Call-Put Cross Strike Match [Pro]📊 Call-Put Cross Strike Match - Professional Options Trading Indicator

Advanced NSE Options Analysis with AI-Powered Trading Signals & Dynamic Display

🎯 Overview

The Call-Put Cross Strike Match is an institutional-grade options analysis tool designed exclusively for NSE NIFTY and BANKNIFTY traders. Built on Pine Script v6, this indicator combines sophisticated cross-strike matching algorithms with intelligent trading signal generation to identify optimal options trading opportunities in real-time.

What makes it unique:

Analyzes 25 call-put combinations simultaneously

Generates actionable BUY/SELL signals using professional strategies

Fully customizable display with 9 table positions and 6 size options

Simplified setup with semi-automatic ATM detection

Clean, clutter-free interface with only essential information

Perfect for intraday scalpers, premium sellers, and positional options traders.

✨ Key Features

1. 🔍 Advanced Cross-Strike Matching Algorithm

The indicator calculates price differences for all 25 combinations (5 call strikes × 5 put strikes) and identifies the best matches based on put-call parity.

How it works:

Compares each call option price with every put option price

Calculates absolute difference: |Call - Put |

Ranks all 25 combinations from lowest to highest difference

Highlights top 3 or top 5 matches with visual checkmarks

Visual indicators:

✓✓ (Double check) = Best match (lowest price difference)

✓ (Single check) = Good matches (top 3 or top 5)

Empty cells = No match (significant price difference)

Why this matters:

When Call ≈ Put at same strike, it indicates fair pricing and synthetic position opportunities. The indicator automatically finds these opportunities across different strike combinations.

2. 🎯 Intelligent Trading Signals (Last Column)

The indicator generates professional trading recommendations based on Call-Put price difference analysis:

Signal Types:

BUY CE - Long call opportunity (bullish)

SELL CE - Short call opportunity (premium selling)

BUY PE - Long put opportunity (bearish/hedge)

SELL PE - Short put opportunity (premium selling)

BULL - Moderate bullish bias

BEAR - Moderate bearish bias

ATM - Neutral market (near parity)

NEUTRAL - No clear bias

Color-Coded for Quick Decisions:

🟩 Green = Long opportunities (BUY CE, BULL)

🟥 Red = Short call opportunities (SELL CE)

🟧 Orange = Long put opportunities (BUY PE)

🟫 Maroon = Short put opportunities (SELL PE)

⬛ Gray = Neutral zones (ATM, NEUTRAL)

3. 🤖 Three Professional Signal Modes

SMART Mode (Recommended) 🎯

Context-aware institutional strategy that considers strike position relative to spot price.

Signal Logic:

text

OTM Call Expensive (C-P > threshold, Strike > Spot):

→ SELL CE (Premium selling opportunity)

ITM Call Underpriced (C-P > threshold, Strike < Spot):

→ BUY CE (Synthetic long opportunity)

OTM Put Expensive (C-P < -threshold, Strike < Spot):

→ SELL PE (Premium selling opportunity)

ITM Put Underpriced (C-P < -threshold, Strike > Spot):

→ BUY PE (Protection or synthetic short)

Near Parity (|C-P| < threshold/4):

→ ATM (Neutral market, straddle/strangle zone)

Moderate Imbalance:

→ BULL or BEAR (Directional bias without extreme pricing)

Best for: Professional traders, option writers, synthetic position builders

MOMENTUM Mode 📈

Trend-following strategy that rides market momentum.

Signal Logic:

text

Calls Expensive (C-P > threshold):

→ BUY CE (Follow bullish momentum)

Puts Expensive (C-P < -threshold):

→ BUY PE (Follow bearish momentum)

Near Parity:

→ NEUTRAL (No clear trend)

Best for: Intraday scalpers, directional traders, swing traders

MEAN REVERSION Mode 🔄

Counter-trend strategy focused on premium selling.

Signal Logic:

text

Calls Overpriced (C-P > threshold):

→ SELL CE (Collect inflated premium)

Puts Overpriced (C-P < -threshold):

→ SELL PE (Collect inflated premium)

Near Parity:

→ ATM (Fair value, no edge)

Best for: Option writers, theta decay strategies, credit spread traders

4. 🎨 Fully Customizable Display

Dynamic Table Positioning (9 Options):

Top: left, center, right

Middle: left, center, right

Bottom: left, center, right

Choose position based on your chart layout and other indicators.

Dynamic Table Sizing (6 Options):

Auto - Adapts to content

Tiny - Minimal space (for cluttered charts)

Small - Default, best balance

Normal - Medium size (1080p monitors)

Large - Big text (4K monitors)

Huge - Maximum size (presentations)

Text scales intelligently:

Headers, data, and checkmarks adjust proportionally

Checkmarks remain visible even in tiny mode

Info row stays readable at all sizes

5. ⚙️ Simplified Input System

Auto Mode (Recommended):

Enter just 5 strikes once at market open - used for both calls and puts.

Example for NIFTY at 25,900:

text

Strike 1: 25850 (ATM - 100)

Strike 2: 25900 (ATM - 50)

Strike 3: 25950 (ATM)

Strike 4: 26000 (ATM + 50)

Strike 5: 26050 (ATM + 100)

Manual Mode (Advanced):

Enter separate call and put strikes for cross-strike arbitrage analysis.

Why this matters:

50% fewer inputs compared to traditional indicators

One-time setup at market open

Rarely needs updating (only if market moves 100+ points)

6. 🎛️ Semi-Automatic ATM Detection

The indicator automatically:

Detects current NIFTY/BANKNIFTY spot price

Calculates ATM strike (rounded to nearest 50 or 100)

Marks ATM strikes with *ATM in the table

Displays ATM and spot price in info box

No manual recalculation needed!

7. 📊 Clean Information Display

Main Table (Top/Middle/Bottom):

CE \ PE matrix showing all strike combinations

Checkmarks (✓✓ and ✓) highlighting best matches

SIGNAL column with color-coded trading recommendations

Best Match footer showing optimal combination

Info row displaying symbol, signal mode, and spot price

Info Box (Bottom Left):

Symbol (NIFTY/BANKNIFTY)

Signal Mode (Smart/Momentum/Mean Reversion)

Current Spot Price

Detected ATM Strike

Best Matched Call Strike

Best Matched Put Strike

Match Difference

C-P value for best match

📋 Quick Setup Guide (3 Steps)

Step 1: Add Indicator

Open NIFTY or BANKNIFTY chart on TradingView

Add "Call-Put Cross Strike Match " from indicators

Step 2: Configure Basic Settings

text

Symbol Detection: Auto (reads from chart)

Expiry Date: 251219 (format: YYMMDD for 19-Dec-2025)

Strike Mode: Auto

Strike Interval: 50 (for NIFTY) or 100 (for BANKNIFTY)

Step 3: Enter Strikes

At market open (9:15 AM), check current price and enter 5 strikes:

text

Example: NIFTY at 25,937

Strike 1: 25850 (ATM - 100)

Strike 2: 25900 (ATM - 50)

Strike 3: 25950 (ATM) ← Rounded to nearest 50

Strike 4: 26000 (ATM + 50)

Strike 5: 26050 (ATM + 100)

That's it! The indicator handles everything else automatically.

💡 Real-World Use Cases

1. 📉 Premium Selling (Mean Reversion Mode)

Scenario: Looking for overpriced options to write

How to use:

Set Signal Mode to "Mean Reversion"

Set Threshold: 30 (NIFTY) or 75 (BANKNIFTY)

Look for SELL CE or SELL PE signals with ✓ or ✓✓

Sell naked options or credit spreads at those strikes

Target 30-50% profit or 3-5 days theta decay

Perfect for: Credit spreads, iron condors, covered calls, naked puts

2. 📈 Directional Trading (Momentum Mode)

Scenario: Scalping intraday moves

How to use:

Set Signal Mode to "Momentum"

Set Threshold: 15 (aggressive) or 25 (conservative)

BUY CE signal + ✓✓ = Long call entry

Enter with tight stop (20% of premium)

Target 30-50% gain within 1-2 hours

Perfect for: Intraday scalping, swing trading, trend following

3. 🔄 Synthetic Positions (Smart Mode)

Scenario: Building synthetic long/short with defined risk

How to use:

Set Signal Mode to "Smart"

Look for BUY CE at ITM strike + SELL PE at OTM strike

Both should have ✓ indicator (good parity)

Creates synthetic long position

Lower capital than buying futures

Perfect for: Professional traders, arbitrage, capital efficiency

4. ⚖️ ATM Strategy Optimization (Smart Mode)

Scenario: Finding optimal strikes for straddle/strangle

How to use:

Identify strike marked *ATM

Check if signal shows ATM (balanced market)

If BULL/BEAR → Market has directional bias, adjust accordingly

✓✓ indicates best matched strike for neutral strategies

Perfect for: Volatility trading, earnings plays, event trading

5. 🛡️ Hedging Optimization (Smart Mode)

Scenario: Protecting long equity positions

How to use:

Look for BUY PE signals (protection signals)

Avoid strikes with SELL PE (expensive hedges)

✓✓ shows best value for hedge entry

Optimize hedge timing and strike selection

Perfect for: Portfolio hedging, risk management, protective puts

⚙️ Settings Guide

Symbol Settings

Symbol Detection: Auto (recommended) or Manual

Manual Symbol: NIFTY or BANKNIFTY

Expiry Date: Format YYMMDD (e.g., 251219 = 19-Dec-2025)

Update every Thursday after 3:30 PM for next week's expiry

Strike Settings

Strike Mode: Auto (recommended) or Manual

Strike Interval:

50 for NIFTY

100 for BANKNIFTY

Trading Signals

Signal Mode: Smart / Momentum / Mean Reversion

Smart: Professional institutional strategy (default)

Momentum: Trend-following for scalpers

Mean Reversion: Premium selling for writers

Signal Threshold: Sensitivity in points

NIFTY Recommendations:

Conservative: 30-40 points (fewer, higher quality signals)

Balanced: 20-25 points (default)

Aggressive: 10-15 points (more signals, more noise)

BANKNIFTY Recommendations:

Conservative: 75-100 points

Balanced: 50-60 points (default)

Aggressive: 30-40 points

Algorithm Settings

Matching Mode:

Top 3: Shows 3 best matches (cleaner display)

Top 5: Shows 5 best matches (more opportunities)

Display Settings

Show Matching Table: Enable/disable main table

Table Position: Choose from 9 positions

top_right (default) - Doesn't block price action

middle_right - Centered vertical view

bottom_right - If top is crowded

Table Size: Choose from 6 sizes

small (default) - Best for most users

normal - For 1080p/4K monitors

tiny - If you have many indicators

📊 Understanding The Table

Table Layout Example:

text

CE \ PE | 25950 | 25900 | 25850 | 26000 | 26050 | SIGNAL

---------|-------|-------|-------|-------|-------|--------

25850 | | | | | | SELL PE

25900*ATM| | ✓ | | | | ATM

25950 | ✓✓ | | | | | BULL

26000 | | | | ✓ | | BUY CE

26050 | | | | | | SELL CE

---------|-------|-------|-------|-------|-------|--------

Best Match: 25950 / 25950 (0.25)

Info: NIFTY | Smart | Spot:25881.9

Reading the Table:

Rows (Left): Call option strike prices

Columns (Top): Put option strike prices

Cells: Checkmarks where Call ≈ Put

✓✓: Best match (minimum price difference)

✓: Good matches (top 3 or 5)

Empty: Prices too different (no match)

*ATM: Automatically detected at-the-money strike

SIGNAL Column: Actionable trading recommendation for each call strike

Info Box Metrics:

Symbol: Currently analyzed index

Signal Mode: Active strategy

Spot: Current underlying price

ATM: Calculated at-the-money strike

Best Call: Matched call strike

Best Put: Matched put strike

Match Diff: Price difference (lower = better)

C-P (Best): Call minus Put for best match

📈 Best Practices

Strike Selection & Maintenance

At Market Open (9:15 AM):

Check current price (e.g., NIFTY at 25,937)

Round to nearest interval (25,950 for 50 interval)

Enter 5 strikes: -100, -50, 0, +50, +100 from ATM

Update Frequency:

Usually no update needed entire day

Update only if market moves 100+ points from initial ATM

Typically 0-2 updates per trading session

Signal Interpretation by Confidence Level

High Confidence (✓✓ + Signal):

Best match indicator present

Strongest signal quality

Highest probability setup

Medium Confidence (✓ + Signal):

Good match present

Reliable signal

Acceptable risk/reward

Low Confidence (Signal without ✓):

No match indicator

Strike far from parity

Requires additional confirmation

Risk Management Rules

Never trade signals blindly. Always:

✅ Confirm with price action and support/resistance

✅ Check overall market trend (NIFTY/BANKNIFTY direction)

✅ Consider time decay (theta) for your position

✅ Monitor IV changes (implied volatility)

✅ Use proper position sizing (1-2% risk per trade)

✅ Set stop losses (20-30% of premium for longs)

✅ Have profit targets (30-50% for scalps)

Timeframe Selection

Intraday Trading:

Use 5-minute or 15-minute chart

Momentum or Smart mode

Lower threshold (aggressive)

Quick entries and exits

Positional Trading:

Use hourly or daily chart

Smart or Mean Reversion mode

Higher threshold (conservative)

Swing trade positions

Combining with Other Tools

Recommended complements:

Support/resistance levels (horizontal lines)

Trend indicators (EMA 20/50, SuperTrend)

Volume analysis (confirm breakouts)

India VIX (volatility context)

Option chain data (open interest)

🎓 Strategy Examples

Strategy 1: Professional Premium Selling

text

Mode: Mean Reversion

Threshold: 30 (NIFTY) / 75 (BANKNIFTY)

Timeframe: Daily

Rules:

1. Wait for SELL CE or SELL PE signal

2. Verify strike has ✓ or ✓✓ (good parity)

3. Check if OTM (Strike away from spot)

4. Sell option or create credit spread

5. Target: 30-50% profit or 3-5 days theta

6. Stop: If signal changes to BUY

Position: Naked short or credit spreads

Risk: Define with spreads or capital allocation

Strategy 2: Intraday Momentum Scalping

text

Mode: Momentum

Threshold: 15 (aggressive)

Timeframe: 5-minute

Rules:

1. Wait for BUY CE signal + ✓✓

2. Enter long call immediately

3. Stop loss: 20% of premium paid

4. Target 1: 30% gain (partial exit)

5. Target 2: 50% gain (full exit)

6. Exit if signal changes or 2 hours pass

Position: Long calls or long puts only

Risk: 1-2% of capital per trade

Strategy 3: Synthetic Long Position

text

Mode: Smart

Threshold: 25 (NIFTY) / 60 (BANKNIFTY)

Timeframe: Hourly

Rules:

1. Identify BUY CE signal at ITM strike

2. Identify SELL PE signal at OTM strike

3. Both should have ✓ indicator

4. Buy ITM call + Sell OTM put = Synthetic Long

5. Lower capital than futures

6. Defined risk (width of strikes)

Position: Call debit + Put credit

Risk: Net debit paid (defined risk)

Strategy 4: ATM Straddle Entry

text

Mode: Smart

Threshold: 20 (default)

Timeframe: Daily

Rules:

1. Find strike marked *ATM

2. Check signal shows "ATM" (neutral)

3. Verify ✓✓ at that strike

4. Sell ATM call + Sell ATM put

5. Collect maximum premium

6. Exit at 30% profit or before expiry

Position: Short straddle or iron condor

Risk: Use defined risk (iron condor recommended)

🔔 Important Notes

Data Accuracy

Indicator uses TradingView's NSE options data feed

Always verify prices independently before trading

Ensure market is open (9:15 AM - 3:30 PM IST)

Check for "-" in cells indicating missing data

Expiry Management

Update expiry date every week on Thursday post-closing

Format: YYMMDD (6 digits)

Weekly expiry: Every Thursday

Monthly expiry: Last Thursday of month

Strike Format

NIFTY: Multiples of 50 (25850, 25900, 25950...)

BANKNIFTY: Multiples of 100 (51800, 51900, 52000...)

Wrong strikes = No data in table

Performance Optimization

Indicator updates every bar close

No lag or performance issues

Works on all timeframes (1m to 1D)

Maximum 5 calls + 5 puts = 10 security calls (within limits)

⚠️ Disclaimer

Trading options involves substantial risk of loss and is not suitable for all investors. This indicator is provided for educational and informational purposes only. It does not constitute financial advice, investment advice, or trading advice.

Important disclaimers:

Options can expire worthless, resulting in 100% loss

Past performance of signals is not indicative of future results

Accuracy depends on TradingView's NSE data feed

Signals are mathematical analysis, not predictions

You are solely responsible for your trading decisions

The developer is not liable for any trading losses incurred while using this indicator.

Before trading, ensure you understand:

Options Greeks (Delta, Gamma, Theta, Vega, Rho)

Implied volatility and its impact

Time decay and expiration risks

Assignment risk for short positions

Liquidity and slippage considerations

Margin requirements and capital needs

Always:

Use proper risk management (1-2% per trade)

Trade with capital you can afford to lose

Paper trade before live trading

Consult with a licensed financial advisor

Start with small position sizes

Never risk more than you can afford to lose

📊 Technical Specifications

Platform: TradingView Pine Script v6

Exchanges: NSE (National Stock Exchange of India)

Instruments: NIFTY, BANKNIFTY options

Timeframes: All (1m, 5m, 15m, 1h, 1D)

Strikes Analyzed: 5 calls × 5 puts = 25 combinations

Security Calls: 10 (5 calls + 5 puts)

Table Positions: 9 (all corners and centers)

Table Sizes: 6 (auto to huge)

Signal Modes: 3 (Smart, Momentum, Mean Reversion)

Performance: Optimized, minimal lag

🎯 Who Should Use This?

✅ Perfect For:

Options Traders: Intraday and positional

Premium Sellers: Option writers and theta strategists

Arbitrage Traders: Synthetic position builders

Straddle/Strangle Traders: ATM strategy traders

Professional Traders: Institutional-grade analysis

Volatility Traders: IV imbalance exploiters

Scalpers: Quick intraday moves

❌ Not Suitable For:

Stock options traders (NSE index-specific)

Equity-only traders (requires options knowledge)

International markets (NSE format only)

Complete beginners (requires basic options understanding)

💬 FAQ

Q: Why manual strike entry? Why not fully automatic?

A: Pine Script's type system limits fully automatic strike generation from live data. However, setup takes just 30 seconds once at market open, and the indicator handles all analysis automatically throughout the day.

Q: How often should I update strikes?

A: Rarely! Only when market moves 100+ points from initial ATM. Usually 0-2 times per day, even in volatile markets.

Q: Which Signal Mode is best?

A: Smart mode (default) for professional trading. Use Momentum for intraday scalping, Mean Reversion for premium selling.

Q: Can I use this for stock options?

A: No. The indicator is designed specifically for NSE index options (NIFTY and BANKNIFTY) with NSE format.

Q: Does it work on mobile?

A: Yes, but table display is optimized for desktop/tablet screens. Use "tiny" or "small" size on mobile.

Q: What if I see "-" in cells?

A: Check expiry format (YYMMDD), verify strikes match NSE strikes, and ensure market is open.

Q: What's the difference between ✓✓ and ✓?

A: ✓✓ = Best match (lowest price difference), highest quality. ✓ = Good matches (top 3-5), reliable quality.

Q: Can I backtest this indicator?

A: The indicator shows live analysis. For backtesting options strategies, you'll need historical options data and separate backtesting tools.

Q: What does the info box show?

A: Bottom-left box shows key metrics: symbol, signal mode, spot price, ATM strike, best matched strikes, match difference, and C-P value.

Q: Why no chart plotting?

A: v1.0 focuses on clean table display with maximum information density. Chart plotting may be added in future versions based on user feedback.

🙏 Credits

Developed by a professional options trader for the Indian trading community. Inspired by institutional trading desks and market makers who use call-put parity for daily trading decisions.

Found This Helpful?

⭐ Rate 5 stars if it improved your trading

💬 Comment with your strategy results

🔔 Follow for updates and new indicators

📢 Share with fellow options traders

Feature Requests

Continuous improvement based on trader feedback. Suggest features in comments!

Planned Features (v2.0):

Multi-expiry comparison

Greeks display (Delta, Theta, Vega)

Historical signal performance stats

Custom signal formulas

Export to CSV functionality

🏷️ Tags for Search

#Options #OptionsTrading #NIFTY #BANKNIFTY #NSE #India #OptionChain #CallPut #PutCallParity #Straddle #Strangle #ATM #TradingSignals #OptionsStrategy #PremiumSelling #OptionsScanner #Derivatives #IntradayTrading #VolatilityTrading #Arbitrage #SyntheticPosition #OptionsGreeks #OptionsSelling #OptionsWriting #IndianStockMarket #NSEOptions #OptionsAnalysis #TechnicalAnalysis #AlgoTrading #QuantTrading #ProfessionalTrading #TradingIndicator #PineScript #TradingView

📝 Version History

v1.0 (Current - Dec 2025)

Pine Script v6 implementation

Cross-strike matching (5×5 matrix, 25 combinations)

Three signal modes (Smart, Momentum, Mean Reversion)

Trading signal generation with color coding

Dynamic table positioning (9 positions)

Dynamic table sizing (6 sizes)

Intelligent text scaling

Semi-automatic ATM detection

Auto symbol detection

Simplified input system (50% fewer inputs in Auto mode)

Clean information display

Info box with key metrics

NSE NIFTY & BANKNIFTY support

Start trading smarter with institutional-grade options analysis! 📈💰🚀

Disclaimer: Options trading is subject to market risk. Please read all scheme-related documents carefully before investing.

Statistics

UT Bilgi Paneli (Ugur TUFAN) English Description

UT Info Panel (Advanced Performance & Correlation Dashboard)

UT Info Panel is a comprehensive dashboard designed to help traders analyze the performance of an asset over multiple timeframes and compare it instantly with other assets or benchmark indices.

This tool overlays on the main chart, providing critical data in a clean, organized table located at the top-right corner without cluttering your workspace.

Key Features:

Detailed Performance Analysis:

Displays percentage returns for Daily, Weekly, Monthly, 3-Month, 6-Month, and 1-Year periods.

High & Low Distance Metrics:

Calculates the percentage distance to the 52-week (1 Year) High and Low levels.

Shows the distance to the All-Time High (ATH), helping to visualize potential recovery or growth margins.

Smart Dual Mode:

Mode 1 (Index Harmony): If no comparison symbols are entered, it compares the current asset with a benchmark index (e.g., XU100). It visually indicates directional correlation (Harmony) with checkmarks (✔) or crosses (✖).

Mode 2 (Multi-Asset Comparison): By adding up to 5 different symbols in the settings, the table automatically expands to show a side-by-side performance comparison of all selected assets.

Localized Visualization:

Data is presented with clear color coding (Green for positive, Red for negative) for easy reading.

How to Use:

When added, it defaults to the harmony mode with the benchmark index.

Open settings to input up to 5 different symbols you wish to compare.

The table automatically adjusts its size and positions itself at the top right.

Deviation Burn + Pivots + Advanced stop + Midpoint CancelA session-based range strategy that places buy and sell orders at the session high and low, expecting price reactions from these levels.

Additional filters help avoid low-probability trades.

Improved Candle Strategy (without daily squared)# Candle Pattern Trading Strategy

## Core Logic

Analyzes the last 5 candlesticks to identify "close at high" and "close at low" patterns, generating long/short signals.

## Trading Conditions

- **Long**: ≥2 bars closed at high in past 5 bars + current bar closes at high → Open long

- **Short**: ≥2 bars closed at low in past 5 bars + current bar closes at low → Open short

- **Filter**: If ≥3 doji patterns detected, skip trading

## Risk Management

- Stop Loss: Based on entry bar's high/low

- Take Profit: Risk × 2x multiplier

- Cooldown: No trading for 2 bars after entry

- Session Filter: No trading for first 5 bars after market open

## Configurable Parameters

- Lookback period, doji threshold, close proximity ratio, TP/SL ratio, cooldown bars, etc.

**Use Cases**: 1-minute and higher timeframes on stocks/futures

Day of WeekDay of Week is an indicator that runs in a separate panel and colors the panel background according to the day of the week.

Main Features

Colors the background of the lower panel based on the day of the week

Includes all days, from Monday to Sunday

Customizable colors

Time Offset Correction

TradingView calculates the day of the week using the exchange’s timezone, which can cause visual inconsistencies on certain symbols.

To address this, the indicator includes a configurable time offset that allows the user to synchronize the calculated day with the day displayed on the chart.

By simply adjusting the Time Offset (hours) parameter, the background will align correctly with the visible chart calendar.

Momentum Table View (Bar-Based)// NOTE:

// This script uses bar-based lookbacks instead of calendar months.

// Approximate conversions for daily charts:

// - 21 bars ≈ 1 month

// - 63 bars ≈ 3 months

// - 252 bars ≈ 1 year

// For other timeframes, adjust accordingly for different time periods and needs.

// For hourly I have it set at 24*5, 24*5*4 and then finally 24*5*4 to give the same,

// daily, weekly and monthly aggregate returns but on the hourly scale.

// Of course you can split it anyway you like as well depends on the expected needs you have.

Running idea so there will likely be revisions to the z scoring to possibly a different method and the atan angle represented in the code will also likely be changed at some point as to maybe a regression method. These changes will take time as this is only a secondary platform for me not the main source of data. In saying that the table has the data representing the log returns of an asset of n bars which I decided on over the original more accurate daily, weekly and monthly close points which the user can always specify using this method if wanting to be more accurate with the standard method of momentum returns factor.

EMA Slope Angle V2 Auto Threshold# EMA Slope Angle Indicator

## Overview

The EMA Slope Angle Indicator visualizes the Exponential Moving Average (EMA) slope as an angle in degrees, providing traders with a clear, quantitative measure of trend strength and direction. The indicator features **automatic threshold calculation based on Gaussian distribution**, making it adaptive to any market and timeframe.

## Key Features

### 🎯 **Automatic Threshold Calculation (NEW!)**

- **Gaussian Distribution-Based**: Automatically calculates optimal thresholds from the 50% interquartile range (IQR) of historical angle data

- **Asset-Adaptive**: Thresholds adjust to each instrument's unique volatility and price characteristics

- **No Manual Tuning Required**: Simply enable "Use Auto Thresholds" and let the indicator optimize itself

### 📊 **Dynamic EMA Coloring**

- **Color Intensity**: EMA line color intensity reflects slope strength

- **Visual Feedback**:

- Green shades for uptrends (darker = stronger)

- Red shades for downtrends (darker = stronger)

- Gray for flat/neutral conditions

### 📈 **Regime Detection**

- **Three Regimes**: RISING, FALLING, and FLAT

- **Smart Classification**: Based on statistical distribution of angles

- **Non-Repainting**: All calculations use confirmed bars only

### 🔔 **Trend-Shift Signals**

- **Visual Arrows**: Automatic signals when transitioning from FLAT to RISING/FALLING

- **Configurable**: Enable/disable signals as needed

- **Reliable**: Only triggers on significant regime changes

### 📋 **KPI Dashboard**

- **Real-Time Metrics**: Current angle, regime, and last signal

- **Auto-Threshold Display**: Shows calculated thresholds when auto-mode is active

- **Statistics**: Optional angle distribution statistics

- **Clean Layout**: Top-right corner, non-intrusive

### 📊 **Angle Statistics (Optional)**

- **Distribution Analysis**: Histogram of angle ranges

- **Dynamic Buckets**: Automatically adjusts to data distribution when auto-mode is enabled

- **Percentage Breakdown**: See how often each angle range occurs

## Settings

### Main Settings

- **EMA Length**: Period for the Exponential Moving Average (default: 50)

- **Slope Lookback Bars**: Number of bars to calculate slope over (default: 5)

### Angle Settings

- **Use Auto Thresholds**: Enable automatic threshold calculation (recommended!)

- **Analysis Period**: Number of bars to analyze for distribution (default: 500)

- **Manual Thresholds**: Flat, Rising, and Falling triggers (used when auto-mode is off)

- **Max Angle for Color Saturation**: Maximum angle for color intensity scaling

### Display Options

- **Colors**: Customize uptrend, downtrend, and flat colors

- **Show Signals**: Enable/disable trend-shift arrows

- **Show Statistics**: Display angle distribution table

- **Show Dashboard**: Toggle KPI dashboard visibility

## How It Works

### Angle Calculation

The indicator calculates the angle between the current EMA value and the EMA value N bars ago:

```

Angle = arctan((EMA_now - EMA_then) / lookback) × 180° / π

```

### Auto-Threshold Calculation

When enabled, the indicator:

1. Analyzes historical angle data over the specified period

2. Calculates mean and standard deviation

3. Determines thresholds based on the 50% interquartile range (IQR):

- **Flat Threshold**: ±0.674σ (middle 50% of data)

- **Rising Trigger**: 75th percentile (mean + 0.674σ)

- **Falling Trigger**: 25th percentile (mean - 0.674σ)

### Regime Classification

- **FLAT**: Angle within ±Flat Threshold

- **RISING**: Angle ≥ Rising Trigger

- **FALLING**: Angle ≤ Falling Trigger

## Use Cases

### Trend Following

- Identify strong trends (high angle values)

- Spot trend reversals (regime changes)

- Filter trades based on trend strength

### Range Trading

- Detect flat/consolidation periods

- Avoid trading during choppy markets

- Enter when regime shifts from FLAT to RISING/FALLING

### Multi-Timeframe Analysis

- Apply to different timeframes for confirmation

- Use higher timeframe for trend direction

- Use lower timeframe for entry timing

## Tips for Best Results

1. **Enable Auto-Thresholds**: Let the indicator adapt to your instrument

2. **Adjust Analysis Period**: Use more bars for stable markets, fewer for volatile ones

3. **Combine with Price Action**: Use regime changes as confirmation, not standalone signals

4. **Multi-Timeframe**: Check higher timeframes for trend context

5. **Backtest First**: Test settings on historical data before live trading

## Technical Details

- **Non-Repainting**: All calculations use `barstate.isconfirmed`

- **Pine Script v6**: Latest version for optimal performance

- **Efficient**: Minimal computational overhead

- **Customizable**: Extensive settings for fine-tuning

## Version History

**v2.0** (Current)

- Added automatic threshold calculation based on Gaussian distribution

- Dynamic bucket adjustment for statistics

- Enhanced dashboard with auto-threshold display

- Improved regime detection using IQR method

**v1.0**

- Initial release with manual thresholds

- Basic EMA coloring

- Trend-shift signals

- KPI dashboard

## Support

For questions, suggestions, or bug reports, please leave a comment or contact the author.

---

**Disclaimer**: This indicator is for educational purposes only. Past performance does not guarantee future results. Always use proper risk management and never risk more than you can afford to lose.

**Keywords**: EMA, slope, angle, trend, automatic thresholds, Gaussian distribution, regime detection, non-repainting, adaptive

EM Levelsstdv levels for you using VIX and VXN for ES and NQ so hopefully it helps you try it out and have fun

Session HeatmapIntraday Seasonality

Overview

Analyzes historical patterns by time of day. Identifies when volatility, volume, and open interest changes tend to be highest or lowest.

Features

Multiple Metrics: TR (volatility), Volume, and Open Interest changes

Flexible Grouping: View patterns by weekday or month to spot day-of-week or seasonal effects

Heatmap Visualization: Blue (low) to Red (high) color scale for quick pattern recognition

Percentile Mode: Reduces outlier impact by using 5th-95th percentile range

Timezone Support: Display in UTC alongside your local time

Metrics Explained

TR: Volatility - when markets move most

Volume: Liquidity - when participation is highest

OI Increase: When new positions are opened

OI Decrease: When positions are closed

OI Net: Net open interest change

Usage

Set your timezone and preferred slot size (30min/1H)

Choose a date range (relative or custom)

Select a metric to analyze

Use "Group By" to see weekday or monthly patterns

Switch to Percentile color scale if outliers dominate

Notes

Chart timeframe should be equal to or smaller than Slot Size

OI metrics require Binance Perpetual symbols

DST is not automatically adjusted; consider seasonal shifts for US/EU sessions

Probability-Based Adaptive Detection🙏🏻 PBAD (Probability-Based Adaptive Detection) : adaptive control tool for outliers || novelty detection, made for worst case data & processes, for the highest time complexity O(n^2) compared with the alternatives (would be explained in a sec). Thresholds are completely data driven and axiomatic, no need in provided hyperparameters, are not learned or optimized. The method accepts multiple weights, e.g. both temporal and volatility weights.

Method briefly explained (I can go deeper if any1 asks explicitly):

Performs weighted KDE on initial input data, finds KDE global maximum (mode), creates new “residuals” dataset by centering initial data around this value;

Performs weighted KDE on residuals, uses sigmoid based probability mass targets with increasing probability coverage to construct a set of non-disjoint High Density Intervals (also called HDR, HPD in Bayesian terms);

Uses these intervals to calculate analogs of centralized & standardized moments;

Uses these ^^ moments to construct a set of control thresholds. The scheme used in PBAD is not only based on a central threshold, or on neighboring ones, it utilizes all previous thresholds, gaining more information.

...

The most important part is to understand whether you really need PBAD. Because even tho it seems to be the best one given highest algocomplexity, irl it would work worse in cases when it’s not required by your data.

Here’s the menu (aka taxonomy omg) of methods you can use that would let you make the right choice:

Moment-Based Adaptive Detection (MBAD) :

Norm: L2

Time complexity: original O(n), successfully reduced to O(1) in online version

Use case: default, general purpose

Based on: method of moments (powers of residuals from mean)

Thresholds architecture: centralized

Quantile-Based Adaptive Detection (QBAD):

Norm: L1

Time complexity: O(nlogn)

Use case: either bad data Or process instability

Based on: quantile moments (dyadic percentiles of residuals from median)

Thresholds architecture: chained/recursive/sequential

Probability-Based Adaptive Detection (PBAD):

Norm: L0

Time complexity: O(n^2)

Use case: both bad data And process instability

Based on: probability moments (target probability masses of residuals from KDE mode)

Thresholds architecture: decentralized (for lack of a better name xd, the idea is that these thresholds gain information from the all other threshold and are Not exclusively based on the central or neighboring thresholds)

...

Examples of true use cases:

^^ an appropriate financial instrument to use PBAD

^^ and another one

...

Additional details about how to use it:

Keep the student5 kernel, it’s the best you can do. I added others mostly for comparisons and if you want to use the tool Not for its primary purpose (on a fine data)

“Calculate for N bars” and “Starting at bar N” options allow to reduce calculation period only on the N number of last bars or next bars from a chosen one. It's vital, because calculations here are heavy

Keep plotting offset at 1 (allows to visually compare current bar with the previous threshold values). This is the way it should be done on price data.

HLC3 is the optimal source input, unless you want to use your own better one point estimate of each datapoint (in the best case done by using PBAD itself on OHLC+ values).

In essence it should be used just like MBAD or QBAD, fade/push extensions and limit, fade/push/skip deviations & basis, or other strategies of your. Again, the only reason for 3 methods to exist is to be chosen for according data characteristics.

Btw:

This is the initial version, I don’t consider it perfected tbh, even tho it works as expected, however this method is very situational anyways.

In this script KDE function is modified to ensure the outcoming probabilities Do sum up to 1. I didn’t do this normalization in Weighted KDE Mode script , but there it’s not required since we just need a KDE global max.

see ya

∞

GC1! H1 Stats+GC1! H1 Stats - Detailed Prob & Excursion Indicator

Overview

GC1! H1 Stats - Detailed Prob & Excursion is a specialized statistical overlay indicator for TradingView, tailored for Gold futures (GC1!) on a 1-hour framework. It provides real-time insights into the probability of price returning to the hourly open after sweeping the previous hour’s high (PHH) or previous hour’s low (PHL), based on historical data segmented by hour (0–23) and 20-minute intervals. The indicator visualizes these sweeps with lines, labels, circles, background fills, and “excursion zones” (also called “Magic Boxes”) that highlight median/mean extensions post-sweep, along with percentile lines (75th / 90th / 95th) for gauging potential “pain” or extreme moves. This tool is designed for intraday Gold traders focusing on liquidity sweeps and mean-reversion behavior, helping to quantify edge using empirical probabilities and excursion statistics.

The data is hardcoded from extensive historical analysis of GC1! behavior (e.g., probabilities ranging roughly from ~7% to ~91%, with sample sizes up to 2000+ per segment), making it a backtested reference rather than a dynamic learning model. It emphasizes visual clarity during active hours, with options to filter for Regular Trading Hours (RTH: 09:00–15:59 ET) or high-probability (>70%) events only. Note: This is an educational tool for analyzing market structure; it does not predict future performance or provide trading signals/advice. Past data does not guarantee future results, and users should backtest on current conditions (as of December 2025 data availability) and use at their own risk, in compliance with TradingView’s house rules.

________________________________________

Key Features

• Sweep Detection & Probability Labels: Identifies when price breaks PHH (upside) or PHL (downside), displaying a centered label with probability of returning to the hourly open, sample size (N), time of sweep, and a checkmark (✅) if the open is retested post-sweep.

• Visual Lines & Markers: Draws hourly open (h.o.), PHH, and PHL lines with customizable styles/colors; adds small circles on sweep bars for quick spotting.

• Breakout→Open Background Fill: Shaded zone from sweep bar until price returns to open, visualizing extension duration and retracement.

• Excursion (Pain) Zone - “Magic Box”: Post-sweep box showing median/mean extension percentages, colored dynamically by probability (green high, orange mid, red low); includes dashed lines for 75th/90th/95th percentiles to mark statistical extremes.

• Time-Segmented Data: Probabilities and excursions vary by hour (0–23) and 20-min segments (0–19 min: _0, 20–39: _1, 40–59: _2), capturing intraday nuances (e.g., higher probs in early/late hours).

• Filters for Focus: RTH-only mode hides non-session elements; high-prob-only shows >70% events to reduce noise.

• Alerts: Triggers on PHH/PHL sweeps with messages for chart checks.

________________________________________

How It Works

• Data Foundation: Uses pre-computed maps for probabilities (prob_high_taken/prob_low_taken), sample sizes, and excursions (mean, median, p75/p90/p95 as percentages of open). Data is initialized on the first bar via f_init_high_data() and f_init_low_data(), covering 24 hours with 3 segments each (e.g., key "9_1" for 09:20–09:39). Probabilities represent historical likelihood of price returning to open after sweep; excursions quantify average/rare extensions (e.g., 0.156% mean = 0.156% of open price).

• Period Detection: On new 1H bars (new_period_bar), resets visuals, draws lines for open/PHH/PHL extending 1 hour forward, and labels if enabled. Uses request.security on standard ticker for real OHLC, bypassing chart transformations (e.g., Heikin Ashi).

• Sweep Logic: On each bar, checks if real high > PHH or real low < PHL. If so, fetches segment-specific data (hour + floor(minute/20)), displays probability label centered mid-hour. Skips if filtered (RTH-only or <70% prob).

• Excursion Visualization: If enabled, draws “Magic Box” from 1-min to 58-min into the hour, bounded by mean/median levels (top/bottom adjusted for high/low sweep). Adds percentile lines with labels (e.g., “75%”) at right end. Box color reflects prob strength for quick bias assessment.

• Retest Check: Monitors for open retest post-sweep (high/low cross open, or gap scenarios from prev bar). Adds ✅ to label if hit on subsequent bars (skips sweep bar to avoid false positives). Stops background fill on retest or at 58-min mark.

• Background Fill: Activates on sweep, shades until retest, using user color.

• Cleanup & Performance: Manages labels in arrays, clears on new periods; no excess drawing beyond max counts (500 lines/labels/boxes).

This setup blends statistical backtesting with real-time visualization: hardcoded data provides empirical probabilities/excursions (reducing subjectivity in breakouts), while dynamic elements (lines, fills, boxes) overlay structure on the chart. It helps Gold traders assess if a sweep is “high-edge” (e.g., >70% probability of reverting) or likely to run (low probability, high excursion), pairing historical context with current price action.

________________________________________

Settings and Customization

Inputs are grouped for ease:

1. Settings:

o Show RTH Only (9:00–15:59): Restricts to main session (default: false; tooltip: for RTH-focused stats).

o Show High Prob Only (>70%): Filters low-prob sweeps visually (default: false; tooltip: highlights confidence).

2. Visuals:

o Show Line Labels: Toggle “h.o.” / “phh” / “phl” (default: true).

o Period Open Line Color: Gray 50% (default).

o Previous High/Low Line Colors: Gray 100% (default).

o Open Line Style/Width: Dotted/1 (default; options: Solid/Dotted/Dashed).

3. Breakout→Open Background:

o Show Breakout→Open Background: Toggle fill (default: true).

o Fill Color: Teal 85% (default).

4. Breakout Circles:

o Show Breakout Circles: Toggle (default: true).

o PHH/PHL Break Circle Colors: White 20% (default).

5. Info Label Style:

o Text Size: Small (default; options: Auto/Tiny/Normal/Large/Huge).

o Label Text Color: White (default).

o Low/Mid/High Probability Colors: Red 20% / Orange 20% / Green 20% (default).

6. Excursion (Pain) Zone:

o Show Excursion Zone: Toggle Magic Box (default: true).

o Excursion Box Color: Gray 75% (default; dynamic overrides).

o 75th/90th/95th Percentile Lines: Orange 30% / Red 30% / Dark Red 100% (default).

No additional tables/plots; all elements are lines/labels/boxes for overlay focus.

________________________________________

Usage Tips

• Breakout Trading: Watch for sweeps with high probability (>70%, green label) as potential fades back to open; low probability (red) may signal runs—use the excursion box for targets (e.g., exit at 90th percentile for extremes).

• Time Awareness: Probabilities often peak in key liquidity windows and drop in quieter hours; segments capture momentum shifts (e.g., _2 often lower prob).

• RTH Focus: Enable for cleaner stats during high-liquidity session hours; disable for a 24-hour view.

• Visual Filtering: Use high-prob-only in volatile conditions to reduce noise; combine with volume or other confluence tools for confirmation.

• Alerts Integration: Set TradingView alerts on sweeps; check label for probability/N before acting.

• Chart Setup: Best on 1H or lower GC1! charts; adjust text size for readability on smaller screens.

• Backtesting: Manually review historical sweeps against data maps to validate; update hardcoded values if new data emerges (as of 2025).

________________________________________

Limitations

• Fixed Data: Hardcoded stats may not reflect recent market changes (e.g., post-2025 regime shifts); not adaptive.

• Reactive Only: Detects sweeps after they occur; no predictive signals.

• Timeframe Specific: Locked to 1H logic; may not translate to other assets/timeframes without recoding data.

• Visual Clutter: On busy charts, labels/boxes may overlap—toggle selectively.

• No Live Stats: Sample sizes are historical; real-time N/prob not updated.

• Gaps & Extremes: Handles gaps in retest logic, but rare events (e.g., macro news) may exceed the 95th percentile.

________________________________________

Disclaimer

This indicator is for informational and educational purposes only. Trading involves significant risk of loss and is not suitable for all investors. The hardcoded data represents past Gold futures (GC1!) performance and does not guarantee future outcomes. No claims of profitability are made—results depend on market conditions, user strategy, and risk management. Consult a financial advisor before trading, and backtest extensively. Abiding by TradingView rules, this tool provides no investment recommendations.

BTC - Bitcoin Strategic Dashboard by RM Title: BTC - Bitcoin Strategic Dashboard | RM

Overview & Philosophy

The Bitcoin Strategic Dashboard is a comprehensive analytics tool designed to provide deeper market context beyond simple price action.

While a standard chart displays price history, this dashboard focuses on the structural health of the market. It aims to answer clearer questions: Is the asset statistically overextended? Is the current volatility compressed or expanding? How is Bitcoin currently correlating with traditional equity markets?

This script aggregates key data points—Performance, Risk, Valuation, and Macro Correlations—into a single, organized table. It is designed to be a quiet, high-density reference tool that sits unobtrusively in the corner of your screen, helping to contextualize daily price movements without cluttering your workspace.

Methodology & Module Breakdown

The dashboard is divided into 5 strategic modules. Here is exactly how to read them, how they are calculated, and how to interpret the data.

1. PERFORMANCE

This section answers: "Is Bitcoin actually beating the traditional market, and by how much?"

BTC Return : The raw percentage growth of Bitcoin.

Timeframes: 1-Year (Tactical Trend) and 4-Year (The Halving Cycle).

Alpha (vs SPX / Gold):

Meaning : "Alpha" measures true outperformance. It tells you how much better your capital worked in Bitcoin compared to the S&P 500 (Stocks) or Gold.

Calculation : We use a Relative Growth Ratio. Instead of simple subtraction, we calculate the growth factor of BTC divided by the growth factor of the Benchmark.

Interpretation :

Green: Bitcoin is outperforming. It is the superior vehicle for capital.

Red: Bitcoin is underperforming traditional assets (Opportunity Cost is high).

2. RISK PROFILE

This section answers: "How dangerous is the market right now?"

Drawdown (DD):

Meaning : The percentage loss from the 1-Year High.

Interpretation : Deep Drawdowns (e.g., > -50%) historically signal generational buying opportunities (Deep Red). Small Drawdowns (< -5%) signal we are near "Discovery Mode" (Blue/Green).

Sharpe Ratio:

Meaning : The industry standard for "Risk-Adjusted Return." It asks: "Is the profit worth the stress?"

Timeframe : Annualized over 365 Days.

Interpretation :

> 1.0: Good. The return justifies the risk.

> 2.0: Excellent. (Dark Green).

< 0.0: Bad. You are taking risk for negative returns.

Sortino Ratio:

Meaning : Similar to Sharpe, but it only counts downside volatility as "risk." Bitcoin often rallies aggressively (Good Volatility); Sortino ignores the upside "risk" and focuses only on minimizing losses.

Volatility (Vol) & Rank:

Meaning : How violently the price is moving.

Calculation : We compare the current 30-Day Volatility against the last 4 Years of volatility history (Rank 0-100).

Interpretation (The Squeeze Strategy) :

BLUE (Cold / <25%): Volatility is historically low. The market is "compressed." Big moves often follow these periods.

RED (Hot / >75%): Volatility is extreme. High risk of mean reversion or panic.

3. VALUATION & MOMENTUM

This section answers: "Is Bitcoin cheap or expensive?"

Mayer Multiple (MM):

Meaning: A "Godfather" of Bitcoin ratios.

Calculation : Current Price divided by the 200-Day Moving Average.

Interpretation :

< 0.8 (Blue): Historically "Cheap."

1.0: Fair Value (Price = Trend).

> 2.4 (Red): Speculative Bubble territory.

RSI (Relative Strength Index):

Timeframe : 14 Days.

Interpretation : >70 suggests the market is overheated (Red). <30 suggests oversold conditions (Blue).

Trend (ADX) :

Meaning : The Average Directional Index measures the strength of a trend, not the direction.

Interpretation : Values >25 (Green) indicate a strong trend is present. Values <20 (Gray) indicate a choppy/sideways market (no trend).

vs 200W (Macro):

Meaning : The distance to the 200-Week Moving Average.

Interpretation : This line is historically the "Cycle Bottom" or "Absolute Support" for Bitcoin. Being close to it (or below it) is rare and often marks cycle lows.

4. MACRO CORRELATIONS

This section answers: "Is Bitcoin moving on its own, or just following the Stock Market?"

vs TradFi (SPX):

Timeframe : 90-Day Correlation Coefficient.

Interpretation :

High Positive (Red): BTC is just acting like a tech stock. No "Safe Haven" status.

Negative/Zero (Green): BTC is "decoupled." It is moving independently of Wall Street.

vs DXY (US Dollar):

Interpretation : Bitcoin usually moves inverse to the Dollar.

Negative (Green): Normal healthy behavior.

Positive (Red): Warning signal. If both DXY and BTC rise, something is breaking in the system.

5. HISTORICAL LEDGER

A Year-by-Year breakdown of returns.

Feature : You can toggle the comparison column in the settings to compare Bitcoin against either S&P 500 or Gold.

Usage : Helps visualize the cyclical nature of returns (e.g., the 4-year cycle pattern of Green-Green-Green-Red).

How to Read the Visuals (Heatmap)

The dashboard uses a standardized Bloomberg-style heatmap to let you assess the market state in milliseconds:

🟢 Green: Profit / Good Performance / Positive Alpha.

🔴 Red: Loss / Overheating / High Risk.

🔵 Blue: "Cold" / Cheap / Low Volatility (Potential Buy Zones).

🟠 Orange: Warning / High Drawdown.

⚫ Gray/Black: Neutral or Fair Value.

Settings & Customization

Visuals: Change the text size (Tiny, Small, Normal) to fit your screen resolution.

Modules: You can toggle individual sections on/off to save screen space.

Calculation: Switch the Historical Benchmark between "S&P 500" and "Gold" depending on your thesis.

Disclaimer

This script is for research and educational purposes only. The metrics provided (Sharpe, Sortino, Mayer Multiple) are derived from historical data and do not guarantee future performance. "Cheap" (Low Mayer Multiple) does not mean the price cannot go lower. Always manage your own risk.

Tags

bitcoin, btc, bloomberg, terminal, dashboard, onchain, mayer multiple, sharpe ratio, volatility, alpha, risk management, Rob Maths

Student Wyckoff Relative StrengthSTUDENT WYCKOFF Relative Strength compares one instrument against another and plots their relative performance as a single line.

Instead of asking “is this chart going up or down?”, the script answers a more practical question: “is THIS asset doing better or worse than my benchmark?”

━━━━━━━━━━

1. Concept

━━━━━━━━━━

The indicator builds a classic relative strength (RS) line:

• Main symbol = the chart you attach the script to.

• Benchmark symbol = any symbol you choose in the settings (index, ETF, sector, another coin, etc.).

RS is calculated as:

RS = Price(main symbol) / Price(benchmark)

If RS is rising, your symbol outperforms the benchmark.

If RS is falling, your symbol underperforms the benchmark.

You can optionally normalize RS from the first bar (start at 1 or 100) to clearly see how many times the asset has outperformed or lagged behind over the visible history.

This is not a “buy/sell” indicator. It is a **context tool** for rotation, selection and Wyckoff-style comparative analysis.

━━━━━━━━━━

2. How the RS line is built

━━━━━━━━━━

Inputs:

• Source of main symbol – default is close, but you can choose any OHLC/HL2/typical price etc.

• Benchmark symbol – ticker used as reference (index, sector, futures, Bitcoin, stablecoin pair, etc.).

• Benchmark timeframe – by default the current chart timeframe is used, or you can force a different TF.

The script uses `request.security()` with `lookahead_off` and `gaps_off` to pull benchmark prices **without look-ahead**.

A small epsilon is used internally to avoid division by zero when the benchmark price is very close to 0.

Normalization options:

• Normalize RS from first bar – if enabled, the very first valid RS value becomes “1” (or 100), and all further values are expressed relative to this starting point.

• Multiply RS by 100 – purely cosmetic; makes it easier to read RS as a “percentage-like” scale.

━━━━━━━━━━

3. Smoothing and color logic

━━━━━━━━━━

To help read the trend of relative strength, the script calculates a simple moving average of the RS line:

• RS MA length – period of smoothing over the RS values.

• Show RS moving average – toggle to display or hide this line.

Color logic:

• When RS is above its own MA → the line is drawn with the “stronger” color.

• When RS is below its MA → the line uses the “weaker” color.

• When RS is close to its MA → neutral color.

Optional background shading:

• When RS > RS MA → background can be tinted softly green (phase of relative strength).

• When RS < RS MA → background can be tinted softly red (phase of relative weakness).

This makes it easy to read the **trend of strength** at a glance, without measuring every small swing.

━━━━━━━━━━

4. How to interpret it

━━━━━━━━━━

Basic reading rules:

• Rising RS line

– The main symbol is outperforming the benchmark.

– In Wyckoff terms, this can indicate a leader within its group, or a sign of accumulation relative to the market.

• Falling RS line

– The main symbol is underperforming the benchmark.

– Can point to laggards, distribution, or simply an asset that is “dead money” compared to alternatives.

• Flat or choppy RS line

– No clear edge versus the benchmark; performance is similar or rotating back and forth.

With normalization on:

• RS > 1 (or > 100) – the asset has grown more than the benchmark since the starting point.

• RS < 1 (or < 100) – it has grown less (or fallen more) than the benchmark over the same period.

The RS moving average and colored background highlight whether this outperformance/underperformance is a **temporary fluctuation** or a more sustained phase.

━━━━━━━━━━

5. Practical uses

━━━━━━━━━━

This indicator is useful for:

• **Selecting stronger assets inside a group**

– Compare individual stocks vs an index, sector, or industry ETF.

– Compare altcoins vs BTC, ETH, or a crypto index.

– Prefer charts where RS is in a sustained uptrend rather than just price going “up on its own”.

• **Monitoring sector and rotation flows**

– Attach the script to sector ETFs or major coins and switch the benchmark to a broad market index.

– See where capital is rotating: which areas are gaining or losing strength over time.

• **Supporting Wyckoff-style analysis**

– Use RS together with volume, structure, phases and trading ranges.

– A breakout or SOS with rising RS vs the market tells a different story than the same pattern with falling RS.

• **Portfolio review and risk decisions**

– When an asset shows a long period of relative weakness, it may be a candidate to reduce or replace.

– When RS turns up from a long weak phase, it can signal the start of potential leadership (not an entry by itself, but a reason to study the chart deeper).

━━━━━━━━━━

6. Notes and disclaimer

━━━━━━━━━━

• Works on any symbol and timeframe available on TradingView.

• The last bar can change in real time as new prices arrive; this is normal behaviour for all indicators that depend on current close.

• There are no built-in alerts or trading signals – this tool is meant to support your own analysis and trading plan.

This script is published for educational and analytical purposes only.

It does not constitute financial or investment advice and does not guarantee any performance. Always test your ideas, understand the logic of your tools and use proper risk management.

Seasonal Trend by LogReturn ProSeasonal Trend by LogReturn Pro

Seasonal Trend by LogReturn Pro is a seasonality indicator that analyzes historical average logarithmic returns to visualize recurring price behavior throughout the trading year.

Instead of using simple price averages, this indicator is based on log returns, making it scale-independent and mathematically consistent across different price levels and assets.

🔍 How It Works

The indicator calculates daily logarithmic returns for each trading day of the year.

These returns are aggregated and averaged over a user-defined number of past years.

Based on this historical data, a seasonal trend profile is constructed that represents the statistically expected market behavior over the year.

All calculations are aligned by trading day index, not calendar days, ensuring accurate seasonality even across different years and holidays.

📈 Display Modes

The indicator offers two complementary visualizations:

1. Absolute Seasonal Projection (Main Chart)

- Projects a price path based on historical average log returns.

- Can be displayd:

- Only for the remaining part of the current year, or

- For the entire year, starting from the beginning.

- Useful for visualizing potential seasonal price tendencies relative to the current price.

2. Relative Seasonal Performance (Indicator Pane)

Shows the cumulative seasonal return in percentage terms.

Centered around a zero line for easy interpretation.

Ideal for identifying periods with historically positive or negative seasonal bias.

💡 Use Cases

Identifying seasonal bullish or bearish phases

Timing entries and exits based on historical tendencies

Combining seasonality with technical or fundamental analysis

Gaining a long-term probabilistic market perspective

⚠️ Disclaimer

This indicator is based on historical data and does not predict future price movements.

It should be used as a statistical reference tool, not as a standalone trading signal.

Session ATR Progression Tracker📊 Session ATR Progression Tracker - SIYL Regression Trading Tool

Track how much of your instrument's 7-day Average True Range (ATR) has been covered during the current trading session. This indicator is specifically designed for regression traders who follow the "Stay In Your Lane" (SIYL) methodology, helping you identify when the probability of mean reversion significantly increases. If you are interested in more on that check out Rod Casselli and tradersdevgroup.com.

🎯 Key Features:

• Real-time ATR Coverage Percentage - See at a glance what percentage of the 7-day ATR has been covered in the current session

• SIYL-Optimized Thresholds - See at a glance when the instrument has achieved 80% and 100% ATR coverage, the proven thresholds where mean reversion probability increases (customizable)

• Flexible Session Modes:

- Daily: Resets at calendar day change

- Session: Uses exchange-defined trading sessions

- Custom Session: Set your exact session start/end times (perfect for futures traders and international markets)

• Visual Alerts - Color-coded display (gray → orange → red) and optional background highlighting

• Repositionable Display - Choose from 9 screen positions to avoid chart clutter

• Session Markers - Green triangles mark the start of each new session

• Detailed Stats - View current range, ATR value, session high/low, and session status

💡 Why Use This Indicator?

This tool is built around a proven concept: regression trading becomes significantly more effective once a session has achieved at least 80% of its 7-day ATR. At this threshold, the probability of price reverting to mean increases substantially, creating higher-probability trade setups for SIYL practitioners.

Benefits for regression traders:

- Identify optimal entry points when mean reversion probability is highest (≥80% ATR coverage)

- Avoid premature regression entries before adequate range has been established

- Recognize when daily moves have "earned their range" and are ripe for reversal

- Time fade-the-move and counter-trend strategies with statistical backing

- Improve win rates by trading only after proven probability thresholds are met

⚙️ Setup Instructions:

1. Add the indicator to your chart

2. Select your preferred "Reset Mode" (recommend "Custom Session" for futures/international markets)

3. If using Custom Session, enter your session times in 24-hour format (e.g., 0930-1600 for US stocks, 1700-1600 for CME futures)

4. Adjust alert thresholds if desired (default: 80% and 100% - proven SIYL thresholds)

5. Position the display where it's most visible on your chart

📈 Works Across All Markets:

Stocks • Futures • Forex • Indices • Crypto • Commodities

Perfect for regression traders, mean reversion specialists, and SIYL practitioners who want to trade with probability on their side by entering only after the session has "earned its range."

---

Tip: For futures contracts with overnight sessions that span calendar days (like MES, MNQ, MYM), use "Custom Session" mode with your exchange's official session times for accurate tracking.

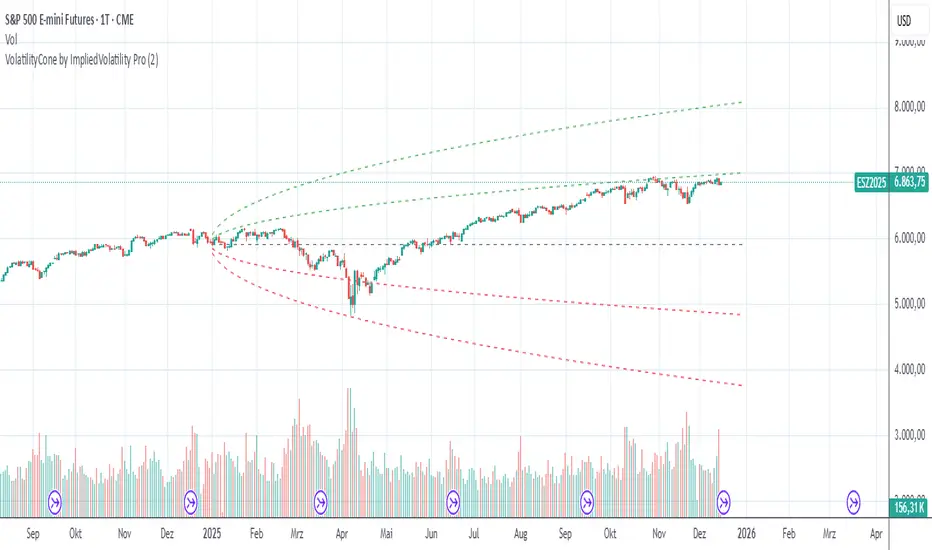

VolatilityCone by ImpliedVolatility ProVolatilityCone by ImpliedVolatility Pro

VolatilityCone by ImpliedVolatility Pro is a forward-looking volatility projection tool that visualizes expected price ranges based on implied volatility.

It draws a volatility cone starting from a user-defined date and projects statistically expected price boundaries into the future using standard deviation theory.

🔍 What does this indicator do?

This indicator calculates and plots price ranges that represent ±1, ±2, and ±3 standard deviations from a starting price, based on implied volatility.

The result is a cone-shaped projection that shows where price is statistically likely to move over time.

In addition, the indicator calculates a Z-Score, showing how far the current price deviates from the expected mean in volatility terms.

📐 Key Features

→ Forward projection based on implied volatility

→ Supports up to 3 standard deviation levels

→ Optional display of half standard deviation levels

→ Manually enter implied volatility or automatically fetch IV from another symbol (e.g. VIX)

→ Custom Start Date

→ The cone starts exactly at the selected date

→ Ideal for earnings, events, or cycle-based analysis

→ Displays the statistical mean price

→ Z-Score indicates how extreme the current price is relative to the cone

📊 How to Use

Price inside the cone

→ Normal volatility behavior

Price near ±1σ

→ Typical volatility range

Price near ±2σ or ±3σ

→ Statistically stretched or extreme conditions

Positive Z-Score

→ Price trading above the mean

Negative Z-Score

→ Price trading below the mean

This makes the indicator useful for:

→ Volatility analysis

→ Mean reversion strategies

→ Risk assessment

→ Event-based forecasting

→ Options-related analysis

⚙️ Notes & Disclaimer

This indicator is not a prediction tool, but a statistical projection

It assumes volatility follows a square-root-of-time model

Best used as a context tool, not as a standalone trading signal

Expectativa de Juros (Fed)An indicator that measures future expectations for US interest rates, measured by the difference between the Fed's interest rate and pricing on the CME.

Unmitigated Liquidity ZonesUnmitigated Liquidity Zones

Description:

Unmitigated Liquidity Zones is a professional-grade Smart Money Concepts (SMC) tool designed to visualize potential "draws on liquidity" automatically.

Unlike standard Support & Resistance indicators, this script focuses exclusively on unmitigated price levels — Swing Highs and Swing Lows that price has not yet revisited. These levels often harbor resting liquidity (Stop Losses, Buy/Sell Stops) and act as magnets for market makers.

How it works:

Detection: The script identifies significant Pivot Points based on your customizable length settings.

Visualization: It draws a line extending forward from the pivot, labeled with the exact Price and the Volume generated at that specific swing.

Mitigation Logic: The moment price "sweeps" or touches a level, the script treats the liquidity as "collected" and automatically removes the line and label from the chart. This keeps your workspace clean and focused only on active targets.

Key Features:

Dynamic Cleanup: Old levels are removed instantly upon testing. No chart clutter.

Volume Context: Displays the volume (formatted as K/M/B) of the pivot candle. This helps you distinguish between weak structure and strong institutional levels.

High Visibility: customizable bold lines and clear labels with backgrounds, designed to be visible on any chart theme.

Performance: Optimized using Pine Script v6 arrays to handle hundreds of levels without lag.

How to trade with this:

Targets: Use the opposing liquidity pools (Green lines for shorts, Red lines for longs) as high-probability Take Profit levels.

Reversals (Turtle Soup): Wait for price to sweep a bold liquidity line. If price aggressively reverses after taking the line, it indicates a "Liquidity Grab" setup.

Magnets: Price tends to gravitate toward "old" unmitigated levels.

Settings:

Pivot Length: Sensitivity of the swing detection (default: 20). Higher values find more significant/long-term levels.

Limit: Maximum number of active lines to prevent memory overload.

Visuals: Toggle Price/Volume labels, adjust line thickness and text size.

Simple Candle Strategy# Candle Pattern Strategy - Pine Script V6

## Overview

A TradingView trading strategy script (Pine Script V6) that identifies candlestick patterns over a configurable lookback period and generates trading signals based on pattern recognition rules.

## Strategy Logic

The strategy analyzes the most recent N candlesticks (default: 5) and classifies their patterns into three categories, then generates buy/sell signals based on specific pattern combinations.

### Candlestick Pattern Classification

Each candlestick is classified as one of three types:

| Pattern | Definition | Formula |

|---------|-----------|---------|

| **Close at High** | Close price near the highest price of the candle | `(high - close) / (high - low) ≤ (1 - threshold)` |

| **Close at Low** | Close price near the lowest price of the candle | `(close - low) / (high - low) ≤ (1 - threshold)` |

| **Doji** | Opening and closing prices very close; long upper/lower wicks | `abs(close - open) / (high - low) ≤ threshold` |

### Trading Rules

| Condition | Action | Signal |

|-----------|--------|--------|

| Number of Doji candles ≥ 3 | **SKIP** - Market is too chaotic | No trade |

| "Close at High" count ≥ 2 + Last candle closes at high | **LONG** - Bullish confirmation | Buy Signal |

| "Close at Low" count ≥ 2 + Last candle closes at low | **SHORT** - Bearish confirmation | Sell Signal |

## Configuration Parameters

All parameters are adjustable in TradingView's "Settings/Inputs" tab:

| Parameter | Default | Range | Description |

|-----------|---------|-------|-------------|

| **K-line Lookback Period** | 5 | 3-20 | Number of candlesticks to analyze |

| **Doji Threshold** | 0.1 | 0.0-1.0 | Body size / Total range ratio for doji identification |

| **Doji Count Limit** | 3 | 1-10 | Number of dojis that triggers skip signal |

| **Close at High Proximity** | 0.9 | 0.5-1.0 | Required proximity to highest price (0.9 = 90%) |

| **Close at Low Proximity** | 0.9 | 0.5-1.0 | Required proximity to lowest price (0.9 = 90%) |

### Parameter Tuning Guide

#### Proximity Thresholds (Close at High/Low)

- **0.95 or higher**: Stricter - only very strong candles qualify

- **0.90 (default)**: Balanced - good for most market conditions

- **0.80 or lower**: Looser - catches more patterns, higher false signals

#### Doji Threshold

- **0.05-0.10**: Strict doji identification

- **0.10-0.15**: Standard doji detection

- **0.15+**: Includes near-doji patterns

#### Lookback Period

- **3-5 bars**: Fast, sensitive to recent patterns

- **5-10 bars**: Balanced approach

- **10-20 bars**: Slower, filters out noise

## Visual Indicators

### Chart Markers

- **Green Up Arrow** ▲: Long entry signal triggered

- **Red Down Arrow** ▼: Short entry signal triggered

- **Gray X**: Skip signal (too many dojis detected)

### Statistics Table

Located at top-right corner, displays real-time pattern counts:

- **Close at High**: Count of candles closing near the high

- **Close at Low**: Count of candles closing near the low

- **Doji**: Count of doji/near-doji patterns

### Signal Labels

- Green label: "✓ Long condition met" - below entry bar

- Red label: "✓ Short condition met" - above entry bar

- Gray label: "⊠ Too many dojis, skip" - trade skipped

## Risk Management

### Exit Strategy

The strategy includes built-in exit rules based on ATR (Average True Range):

- **Stop Loss**: ATR × 2

- **Take Profit**: ATR × 3

Example: If ATR is $10, stop loss is at -$20 and take profit is at +$30

### Position Sizing

Default: 100% of equity per trade (adjustable in strategy properties)

**Recommendation**: Reduce to 10-25% of equity for safer capital allocation

## How to Use

### 1. Copy the Script

1. Open TradingView

2. Go to Pine Script Editor

3. Create a new indicator

4. Copy the entire `candle_pattern_strategy.pine` content

5. Click "Add to Chart"

### 2. Apply to Chart

- Select your preferred timeframe (1m, 5m, 15m, 1h, 4h, 1d)

- Choose a trading symbol (stocks, forex, crypto, etc.)

- The strategy will generate signals on all historical bars and in real-time

### 3. Configure Parameters

1. Right-click the strategy on chart → "Settings"

2. Adjust parameters in the "Inputs" tab

3. Strategy will recalculate automatically

4. Backtest results appear in the Strategy Tester panel

### 4. Backtesting

1. Click "Strategy Tester" (bottom panel)

2. Set date range for historical testing

3. Review performance metrics:

- Win rate

- Profit factor

- Drawdown

- Total returns

## Key Features

✅ **Execution Model Compliant** - Follows official Pine Script V6 standards

✅ **Global Scope** - All historical references in global scope for consistency

✅ **Adjustable Sensitivity** - Fine-tune all pattern detection thresholds

✅ **Real-time Updates** - Works on both historical and real-time bars

✅ **Visual Feedback** - Clear signals with labels and statistics table

✅ **Risk Management** - Built-in ATR-based stop loss and take profit

✅ **No Repainting** - Signals remain consistent after bar closes

## Important Notes

### Before Trading Live

1. **Backtest thoroughly**: Test on at least 6-12 months of historical data

2. **Paper trading first**: Practice with simulated trades

3. **Optimize parameters**: Find the best settings for your trading instrument

4. **Manage risk**: Never risk more than 1-2% per trade

5. **Monitor performance**: Review trades regularly and adjust as needed

### Market Conditions

The strategy works best in:

- Trending markets with clear directional bias

- Range-bound markets with defined support/resistance

- Markets with moderate volatility

The strategy may underperform in:

- Highly choppy/noisy markets (many false signals)

- Markets with gaps or overnight gaps

- Low liquidity periods

### Limitations

- Works on chart timeframes only (not intrabar analysis)

- Requires at least 5 bars of history (configurable)

- Fixed exit rules may not suit all trading styles

- No trend filtering (will trade both directions)

## Technical Details

### Historical Buffer Management

The strategy declares maximum bars back to ensure enough historical data:

```pine

max_bars_back(close, 20)

max_bars_back(open, 20)

max_bars_back(high, 20)

max_bars_back(low, 20)

```

This prevents runtime errors when accessing historical candlestick data.

### Pattern Detection Algorithm

```

For each bar in lookback period:

1. Calculate (high - close) / (high - low) → close_to_high_ratio

2. If close_to_high_ratio ≤ (1 - threshold) → count as "Close at High"

3. Calculate (close - low) / (high - low) → close_to_low_ratio

4. If close_to_low_ratio ≤ (1 - threshold) → count as "Close at Low"

5. Calculate abs(close - open) / (high - low) → body_ratio

6. If body_ratio ≤ doji_threshold → count as "Doji"

Signal Generation:

7. If doji_count ≥ cross_count_limit → SKIP_SIGNAL

8. If close_at_high_count ≥ 2 AND last_close_at_high → LONG_SIGNAL

9. If close_at_low_count ≥ 2 AND last_close_at_low → SHORT_SIGNAL

```

## Example Scenarios

### Scenario 1: Bullish Signal

```

Last 5 bars pattern:

Bar 1: Closes at high (95%) ✓

Bar 2: Closes at high (92%) ✓

Bar 3: Closes at mid (50%)

Bar 4: Closes at low (10%)

Bar 5: Closes at high (96%) ✓ (last bar)

Result:

- Close at high count: 3 (≥ 2) ✓

- Last closes at high: ✓