Sma Standard Deviation | viResearchSma Standard Deviation | viResearch

Conceptual Foundation and Innovation

The "Sma Standard Deviation" indicator from viResearch combines the benefits of Simple Moving Average (SMA) smoothing with Standard Deviation (SD) analysis, offering traders a powerful tool for understanding price trends and volatility. The SMA provides a straightforward approach to trend detection by calculating the average price over a defined period, while the SD component adds insight into the market's volatility by measuring the variation of prices around the SMA. This combination helps traders identify whether the price is moving within a typical range or deviating significantly, which can signal potential trend shifts or periods of increased volatility. By using both SMA and SD together, this indicator enhances the trader's ability to detect not only the trend direction but also how strongly the market is deviating from that trend, offering more informed decision-making.

Technical Composition and Calculation

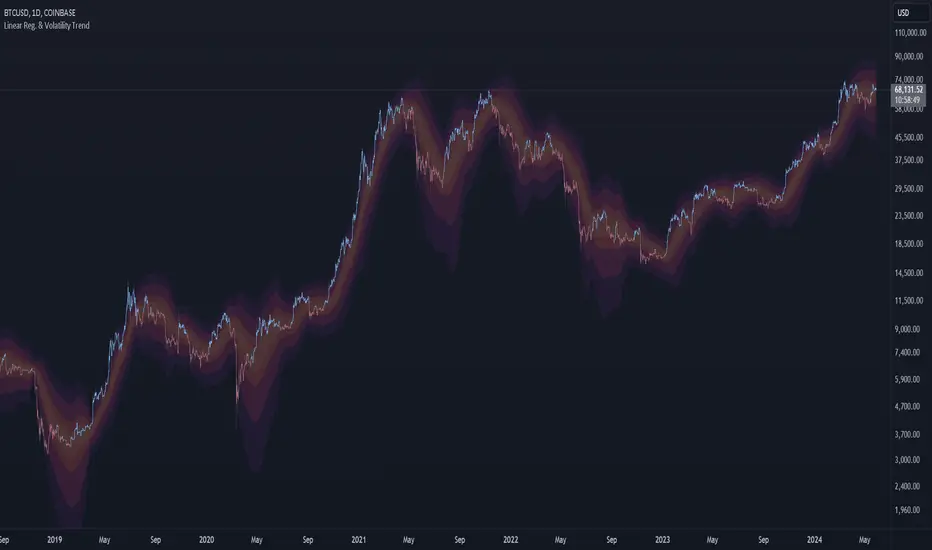

The "Sma Standard Deviation" script uses two key elements: the Simple Moving Average (SMA) and Standard Deviation (SD). The SMA is calculated over a user-defined length and represents the smoothed average price over this period. The script also incorporates DEMA smoothing applied to different price sources, providing further refinement to the trend analysis. The SD is calculated by measuring the deviation of the price from the SMA over a separate user-defined length, showing how volatile the price is relative to its average. The script generates upper and lower SD boundaries by adding and subtracting the SD from the SMA, creating a volatility-adjusted range for the price. This allows traders to visualize whether the price is moving within expected bounds or breaking out of its typical range. The script monitors crossovers between the DEMA, SMA, and SD boundaries, generating trend signals based on these interactions.

Features and User Inputs

The "Sma Standard Deviation" script offers several customizable inputs, allowing traders to adjust the indicator to their specific strategies. The SMA Length controls the period for which the moving average is calculated, while the SD Length defines how long the period is for measuring price deviation. Additionally, the DEMA smoothing length can be adjusted for both the trend and standard deviation calculations, giving traders control over how responsive or smooth they want the indicator to be. The script also includes alert conditions that notify traders when trend shifts occur, either to the upside or downside.

Practical Applications

The "Sma Standard Deviation" indicator is designed for traders who want to analyze both market trends and volatility in a unified tool. The combination of the SMA and SD helps traders identify potential trend reversals, as large deviations from the SMA can indicate periods of increased volatility that precede significant price moves. This makes the indicator particularly effective for identifying trend reversals, managing volatility, and improving trend-following strategies. By analyzing when the price moves outside the volatility-adjusted range defined by the SD, traders can detect early signals of potential trend reversals. The SD component helps traders understand how volatile the market is relative to its average price, allowing for more informed decisions in both trending and volatile market conditions. The dual use of DEMA and SMA smoothing allows for a clearer trend signal, helping traders stay aligned with the prevailing market direction while managing the noise caused by short-term volatility.

Advantages and Strategic Value

The "Sma Standard Deviation" script offers significant value by integrating both trend detection and volatility analysis into a single tool. The use of SMA for smoothing price trends, combined with the SD for assessing price volatility, provides a more comprehensive view of the market. This dual approach helps traders filter out false signals caused by short-term fluctuations while identifying potential trend changes driven by increased volatility. This makes the "Sma Standard Deviation" indicator ideal for traders seeking a balance between trend-following and volatility management.

Alerts and Visual Cues

The script includes alert conditions that notify traders when significant trend shifts occur based on price crossovers with the SMA and SD boundaries. The "Sma Standard Deviation Long" alert is triggered when the price crosses above the upper volatility boundary, indicating a potential upward trend. Conversely, the "Sma Standard Deviation Short" alert signals a possible downward trend when the price crosses below the lower boundary. Visual cues, such as changes in the color of the SMA line, help traders quickly identify trend shifts and act accordingly.

Summary and Usage Tips

The "Sma Standard Deviation | viResearch" indicator provides traders with a robust tool for analyzing market trends and volatility. By combining the benefits of SMA smoothing with SD analysis, this script offers a comprehensive approach to detecting trend changes and managing risk. Incorporating this indicator into your trading strategy can help improve your ability to spot trend reversals, understand market volatility, and stay aligned with the broader market direction. The "Sma Standard Deviation" is a reliable and customizable solution for traders looking to enhance their technical analysis in both trending and volatile markets.

Note: Backtests are based on past results and are not indicative of future performance.

Pine Script®指标