SOPR with Z-Score Table📊 Glassnode SOPR with Dynamic Z-Score Table

ℹ️ Powered by Glassnode On-Chain Metrics

📈 Description:

This indicator visualizes the Spent Output Profit Ratio (SOPR) for major cryptocurrencies — Bitcoin, Ethereum, and Litecoin — along with a dynamically normalized Z-Score. SOPR is a key on-chain metric that reflects whether coins moved on-chain are being sold at a profit or a loss.

🔍 SOPR is calculated using Glassnode’s entity-adjusted SOPR feed, and a custom SMA is applied to smooth the signal. The normalized Z-Score helps identify market sentiment extremes by scaling SOPR relative to its historical context.

📊 Features:

Selectable cryptocurrency: Bitcoin, Ethereum, or Litecoin

SOPR smoothed by user-defined SMA (default: 10 periods)

Upper & lower bounds (±4%) for SOPR, shown as red/green lines

Background highlighting when SOPR moves outside normal range

Normalized Z-Score scaled between –2 and +2

Live Z-Score display in a compact top-right table

🧮 Calculations:

SOPR data is sourced daily from Glassnode:

Bitcoin: XTVCBTC_SOPR

Ethereum: XTVCETH_SOPR

Litecoin: XTVCLTC_SOPR

Z-Score is calculated as:

SMA of SOPR over zscore_length periods

Standard deviation of SOPR

Z-Score = (SOPR – mean) / standard deviation

Z-Score is clamped between –2 and +2 for visual consistency

🎯 Interpretation:

SOPR > 1 implies coins are sold in profit

SOPR < 1 suggests coins are sold at a loss

When SOPR is significantly above or below its recent range (e.g., +4% or –4%), it may signal overheating or capitulation

The Z-Score contextualizes how extreme the current SOPR is relative to history

📌 Notes:

Best viewed on daily charts

Works across selected assets (BTC, ETH, LTC)

Statistics

MVRVZ BTCMVRVZ BTC (Market Value to Realized Value Z-Score)

Description:

The MVRVZ BTC indicator provides insights into the relationship between the market value and realized value of Bitcoin, using the Market Value to Realized Value (MVRV) ratio, which is then adjusted using a Z-Score. This indicator highlights potential market extremes and helps in identifying overbought or oversold conditions, offering a unique perspective on Bitcoin's valuation.

How It Works:

MVRVZ is calculated by taking the difference between Bitcoin's Market Capitalization (MC) and Realized Capitalization (MCR), then dividing that by the Standard Deviation (Stdev) of the price over a specified period (usually 104 weeks).

The resulting value is plotted as the MVRVZ line, representing how far the market price deviates from its realized value.

Z-Score is then applied to the MVRVZ line, with the Z-Score bounded between +2 and -2, which allows it to be used within a consistent evaluation framework, regardless of how high or low the MVRVZ line goes. The Z-Score will reflect overbought or oversold conditions:

A Z-Score above +2 indicates the market is likely overbought (possible market top).

A Z-Score below -2 indicates the market is likely oversold (possible market bottom).

Values between -2 and +2 indicate more neutral market conditions.

How to Read the Indicator:

MVRVZ Line:

The MVRVZ line shows the relationship between market cap and realized cap. A higher value indicates the market is overvalued relative to the actual capital realized by holders.

The MVRVZ line can move above or below the top and bottom lines you define, which are adjustable according to your preferences. These lines act as trigger levels.

Top and Bottom Trigger Lines:

You can customize the Top Line and Bottom Line values to your preference.

When the MVRVZ line crosses the Top Line, the market might be considered overbought.

When the MVRVZ line crosses the Bottom Line, the market might be considered oversold.

SCDA Z-Score:

The Z-Score is displayed alongside the MVRVZ line and is bounded between -2 and +2. It scales proportionally based on the MVRVZ line's position relative to the top and bottom trigger lines.

The Z-Score ensures that even if the MVRVZ line moves beyond the trigger lines, the Z-Score will stay within the limits of -2 to +2, making it ideal for your custom evaluation system (SCDA).

Background Highlighting:

The background color changes when the MVRVZ line crosses key levels:

When the MVRVZ line exceeds the Top Trigger, the background turns red, indicating overbought conditions.

When the MVRVZ line falls below the Bottom Trigger, the background turns green, indicating oversold conditions.

Data Sources:

The data for the MVRVZ indicator is sourced from Glassnode and Coinmetrics, which provide the necessary values for:

BTC Market Cap (MC) – The total market capitalization of Bitcoin.

BTC Realized Market Cap (MCR) – The capitalization based on the price at which Bitcoin was last moved on the blockchain (realized value).

How to Use the Indicator:

Market Extremes:

Use the MVRVZ and Z-Score to spot potential market tops or bottoms.

A high Z-Score (above +2) suggests the market is overbought, while a low Z-Score (below -2) suggests the market is oversold.

Adjusting the Triggers:

Customize the Top and Bottom Trigger Lines to suit your trading strategy. These lines can act as dynamic reference points for when to take action based on the Z-Score or MVRVZ line crossing these levels.

Market Evaluation (SCDA Framework):

The bounded Z-Score (from -2 to +2) is tailored for your SCDA evaluation system, allowing you to assess market conditions based on consistent criteria, no matter how volatile the MVRVZ line becomes.

Conclusion:

The MVRVZ BTC indicator is a powerful tool for assessing the relative valuation of Bitcoin based on its market and realized capitalization. By combining it with the Z-Score, you get an easy-to-read, bounded evaluation system that highlights potential market extremes and helps you make informed decisions about Bitcoin's price behavior.

Correlation Drift📈 Correlation Drift

The Correlation Drift indicator is designed to detect shifts in market momentum by analyzing the relationship between correlation and price lag. It combines the principles of correlation analysis and lag factor measurement to provide a unique perspective on trend alignment and momentum shifts.

🔍 Core Concept:

The indicator calculates the Correlation vs PLF Ratio, which measures the alignment between an asset’s price movement and a chosen benchmark (e.g., BTCUSD). This ratio reflects how well the asset’s momentum matches the market trend while accounting for price lag.

📊 How It Works:

Correlation Calculation:

The script calculates the correlation between the asset and the selected benchmark over a specified period.

A higher correlation indicates that the asset’s price movements are in sync with the benchmark.

Price Lag Factor (PLF) Calculation:

The PLF measures the difference between long-term and short-term price momentum, dynamically scaled by recent volatility.

It highlights potential overextensions or lags in the asset’s price movements.

Combining Correlation and PLF:

The Correlation vs PLF Ratio combines these metrics to detect momentum shifts relative to the trend.

The result is a dynamic, smoothed histogram that visualizes whether the asset is leading or lagging behind the trend.

💡 How to Interpret:

Positive Values (Green/Aqua Bars):

Indicates bullish alignment with the trend.

Aqua: Rising bullish momentum, suggesting continuation.

Teal: Decreasing bullish momentum, signaling caution.

Negative Values (Purple/Fuchsia Bars):

Indicates bearish divergence from the trend.

Fuchsia: Falling bearish momentum, indicating increasing pressure.

Purple: Rising bearish momentum, suggesting potential reversal.

Clipping for Readability:

Values are clipped between -3 and +3 to prevent outliers from compressing the histogram.

This ensures clear visualization of typical momentum shifts while still marking extreme cases.

🚀 Best Practices:

Use Correlation Drift as a confirmation tool in conjunction with trend indicators (e.g., moving averages) to identify momentum alignment or divergence.

Look for transitions from positive to negative (or vice versa) as signals of potential trend shifts.

Combine with volume analysis to strengthen confidence in breakout or breakdown signals.

⚠️ Key Features:

Customizable Settings: Adjust the correlation length, PLF length, and smoothing factor to fine-tune the indicator for different market conditions.

Visual Gradient: The histogram changes color based on the strength and direction of the ratio, making it easy to identify shifts at a glance.

Zero Line Reference: Clearly distinguishes between bullish and bearish momentum zones.

🔧 Recommended Settings:

Correlation Length: 14 (for short to medium-term analysis)

PLF Length: 50 (to smooth out noise while capturing trend shifts)

Smoothing Factor: 3 (for enhanced clarity without excessive lag)

Benchmark Symbol: BTCUSD (or another relevant market indicator)

By providing a quantitative measure of trend alignment while accounting for price lag, the Correlation Drift indicator helps traders make more informed decisions during periods of momentum change. Whether you are trading crypto, forex, or equities, this tool can be a powerful addition to your momentum-based trading strategies.

⚠️ Disclaimer:

The Correlation Drift indicator is a technical analysis tool designed to aid in identifying potential shifts in market momentum and trend alignment. It is intended for informational and educational purposes only and should not be considered as financial advice or a recommendation to buy, sell, or hold any financial instrument.

Trading financial instruments, including cryptocurrencies, involves significant risk and may result in the loss of your capital. Past performance is not indicative of future results. Always conduct thorough research and seek advice from a certified financial professional before making any trading decisions.

The developer (RWCS_LTD) is not responsible for any trading losses or adverse outcomes resulting from the use of this indicator. Users are encouraged to test and validate the indicator in a simulated environment before applying it to live trading. Use at your own risk.

Hurst Exponent Oscillator [PhenLabs]📊 Hurst Exponent Oscillator -

Version: PineScript™ v5

📌 Description

The Hurst Exponent Oscillator (HEO) by PhenLabs is a powerful tool developed for traders who want to distinguish between trending, mean-reverting, and random market behaviors with clarity and precision. By estimating the Hurst Exponent—a statistical measure of long-term memory in financial time series—this indicator helps users make sense of underlying market dynamics that are often not visible through traditional moving averages or oscillators.

Traders can quickly know if the market is likely to continue its current direction (trending), revert to the mean, or behave randomly, allowing for more strategic timing of entries and exits. With customizable smoothing and clear visual cues, the HEO enhances decision-making in a wide range of trading environments.

🚀 Points of Innovation

Integrates advanced Hurst Exponent calculation via Rescaled Range (R/S) analysis, providing unique market character insights.

Offers real-time visual cues for trending, mean-reverting, or random price action zones.

User-controllable EMA smoothing reduces noise for clearer interpretation.

Dynamic coloring and fill for immediate visual categorization of market regime.

Configurable visual thresholds for critical Hurst levels (e.g., 0.4, 0.5, 0.6).

Fully customizable appearance settings to fit different charting preferences.

🔧 Core Components

Log Returns Calculation: Computes log returns of the selected price source to feed into the Hurst calculation, ensuring robust and scale-independent analysis.

Rescaled Range (R/S) Analysis: Assesses the dispersion and cumulative deviation over a rolling window, forming the core statistical basis for the Hurst exponent estimate.

Smoothing Engine: Applies Exponential Moving Average (EMA) smoothing to the raw Hurst value for enhanced clarity.

Dynamic Rolling Windows: Utilizes arrays to maintain efficient, real-time calculations over user-defined lengths.

Adaptive Color Logic: Assigns different highlight and fill colors based on the current Hurst value zone.

🔥 Key Features

Visually differentiates between trending, mean-reverting, and random market modes.

User-adjustable lookback and smoothing periods for tailored sensitivity.

Distinct fill and line styles for each regime to avoid ambiguity.

On-chart reference lines for strong trending and mean-reverting thresholds.

Works with any price series (close, open, HL2, etc.) for versatile application.

🎨 Visualization

Hurst Exponent Curve: Primary plotted line (smoothed if EMA is used) reflects the ongoing estimate of the Hurst exponent.

Colored Zone Filling: The area between the Hurst line and the 0.5 reference line is filled, with color and opacity dynamically indicating the current market regime.

Reference Lines: Dash/dot lines mark standard Hurst thresholds (0.4, 0.5, 0.6) to contextualize the current regime.

All visual elements can be customized for thickness, color intensity, and opacity for user preference.

📖 Usage Guidelines

Data Settings

Hurst Calculation Length

Default: 100

Range: 10-300

Description: Number of bars used in Hurst calculation; higher values mean longer-term analysis, lower values for quicker reaction.

Data Source

Default: close

Description: Select which data series to analyze (e.g., Close, Open, HL2).

Smoothing Length (EMA)

Default: 5

Range: 1-50

Description: Length for smoothing the Hurst value; higher settings yield smoother but less responsive results.

Style Settings

Trending Color (Hurst > 0.5)

Default: Blue tone

Description: Color used when trending regime is detected.

Mean-Reverting Color (Hurst < 0.5)

Default: Orange tone

Description: Color used when mean-reverting regime is detected.

Neutral/Random Color

Default: Soft blue

Description: Color when market behavior is indeterminate or shifting.

Fill Opacity

Default: 70-80

Range: 0-100

Description: Transparency of area fills—higher opacity for stronger visual effect.

Line Width

Default: 2

Range: 1-5

Description: Thickness of the main indicator curve.

✅ Best Use Cases

Identifying if a market is regime-shifting from trending to mean-reverting (or vice versa).

Filtering signals in automated or systematic trading strategies.

Spotting periods of randomness where trading signals should be deprioritized.

Enhancing mean-reversion or trend-following models with regime-awareness.

⚠️ Limitations

Not predictive: Reflects current and recent market state, not future direction.

Sensitive to input parameters—overfitting may occur if settings are changed too frequently.

Smoothing can introduce lag in regime recognition.

May not work optimally in markets with structural breaks or extreme volatility.

💡 What Makes This Unique

Employs advanced statistical market analysis (Hurst exponent) rarely found in standard toolkits.

Offers immediate regime visualization through smart dynamic coloring and zone fills.

🔬 How It Works

Rolling Log Return Calculation:

Each new price creates a log return, forming the basis for robust, non-linear analysis. This ensures all price differences are treated proportionally.

Rescaled Range Analysis:

A rolling window maintains cumulative deviations and computes the statistical “range” (max-min of deviations). This is compared against the standard deviation to estimate “memory”.

Exponent Calculation & Smoothing:

The raw Hurst value is translated from the log of the rescaled range ratio, and then optionally smoothed via EMA to dampen noise and false signals.

Regime Detection Logic:

The smoothed value is checked against 0.5. Values above = trending; below = mean-reverting; near 0.5 = random. These control plot/fill color and zone display.

💡 Note:

Use longer calculation lengths for major market character study, and shorter ones for tactical, short-term adaptation. Smoothing balances noise vs. lag—find a best fit for your trading style. Always combine regime awareness with broader technical/fundamental context for best results.

Enhanced Volume Trend Indicator with BB SqueezeEnhanced Volume Trend Indicator with BB Squeeze: Comprehensive Explanation

The visualization system allows traders to quickly scan multiple securities to identify high-probability setups without detailed analysis of each chart. The progression from squeeze to breakout, supported by volume trend confirmation, offers a systematic approach to identifying trading opportunities.

The script combines multiple technical analysis approaches into a comprehensive dashboard that helps traders make informed decisions by identifying high-probability setups while filtering out noise through its sophisticated confirmation requirements. It combines multiple technical analysis approaches into an integrated visual system that helps traders identify potential trading opportunities while filtering out false signals.

Core Features

1. Volume Analysis Dashboard

The indicator displays various volume-related metrics in customizable tables:

AVOL (After Hours + Pre-Market Volume): Shows extended hours volume as a percentage of the 21-day average volume with color coding for buying/selling pressure. Green indicates buying pressure and red indicates selling pressure.

Volume Metrics: Includes regular volume (VOL), dollar volume ($VOL), relative volume compared to 21-day average (RVOL), and relative volume compared to 90-day average (RVOL90D).

Pre-Market Data: Optional display of pre-market volume (PVOL), pre-market dollar volume (P$VOL), pre-market relative volume (PRVOL), and pre-market price change percentage (PCHG%).

2. Enhanced Volume Trend (VTR) Analysis

The Volume Trend indicator uses adaptive analysis to evaluate buying and selling pressure, combining multiple factors:

MACD (Moving Average Convergence Divergence) components

Volume-to-SMA (Simple Moving Average) ratio

Price direction and market conditions

Volume change rates and momentum

EMA (Exponential Moving Average) alignment and crossovers

Volatility filtering

VTR Visual Indicators

The VTR score ranges from 0-100, with values above 50 indicating bullish conditions and below 50 indicating bearish conditions. This is visually represented by colored circles:

"●" (Filled Circle):

Green: Strong bullish trend (VTR ≥ 80)

Red: Strong bearish trend (VTR ≤ 20)

"◯" (Hollow Circle):

Green: Moderate bullish trend (VTR 65-79)

Red: Moderate bearish trend (VTR 21-35)

"·" (Small Dot):

Green: Weak bullish trend (VTR 55-64)

Red: Weak bearish trend (VTR 36-45)

"○" (Medium Hollow Circle): Neutral conditions (VTR 46-54), shown in gray

In "Both" display mode, the VTR shows both the numerical score (0-100) alongside the appropriate circle symbol.

Enhanced VTR Settings

The Enhanced Volume Trend component offers several advanced customization options:

Adaptive Volume Analysis (volTrendAdaptive):

When enabled, dynamically adjusts volume thresholds based on recent market volatility

Higher volatility periods require proportionally higher volume to generate significant signals

Helps prevent false signals during highly volatile markets

Keep enabled for most trading conditions, especially in volatile markets

Speed of Change Weight (volTrendSpeedWeight, range 0-1):

Controls emphasis on volume acceleration/deceleration rather than absolute levels

Higher values (0.7-1.0): More responsive to new volume trends, better for momentum trading

Lower values (0.2-0.5): Less responsive, better for trend following

Helps identify early volume trends before they fully develop

Momentum Period (volTrendMomentumPeriod, range 2-10):

Defines lookback period for volume change rate calculations

Lower values (2-3): More responsive to recent changes, better for short timeframes

Higher values (7-10): Smoother, better for daily/weekly charts

Directly affects how quickly the indicator responds to new volume patterns

Volatility Filter (volTrendVolatilityFilter):

Adjusts significance of volume by factoring in current price volatility

High volume during high volatility receives less weight

High volume during low volatility receives more weight

Helps distinguish between genuine volume-driven moves and volatility-driven moves

EMA Alignment Weight (volTrendEmaWeight, range 0-1):

Controls importance of EMA alignments in final VTR calculation

Analyzes multiple EMA relationships (5, 10, 21 period)

Higher values (0.7-1.0): Greater emphasis on trend structure

Lower values (0.2-0.5): More focus on pure volume patterns

Display Mode (volTrendDisplayMode):

"Value": Shows only numerical score (0-100)

"Strength": Shows only symbolic representation

"Both": Shows numerical score and symbol together

3. Bollinger Band Squeeze Detection (SQZ)

The BB Squeeze indicator identifies periods of low volatility when Bollinger Bands contract inside Keltner Channels, often preceding significant price movements.

SQZ Visual Indicators

"●" (Filled Circle): Strong squeeze - high probability setup for an impending breakout

Green: Strong squeeze with bullish bias (likely upward breakout)

Red: Strong squeeze with bearish bias (likely downward breakout)

Orange: Strong squeeze with unclear direction

"◯" (Hollow Circle): Moderate squeeze - medium probability setup

Green: With bullish EMA alignment

Red: With bearish EMA alignment

Orange: Without clear directional bias

"-" (Dash): Gray dash indicates no squeeze condition (normal volatility)

The script identifies squeeze conditions through multiple methods:

Bollinger Bands contracting inside Keltner Channels

BB width falling to bottom 20% of recent range (BB width percentile)

Very narrow Keltner Channel (less than 5% of basis price)

Tracking squeeze duration in consecutive bars

Different squeeze strengths are detected:

Strong Squeeze: BB inside KC with tight BB width and narrow KC

Moderate Squeeze: BB inside KC with either tight BB width or narrow KC

No Squeeze: Normal market conditions

4. Breakout Detection System

The script includes two breakout indicators working in sequence:

4.1 Pre-Breakout (PBK) Indicator

Detects potential upcoming breakouts by analyzing multiple factors:

Squeeze conditions lasting 2-3 bars or more

Significant price ranges

Strong volume confirmation

EMA/MACD crossovers

Consistent price direction

PBK Visual Indicators

"●" (Filled Circle): Detected pre-breakout condition

Green: Likely upward breakout (bullish)

Red: Likely downward breakout (bearish)

Orange: Direction not yet clear, but breakout likely

"-" (Dash): Gray dash indicates no pre-breakout condition

The PBK uses sophisticated conditions to reduce false signals including minimum squeeze length, significant price movement, and technical confirmations.

4.2 Breakout (BK) Indicator

Confirms actual breakouts in progress by identifying:

End of squeeze or strong expansion of Bollinger Bands

Volume expansion

Price moving outside Bollinger Bands

EMA crossovers with volume confirmation

MACD crossovers with significant price range

BK Visual Indicators

"●" (Filled Circle): Confirmed breakout in progress

Green: Upward breakout (bullish)

Red: Downward breakout (bearish)

Orange: Unusual breakout pattern without clear direction

"◆" (Diamond): Special breakout conditions (meets some but not all criteria)

"-" (Dash): Gray dash indicates no breakout detected

The BK indicator uses advanced filters for confirmation:

Requires consecutive breakout signals to reduce false positives

Strong volume confirmation requirements (40% above average)

Significant price movement thresholds

Consistency checks between price action and indicators

5. Market Metrics and Analysis

Price Change Percentage (CHG%)

Displays the current percentage change relative to the previous day's close, color-coded green for positive changes and red for negative changes.

Average Daily Range (ADR%)

Calculates the average daily percentage range over a specified period (default 20 days), helping traders gauge volatility and set appropriate price targets.

Average True Range (ATR)

Shows the Average True Range value, a volatility indicator developed by J. Welles Wilder that measures market volatility by decomposing the entire range of an asset price for that period.

Relative Strength Index (RSI)

Displays the standard 14-period RSI, a momentum oscillator that measures the speed and change of price movements on a scale from 0 to 100.

6. External Market Indicators

QQQ Change

Shows the percentage change in the Invesco QQQ Trust (tracking the Nasdaq-100 Index), useful for understanding broader tech market trends.

UVIX Change

Displays the percentage change in UVIX, a volatility index, providing insight into market fear and potential hedging activity.

BTC-USD

Shows the current Bitcoin price from Coinbase, useful for traders monitoring crypto correlation with equities.

Market Breadth (BRD)

Calculates the percentage difference between ATHI.US and ATLO.US (high vs. low securities), indicating overall market direction and strength.

7. Session Analysis and Volume Direction

Session Detection

The script accurately identifies different market sessions:

Pre-market: 4:00 AM to 9:30 AM

Regular market: 9:30 AM to 4:00 PM

After-hours: 4:00 PM to 8:00 PM

Closed: Outside trading hours

This detection works on any timeframe through careful calculation of current time in seconds.

Buy/Sell Volume Direction

The script analyzes buying and selling pressure by:

Counting up volume when close > open

Counting down volume when close < open

Tracking accumulated volume within the day

Calculating intraday pressure (up volume minus down volume)

Enhanced AVOL Calculation

The improved AVOL calculation works in all timeframes by:

Estimating typical pre-market and after-hours volume percentages

Combining yesterday's after-hours with today's pre-market volume

Calculating this as a percentage of the 21-day average volume

Determining buying/selling pressure by analyzing after-hours and pre-market price changes

Color-coding results: green for buying pressure, red for selling pressure

This calculation is particularly valuable because it works consistently across any timeframe.

Customization Options

Display Settings

The dashboard has two customizable tables: Volume Table and Metrics Table, with positions selectable as bottom_left or bottom_right.

All metrics can be individually toggled on/off:

Pre-market data (PVOL, P$VOL, PRVOL, PCHG%)

Volume data (AVOL, RVOL Day, RVOL 90D, Volume, SEED_YASHALGO_NSE_BREADTH:VOLUME )

Price metrics (ADR%, ATR, RSI, Price Change%)

Market indicators (QQQ, UVIX, Breadth, BTC-USD)

Analysis indicators (Volume Trend, BB Squeeze, Pre-Breakout, Breakout)

These toggle options allow traders to customize the dashboard to show only the metrics they find most valuable for their trading style.

Table and Text Customization

The dashboard's appearance can be customized:

Table background color via tableBgColor

Text color (White or Black) via textColorOption

The indicator uses smart formatting for volume and price values, automatically adding appropriate suffixes (K, M, B) for readability.

MACD Configuration for VTR

The Volume Trend calculation incorporates MACD with customizable parameters:

Fast Length: Controls the period for the fast EMA (default 3)

Slow Length: Controls the period for the slow EMA (default 9)

Signal Length: Controls the period for the signal line EMA (default 5)

MACD Weight: Controls how much influence MACD has on the volume trend score (default 0.3)

These settings allow traders to fine-tune how momentum is factored into the volume trend analysis.

Bollinger Bands and Keltner Channel Settings

The Bollinger Bands and Keltner Channels used for squeeze detection have preset (hidden) parameters:

BB Length: 20 periods

BB Multiplier: 2.0 standard deviations

Keltner Length: 20 periods

Keltner Multiplier: 1.5 ATR

These settings follow standard practice for squeeze detection while maintaining simplicity in the user interface.

Practical Trading Applications

Complete Trading Strategies

1. Squeeze Breakout Strategy

This strategy combines multiple components of the indicator:

Wait for a strong squeeze (SQZ showing ●)

Look for pre-breakout confirmation (PBK showing ● in green or red)

Enter when breakout is confirmed (BK showing ● in same direction)

Use VTR to confirm volume supports the move (VTR ≥ 65 for bullish or ≤ 35 for bearish)

Set profit targets based on ADR (Average Daily Range)

Exit when VTR begins to weaken or changes direction

2. Volume Divergence Strategy

This strategy focuses on the volume trend relative to price:

Identify when price makes a new high but VTR fails to confirm (divergence)

Look for VTR to show weakening trend (● changing to ◯ or ·)

Prepare for potential reversal when SQZ begins to form

Enter counter-trend position when PBK confirms reversal direction

Use external indicators (QQQ, BTC, Breadth) to confirm broader market support

3. Pre-Market Edge Strategy

This strategy leverages pre-market data:

Monitor AVOL for unusual pre-market activity (significantly above 100%)

Check pre-market price change direction (PCHG%)

Enter position at market open if VTR confirms direction

Use SQZ to determine if volatility is likely to expand

Exit based on RVOL declining or price reaching +/- ADR for the day

Market Context Integration

The indicator provides valuable context for trading decisions:

QQQ change shows tech market direction

BTC price shows crypto market correlation

UVIX change indicates volatility expectations

Breadth measurement shows market internals

This context helps traders avoid fighting the broader market and align trades with overall market direction.

Timeframe Optimization

The indicator is designed to work across different timeframes:

For day trading: Focus on AVOL, VTR, PBK/BK, and use shorter momentum periods

For swing trading: Focus on SQZ duration, VTR strength, and broader market indicators

For position trading: Focus on larger VTR trends and use EMA alignment weight

Advanced Analytical Components

Enhanced Volume Trend Score Calculation

The VTR score calculation is sophisticated, with the base score starting at 50 and adjusting for:

Price direction (up/down)

Volume relative to average (high/normal/low)

Volume acceleration/deceleration

Market conditions (bull/bear)

Additional factors are then applied, including:

MACD influence weighted by strength and direction

Volume change rate influence (speed)

Price/volume divergence effects

EMA alignment scores

Volatility adjustments

Breakout strength factors

Price action confirmations

The final score is clamped between 0-100, with values above 50 indicating bullish conditions and below 50 indicating bearish conditions.

Anti-False Signal Filters

The indicator employs multiple techniques to reduce false signals:

Requiring significant price range (minimum percentage movement)

Demanding strong volume confirmation (significantly above average)

Checking for consistent direction across multiple indicators

Requiring prior bar consistency (consecutive bars moving in same direction)

Counting consecutive signals to filter out noise

These filters help eliminate noise and focus on high-probability setups.

MACD Enhancement and Integration

The indicator enhances standard MACD analysis:

Calculating MACD relative strength compared to recent history

Normalizing MACD slope relative to volatility

Detecting MACD acceleration for stronger signals

Integrating MACD crossovers with other confirmation factors

EMA Analysis System

The indicator uses a comprehensive EMA analysis system:

Calculating multiple EMAs (5, 10, 21 periods)

Detecting golden cross (10 EMA crosses above 21 EMA)

Detecting death cross (10 EMA crosses below 21 EMA)

Assessing price position relative to EMAs

Measuring EMA separation percentage

Recent Enhancements and Evolution

Version 5.2 includes several improvements:

Enhanced AVOL to show buying/selling direction through color coding

Improved VTR with adaptive analysis based on market conditions

AVOL display now works in all timeframes through sophisticated estimation

Removed animal symbols and streamlined code with bright colors for better visibility

Improved anti-false signal filters throughout the system

Optimizing Indicator Settings

For Different Market Types

Range-Bound Markets:

Lower EMA Alignment Weight (0.2-0.4)

Higher Speed of Change Weight (0.8-1.0)

Focus on SQZ and PBK signals for breakout potential

Trending Markets:

Higher EMA Alignment Weight (0.7-1.0)

Moderate Speed of Change Weight (0.4-0.6)

Focus on VTR strength and BK confirmations

Volatile Markets:

Enable Volatility Filter

Enable Adaptive Volume Analysis

Lower Momentum Period (2-3)

Focus on strong volume confirmation (VTR ≥ 80 or ≤ 20)

For Different Asset Classes

Equities:

Standard settings work well

Pay attention to AVOL for gap potential

Monitor QQQ correlation

Futures:

Consider higher Volume/RVOL weight

Reduce MACD weight slightly

Pay close attention to SQZ duration

Crypto:

Higher volatility thresholds may be needed

Monitor BTC price for correlation

Focus on stronger confirmation signals

Integrated Visual System for Trading Decisions

The colored circle indicators create an intuitive visual system for quick market assessment:

Progression Sequence: SQZ (Squeeze) → PBK (Pre-Breakout) → BK (Breakout)

This sequence often occurs in order, with the squeeze leading to pre-breakout conditions, followed by an actual breakout.

VTR (Volume Trend): Provides context about the volume supporting these movements.

Color Coding: Green for bullish conditions, red for bearish conditions, and orange/gray for neutral or undefined conditions.

Statistical Reliability Index (SRI)Statistical Reliability Index (SRI)

The Statistical Reliability Index (SRI) is a professional financial analysis tool designed to assess the statistical stability and reliability of market conditions. It combines advanced statistical methods to gauge whether current market trends are statistically consistent or prone to erratic behavior. This allows traders to make more informed decisions when navigating trending and choppy markets.

Key Concepts:

1. Extrapolation of Cumulative Distribution Functions (CDF)

What is CDF?

A Cumulative Distribution Function (CDF) is a statistical tool that models the probability of a random variable falling below a certain value.

How it’s used in SRI:

The SRI utilizes the 95th percentile CDF of recent returns to estimate the likelihood of extreme price movements. This helps identify when a market is experiencing statistically significant changes, crucial for forecasting potential breakouts or breakdowns.

Weight in SRI:

The weight of the CDF extrapolation can be adjusted to emphasize its impact on the overall reliability index, allowing customization based on the trader's preference for tail risk analysis.

2. Bias Factor (BF)

What is the Bias Factor?

The Bias Factor measures the ratio of the current market price to the expected mean price calculated over a defined period. It represents the deviation from the typical price level.

How it’s used in SRI:

A higher bias factor indicates that the current price significantly deviates from the historical average, suggesting a potential mean reversion or trend exhaustion.

Weight in SRI:

Adjusting the Bias Factor weight lets users control how much this deviation influences the SRI, balancing between momentum trading and mean reversion strategies.

3. Coefficient of Variation (CV)

What is CV?

The Coefficient of Variation (CV) is a statistical measure that expresses the ratio of the standard deviation to the mean. It indicates the relative variability of asset returns, helping gauge the risk-to-return consistency.

How it’s used in SRI:

A lower CV indicates more stable and predictable price behavior, while a higher CV signals increased volatility. The SRI incorporates the inverse of the normalized CV to reflect price stability positively.

Weight in SRI:

By adjusting the CV weight, users can prioritize consistent price movements over erratic volatility, aligning the indicator with risk tolerance and strategy preferences.

Interpreting the SRI:

1. SRI Plot:

The SRI plot dynamically changes color to reflect market conditions:

Aqua Line: Indicates uptrend stability, signaling statistically consistent upward movements.

Fuchsia Line: Indicates downtrend stability, where statistically reliable downward movements are present.

The overlay background shifts between colors:

Aqua Background: Signifies statistical stability, where trends are historically consistent.

Fuchsia Background: Indicates statistical instability, often associated with trend uncertainty.

Yellow Background: Marks choppy periods, where statistical data suggests that market conditions are not conducive to reliable trading.

2. SRI Volatility Plot:

Displays the volatility of the SRI itself to detect when the indicator is stable or unstable:

Blue Area Fill: Signifies that the SRI is stable, indicating trending conditions.

Yellow Area Fill: Represents choppy or unstable SRI movements, suggesting sideways or unreliable market conditions.

A Chop Threshold Line (dotted yellow) highlights the maximum acceptable SRI volatility before the market is considered too unpredictable.

3. Stability Assessment:

Stable Trend (No Chop):

The SRI is smooth and consistent, often accompanied by aqua or fuchsia lines.

Volatility remains below the chop threshold, indicating a low-risk, trend-following environment.

Chop Mode:

The SRI becomes erratic, and the volatility plot spikes above the threshold.

Marked by a yellow shaded background, indicating uncertain and non-trending conditions.

[Trend Identification:

Use the color-coded SRI line and background to determine uptrend or downtrend reliability.

Be cautious when the SRI volatility plot shows yellow, as this signals trading conditions may not be reliable.

Practical Use Cases:

Trend Confirmation:

Utilize the SRI plot color and background to confirm whether a detected trend is statistically reliable.

Chop Mode Filtering:

During yellow chop periods, it is advisable to reduce trading activity or adopt range-bound strategies.

Strategy Filter:

Combine the SRI with trend-following indicators (like moving averages) to enhance entry and exit accuracy.

Volatility Monitoring:

Pay attention to the SRI volatility plot, as spikes often precede erratic price movements or trend reversals.

Disclaimer:

The Statistical Reliability Index (SRI) is a technical analysis tool designed to aid in market stability assessment and trend validation. It is not intended as a standalone trading signal generator. While the SRI can help identify statistically reliable trends, it is essential to incorporate additional technical and fundamental analysis to make well-informed trading decisions.

Trading and investing involve substantial risk, and past performance does not guarantee future results. Always use risk management practices and consult with a financial advisor to tailor strategies to your individual risk profile and objectives.

cc AJGB Candle Range Finder with TableOverview:

The "cc AJGB Candle Range Finder with Table" is a versatile Pine Script indicator designed to identify and visualize price ranges within the 1 minute charts based on UTC+2 Time Zone. Unlike traditional range indicators, it offers three unique calculation methods to define ranges based on minute and hour interactions, displays ranges as boxes with labeled point values, and summarizes average range sizes in a customizable table. This tool is ideal for analyzing price ranges of specific time based ranges.

Features:

Customizable Time Range: Users specify a start and end minute (0-59) to define the range period (e.g., 29th to 35th minute).

Three Calculation Methods:

Minute Only: Uses the minute of each bar to identify ranges (e.g., matches user-specified minutes).

Minute - Hour: Adjusts the minute by subtracting the hour, allowing for dynamic range detection across hourly cycles.

Minute + Hour: Combines minute and hour values for a unique range calculation, useful for specific intraday patterns.

Visual Output: Draws boxes around detected ranges, with labels showing the start/end minutes and range size in points.

Summary Table: Displays the average range size (in points) for each method, with customizable position, colors, and text size.

How It Works:

The indicator evaluates each bar’s timestamp in (UTC+2 ONLY) to match user-specified minutes using one or more selected methods. When a start minute is detected, it tracks the high and low prices until the end minute, drawing a box to highlight the range and labeling it with the range size in points. A table summarizes the average range size for each method, helping traders assess typical price movements during the specified period.

Market Analysis: Compare range sizes across different methods to understand intraday volatility patterns.

Settings Customization: Adjust colors, table position, and label sizes to suit your chart preferences.

Settings:

Range to Find: Set start and end minutes.

Range Selection: Enable/disable each method and customize colors.

Range Label Size: Choose label size (Tiny to Huge).

Table Settings: Configure table position (Top, Bottom, Left, Right), sub-position, text size, and colors.

Notes:

Only works on 1 minute charts

The indicator works best using Start Times that are lower than the End Times.

Ensure the chart is set to UTC+2 Time Zone for accurate range detection.

Why It’s Unique:

Unlike standard range indicators that focus on sessions or fixed periods, this tool allows precise minute-based range detection with three distinct calculation methods, offering flexibility for data gathering. The interactive table provides quick insights into average range sizes.

Linear Regression Volume | Lyro RSLinear Regression Volume | Lyro RS

⚠️Disclaimer⚠️

Always combine this indicator with other forms of analysis and risk management. Please do your own research before making any trading decisions.

The LR Volume | 𝓛𝔂𝓻𝓸 𝓡𝓢 indicator blends linear regression with volume-adjusted moving average s to dynamically outline price equilibrium and trend intensity. By integrating volume into its regression model, it highlights meaningful price movement relative to trading activity.

📌 How It Works:

Volume-Weighted Regression Baseline

Price is filtered through one of four volume-adjusted moving averages (SMA, RMA, HMA, ALMA) before being passed through a linear regression model, forming a dynamic fair value line.

Deviation Bands

The indicator plots 1x, 2x, and 3x standard deviation zones above and below the baseline, helping identify potential extremes, volatility spikes, and mean reversion areas.

Slope-Based Color Logic

The baseline and fill areas are dynamically colored:

- 🟢 Green for positive slope (uptrend)

- 🔴 Red for negative slope (downtrend)

- ⚪ Gray for neutral movement

⚙️ Inputs & Options:

Regression Length – Controls how many bars are used in the moving average and regression calculation.

Deviation Multiplier – Adjusts the width of the bands surrounding the regression baseline.

MA Type – Choose from 4 types:

SMA (Simple Moving Average)

RMA (Relative Moving Average)

HMA (Hull Moving Average)

ALMA (Arnaud Legoux Moving Average)

Band Colors – Customizable upper/lower band colors to match your visual style.

🔔 Alerts:

Long Signal – Triggers when the regression slope turns positive.

Short Signal – Triggers when the regression slope turns negative.

Money Flow: In & Out Detector[THANHCONG]Indicator Name:

Money Flow: In & Out Detector

Indicator Description:

The Money Flow: In & Out Detector indicator uses technical indicators such as RSI (Relative Strength Index), MFI (Money Flow Index), and volume analysis to determine money inflow and outflow in the market.

This indicator helps traders identify changes in money flow, allowing them to detect buy and sell signals based on the combination of the following factors:

RSI > 50 and MFI > 50: Money inflow, indicating a buy signal.

RSI < 50 and MFI < 50: Money outflow, indicating a sell signal.

Volume increase/decrease relative to the average: Identifies strong market behavior changes.

Adjustable Parameters:

RSI Length: The number of periods to calculate the RSI (default is 14).

MFI Length: The number of periods to calculate the MFI (default is 14).

Volume MA Length: The number of periods to calculate the moving average of volume (default is 20).

Volume Increase/Decrease (%): The percentage threshold for volume change compared to the moving average (default is 20%).

Look Back Period: The number of periods used to identify peaks and troughs (default is 20).

How to Use the Indicator:

Money Inflow: When both RSI and MFI are above 50, and volume increases significantly relative to the moving average, the indicator shows a Buy signal.

Money Outflow: When both RSI and MFI are below 50, and volume decreases significantly relative to the moving average, the indicator shows a Sell signal.

Identifying Peaks and Troughs: The indicator also helps identify market peaks and troughs based on technical conditions.

Note:

This indicator assists in decision-making, but does not replace comprehensive market analysis.

Use this indicator in conjunction with other technical analysis methods to increase the accuracy of trade signals.

Steps for Publishing the Indicator on TradingView:

Log in to TradingView:

Go to TradingView and log into your account.

Access Pine Script Editor:

Click on Pine Editor from the menu under the chart.

Paste your Pine Script® code into the editor window.

Check the Source Code:

Ensure your code is error-free and running correctly.

Review the entire source code and add the MPL-2.0 license notice if necessary.

Save and Publish:

After testing and confirming the code works correctly, click Add to Chart to try the indicator on your chart.

If satisfied with the result, click Publish Script at the top right of the Pine Editor.

Provide a name for the indicator and then enter the detailed description you’ve prepared.

Ensure you specify the MPL-2.0 license in the description if required.

Choose the Access Type:

You can choose either Public or Private access for your indicator depending on your intention.

Submit for Publication:

Wait for TradingView to review and approve your indicator. Typically, this process takes a few working days for verification and approval.

User Guide:

You can share detailed instructions for users on how to use the indicator on TradingView, including how to adjust the parameters and interpret the signals. For example:

Set RSI Length: Experiment with different RSI Length values to find the sensitivity that suits your strategy.

Interpreting In/Out Signals: When there is strong money inflow (In), consider entering a buy order. When there is strong money outflow (Out), consider selling.

CorrelationMulti-Timeframe Correlation Indicator

This Pine Script indicator measures the correlation between the current symbol and a reference symbol (default: GLD) across three different timeframes. It provides traders with valuable insights into how assets move in relation to each other over short, medium, and long-term periods.

Key Features

Multiple Timeframe Analysis: Calculates correlation coefficients over three customizable periods (default: 20, 50, and 200 bars)

Visual Reference Lines: Displays horizontal lines at +1, 0, and -1 to indicate perfect positive correlation, no correlation, and perfect negative correlation

Color-Coded Outputs: Shows short-term correlation in green, medium-term in yellow, and long-term in red for easy visual interpretation

Understanding Correlation

The correlation coefficient measures the statistical relationship between two data series, ranging from -1 to +1:

+1: Perfect positive correlation (both assets move together in the same direction)

0: No correlation (movements are random and independent)

-1: Perfect negative correlation (assets move in opposite directions)

How To Use This Indicator

Market Relationships: Identify how strongly your current asset correlates with the reference symbol

Diversification Analysis: Find assets with negative correlations to build a diversified portfolio

Divergence Opportunities: Watch for changes in correlation patterns that might signal trading opportunities

Trend Confirmation: Use correlation with benchmark assets to confirm broader market trends

Customization Options

Reference Symbol: Change the default GLD to any other symbol you want to compare against

Period Lengths: Adjust the short, medium, and long timeframes to match your trading strategy and timeframe

This indicator helps traders make more informed decisions by understanding the interrelationships between different assets across various timeframes, potentially improving portfolio construction and risk management strategies.

Daily Average 5m Candle SizeThis indicator measures the average size of each 5 min candle then works out the end of day average for you. Very important for profit targets and stops

Daily Price RangeThe indicator is designed to analyze an instrument’s volatility based on daily extremes (High-Low) and to compare the current day’s range with the typical (median) range over a selected period. This helps traders assess how much of the "usual" daily movement has already occurred and how much may still be possible during the trading day.

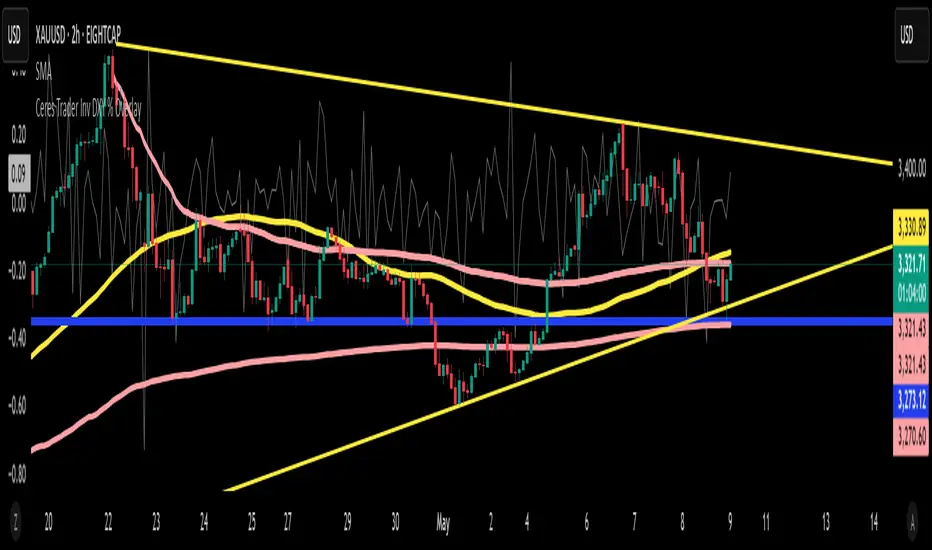

Ceres Trader Inv DXY % OverlayIntroducing the “Inverse DXY % Overlay” for TradingView

What it does:

• Plots the U.S. Dollar Index (DXY) as an inverted %-change line directly over your primary chart (e.g. XAUUSD).

• Dollar strength shows as a downward line; dollar weakness shows as an upward line—instantly highlighting negative correlation.

Why it helps:

• Trend confirmation – Ride Gold breakouts only when the dollar is actually weakening.

• Divergence signals – Spot early turn setups when Gold and DXY % don’t move in sync.

• Risk management – Trim or tighten stops when the dollar pivots against your position.

Key features:

Overlay on any symbol (Gold, Silver, Oil, Crypto, equities)

Auto-scaled to left-axis %, so your price chart stays on the right

Lightweight & transparent—1 px grey line, minimal clutter

Now you’ll have a real-time, inverted DXY % line beneath your candles—perfect for gauging USD flow before you pull the trigger on any trade.

Happy trading! 🚀

—Michael (Ceres Trader)

Price Lag Factor (PLF)📊 Price Lag Factor (PLF) for Crypto Traders: A Comprehensive Breakdown

The Price Lag Factor (PLF) is a momentum indicator designed to identify overextended price movements and gauge market momentum. It is particularly optimized for the crypto market, which is known for its high volatility and rapid trend shifts.

🔎 What is the Price Lag Factor (PLF)?

The PLF measures the difference between long-term and short-term price momentum and scales it dynamically based on recent volatility. This helps traders identify when the market might be overbought or oversold while filtering out noise.

The formula used in the PLF calculation is:

PLF = (Z-Long - Z-Short) / Stdev(PLF)

Where:

Z-long: Z-score of the long-term moving average (50-period by default).

Z-short: Z-score of the short-term moving average (14-period by default).

Stdev(PLF): Standard deviation of the PLF over a longer period (50-period by default).

🧠 How to Interpret the PLF:

1. Trend Direction:

Positive PLF (Green Bars): Indicates bullish momentum. The long-term trend is up, and short-term movements are confirming it.

Negative PLF (Red Bars): Indicates bearish momentum. The long-term trend is down, and short-term movements are consistent with it.

2. Momentum Strength:

PLF near Zero (±0.5): Low momentum; trend direction is not strong.

PLF between ±1 and ±2: Moderate momentum, indicating that the market is moving with strength but not in an overextended state.

PLF beyond ±2: High momentum (overbought/oversold), indicating potential trend exhaustion and a possible reversal.

📈 Trading Strategies:

1. Trend Following:

Bullish Signal:

Enter long when PLF crosses above 0 and remains green.

Confirm with other indicators like RSI or MACD to reduce false signals.

Bearish Signal:

Enter short when PLF crosses below 0 and remains red.

Use trend confirmation (e.g., moving average crossover) for better accuracy.

2. Reversal Trading:

Overbought Signal:

If PLF rises above +2, look for signs of bearish divergence or a reversal pattern to consider a short entry.

Oversold Signal:

If PLF falls below -2, watch for bullish divergence or a support bounce to consider a long entry.

3. Momentum Divergence:

Bullish Divergence:

Price makes a lower low while PLF makes a higher low.

Indicates weakening bearish momentum and a potential bullish reversal.

Bearish Divergence:

Price makes a higher high while PLF makes a lower high.

Signals weakening bullish momentum and a potential bearish reversal.

💡 Best Practices:

Combine with Volume:

Volume spikes during high PLF readings can confirm trend continuation.

Low volume during PLF extremes may hint at false breakouts.

Watch for Extreme Levels:

PLF beyond ±2 suggests overextended price action. Use caution when entering new positions.

Confirm with Other Indicators:

Use with Relative Strength Index (RSI) or Bollinger Bands to get a better sense of overbought/oversold conditions.

Overlay with a moving average to gauge trend consistency.

🚀 Why the PLF Works for Crypto:

Crypto markets are highly volatile and prone to rapid trend changes. The PLF's adaptive scaling ensures it remains relevant regardless of market conditions.

It highlights momentum shifts more accurately than static indicators because it accounts for changing volatility in its calculation.

🚨 Disclaimer for Traders Using the Price Lag Factor (PLF) Indicator:

The Price Lag Factor (PLF) indicator is designed as a technical analysis tool to gauge momentum and identify potential overbought or oversold conditions. However, it should not be relied upon as a sole decision-making factor for trading or investing.

Important Points to Consider:

Market Risk: Trading cryptocurrencies and other financial assets involves significant risk. The PLF may not accurately predict future price movements, especially during unexpected market events.

Indicator Limitations: No technical indicator, including the PLF, is infallible. False signals can occur, particularly in low-volume or highly volatile conditions.

Supplementary Analysis: Always combine PLF insights with other technical indicators, fundamental analysis, and risk management strategies to make informed decisions.

Personal Judgment: Traders should use their own discretion when interpreting PLF signals and never trade based solely on this indicator.

No Guarantees: The PLF is designed for educational and informational purposes only. Past performance is not indicative of future results.

Always perform thorough research and consider consulting with a professional financial advisor before making any trading decisions.

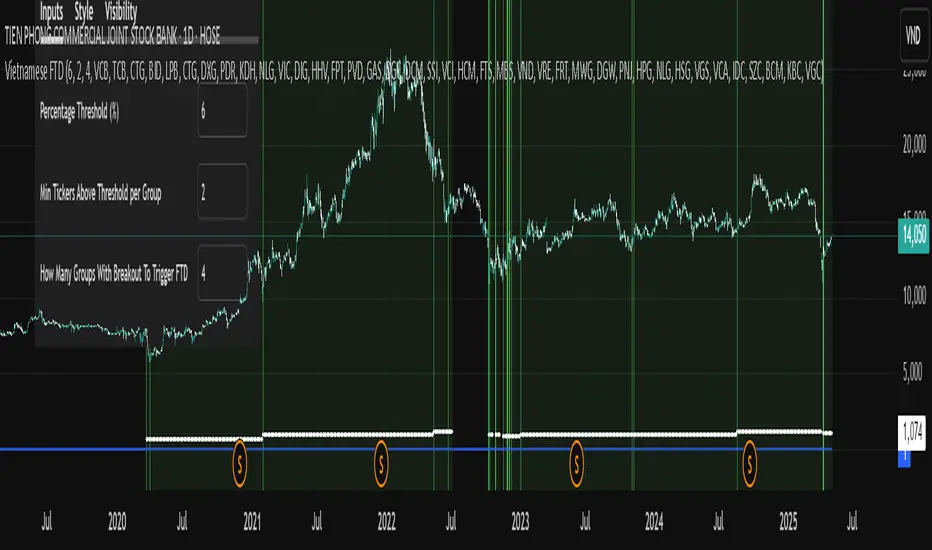

Vietnamese Stock Market FTD (Follow Through Day) AlertA Pine Script implementing William O'Neil’s Follow Through Day (FTD) strategy for the Vietnamese stock market. It scans 7 predefined sector groups (Banks, Real Estate, Retail, etc.) to detect momentum breakouts.

Key Features :

Triggers an FTD signal when ≥X groups (default: 3) have ≥Y stocks (default: 2) rising above a Z% threshold (default: 5%) daily.

Highlights qualifying stocks by group in a dynamic label during alerts.

Visualizes strength via histograms and background shading.

Open-source under Mozilla Public License 2.0 .

Purpose : Identify institutional buying and potential market reversals.

ETI IndicatorThe Ensemble Technical Indicator (ETI) is a script that combines multiple established indicators into one single powerful indicator. Specifically, it takes a number of technical indicators and then converts them into +1 to represent a bullish trend, or a -1 to represent a bearish trend. It then adds these values together and takes the running sum over the past 20 days.

The ETI is composed of the following indicators and converted to +1 or -1 using the following criteria:

Simple Moving Average (10 days) : When the price is above the 10-day simple moving averaging, +1, when below -1

Weighted Moving Average (10 days) : Similar to the SMA 10, when the the price is above the 10-day weighted moving average, +1, when below -1

Stochastic K% : If the current Stochastic K% is greater than the previous value, then +1, else -1.

Stochastic D% : Similar to the Stochastic K%, when the current Stochastic D% is greater than the previous value, +1, else -1.

MACD Difference : First subtract the MACD signal (i.e. the moving average) from the MACD value and if the current value is higher than the previous value, then +1, else -1.

William's R% : If the current William's R% is greater than the previous one, then +1, else -1.

William's Accumulation/Distribution : If the current William's AD value is greater than the previous value, then +1, else -1.

Commodity Channel Index : If the Commodity Channel Index is greater than 200 (overbought), then -1, if it is less than -200 (oversold) then +1. When it is between those values, if the current value is greater than the previous value then +1, else -1.

Relative Strength Index : If the Relative Strength Index is over 70 (overbought) then -1 and if under 30 (oversold) then +1. If the Relative Strength Indicator is between those values then if the current value is higher than the previous value +1, else -1.

Momentum (9 days) : If the momentum value is greater than 0, then +1, else -1.

Again, once these values have been calculated and converted, they are added up to produce a single value. This single value is then summed across the previous 20 candles to produce a running sum.

By coalescing multiple technical indicators into a single value across time, traders can better understand how multiple inter-related indicators are behaving at once; high scores indicate that numerous indicators are showing bullish signals indicating a potential or ongoing uptrend (and vice-versa with low scores).

Additional Features

Numerous smoothing transformations have also been added (e.g. gaussian smoothing) to remove some of the noise might exist.

Suggested Use

It is recommended that stocks are shorted when the cross below 0, and are bought when the ETI crosses above -40. Arrows can be shown on the indicator to show these points. However feel free to use levels that work best for you.

Traditionally, I have treated values above +50 as overbought and below -40 as undersold (with -80 indicating extremely oversold); however these levels could also indicate either upwards and downwards momentum so taking a position based on where the ETI is (rather than crossing levels) should be done with caution.

Relative Strength Index with Percentile📈 Relative Strength Index with Percentile Rank (RSI + Percentile)

This advanced RSI indicator adds a powerful percentile ranking system to the classic Relative Strength Index, providing deeper insight into current RSI values relative to recent history.

🔍 Key Features:

Standard RSI Calculation: Identifies overbought/oversold levels using a customizable period.

RSI Percentile (0–100%): Calculates where the current RSI value stands within a user-defined lookback period.

Dynamic Background Coloring:

🟩 Green when RSI percentile is above 80% (strong relative strength)

🟥 Red when RSI percentile is below 20% (strong relative weakness)

Optional Divergence Detection: Spot classic bullish and bearish divergences between price and RSI.

Smoothing Options: Apply various moving averages (SMA, EMA, RMA, etc.) to the RSI, with optional Bollinger Bands.

Flexible Settings: Full control over lookback periods, smoothing type, and band sensitivity.

🧠 Why Use RSI Percentile?

Traditional RSI values can become less informative during trending markets. By ranking the RSI as a percentile, you gain contextual insight into whether the current strength is unusually high or low compared to recent history, rather than just a fixed 70/30 threshold.

Money Flow based probabilityMoney Flow based probability

This indicator provides a comprehensive correlation and momentum analysis between your main asset and up to three selected correlated assets. It combines correlation, trend, momentum, and overbought/oversold signals into a single, easy-to-read table directly on your chart.

Correlated Asset Selection :

You can select up to three correlated assets (e.g., indices, currencies, bonds) to compare with your main chart symbol. Each asset can be toggled on or off.

Correlation Calculation :

The indicator uses the native Pine Script ta.correlation function to measure the statistical relationship between the closing prices of your asset and each selected pair over a user-defined period.

Technical Analysis Integration :

For each asset (including the main one), the indicator calculates:

Trend direction using EMA (Exponential Moving Average) – optional

Momentum using MACD – optional

Overbought/oversold status using RSI – optional

Probability Scoring :

A weighted scoring system combines correlation, trend, MACD, RSI, and trend exhaustion signals to produce buy and sell probabilities for the main asset.

Visual Table Output :

A customizable table is displayed on the chart, showing:

Asset name

Correlation (as a percentage, -100% to +100%)

Trend (Bullish/Bearish)

MACD status (Bullish/Bearish)

RSI value and status

Buy/Sell probability (with fixed-width formatting for stability)

User Customization :

You can adjust:

Table size, color, and position

Correlation period

EMA, MACD, and RSI parameters

Which assets to display

This indicator is ideal for traders who want to quickly assess the influence of major correlated markets and technical signals on their trading instrument, all in a single glance.

---

Example: Correlation Calculation

corrCurrentAsset1 = ta.correlation(close, asset1Data, correlationPeriod)

Example: Table Output (Buy/Sell %)

buyStr = f_formatPercent(buyProbability) + "%"

sellStr = f_formatPercent(sellProbability) + "%"

cellStr = buyStr + " / " + sellStr

The Echo System🔊 The Echo System – Trend + Momentum Trading Strategy

Overview:

The Echo System is a trend-following and momentum-based trading tool designed to identify high-probability buy and sell signals through a combination of market trend analysis, price movement strength, and candlestick validation.

Key Features:

📈 Trend Detection:

Uses a 30 EMA vs. 200 EMA crossover to confirm bullish or bearish trends.

Visual trend strength meter powered by percentile ranking of EMA distance.

🔄 Momentum Check:

Detects significant price moves over the past 6 bars, enhanced by ATR-based scaling to filter weak signals.

🕯️ Candle Confirmation:

Validates recent price action using the previous and current candle body direction.

✅ Smart Conditions Table:

A live dashboard showing all trade condition checks (Trend, Recent Price Move, Candlestick confirmations) in real-time with visual feedback.

📊 Backtesting & Stats:

Auto-calculates average win, average loss, risk-reward ratio (RRR), and win rate across historical signals.

Clean performance dashboard with color-coded metrics for easy reading.

🔔 Alerts:

Set alerts for trade signals or significant price movements to stay updated without monitoring the chart 24/7.

Visuals:

Trend markers and price movement flags plotted directly on the chart.

Dual tables:

📈 Conditions table (top-right): breaks down trade criteria status.

📊 Performance table (bottom-right): shows real-time stats on win/loss and RRR.🔊 The Echo System – Trend + Momentum Trading Strategy

Overview:

The Echo System is a trend-following and momentum-based trading tool designed to identify high-probability buy and sell signals through a combination of market trend analysis, price movement strength, and candlestick validation.

Key Features:

📈 Trend Detection:

Uses a 30 EMA vs. 200 EMA crossover to confirm bullish or bearish trends.

Visual trend strength meter powered by percentile ranking of EMA distance.

🔄 Momentum Check:

Detects significant price moves over the past 6 bars, enhanced by ATR-based scaling to filter weak signals.

🕯️ Candle Confirmation:

Validates recent price action using the previous and current candle body direction.

✅ Smart Conditions Table:

A live dashboard showing all trade condition checks (Trend, Recent Price Move, Candlestick confirmations) in real-time with visual feedback.

📊 Backtesting & Stats:

Auto-calculates average win, average loss, risk-reward ratio (RRR), and win rate across historical signals.

Clean performance dashboard with color-coded metrics for easy reading.

🔔 Alerts:

Set alerts for trade signals or significant price movements to stay updated without monitoring the chart 24/7.

Visuals:

Trend markers and price movement flags plotted directly on the chart.

Dual tables:

📈 Conditions table (top-right): breaks down trade criteria status.

📊 Performance table (bottom-right): shows real-time stats on win/loss and RRR.

Machine Learning: ARIMA + SARIMADescription

The ARIMA (Autoregressive Integrated Moving Average) and SARIMA (Seasonal ARIMA) are advanced statistical models that use machine learning to forecast future price movements. It uses autoregression to find the relationship between observed data and its lagged observations. The data is differenced to make it more predictable. The MA component creates a dependency between observations and residual errors. The parameters are automatically adjusted to market conditions.

Differences

ARIMA - This excels at identifying trends in the form of directions

SARIMA - Incorporates seasonality. It's better at capturing patterns previously seen

How To Use

1. Model: Determine if you want to use ARIMA (better for direction) or SARIMA (better for overall prediction). You can click on the 'Show Historic Prediction' to see the direction of the previous candles. Green = forecast ending up, red = forecast ending down

2. Metrics: The RMSE% and MAPE are 10 day moving averages of the first 10 predictions made at candle close. They're error metrics that compare the observed data with the predicted data. It is better to use them when they're below 8%. Higher timeframes will be higher, as these models are partly mean-reverting and higher TFs tend to trend more. Better to compare RMSE% and MAPE with similar timeframes. They naturally lag as data is being collected

3. Parameter selection: The simpler, the better. Both are used for ARIMA(1,1,1) and SARIMA(1,1,1)(1,1,1)5. Increasing may cause overfitting

4. Training period: Keep at 50. Because of limitations in pine, higher values do not make for more powerful forecasts. They will only criminally lag. So best to keep between 20 and 80

BTC vs ALT Lag Detector [MEXC Overlay]This indicator monitors the price movement of Bitcoin (BTC) and compares it in real time to a customizable list of major altcoins on the MEXC exchange.

It helps you identify lagging altcoins — tokens that are underperforming or overperforming BTC’s price action over a selected timeframe. These temporary deviations can offer profitable entry or rotation opportunities, especially for scalpers, day traders, and arbitrage-style strategies.

Key Features:

- Real-time deviation detection between BTC and altcoins

- Customizable comparison timeframe: 1m, 6m, 12m, 30m, 1h, 4h, or 1d

- Deviation threshold alert: Highlights coins that lag BTC by more than 0.5%, 1%, 2%, or 3%

- Compact stats table embedded in the price chart

- Fully adjustable layout: Table position (Top/Bottom/Center + Left/Right), Font size (Tiny, Small, Medium)

- Built-in alert system when deviation exceeds your chosen threshold

How to Use It:

Set your desired timeframe for comparison (e.g., 1 hour).

Select a deviation threshold (e.g., 1.0%).

The table will show:

Each altcoin’s % change

BTC’s % change

The delta (deviation) vs BTC

Red highlights indicate alts whose deviation exceeded the threshold.

When at least one alt lags beyond your threshold, the indicator can trigger an alert — helping you capitalize on potential catch-up trades.

Please provide any feedback on it.

Best SMA FinderThis script, Best SMA Finder, is a tool designed to identify the most robust simple moving average (SMA) length for a given chart, based on historical backtest performance. It evaluates hundreds of SMA values (from 10 to 1000) and selects the one that provides the best balance between profitability, consistency, and trade frequency.

What it does:

The script performs individual backtests for each SMA length using either "Long Only" or "Buy & Sell" logic, as selected by the user. For each tested SMA, it computes:

- Total number of trades

- Profit Factor (total profits / total losses)

- Win Rate

- A composite Robustness Score, which integrates Profit Factor, number of trades (log-scaled), and win rate.

Only SMA configurations that meet the user-defined minimum trade count are considered valid. Among all valid candidates, the script selects the SMA length with the highest robustness score and plots it on the chart.

How to use it:

- Choose the strategy type: "Long Only" or "Buy & Sell"

- Set the minimum trade count to filter out statistically irrelevant results

- Enable or disable the summary stats table (default: enabled)

The selected optimal SMA is plotted on the chart in blue. The optional table in the top-right corner shows the corresponding SMA length, trade count, Profit Factor, Win Rate, and Robustness Score for transparency.

Key Features:

- Exhaustive SMA optimization across 991 values

- Customizable trade direction and minimum trade filters

- In-chart visualization of results via table and plotted optimal SMA

- Uses a custom robustness formula to rank SMA lengths

Use cases:

Ideal for traders who want to backtest and auto-select a historically effective SMA without manual trial-and-error. Useful for swing and trend-following strategies across different timeframes.

📌 Limitations:

- Not a full trading strategy with position sizing or stop-loss logic

- Only one entry per direction at a time is allowed

- Designed for exploration and optimization, not as a ready-to-trade system

This script is open-source and built entirely from original code and logic. It does not replicate any closed-source script or reuse significant external open-source components.

Bitcoin Monthly Seasonality [Alpha Extract]The Bitcoin Monthly Seasonality indicator analyzes historical Bitcoin price performance across different months of the year, enabling traders to identify seasonal patterns and potential trading opportunities. This tool helps traders:

Visualize which months historically perform best and worst for Bitcoin.

Track average returns and win rates for each month of the year.

Identify seasonal patterns to enhance trading strategies.

Compare cumulative or individual monthly performance.

🔶 CALCULATION

The indicator processes historical Bitcoin price data to calculate monthly performance metrics

Monthly Return Calculation

Inputs:

Monthly open and close prices.

User-defined lookback period (1-15 years).

Return Types:

Percentage: (monthEndPrice / monthStartPrice - 1) × 100

Price: monthEndPrice - monthStartPrice

Statistical Measures

Monthly Averages: ◦ Average return for each month calculated from historical data.

Win Rate: ◦ Percentage of positive returns for each month.

Best/Worst Detection: ◦ Identifies months with highest and lowest average returns.

Cumulative Option

Standard View: Shows discrete monthly performance.

Cumulative View: Shows compounding effect of consecutive months.

Example Calculation (Pine Script):

monthReturn = returnType == "Percentage" ?

(monthEndPrice / monthStartPrice - 1) * 100 :

monthEndPrice - monthStartPrice

calcWinRate(arr) =>

winCount = 0

totalCount = array.size(arr)

if totalCount > 0

for i = 0 to totalCount - 1

if array.get(arr, i) > 0

winCount += 1

(winCount / totalCount) * 100

else

0.0

🔶 DETAILS

Visual Features

Monthly Performance Bars: ◦ Color-coded bars (teal for positive, red for negative returns). ◦ Special highlighting for best (yellow) and worst (fuchsia) months.

Optional Trend Line: ◦ Shows continuous performance across months.

Monthly Axis Labels: ◦ Clear month names for easy reference.

Statistics Table: ◦ Comprehensive view of monthly performance metrics. ◦ Color-coded rows based on performance.

Interpretation

Strong Positive Months: Historically bullish periods for Bitcoin.

Strong Negative Months: Historically bearish periods for Bitcoin.

Win Rate Analysis: Higher win rates indicate more consistently positive months.

Pattern Recognition: Identify recurring seasonal patterns across years.

Best/Worst Identification: Quickly spot the historically strongest and weakest months.

🔶 EXAMPLES

The indicator helps identify key seasonal patterns

Bullish Seasons: Visualize historically strong months where Bitcoin tends to perform well, allowing traders to align long positions with favorable seasonality.

Bearish Seasons: Identify historically weak months where Bitcoin tends to underperform, helping traders avoid unfavorable periods or consider short positions.

Seasonal Strategy Development: Create trading strategies that capitalize on recurring monthly patterns, such as entering positions in historically strong months and reducing exposure during weak months.

Year-to-Year Comparison: Assess how current year performance compares to historical seasonal patterns to identify anomalies or confirmation of trends.

🔶 SETTINGS

Customization Options

Lookback Period: Adjust the number of years (1-15) used for historical analysis.

Return Type: Choose between percentage returns or absolute price changes.

Cumulative Option: Toggle between discrete monthly performance or cumulative effect.

Visual Style Options: Bar Display: Enable/disable and customize colors for positive/negative bars, Line Display: Enable/disable and customize colors for trend line, Axes Display: Show/hide reference axes.

Visual Enhancement: Best/Worst Month Highlighting: Toggle special highlighting of extreme months, Custom highlight colors for best and worst performing months.

The Bitcoin Monthly Seasonality indicator provides traders with valuable insights into Bitcoin's historical performance patterns throughout the year, helping to identify potentially favorable and unfavorable trading periods based on seasonal tendencies.