ATRvsDTR + ADR Zone + SSS50%This Script is to be used for intra day as far as the adr zones. The adr zones are used as support and resistance but also can be used to determine whether the stock is breaking out or not. Also being that the adr zones are calculated using a 5 or 10 day period unless you change the settings, and are set when price opens. It does really help you know whether a stock is moving more than it does on average to me it just signifies its directional. So I added the atr vs dtr so you can see what a stock moves on average versus what it has moved today.

The atr period is calculated based on the daily period unless you change the settings. I added to the original script 3 more percentages the atr vs dtr will change as it goes higher so that you can be aware when the stock is getting closer to moving 100% of its atr. Even though a stock breaks above or below the adr that doesn't mean it has moved more than it normally moves.

I also have the weekly open on the script as I trade the strat and I want to know, at what price the the week will change from bearish to bullish and vice versa. So that I can understand the trend when I am trading intraday.

The 50% lines were added for Sara strat snipers 50% rule and you can change the timeframes on them. This is used to know whether a candle will go 3. This also can help with retracements vs reversals, because in traditional technical analysis 50% is around where people start think its a reversal more so than a retracement.

I believe the script will be very help as it can show you price being directional but can also let you know when the stock is getting close to moving more than it normally has or if it has moved more than it normally has. As well as being able to see if something is a retracement vs a reversal. I trade TheStrat strategy so this can be very helpful in that regard

The 50% retracement levels are default 1h and daily. You can change them and whether or not they show

In the example chart you can see we are below weekly open which is bearish and you can also see where price reverses out of the upper adr zone. As well as how much of the atr we have moved on this day in time.

在脚本中搜索"蔚山现代vs川崎前锋"

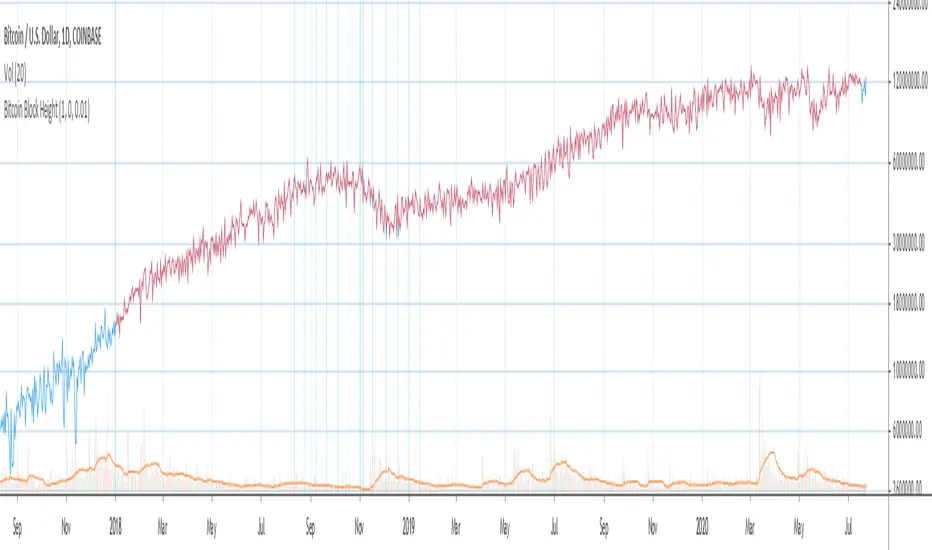

Bitcoin Block Height (Total Blocks)Bitcoin Block Height by RagingRocketBull 2020

Version 1.0

Differences between versions are listed below:

ver 1.0: compare QUANDL Difficulty vs Blockchain Difficulty sources, get total error estimate

ver 2.0: compare QUANDL Hash Rate vs Blockchain Hash Rate sources, get total error estimate

ver 3.0: Total Blocks estimate using different methods

--------------------------------

This indicator estimates Bitcoin Block Height (Total Blocks) using Difficulty and Hash Rate in the most accurate way possible, since

QUANDL doesn't provide a direct source for Bitcoin Block Height (neither QUANDL:BCHAIN, nor QUANDL:BITCOINWATCH/MINING).

Bitcoin Block Height can be used in other calculations, for instance, to estimate the next date of Bitcoin Halving.

Using this indicator I demonstrate:

- that QUANDL data is not accurate and differ from Blockchain source data (industry standard), but still can be used in calculations

- how to plot a series of data points from an external csv source and compare it with another source

- how to accurately estimate Bitcoin Block Height

Features:

- compare QUANDL Difficulty source (EOD, D1) with external Blockchain Difficulty csv source (EOD, D1, embedded)

- show/hide Quandl/Blockchain Difficulty curves

- show/hide Blockchain Difficulty candles

- show/hide differences (aqua vertical lines)

- show/hide time gaps (green vertical lines)

- count source differences within data range only or for the whole history

- multiply both sources by alpha to match before comparing

- floor/round both matched sources when comparing

- Blockchain Difficulty offset to align sequences, bars > 0

- count time gaps and missing bars (as result of time gaps)

WARNING:

- This indicator hits the max 1000 vars limit, adding more plots/vars/data points is not possible

- Both QUANDL/Blockchain provide daily EOD data and must be plotted on a daily D1 chart otherwise results will be incorrect

- current chart must not have any time gaps inside the range (time gaps outside the range don't affect the calculation). Time gaps check is provided.

Otherwise hardcoded Blockchain series will be shifted forward on gaps and the whole sequence become truncated at the end => data comparison/total blocks estimate will be incorrect

Examples of valid charts that can run this indicator: COINBASE:BTCUSD,D1 (has 8 time gaps, 34 missing bars outside the range), QUANDL:BCHAIN/DIFF,D1 (has no gaps)

Usage:

- Description of output plot values from left to right:

- c_shifted - 4x blockchain plotcandles ohlc, green/black (default na)

- diff - QUANDL Difficulty

- c_shifted - Blockchain Difficulty with offset

- QUANDL Difficulty multiplied by alpha and rounded

- Blockchain Difficulty multiplied by alpha and rounded

- is_different, bool - cur bar's source values are different (1) or not (0)

- count, number of differences

- bars, total number of bars/data points in the range

- QUANDL daily blocks

- Blockchain daily blocks

- QUANDL total blocks

- Blockchain total blocks

- total_error - difference between total_blocks estimated using both sources as of cur bar, blocks

- number_of_gaps - number of time gaps on a chart

- missing_bars - number of missing bars as result of time gaps on a chart

- Color coding:

- Blue - QUANDL data

- Red - Blockchain data

- Black - Is Different

- Aqua - number of differences

- Green - number of time gaps

- by default the indicator will show lots of vertical aqua lines, 138 differences, 928 bars, total error -370 blocks

- to compare the best match of the 2 sources shift Blockchain source 1 bar into the future by setting Blockchain Difficulty offset = 1, leave alpha = 0.01 =>

this results in no vertical aqua lines, 0 differences, total_error = 0 blocks

if you move the mouse inside the range some bars will show total_error = 1 blocks => total_error <= 1 blocks

- now uncheck Round Difficulty Values flag => some filled aqua areas, 218 differences.

- now set alpha = 1 (use raw source values) instead of 0.01 => lots of filled aqua areas, 871 differences.

although there are many differences this still doesn't affect the total_blocks estimate provided Difficulty offset = 1

Methodology:

To estimate Bitcoin Block Height we need 3 steps, each step has its own version:

- Step 1: Compare QUANDL Difficulty vs Blockchain Difficulty sources and estimate error based on differences

- Step 2: Compare QUANDL Hash Rate vs Blockchain Hash Rate sources and estimate error based on differences

- Step 3: Estimate Bitcoin Block Height (Total Blocks) using different methods in the most accurate way possible

QUANDL doesn't provide block time data, but we can calculate it using the Hash Rate approximation formula:

estimated Hash rate/sec H = 2^32 * D / T, where D - Difficulty, T - block time, sec

1. block time (T) can be derived from the formula, since we already know Difficulty (D) and Hash Rate (H) from QUANDL

2. using block time (T) we can estimate daily blocks as daily time / block time

3. block height (total blocks) = cumulative sum of daily blocks of all bars on the chart (that's why having no gaps is important)

Notes:

- This code uses Pinescript v3 compatibility framework

- hash rate is in THash/s, although QUANDL falsely states in description GHash/s! THash = 1000 GHash

- you can't read files, can only embed/hardcode raw data in script

- both QUANDL and Blockchain sources have no gaps

- QUANDL and Blockchain series are different in the following ways:

- all QUANDL data is already shifted 1 bar into the future, i.e. prev day's value is shown as cur day's value => Blockchain data must be shifted 1 bar forward to match

- all QUANDL diff data > 1 bn (10^12) are truncated and have last 1-2 digits as zeros, unlike Blockchain data => must multiply both values by 0.01 and floor/round the results

- QUANDL sometimes rounds, other times truncates those 1-2 last zero digits to get the 3rd last digit => must use both floor/round

- you can only shift sequences forward into the future (right), not back into the past (left) using positive offset => only Blockchain source can be shifted

- since total_blocks is already a cumulative sum of all prev values on each bar, total_error must be simple delta, can't be also int(cum()) or incremental

- all Blockchain values and total_error are na outside the range - move you mouse cursor on the last bar/inside the range to see them

TLDR, ver 1.0 Conclusion:

QUANDL/Blockchain Difficulty source differences don't affect total blocks estimate, total error <= 1 block with avg 150 blocks/day is negligible

Both QUANDL/Blockchain Difficulty sources are equally valid and can be used in calculations. QUANDL is a relatively good stand in for Blockchain industry standard data.

Links:

QUANDL difficulty source: www.quandl.com

QUANDL hash rate source: www.quandl.com

Blockchain difficulty source (export data as csv): www.blockchain.com

RedK_Supply/Demand Volume Viewer v1Background

============

VolumeViewer is a volume indicator, that offers a simple way to estimate the movement and balance (or lack of) of supply & demand volume based on the shape of the price bar. i put this together few years ago and i have a version of this published for another platform under different names (Directional Volume, BetterVolume) in case you come across them

what is V.Viewer

=====================

The idea here is to find a "simple proxy" for estimating the demand or supply portions of a volume bar - these 2 forces have the potential to affect the current price trend so we want an easy way to track them - or to understand if a stock is in accumulation or distribution - we want to do this without having access to Level II or bid/ask data, and without having to get into the complexity of exploring the lower timeframe price & volume data

- to achieve that, we depend on a simple assumption, that the volume associated with an up move is "demand" and the volume associated with a down move is "Supply". so we basically extrapolate these supply and demand values based on how the bar looks like - a full "green" price bar / candle will be considered 100% demand, and a full "red" price bar will be considered 100% supply - a bar that opens and closes at the same level will be 50/50 split between supply & demand.

- you may say this is a "too simple" of an assumption to make, but believe me, it works :) at least at the basic scenario we need here: i'm just exploring the volume movement and finding key levels - and it provides a good improvement compared to the classic way we see volume on a chart - which is still available here in VolumeViewer.

in all cases, i consider this to be work in progress, so i'd welcome any ideas to improve (without getting too complicated) - there's already a host of great volume-based indicators that will do the multi timeframe drill down, but that's not my scope here.

Technical Jargon & calculation

===========================

1. first we calculate a score % for the volume portion that is considered demand based on the bar shape

skip this part if it sounds too technical => if you're into coding indicators, you would probably know there are couple of different concepts for that algorithm - for example, the one used in Balance Of Power formula - which i'm a big fan of - but the one i use here is different. (how?) this is my own, ant it simply applies double weight for the "wick" parts of a price bar compared to the "body of the bar" -- i did some side-by-side comparison in past and decided this one works better. you can change it in the code if you like

2. after calculating the Bull vs Bears portion of volume, we take a moving average of both for the length you set, to come up with what we consider to be the Demand vs Supply - as usual, i use a weighted moving average (WMA) here.

3. the balance or net volume between these 2 lines is calculated, then we apply a final smoothing and that's the main plot we will get

4. being a very visual person, i did my best to build up the visuals in the correct order - then also to ensure the "study title" bar is properly organized and is simple and useful (Full Volume, Supply, Demand, Net Volume).

- i wish there was a way in Pine to hide a value that i still need to visually plot but don't want it showing its value on the study title bar, but couldn't find it. so the last plot value is repeated twice.

How to use

===========

- V.Viewer is set up to show the simplified view by default for simplicity. so when you first add it to a chart, you will get only the supply vs demand view you can see in the middle pane in the above chart

- Optional / detailed mode: go into the settings, and expose all other plots, you will be able to add the classic volume histogram, and the Supply / Demand lines - note these 2 lines will be overlay-ed on top of each other - this provides an easy way to see who is in control - especially if you change the display of these 2 lines into "area" style. This is what is showing in the lower pane in the above chart.

** Exploring Key Price Levels

- the premise is, at spots where there's big lack of balance, that's where to expect to find key price levels (support / resistance) and these price levels will come into play in future so can be used to set entry / exit targets for our trades - see the example in the AAPL chart where you can easily locate these "balance or reversal levels" using the tops/bottoms/zero-crossings from the Net Volume line

** Use for longer-term Price Analysis

- we can also use this simple indicator to gain more insights (at a high level) of the price in terms of accumulation vs distribution and if the sellers or buyers are in control - for example, in the above AAPL chart, V.Viewer tells us that buyers have been in control since October 19 - even during the recent drop, demand continued to be in play - compare that to DIS chart below for the same period, where it shows that the market was dumping DIS thru the weakness. DIS was bleeding red most of the time

Final thoughts

=============

- V.Viewer is an attempt to enhance the way we see and use Volume by leveraging the shape of the price bar to estimate volume supply & demand - and the Net between the 2

- it will work for stocks and other instruments as long as there's volume data

- note that V.Viewer does not track trend. each bar is taken in isolation of prior bars - the price may be going down and V.Viewer is showing supply going up (absorption scenario?) - so i suggest you do not use it to make decisions without consulting other trend / momentum indicators - of course this is a possible improvement idea, or can be implemented in another indicator, add in trend somehow, or maybe think of making this a +100 / -100 Oscillator .. feel free to play with these thoughts

- all thoughts welcome - if this is useful to you in your trading, please share with other trades here to learn from each other

- the code is commented - please feel free to use it as you like, or build things on top of it - but please continue to credit the author of this code :)

good luck!

-

Chiki-Poki BFXLS Longs Shorts Abs Normalized Volume Pro by RRBChiki-Poki BFXLS Longs vs Shorts Absolute Normalized Volume Value Pro by RagingRocketBull 2018

Version 1.0

This indicator displays Longs vs Shorts in a side by side graph, shows volume's absolute price value and normalized volume of Longs/Shorts for the current asset. This allows for more accurate L/S comparisons (like a log scale for volume) since volume on spot exchanges (Bitstamp, Bitfinex, Coinbase etc) is measured in coins traded, not USD traded. Similarly, L/S is usually the amount of coins in open L/S positions, not their total USD value. On Bitmex and other futures exchanges volume is measured in USD traded, so you don't need to apply the Volume Absolute Price Value checkbox to compare L/S. You should always check first whether your source is measured in coins or USD.

Chiki-Poki BFXLS primarily uses *SHORTS/LONGS feeds from Bitfinex for the current crypto asset, but you can specify custom L/S source tickers instead.

This 2-in-1 works both in the Main Chart and in the indicator pane below. You can switch between Main/Sub Window panes using RMB on the indicator's name and selecting Move To/Pane Above/Below.

This indicator doesn't use volume of the current asset. It uses L/S ticker's OHLC as a source for SHORTS/LONGS volumes instead. Essentially L/S => L/S Volume == L/S

Features:

- Display Longs vs Shorts side by side graph for the current crypto asset, i.e. for BTCUSD - BTCUSDLONGS/BTCUSDSHORTS, for ETHUSD - ETHUSDLONGS/ETHUSDSHORTS etc.

- Use custom OHLC ticker sources for Longs/Shorts from different exchanges/crypto assets with/without exchange prefix.

- Plot Longs/Shorts as lines or candles

- Show/Hide L/S, Diff, MAs, ATH/ATL

- Use Longs/Shorts Volume Absolute Price Value (Price * L/S Volume) instead of Coins Traded in open L/S positions to compare total L/S value/capitalization

- Normalize L/S Volume using Price / Price MA / L/S Volume MA

- Supports any existing type of MA: SMA, EMA, WMA, HMA etc

- Volume Absolute Price Value / Normalize also works on candles

- Oscillator mode with negative axis (works in both Main Chart/Subwindow panes).

- Highlight L/S Volume spikes above L/S MAs in both lines/oscillator.

- Change L/S MA color based on a number of last rising/falling L/S bars, colorize candles

- Display L/S volume as 1000s, mlns, or blns using alpha multiplier

1. based on BFXLS Longs vs Shorts and Compare Style, uses plot*, security and custom hma functions

2. swma has a fixed length = 4, alma and linreg have additional offset and smoothing params

Notes:

- Make sure that Left Price Scale shows up with Auto Fit Data enabled. You can reattach indicator to a different scale in Style.

- It is not recommended to switch modes multiple times due to TradingView's scale reattachment bugs. You should switch between Main Chart and Sub Window only once.

- When the USD price of an asset is lower you can trade more coins but capitalization value won't be as significant as when there are less coins for a higher price. Same goes for Shorts/Longs.

Current ATH in shorts doesn't trigger a squeeze because its total value is now far less than before and we are in a bear market where it's normal to have a higher number of shorts.

- You should always subtract Hedged L/S from L/S because hedged positions are temporary - used to preserve the value of the main position in the opposite direction and should be disregarded as such.

- Low margin rates increase the probability of a move in an underlying direction because it is cheaper. High margin rates => the market is anticipating a move in this direction, thus a more expensive rate. Sudden 5-10x rate raises imply a possible reversal soon. high - 0.1%, avg - 0.01-0.02%, low - 0.001-0.005%

You can also check out:

- BFXLS Longs/Shorts on BFXData

- Bitfinex L/S margin rates and Hedged L/S on datamish

- Bitmex L/S on Coinfarm.online

Advanced Confluence DashboardAdvanced Confluence Dashboard - Multi-Indicator Technical Analysis Tool

OVERVIEW

The Advanced Confluence Dashboard is a comprehensive technical analysis tool designed to help traders identify high-probability trade setups by tracking multiple technical indicators simultaneously. The indicator displays up to 13 different technical confluences in an easy-to-read dashboard format, providing both individual signals and an overall market bias percentage. Switch between full table view and condensed view for maximum chart flexibility.

FEATURES

- 13 Technical Confluences: RSI, VWAP, EMA Cross (9/21), MACD, Stochastic, Trend (50 EMA), Bollinger Bands, ADX Strength, Price Momentum, Volume Breakout, VWAP Bands, 200 EMA, and Price Action (Higher Highs/Lower Lows)

- Real-time Confluence Scoring: Automatically calculates bullish vs bearish signal strength

- Multi-Timeframe Support: Analyze indicators on any timeframe while viewing your chart on another

- Customizable Display: Toggle individual indicators on/off, adjust table position, size, and transparency

- ATR Information: Optional ATR display for volatility-based position sizing

- Condensed View Mode: Ultra-minimal display showing only confluence score and ATR (perfect for scalpers who want maximum chart visibility)

- Full Table View: Detailed breakdown of each indicator's value and signal

- Color-Coded Signals: Green (bullish), red (bearish), white (neutral) for instant visual clarity

HOW IT WORKS

The indicator evaluates each enabled technical indicator and assigns it either a bullish or bearish signal based on its current state. The confluence score shows how many indicators are aligned in each direction, giving you a clear percentage-based view of market bias. For example, if 8 out of 13 indicators are bullish, you'll see a 62% LONG BIAS signal.

DISPLAY MODES

Full View: Shows all enabled indicators with their current values and signals in a detailed table format. Perfect for understanding exactly which indicators are bullish or bearish and why.

Condensed View: Shows only the confluence score (e.g., "4/13 LONG | 9/13 SHORT - SHORT BIAS 69%") and optional ATR information. This minimal display keeps your chart clean while still providing the essential confluence data you need for quick trading decisions. Ideal for scalpers and traders who want maximum chart space.

CONFLUENCES EXPLAINED

- RSI: Momentum oscillator (>50 bullish, <50 bearish, shows overbought/oversold)

- VWAP: Volume-weighted average price (above = bullish, below = bearish)

- EMA Cross: Fast EMA (9) vs Slow EMA (21) with price position

- MACD: Trend-following momentum (line above signal = bullish)

- Stochastic: Momentum oscillator (>50 bullish, <50 bearish)

- Trend (50 EMA): Price position relative to 50-period EMA

- Bollinger Bands: Volatility and mean reversion (above middle = bullish)

- ADX Strength: Trend strength indicator (shows strong trends)

- Price Momentum: Rate of price change over specified period

- Volume Breakout: Detects unusual volume with directional bias

- VWAP Bands: Standard deviation bands around VWAP

- 200 EMA: Long-term trend indicator

- Price Action: Higher Highs and Lower Lows pattern detection

SETTINGS

Timeframe Settings:

- Indicator Timeframe: Analyze indicators on a different timeframe than your chart

Display Options:

- Condensed View: Toggle between full table and minimal display

- Show ATR Info: Display/hide ATR information

- Table Position: 9 positions (top/middle/bottom + left/center/right)

- Text Size: Auto, tiny, small, normal, large, huge

- Table Transparency: 0-100%

- Border Width: 1-5 pixels

Confluence Toggles:

- Enable/disable any of the 13 confluences individually

- Confluence score automatically adjusts based on enabled indicators

Indicator Settings:

- RSI Length (default: 14)

- ATR Length (default: 14)

- Fast/Slow EMA (default: 9/21)

- Trend EMA (default: 50)

- Volume SMA Length (default: 20)

- Volume Breakout Multiplier (default: 2.0x)

- Bollinger Bands Length/StdDev (default: 20/2.0)

- ADX Length (default: 14)

- ADX Strength Threshold (default: 25)

- Momentum Length (default: 10)

IDEAL USE CASES

- Scalping: Quick identification of confluence for fast entries/exits - use condensed view for clean charts

- Day Trading: Multi-timeframe analysis for intraday setups

- Swing Trading: Confirmation of longer-term bias

- Risk Management: Higher confluence = higher probability trades

- Trade Filtering: Only take trades when confluence reaches your threshold

- Multi-Monitor Setups: Use condensed view on execution charts, full view on analysis charts

HOW TO USE

1. Add the indicator to your chart

2. Toggle on/off the confluences you prefer to use

3. Choose between Full View (detailed) or Condensed View (minimal)

4. Adjust the table position and size to your preference

5. Look for high confluence percentages (70%+ is strong bias)

6. Use the individual indicator signals (full view) to understand market structure

7. Combine with your trading strategy for entry/exit confirmation

TIPS

- Use Condensed View when scalping to keep your chart clean and uncluttered

- Switch to Full View when you need to analyze which specific indicators are conflicting

- Higher confluence doesn't guarantee success - always use proper risk management

- Consider using 60%+ confluence as a minimum threshold for trades

- Pay attention to which specific indicators are aligned vs conflicting

- Use the ATR display for quick reference on position sizing

- Experiment with different timeframes to find what works for your style

- Disable indicators you don't use to simplify your confluence scoring

DISCLAIMER

This indicator is for educational and informational purposes only. It does not constitute financial advice, investment advice, trading advice, or any other type of advice. Trading and investing in financial markets involves substantial risk of loss and is not suitable for every investor. Past performance is not indicative of future results. Always do your own research and consult with a qualified financial advisor before making any investment decisions.

Adaptive Genesis Engine [AGE]ADAPTIVE GENESIS ENGINE (AGE)

Pure Signal Evolution Through Genetic Algorithms

Where Darwin Meets Technical Analysis

🧬 WHAT YOU'RE GETTING - THE PURE INDICATOR

This is a technical analysis indicator - it generates signals, visualizes probability, and shows you the evolutionary process in real-time. This is NOT a strategy with automatic execution - it's a sophisticated signal generation system that you control .

What This Indicator Does:

Generates Long/Short entry signals with probability scores (35-88% range)

Evolves a population of up to 12 competing strategies using genetic algorithms

Validates strategies through walk-forward optimization (train/test cycles)

Visualizes signal quality through premium gradient clouds and confidence halos

Displays comprehensive metrics via enhanced dashboard

Provides alerts for entries and exits

Works on any timeframe, any instrument, any broker

What This Indicator Does NOT Do:

Execute trades automatically

Manage positions or calculate position sizes

Place orders on your behalf

Make trading decisions for you

This is pure signal intelligence. AGE tells you when and how confident it is. You decide whether and how much to trade.

🔬 THE SCIENCE: GENETIC ALGORITHMS MEET TECHNICAL ANALYSIS

What Makes This Different - The Evolutionary Foundation

Most indicators are static - they use the same parameters forever, regardless of market conditions. AGE is alive . It maintains a population of competing strategies that evolve, adapt, and improve through natural selection principles:

Birth: New strategies spawn through crossover breeding (combining DNA from fit parents) plus random mutation for exploration

Life: Each strategy trades virtually via shadow portfolios, accumulating wins/losses, tracking drawdown, and building performance history

Selection: Strategies are ranked by comprehensive fitness scoring (win rate, expectancy, drawdown control, signal efficiency)

Death: Weak strategies are culled periodically, with elite performers (top 2 by default) protected from removal

Evolution: The gene pool continuously improves as successful traits propagate and unsuccessful ones die out

This is not curve-fitting. Each new strategy must prove itself on out-of-sample data through walk-forward validation before being trusted for live signals.

🧪 THE DNA: WHAT EVOLVES

Every strategy carries a 10-gene chromosome controlling how it interprets market data:

Signal Sensitivity Genes

Entropy Sensitivity (0.5-2.0): Weight given to market order/disorder calculations. Low values = conservative, require strong directional clarity. High values = aggressive, act on weaker order signals.

Momentum Sensitivity (0.5-2.0): Weight given to RSI/ROC/MACD composite. Controls responsiveness to momentum shifts vs. mean-reversion setups.

Structure Sensitivity (0.5-2.0): Weight given to support/resistance positioning. Determines how much price location within swing range matters.

Probability Adjustment Genes

Probability Boost (-0.10 to +0.10): Inherent bias toward aggressive (+) or conservative (-) entries. Acts as personality trait - some strategies naturally optimistic, others pessimistic.

Trend Strength Requirement (0.3-0.8): Minimum trend conviction needed before signaling. Higher values = only trades strong trends, lower values = acts in weak/sideways markets.

Volume Filter (0.5-1.5): Strictness of volume confirmation. Higher values = requires strong volume, lower values = volume less important.

Risk Management Genes

ATR Multiplier (1.5-4.0): Base volatility scaling for all price levels. Controls whether strategy uses tight or wide stops/targets relative to ATR.

Stop Multiplier (1.0-2.5): Stop loss tightness. Lower values = aggressive profit protection, higher values = more breathing room.

Target Multiplier (1.5-4.0): Profit target ambition. Lower values = quick scalping exits, higher values = swing trading holds.

Adaptation Gene

Regime Adaptation (0.0-1.0): How much strategy adjusts behavior based on detected market regime (trending/volatile/choppy). Higher values = more reactive to regime changes.

The Magic: AGE doesn't just try random combinations. Through tournament selection and fitness-weighted crossover, successful gene combinations spread through the population while unsuccessful ones fade away. Over 50-100 bars, you'll see the population converge toward genes that work for YOUR instrument and timeframe.

📊 THE SIGNAL ENGINE: THREE-LAYER SYNTHESIS

Before any strategy generates a signal, AGE calculates probability through multi-indicator confluence:

Layer 1 - Market Entropy (Information Theory)

Measures whether price movements exhibit directional order or random walk characteristics:

The Math:

Shannon Entropy = -Σ(p × log(p))

Market Order = 1 - (Entropy / 0.693)

What It Means:

High entropy = choppy, random market → low confidence signals

Low entropy = directional market → high confidence signals

Direction determined by up-move vs down-move dominance over lookback period (default: 20 bars)

Signal Output: -1.0 to +1.0 (bearish order to bullish order)

Layer 2 - Momentum Synthesis

Combines three momentum indicators into single composite score:

Components:

RSI (40% weight): Normalized to -1/+1 scale using (RSI-50)/50

Rate of Change (30% weight): Percentage change over lookback (default: 14 bars), clamped to ±1

MACD Histogram (30% weight): Fast(12) - Slow(26), normalized by ATR

Why This Matters: RSI catches mean-reversion opportunities, ROC catches raw momentum, MACD catches momentum divergence. Weighting favors RSI for reliability while keeping other perspectives.

Signal Output: -1.0 to +1.0 (strong bearish to strong bullish)

Layer 3 - Structure Analysis

Evaluates price position within swing range (default: 50-bar lookback):

Position Classification:

Bottom 20% of range = Support Zone → bullish bounce potential

Top 20% of range = Resistance Zone → bearish rejection potential

Middle 60% = Neutral Zone → breakout/breakdown monitoring

Signal Logic:

At support + bullish candle = +0.7 (strong buy setup)

At resistance + bearish candle = -0.7 (strong sell setup)

Breaking above range highs = +0.5 (breakout confirmation)

Breaking below range lows = -0.5 (breakdown confirmation)

Consolidation within range = ±0.3 (weak directional bias)

Signal Output: -1.0 to +1.0 (bearish structure to bullish structure)

Confluence Voting System

Each layer casts a vote (Long/Short/Neutral). The system requires minimum 2-of-3 agreement (configurable 1-3) before generating a signal:

Examples:

Entropy: Bullish, Momentum: Bullish, Structure: Neutral → Signal generated (2 long votes)

Entropy: Bearish, Momentum: Neutral, Structure: Neutral → No signal (only 1 short vote)

All three bullish → Signal generated with +5% probability bonus

This is the key to quality. Single indicators give too many false signals. Triple confirmation dramatically improves accuracy.

📈 PROBABILITY CALCULATION: HOW CONFIDENCE IS MEASURED

Base Probability:

Raw_Prob = 50% + (Average_Signal_Strength × 25%)

Then AGE applies strategic adjustments:

Trend Alignment:

Signal with trend: +4%

Signal against strong trend: -8%

Weak/no trend: no adjustment

Regime Adaptation:

Trending market (efficiency >50%, moderate vol): +3%

Volatile market (vol ratio >1.5x): -5%

Choppy market (low efficiency): -2%

Volume Confirmation:

Volume > 70% of 20-bar SMA: no change

Volume below threshold: -3%

Volatility State (DVS Ratio):

High vol (>1.8x baseline): -4% (reduce confidence in chaos)

Low vol (<0.7x baseline): -2% (markets can whipsaw in compression)

Moderate elevated vol (1.0-1.3x): +2% (trending conditions emerging)

Confluence Bonus:

All 3 indicators agree: +5%

2 of 3 agree: +2%

Strategy Gene Adjustment:

Probability Boost gene: -10% to +10%

Regime Adaptation gene: scales regime adjustments by 0-100%

Final Probability: Clamped between 35% (minimum) and 88% (maximum)

Why These Ranges?

Below 35% = too uncertain, better not to signal

Above 88% = unrealistic, creates overconfidence

Sweet spot: 65-80% for quality entries

🔄 THE SHADOW PORTFOLIO SYSTEM: HOW STRATEGIES COMPETE

Each active strategy maintains a virtual trading account that executes in parallel with real-time data:

Shadow Trading Mechanics

Entry Logic:

Calculate signal direction, probability, and confluence using strategy's unique DNA

Check if signal meets quality gate:

Probability ≥ configured minimum threshold (default: 65%)

Confluence ≥ configured minimum (default: 2 of 3)

Direction is not zero (must be long or short, not neutral)

Verify signal persistence:

Base requirement: 2 bars (configurable 1-5)

Adapts based on probability: high-prob signals (75%+) enter 1 bar faster, low-prob signals need 1 bar more

Adjusts for regime: trending markets reduce persistence by 1, volatile markets add 1

Apply additional filters:

Trend strength must exceed strategy's requirement gene

Regime filter: if volatile market detected, probability must be 72%+ to override

Volume confirmation required (volume > 70% of average)

If all conditions met for required persistence bars, enter shadow position at current close price

Position Management:

Entry Price: Recorded at close of entry bar

Stop Loss: ATR-based distance = ATR × ATR_Mult (gene) × Stop_Mult (gene) × DVS_Ratio

Take Profit: ATR-based distance = ATR × ATR_Mult (gene) × Target_Mult (gene) × DVS_Ratio

Position: +1 (long) or -1 (short), only one at a time per strategy

Exit Logic:

Check if price hit stop (on low) or target (on high) on current bar

Record trade outcome in R-multiples (profit/loss normalized by ATR)

Update performance metrics:

Total trades counter incremented

Wins counter (if profit > 0)

Cumulative P&L updated

Peak equity tracked (for drawdown calculation)

Maximum drawdown from peak recorded

Enter cooldown period (default: 8 bars, configurable 3-20) before next entry allowed

Reset signal age counter to zero

Walk-Forward Tracking:

During position lifecycle, trades are categorized:

Training Phase (first 250 bars): Trade counted toward training metrics

Testing Phase (next 75 bars): Trade counted toward testing metrics (out-of-sample)

Live Phase (after WFO period): Trade counted toward overall metrics

Why Shadow Portfolios?

No lookahead bias (uses only data available at the bar)

Realistic execution simulation (entry on close, stop/target checks on high/low)

Independent performance tracking for true fitness comparison

Allows safe experimentation without risking capital

Each strategy learns from its own experience

🏆 FITNESS SCORING: HOW STRATEGIES ARE RANKED

Fitness is not just win rate. AGE uses a comprehensive multi-factor scoring system:

Core Metrics (Minimum 3 trades required)

Win Rate (30% of fitness):

WinRate = Wins / TotalTrades

Normalized directly (0.0-1.0 scale)

Total P&L (30% of fitness):

Normalized_PnL = (PnL + 300) / 600

Clamped 0.0-1.0. Assumes P&L range of -300R to +300R for normalization scale.

Expectancy (25% of fitness):

Expectancy = Total_PnL / Total_Trades

Normalized_Expectancy = (Expectancy + 30) / 60

Clamped 0.0-1.0. Rewards consistency of profit per trade.

Drawdown Control (15% of fitness):

Normalized_DD = 1 - (Max_Drawdown / 15)

Clamped 0.0-1.0. Penalizes strategies that suffer large equity retracements from peak.

Sample Size Adjustment

Quality Factor:

<50 trades: 1.0 (full weight, small sample)

50-100 trades: 0.95 (slight penalty for medium sample)

100 trades: 0.85 (larger penalty for large sample)

Why penalize more trades? Prevents strategies from gaming the system by taking hundreds of tiny trades to inflate statistics. Favors quality over quantity.

Bonus Adjustments

Walk-Forward Validation Bonus:

if (WFO_Validated):

Fitness += (WFO_Efficiency - 0.5) × 0.1

Strategies proven on out-of-sample data receive up to +10% fitness boost based on test/train efficiency ratio.

Signal Efficiency Bonus (if diagnostics enabled):

if (Signals_Evaluated > 10):

Pass_Rate = Signals_Passed / Signals_Evaluated

Fitness += (Pass_Rate - 0.1) × 0.05

Rewards strategies that generate high-quality signals passing the quality gate, not just profitable trades.

Final Fitness: Clamped at 0.0 minimum (prevents negative fitness values)

Result: Elite strategies typically achieve 0.50-0.75 fitness. Anything above 0.60 is excellent. Below 0.30 is prime candidate for culling.

🔬 WALK-FORWARD OPTIMIZATION: ANTI-OVERFITTING PROTECTION

This is what separates AGE from curve-fitted garbage indicators.

The Three-Phase Process

Every new strategy undergoes a rigorous validation lifecycle:

Phase 1 - Training Window (First 250 bars, configurable 100-500):

Strategy trades normally via shadow portfolio

All trades count toward training performance metrics

System learns which gene combinations produce profitable patterns

Tracks independently: Training_Trades, Training_Wins, Training_PnL

Phase 2 - Testing Window (Next 75 bars, configurable 30-200):

Strategy continues trading without any parameter changes

Trades now count toward testing performance metrics (separate tracking)

This is out-of-sample data - strategy has never seen these bars during "optimization"

Tracks independently: Testing_Trades, Testing_Wins, Testing_PnL

Phase 3 - Validation Check:

Minimum_Trades = 5 (configurable 3-15)

IF (Train_Trades >= Minimum AND Test_Trades >= Minimum):

WR_Efficiency = Test_WinRate / Train_WinRate

Expectancy_Efficiency = Test_Expectancy / Train_Expectancy

WFO_Efficiency = (WR_Efficiency + Expectancy_Efficiency) / 2

IF (WFO_Efficiency >= 0.55): // configurable 0.3-0.9

Strategy.Validated = TRUE

Strategy receives fitness bonus

ELSE:

Strategy receives 30% fitness penalty

ELSE:

Validation deferred (insufficient trades in one or both periods)

What Validation Means

Validated Strategy (Green "✓ VAL" in dashboard):

Performed at least 55% as well on unseen data compared to training data

Gets fitness bonus: +(efficiency - 0.5) × 0.1

Receives priority during tournament selection for breeding

More likely to be chosen as active trading strategy

Unvalidated Strategy (Orange "○ TRAIN" in dashboard):

Failed to maintain performance on test data (likely curve-fitted to training period)

Receives 30% fitness penalty (0.7x multiplier)

Makes strategy prime candidate for culling

Can still trade but with lower selection probability

Insufficient Data (continues collecting):

Hasn't completed both training and testing periods yet

OR hasn't achieved minimum trade count in both periods

Validation check deferred until requirements met

Why 55% Efficiency Threshold?

If a strategy earned 10R during training but only 5.5R during testing, it still proved an edge exists beyond random luck. Requiring 100% efficiency would be unrealistic - market conditions change between periods. But requiring >50% ensures the strategy didn't completely degrade on fresh data.

The Protection: Strategies that work great on historical data but fail on new data are automatically identified and penalized. This prevents the population from being polluted by overfitted strategies that would fail in live trading.

🌊 DYNAMIC VOLATILITY SCALING (DVS): ADAPTIVE STOP/TARGET PLACEMENT

AGE doesn't use fixed stop distances. It adapts to current volatility conditions in real-time.

Four Volatility Measurement Methods

1. ATR Ratio (Simple Method):

Current_Vol = ATR(14) / Close

Baseline_Vol = SMA(Current_Vol, 100)

Ratio = Current_Vol / Baseline_Vol

Basic comparison of current ATR to 100-bar moving average baseline.

2. Parkinson (High-Low Range Based):

For each bar: HL = log(High / Low)

Parkinson_Vol = sqrt(Σ(HL²) / (4 × Period × log(2)))

More stable than close-to-close volatility. Captures intraday range expansion without overnight gap noise.

3. Garman-Klass (OHLC Based):

HL_Term = 0.5 × ²

CO_Term = (2×log(2) - 1) × ²

GK_Vol = sqrt(Σ(HL_Term - CO_Term) / Period)

Most sophisticated estimator. Incorporates all four price points (open, high, low, close) plus gap information.

4. Ensemble Method (Default - Median of All Three):

Ratio_1 = ATR_Current / ATR_Baseline

Ratio_2 = Parkinson_Current / Parkinson_Baseline

Ratio_3 = GK_Current / GK_Baseline

DVS_Ratio = Median(Ratio_1, Ratio_2, Ratio_3)

Why Ensemble?

Takes median to avoid outliers and false spikes

If ATR jumps but range-based methods stay calm, median prevents overreaction

If one method fails, other two compensate

Most robust approach across different market conditions

Sensitivity Scaling

Scaled_Ratio = (Raw_Ratio) ^ Sensitivity

Sensitivity 0.3: Cube root - heavily dampens volatility impact

Sensitivity 0.5: Square root - moderate dampening

Sensitivity 0.7 (Default): Balanced response to volatility changes

Sensitivity 1.0: Linear - full 1:1 volatility impact

Sensitivity 1.5: Exponential - amplified response to volatility spikes

Safety Clamps: Final DVS Ratio always clamped between 0.5x and 2.5x baseline to prevent extreme position sizing or stop placement errors.

How DVS Affects Shadow Trading

Every strategy's stop and target distances are multiplied by the current DVS ratio:

Stop Loss Distance:

Stop_Distance = ATR × ATR_Mult (gene) × Stop_Mult (gene) × DVS_Ratio

Take Profit Distance:

Target_Distance = ATR × ATR_Mult (gene) × Target_Mult (gene) × DVS_Ratio

Example Scenario:

ATR = 10 points

Strategy's ATR_Mult gene = 2.5

Strategy's Stop_Mult gene = 1.5

Strategy's Target_Mult gene = 2.5

DVS_Ratio = 1.4 (40% above baseline volatility - market heating up)

Stop = 10 × 2.5 × 1.5 × 1.4 = 52.5 points (vs. 37.5 in normal vol)

Target = 10 × 2.5 × 2.5 × 1.4 = 87.5 points (vs. 62.5 in normal vol)

Result:

During volatility spikes: Stops automatically widen to avoid noise-based exits, targets extend for bigger moves

During calm periods: Stops tighten for better risk/reward, targets compress for realistic profit-taking

Strategies adapt risk management to match current market behavior

🧬 THE EVOLUTIONARY CYCLE: SPAWN, COMPETE, CULL

Initialization (Bar 1)

AGE begins with 4 seed strategies (if evolution enabled):

Seed Strategy #0 (Balanced):

All sensitivities at 1.0 (neutral)

Zero probability boost

Moderate trend requirement (0.4)

Standard ATR/stop/target multiples (2.5/1.5/2.5)

Mid-level regime adaptation (0.5)

Seed Strategy #1 (Momentum-Focused):

Lower entropy sensitivity (0.7), higher momentum (1.5)

Slight probability boost (+0.03)

Higher trend requirement (0.5)

Tighter stops (1.3), wider targets (3.0)

Seed Strategy #2 (Entropy-Driven):

Higher entropy sensitivity (1.5), lower momentum (0.8)

Slight probability penalty (-0.02)

More trend tolerant (0.6)

Wider stops (1.8), standard targets (2.5)

Seed Strategy #3 (Structure-Based):

Balanced entropy/momentum (0.8/0.9), high structure (1.4)

Slight probability boost (+0.02)

Lower trend requirement (0.35)

Moderate risk parameters (1.6/2.8)

All seeds start with WFO validation bypassed if WFO is disabled, or must validate if enabled.

Spawning New Strategies

Timing (Adaptive):

Historical phase: Every 30 bars (configurable 10-100)

Live phase: Every 200 bars (configurable 100-500)

Automatically switches to live timing when barstate.isrealtime triggers

Conditions:

Current population < max population limit (default: 8, configurable 4-12)

At least 2 active strategies exist (need parents)

Available slot in population array

Selection Process:

Run tournament selection 3 times with different seeds

Each tournament: randomly sample active strategies, pick highest fitness

Best from 3 tournaments becomes Parent 1

Repeat independently for Parent 2

Ensures fit parents but maintains diversity

Crossover Breeding:

For each of 10 genes:

Parent1_Fitness = fitness

Parent2_Fitness = fitness

Weight1 = Parent1_Fitness / (Parent1_Fitness + Parent2_Fitness)

Gene1 = parent1's value

Gene2 = parent2's value

Child_Gene = Weight1 × Gene1 + (1 - Weight1) × Gene2

Fitness-weighted crossover ensures fitter parent contributes more genetic material.

Mutation:

For each gene in child:

IF (random < mutation_rate):

Gene_Range = GENE_MAX - GENE_MIN

Noise = (random - 0.5) × 2 × mutation_strength × Gene_Range

Mutated_Gene = Clamp(Child_Gene + Noise, GENE_MIN, GENE_MAX)

Historical mutation rate: 20% (aggressive exploration)

Live mutation rate: 8% (conservative stability)

Mutation strength: 12% of gene range (configurable 5-25%)

Initialization of New Strategy:

Unique ID assigned (total_spawned counter)

Parent ID recorded

Generation = max(parent generations) + 1

Birth bar recorded (for age tracking)

All performance metrics zeroed

Shadow portfolio reset

WFO validation flag set to false (must prove itself)

Result: New strategy with hybrid DNA enters population, begins trading in next bar.

Competition (Every Bar)

All active strategies:

Calculate their signal based on unique DNA

Check quality gate with their thresholds

Manage shadow positions (entries/exits)

Update performance metrics

Recalculate fitness score

Track WFO validation progress

Strategies compete indirectly through fitness ranking - no direct interaction.

Culling Weak Strategies

Timing (Adaptive):

Historical phase: Every 60 bars (configurable 20-200, should be 2x spawn interval)

Live phase: Every 400 bars (configurable 200-1000, should be 2x spawn interval)

Minimum Adaptation Score (MAS):

Initial MAS = 0.10

MAS decays: MAS × 0.995 every cull cycle

Minimum MAS = 0.03 (floor)

MAS represents the "survival threshold" - strategies below this fitness level are vulnerable.

Culling Conditions (ALL must be true):

Population > minimum population (default: 3, configurable 2-4)

At least one strategy has fitness < MAS

Strategy's age > culling interval (prevents premature culling of new strategies)

Strategy is not in top N elite (default: 2, configurable 1-3)

Culling Process:

Find worst strategy:

For each active strategy:

IF (age > cull_interval):

Fitness = base_fitness

IF (not WFO_validated AND WFO_enabled):

Fitness × 0.7 // 30% penalty for unvalidated

IF (Fitness < MAS AND Fitness < worst_fitness_found):

worst_strategy = this_strategy

worst_fitness = Fitness

IF (worst_strategy found):

Count elite strategies with fitness > worst_fitness

IF (elite_count >= elite_preservation_count):

Deactivate worst_strategy (set active flag = false)

Increment total_culled counter

Elite Protection:

Even if a strategy's fitness falls below MAS, it survives if fewer than N strategies are better. This prevents culling when population is generally weak.

Result: Weak strategies removed from population, freeing slots for new spawns. Gene pool improves over time.

Selection for Display (Every Bar)

AGE chooses one strategy to display signals:

Best fitness = -1

Selected = none

For each active strategy:

Fitness = base_fitness

IF (WFO_validated):

Fitness × 1.3 // 30% bonus for validated strategies

IF (Fitness > best_fitness):

best_fitness = Fitness

selected_strategy = this_strategy

Display selected strategy's signals on chart

Result: Only the highest-fitness (optionally validated-boosted) strategy's signals appear as chart markers. Other strategies trade invisibly in shadow portfolios.

🎨 PREMIUM VISUALIZATION SYSTEM

AGE includes sophisticated visual feedback that standard indicators lack:

1. Gradient Probability Cloud (Optional, Default: ON)

Multi-layer gradient showing signal buildup 2-3 bars before entry:

Activation Conditions:

Signal persistence > 0 (same directional signal held for multiple bars)

Signal probability ≥ minimum threshold (65% by default)

Signal hasn't yet executed (still in "forming" state)

Visual Construction:

7 gradient layers by default (configurable 3-15)

Each layer is a line-fill pair (top line, bottom line, filled between)

Layer spacing: 0.3 to 1.0 × ATR above/below price

Outer layers = faint, inner layers = bright

Color transitions from base to intense based on layer position

Transparency scales with probability (high prob = more opaque)

Color Selection:

Long signals: Gradient from theme.gradient_bull_mid to theme.gradient_bull_strong

Short signals: Gradient from theme.gradient_bear_mid to theme.gradient_bear_strong

Base transparency: 92%, reduces by up to 8% for high-probability setups

Dynamic Behavior:

Cloud grows/shrinks as signal persistence increases/decreases

Redraws every bar while signal is forming

Disappears when signal executes or invalidates

Performance Note: Computationally expensive due to linefill objects. Disable or reduce layers if chart performance degrades.

2. Population Fitness Ribbon (Optional, Default: ON)

Histogram showing fitness distribution across active strategies:

Activation: Only draws on last bar (barstate.islast) to avoid historical clutter

Visual Construction:

10 histogram layers by default (configurable 5-20)

Plots 50 bars back from current bar

Positioned below price at: lowest_low(100) - 1.5×ATR (doesn't interfere with price action)

Each layer represents a fitness threshold (evenly spaced min to max fitness)

Layer Logic:

For layer_num from 0 to ribbon_layers:

Fitness_threshold = min_fitness + (max_fitness - min_fitness) × (layer / layers)

Count strategies with fitness ≥ threshold

Height = ATR × 0.15 × (count / total_active)

Y_position = base_level + ATR × 0.2 × layer

Color = Gradient from weak to strong based on layer position

Line_width = Scaled by height (taller = thicker)

Visual Feedback:

Tall, bright ribbon = healthy population, many fit strategies at high fitness levels

Short, dim ribbon = weak population, few strategies achieving good fitness

Ribbon compression (layers close together) = population converging to similar fitness

Ribbon spread = diverse fitness range, active selection pressure

Use Case: Quick visual health check without opening dashboard. Ribbon growing upward over time = population improving.

3. Confidence Halo (Optional, Default: ON)

Circular polyline around entry signals showing probability strength:

Activation: Draws when new position opens (shadow_position changes from 0 to ±1)

Visual Construction:

20-segment polyline forming approximate circle

Center: Low - 0.5×ATR (long) or High + 0.5×ATR (short)

Radius: 0.3×ATR (low confidence) to 1.0×ATR (elite confidence)

Scales with: (probability - min_probability) / (1.0 - min_probability)

Color Coding:

Elite (85%+): Cyan (theme.conf_elite), large radius, minimal transparency (40%)

Strong (75-85%): Strong green (theme.conf_strong), medium radius, moderate transparency (50%)

Good (65-75%): Good green (theme.conf_good), smaller radius, more transparent (60%)

Moderate (<65%): Moderate green (theme.conf_moderate), tiny radius, very transparent (70%)

Technical Detail:

Uses chart.point array with index-based positioning

5-bar horizontal spread for circular appearance (±5 bars from entry)

Curved=false (Pine Script polyline limitation)

Fill color matches line color but more transparent (88% vs line's transparency)

Purpose: Instant visual probability assessment. No need to check dashboard - halo size/brightness tells the story.

4. Evolution Event Markers (Optional, Default: ON)

Visual indicators of genetic algorithm activity:

Spawn Markers (Diamond, Cyan):

Plots when total_spawned increases on current bar

Location: bottom of chart (location.bottom)

Color: theme.spawn_marker (cyan/bright blue)

Size: tiny

Indicates new strategy just entered population

Cull Markers (X-Cross, Red):

Plots when total_culled increases on current bar

Location: bottom of chart (location.bottom)

Color: theme.cull_marker (red/pink)

Size: tiny

Indicates weak strategy just removed from population

What It Tells You:

Frequent spawning early = population building, active exploration

Frequent culling early = high selection pressure, weak strategies dying fast

Balanced spawn/cull = healthy evolutionary churn

No markers for long periods = stable population (evolution plateaued or optimal genes found)

5. Entry/Exit Markers

Clear visual signals for selected strategy's trades:

Long Entry (Triangle Up, Green):

Plots when selected strategy opens long position (position changes 0 → +1)

Location: below bar (location.belowbar)

Color: theme.long_primary (green/cyan depending on theme)

Transparency: Scales with probability:

Elite (85%+): 0% (fully opaque)

Strong (75-85%): 10%

Good (65-75%): 20%

Acceptable (55-65%): 35%

Size: small

Short Entry (Triangle Down, Red):

Plots when selected strategy opens short position (position changes 0 → -1)

Location: above bar (location.abovebar)

Color: theme.short_primary (red/pink depending on theme)

Transparency: Same scaling as long entries

Size: small

Exit (X-Cross, Orange):

Plots when selected strategy closes position (position changes ±1 → 0)

Location: absolute (at actual exit price if stop/target lines enabled)

Color: theme.exit_color (orange/yellow depending on theme)

Transparency: 0% (fully opaque)

Size: tiny

Result: Clean, probability-scaled markers that don't clutter chart but convey essential information.

6. Stop Loss & Take Profit Lines (Optional, Default: ON)

Visual representation of shadow portfolio risk levels:

Stop Loss Line:

Plots when selected strategy has active position

Level: shadow_stop value from selected strategy

Color: theme.short_primary with 60% transparency (red/pink, subtle)

Width: 2

Style: plot.style_linebr (breaks when no position)

Take Profit Line:

Plots when selected strategy has active position

Level: shadow_target value from selected strategy

Color: theme.long_primary with 60% transparency (green, subtle)

Width: 2

Style: plot.style_linebr (breaks when no position)

Purpose:

Shows where shadow portfolio would exit for stop/target

Helps visualize strategy's risk/reward ratio

Useful for manual traders to set similar levels

Disable for cleaner chart (recommended for presentations)

7. Dynamic Trend EMA

Gradient-colored trend line that visualizes trend strength:

Calculation:

EMA(close, trend_length) - default 50 period (configurable 20-100)

Slope calculated over 10 bars: (current_ema - ema ) / ema × 100

Color Logic:

Trend_direction:

Slope > 0.1% = Bullish (1)

Slope < -0.1% = Bearish (-1)

Otherwise = Neutral (0)

Trend_strength = abs(slope)

Color = Gradient between:

- Neutral color (gray/purple)

- Strong bullish (bright green) if direction = 1

- Strong bearish (bright red) if direction = -1

Gradient factor = trend_strength (0 to 1+ scale)

Visual Behavior:

Faint gray/purple = weak/no trend (choppy conditions)

Light green/red = emerging trend (low strength)

Bright green/red = strong trend (high conviction)

Color intensity = trend strength magnitude

Transparency: 50% (subtle, doesn't overpower price action)

Purpose: Subconscious awareness of trend state without checking dashboard or indicators.

8. Regime Background Tinting (Subtle)

Ultra-low opacity background color indicating detected market regime:

Regime Detection:

Efficiency = directional_movement / total_range (over trend_length bars)

Vol_ratio = current_volatility / average_volatility

IF (efficiency > 0.5 AND vol_ratio < 1.3):

Regime = Trending (1)

ELSE IF (vol_ratio > 1.5):

Regime = Volatile (2)

ELSE:

Regime = Choppy (0)

Background Colors:

Trending: theme.regime_trending (dark green, 92-93% transparency)

Volatile: theme.regime_volatile (dark red, 93% transparency)

Choppy: No tint (normal background)

Purpose:

Subliminal regime awareness

Helps explain why signals are/aren't generating

Trending = ideal conditions for AGE

Volatile = fewer signals, higher thresholds applied

Choppy = mixed signals, lower confidence

Important: Extremely subtle by design. Not meant to be obvious, just subconscious context.

📊 ENHANCED DASHBOARD

Comprehensive real-time metrics in single organized panel (top-right position):

Dashboard Structure (5 columns × 14 rows)

Header Row:

Column 0: "🧬 AGE PRO" + phase indicator (🔴 LIVE or ⏪ HIST)

Column 1: "POPULATION"

Column 2: "PERFORMANCE"

Column 3: "CURRENT SIGNAL"

Column 4: "ACTIVE STRATEGY"

Column 0: Market State

Regime (📈 TREND / 🌊 CHAOS / ➖ CHOP)

DVS Ratio (current volatility scaling factor, format: #.##)

Trend Direction (▲ BULL / ▼ BEAR / ➖ FLAT with color coding)

Trend Strength (0-100 scale, format: #.##)

Column 1: Population Metrics

Active strategies (count / max_population)

Validated strategies (WFO passed / active total)

Current generation number

Total spawned (all-time strategy births)

Total culled (all-time strategy deaths)

Column 2: Aggregate Performance

Total trades across all active strategies

Aggregate win rate (%) - color-coded:

Green (>55%)

Orange (45-55%)

Red (<45%)

Total P&L in R-multiples - color-coded by positive/negative

Best fitness score in population (format: #.###)

MAS - Minimum Adaptation Score (cull threshold, format: #.###)

Column 3: Current Signal Status

Status indicator:

"▲ LONG" (green) if selected strategy in long position

"▼ SHORT" (red) if selected strategy in short position

"⏳ FORMING" (orange) if signal persisting but not yet executed

"○ WAITING" (gray) if no active signal

Confidence percentage (0-100%, format: #.#%)

Quality assessment:

"🔥 ELITE" (cyan) for 85%+ probability

"✓ STRONG" (bright green) for 75-85%

"○ GOOD" (green) for 65-75%

"- LOW" (dim) for <65%

Confluence score (X/3 format)

Signal age:

"X bars" if signal forming

"IN TRADE" if position active

"---" if no signal

Column 4: Selected Strategy Details

Strategy ID number (#X format)

Validation status:

"✓ VAL" (green) if WFO validated

"○ TRAIN" (orange) if still in training/testing phase

Generation number (GX format)

Personal fitness score (format: #.### with color coding)

Trade count

P&L and win rate (format: #.#R (##%) with color coding)

Color Scheme:

Panel background: theme.panel_bg (dark, low opacity)

Panel headers: theme.panel_header (slightly lighter)

Primary text: theme.text_primary (bright, high contrast)

Secondary text: theme.text_secondary (dim, lower contrast)

Positive metrics: theme.metric_positive (green)

Warning metrics: theme.metric_warning (orange)

Negative metrics: theme.metric_negative (red)

Special markers: theme.validated_marker, theme.spawn_marker

Update Frequency: Only on barstate.islast (current bar) to minimize CPU usage

Purpose:

Quick overview of entire system state

No need to check multiple indicators

Trading decisions informed by population health, regime state, and signal quality

Transparency into what AGE is thinking

🔍 DIAGNOSTICS PANEL (Optional, Default: OFF)

Detailed signal quality tracking for optimization and debugging:

Panel Structure (3 columns × 8 rows)

Position: Bottom-right corner (doesn't interfere with main dashboard)

Header Row:

Column 0: "🔍 DIAGNOSTICS"

Column 1: "COUNT"

Column 2: "%"

Metrics Tracked (for selected strategy only):

Total Evaluated:

Every signal that passed initial calculation (direction ≠ 0)

Represents total opportunities considered

✓ Passed:

Signals that passed quality gate and executed

Green color coding

Percentage of evaluated signals

Rejection Breakdown:

⨯ Probability:

Rejected because probability < minimum threshold

Most common rejection reason typically

⨯ Confluence:

Rejected because confluence < minimum required (e.g., only 1 of 3 indicators agreed)

⨯ Trend:

Rejected because signal opposed strong trend

Indicates counter-trend protection working

⨯ Regime:

Rejected because volatile regime detected and probability wasn't high enough to override

Shows regime filter in action

⨯ Volume:

Rejected because volume < 70% of 20-bar average

Indicates volume confirmation requirement

Color Coding:

Passed count: Green (success metric)

Rejection counts: Red (failure metrics)

Percentages: Gray (neutral, informational)

Performance Cost: Slight CPU overhead for tracking counters. Disable when not actively optimizing settings.

How to Use Diagnostics

Scenario 1: Too Few Signals

Evaluated: 200

Passed: 10 (5%)

⨯ Probability: 120 (60%)

⨯ Confluence: 40 (20%)

⨯ Others: 30 (15%)

Diagnosis: Probability threshold too high for this strategy's DNA.

Solution: Lower min probability from 65% to 60%, or allow strategy more time to evolve better DNA.

Scenario 2: Too Many False Signals

Evaluated: 200

Passed: 80 (40%)

Strategy win rate: 45%

Diagnosis: Quality gate too loose, letting low-quality signals through.

Solution: Raise min probability to 70%, or increase min confluence to 3 (all indicators must agree).

Scenario 3: Regime-Specific Issues

⨯ Regime: 90 (45% of rejections)

Diagnosis: Frequent volatile regime detection blocking otherwise good signals.

Solution: Either accept fewer trades during chaos (recommended), or disable regime filter if you want signals regardless of market state.

Optimization Workflow:

Enable diagnostics

Run 200+ bars

Analyze rejection patterns

Adjust settings based on data

Re-run and compare pass rate

Disable diagnostics when satisfied

⚙️ CONFIGURATION GUIDE

🧬 Evolution Engine Settings

Enable AGE Evolution (Default: ON):

ON: Full genetic algorithm (recommended for best results)

OFF: Uses only 4 seed strategies, no spawning/culling (static population for comparison testing)

Max Population (4-12, Default: 8):

Higher = more diversity, more exploration, slower performance

Lower = faster computation, less exploration, risk of premature convergence

Sweet spot: 6-8 for most use cases

4 = minimum for meaningful evolution

12 = maximum before diminishing returns

Min Population (2-4, Default: 3):

Safety floor - system never culls below this count

Prevents population extinction during harsh selection

Should be at least half of max population

Elite Preservation (1-3, Default: 2):

Top N performers completely immune to culling

Ensures best genes always survive

1 = minimal protection, aggressive selection

2 = balanced (recommended)

3 = conservative, slower gene pool turnover

Historical: Spawn Interval (10-100, Default: 30):

Bars between spawning new strategies during historical data

Lower = faster evolution, more exploration

Higher = slower evolution, more evaluation time per strategy

30 bars = ~1-2 hours on 15min chart

Historical: Cull Interval (20-200, Default: 60):

Bars between culling weak strategies during historical data

Should be 2x spawn interval for balanced churn

Lower = aggressive selection pressure

Higher = patient evaluation

Live: Spawn Interval (100-500, Default: 200):

Bars between spawning during live trading

Much slower than historical for stability

Prevents population chaos during live trading

200 bars = ~1.5 trading days on 15min chart

Live: Cull Interval (200-1000, Default: 400):

Bars between culling during live trading

Should be 2x live spawn interval

Conservative removal during live trading

Historical: Mutation Rate (0.05-0.40, Default: 0.20):

Probability each gene mutates during breeding (20% = 2 out of 10 genes on average)

Higher = more exploration, slower convergence

Lower = more exploitation, faster convergence but risk of local optima

20% balances exploration vs exploitation

Live: Mutation Rate (0.02-0.20, Default: 0.08):

Mutation rate during live trading

Much lower for stability (don't want population to suddenly degrade)

8% = mostly inherits parent genes with small tweaks

Mutation Strength (0.05-0.25, Default: 0.12):

How much genes change when mutated (% of gene's total range)

0.05 = tiny nudges (fine-tuning)

0.12 = moderate jumps (recommended)

0.25 = large leaps (aggressive exploration)

Example: If gene range is 0.5-2.0, 12% strength = ±0.18 possible change

📈 Signal Quality Settings

Min Signal Probability (0.55-0.80, Default: 0.65):

Quality gate threshold - signals below this never generate

0.55-0.60 = More signals, accept lower confidence (higher risk)

0.65 = Institutional-grade balance (recommended)

0.70-0.75 = Fewer but higher-quality signals (conservative)

0.80+ = Very selective, very few signals (ultra-conservative)

Min Confluence Score (1-3, Default: 2):

Required indicator agreement before signal generates

1 = Any single indicator can trigger (not recommended - too many false signals)

2 = Requires 2 of 3 indicators agree (RECOMMENDED for balance)

3 = All 3 must agree (very selective, few signals, high quality)

Base Persistence Bars (1-5, Default: 2):

Base bars signal must persist before entry

System adapts automatically:

High probability signals (75%+) enter 1 bar faster

Low probability signals (<68%) need 1 bar more

Trending regime: -1 bar (faster entries)

Volatile regime: +1 bar (more confirmation)

1 = Immediate entry after quality gate (responsive but prone to whipsaw)

2 = Balanced confirmation (recommended)

3-5 = Patient confirmation (slower but more reliable)

Cooldown After Trade (3-20, Default: 8):

Bars to wait after exit before next entry allowed

Prevents overtrading and revenge trading

3 = Minimal cooldown (active trading)

8 = Balanced (recommended)

15-20 = Conservative (position trading)

Entropy Length (10-50, Default: 20):

Lookback period for market order/disorder calculation

Lower = more responsive to regime changes (noisy)

Higher = more stable regime detection (laggy)

20 = works across most timeframes

Momentum Length (5-30, Default: 14):

Period for RSI/ROC calculations

14 = standard (RSI default)

Lower = more signals, less reliable

Higher = fewer signals, more reliable

Structure Length (20-100, Default: 50):

Lookback for support/resistance swing range

20 = short-term swings (day trading)

50 = medium-term structure (recommended)

100 = major structure (position trading)

Trend EMA Length (20-100, Default: 50):

EMA period for trend detection and direction bias

20 = short-term trend (responsive)

50 = medium-term trend (recommended)

100 = long-term trend (position trading)

ATR Period (5-30, Default: 14):

Period for volatility measurement

14 = standard ATR

Lower = more responsive to vol changes

Higher = smoother vol calculation

📊 Volatility Scaling (DVS) Settings

Enable DVS (Default: ON):

Dynamic volatility scaling for adaptive stop/target placement

Highly recommended to leave ON

OFF only for testing fixed-distance stops

DVS Method (Default: Ensemble):

ATR Ratio: Simple, fast, single-method (good for beginners)

Parkinson: High-low range based (good for intraday)

Garman-Klass: OHLC based (sophisticated, considers gaps)

Ensemble: Median of all three (RECOMMENDED - most robust)

DVS Memory (20-200, Default: 100):

Lookback for baseline volatility comparison

20 = very responsive to vol changes (can overreact)

100 = balanced adaptation (recommended)

200 = slow, stable baseline (minimizes false vol signals)

DVS Sensitivity (0.3-1.5, Default: 0.7):

How much volatility affects scaling (power-law exponent)

0.3 = Conservative, heavily dampens vol impact (cube root)

0.5 = Moderate dampening (square root)

0.7 = Balanced response (recommended)

1.0 = Linear, full 1:1 vol response

1.5 = Aggressive, amplified response (exponential)

🔬 Walk-Forward Optimization Settings

Enable WFO (Default: ON):

Out-of-sample validation to prevent overfitting

Highly recommended to leave ON

OFF only for testing or if you want unvalidated strategies

Training Window (100-500, Default: 250):

Bars for in-sample optimization

100 = fast validation, less data (risky)

250 = balanced (recommended) - about 1-2 months on daily, 1-2 weeks on 15min

500 = patient validation, more data (conservative)

Testing Window (30-200, Default: 75):

Bars for out-of-sample validation

Should be ~30% of training window

30 = minimal test (fast validation)

75 = balanced (recommended)

200 = extensive test (very conservative)

Min Trades for Validation (3-15, Default: 5):

Required trades in BOTH training AND testing periods

3 = minimal sample (risky, fast validation)

5 = balanced (recommended)

10+ = conservative (slow validation, high confidence)

WFO Efficiency Threshold (0.3-0.9, Default: 0.55):

Minimum test/train performance ratio required

0.30 = Very loose (test must be 30% as good as training)

0.55 = Balanced (recommended) - test must be 55% as good

0.70+ = Strict (test must closely match training)

Higher = fewer validated strategies, lower risk of overfitting

🎨 Premium Visuals Settings

Visual Theme:

Neon Genesis: Cyberpunk aesthetic (cyan/magenta/purple)

Carbon Fiber: Industrial look (blue/red/gray)

Quantum Blue: Quantum computing (blue/purple/pink)

Aurora: Northern lights (teal/orange/purple)

⚡ Gradient Probability Cloud (Default: ON):

Multi-layer gradient showing signal buildup

Turn OFF if chart lags or for cleaner look

Cloud Gradient Layers (3-15, Default: 7):

More layers = smoother gradient, more CPU intensive

Fewer layers = faster, blockier appearance

🎗️ Population Fitness Ribbon (Default: ON):

Histogram showing fitness distribution

Turn OFF for cleaner chart

Ribbon Layers (5-20, Default: 10):

More layers = finer fitness detail

Fewer layers = simpler histogram

⭕ Signal Confidence Halo (Default: ON):

Circular indicator around entry signals

Size/brightness scales with probability

Minimal performance cost

🔬 Evolution Event Markers (Default: ON):

Diamond (spawn) and X (cull) markers

Shows genetic algorithm activity

Minimal performance cost

🎯 Stop/Target Lines (Default: ON):

Shows shadow portfolio stop/target levels

Turn OFF for cleaner chart (recommended for screenshots/presentations)

📊 Enhanced Dashboard (Default: ON):

Comprehensive metrics panel

Should stay ON unless you want zero overlays

🔍 Diagnostics Panel (Default: OFF):

Detailed signal rejection tracking

Turn ON when optimizing settings

Turn OFF during normal use (slight performance cost)

📈 USAGE WORKFLOW - HOW TO USE THIS INDICATOR

Phase 1: Initial Setup & Learning

Add AGE to your chart

Recommended timeframes: 15min, 30min, 1H (best signal-to-noise ratio)

Works on: 5min (day trading), 4H (swing trading), Daily (position trading)

Load 1000+ bars for sufficient evolution history

Let the population evolve (100+ bars minimum)

First 50 bars: Random exploration, poor results expected

Bars 50-150: Population converging, fitness improving

Bars 150+: Stable performance, validated strategies emerging

Watch the dashboard metrics

Population should grow toward max capacity

Generation number should advance regularly

Validated strategies counter should increase

Best fitness should trend upward toward 0.50-0.70 range

Observe evolution markers

Diamond markers (cyan) = new strategies spawning

X markers (red) = weak strategies being culled

Frequent early activity = healthy evolution

Activity slowing = population stabilizing

Be patient. Evolution takes time. Don't judge performance before 150+ bars.

Phase 2: Signal Observation

Watch signals form

Gradient cloud builds up 2-3 bars before entry

Cloud brightness = probability strength

Cloud thickness = signal persistence

Check signal quality

Look at confidence halo size when entry marker appears

Large bright halo = elite setup (85%+)

Medium halo = strong setup (75-85%)

Small halo = good setup (65-75%)

Verify market conditions

Check trend EMA color (green = uptrend, red = downtrend, gray = choppy)

Check background tint (green = trending, red = volatile, clear = choppy)

Trending background + aligned signal = ideal conditions

Review dashboard signal status

Current Signal column shows:

Status (Long/Short/Forming/Waiting)

Confidence % (actual probability value)

Quality assessment (Elite/Strong/Good)

Confluence score (2/3 or 3/3 preferred)

Only signals meeting ALL quality gates appear on chart. If you're not seeing signals, population is either still learning or market conditions aren't suitable.

Phase 3: Manual Trading Execution

When Long Signal Fires:

Verify confidence level (dashboard or halo size)

Confirm trend alignment (EMA sloping up, green color)

Check regime (preferably trending or choppy, avoid volatile)

Enter long manually on your broker platform

Set stop loss at displayed stop line level (if lines enabled), or use your own risk management

Set take profit at displayed target line level, or trail manually

Monitor position - exit if X marker appears (signal reversal)

When Short Signal Fires:

Same verification process

Confirm downtrend (EMA sloping down, red color)

Enter short manually

Use displayed stop/target levels or your own