction flags

This Implementation: 20-bar rolling window with simple open/close heuristic (close > open = buy volume)

Impact: May misclassify volume during ranging/choppy markets; works best in directional moves

2. Pseudo-Random Sampling:

Academic Implementation: Thompson Sampling requires true random number generation from beta distributions using inverse transform sampling or acceptance-rejection methods

This Implementation: Deterministic pseudo-randomness derived from price and volume decimal digits: (close × 100 - floor(close × 100)) + (volume % 100) / 100

Impact: Not cryptographically random; may have subtle biases in specific price ranges; provides sufficient variation for agent selection

3. Hawkes Process Approximation:

Academic Implementation: Full Hawkes process uses maximum likelihood estimation with exponential kernels: λ(t) = μ + Σ α·exp(-β(t-tᵢ)) fitted via iterative optimization

This Implementation: Simple exponential decay (0.9 multiplier) with binary event triggers (volume spike = event)

Impact: Captures self-exciting property but lacks parameter optimization; fixed decay rate may not suit all instruments

4. Kyle's Lambda Simplification:

Academic Implementation: Estimated via regression of price impact on signed order flow over multiple time intervals: Δp = λ × Δv + ε

This Implementation: Simplified ratio: price_change / sqrt(volume_sum) without proper signed order flow or regression

Impact: Provides directional indicator of impact but not true market depth measurement; no statistical confidence intervals

5. Entropy Calculation:

Academic Implementation: True Shannon entropy requires probability distribution: H(X) = -Σ p(x)·log₂(p(x)) where p(x) is probability of each price change magnitude

This Implementation: Simple ratio of unique price changes to total observations (variety measure)

Impact: Measures diversity but not true information entropy with probability weighting; less sensitive to distribution shape

6. Memory System Constraints:

Full ML Implementation: Neural networks with backpropagation, experience replay buffers (storing state-action-reward tuples), gradient descent optimization, and eligibility traces

This Implementation: Fixed-size array queues with simple averaging; no gradient-based learning, no state representation beyond raw scores

Impact: Cannot learn complex non-linear patterns; limited to linear performance tracking

7. Limited Feature Engineering:

Advanced Implementation: Dozens of engineered features, polynomial interactions (x², x³), dimensionality reduction (PCA, autoencoders), feature selection algorithms

This Implementation: Raw agent scores and basic market metrics (RSI, ATR, volume ratio); minimal transformation

Impact: May miss subtle cross-feature interactions; relies on agent-level intelligence rather than feature combinations

8. Single-Instrument Data:

Full Implementation: Multi-asset correlation analysis (sector ETFs, currency pairs, volatility indices like VIX), lead-lag relationships, risk-on/risk-off regimes

This Implementation: Only OHLCV data from displayed instrument

Impact: Cannot incorporate broader market context; vulnerable to correlated moves across assets

9. Fixed Performance Horizon:

Full Implementation: Adaptive horizon based on trade duration, volatility regime, or profit target achievement

This Implementation: Fixed 8-bar evaluation window

Impact: May evaluate too early in slow markets or too late in fast markets; one-size-fits-all approach

Performance Impact Summary:

These simplifications make the script:

✅ Faster: Executes in milliseconds vs. seconds (or minutes) for full academic implementations

✅ More Accessible: Runs on any TradingView plan without external data feeds, APIs, or compute servers

✅ More Transparent: All calculations visible in Pine Script (no black-box compiled models)

✅ Lower Resource Usage: <500 bars lookback, minimal memory footprint

⚠️ Less Precise: Approximations may reduce statistical edge by 5-15% vs. academic implementations

⚠️ Limited Scope: Cannot capture tick-level dynamics, multi-order-book interactions, or cross-asset flows

⚠️ Fixed Parameters: Some thresholds hardcoded rather than dynamically optimized

When to Upgrade to Full Implementation:

Consider professional Python/C++ versions with institutional data feeds if:

Trading with >$100K capital where precision differences materially impact returns

Operating in microsecond-competitive environments (HFT, market making)

Requiring regulatory-grade audit trails and reproducibility

Backtesting with tick-level precision for strategy validation

Need true real-time adaptation with neural network-based learning

For retail swing/day trading and position management, these approximations provide sufficient signal quality while maintaining usability, transparency, and accessibility. The core logic—multi-agent detection with adaptive selection—remains intact.

Technical Notes

All calculations use standard Pine Script built-in functions ( ta.ema, ta.atr, ta.rsi, ta.bb, ta.sma, ta.stdev, ta.vwap )

VPIN and Kyle's Lambda use simplified formulas optimized for OHLCV data (see "Lite" section above)

Thompson Sampling uses pseudo-random noise from price/volume decimal digits for beta distribution sampling

No repainting: All calculations use confirmed bar data (no forward-looking)

Maximum lookback: 500 bars (set via max_bars_back parameter)

Performance evaluation: 8-bar forward-looking window for reward calculation (clearly disclosed)

Confidence threshold: Minimum 0.25 (25%) enforced on all signals

Memory arrays: Dynamic sizing with FIFO queue management

Limitations and Disclaimers

Not Predictive: This indicator identifies patterns in historical data. It cannot predict future price movements with certainty.

Requires Human Judgment: Signals are entry triggers, not complete trading strategies. Must be confirmed with your own analysis, risk management rules, and market context.

Learning Period Required: The adaptive system requires 50-100 bars minimum to build statistically meaningful performance data for bandit algorithms.

Overfitting Risk: Restoring memory parameters from one market regime to a drastically different regime (e.g., low volatility to high volatility) may cause poor initial performance until system re-adapts.

Approximation Limitations: Simplified calculations (see "Lite" section) may underperform academic implementations by 5-15% in highly efficient markets.

No Guarantee of Profit: Past performance, whether backtested or live-traded, does not guarantee future performance. All trading involves risk of loss.

Forward-Looking Bias: Performance evaluation uses 8-bar forward window—this creates slight look-ahead for learning (though not for signals). Real-time performance may differ from indicator's internal statistics.

Single-Instrument Limitation: Does not account for correlations with related assets or broader market regime changes.

Recommended Settings

Timeframe: 15-minute to 4-hour charts (sufficient volatility for ATR-based stops; adequate bar volume for learning)

Assets: Liquid instruments with >100k daily volume (forex majors, large-cap stocks, BTC/ETH, major indices)

Not Recommended: Illiquid small-caps, penny stocks, low-volume altcoins (microstructure metrics unreliable)

Complementary Tools: Volume profile, order book depth, market breadth indicators, fundamental catalysts

Position Sizing: Risk no more than 1-2% of capital per signal using ATR-based stop-loss

Signal Filtering: Consider external confluence (support/resistance, trendlines, round numbers, session opens)

Start With: Balanced mode, Thompson Sampling, Blend mode, default agent sensitivities (1.0)

After 30+ Signals: Review agent win rates, consider increasing sensitivity of top performers or locking to dominant agent

Alert Configuration

The script includes built-in alert conditions:

Long Signal: Fires when validated long entry confirmed

Short Signal: Fires when validated short entry confirmed

Alerts fire once per bar (after confirmation requirements met)

Set alert to "Once Per Bar Close" for reliability

Taking you to school. — Dskyz, Trade with insight. Trade with anticipation.

Force DashboardScalping Dashboard - Complete User Guide

Overview

This scalping system consists of two complementary TradingView indicators designed for intraday trading with no overnight holds:

Force Dashboard - Single-row table showing real-time market bias and entry signals

Large Order Detection - Visual diamonds showing institutional order flow

Together, they provide a complete at-a-glance view of market conditions optimized for quick entries and exits.

Recommended Timeframes

Primary Scalping Timeframes

1-minute chart: Ultra-fast scalps (30 seconds - 3 minutes hold time)

2-minute chart: Quick scalps (2-5 minutes hold time)

5-minute chart: Standard scalps (5-15 minutes hold time)

Best Practices

Use 1-2 minute for highly liquid instruments (ES, NQ, major forex pairs)

Use 5-minute for less liquid markets or if you prefer fewer signals

Never hold past the last hour of trading to avoid overnight risk

Set hard stop times (e.g., exit all positions by 3:45 PM EST)

Dashboard Components Explained

Core Indicators (Circles ●)

MACD (5/13/5)

Green ● = Bullish momentum (MACD histogram positive)

Red ● = Bearish momentum (MACD histogram negative)

Gray ● = No clear momentum

Use: Confirms trend direction and momentum shifts

EMA (9/20/50)

Green ● = Price > EMA9 > EMA20 (uptrend)

Red ● = Price < EMA9 < EMA20 (downtrend)

Gray ● = Choppy/sideways

Use: Identifies the immediate micro-trend

Stoch (5-period Stochastic)

Green ● = Oversold (<20) - potential reversal up

Red ● = Overbought (>80) - potential reversal down

Gray ● = Neutral zone (20-80)

Use: Spots reversal opportunities at extremes

RSI (7-period)

Green ● = Oversold (<30)

Red ● = Overbought (>70)

Gray ● = Neutral

Use: Confirms overbought/oversold conditions

CVD (Cumulative Volume Delta)

Green ● = CVD above its moving average (buying pressure)

Red ● = CVD below its moving average (selling pressure)

Gray ● = Neutral

Use: Shows overall buying vs selling pressure

ΔCVD (Delta CVD - Rate of Change)

Green ● = CVD accelerating upward (buying acceleration)

Red ● = CVD accelerating downward (selling acceleration)

Gray ● = No acceleration