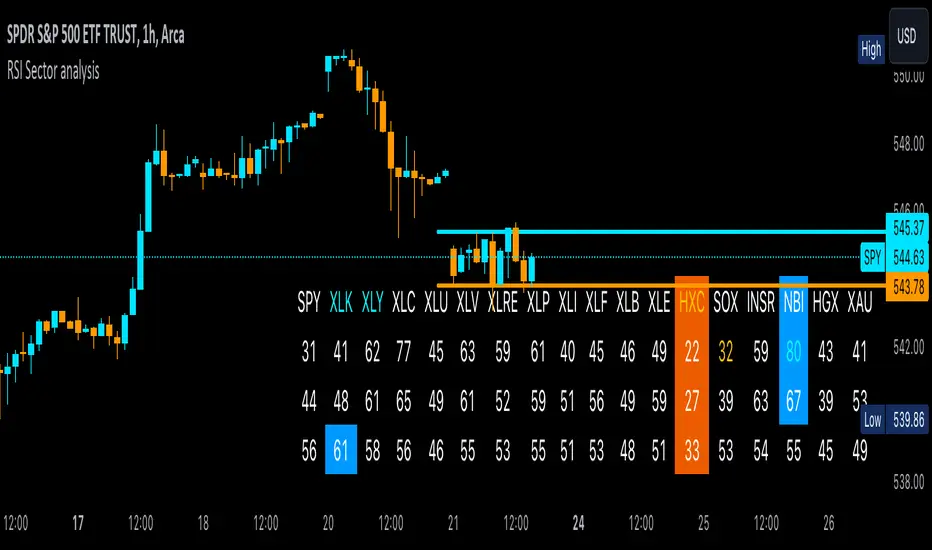

RSI Sector analysis

Screening tool that produces a table with the various sectors and their RSI values. The values are shown in 3 rows, each with a user-defined length, and can be averaged out and displayed as a single value. The chart is color coded as well. Each ETF representing a sector can be looked at individually, with the top holdings in each preprogrammed, but users can define their own if they wish. The left most ticker is the "benchmark"; SPY is the benchmark for the various sectors, and the ETF is the benchmark for the tickers within.

Symbols are color coded: light blue text indicates that a symbol has greater RSI values in all three timeframes than the benchmark (the leftmost symbol). Orange text indicates that a symbol has a lower RSI value for all three timeframes. In the first row, light blue text indicates the largest RSI increase from the third row to the first row. Orange text indicates the largest RSI decrease from the third row to the first row.

A blue highlight indicates that the value is the highest among the tickers, excluding the benchmark, and an orange highlight indicates that the value is the lowest among the tickers, also excluding the benchmark. A blue highlight on the ticker indicates that it has the highest average value of the 3 rows, and a orange highlight on the ticker indicates that it has the lowest average value of the 3 rows.

在脚本中搜索"文华财经tick价格"

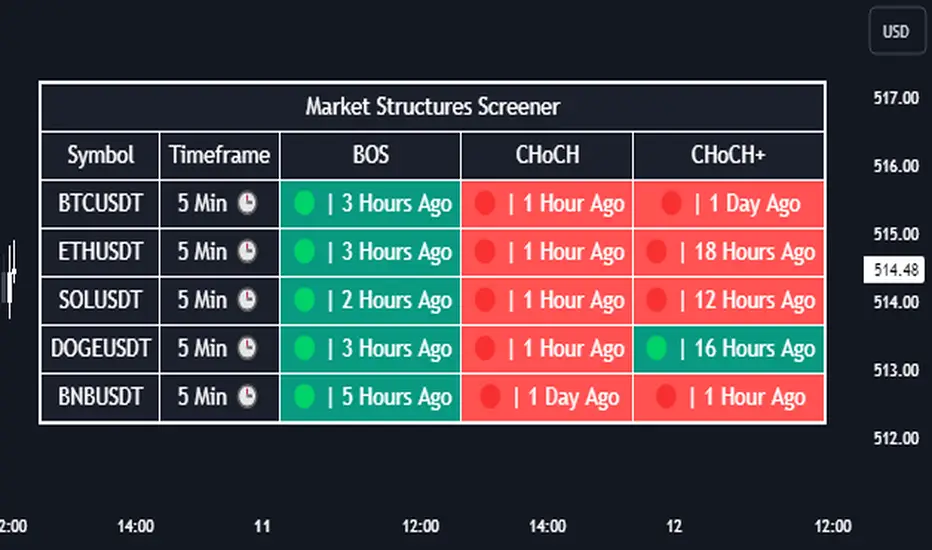

Market Structures Screener | Flux Charts💎 GENERAL OVERVIEW

Introducing our new Market Structures Screener! This screener can provide information about the latest market structures in up to 5 tickers. You can also customize the styling of the screener.

Features of the new Market Structures Screener :

Find Latest Market Structures Across 5 Tickers

Break Of Structure (BOS)

Change of Character (CHoCH)

Change of Character+ (CHoCH+)

Customizable Algoritm / Styling

📌 HOW DOES IT WORK ?

Sometimes specific market structures form and break as the market fills buy & sell orders. Formed Change of Character (CHoCH) and Break of Structure (BOS) often mean that market will change direction, and they can be spotted by inspecting low & high pivot points of the chart.

This screener then finds market structures across 5 different tickers, and shows the latest information about them.

🚩UNIQUENESS

Formed market structures can be strong hints about the current direction and the state of the market, and our screener has the ability to detect Change Of Character structures of the market with higher sensitivity (CHoCH+), so you will miss less hints. This screener will then show the elapsed time of the found BOS, CHoCH and CHoCH+ structures.

⚙️SETTINGS

1. Tickers

You can set up to 5 tickers for the screener to scan market structures here. You can also enable / disable them and set their individual timeframes.

Liquidity Grab Screener | Flux Charts💎 GENERAL OVERVIEW

Introducing our new Liquidity Grab Screener! This screener can provide information about the latest liquidity grabs in up to 5 tickers. You can also customize the algorithm that finds the liquidity grabs and the styling of the screener.

Features of the new Liquidity Grab Screener :

Find Latest Liquidity Grabs Accross 5 Tickers

Price, Size, Status Information

Customizable Algoritm / Styling

📌 HOW DOES IT WORK ?

Liquidity grabs occur when one of the latest pivots has a false breakout. Then, if the wick to body ratio of the bar is higher than 0.5 (can be changed from the settings) a bubble is plotted.

The bubble size is determined by the wick to body ratio of the candle.

This screener then finds liquidity grabs accross 5 different tickers, and shows the latest information about them.

Price -> The price when the liquidity grab happened.

Size -> Size of the liquidity grab, determined by the wick-body ratio.

Status -> Shows the elapsed time of the liquidity grab.

🚩UNIQUENESS

Liquidity grabs can be useful when determining candles that have executed a lot of market orders, and planning your trades accordingly. This screener will find liquidity grabs from up to 5 tickers and give information about their price, size and status. The screener also lets you customize the pivot length and the wick-body ratio for liquidity grabs.

⚙️SETTINGS

1. Tickers

You can set up to 5 tickers for the screener to scan order blocks here. You can also enable / disable them and set their individual timeframes.

2. General Configuration

Pivot Length -> This setting determines the range of the pivots. This means a candle has to have the highest / lowest wick of the previous X bars and the next X bars to become a high / low pivot.

Wick-Body Ratio -> After a pivot has a false breakout, the wick-body ratio of the latest candle is tested. The resulting ratio must be higher than this setting for it to be considered as a liquidity grab.

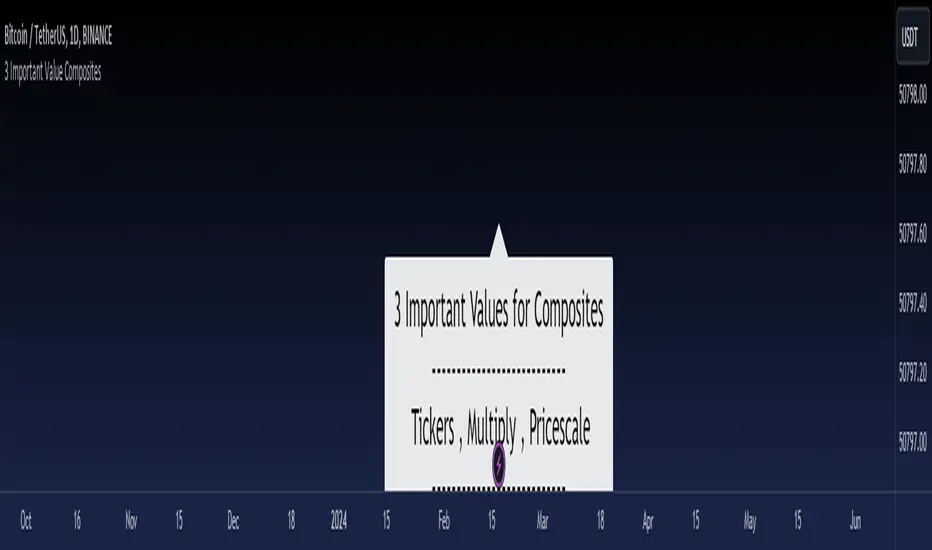

3 Important Value CompositesCalculated on February 17, 2024. USDT 378 items, BTC 282 items, BINANCE

This is a watchlist, along with the most accurate computed values that I could achieve. It may be beneficial for those who want to change values from the "120x ticker screener (composite tickers)" indicator, which is one of the excellent indicators to bypass the limitation of the request. security() function that limits to only 40 requests. I've thought about this before but couldn't succeed, but someone finally did it. :)

--> 120x ticker screener (composite tickers)

Thank you once again for this idea.

You must look for this and change it.

t1 = 'symbol', n1 = Multiply , r1 = Pricescale(decimal)

Example of grouping: Group 1

BINANCE:ETHUSDT , BINANCE:FDUSDUSDT , BINANCE:BTCUSDT

2, 4, 2

13, 10

█ Note

• Tickers: For your watchlist, arrange them from left to right, pairing them in groups of 3.

• Pricescale: This represents the decimal length, arrange them from left to right, pairing them in groups of 3.

• Multiply: This involves multiplying the first 2 items in each pair of watchlists. Arrange them from left to right, pairing them in groups of 2.

* If you group items incorrectly, it may lead to inaccurate results.

* Please be advised that if one of the values in the "Pricescale"(decimal) trio changes, there may be a need to adjust those values accordingly to ensure correct digit separation. Otherwise, within the group, the numbers might appear peculiar.

ORB Algo | Flux Charts💎 GENERAL OVERVIEW

Introducing our new ORB Algo indicator! ORB stands for "Opening Range Breakout" which is a common trading strategy. The indicator can analyze the market trend in the current session and give "Buy / Sell", "Take Profit" and "Stop Loss" signals. For more information about the analyzing process of the indicator, you can read "How Does It Work ?" section of the description.

Features of the new ORB Algo indicator :

Buy & Sell Signals

Up To 3 Take Profit Signals

Stop-Loss Signals

Alerts for Buy / Sell, Take-Profit and Stop-Loss

Customizable Algoritm

Session Dashboard

Backtesting Dashboard

📌 HOW DOES IT WORK ?

This indicator works best in 1-minute timeframe. The idea is that the trend of the current session can be forecasted by analyzing the market for a while after the session starts. However, each market has it's own dynamics and the algorithm will need fine-tuning to get the best performance possible. So, we've implemented a "Backtesting Dashboard" that shows the past performance of the algorithm in the current ticker with your current settings. Always keep in mind that past performance does not guarantee future results.

Here are the steps of the algorithm explained briefly :

1. The algorithm follows and analyzes the first 30 minutes (can be adjusted) of the session.

2. Then, algorithm checks for breakouts of the opening range's high or low.

3. If a breakout happens in a bullish or a bearish direction, the algorithm will now check for retests of the breakout. Depending on the sensitivity setting, there must be 0 / 1 / 2 / 3 failed retests for the breakout to be considered as reliable.

4. If the breakout is reliable, the algorithm will give an entry signal.

5. After the position entry, algorithm will now wait for Take-Profit or Stop-Loss zones and signal if any of them occur.

If you wonder how does the indicator find Take-Profit & Stop-Loss zones, you can check the "Settings" section of the description.

🚩UNIQUENESS

While there are indicators that show the opening range of the session, they come short with features like indicating breakouts, entries, and Take-Profit & Stop-Loss zones. We are also aware of that different stock markets have different dynamics, and tuning the algorithm for different markets is really important for better results, so we decided to make the algorithm fully customizable. Besides all that, our indicator contains a detailed backtesting dashboard, so you can see past performance of the algorithm in the current ticker. While past performance does not yield any guarantee for future results, we believe that a backtesting dashboard is necessary for tuning the algorithm. Another strength of this indicator is that there are multiple options for detection of Take-Profit and Stop-Loss zones, which the trader can select one of their liking.

⚙️SETTINGS

Keep in mind that best chart timeframe for this indicator to work is the 1-minute timeframe.

TP = Take-Profit

SL = Stop-Loss

EMA = Exponential Moving Average

OR = Opening Range

ATR = Average True Range

1. Algorithm

ORB Timeframe -> This setting determines the timeframe that the algorithm will analyze the market after a new session begins before giving any signals. It's important to experiment with this setting and find the best option that suits the current ticker for the best performance. More volatile stocks will often require this setting to be larger, while more stabilized stocks may have this setting shorter.

Sensitivity -> This setting determines how much failed retests are needed to take a position entry. Higher senstivity means that less retests are needed to consider the breakout as reliable. If you think that the current ticker makes strong movements in a bullish & bearish direction after a breakout, you should set this setting higher. If you think the opposite, meaning that the ticker does not decide the trend right after a breakout, this setting show be lower.

(High = 0 Retests, Medium = 1 Retest, Low = 2 Retests, Lowest = 3 Retests)

Breakout Condition -> The condition for the algorithm to detect breakouts.

Close = Bar needs to close higher than the OR High Line in a bullish breakout, or lower than the OR Low Line in a bearish breakout. EMA = The EMA of the bar must be higher / lower than OR Lines instead of the close price.

TP Method -> The method for the algorithm to use when determining TP zones.

Dynamic = This TP method essentially tries to find the bar that price starts declining the current trend and going to the other direction, and puts a TP zone there. To achieve this, it uses an EMA line, and when the close price of a bar crosses the EMA line, It's a TP spot.

ATR = In this TP method, instead of a dynamic approach the TP zones are pre-determined using the ATR of the entry bar. This option is generally for traders who just want to know their TP spots beforehand while trading. Selecting this option will also show TP zones at the ORB Dashboard.

"Dynamic" option generally performs better, while the "ATR" method is safer to use.

EMA Length -> This setting determines the length of the EMA line used in "Dynamic TP method" and "EMA Breakout Condition". This is completely up to the trader's choice, though the default option should generally perform well. You might want to experiment with this setting and find the optimal length for the current ticker.

Stop-Loss -> Algorithm will place the Stop-Loss zone using setting.

Safer = The SL zone will be placed closer to the OR High for a bullish entry, and closer to the OR Low for a bearish entry.

Balanced = The SL zone will be placed in the center of OR High & OR Low

Risky = The SL zone will be placed closer to the OR Low for a bullish entry, and closer to the OR High for a bearish entry.

Adaptive SL -> This option only takes effect if the first TP zone is hit.

Enabled = After the 1st TP zone is hit, the SL zone will be moved to the entry price, essentially making the position risk-free.

Disabled = The SL zone will never change.

2. ORB Dashboard

ORB Dashboard shows the information about the current session.

3. ORB Backtesting

ORB Backtesting Dashboard allows you to see past performance of the algorithm in the current ticker with current settings.

Total amount of days that can be backtested depends on your TV subscription.

Backtesting Exit Ratios -> You can select how much of percent your entry will be closed at any TP zone while backtesting. For example, %90, %5, %5 means that %90 of the position will be closed at the first TP zone, %5 of it will be closed at the 2nd TP zone, and %5 of it will be closed at the last TP zone.

COSTAR Strategy [SS]A little late posting this but here it is, as promised!

This is the companion to the COSTAR indicator.

What it does:

It creates a co-integration paired relationship with a separate, cointegrated ticker. It then plots out the expected range based on the value of the cointegrated pair. When the current ticker is below the value of its co-integrated partner, it becomes a "Buy" and should be longed. When it becomes overvalued in comparison, it becomes a "Sell" and should be shorted.

The example above is with BA and USO, which have a strong inverse relationship.

How it works:

I made the strategy version a bit more intuitive. Instead of you selecting the parameters for your model, it will autoselect the ideal parameters based on your desired co-integrated pair. You simply enter the ticker you want to compare against, and it will sort through the values at various lags to find significance and stationarity. It will then create a model and plot the model out for you on your chart, as you can see above.

The premise of the strategy:

The premise of the strategy is as stated before. You long when the ticker is undervalued in comparison to its co-integrated pair, and short when it is overvalued. The conditions for entry are simply a co-integrated pair being over the expected range (short) or below the expected range (long).

The condition to exit is a "re-integration", or a crossover of the expected value of the ticker (the centreline).

What if it can't find a relationship?

In some instances, the indicator will not be able to determine a co-integrated relationship, owning to a lack of stationarity between the data. When this happens, you will get the following error:

The indicator provides you with prompts, such as switching the timeframe or trying an alternative ticker. In the case displayed above, if we simply switch to the 1 hour timeframe, we have a viable model with great backtest results:

You can toggle in the settings menu the various parameters, such as timeframe, fills and displays.

And that is the strategy in a nutshell, be sure to check out its partner indicator, COSTAR, for more information on the premise of using co-integrated models for trading. And let me know your questions below!

Safe trades everyone!

KNN ATR Dual Range Predictions [SS]Excited to release this indicator!

I wanted to do a machine learning, ATR based indicator for a while, but I first had to learn about machine learning algos haha.

Now that I have created a KNN based regression methodology (shared in a previous indicator), I can finally do it!

So this is a Nearest Known Neighbor or KNN regression based indicator that uses ATR (average ranges) to predict future ranges.

It operates by calculating the move from High to Open and Open to Low and performing KNN regression to look for other, similar instances of similar movements and what followed those movements.

It provides for 2 methods of KNN regression, the traditional Cluster method (where it identifies a number of clusters within a tolerance range and averages them out), or the method of last instance (where it finds the most recent identical instance and plots the result from that).

You can toggle the parameters as you wish, including the:

a) Type of Regression

b) Number of Clusters

c) Tolerance for Clusters

Others functions:

The indicator provides for the ability to view 2 different timeframe targets. The default calculation is the current timeframe you are on. So if you are on the 1 minute, 5 minute or 1 hour, it will automatically default the primary range to this timeframe. This cannot be changed.

But it permits for a second prediction to be calculated for a timeframe you can specify. The example in the chart above is the 1 hour overlaid on the 5 minute chart.

You can see how the model is performing in the statistics table. The statistics table can be removed as well if you don't want it overlaid on your chart.

You can also toggle off and on the various ranges. IF you only want to visualize 1 hour levels on a 5 minute chart, you can toggle off the bands and just view the higher tf data. Inversely, if you only want the current timeframe data and not the higher tf data, you can toggle the higher tf data off as well.

General Use Tips:

Some general use tips include:

🎯The default settings are appropriate for most common tickers. Because this is performing an autoregression on itself, the parameters tend to be more tight vs. performing dual correlation between two separate tickers which are sizably different in scale (which would require a higher tolerance).

Here is an example of YM1!, which is a sizably larger ticker, however it is performing well with the current settings.

🎯 If you get not great results from your ranges or an error in the correlation table, something like this:

It means the parameters are too tight for what you want to do and it is having trouble identifying other, similar cases (in this case, the lookback length was significantly shortened). The first step is to:

a) Expand your lookback range (up to 500 is usually sufficient). This should resolve most issues in most cases. If not:

b) If you are using the Cluster method, try broadening your cluster tolerance by 0.5 increments.

Between those two implementations, you should get a functional model. And it actually honestly hasn't happened to me in general use, I had to force that example by significantly shortening the lookback period.

Concluding Remarks

And that's pretty much the indicator.

I hope you enjoy it! I was really excited to be finally able to do it, like I said I attempted to do this for a while but needed to research the whole KNN process and how its performed.

Enjoy and leave your comments and questions below!

Bollinger Bands (Nadaraya Smoothed) | Flux ChartsTicker: AMEX:SPY , Timeframe: 1m, Indicator settings: default

General Purpose

This script is an upgrade to the classic Bollinger Bands. The idea behind Bollinger bands is the detection of price movements outside of a stock's typical fluctuations. Bollinger Bands use a moving average over period n plus/minus the standard deviation over period n times a multiplier. When price closes above or below either band this can be considered an abnormal movement. This script allows for the classic Bollinger Band interpretation while de-noising or "smoothing" the bands.

Efficacy

Ticker: AMEX:SPY , Timeframe: 1m, Indicator settings: Standard Dev: 2; Level 1 : off; Level 2: off; labels: off

Upper Band Key:

Blue: Bollinger No smoothing

Orange: Bollinger SMA smoothing period of 10

Purple: Bollinger EMA smoothing period of 10

Red: Nadaraya Smoothed Bollinger bandwidth of 6

Here we chose periods so that each would have a similar offset from the original Bollinger's. Notice that the Red Band has a much smoother result while on average having a similar fit to the other smoothing techniques. Increasing the EMA's or SMA's period would result in them being smoother however the offset would increase making them less accurate to the original data.

Ticker: AMEX:SPY , Timeframe: 1m, Indicator settings: Standard Dev: 2; Level 1: off; Level 2: off; labels: off

Upper Band Key:

Blue: Bollinger No smoothing

Orange: Bollinger SMA smoothing period of 20

Purple: Bollinger EMA smoothing period of 20

Red: Nadaraya Smoothed Bollinger bandwidth of 6

This makes the Nadaraya estimator a particularly efficacious technique in this use case as it achieves a superior smoothness to fit ratio.

How to Use

This indicator is not intended to be used on its own. Its use case is to identify outlier movements and periods of consolidation. The Smoothing Factor when lowered results in a more reactive but noisy graph. This setting is also known as the "bandwidth" ; it essentially raises the amplitude of the kernel function causing a greater weighting to recent data similar to lowering the period of a SMA or EMA. The repaint smoothing simply draws on the Bollinger's each chart update. Typically repaint would be used for processing and displaying discrete data however currently it's simply another way to display the Bollinger Bands.

What makes this script unique.

Since Bollinger bands use standard deviation they have excess noise. By noise we mean minute fluctuations which most traders will not find useful in their strategies. The Nadaraya-Watson estimator, as used, is essentially a weighted average akin to an ema. A gaussian kernel is placed at the candlestick of interest. That candlestick's value will have the highest weight. From that point the other candlesticks' values effect on the average will decrease with the slope of the kernel function. This creates a localized mean of the Bollinger Bands allowing for reduced noise with minimal distortion of the original Bollinger data.

Modern Portfolio Management IndicatorAfter weeks of grueling over this indicator, I am excited to be releasing it!

Intro:

This is not a sexy, technical or math based indicator that will give you buy and sell signals or anything fancy, but it is an indicator that I created in hopes to bridge a gap I have noticed. That gap is the lack of indicators and technical resources for those who also like to plan their investments. This indicator is tailored to those who are either established investors and to those who are looking to get into investing but don't really know where to start.

The premise of this indicator is based on Modern Portfolio Theory (MPT). Before we get into the indicator itself, I think its important to provide a quick synopsis of MPT.

About MPT:

Modern Portfolio Theory (MPT) is an investment framework that was developed by Harry Markowitz in the 1950s. It is based on the idea that an investor can optimize their investment portfolio by considering the trade-off between risk and return. MPT emphasizes diversification and holds that the risk of an individual asset should be assessed in the context of its contribution to the overall portfolio's risk. The theory suggests that by diversifying investments across different asset classes with varying levels of risk, an investor can achieve a more efficient portfolio that maximizes returns for a given level of risk or minimizes risk for a desired level of return. MPT also introduced the concept of the efficient frontier, which represents the set of portfolios that offer the highest expected return for a given level of risk. MPT has been widely adopted and used by investors, financial advisors, and portfolio managers to construct and manage portfolios.

So how does this indicator help with MPT?

The thinking and theory that went behind this indicator was this: I wanted an indicator, or really just a "way" to test and back-test ticker performance over time and under various circumstances and help manage risk.

Over the last 3 years we have seen a massive bull market, followed by a pretty huge bear market, followed by a very unexpected bull market. We have been and continue to be plagued with economic and political uncertainty that seems to constantly be looming over everyone with each waking day. Some people have liquidated their retirement investments, while others are fomoing in to catch this current bull run. But which tickers are sound and how tickers and funds have compared amongst each other remains somewhat difficult to ascertain, absent manually reviewing and calculating each ticker individually.

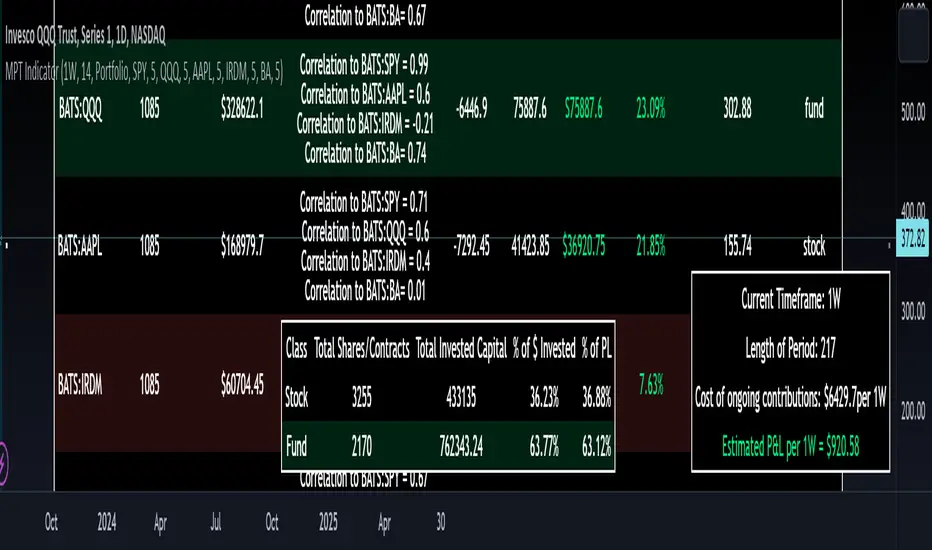

That is where this indicator comes in. This indicator permits the user to define up to 5 equities that they are potentially interested in investing in, or are already invested in. The user can then select a specific period in time, say from the beginning of 2022 till now. The user can then define how much they want to invest in each company by number of shares, so if they want to buy 1 share a week, or 2 shares a month, they can input these variables into the indicator to draw conclusions. As many brokers are also now permitting fractional share trading, this ability is also integrated into the indicator. So for shares, you can put in, say, 0.25 shares of SPY and the indicator will accept this and account for this fractional share.

The indicator will then show you a portfolio summary of what your earnings and returns would be for the defined period. It will provide a percent return as well as the projected P&L based on your desired investment amount and frequency.

But it goes beyond just that, you can also have the indicator display a simple forecasting projection of the portfolio. It will show the projected P&L and % Return over various periods in time on each of the ticker (see image below):

The indicator will also break down your portfolio allocation, it will show where the majority of your holdings are and where the majority of your P&L in coming from (best performers will show a green fill and worst will show a red fill, see image below):

This colour coding also extends to the portfolio breakdown itself.

Dollar cost averaging (DCA) is incorporated into the indicator itself, by assuming ongoing contributions. If you want to stop contributions at a certain point, you just select your end time for contributions at the point in which you would stop contributing.

The indicator also provides some basic fundamental information about the company tickers (if applicable). Simply select the "Fundamental" chart and it will display a breakdown of the fundamentals, including dividends paid, market cap and earnings yield:

The indicator also provides a correlation assessment of each holding against each other holding. This emphasizes the profound role of diversification on portfolios. The less correlation you have in your portfolio among your holdings, the better diversified you are. As well, if you have holdings that are perfectly inverse other holdings, you have a pseudo hedge against the downturn of one of your holdings. This is even more helpful if the inverse is a company with solid fundamentals.

In the below example you will see NASDAQ:IRDM in the portfolio. You will be able to see that NASDAQ:IRDM has a slight inverse relationship to SPY:

Yet IRDM has solid fundamentals and is performing well fundamentally. Thus, this makes IRDIM a solid addition to your portfolio as it can potentially hedge against a downturn for SPY and is less risky than simply holding an inverse leveraged share on SPY which is most likely just going to cost you money than make you money.

Concluding remarks:

There are many fun and interesting things you can do with this indicator and I encourage you to try it out and have fun with it! The overall objective with the indicator is to help you plan for your portfolio and not necessarily to manage your portfolio. If you have a few stocks you are looking at and contemplating investing in, this will help you run some theoretical scenarios with this stock based on historical performance and also help give you a feel of how it will perform in the future based on past behaviour.

It is important to remember that past behaviour does not indicate future behaviour, but the indicator provides you with tools to get a feel for how a stock has performed under various circumstances and get a general feel of the fundamentals of the company you could potentially be investing in.

Please note, this indicator is not meant to replace full, fundamental analyses of individual companies. It is simply meant to give you a "gist" of how companies are fundamentally and how they have performed historically.

I hope you enjoy it!

Safe trades everyone!

Autocorrelation OscillatorReleasing the autocorrelation oscillator.

NOTE! Please be sure to read the description. This is a theoretical indicator and its important to understand the theory behind its use.

About the indicator:

Before getting into the indicator and its functionality, its important to discuss the theoretical underpinnings of the indicator.

The autocorrelation oscillator operates on two theories of market behaviour that go hand in hand. Those theories are the market efficiency theory and the random walk theory (or hypothesis ).

Market efficiency theory: The market efficiency theory or "Efficient Market Hypothesis (EMH)" postulates that all available information is reflected in a ticker's price almost instantaneously and thus it is impossible for an investor or trader to get ahead of the market because we cannot respond to the speed that the market responds. Of course, there are many holes in this theory, the most notable being that the market is a function of humans. Absent humans and their technological integrations into the market, the market would cease to react at all. But that's besides the point. This is a widely accepted theory and one in which I can mathematically observe through statistical tests. The truth behind this theory is the market is efficient for responding to evolving economic and financial information, likely owning to huge amounts of computer and algorithmic integration into trading, and thus the market is more efficient than the average person is capable (absent computerized algorithms and integration) of ascertaining nuanced financial and economic circumstances. By the time we the people can appraise information, the market has already acted on it. And that is the main premise of the EMH.

The next theory is the Random Walk Theory or Hypothesis (RWH). This builds on the EMH and essentially postulates that the market reacts so quickly to price in current circumstances that it is too random for people to truly exploit and benefit from.

The result of these two theories is two-fold and can be summarized as such:

a) The market behaves in a chaotic fashion that is seemingly random and is incapable of being predicted effectively; and

b) The market is more efficient than a person in incorporating key fundamental information, contributing to the high degree of seemingly random behaviour.

So, how does this help us?

It is said, because of the EMH and the RWH, the only way to truly exploit the market for profit is by:

a) Buying and holding and investing under the bias that stocks will eventually rise in value; or

b) For short term trading, exploiting the pricing anomalies within the data.

So how do we exploit pricing anomalies within the data?

Well, in my own research on market efficiency and behaviour, I have identified many ways of figuring out some anomalies. One of the most effective ways is by looking at simple correlation of lagged values, or autocorrelation for short.

What is autocorrelation and how to use it in relation to EMH and RWH?

Autocorrelation refers to the correlative relationship among the values in a series. Put simply, its the relationship of the same variable over time. For example, if we wanted to look at the auto-correlation of a ticker's high price, we would take, say, 5 to 7 previous high prices and correlate them with the current high price in a series dataset. If the EMH and RWH are true, the correlation among all the variables should have an average less than 0.5 or greater than -0.5. This would indicate true randomness in the dataset and thus an efficient market.

However, if the average of all of the sum's of these correlations are greater than or equal to 0.5 or less than or equal to -0.5, that indicates there is a high degree of autocorrelation and thus the EMH ad RWH is being invalidated as the market is not operating efficiently. This is an anomaly and this anomaly can be exploited.

So how do we exploit it?

Well, when the EMH and RWH hypothesis is being invalidated, we can expect what I coin as a "Regression to Chaos" i.e. the market will revert back to an efficient equilibrium state. So if we have a high correlation of the lagged variables and a strong uptrend or downtrend correlation, we can expect an inefficient market to correct back to an efficient market (i.e. have a reversal from the current trend).

So how does the indicator work?

The indicator measures the lagged correlation of the previous 5 highs and lows of a ticker. A high correlation among all of the highs and lows that exceeds 0.8 would be an invalidation of the EMH and RWH and thus signal a correction to come (i.e. a Regression to Chaos).

The indicator will display this by changing colour. Red for a bearish reversal and green for a bullish. Let's take a look below using the ticker MSFT:

Above we can see the indicator identifying observed inefficiencies within the MSFT ticker on the 1 minute timeframe. The green vertical lines correspond to potential bullish reversals as a result of bearish inefficiencies, the red correspond to bearish reversals as a result of bullish inefficiencies.

You can see these lead to reversals within the ticker.

Components of the indicator:

In the chart above we see the following that are being indicated by arrows:

Red Arrows: Show the identified inefficiencies. Red for bullish inefficiencies (i.e. bearish reversal), green for bearish inefficiencies (i.e. bullish reversal)

Yellow Arrow: The lagged variable chart. This will display the current correlation among all the lagged variables the indicator is assessing.

Teal arrow: Displays the current strength of the trend by correlating the trend to time. A strong negative value (i.e. a value less than or equal to -0.5) indicates a strong downtrend, a strong positive value indicates the inverse.

You can unselect the data-tables in the settings menu if you just want to view the correlation line itself. This part of the indicator is customizable. You can also define the lookback period; however, it is strongly recommended to leave it at 14 as this maintains the use of this indicator as an oscillator.

And that is the indicator! Let me know your comments, questions and feedback below.

Safe trades everyone!

Open Interest Chart [LuxAlgo]The Open Interest Chart displays Commitments of Traders %change of futures open interest , with a unique circular plotting technique, inspired from this publication Periodic Ellipses .

🔶 USAGE

Open interest represents the total number of contracts that have been entered by market participants but have not yet been offset or delivered. This can be a direct indicator of market activity/liquidity, with higher open interest indicating a more active market.

Increasing open interest is highlighted in green on the circular plot, indicating money coming into the market, while decreasing open interests highlighted in red indicates money coming out of the market.

You can set up to 6 different Futures Open interest tickers for a quick follow up:

🔶 DETAILS

Circles are drawn, using plot() , with the functions createOuterCircle() (for the largest circle) and createInnerCircle() (for inner circles).

Following snippet will reload the chart, so the circles will remain at the right side of the chart:

if ta.change(chart.left_visible_bar_time ) or

ta.change(chart.right_visible_bar_time)

n := bar_index

Here is a snippet which will draw a 39-bars wide circle that will keep updating its position to the right.

//@version=5

indicator("")

n = bar_index

barsTillEnd = last_bar_index - n

if ta.change(chart.left_visible_bar_time ) or

ta.change(chart.right_visible_bar_time)

n := bar_index

createOuterCircle(radius) =>

var int end = na

var int start = na

var basis = 0.

barsFromNearestEdgeCircle = 0.

barsTillEndFromCircleStart = radius

startCylce = barsTillEnd % barsTillEndFromCircleStart == 0 // start circle

bars = ta.barssince(startCylce)

barsFromNearestEdgeCircle := barsTillEndFromCircleStart -1

basis := math.min(startCylce ? -1 : basis + 1 / barsFromNearestEdgeCircle * 2, 1) // 0 -> 1

shape = math.sqrt(1 - basis * basis)

rad = radius / 2

isOK = barsTillEnd <= barsTillEndFromCircleStart and barsTillEnd > 0

hi = isOK ? (rad + shape * radius) - rad : na

lo = isOK ? (rad - shape * radius) - rad : na

start := barsTillEnd == barsTillEndFromCircleStart ? n -1 : start

end := barsTillEnd == 0 ? start + radius : end

= createOuterCircle(40)

plot(h), plot(l)

🔶 LIMITATIONS

Due to the inability to draw between bars, from time to time, drawings can be slightly off.

Bar-replay can be demanding, since it has to reload on every bar progression. We don't recommend using this script on bar-replay. If you do, please choose the lowest speed and from time to time pause bar-replay for a second. You'll see the script gets reloaded.

🔶 SETTINGS

🔹 TICKERS

Toggle :

• Enabled -> uses the first column with a pre-filled list of Futures Open Interest tickers/symbols

• Disabled -> uses the empty field where you can enter your own ticker/symbol

Pre-filled list : the first column is filled with a list, so you can choose your open interest easily, otherwise you would see COT:088691_F_OI aka Gold Futures Open Interest for example.

If applicable, you will see 3 different COT data:

• COT: Legacy Commitments of Traders report data

• COT2: Disaggregated Commitments of Traders report data

• COT3: Traders in Financial Futures report data

Empty field : When needed, you can pick another ticker/symbol in the empty field at the right and disable the toggle.

Timeframe : Commitments of Traders (COT) data is tallied by the Commodity Futures Trading Commission (CFTC) and is published weekly. Therefore data won't change every day.

Default set TF is Daily

🔹 STYLE

From middle:

• Enabled (default): Drawings start from the middle circle -> towards outer circle is + %change , towards middle of the circle is - %change

• Disabled: Drawings start from the middle POINT of the circle, towards outer circle is + OR -

-> in both options, + %change will be coloured green , - %change will be coloured red .

-> 0 %change will be coloured blue , and when no data is available, this will be coloured gray .

Size circle : options tiny, small, normal, large, huge.

Angle : Only applicable if "From middle" is disabled!

-> sets the angle of the spike:

Show Ticker : Name of ticker, as seen in table, will be added to labels.

Text - fill

• Sets colour for +/- %change

Table

• Sets 2 text colours, size and position

Circles

• Sets the colour of circles, style can be changed in the Style section.

You can make it as crazy as you want:

Ultimate P&L IndicatorHello everyone,

Excited to release this P&L Indicator! Read below for more details.

What it does:

This is an indicator that permits you to track your active P&L live on Tradingview. As well, it provides some insight into DCAing your position by giving you live estimates of your revised DCA if you were to add to your position at various targets/price points.

Who is it for:

I developed it because I trade 100% off of Tradingview but my broker does not support Tradingview integration. So I wanted a way to track my position live on the Tradingview platform without having to constantly reference my broker. I also wanted to be able to set position specific alerts right on Tradingview.

How does it work:

It works by the user manually inputting their trade information, including their DCA, position size and the date and time of position entry. The indicator can provide real time and live DCA adjusted estimates if you were to add to your position at the current stock price, or you can manually calculcate your revised DCA at a specific price target.

The indicator also displays your current and past performance on your position for the duration of the position period:

Elements:

Capabilities:

The indicator is compatible with both futures and share trading.

Option trading is not directly available, however, you can get an idea for your option position P&L by following the 1 option contract = 100 share rule.

So if you have 5 option contracts that you bought at a ticker price of, say, 38$, your average cost or DCA would be 38 and your position size would be 500. This will not be 100% accurate, but will be close enough to give you a feel for your active P&L.

If you are trading futures, you will need to select "Futures Trading" and specify the TIck and Index costs. A cheat sheet has been provided in the tool tip for ES, Oil and MNQ. The default is set for ES1! mini futures at 0.25 ticks per 50$.

Important tips:

1. Select the date and time of your position (optional): This is optional but will provide you with the clearest and most accurate review of how your position has performed, including the highest and lowest (drawdown).

2. Select whether it is a share position or a futures position (this is required).

3. Select whether it is a long or short position (this is required).

4. Input your DCA and position size (this is required).

5. Most importantly, select the ticker your position is based in!

I have also prepared a quick start video which is linked below:

As always, please let me know your comments/questions and feedback for the indicator.

Thanks for checking it out and safe trades everyone!

Accumulated Put/Call Ratio V2This is an updated version of the Accumulated P/C Ratio. Some changes include:

- Pinescript privacy changed from protected to open.

- Utilizes the "request.security_lower_tf" function for weekly and monthly charts.

- Now acquires and sums raw put volume (ticker: PVOL) and call volume (ticker: CVOL) separately, then divides the aggregate put to aggregate call to get the P/C ratio, as opposed to the original version which directly sums the put call ratio (ticker: PCC). Mathematically this calculation makes more sense, but the major drawback of this change seems to be that PVOL and CVOL don't have as much historical data as PCC.

The way to interpret the indicator is the same as the original version - higher values are bullish while lower values are bearish. A solid (0 transparency) bar means that the value is beyond 3 standard deviations within a particular period.

Realtime FootprintThe purpose of this script is to gain a better understanding of the order flow by the footprint. To that end, i have added unusual features in addition to the standard features.

I use "Real Time 5D Profile by LucF" main engine to create basic footprint(profile type) and added some popular features and my favorites.

This script can only be used in realtime, because tradingview doesn't provide historical Bid/Ask date.

Bid/Ask date used this script are up/down ticks.

This script can only be used by time based chart (1m, 5m , 60m and daily etc)

This script use many labels and these are limited max 500, so you can't display many bars.

If you want to display foot print bars longer, turn off the unused sub-display function.

Default setting is footprint is 25 labels, IB count is 1, COT high and Ratio high is 1, COT low and Ratio low is 1 and Delta Box Ratio Volume is 1 , total 29.

plus UA , IB stripes , ladder fading mark use several labels.

///////// General Setting ///////////

Resets on Volume / Range bar

: If you want to use simple time based Resets on, please set Total Volume is 0.

Your timeframe is always the first condition. So if you set Total Volume is 1000, both conditions(Volume >= 1000 and your timeframe start next bar) must be met. (that is, new footprint bar doesn't start at when total volume = exactly 1000).

Ticks per row and Maximum row of Bar

: 1 is minimum size(tick). "Maximum row of Bar" decide the number of rows used in one footprint. 1 row is created from 1 label, so you need to reduce this number to display many footprints (Max label is 500).

Volume Filter and For Calculation and Display

: "Volume Filter" decide minimum size of using volume for this script.

"For Calculation and Display" is used to convert volume to an integer.

This script only use integer to make profile look better (I contained Bid number and Ask number in one row( one label) to saving labels. This require to make no difference in width by the number of digits and this script corresponds integers from 0 to 3 digits).

ex) Symbol average volume size is from 0.0001 to 0.001. You decide only use Volume >= 0.0005 by "Volume Filter".

Next, you convert volume to integer, by setting "For Calculation and Display" is 1000 (0.0005 * 1000 = 5).

If 0.00052 → 5.2 → 5, 0.00058 → 5.8 → 6 (Decimal numbers are rounded off)

This integer is used to all calculation in this script.

//////// Main Display ///////

Footprint, Total, Row Delta, Diagonal Delta and Profile

: "Footprint" display Ask and Bid per row. "Total" display Ask + Bid per row.

"Row Delta" display Ask - Bid per row. "Diagonal Delta" display Ask(row N) - Bid(row N -1) per row.

Profile display Total Volume(Ask + Bid) per row by using Block. Profile Block coloring are decided by Row Delta value(default: positive Row Delta (Ask > Bid) is greenish colors and negative Row Delta (Ask < Bid) is reddish colors.)

Volume per Profile Block, Row Imbalance Ratio and Delta Bull/Bear/Neutral Colors

: "Volume per Profile Block" decide one block contain how many total volume.

ex) When you set 20, Total volume 70 display 3 block.

The maximum number of blocks that can be used per low is 20.

So if you set 20, Total volume 400 is 20 blocks. total volume 800 is 20 blocks too.

"Row Imbalance Ratio" decide block coloring. The row imbalance is that the difference between Ask and Bid (row delta) is large.

default is x3, x2 and x1. The larger the difference, the brighter the color.

ex) Ask 30 Bid 10 is light green. Ask 20 Bid 10 is green. Ask 11 Bid 10 is dark green.

Ask 0 Bid 1 is light red. Ask 1 Bid 2 is red. ask 30 Bid 59 is dark green.

Ask 10 Bid 10 is neutral color(gray)

profile coloring is reflected same row's other elements(Ask, Bid, Total and Delta) too.

It's because one label can only use one text color.

/////// Sub Display ///////

Delta, total and Commitment of Traders

: "Delta" is total Ask - total Bid in one footprint bar. Total is total Ask + total Bid in one footprint bar.

"Commitment of traders" is variation of "Delta". COT High is reset to 0 when current highest is touched. COT Low is opposite.

Basic concept of Delta is to compare price with Delta. Ordinary, when price move up, delta is positive. Price move down is negative delta.

This is because market orders move price and market orders are counted by Delta (although this description is not exactly correct).

But, sometimes prices do not move even though many market orders are putting pressure on price , or conversely, price move strongly without many market orders.

This is key point. Big player absorb market orders by iceberg order(Subdivide large orders and pretend to be small limit orders.

Small limit orders look weak in the order book, but they are added each time you fill, so they are more powerful than they look.), so price don't move.

On the other hand, when the price is moving easily, smart players may be aiming to attract and counterattack to a better price for them.

It's more of a sport than science, and there's always no right response. Pay attention to the relationship between price, volume and delta.

ex) If COT Low is large negative value, it means many sell market orders is coming, but iceberg order is absorbing their attack at limit order.

you should not do buy entry, only this clue. but this is one of the hints.

"Delta, Box Ratio and Total texts is contained same label and its color are "Delta" coloring. Positive Delta is Delta Bull color(green),Negative Delta is Delta Bear Color

and Delta = 0 is Neutral Color(gray). When Delta direction and price direction are opposite is Delta Divergence Color(yellow).

I didn't add the cumulative volume delta because I prefer to display the CVD line on the price chart rather than the number.

Box Ratio , Box Ratio Divisor and Heavy Box Ratio Ratio

: This is not ordinary footprint features, but I like this concept so I added.

Box Ratio by Richard W. Arms is simple but useful tool. calculation is "total volume (one bar) divided by Bar range (highest - lowest)."

When Bull and bear are fighting fiercely this number become large, and then important price move happen.

I made average BR from something like 5 SMA and if current BR exceeds average BR x (Heavy Box Ratio Ratio), BR box mark will be filled.

Box Ratio Divisor is used to good looking display(BR multiplied by Box Ratio Divisor is rounded off and displayed as an integer)

Diagonal Imbalance Count , D IB Mark and D IB Stripes

: Diagonal Imbalance is defined by "Diagonal Imbalance Ratio".

ex) You set 2. When Ask(row N) 30 Bid(row N -1)10, it's 30 > 10*2, so positive Diagonal Imbalance.

When Ask(row N) 4 Bid(row N -1)9, it's 4*2 < 9, so negative Diagonal Imbalance.

This calculation does not use equals to avoid Ask(row N) 0 Bid(row N -1)0 became Diagonal Imbalance.

Ask(row N) 0 Bid(row N -1)0, it's 0 = 0*2, not Diagonal Imbalance. Ask(row N) 10 Bid(row N -1)5, it's 10 = 5*2, not Diagonal Imbalance.

"D IB Mark" emphasize Ask or Bid number which is dominant side(Winner of Diagonal Imbalance calculation), by under line.

"Diagonal Imbalance Count" compare Ask side D IB Mark to Bid side D IB Mark in one footprint.

Coloring depend on which is more aggressive side (it has many IB Mark) and When Aggressive direction and price direction are opposite is Delta Divergence Color(yellow).

"D IB Stripes" is a function that further emphasizes with an arrow Mark, when a DIB mark is added on the same side for three consecutive row. Three consecutive arrow is added at third row.

Unfinished Auction, Ratio Bounds and Ladder fading Mark

: "Unfinished Auction" emphasize highest or lowest row which has both Ask and Bid, by Delta Divergence Color(yellow) XXXXXX mark.

Unfinished Auction sometimes has magnet effect, price may touch and breakout at UA side in the future.

This concept is famous as profit taking target than entry decision.

But, I'm interested in the case that Big player make fake breakout at UA side and trapped retail traders, and then do reversal with retail traders stop-loss hunt.

Anyway, it's not stand alone signal.

"Ratio Bounds" gauge decrease of pressure at extreme price. Ratio Bounds High is number which second highest ask is divided by highest ask.

Ratio Bounds Low is number which second lowest bid is divided by lowest bid. The larger the number, the less momentum the price has.

ex)first footprint bar has Ratio Bounds Low 2, second footprint bar has RBL 4, third footprint bar has RBL 20.

This indicates that the bear's power is gradually diminishing.

"Ladder fading mark" emphasizes the decrease of the value in 3 consecutive row at extreme price. I added two type Marks.

Ask/Bid type(triangle Mark) is Ask/Bid values are decreasing of three consecutive row at extreme price.

Row Imbalance type(Diamond Mark) are row Imbalance values are decreasing of three consecutive row at extreme price.

ex)Third lowest Bid 40, second lowest Bid 10 and lowest Bid 5 have triangle up Mark. That is bear's power is gradually diminishing.

(This Mark only check Bid value at lowest price and Ask value at highest price).

Third highest row delta + 60, second highest row delta + 5, highest delta - 20 have diamond Mark. That is Bull's power is gradually diminishing.

Sub display use Delta colors at bottom of Sub display section.

////// Candle & POC /////////

candle and POC

: Ordinary, "POC" Point of Control is row of largest total volume, but this script'POC is volume weighted average.

This is because the regular POC was visually displayed by the profile ,and I was influenced LucF's ideas.

POC coloring is decided in relation to the previous POC. When current POC is higher than previous POC, color is UP Bar Color(green).

In the opposite case, Down Bar color is used.

POC Divergence Color is used when Current POC is up but current bar close is lower than open (Down price Bar),or in the opposite case.

POC coloring has option also highlight background by Delta Divergence Color(yellow). but bg color is displayed at your time frame current price bar not current footprint bar.

The basic explanation is over.

I add some image to promote understanding basic ideas.

Close Combination Lock Style - Visual AppealThis creates a combination style closing price change on each tick.

It has two theme options, one as silver dials for Dark Theme and the other as black dials for White Theme.

We get fixated to watching closing prices on charts and it gets visually daunting. This creates a combination style price change which updates on each tick, which is quite pleasing to the eye.

When new price is above current center line, it shift the above prices showing ▲ arrow, and if new price is lower, it will shift the bottom prices showing ▼ arrow. If there is no change in price between the ticks, it will show =.

FINRA Daily Short Sale Volume█ OVERVIEW

This indicator displays the Daily Short Sale Volume data reported by FINRA for US Stocks markets, namely NASDAQ, NYSE and NYSE ARCA.

█ CONCEPTS

Daily Short Sale Volume data is different from the bi-monthly Short Interest data also reported by FINRA. Whereas Short Interest represents open positions, Short Sale Volume represents transactions, some of which are executed to offset other trades that will not necessarily result in an open short position reported in Short Interest data. This explains why Short Sale Volume values are always greater than Short Interest ones.

Daily Short Sale Volume provides aggregated volume by security for all short trades executed and reported to FINRA during normal market hours, i.e., media-reported trades. It's important to note that Short Sale Volume is not consolidated with exchange data and excludes trading activity that is not publicly disseminated.

█ HOW TO USE IT

Load the indicator on an active chart (see here if you don't know how).

If the chart's symbol is traded on one of the exchanges for which FINRA provides Daily Short Sale Volume, it will be displayed in columns. The columns are a brighter red when their value is above average.

You can display Short Sale Volume for another symbol by checking the "Other symbol" checkbox of the script settings' "Inputs" tab and selecting the symbol.

The moving average's length is in days, as Short Volume is daily data. You can hide the average in the script's settings "Style" tab.

█ NOTES

You will find more information on the Short Sale Volume Data and Understanding Short Sale Volume Data pages of the FINRA website.

Short Interest data reported by FINRA is not yet available on our platform.

On TradingView, Short Sale Volume data is accessible through tickers using special names. For example, NASDAQ:AAPL's Short Sale Volume data can be loaded on your chart via the FINRA:AAPL_SHORT_VOLUME ticker. The indicator displays the name of the ticker used to fetch data in the bottom left. It can be hidden by unchecking the "Tables" item in the "Style" tab of the script's settings.

Look first. Then leap.

The Strat Screener - yungchoppsThis indicator scan up to 40 tickers of your choice for bullish and bearish Randy Jackson setups. Randy Jackson setups are 2u-2u-2d-2u for bullish cases and 2d-2d-2u-2d for bearish cases. If a ticker has a possible RJ setup, the ticker name will be display on the table depending if it is bullish or bearish. The only thing you need to do it change one of the default tickers to the ones you desire and the table will update if there are any RJ setups. The indicators search for RJ setups on the current timeframe that you are on.

Randy Jackson setups are part of the 'Strat' candlestick analysist. More information about the Strat can be found on the internet and YouTube. This indicator reads the previous candles of every selected ticker and searched for a RJ setup. If one exist, it will update the table with the tickers name. I will add more setups in the future.

This is a screener. This indicator really just makes it easier to scan many indicators at once. Its not hard to use... just place it on the chart and it will do the work for you. Hopefully mods find this enough of a description...

FOMO DRIVEN DEVELOPMENT OPTIONS RETICLE Options Reticle caters to degenerate traders and gamblers worldwide, reaching out for long distant contract expiration and just OTM strike placement.

Generate the overlay yourself using the tradingview-options-reticle CLI tool found on GitHub.

The Options Reticle provides a targeting system overlay that will show a horizontal OTM strike price and verticle expiration target. If you're thinking as soon as the expiration date has passed, this overlay will be useless; you're right but, you can use the options-reticle CLI tool to generate a new overlay from a watchlist exported from TradingView.

OVERLAY FEATURES:

Quick Action PUT (QAP) Mode - When you flip the chart by adding a 0- in front of the symbol, you will see the PUT contract target. Strike Price / Expiration Crosshairs.

Fill Mode - Shows a fill between the historical price and the target strike price. It will show green when ITM and red when OTM. Target information panel - Shows the company name, days till expiration, month and day of expiration, strike price, dollars OTM or ITM, and the contract type.

Emotion Indicator - Shows an exact representation of your feelings based on if you were in the trade. It has an accuracy of 99.9 percent.

QUICK ACTION PUT (QAP) MODE :

This style of reticle is not visible until you flip the chart. The advantage of the (QAP) is that it maintains the same appearance as the standard style of reticle, making PUT contract targeting feel the same. When targeting with (QAP) mode, be aware that the chart prices are reversed. Up is down, and down is up; this can be confusing but will feel normal overtime. Activate QAP mode by appending a 0- to the symbol of the chart. If nothing appears, no put option data was found for that symbol.

CALIBRATING YOUR RETICLE :

The overlay is generated using the options-reticle CLI tool found on GitHub. The adjustment script will parse a watchlist exported from TradingView then download options data for each ticker in the watchlist. The max amount of symbols you can add to a single overlay is about 200. Any more than 200 and the overlay will crash. Luckily, If you use a TradingView watchlist with more than 200 ticker symbols to generate overlays, the options-reticle command-line tool will automatically create multiple overlays with 200 tickers each. You can add multiple overlays to your chart to get all the tickers in the watchlist.

RETICLE GENERATION AND MOUNTING :

Add all the tickers you want to track into a watchlist on Tradingview.

Export the watchlist into a txt file using TradingView's watchlist export list button.

Open the terminal and change to the directory with the downloaded watchlist txt file.

Install options-reticle command tool with pipx. pipx install tradingview-options-reticle.

Run the command options-reticle download --watchlist {name of watchlist.txt file}. This will download the options data to an options_data.toml in the same directory as the watchlist txt file.

Run the command options-reticle build --options-data-input-path options_data.toml. This will generate the overlay scripts. If the watch list has more than 200 ticker symbols, it will generate a separate overlay script for every 200 ticker symbol chunk.

Copy and paste each of the generated overlay scripts one at a time into the Pine Editor on TradingView, then click the Add to Chart button. Make sure you copy the entire code.

FUTURE FEATURES :

Give the choice to generate PUT option contracts without using QAP mode. This option will allow you to use the input settings to change the contract type without flipping the chart.

Max OTM target argument - This will allow the option-reticle CLI to generate overlays with deeper OTM contracts. It currently only searches for the first OTM contract.

Add the ability to change the crosshair line type.

vstop5 (RA)Upgrade standart Volatility Stop with 5 fixed values for selected tickers.

When switching between tickers - VStop multiplier will be changed to desired fixed value for fixed tickers.

If nothing mached - will be used standart value

See the example of setting here

As You can see on screenshot 5 different VStops can be set up for different tickers.

and as a result:

Доработка стандартного индикатора VStop, но с возможностью зафиксировать для 5-ти разных инструментов свое значение мультипликатора.

Далее при переключении с одного инструмента на другой - значение Мультипликатора VStop будет меняться в соответствии с сохраненными привязанными настройками. для всех НЕ привязанных инструментов - будет использовано значение Мультипликатора по умолчанию, которое также задается в Настройках.

Пример настроек тут

Market Delta [Makit0]MARKET DELTA INDICATOR v0.5 beta

Market Delta is suitable for daytrading on intraday timeframes, is a volume based indicator which allows to see the UP VOLUME vs the DOWN VOLUME, the DELTA (difference) and the CUMULATIVE DELTA (cumulative sum of difference) between them

This indicator is based on contracts volume (data avaiable), not in ask/bid volume (data not avaiable)

The up/down volume is calculated at each candle as follows:

- calculate the ticks of the range, top wick and bottom wick

- calculate the ticks up and ticks down to get the total ticks of the candle

- calculate the volume per tick as total volume divided by total ticks

- calculate the up and down volume as volume per tick multiplied by up ticks and down ticks

The delta is calculated as volume up minus volume down

The cumulative delta is a cumulative sum of delta and is resetted to 0 twice a day at the globex open and at the us cash open

By default the indicator plots the 'CANDLE MODE' which is useful for charting the cumulative volume to find out support and resistance zones where the volume is rejected or pass thru, as the volume moves so does the price, price always follows the volume, price goes away from where volume dries and price auctions comfortable where is plenty of volume, in a way PRICE FEEDS ON VOLUME

An indication about the plotting style in the volume, delta and cumulative delta modes: I can't use histogram as intended due a bug at autoresizing the scale in the candle mode, so the styles used are areabr and circles.

FEATURES

- Plot volume in one of four modes: Volume Up/Down, Delta, Cumulative Delta, Cumulative Delta as Candles

- Cumulative delta resetted twice a day (globex and cash open)

- Show a base line at 0

SETTINGS

- Mode: select one of the four volume output modes: Volume, Delta, Cumulative Delta and Candles. Candles by default

- Show zero line: show/hide the zero base line. False by default.

HOW TO SETTING UP THE INDICATOR:

BE AWARE, by default the indicator settings are configured for using the Cumulative Delta Candle Mode

- Candles Mode Settings: configured by default, mode candles and zero line off

- Volume, Delta, Cumulative Delta Mode Settings: select the mode you want and switch on/off the zero line

GOOD LUCK AND HAPPY TRADING

Trading Range Indicator - TRISimple script made to identify trading ranges in any timeframe

The oscillator bounces between 1 and 0. 1 means that the current asset is in a trading range and 0 meaning it is not.

The determination of a trading range is determined by the following:

ATR(14)40 and RSI<60

ADX<25

Due to all 3 having to be fulfilled in order for the oscillator to show there is a trading range, this causes a problem where 2 of the conditions are fulfilled and therefore still shows 0 on the oscillator, however, the asset could very well be in a trading range.

So what in the world do you use this for if there is such a significant margin of error?

Since all 3 conditions need to be fulfilled in order for it to be considered a trading range, this gives a very strong indicator of said trading ranges. So if a person is looking at individual stock tickers or the SPY index ticker, then when the oscillator reads a 1, it could be ideal to open an Iron Condor on said ticker. This means that this indicator is not well suiting for traditional long and short stock positions, but rather it is made for options traders who by using an Iron Condor can make money of a range-bound market.

Acc/Dist. Cloud with Fractal Deviation Bands by @XeL_ArjonaACCUMULATION / DISTRIBUTION CLOUD with MORPHIC DEVIATION BANDS

Ver. 2.0.beta.23:08:2015

by Ricardo M. Arjona @XeL_Arjona

DISCLAIMER

The Following indicator/code IS NOT intended to be a formal investment advice or recommendation by the author, nor should be construed as such. Users will be fully responsible by their use regarding their own trading vehicles/assets.

The embedded code and ideas within this work are FREELY AND PUBLICLY available on the Web for NON LUCRATIVE ACTIVITIES and must remain as is.

Pine Script code MOD's and adaptations by @XeL_Arjona with special mention in regard of:

Buy (Bull) and Sell (Bear) "Power Balance Algorithm by Vadim Gimelfarb published at Stocks & Commodities V. 21:10 (68-72).

Custom Weighting Coefficient for Exponential Moving Average (nEMA) adaptation work by @XeL_Arjona with contribution help from @RicardoSantos at TradingView @pinescript chat room.

Morphic Numbers (PHI & Plastic) Pine Script adaptation from it's algebraic generation formulas by @XeL_Arjona

Fractal Deviation Bands idea by @XeL_Arjona

CHANGE LOG:

ACCUMULATION / DISTRIBUTION CLOUD: I decided to change it's name from the Buy to Sell Pressure. The code is essentially the same as older versions and they are the center core (VORTEX?) of all derived New stuff which are:

MORPHIC NUMBERS: The "Golden Ratio" expressed by the result of the constant "PHI" and the newer and same in characteristics "Plastic Number" expressed as "PN". For more information about this regard take a look at: HERE!

CUSTOM(K) EXPONENTIAL MOVING AVERAGE: Some code has cleaned from last version to include as custom function the nEMA , which use an additional input (K) to customise the way the "exponentially" is weighted from the custom array. For the purpose of this indicator, I implement a volatility algorithm using the Average True Range of last 9 periods multiplied by the morphic number used in the fractal study. (Golden Ratio as default) The result is very similar in response to classic EMA but tend to accelerate or decelerate much more responsive with wider bars presented in trending average.

FRACTAL DEVIATION BANDS: The main idea is based on the so useful Standard Deviation process to create Bands in favor of a multiplier (As John Bollinger used in it's own bands) from a custom array, in which for this case is the "Volume Pressure Moving Average" as the main Vortex for the "Fractallitly", so then apply as many "Child bands" using the older one as the new calculation array using the same morphic constant as multiplier (Like Fibonacci but with other approach rather than %ratios). Results are AWSOME! Market tend to accelerate or decelerate their Trend in favor of a Fractal approach. This bands try to catch them, so please experiment and feedback me your own observations.

EXTERNAL TICKER FOR VOLUME DATA: I Added a way to input volume data for this kind of study from external tickers. This is just a quicky-hack given that currently TradingView is not adding Volume to their Indexes so; maybe this is temporary by now. It seems that this part of the code is conflicting with intraday timeframes, so You are advised.

This CODE is versioned as BETA FOR TESTING PROPOSES. By now TradingView Admins are changing lot's of things internally, so maybe this could conflict with correct rendering of this study with special tickers or timeframes. I will try to code by itself just the core parts of this study in order to use them at discretion in other areas. ALL NEW IDEAS OR MODIFICATIONS to these indicator(s) are Welcome in favor to deploy a better and more accurate readings. I will be very glad to be notified at Twitter or TradingView accounts at: @XeL_Arjona

ATR Risk Display - Multi FuturesWhat This Does

I got tired of manually calculating my ATR stops and risk for different futures contracts, especially when switching between ES, NQ, and their micro versions. This indicator automatically detects what futures symbol you're trading and shows you the exact tick count and dollar risk for your stop loss.

The Problem It Solves

If you trade futures with ATR-based stops, you know the hassle:

Different contracts have different tick values

You need to calculate position risk in dollars

Switching between symbols means redoing all the math

Renko charts make it even more confusing since ATR needs to come from regular candles

This handles all of that automatically.

Key Features

Auto-detects futures symbols - ES, NQ, YM, RTY, GC, CL, and all the micros (MES, MNQ, etc.)

Shows everything you need in one line: ATR(timeframe) × multiplier = X ticks ($XXX)

Works on Renko charts - pulls ATR from regular timeframe charts (super important if you use Renko)

Adjustable position sizing - set your contract count and see total risk instantly

Clean, minimal display - just the info you need, no clutter

How to Use

Add it to any futures chart

Set your preferred ATR timeframe (I use 5-minute)

Set your ATR multiplier (I use 1.5x for my stops)

Set your contract size

That's it - the indicator handles the rest

The display will show something like: "ES ATR(5) × 1.5 = 12 ticks ($150)"

Settings Explained

ATR Timeframe: What timeframe to calculate ATR from (always uses regular candles, even on Renko)

ATR Multiplier: How many ATRs for your stop (1.5 is common, 2.0 for wider stops)

Number of Contracts: Your position size for risk calculation

Auto-Detect Symbol: Leave on unless you want to manually override

Supported Futures

Full size: ES, NQ, YM, RTY, GC, CL, ZB, ZN, 6E, 6J

Micros: MES, MNQ, MYM, M2K, MGC, MCL

Notes

Made this primarily for my own ES trading but figured others might find it useful

The tick values are based on standard CME specs

If you trade other futures, you can modify the code to add them

Works great alongside level indicators for risk management

Why This Exists

I use ATR trailing stops on all my trades and got tired of doing mental math every time I switched between charts or contracts. Especially useful if you trade both full-size and micro contracts - the risk difference is huge and easy to mess up.

Hope this helps your trading! Feel free to suggest improvements.