Demand IndexLibrary "DemandIndex"

di()

The Demand Index is a complex technical indicator that uses price and volume to assess buying and selling pressure affecting a security.

James Sibbet established six rules for using Demand Index when the technical indicator was originally published. While traders may use variations of these rules, they serve as a great baseline for using the indicator in practice.

The six rules are as follows:

A divergence between the Demand Index and price is a bearish indication.

Prices often rally to new highs following an extreme peak in the Demand Index.

Higher prices with a low Demand Index often indicate a top in the market.

The Demand Index moving through the zero line suggests a change in trend.

The Demand Index remaining near the zero line indicates weak price movement that won’t last long.

A long-term divergence between the Demand Index and price predicts a major top or bottom.

Traders should use the Demand Index in conjunction with other technical indicators and chart patterns to maximize their odds of success.

Techindicator

L_Index_4khansoloLibrary "L_Index_4khansolo"

countrySelect()

colorPositron()

indexName()

indexRSI()

maRSI()

colorRSIfull()

rsiColor()

rsiFillColor()

rsiCompartments()

fiatIndexer()

colorMACD()

indexMACD()

colour()

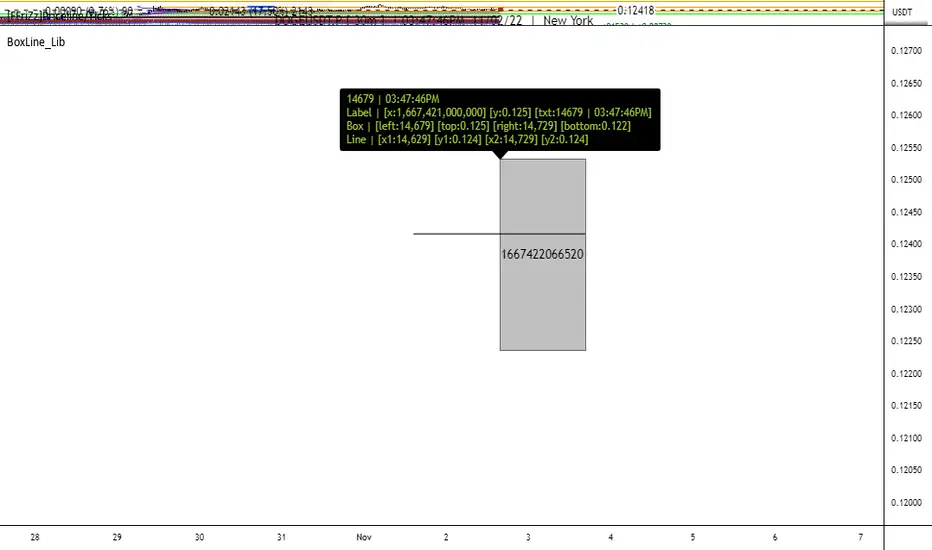

BoxLine_LibLibrary "BoxLine_Lib"

personal Library for line and box built in functions

lineXY(x)

get x1,y1,x2,y2 in a tuple

Parameters:

x : TODO: line

Returns: tuple of x1,y1,x2,y2

line(x)

Create line with only the y1 value(when line == na) or all

when line != na set x1,y1,x2,y2 individually just 1 or all

- use just the line value to set the x2 to current bar or time will set to time

- will auto pick xloc.bar_index or xloc.bar_time if not used

Parameters:

x : (line line,int x1,float y1,int x2,float y2,

string xloc,string extend,color color,string style,int width)

Returns: Line

boxXY(x)

get left,top,right,bottom in a tuple

Parameters:

x : box

Returns: tuple of left,top,right,bottom

box(x)

Create line with only the top,bottom value(when line == na) or all

when box != na set left,top,right,bottom individually just 1 or all

- use just the box value to set the right to current bar or time will set to time

- if right is above a number that a bar_index wouldnt be

Parameters:

x : box box,int left,float top,int right,

float bottom,color border_color, int border_width,

string border_style,string extend,string xloc,

color bgcolor,string text,string text_size, color text_color,

string text_halign,string text_valign,string text_wrap)

Returns: TODO: Box

DegreeALineLibrary "DegreeALine"

TODO: add library description here

Degree(x1, y1, x2, y2)

TODO: add function description here

Parameters:

x1 : First X coordinate of a line, index of the bar where the line starts.

y1 : First Y coordinate of a line, price on the price scale.

x2 : Second X coordinate of a line, index of the bar where the line ends.

y2 : Second Y coordinate of a line, price on the price scale.

Returns: Degree Of Line

lib_hlmLibrary "lib_hlm"

Ichimoku trend line and plotting tools.

HLM(Period)

Optionless Ichimoku/Donchian trend line calculation.

Parameters:

Period : The period for the trend line calculation.

Returns: The midpoint of the highest high and the lowest low.

HLM_Offset(offset, currentIsZero, intoPast)

Standardized language for plotting offsets.

Parameters:

offset : The offset number to use.

currentIsZero : `true` for ichimoku counting. `false` for natural language

intoPast : `true` if projecting backwards. `false` if projecting forwards.

Returns: The offset adjusted by counting style and direction.

TK()

Calculates the Ichimoku Tenkan and Kijun lines.

Returns: {tenkan, kijun}

SenkouSpans(period_1, period_2, period_3)

Calculates the Ichimoku Senkou Span A and Senkou Span B values.

Parameters:

period_1 : default=9

period_2 : default=26

period_3 : default=52

Returns: {senkou_a, senkou_b}

Ichimoku_Cloud(period_1, period_2, period_3)

Calculate the Ichimoku cloud value and offsets.

Parameters:

period_1 : default=9

period_2 : default=26

period_3 : default=52

Returns: {senkou_a, senkou_b, cloud_offset}

Chikou_Span()

Gets the chikou span and offsets.

Returns: {chikou, chikou_offset}

Ichimoku(enabled)

Get the values for the full, default Ichimoku system, including plotting offsets. Common toggle for all values.

Parameters:

enabled : `true` will return plottable values. `false` will return only na's (turns off plotting).

Returns: {tenkan, kijun, senkou_a, senkou_b, cloud_offset, chikou, chikou_offset}

Ichimoku_Line_Colors()

Get a set of colors with a common transparency for Ichimoku.

Returns: {tenkan_color, kijun_color, senkou_a_color, senkou_b_color, chikou_color}

Ichimoku_Cloud_Color()

Determines the cloud color and applies transparency (Ichimoku).

Returns: the dominant lines color with applied transparency

Ichimoku_Colors()

Gets a full set of default ichimoku colors with cloud color based on the input senkou values.

Returns: {tenkan_color, kijun_color, senkou_a_color, senkou_b_color, chikou_color, cloud_color}

SAT_LIBLibrary "SAT_LIB"

TODO: This library regroups indicator's functions and functions i use a lot

getRENKOLEVELS(upColor1, dnColor1, HIGH, LOW, ATR)

TODO: RenkoLevels indicator by Mongolor function

Parameters:

upColor1 : TODO: (Type: color) renko up color

dnColor1 : TODO: (Type: color) renko down color

HIGH : TODO: (Type: float)

LOW : TODO: (Type: float)

ATR : TODO: (Type: float)

Returns: TODO: Renkolevels

TR_HighLow_LibLibrary "TR_HighLow_Lib"

TODO: add library description here

ShowLabel(_Text, _X, _Y, _Style, _Size, _Yloc, _Color)

TODO: Function to display labels

Parameters:

_Text : TODO: text (series string) Label text.

_X : TODO: x (series int) Bar index.

_Y : TODO: y (series int/float) Price of the label position.

_Style : TODO: style (series string) Label style.

_Size : TODO: size (series string) Label size.

_Yloc : TODO: yloc (series string) Possible values are yloc.price, yloc.abovebar, yloc.belowbar.

_Color : TODO: color (series color) Color of the label border and arrow

Returns: TODO: No return values

GetColor(_Index)

TODO: Function to take out 12 colors in order

Parameters:

_Index : TODO: color number.

Returns: TODO: color code

Tbl_position(_Pos)

TODO: Table display position function

Parameters:

_Pos : TODO: position.

Returns: TODO: Table position

DeleteLine()

TODO: Delete Line

Parameters:

: TODO: No parameter

Returns: TODO: No return value

DeleteLabel()

TODO: Delete Label

Parameters:

: TODO: No parameter

Returns: TODO: No return value

ZigZag(_a_PHiLo, _a_IHiLo, _a_FHiLo, _a_DHiLo, _Histories, _Provisional_PHiLo, _Provisional_IHiLo, _Color1, _Width1, _Color2, _Width2, _ShowLabel, _ShowHighLowBar, _HighLowBarWidth, _HighLow_LabelSize)

TODO: Draw a zig-zag line.

Parameters:

_a_PHiLo : TODO: High-Low price array

_a_IHiLo : TODO: High-Low INDEX array

_a_FHiLo : TODO: High-Low flag array sequence 1:High 2:Low

_a_DHiLo : TODO: High-Low Price Differential Array

_Histories : TODO: Array size (High-Low length)

_Provisional_PHiLo : TODO: Provisional High-Low Price

_Provisional_IHiLo : TODO: Provisional High-Low INDEX

_Color1 : TODO: Normal High-Low color

_Width1 : TODO: Normal High-Low width

_Color2 : TODO: Provisional High-Low color

_Width2 : TODO: Provisional High-Low width

_ShowLabel : TODO: Label display flag True: Displayed False: Not displayed

_ShowHighLowBar : TODO: High-Low bar display flag True:Show False:Hide

_HighLowBarWidth : TODO: High-Low bar width

_HighLow_LabelSize : TODO: Label Size

Returns: TODO: No return value

TrendLine(_a_PHiLo, _a_IHiLo, _Histories, _MultiLine, _StartWidth, _EndWidth, _IncreWidth, _StartTrans, _EndTrans, _IncreTrans, _ColorMode, _Color1_1, _Color1_2, _Color2_1, _Color2_2, _Top_High, _Top_Low, _Bottom_High, _Bottom_Low)

TODO: Draw a Trend Line

Parameters:

_a_PHiLo : TODO: High-Low price array

_a_IHiLo : TODO: High-Low INDEX array

_Histories : TODO: Array size (High-Low length)

_MultiLine : TODO: Draw a multiple Line.

_StartWidth : TODO: Line width start value

_EndWidth : TODO: Line width end value

_IncreWidth : TODO: Line width increment value

_StartTrans : TODO: Transparent rate start value

_EndTrans : TODO: Transparent rate finally

_IncreTrans : TODO: Transparent rate increase value

_ColorMode : TODO: 0:Nomal 1:Gradation

_Color1_1 : TODO: Gradation Color 1_1

_Color1_2 : TODO: Gradation Color 1_2

_Color2_1 : TODO: Gradation Color 2_1

_Color2_2 : TODO: Gradation Color 2_2

_Top_High : TODO: _Top_High Value for Gradation

_Top_Low : TODO: _Top_Low Value for Gradation

_Bottom_High : TODO: _Bottom_High Value for Gradation

_Bottom_Low : TODO: _Bottom_Low Value for Gradation

Returns: TODO: No return value

Fibonacci(_a_Fibonacci, _a_PHiLo, _Provisional_PHiLo, _Index, _FrontMargin, _BackMargin)

TODO: Draw a Fibonacci line

Parameters:

_a_Fibonacci : TODO: Fibonacci Percentage Array

_a_PHiLo : TODO: High-Low price array

_Provisional_PHiLo : TODO: Provisional High-Low price (when _Index is 0)

_Index : TODO: Where to draw the Fibonacci line

_FrontMargin : TODO: Fibonacci line front-margin

_BackMargin : TODO: Fibonacci line back-margin

Returns: TODO: No return value

Fibonacci(_a_Fibonacci, _a_PHiLo, _Provisional_PHiLo, _Index1, _FrontMargin1, _BackMargin1, _Transparent1, _Index2, _FrontMargin2, _BackMargin2, _Transparent2)

TODO: Draw a Fibonacci line

Parameters:

_a_Fibonacci : TODO: Fibonacci Percentage Array

_a_PHiLo : TODO: High-Low price array

_Provisional_PHiLo : TODO: Provisional High-Low price (when _Index is 0)

_Index1 : TODO: Where to draw the Fibonacci line 1

_FrontMargin1 : TODO: Fibonacci line front-margin 1

_BackMargin1 : TODO: Fibonacci line back-margin 1

_Transparent1 : TODO: Transparent rate 1

_Index2 : TODO: Where to draw the Fibonacci line 2

_FrontMargin2 : TODO: Fibonacci line front-margin 2

_BackMargin2 : TODO: Fibonacci line back-margin 2

_Transparent2 : TODO: Transparent rate 2

Returns: TODO: No return value

High_Low_Judgment(_Length, _Extension, _Difference)

TODO: Judges High-Low

Parameters:

_Length : TODO: High-Low Confirmation Length

_Extension : TODO: Length of extension when the difference did not open

_Difference : TODO: Difference size

Returns: TODO: _HiLo=High-Low flag 0:Neither high nor low、1:High、2:Low、3:High-Low

_PHi=high price、_PLo=low price、_IHi=High Price Index、_ILo=Low Price Index、

_Cnt=count、_ECnt=Extension count、

_DiffHi=Difference from Start(High)、_DiffLo=Difference from Start(Low)、

_StartHi=Start value(High)、_StartLo=Start value(Low)

High_Low_Data_AddedAndUpdated(_HiLo, _Histories, _PHi, _PLo, _IHi, _ILo, _DiffHi, _DiffLo, _a_PHiLo, _a_IHiLo, _a_FHiLo, _a_DHiLo)

TODO: Adds and updates High-Low related arrays from given parameters

Parameters:

_HiLo : TODO: High-Low flag

_Histories : TODO: Array size (High-Low length)

_PHi : TODO: Price Hi

_PLo : TODO: Price Lo

_IHi : TODO: Index Hi

_ILo : TODO: Index Lo

_DiffHi : TODO: Difference in High

_DiffLo : TODO: Difference in Low

_a_PHiLo : TODO: High-Low price array

_a_IHiLo : TODO: High-Low INDEX array

_a_FHiLo : TODO: High-Low flag array 1:High 2:Low

_a_DHiLo : TODO: High-Low Price Differential Array

Returns: TODO: _PHiLo price array、_IHiLo indexed array、_FHiLo flag array、_DHiLo price-matching array、

Provisional_PHiLo Provisional price、Provisional_IHiLo 暫定インデックス

High_Low(_a_PHiLo, _a_IHiLo, _a_FHiLo, _a_DHiLo, _a_Fibonacci, _Length, _Extension, _Difference, _Histories, _ShowZigZag, _ZigZagColor1, _ZigZagWidth1, _ZigZagColor2, _ZigZagWidth2, _ShowZigZagLabel, _ShowHighLowBar, _ShowTrendLine, _TrendMultiLine, _TrendStartWidth, _TrendEndWidth, _TrendIncreWidth, _TrendStartTrans, _TrendEndTrans, _TrendIncreTrans, _TrendColorMode, _TrendColor1_1, _TrendColor1_2, _TrendColor2_1, _TrendColor2_2, _ShowFibonacci1, _FibIndex1, _FibFrontMargin1, _FibBackMargin1, _FibTransparent1, _ShowFibonacci2, _FibIndex2, _FibFrontMargin2, _FibBackMargin2, _FibTransparent2, _ShowInfoTable1, _TablePosition1, _ShowInfoTable2, _TablePosition2)

TODO: Draw the contents of the High-Low array.

Parameters:

_a_PHiLo : TODO: High-Low price array

_a_IHiLo : TODO: High-Low INDEX array

_a_FHiLo : TODO: High-Low flag sequence 1:High 2:Low

_a_DHiLo : TODO: High-Low Price Differential Array

_a_Fibonacci : TODO: Fibonacci Gnar Matching

_Length : TODO: Length of confirmation

_Extension : TODO: Extension Length of extension when the difference did not open

_Difference : TODO: Difference size

_Histories : TODO: High-Low Length

_ShowZigZag : TODO: ZigZag Display

_ZigZagColor1 : TODO: Colors of ZigZag1

_ZigZagWidth1 : TODO: Width of ZigZag1

_ZigZagColor2 : TODO: Colors of ZigZag2

_ZigZagWidth2 : TODO: Width of ZigZag2

_ShowZigZagLabel : TODO: ZigZagLabel Display

_ShowHighLowBar : TODO: High-Low Bar Display

_ShowTrendLine : TODO: Trend Line Display

_TrendMultiLine : TODO: Trend Multi Line Display

_TrendStartWidth : TODO: Line width start value

_TrendEndWidth : TODO: Line width end value

_TrendIncreWidth : TODO: Line width increment value

_TrendStartTrans : TODO: Starting transmittance value

_TrendEndTrans : TODO: Transmittance End Value

_TrendIncreTrans : TODO: Increased transmittance value

_TrendColorMode : TODO: color mode

_TrendColor1_1 : TODO: Trend Color 1_1

_TrendColor1_2 : TODO: Trend Color 1_2

_TrendColor2_1 : TODO: Trend Color 2_1

_TrendColor2_2 : TODO: Trend Color 2_2

_ShowFibonacci1 : TODO: Fibonacci1 Display

_FibIndex1 : TODO: Fibonacci1 Index No.

_FibFrontMargin1 : TODO: Fibonacci1 Front margin

_FibBackMargin1 : TODO: Fibonacci1 Back Margin

_FibTransparent1 : TODO: Fibonacci1 Transmittance

_ShowFibonacci2 : TODO: Fibonacci2 Display

_FibIndex2 : TODO: Fibonacci2 Index No.

_FibFrontMargin2 : TODO: Fibonacci2 Front margin

_FibBackMargin2 : TODO: Fibonacci2 Back Margin

_FibTransparent2 : TODO: Fibonacci2 Transmittance

_ShowInfoTable1 : TODO: InfoTable1 Display

_TablePosition1 : TODO: InfoTable1 position

_ShowInfoTable2 : TODO: InfoTable2 Display

_TablePosition2 : TODO: InfoTable2 position

Returns: TODO: 無し

TR_HighLowLibrary "TR_HighLow"

TODO: add library description here

ShowLabel(_Text, _X, _Y, _Style, _Size, _Yloc, _Color)

TODO: Function to display labels

Parameters:

_Text : TODO: text (series string) Label text.

_X : TODO: x (series int) Bar index.

_Y : TODO: y (series int/float) Price of the label position.

_Style : TODO: style (series string) Label style.

_Size : TODO: size (series string) Label size.

_Yloc : TODO: yloc (series string) Possible values are yloc.price, yloc.abovebar, yloc.belowbar.

_Color : TODO: color (series color) Color of the label border and arrow

Returns: TODO: No return values

GetColor(_Index)

TODO: Function to take out 12 colors in order

Parameters:

_Index : TODO: color number.

Returns: TODO: color code

Tbl_position(_Pos)

TODO: Table display position function

Parameters:

_Pos : TODO: position.

Returns: TODO: Table position

DeleteLine()

TODO: Delete Line

Parameters:

: TODO: No parameter

Returns: TODO: No return value

DeleteLabel()

TODO: Delete Label

Parameters:

: TODO: No parameter

Returns: TODO: No return value

ZigZag(_a_PHiLo, _a_IHiLo, _a_FHiLo, _a_DHiLo, _Histories, _Provisional_PHiLo, _Provisional_IHiLo, _Color1, _Width1, _Color2, _Width2, _ShowLabel, _ShowHighLowBar, _HighLowBarWidth, _HighLow_LabelSize)

TODO: Draw a zig-zag line.

Parameters:

_a_PHiLo : TODO: High-Low price array

_a_IHiLo : TODO: High-Low INDEX array

_a_FHiLo : TODO: High-Low flag array sequence 1:High 2:Low

_a_DHiLo : TODO: High-Low Price Differential Array

_Histories : TODO: Array size (High-Low length)

_Provisional_PHiLo : TODO: Provisional High-Low Price

_Provisional_IHiLo : TODO: Provisional High-Low INDEX

_Color1 : TODO: Normal High-Low color

_Width1 : TODO: Normal High-Low width

_Color2 : TODO: Provisional High-Low color

_Width2 : TODO: Provisional High-Low width

_ShowLabel : TODO: Label display flag True: Displayed False: Not displayed

_ShowHighLowBar : TODO: High-Low bar display flag True:Show False:Hide

_HighLowBarWidth : TODO: High-Low bar width

_HighLow_LabelSize : TODO: Label Size

Returns: TODO: No return value

TrendLine(_a_PHiLo, _a_IHiLo, _Histories, _MultiLine, _StartWidth, _EndWidth, _IncreWidth, _StartTrans, _EndTrans, _IncreTrans, _ColorMode, _Color1_1, _Color1_2, _Color2_1, _Color2_2, _Top_High, _Top_Low, _Bottom_High, _Bottom_Low)

TODO: Draw a Trend Line

Parameters:

_a_PHiLo : TODO: High-Low price array

_a_IHiLo : TODO: High-Low INDEX array

_Histories : TODO: Array size (High-Low length)

_MultiLine : TODO: Draw a multiple Line.

_StartWidth : TODO: Line width start value

_EndWidth : TODO: Line width end value

_IncreWidth : TODO: Line width increment value

_StartTrans : TODO: Transparent rate start value

_EndTrans : TODO: Transparent rate finally

_IncreTrans : TODO: Transparent rate increase value

_ColorMode : TODO: 0:Nomal 1:Gradation

_Color1_1 : TODO: Gradation Color 1_1

_Color1_2 : TODO: Gradation Color 1_2

_Color2_1 : TODO: Gradation Color 2_1

_Color2_2 : TODO: Gradation Color 2_2

_Top_High : TODO: _Top_High Value for Gradation

_Top_Low : TODO: _Top_Low Value for Gradation

_Bottom_High : TODO: _Bottom_High Value for Gradation

_Bottom_Low : TODO: _Bottom_Low Value for Gradation

Returns: TODO: No return value

Fibonacci(_a_Fibonacci, _a_PHiLo, _Provisional_PHiLo, _Index, _FrontMargin, _BackMargin)

TODO: Draw a Fibonacci line

Parameters:

_a_Fibonacci : TODO: Fibonacci Percentage Array

_a_PHiLo : TODO: High-Low price array

_Provisional_PHiLo : TODO: Provisional High-Low price (when _Index is 0)

_Index : TODO: Where to draw the Fibonacci line

_FrontMargin : TODO: Fibonacci line front-margin

_BackMargin : TODO: Fibonacci line back-margin

Returns: TODO: No return value

Fibonacci(_a_Fibonacci, _a_PHiLo, _Provisional_PHiLo, _Index1, _FrontMargin1, _BackMargin1, _Transparent1, _Index2, _FrontMargin2, _BackMargin2, _Transparent2)

TODO: Draw a Fibonacci line

Parameters:

_a_Fibonacci : TODO: Fibonacci Percentage Array

_a_PHiLo : TODO: High-Low price array

_Provisional_PHiLo : TODO: Provisional High-Low price (when _Index is 0)

_Index1 : TODO: Where to draw the Fibonacci line 1

_FrontMargin1 : TODO: Fibonacci line front-margin 1

_BackMargin1 : TODO: Fibonacci line back-margin 1

_Transparent1 : TODO: Transparent rate 1

_Index2 : TODO: Where to draw the Fibonacci line 2

_FrontMargin2 : TODO: Fibonacci line front-margin 2

_BackMargin2 : TODO: Fibonacci line back-margin 2

_Transparent2 : TODO: Transparent rate 2

Returns: TODO: No return value

High_Low_Judgment(_Length, _Extension, _Difference)

TODO: Judges High-Low

Parameters:

_Length : TODO: High-Low Confirmation Length

_Extension : TODO: Length of extension when the difference did not open

_Difference : TODO: Difference size

Returns: TODO: _HiLo=High-Low flag 0:Neither high nor low、1:High、2:Low、3:High-Low

_PHi=high price、_PLo=low price、_IHi=High Price Index、_ILo=Low Price Index、

_Cnt=count、_ECnt=Extension count、

_DiffHi=Difference from Start(High)、_DiffLo=Difference from Start(Low)、

_StartHi=Start value(High)、_StartLo=Start value(Low)

High_Low_Data_AddedAndUpdated(_HiLo, _Histories, _PHi, _PLo, _IHi, _ILo, _DiffHi, _DiffLo, _a_PHiLo, _a_IHiLo, _a_FHiLo, _a_DHiLo)

TODO: Adds and updates High-Low related arrays from given parameters

Parameters:

_HiLo : TODO: High-Low flag

_Histories : TODO: Array size (High-Low length)

_PHi : TODO: Price Hi

_PLo : TODO: Price Lo

_IHi : TODO: Index Hi

_ILo : TODO: Index Lo

_DiffHi : TODO: Difference in High

_DiffLo : TODO: Difference in Low

_a_PHiLo : TODO: High-Low price array

_a_IHiLo : TODO: High-Low INDEX array

_a_FHiLo : TODO: High-Low flag array 1:High 2:Low

_a_DHiLo : TODO: High-Low Price Differential Array

Returns: TODO: _PHiLo price array、_IHiLo indexed array、_FHiLo flag array、_DHiLo price-matching array、

Provisional_PHiLo Provisional price、Provisional_IHiLo 暫定インデックス

High_Low(_a_PHiLo, _a_IHiLo, _a_FHiLo, _a_DHiLo, _a_Fibonacci, _Length, _Extension, _Difference, _Histories, _ShowZigZag, _ZigZagColor1, _ZigZagWidth1, _ZigZagColor2, _ZigZagWidth2, _ShowZigZagLabel, _ShowHighLowBar, _ShowTrendLine, _TrendMultiLine, _TrendStartWidth, _TrendEndWidth, _TrendIncreWidth, _TrendStartTrans, _TrendEndTrans, _TrendIncreTrans, _TrendColorMode, _TrendColor1_1, _TrendColor1_2, _TrendColor2_1, _TrendColor2_2, _ShowFibonacci1, _FibIndex1, _FibFrontMargin1, _FibBackMargin1, _FibTransparent1, _ShowFibonacci2, _FibIndex2, _FibFrontMargin2, _FibBackMargin2, _FibTransparent2, _ShowInfoTable1, _TablePosition1, _ShowInfoTable2, _TablePosition2)

TODO: Draw the contents of the High-Low array.

Parameters:

_a_PHiLo : TODO: High-Low price array

_a_IHiLo : TODO: High-Low INDEX array

_a_FHiLo : TODO: High-Low flag sequence 1:High 2:Low

_a_DHiLo : TODO: High-Low Price Differential Array

_a_Fibonacci : TODO: Fibonacci Gnar Matching

_Length : TODO: Length of confirmation

_Extension : TODO: Extension Length of extension when the difference did not open

_Difference : TODO: Difference size

_Histories : TODO: High-Low Length

_ShowZigZag : TODO: ZigZag Display

_ZigZagColor1 : TODO: Colors of ZigZag1

_ZigZagWidth1 : TODO: Width of ZigZag1

_ZigZagColor2 : TODO: Colors of ZigZag2

_ZigZagWidth2 : TODO: Width of ZigZag2

_ShowZigZagLabel : TODO: ZigZagLabel Display

_ShowHighLowBar : TODO: High-Low Bar Display

_ShowTrendLine : TODO: Trend Line Display

_TrendMultiLine : TODO: Trend Multi Line Display

_TrendStartWidth : TODO: Line width start value

_TrendEndWidth : TODO: Line width end value

_TrendIncreWidth : TODO: Line width increment value

_TrendStartTrans : TODO: Starting transmittance value

_TrendEndTrans : TODO: Transmittance End Value

_TrendIncreTrans : TODO: Increased transmittance value

_TrendColorMode : TODO: color mode

_TrendColor1_1 : TODO: Trend Color 1_1

_TrendColor1_2 : TODO: Trend Color 1_2

_TrendColor2_1 : TODO: Trend Color 2_1

_TrendColor2_2 : TODO: Trend Color 2_2

_ShowFibonacci1 : TODO: Fibonacci1 Display

_FibIndex1 : TODO: Fibonacci1 Index No.

_FibFrontMargin1 : TODO: Fibonacci1 Front margin

_FibBackMargin1 : TODO: Fibonacci1 Back Margin

_FibTransparent1 : TODO: Fibonacci1 Transmittance

_ShowFibonacci2 : TODO: Fibonacci2 Display

_FibIndex2 : TODO: Fibonacci2 Index No.

_FibFrontMargin2 : TODO: Fibonacci2 Front margin

_FibBackMargin2 : TODO: Fibonacci2 Back Margin

_FibTransparent2 : TODO: Fibonacci2 Transmittance

_ShowInfoTable1 : TODO: InfoTable1 Display

_TablePosition1 : TODO: InfoTable1 position

_ShowInfoTable2 : TODO: InfoTable2 Display

_TablePosition2 : TODO: InfoTable2 position

Returns: TODO: 無し

SumOfCandlesLibrary "SumOfCandles"

This function returns sum of candlestick's body.

calc(_open, _close, _len, _malen, _usema)

Returns the sum of candlestick body.

Parameters:

_open : Source

_close : Source

_len : Period

_malen : MA Period

_usema : A flag of using MA

Returns: sum

calc(_len, _malen, _usema)

Returns the sum of candlestick body.

Parameters:

_len : Period

_malen : MA period

_usema : A flag of using MA

Returns: sum

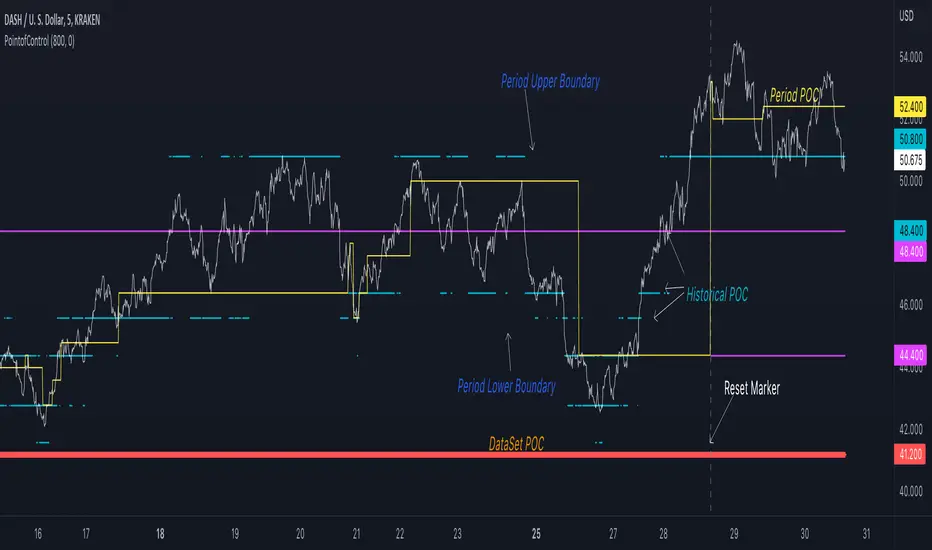

PointofControlLibrary "PointofControl"

POC_f()

The genesis of this project was to create a POC library that would be available to deliver volume profile information via pine to other scripts of indicators and strategies.

This is the indicator version of the library function.

A few things that would be unique with the built in

- it allows you to choose the kind of reset of the period, day/week or bars. This is simple enough to expand to other conditions

- it resets on bar count starting from the beginning of the data set (bar index =0) vs bars back from the end of the data set

- A 'period' in this context is the time between resets - the start of the POC until it resets (for example at the beginning of a new day or week)

- it will calculate an increment level rather than the user specifying ticks or price brackets

- it does not allow for setting the # of rows and then calculating the implied price levels

- When a period is complete it is often useful to look back at the POCs of historical periods, or extend them forward.

- This script will find the historical POCs around the current price and display them rather than extend all the historical POC lines to the right

- This script also looks across all the period POCs and identifies the master POC or what I call the Grand POC, and also the next 3 runner up POCs

There is a matching indicator to this library

loxxvarietyrsiLibrary "loxxvarietyrsi"

7 varieties of RSI used in Loxx's indicators and strategies. Default is "rsi_rsi" which is just TV's built int ta.rsi() function.

"rsi_rsi" is regular ta.rsi()

"rsi_slo" is slowed down version of regular RSI

"rsi_rap" is ta.rsi() but uses SMA instead of RMA, this is the same as Cuttlers RSI

"rsi_har" is Michael Harris RSI, but a word of "warning". I left the Harris' rsi in the choices of rsi, but be advised that, due to the way how Harris rsi is calculated, if price filtering is used (ie: some randomness is taken away from price series) Harris RSI tends to produce results that can be "surprising" at the least in some cases. Even though Harris RSI is good when it comes to natural (semi-random) price usage, keep in mind what happens if the prices are filtered and why it happens

"rsi_rsx" is Jurik's RSX

"rsi_cut" is ta.rsi() but uses SMA instead of RMA, this is the same as Rapid RSI

"rsi_ehl" is Ehles' Smoothed RSI

rsiVariety(rsiMode, src, per)

method for returning 1 of 7 different RSI calculation outputs.

Parameters:

rsiMode : string, rsi mode, can be 1 of 7 of the following: "rsi_rsi", "rsi_slo", "rsi_rap", "rsi_har", "rsi_rsx", "rsi_cut", "rsi_ehl"; defaults to "rsi_rsi"

src : float, source, either regular source type or some other caculated value.

per : int, period lookback.

Returns: float RSI.

usage:

rsiVariety("rsi_rsi", src, per)

EchoMorphicAverageLibrary "EchoMorphicAverage"

Original Self Referencing Moving Average which references

it's own output agsainst itself and the incoming source to dynamically

alter smoothness and length internally per calculation cycle.

@kaigouthro

Inputs are float length series.

Contact Me for More Dynamic Float Length Indicators.

wema(src, mod, len)

Waited Echo-Morphic Average

Parameters:

src : (float) input value

mod : (float) modifier(0-1) mix of current value

len : (float) length

Returns: output processed smoothed value

wemaStack(src, mod, len)

Stacked Multipass Waited Echo-Morphic Average

Parameters:

src : (float) input value

mod : (float) modifier(0-1) mix of current value

len : (float) length

Returns: output processed smoothed value

loxxdynamiczoneLibrary "loxxdynamiczone"

Dynamic Zones

Derives Leo Zamansky and David Stendahl's Dynamic Zone,

see "Stocks & Commodities V15:7 (306-310): Dynamic Zones by Leo Zamansky, Ph .D., and David Stendahl"

What are Dynamic Zones?

As explained in "Stocks & Commodities V15:7 (306-310): Dynamic Zones by Leo Zamansky, Ph .D., and David Stendahl"

Most indicators use a fixed zone for buy and sell signals. Here’ s a concept based on zones that are responsive to past levels of the indicator.

One approach to active investing employs the use of oscillators to exploit tradable market trends. This investing style follows a very simple form of logic: Enter the market only when an oscillator has moved far above or below traditional trading lev- els. However, these oscillator- driven systems lack the ability to evolve with the market because they use fixed buy and sell zones. Traders typically use one set of buy and sell zones for a bull market and substantially different zones for a bear market. And therein lies the problem.

Once traders begin introducing their market opinions into trading equations, by changing the zones, they negate the system’s mechanical nature. The objective is to have a system automatically define its own buy and sell zones and thereby profitably trade in any market — bull or bear. Dynamic zones offer a solution to the problem of fixed buy and sell zones for any oscillator-driven system.

An indicator’s extreme levels can be quantified using statistical methods. These extreme levels are calculated for a certain period and serve as the buy and sell zones for a trading system. The repetition of this statistical process for every value of the indicator creates values that become the dynamic zones. The zones are calculated in such a way that the probability of the indicator value rising above, or falling below, the dynamic zones is equal to a given probability input set by the trader.

To better understand dynamic zones, let's first describe them mathematically and then explain their use. The dynamic zones definition:

Find V such that:

For dynamic zone buy: P{X <= V}=P1

For dynamic zone sell: P{X >= V}=P2

where P1 and P2 are the probabilities set by the trader, X is the value of the indicator for the selected period and V represents the value of the dynamic zone.

The probability input P1 and P2 can be adjusted by the trader to encompass as much or as little data as the trader would like. The smaller the probability, the fewer data values above and below the dynamic zones. This translates into a wider range between the buy and sell zones. If a 10% probability is used for P1 and P2, only those data values that make up the top 10% and bottom 10% for an indicator are used in the construction of the zones. Of the values, 80% will fall between the two extreme levels. Because dynamic zone levels are penetrated so infrequently, when this happens, traders know that the market has truly moved into overbought or oversold territory.

Calculating the Dynamic Zones

The algorithm for the dynamic zones is a series of steps. First, decide the value of the lookback period t. Next, decide the value of the probability Pbuy for buy zone and value of the probability Psell for the sell zone.

For i=1, to the last lookback period, build the distribution f(x) of the price during the lookback period i. Then find the value Vi1 such that the probability of the price less than or equal to Vi1 during the lookback period i is equal to Pbuy. Find the value Vi2 such that the probability of the price greater or equal to Vi2 during the lookback period i is equal to Psell. The sequence of Vi1 for all periods gives the buy zone. The sequence of Vi2 for all periods gives the sell zone.

In the algorithm description, we have: Build the distribution f(x) of the price during the lookback period i. The distribution here is empirical namely, how many times a given value of x appeared during the lookback period. The problem is to find such x that the probability of a price being greater or equal to x will be equal to a probability selected by the user. Probability is the area under the distribution curve. The task is to find such value of x that the area under the distribution curve to the right of x will be equal to the probability selected by the user. That x is the dynamic zone.

dZone(type, src, pval, per)

method for retrieving the dynamic zone levels from input source.

Parameters:

type : string, value of either 'buy' or 'sell'.

src : float, source, either regular source type or some other caculated value.

pval : float, probability defined by extension over/under source, a number <= 1.0.

per : int, period lookback.

Returns: float dynamic zone level.

usage:

dZone("buy", close, 0.2, 70)

McNichollBandsLibrary "McNichollBands"

This is a library which only functions to make the McNicholl's Bollinger Bands modifications. It's also my first library, so I'll probably screw some things up.

mcNichollBands(alpha, useLogScale, widthMultiplier)

Calculates the McNicholl's Bollinger Bands modifications.

Parameters:

alpha : The alpha constant to be used on the EMA calculations.

useLogScale : Whether to use the log version of the prices or not.

widthMultiplier : The number that shall be multiplied by the volatility to form the bands.

Returns: A tuple containing the lower band, the center line, and the upper band.

loxxrsxLibrary "loxxrsx"

loxxrsx: Jurik RSX

rsx(src, len)

rsx

Parameters:

src : float

len : int

Returns: result float

loxxpaaspecialLibrary "loxxpaaspecial"

loxxpaaspecial: Ehlers Phase Accumulation Dominant Cycle Period with multiplier and filter

paa(src, mult, filt)

(src, mult, filt)

Parameters:

src : float

mult : float

filt : float

Returns: result float

loxxfsrrdspfiltsLibrary "loxxfsrrdspfilts"

loxxfsrrdspfilts : FATL, SATL, RFTL, & RSTL Digital Signal Filters

fatl(src)

fatl

Parameters:

src : float

Returns: result float

rftl(src)

rftl

Parameters:

src : float

Returns: result float

satl(src)

satl

Parameters:

src : float

Returns: result float

rstl(src)

rstl

Parameters:

src : float

Returns: result float

loxxjuriktoolsLibrary "loxxjuriktools"

loxxjuriktools: Jurik tools used in Loxx's idicators and strategies

jcfbaux(src, len)

jcfbaux

Parameters:

src : float

len : int

Returns: result float

jcfb(src, len, len)

jcfb

Parameters:

src : float

len : int

len : int

Returns: result float

jurik_filt(src, len, phase)

jurik_filt

Parameters:

src : float

len : int

phase : float

Returns: result float

loxxmas - moving averages used in Loxx's indis & stratsLibrary "loxxmas"

TODO:loxx moving averages used in indicators

kama(src, len, kamafastend, kamaslowend)

KAMA Kaufman adaptive moving average

Parameters:

src : float

len : int

kamafastend : int

kamaslowend : int

Returns: array

ama(src, len, fl, sl)

AMA, adaptive moving average

Parameters:

src : float

len : int

fl : int

sl : int

Returns: array

t3(src, len)

T3 moving average, adaptive moving average

Parameters:

src : float

len : int

Returns: array

adxvma(src, len)

ADXvma - Average Directional Volatility Moving Average

Parameters:

src : float

len : int

Returns: array

ahrma(src, len)

Ahrens Moving Average

Parameters:

src : float

len : int

Returns: array

alxma(src, len)

Alexander Moving Average - ALXMA

Parameters:

src : float

len : int

Returns: array

dema(src, len)

Double Exponential Moving Average - DEMA

Parameters:

src : float

len : int

Returns: array

dsema(src, len)

Double Smoothed Exponential Moving Average - DSEMA

Parameters:

src : float

len : int

Returns: array

ema(src, len)

Exponential Moving Average - EMA

Parameters:

src : float

len : int

Returns: array

fema(src, len)

Fast Exponential Moving Average - FEMA

Parameters:

src : float

len : int

Returns: array

hma(src, len)

Hull moving averge

Parameters:

src : float

len : int

Returns: array

ie2(src, len)

Early T3 by Tim Tilson

Parameters:

src : float

len : int

Returns: array

frama(src, len, FC, SC)

Fractal Adaptive Moving Average - FRAMA

Parameters:

src : float

len : int

FC : int

SC : int

Returns: array

instant(src, float)

Instantaneous Trendline

Parameters:

src : float

float : alpha

Returns: array

ilrs(src, int)

Integral of Linear Regression Slope - ILRS

Parameters:

src : float

int : len

Returns: array

laguerre(src, float)

Laguerre Filter

Parameters:

src : float

float : alpha

Returns: array

leader(src, int)

Leader Exponential Moving Average

Parameters:

src : float

int : len

Returns: array

lsma(src, int, int)

Linear Regression Value - LSMA (Least Squares Moving Average)

Parameters:

src : float

int : len

int : offset

Returns: array

lwma(src, int)

Linear Weighted Moving Average - LWMA

Parameters:

src : float

int : len

Returns: array

mcginley(src, int)

McGinley Dynamic

Parameters:

src : float

int : len

Returns: array

mcNicholl(src, int)

McNicholl EMA

Parameters:

src : float

int : len

Returns: array

nonlagma(src, int)

Non-lag moving average

Parameters:

src : float

int : len

Returns: array

pwma(src, int, float)

Parabolic Weighted Moving Average

Parameters:

src : float

int : len

float : pwr

Returns: array

rmta(src, int)

Recursive Moving Trendline

Parameters:

src : float

int : len

Returns: array

decycler(src, int)

Simple decycler - SDEC

Parameters:

src : float

int : len

Returns: array

sma(src, int)

Simple Moving Average

Parameters:

src : float

int : len

Returns: array

swma(src, int)

Sine Weighted Moving Average

Parameters:

src : float

int : len

Returns: array

slwma(src, int)

linear weighted moving average

Parameters:

src : float

int : len

Returns: array

smma(src, int)

Smoothed Moving Average - SMMA

Parameters:

src : float

int : len

Returns: array

super(src, int)

Ehlers super smoother

Parameters:

src : float

int : len

Returns: array

smoother(src, int)

Smoother filter

Parameters:

src : float

int : len

Returns: array

tma(src, int)

Triangular moving average - TMA

Parameters:

src : float

int : len

Returns: array

tema(src, int)

Tripple exponential moving average - TEMA

Parameters:

src : float

int : len

Returns: array

vwema(src, int)

Volume weighted ema - VEMA

Parameters:

src : float

int : len

Returns: array

vwma(src, int)

Volume weighted moving average - VWMA

Parameters:

src : float

int : len

Returns: array

zlagdema(src, int)

Zero-lag dema

Parameters:

src : float

int : len

Returns: array

zlagma(src, int)

Zero-lag moving average

Parameters:

src : float

int : len

Returns: array

zlagtema(src, int)

Zero-lag tema

Parameters:

src : float

int : len

Returns: array

threepolebuttfilt(src, int)

Three-pole Ehlers Butterworth

Parameters:

src : float

int : len

Returns: array

threepolesss(src, int)

Three-pole Ehlers smoother

Parameters:

src : float

int : len

Returns: array

twopolebutter(src, int)

Two-pole Ehlers Butterworth

Parameters:

src : float

int : len

Returns: array

twopoless(src, int)

Two-pole Ehlers smoother

Parameters:

src : float

int : len

Returns: array

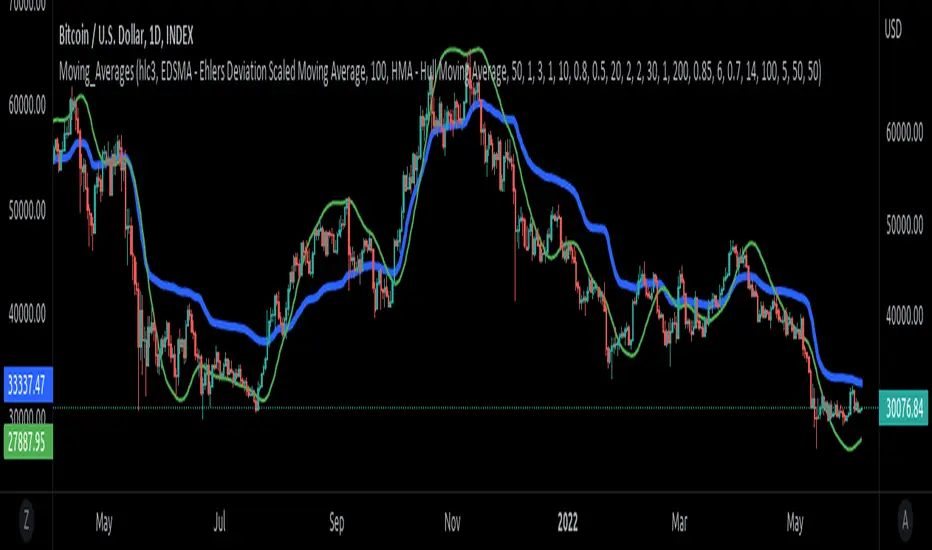

Moving_AveragesLibrary "Moving_Averages"

This library contains majority important moving average functions with int series support. Which means that they can be used with variable length input. For conventional use, please use tradingview built-in ta functions for moving averages as they are more precise. I'll use functions in this library for my other scripts with dynamic length inputs.

ema(src, len)

Exponential Moving Average (EMA)

Parameters:

src : Source

len : Period

Returns: Exponential Moving Average with Series Int Support (EMA)

alma(src, len, a_offset, a_sigma)

Arnaud Legoux Moving Average (ALMA)

Parameters:

src : Source

len : Period

a_offset : Arnaud Legoux offset

a_sigma : Arnaud Legoux sigma

Returns: Arnaud Legoux Moving Average (ALMA)

covwema(src, len)

Coefficient of Variation Weighted Exponential Moving Average (COVWEMA)

Parameters:

src : Source

len : Period

Returns: Coefficient of Variation Weighted Exponential Moving Average (COVWEMA)

covwma(src, len)

Coefficient of Variation Weighted Moving Average (COVWMA)

Parameters:

src : Source

len : Period

Returns: Coefficient of Variation Weighted Moving Average (COVWMA)

dema(src, len)

DEMA - Double Exponential Moving Average

Parameters:

src : Source

len : Period

Returns: DEMA - Double Exponential Moving Average

edsma(src, len, ssfLength, ssfPoles)

EDSMA - Ehlers Deviation Scaled Moving Average

Parameters:

src : Source

len : Period

ssfLength : EDSMA - Super Smoother Filter Length

ssfPoles : EDSMA - Super Smoother Filter Poles

Returns: Ehlers Deviation Scaled Moving Average (EDSMA)

eframa(src, len, FC, SC)

Ehlrs Modified Fractal Adaptive Moving Average (EFRAMA)

Parameters:

src : Source

len : Period

FC : Lower Shift Limit for Ehlrs Modified Fractal Adaptive Moving Average

SC : Upper Shift Limit for Ehlrs Modified Fractal Adaptive Moving Average

Returns: Ehlrs Modified Fractal Adaptive Moving Average (EFRAMA)

ehma(src, len)

EHMA - Exponential Hull Moving Average

Parameters:

src : Source

len : Period

Returns: Exponential Hull Moving Average (EHMA)

etma(src, len)

Exponential Triangular Moving Average (ETMA)

Parameters:

src : Source

len : Period

Returns: Exponential Triangular Moving Average (ETMA)

frama(src, len)

Fractal Adaptive Moving Average (FRAMA)

Parameters:

src : Source

len : Period

Returns: Fractal Adaptive Moving Average (FRAMA)

hma(src, len)

HMA - Hull Moving Average

Parameters:

src : Source

len : Period

Returns: Hull Moving Average (HMA)

jma(src, len, jurik_phase, jurik_power)

Jurik Moving Average - JMA

Parameters:

src : Source

len : Period

jurik_phase : Jurik (JMA) Only - Phase

jurik_power : Jurik (JMA) Only - Power

Returns: Jurik Moving Average (JMA)

kama(src, len, k_fastLength, k_slowLength)

Kaufman's Adaptive Moving Average (KAMA)

Parameters:

src : Source

len : Period

k_fastLength : Number of periods for the fastest exponential moving average

k_slowLength : Number of periods for the slowest exponential moving average

Returns: Kaufman's Adaptive Moving Average (KAMA)

kijun(_high, _low, len, kidiv)

Kijun v2

Parameters:

_high : High value of bar

_low : Low value of bar

len : Period

kidiv : Kijun MOD Divider

Returns: Kijun v2

lsma(src, len, offset)

LSMA/LRC - Least Squares Moving Average / Linear Regression Curve

Parameters:

src : Source

len : Period

offset : Offset

Returns: Least Squares Moving Average (LSMA)/ Linear Regression Curve (LRC)

mf(src, len, beta, feedback, z)

MF - Modular Filter

Parameters:

src : Source

len : Period

beta : Modular Filter, General Filter Only - Beta

feedback : Modular Filter Only - Feedback

z : Modular Filter Only - Feedback Weighting

Returns: Modular Filter (MF)

rma(src, len)

RMA - RSI Moving average

Parameters:

src : Source

len : Period

Returns: RSI Moving average (RMA)

sma(src, len)

SMA - Simple Moving Average

Parameters:

src : Source

len : Period

Returns: Simple Moving Average (SMA)

smma(src, len)

Smoothed Moving Average (SMMA)

Parameters:

src : Source

len : Period

Returns: Smoothed Moving Average (SMMA)

stma(src, len)

Simple Triangular Moving Average (STMA)

Parameters:

src : Source

len : Period

Returns: Simple Triangular Moving Average (STMA)

tema(src, len)

TEMA - Triple Exponential Moving Average

Parameters:

src : Source

len : Period

Returns: Triple Exponential Moving Average (TEMA)

thma(src, len)

THMA - Triple Hull Moving Average

Parameters:

src : Source

len : Period

Returns: Triple Hull Moving Average (THMA)

vama(src, len, volatility_lookback)

VAMA - Volatility Adjusted Moving Average

Parameters:

src : Source

len : Period

volatility_lookback : Volatility lookback length

Returns: Volatility Adjusted Moving Average (VAMA)

vidya(src, len)

Variable Index Dynamic Average (VIDYA)

Parameters:

src : Source

len : Period

Returns: Variable Index Dynamic Average (VIDYA)

vwma(src, len)

Volume-Weighted Moving Average (VWMA)

Parameters:

src : Source

len : Period

Returns: Volume-Weighted Moving Average (VWMA)

wma(src, len)

WMA - Weighted Moving Average

Parameters:

src : Source

len : Period

Returns: Weighted Moving Average (WMA)

zema(src, len)

Zero-Lag Exponential Moving Average (ZEMA)

Parameters:

src : Source

len : Period

Returns: Zero-Lag Exponential Moving Average (ZEMA)

zsma(src, len)

Zero-Lag Simple Moving Average (ZSMA)

Parameters:

src : Source

len : Period

Returns: Zero-Lag Simple Moving Average (ZSMA)

evwma(src, len)

EVWMA - Elastic Volume Weighted Moving Average

Parameters:

src : Source

len : Period

Returns: Elastic Volume Weighted Moving Average (EVWMA)

tt3(src, len, a1_t3)

Tillson T3

Parameters:

src : Source

len : Period

a1_t3 : Tillson T3 Volume Factor

Returns: Tillson T3

gma(src, len)

GMA - Geometric Moving Average

Parameters:

src : Source

len : Period

Returns: Geometric Moving Average (GMA)

wwma(src, len)

WWMA - Welles Wilder Moving Average

Parameters:

src : Source

len : Period

Returns: Welles Wilder Moving Average (WWMA)

ama(src, _high, _low, len, ama_f_length, ama_s_length)

AMA - Adjusted Moving Average

Parameters:

src : Source

_high : High value of bar

_low : Low value of bar

len : Period

ama_f_length : Fast EMA Length

ama_s_length : Slow EMA Length

Returns: Adjusted Moving Average (AMA)

cma(src, len)

Corrective Moving average (CMA)

Parameters:

src : Source

len : Period

Returns: Corrective Moving average (CMA)

gmma(src, len)

Geometric Mean Moving Average (GMMA)

Parameters:

src : Source

len : Period

Returns: Geometric Mean Moving Average (GMMA)

ealf(src, len, LAPercLen_, FPerc_)

Ehler's Adaptive Laguerre filter (EALF)

Parameters:

src : Source

len : Period

LAPercLen_ : Median Length

FPerc_ : Median Percentage

Returns: Ehler's Adaptive Laguerre filter (EALF)

elf(src, len, LAPercLen_, FPerc_)

ELF - Ehler's Laguerre filter

Parameters:

src : Source

len : Period

LAPercLen_ : Median Length

FPerc_ : Median Percentage

Returns: Ehler's Laguerre Filter (ELF)

edma(src, len)

Exponentially Deviating Moving Average (MZ EDMA)

Parameters:

src : Source

len : Period

Returns: Exponentially Deviating Moving Average (MZ EDMA)

pnr(src, len, rank_inter_Perc_)

PNR - percentile nearest rank

Parameters:

src : Source

len : Period

rank_inter_Perc_ : Rank and Interpolation Percentage

Returns: Percentile Nearest Rank (PNR)

pli(src, len, rank_inter_Perc_)

PLI - Percentile Linear Interpolation

Parameters:

src : Source

len : Period

rank_inter_Perc_ : Rank and Interpolation Percentage

Returns: Percentile Linear Interpolation (PLI)

rema(src, len)

Range EMA (REMA)

Parameters:

src : Source

len : Period

Returns: Range EMA (REMA)

sw_ma(src, len)

Sine-Weighted Moving Average (SW-MA)

Parameters:

src : Source

len : Period

Returns: Sine-Weighted Moving Average (SW-MA)

vwap(src, len)

Volume Weighted Average Price (VWAP)

Parameters:

src : Source

len : Period

Returns: Volume Weighted Average Price (VWAP)

mama(src, len)

MAMA - MESA Adaptive Moving Average

Parameters:

src : Source

len : Period

Returns: MESA Adaptive Moving Average (MAMA)

fama(src, len)

FAMA - Following Adaptive Moving Average

Parameters:

src : Source

len : Period

Returns: Following Adaptive Moving Average (FAMA)

hkama(src, len)

HKAMA - Hilbert based Kaufman's Adaptive Moving Average

Parameters:

src : Source

len : Period

Returns: Hilbert based Kaufman's Adaptive Moving Average (HKAMA)

bullratioLibrary "bullratio"

Calculate the profit/loss ratio of a permabull for configurable time range

bullratio(len)

calculates the profit/loss ratio for a permabull of age len

Parameters:

len : the number of candles to include in the running bull ratio - 0 for all time

Returns: series float of profit/loss percentage

CarlLibLibrary "CarlLib"

LastLowRedHighGreen(open, close, high, close, reqChangePerc) returns values representing the high of the most recent green and the low of the most recent red

Parameters:

open : open series

close : close series

high : high series

close : close series

reqChangePerc : the minimum require change percentage for the values to switch to new ones.

Returns: