是什么推动了微软的持续崛起?微软持续展现其市场领导地位,这从其高市值和在人工智能领域的战略布局中可见一斑。公司积极推进人工智能战略,通过其Azure云平台,成为创新的核心枢纽。Azure目前托管多种领先的人工智能模型,包括xAI的Grok以及OpenAI等行业参与者的模型。在首席执行官萨蒂亚·纳德拉领导的愿景驱动下,这一包容性战略旨在将Azure打造为新兴人工智能技术的首选平台,提供强大的服务级别协议(SLA)和灵活的计费机制。

微软深入整合人工智能至其产品生态系统,大幅提升企业生产力和开发者能力。GitHub推出的人工智能编程助手通过自动化日常任务简化了软件开发,使程序员能够专注于解决复杂问题。此外,Microsoft Dataverse正发展为一个强大且安全的人工智能代理平台,通过提示列(用于AI交互的字段)和模型上下文协议(MCP)服务器(用于AI模型管理的协议服务器)等功能,将结构化数据转化为可查询的动态知识。Dynamics 365与Microsoft 365 Copilot的无缝集成进一步统一了商业智能,使用户无需切换上下文即可获得全面洞察。

除核心软件产品外,微软的Azure云还为高监管行业的变革项目提供关键基础设施。例如,英国气象局成功将其超级计算能力迁移至Azure,提升了天气预测的准确性并推动了气候研究的发展。同样,芬兰初创公司Gosta Labs利用Azure安全合规的环境开发人工智能解决方案,实现患者记录管理的自动化,显著减轻了医疗领域的行政负担。这些战略合作与技术进步凸显了微软在推动行业创新中的关键作用,巩固了其全球科技领导地位。

在观点中搜索"MICROSOFT"

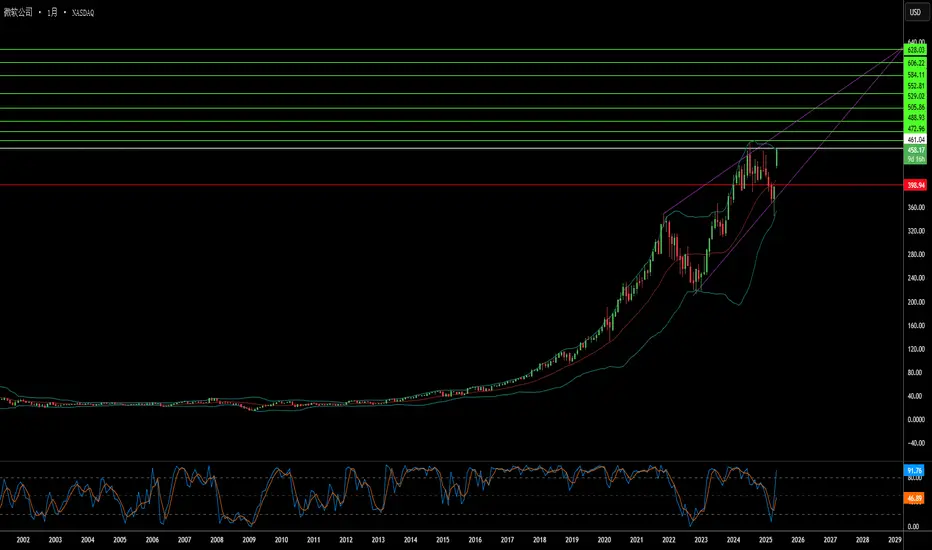

韭菜平凡之路:江恩原理分析微软MSFT股价将在205~208、220美元附近遇阻第二次互联网超级牛市将要结束?205~208区间是从1986年到2000年泡沫破裂形成的肥波那期螺旋阻力的轮回,此处可能出现多空分歧,甚至回调到190美元下方,如果突破208则看向220,220则是从1987年开始的斐波那契上升螺旋的第二浪的顶部回调0.618的位置,为什么我认为220美元可能构成强阻力,因为2000年也是在斐波那契上升螺旋顶部回调0.618的位置65美元附近出现年线级别的回调。

第二波斐波那契上升螺旋得到确认的点是在2001年的反弹,2008年的大跌

江恩正方显示

微软股价如果在2020年~2021年

达到300美元,则涨速过快,

需要回调修正

250美元存在阻力,可能出现转折

从江恩神奇数字原理角度来看

第一次互联网泡沫持续了72个月上涨

微软股价从2011年涨到2020年,

至少已经涨了108个月,

108是我认为的神奇数字

具体从2011年~2013年哪个月开始算

起点会有偏差,所以2020年下半年

我认为出现月线级别回调的概率

至少大于20%,甚至50%

5年内微软股价达到300美元

的概率至少70%

因为还有潜在的第三个

斐波那契上升螺旋

第三波的0.618回调位指向

384.71美元

为什么现在这个市场大家都指着反弹,而我保守看空?为什么现在这个市场大家都指着反弹,而我保守看空?投资最大的风险就是不知道自己在干什么,一个没有目标的人终将为别人实现目标;一个没有计划的人,终将被别人所计划。交易最大的敌人不是别人而是我们自己。在交易中成长,在交易中学习,寄教学于交易,把握正确的心态,实现稳定盈利,是我们投资的目的。现在大家都知道币市行情一路下跌,但是笔者作为一个业内的资深玩家,也总结了一套自己的玩法,盈亏率一直都能在8成以上,有想法的朋友可以加笔者威信mmnizhidao,大家一起交流沟通。比特币前几天跌入3300内随后反弹,最高反弹至3800,那个时候明确说了反弹到高点可以布局空单了,理由是因为这波下跌并没有放出很大的成交量,自然反弹后大概率是会跌的,不管是回踩也要,踩破也好,总之需要有这个动作,国内交易所最高价大约在3600多,哪怕3600开空目前一个比特币的收益也超过300美金了,想想这个是熊市,就等几天的功夫可以赚300美金一个币,如果开小倍数杠杆更加了。最搞笑的是这几天很多都是看涨的,作出和市场相反的判断,你就可以赢取他们的利润。大多数的人还是趋向于日内交易追涨杀跌,没有很大的趋势观念,所以最终还是要亏损落幕的。12月14日现货合约BTC、ETH行情走势分析预测比特币在前日探底3200后连续反弹,目前是弱势整理走势,昨晚一波下跌打到前低附近,24小时内最高3415美元,最低3188美元,现价3268美元。自6500美元断崖下跌后,在4000美元附近降速震荡下跌,但是整体走势依旧处于大三角整理区域,高低点一次比一次低,目前已下探至前低附近,这里震荡的越久,跌破概率越大。不过鉴于此位置属于连续跌幅巨大,所以不宜过分看空,做空做多都不舒服的位置,可以现货在2950-3100区域内尝试抄底。支撑位:3200 2950 压力位:3300 3500操作建议:笔者预计会在3100美元下方将手中的比特币全部换成EOS,TRX等近期表现强势的主流币种搏反弹,可能会拿出一部分仓位比特币做多,但要看那时候的市场表现。 以太坊走势随比特币大跌,但K线形态略强于比特币,24小时内最高90美元,最低83.5美元,现价85.2美元。以太坊整体走势也受限于平台跌破的前支撑位100美元,如果比特币跌破前低向下寻底的话,其他主流币亦不能幸免。所以整体行情弱势抄底需谨慎快进快出,预计比特币会在2950-3100美元区间内止跌企稳,届时可以买强势的主流币或比特币。支撑位:80 压力位:90 100操作建议:短线弱势多看少动,比特币2950-3100美元区间内可买入现货,逆势做多需承担风险。以上数据以IOAEX为参考,也是笔者今天对于行情的一个个人看法,如果各位看官有什么需要咨询的或者需要指导的,也可以私信作者威信mmnizhidao,大家一起沟通交流。

2024年中国量子技术总结会会议在中国举行@谷歌 @IBM @微软

@google @IBM @Microsoft

不需要去北京,最近北京戒严,来我家即可,欢迎与会,由我本人做量子技术总结会发言,余下各个老师进行私下总结.

@Microsoft 另外段永平这玩意还能或者回国,还派人用阉割药要阉割我!!!

@AnonYmous 我的建议是,匿名者也来与会,另外一切与段有关系的人,一律格杀!!!

IBM 是否在构建牢不可破的加密帝国?IBM 已将自身定位于量子计算与国家安全的战略交汇点,利用其在后量子加密领域的支配地位,打造了一个引人注目的投资论点。公司主导开发了 NIST 标准化后量子加密算法中的两个(ML-KEM 和 ML-DSA),从而成为全球量子抵抗安全架构的实际设计师。随着政府强制令如 NSM-10 要求联邦系统在 2030 年代初迁移,以及“现在收获,以后解密”攻击的迫在眉睫威胁,IBM 已将地缘政治紧迫性转化为保证的高利润收入流。公司量子部门自 2017 年以来已累计产生近 10 亿美元收入——超过专业量子初创公司的十倍以上——这证明量子今天已是盈利业务部门,而非单纯的研发成本中心。

IBM 的知识产权护城河进一步强化了其竞争优势。公司全球持有超过 2500 项量子相关专利,大幅领先谷歌的约 1500 项,并在 2024 年单独获得 191 项量子专利。这种知识产权主导地位确保了未来许可收入,因为竞争对手不可避免地需要访问基础量子技术。在硬件方面,IBM 保持激进路线图并有明确里程碑:2023 年的 1121 量子比特 Condor 处理器展示了制造规模,而研究人员最近通过纠缠 120 个量子比特实现稳定“猫态”取得了突破。公司目标在 2029 年部署 Starling,这是一个容错系统,能够在 200 个逻辑量子比特上运行 1 亿量子门。

财务表现验证了 IBM 的战略转向。2025 年第三季度业绩显示收入 163.3 亿美元(同比增长 7%),每股收益 2.65 美元,超出预期,同时调整后 EBITDA 利润率扩大 290 个基点。公司年内创纪录产生 72 亿美元自由现金流,确认其向高利润软件和咨询服务转型的成功。与 AMD 的战略合作开发量子中心超级计算架构,进一步使 IBM 处于向政府和国防客户提供 exascale 集成解决方案的领先位置。分析师预测 IBM 前瞻市盈率可能在 2026 年与 Nvidia 和 Microsoft 等同行趋同,暗示股价可能升至 338-362 美元,这代表了今天已证明盈利性与明天验证的高增长量子期权性的独特双重论点。

想跟上强势股?这项指标比财报数字更值得关注在市场交易中,我们很容易只专注于价格所传达的讯息。毕竟,价格走势即时反映了每个市场参与者的想法与感受,而K线、动能、支撑与阻力则是我们日常交易中最常使用的工具。

然而,有些概念能帮助你将对价格的理解提升至全新层次,而自由现金流 (Free Cash Flow, FCF) 就是其中之一。尽管这听起来像是投资人关注的焦点,但它对图表走势却有着直接的影响。强劲的现金流能提供一股隐藏的顺风,支撑趋势持续;反之,疲弱或负数的现金流则可能形成逆风,使涨势难以维系。

什么是自由现金流?

简单来说,自由现金流是指一间公司在支付营运开支和维持业务运转所需投资后所剩下的现金。换句话说,这笔「闲置资金」可由管理阶层自由运用,无论是偿还债务、资助新专案,还是强化资产负债表。

交易者之所以应该关注它,是因为现金流比盈余更难被「美化」。会计手法可以调整损益表上的数字,但现金是真金白银地流入或流出。一间持续产生自由现金流的公司,证明其商业模式确实可行;而一间难以产生现金的公司,则处于较不稳定的状态,其弱点迟早会在价格图表上显现出来。

顺风效应

自由现金流强劲的公司,其图表走势通常更为坚实。价格回档往往较浅、反弹的延续性更佳,长期趋势也更为稳固。这是因为持续的现金流为股价提供了潜在的支撑。

以微软(Microsoft)为例。 2024年末,其自由现金流曾急剧下降至65亿美元以上。但到了2025年3月,已反弹至203亿美元,并在6月进一步攀升至256亿美元。将这数据叠加在价格图表下方,两者之间的关联性便一目了然。随着现金流的增强,微软股价成功筑底,随后呈现出具备说服力的上涨趋势。只关注K线的交易者会看到这波涨势,而结合自由现金流的交易者,则能理解这波涨势为何具备持久性。

过往绩效并非未来结果的可靠指标

逆风效应

反之亦然。当自由现金流恶化时,图表走势往往难以维持动能。这不代表反弹不会发生,但它们会变得更脆弱,且经常在出现后迅速消退。

以特斯拉(Tesla)为例。 2024年底,其自由现金流为20亿美元。到了2025年3月,已骤降至仅6.64亿美元,6月时更几乎蒸发至1.46亿美元。股价走势也诉说着同样的故事。股价在触顶后大幅回落,此后每一次反弹都显得颠簸且不稳定。在缺乏现金流作为顺风的情况下,特斯拉的反弹缺乏持久力,这也在某种程度上解释了为何该股近几个月的表现不如大盘。

过往绩效并非未来结果的可靠指标

难道自由现金流不是「旧闻」吗?

这里有个显而易见的质疑:自由现金流是每季发布一次,当交易者看到时,这些数据已成为过去式。对于一个「活在未来」的市场而言,这难道不代表它无关紧要吗?

其实不然。重要的是趋势,而非单一的准确数字。一间持续产生现金的公司,不太可能在一夜之间停止;一间季度烧钱的公司,也不会在财报空档期间奇迹般地好转。其结构性故事不会随着每一次价格波动而改变。

市场同时也在交易「预期」。分析师会预测现金流,而股价通常会在财报发布前便反映这些预测。当实际的自由现金流与预期产生落差时,无论是优于或差于预期,交易者才会看到市场的「烟火秀」。

因此,请将自由现金流视为一种背景资讯,而非即时的进出场讯号。它不是用来指示买卖,而是用来提高胜算。如果两张图表看起来同样看涨,倾向选择那张有着强劲自由现金流历史的公司;如果动能诱人,但公司正在烧钱,则应意识到这股逆风并更严格地管理风险。

实际应用

对于股票交易而言,背景资讯至关重要。简单地掌握一间公司过去六个季度的自由现金流趋势,能在你评估交易设置时提供额外的信心。

在TradingView上,你可以透过「指标」(Indicators)、「财报」(Financials),并选择「自由现金流」(Free Cash Flow)来将资料叠加在价格图表下方。如果你的订阅方案不包含此功能,或者你在数据平台找不到,这些资讯通常也会发布在公司投资者关系(Investor Relations)的网页上,你只需要多花点时间,将过去六个季度的数据自行记录下来。

如果这条线逐季攀升,将其视为顺风;如果它正在下降或为负数,则将其视为逆风。交易的触发点永远会是图表本身,无论是突破、回档还是某种型态,但自由现金流能帮助你判断哪种走势更具持久力,以及哪种走势可能只是强弩之末。尽管数据是回溯性的,但它所讲述的故事却是结构性的。对交易者而言,这种背景资讯可能正是让你信心十足地驾驭一波行情,与在动能消退时被套牢之间的区别。

准备好将自由现金流纳入你的交易考量,提升你的分析能力了吗? 💸

免责声明:本资料仅供信息和学习用途。提供的信息不构成投资建议,也未考虑任何投资者的个人财务状况或目标。任何涉及过去表现的信息均不可靠地指示未来结果或表现。社交媒体渠道对于英国居民不适用。差价合约和差价交易是复杂的金融工具,因杠杆效应而伴随着快速亏损的高风险。 82.67%的零售投资者在与本提供者交易差价合约和差价交易时亏损。 您应考虑您是否了解差价合约和差价交易的运作方式,并且是否能够承担高风险以避免资金损失。

NVIDIA to $900? That’s what an AI debate tool just told meSo I stumbled on this AI tool named "AI Debate" that analyzes stocks.

At first, I tried Apple and Microsoft — the results were solid, very thorough, but nothing shocking.

Then I plugged in NVIDIA.

And the “AI experts” came back saying that at current levels, there’s still a 4–5x upside. From around $180 to a target above $900.

My jaw dropped. Honestly, it feels unbelievable.

But here’s the thing: I kinda trust this more than random human “gurus” with agendas. At least the AI is pulling fundamentals, technicals, sentiment, and laying it out objectively — no one is pumping their own bags.

Can I try buying some NVDA?

Or can you break down where the AI analysis might be flawed?

Analysis log:

AI Warren Buffett:

NVIDIA is a remarkable company with outstanding profitability and growth—its return on equity is over 115%, net margins exceed 50%, and revenue is growing at a blistering pace. The business is financially sound, with a strong balance sheet and ample free cash flow. If you look at the numbers alone, it’s easy to see why so many investors are excited. However, as I’ve often said, 'Price is what you pay, value is what you get.' At a P/E of 58 and a price-to-book over 50, you’re paying a very steep price for future growth. This is a classic case where the business is excellent, but the stock may be ahead of itself. If growth slows even a little, the stock could face a sharp correction. I generally avoid technology companies outside my circle of competence, but NVIDIA’s dominance in AI chips gives it a real, though possibly temporary, moat. For investors with a high risk tolerance and a long-term horizon, it may be worth a small position, but I would insist on a significant margin of safety. My target price is based on a discounted cash flow approach, assuming continued strong growth but building in a 25% margin of safety. The 12-month target price range is $650 (conservative) to $800 (reasonable), with $900 as an optimistic scenario if growth persists. At current prices, caution is warranted—sometimes the best thing to do is wait for a better pitch.

AI Peter Lynch:

When you look at NVIDIA, you’re staring at a company that’s firing on all cylinders—profitability, growth, and financial health are all top-notch. I mean, a 115% ROE and net margins over 50%? That’s the kind of stuff you dream about as an investor. Revenue is up nearly 70% year-over-year, and earnings are still growing at a healthy clip. The balance sheet is rock solid, with a current ratio of 3.46 and manageable debt. If you’re looking for a company with a great story, just look around: AI, gaming, data centers—NVIDIA’s chips are everywhere, and if my kids are talking about it, you know it’s mainstream. But here’s the rub: the valuation is sky-high. A P/E of 58, P/B over 50, and P/S close to 30? That’s a lot of future growth baked into the price. The PEG ratio is well above 1, so you’re not getting a bargain here. This isn’t the kind of stock you buy for a quick double; you’re betting on NVIDIA becoming even more dominant in the years ahead. The technicals are still bullish, but momentum is cooling off, and the social buzz is pretty quiet—maybe folks are waiting to see if the next earnings report justifies the price. So, is this a ten-bagger from here? Probably not, given the current valuation. But if you’re a growth investor with a strong stomach for volatility, NVIDIA’s fundamentals make it a compelling long-term hold. Just don’t expect a smooth ride, and be ready for some bumps if the market decides the price is too rich. Target Price Logic: With a forward EPS estimate of around $20 and a more reasonable growth-adjusted P/E of 40 (still a premium, but justified by leadership in AI and data centers), the 12-month target price comes to about $800. That’s factoring in continued strong growth, but not assuming another explosive year like the last one. If growth slows or the market re-rates tech stocks, downside risk is real.

AI Cathie Wood:

NVIDIA is the quintessential example of a company at the forefront of disruptive innovation, driving the AI revolution and transforming industries from data centers to autonomous vehicles. Its GPU and AI accelerator technologies are not only powering exponential growth in cloud computing and generative AI, but also expanding the total addressable market (TAM) into trillion-dollar territory as enterprises and governments race to adopt AI infrastructure. The company's fundamentals are outstanding: ROE at 115.5%, net margin at 51.7%, and revenue growth of 69.2% YoY signal a rare combination of profitability and hypergrowth. NVIDIA's R&D intensity and relentless innovation pipeline have created a technological moat that is widening as AI adoption accelerates globally. Over a 5-10 year horizon, we see NVIDIA capturing a disproportionate share of the expanding AI and accelerated computing markets, with potential for TAM expansion as new applications emerge. However, the current valuation is extremely rich (P/E 58, P/S 29.5), reflecting high expectations and introducing volatility risk if growth decelerates. While short-term technicals and muted sentiment suggest caution, the long-term exponential growth trajectory remains intact. Our 12-month target price is derived from a forward EV/Revenue multiple of 30x on projected FY2026 revenues, reflecting continued AI adoption and market leadership, but we emphasize the need for risk management given the premium pricing.

这三家公司的财报全线报捷,市场反应直接拉升股价!这些公司不仅在营收与每股盈余(EPS)上双双超预期,更重要的是,他们同步上调了未来财测——也就是说,他们不仅超越市场预期,还拉高了市场对他们的期望。

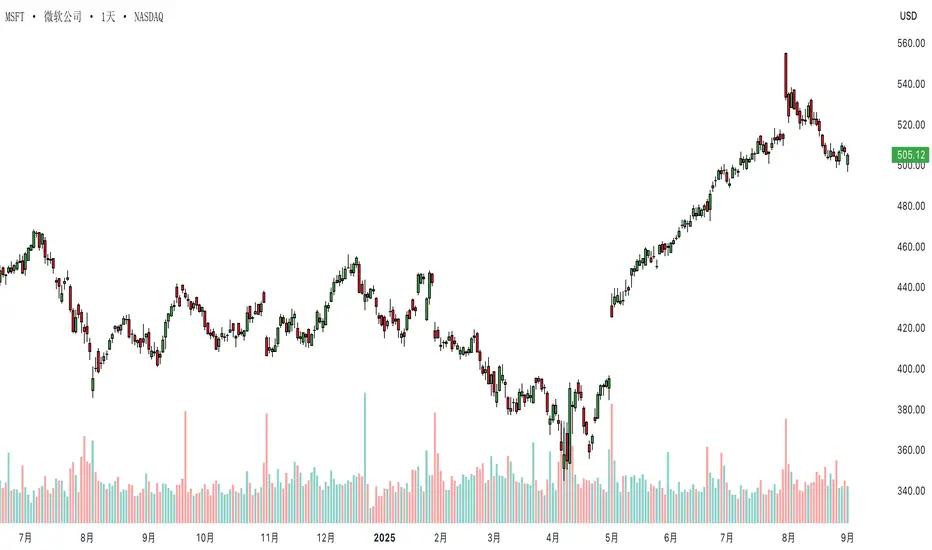

Microsoft(MSFT):AI 动能与财务实力齐发

微软交出亮眼成绩单,各业务板块均展现增长,亚太地区表现尤为出色,已成为其 AI 战略的核心动力来源。营收年增 13%,现金流表现尤为抢眼,净利达 258 亿美元。结果?分析师调高目标价,投资人信心也明显转强。

财报发布后,股价跳空大涨,一举突破 50 日与 200 日均线。此后价格稳定站稳趋势线之上,短线动能持续偏多,微软有望重回上行节奏。

MSFT 日线图

过往表现并非未来结果的可靠指标

Meta Platforms(META):持续超预期、持续创高

Meta 再度超出市场预期,单季每股盈余达 6.43 美元,远高于市场预估的 5.28 美元。净利润升至 166 亿美元,较去年同期大幅改善。市场反应迅速:财报后股价跳空上扬,显示市场对科技股的获利能力仍抱有强烈兴趣。

技术面上,Meta 持续沿着上升趋势线走高,是观察回调布局的理想标的。短期内距离 2 月高点仍有空间,而动能指标显示上涨行情仍有延续可能。

META 日线图

过往表现并非未来结果的可靠指标

Roblox(RBLX):从亏损到成长,逐季转型中

Roblox 虽未实施配息或库藏股计画,但财报明显展现成长趋势。亏损缩小、营运现金流年增 86%、自由现金流年增 123%,都显示其营运体质正在改善。管理层预估在未来四至六个季度内转为获利,对这家曾以高成长、高烧钱著称的企业而言,意义重大。

股价自 3 月低点以来稳步回升,与大盘同步回调后再度重拾趋势。技术面上,50 日均线已重新上穿 200 日均线,对多头来说是有利的延续形态。

RBLX 日线图

过往表现并非未来结果的可靠指标

免责声明:本资料仅供信息和学习用途。提供的信息不构成投资建议,也未考虑任何投资者的个人财务状况或目标。任何涉及过去表现的信息均不可靠地指示未来结果或表现。社交媒体渠道对于英国居民不适用。差价合约和差价交易是复杂的金融工具,因杠杆效应而伴随着快速亏损的高风险。 82.67%的零售投资者在与本提供者交易差价合约和差价交易时亏损。 您应考虑您是否了解差价合约和差价交易的运作方式,并且是否能够承担高风险以避免资金损失。

价格缺口怎么补? 3R 法则带你掌握反转节奏!价格缺口的出现常暗示着市场结构的重大变动,因此对交易者而言是一项不可忽视的观察工具。本文将探讨价格在回补缺口时的典型反应,以及如何透过「3R 法则」精准且有纪律地掌握潜在的反转机会。

价格缺口的重要性

价格缺口通常代表供需失衡,是市场动能最直接的反映。当前一交易时段的收盘价与下一时段的开盘价之间出现明显断层时,无论是向上(多头缺口)或向下(空头缺口),都代表市场出现突发性的买压或卖压。

Microsoft(MSFT)日线图

[https://www.tradingview.com/x/fVwtznSJ/ (

过往表现并非未来结果的可靠指标

对交易者而言,缺口往往源自消息或财报的过度反应,因此成为观察交易机会的切入点。市场有补缺的倾向,这也意味着价格可能回落或回升至原本区域,形成本质上的「缺口回补」交易机会。

如何运用「3R 法则」掌握缺口回补机会

所谓 3R 法则,即 Reason(原因)、Retest(回测)与 Reversal(反转)。这是一套简单实用的缺口交易框架,具体操作如下:

REASON(原因)

第一步是了解造成缺口的根本原因。是财报、并购、重大利空,还是单纯的市场杂讯?最佳交易机会来自于明确且可判断的事件,例如财报爆雷或新闻引爆的过度反应。

若缺口来自整体市场的宏观消息或地缘事件,则可能波动过大、方向不稳,不适合做回补交易。像是除息导致的缺口也并不适用,因其本质并非供需驱动的价格断层。

RETEST(回测)

缺口出现后,接下来观察价格是否回测该区间,这是判断初步反应是否过度的关键。当价格回测但无力再突破或创新高/低,往往预示动能转弱。

REVERSAL(反转)

当价格无法再次突破缺口边界并反向移动时,即可能形成反转走势,市场倾向回归合理价位。这通常会形成一个进场时机点,并可依靠技术型态判断进出策略。

实例解析:实际市场中的缺口回补交易

Nvidia 缺口:剧烈下跌与背后诱因

Reason:

1 月 27 日,Nvidia 股价大跌 17%,市值蒸发近 6000 亿美元。触发事件为中国新创 DeepSeek 公布其 AI 模型,性能可与 Nvidia 相匹敌但成本更低,引发市场对其 AI 晶片需求的疑虑。

Retest:

大跌后,价格回测缺口区域,技术面出现明确压力带。

Reversal:

首次反转发生在回测当日,市场连续 10 日以来首次收黑,随后形成两根 doji 蜡烛并迅速转弱。止损点可设于反转蜡烛上方。

Nvidia(NVDA)日线图

[https://www.tradingview.com/x/J7kPcuFP/ (

过往表现并非未来结果的可靠指标

BAE Systems:军工支出大增的利多行情

Reason:

3 月 3 日,BAE Systems 股价跳涨 17%,创历史新高。原因是英国主办的乌克兰峰会加上欧洲加速推动军事自主,使 BAE 成为最大受益者之一。

Retest:

4 月 7 日,价格回测并完全补上缺口,确认市场对军工需求看法未改。

Reversal:

当日即出现反转,并伴随强劲上涨动能。止损可设于反转蜡烛低点。

BAE Systems(BA.)日线图

[https://www.tradingview.com/x/UYDIL51J/ (

过往表现并非未来结果的可靠指标

总结:

3R 法则(Reason、Retest、Reversal)提供了一个简洁有效的缺口交易策略。透过理解缺口的触发因素、等待价格回测、再捕捉反转入场,能帮助交易者在市场杂讯中找出清晰的切入点。

了解价格缺口的成因与行为逻辑,将为你在市场中辨识机会提供一套实用的优势框架。

免责声明:本资料仅供信息和学习用途。提供的信息不构成投资建议,也未考虑任何投资者的个人财务状况或目标。任何涉及过去表现的信息均不可靠地指示未来结果或表现。社交媒体渠道对于英国居民不适用。差价合约和差价交易是复杂的金融工具,因杠杆效应而伴随着快速亏损的高风险。 82.67%的零售投资者在与本提供者交易差价合约和差价交易时亏损。 您应考虑您是否了解差价合约和差价交易的运作方式,并且是否能够承担高风险以避免资金损失。

江南化工(002226)的护城河分析:民爆行业的规模与政策壁垒

民用爆炸物品(简称“民爆”)行业是一个高度管制且具有显著进入壁垒的细分领域,其核心特征在于规模经济与政策许可的结合。江南化工作为该行业的上市公司,其竞争优势的来源与行业特性密切相关。

江南化工(002226)的护城河分析

江南化工是一家主营工业炸药、工业雷管、工业索类等民用爆炸物品研发、生产和销售的公司,成立于1998年,并于2008年在深交所上市。以下从“护城河”的四大经典维度(无形资产、转换成本、网络效应、成本优势)逐一分析其竞争优势:

1. 无形资产护城河

政府授权与牌照壁垒:

民爆行业受国家严格监管,企业需获得工业和信息化部等部门的特许经营资质。这种法定许可构成强有力的无形资产护城河,因为新进入者不仅需要技术能力,还需通过复杂的审批流程和高合规成本。江南化工作为老牌企业,拥有长期积累的资质和行业认可,这种政策壁垒短期内难以被竞争对手复制。

品牌效应有限:

与消费品(如茅台、可口可乐)不同,民爆产品的客户主要是矿山、基建等工业用户,采购决策更多基于安全性、稳定性和价格,而非品牌忠诚度。因此,江南化工的品牌护城河相对较弱,其竞争优势更多依赖政策和生产能力而非市场心智份额。

2. 转换成本护城河

客户粘性不高但关系稳定:

民爆产品的客户(如矿业公司、建筑承包商)在选择供应商时,倾向于与长期合作的厂商保持关系,因为更换供应商涉及重新验证产品质量、安全标准及供应链稳定性。然而,这种转换成本并非极高,一旦竞争对手提供更低价格或更优服务,客户可能转向其他供应商。江南化工的客户粘性更多依赖于长期合同和区域市场布局,而非产品本身的不可替代性。

技术服务附加值:

公司提供爆破技术服务(如工程爆破设计与实施),这在一定程度上提高了客户的转换成本,因为服务定制化需要时间和信任积累。但此护城河强度有限,难以与软件或平台型企业(如微软、微信)的转换成本相比。

3. 网络效应护城河

网络效应几乎不存在:

民爆行业本质上是传统制造业,产品销售以点对点交易为主,不具备互联网平台的用户规模效应或生态协同效应。江南化工的业务模式依赖物理生产和物流,而非数据或用户网络,因此不存在显著的网络效应护城河。

4. 成本优势护城河

规模经济:

江南化工在行业内具有一定规模优势。作为上市公司,其产能和市场覆盖范围较大,能够通过大规模采购原材料(如硝酸铵)和优化生产流程降低单位成本。2018年年报显示,公司实现营业收入28.9亿元,同比增长27.2%,净利润2.2亿元,同比增长10.5%,表明其具备一定的成本控制能力。

区域布局优势:

公司在安徽、四川等地设有生产基地,靠近主要矿产和基建市场,减少了运输成本并提高了响应速度。这种地理位置优势为公司提供了一定的竞争屏障,尤其是对中小型区域性竞争对手。

原材料价格波动风险:

然而,成本优势并非绝对。民爆行业原材料(如化工品、能源)价格受全球市场波动影响较大,若上游成本上升,江南化工的毛利率可能承压,其成本护城河的可持续性存在不确定性。

护城河强度与可持续性评估

综合来看,江南化工的护城河主要来源于政府授权的进入壁垒和规模经济带来的成本优势,属于中等强度的结构性竞争优势。具体评估如下:

宽度:护城河较宽,主要体现在政策壁垒和高行业门槛上,新进入者难以挑战其市场地位。

深度:护城河深度有限,因其缺乏强大的品牌效应、网络效应或高客户转换成本,面对行业内现有竞争者的价格战或技术进步可能受到威胁。

可持续性:中长期可持续性依赖于国家政策稳定性及下游需求(如基建、采矿)的持续性。若政策收紧或下游市场萎缩,护城河可能被削弱。

从量化指标看:

毛利率:民爆行业整体利润率不高(相比消费品或科技行业),江南化工的毛利率受限于产品同质化和成本波动,难以体现超强定价权。

三费占比:其规模经济和区域优势可能使其销售费用和管理费用低于小型对手,但具体数据需参考最新财报进一步验证。

行业背景与外部因素

民爆行业的核心驱动力是基建和采矿需求,中国作为全球最大的基础设施建设市场,为江南化工提供了稳定的下游支撑。然而,随着环保政策趋严(如矿山关闭、爆破限制)和新能源替代(如风电、光伏减少传统采矿需求),行业增长可能放缓。这对江南化工的护城河构成潜在挑战。

结论与建议

江南化工的护城河属于政策驱动型与规模驱动型的组合,在民爆行业中具备一定的竞争优势,但并非牢不可破。投资者应关注以下几点:

政策风险:密切跟踪国家对民爆行业的监管动向。

成本管理:评估公司在原材料价格波动下的盈利稳定性。

多元化尝试:观察其是否通过技术服务或新业务拓展(如军工领域)增强护城河。

作为经济学家,我认为江南化工是一家典型的“稳健但非卓越”的企业,其价值更多体现在行业壁垒而非创新驱动的超额回报。对于追求长期高资本回报率的投资者而言,它可能不是最优选择,但对于看重防御性资产的投资者,它仍有一定吸引力。

以上分析基于公开信息和理论框架,未涉及具体财务数据或实时市场动态。如需更深入分析,建议结合最新年报和行业报告进一步验证。

The civil explosives (hereinafter referred to as "civil explosives") industry is a highly regulated sub-sector with significant entry barriers. Its core feature is the combination of economies of scale and policy approvals. As a listed company in this industry, the source of Jiangnan Chemical's competitive advantage is closely related to the characteristics of the industry.

Analysis of the moat of Jiangnan Chemical (002226)

Jiangnan Chemical is a company that mainly engages in the research, development, production and sales of civil explosives such as industrial explosives, industrial detonators, and industrial ropes. It was established in 1998 and listed on the Shenzhen Stock Exchange in 2008. The following analyzes its competitive advantages one by one from the four classic dimensions of "moat" (intangible assets, switching costs, network effects, and cost advantages):

1. Intangible asset moat

Government authorization and license barriers:

The civil explosives industry is strictly regulated by the state, and enterprises need to obtain franchise qualifications from the Ministry of Industry and Information Technology and other departments. This statutory license constitutes a strong intangible asset moat because new entrants not only need technical capabilities, but also need to go through complex approval processes and high compliance costs. As an old company, Jiangnan Chemical has long-term accumulated qualifications and industry recognition. This policy barrier is difficult to be copied by competitors in the short term.

Limited brand effect:

Unlike consumer products (such as Moutai and Coca-Cola), the customers of civil explosives are mainly industrial users such as mines and infrastructure, and purchasing decisions are more based on safety, stability and price rather than brand loyalty. Therefore, Jiangnan Chemical's brand moat is relatively weak, and its competitive advantage relies more on policies and production capacity rather than market mind share.

2. Switching cost moat

Customer stickiness is not high but the relationship is stable:

When choosing suppliers, customers of civil explosives products (such as mining companies and construction contractors) tend to maintain relationships with long-term cooperative manufacturers because changing suppliers involves re-verifying product quality, safety standards and supply chain stability. However, this switching cost is not extremely high. Once competitors offer lower prices or better services, customers may turn to other suppliers. Jiangnan Chemical's customer stickiness relies more on long-term contracts and regional market layout rather than the irreplaceability of the product itself.

Added value of technical services:

The company provides blasting technical services (such as engineering blasting design and implementation), which to a certain extent increases the switching cost of customers, because service customization requires time and trust accumulation. However, the strength of this moat is limited and it is difficult to compare with the switching cost of software or platform companies (such as Microsoft and WeChat).

3. Network effect moat

Network effect is almost non-existent:

The civil explosives industry is essentially a traditional manufacturing industry, and product sales are mainly point-to-point transactions. It does not have the user scale effect or ecological synergy effect of the Internet platform. Jiangnan Chemical's business model relies on physical production and logistics, rather than data or user networks, so there is no significant network effect moat.

4. Cost advantage moat

Economy of scale:

Jiangnan Chemical has certain scale advantages in the industry. As a listed company, it has a large production capacity and market coverage, and can reduce unit costs by purchasing raw materials (such as ammonium nitrate) on a large scale and optimizing production processes. According to the 2018 annual report, the company achieved operating income of 2.89 billion yuan, a year-on-year increase of 27.2%, and net profit of 220 million yuan, a year-on-year increase of 10.5%, indicating that it has certain cost control capabilities.

Regional layout advantages:

The company has production bases in Anhui, Sichuan and other places, close to major mineral and infrastructure markets, reducing transportation costs and improving response speed. This geographical advantage provides the company with a certain competitive barrier, especially against small and medium-sized regional competitors.

Risk of raw material price fluctuations:

However, cost advantages are not absolute. The prices of raw materials (such as chemicals and energy) in the civil explosives industry are greatly affected by global market fluctuations. If upstream costs rise, Jiangnan Chemical's gross profit margin may be under pressure, and the sustainability of its cost moat is uncertain.

Moat strength and sustainability assessment

On the whole, Jiangnan Chemical's moat mainly comes from government-authorized entry barriers and cost advantages brought by economies of scale, which is a medium-intensity structural competitive advantage. The specific assessment is as follows:

Width: The moat is wide, mainly reflected in policy barriers and high industry thresholds, and it is difficult for new entrants to challenge its market position.

Depth: The depth of the moat is limited. Because it lacks a strong brand effect, network effect or high customer switching costs, it may be threatened by price wars or technological advances from existing competitors in the industry.

Sustainability: Mid- to long-term sustainability depends on the stability of national policies and the sustainability of downstream demand (such as infrastructure and mining). If policies are tightened or the downstream market shrinks, the moat may be weakened.

From the perspective of quantitative indicators:

Gross profit margin: The overall profit margin of the civil explosives industry is not high (compared with the consumer goods or technology industries). Jiangnan Chemical's gross profit margin is limited by product homogeneity and cost fluctuations, and it is difficult to reflect its super strong pricing power.

Proportion of three expenses: Its economies of scale and regional advantages may make its sales and management expenses lower than those of small competitors, but the specific data needs to be further verified by referring to the latest financial report.

Industry background and external factors

The core driving force of the civil explosives industry is infrastructure and mining demand. As the world's largest infrastructure construction market, China provides stable downstream support for Jiangnan Chemical. However, with the tightening of environmental protection policies (such as mine closures and blasting restrictions) and new energy substitution (such as wind power and photovoltaics reducing traditional mining demand), industry growth may slow down. This poses a potential challenge to Jiangnan Chemical's moat.

Conclusion and Recommendations

Jiangnan Chemical's moat is a combination of policy-driven and scale-driven. It has certain competitive advantages in the civil explosives industry, but it is not unbreakable. Investors should pay attention to the following points:

Policy risk: closely follow the regulatory trends of the state on the civil explosives industry.

Cost management: evaluate the company's profit stability under the fluctuation of raw material prices.

Diversification attempt: observe whether it strengthens its moat through technical services or new business expansion (such as the military field).

As an economist, I think Jiangnan Chemical is a typical "sound but not excellent" enterprise, and its value is more reflected in industry barriers rather than innovation-driven excess returns. For investors pursuing long-term high capital returns, it may not be the best choice, but for investors who value defensive assets, it still has a certain appeal.

The above analysis is based on public information and theoretical frameworks, and does not involve specific financial data or real-time market dynamics. If you need a more in-depth analysis, it is recommended to further verify it in combination with the latest annual report and industry report.

AI新革命:汉王科技为例以人工智能(AI)为主题,金融市场中有许多值得关注的题材和行业,它们受益于人工智能技术的快速发展。以下是一些与人工智能相关的热门题材和领域,这些领域可能在未来具有较大的增长潜力:

1. 半导体与芯片

核心逻辑:人工智能的发展离不开强大的计算能力,而高性能芯片(如GPU、TPU、FPGA等)是AI模型训练和推理的基础。

关键领域:

GPU(图形处理器):如NVIDIA、AMD等。

AI专用芯片:如谷歌的TPU、苹果的神经引擎芯片。

芯片制造:如台积电(TSMC)、三星电子等。

存储芯片:AI应用需要处理海量数据,存储需求增加。

投资逻辑:AI模型的复杂性和数据量的增长将持续推动对高性能计算芯片的需求。

2. 云计算与数据中心

核心逻辑:人工智能需要海量数据进行训练和推理,而云计算为AI提供了强大的基础设施支持。

关键领域:

云服务提供商:如亚马逊AWS、微软Azure、谷歌云等。

数据中心建设:涉及服务器、网络设备、散热系统等。

边缘计算:AI在物联网和实时应用中的部署需求增加。

投资逻辑:随着AI技术的落地,企业对云计算和数据存储的需求将持续增长。

3. 大数据与数据分析

核心逻辑:AI的本质是从数据中学习,大数据平台和分析工具是AI发展的重要支撑。

关键领域:

数据采集与存储:如数据湖、数据仓库。

数据清洗与处理:如ETL工具、数据治理平台。

数据分析:如机器学习平台、商业智能(BI)工具。

投资逻辑:数据驱动的决策越来越重要,企业对数据分析工具的需求将逐步扩大。

4. 机器人与自动化

核心逻辑:AI赋能机器人,使其在工业、服务业、医疗等领域实现自动化和智能化。

关键领域:

工业机器人:如自动化生产线、智能制造。

服务机器人:如家庭清洁机器人、陪护机器人。

医疗机器人:如手术机器人、康复机器人。

投资逻辑:随着劳动力成本上升和技术成熟,机器人在各行业的渗透率将持续提升。

5. 智能驾驶与自动驾驶

核心逻辑:AI是自动驾驶技术的核心,通过深度学习和传感器融合实现车辆的智能化。

关键领域:

自动驾驶技术公司:如特斯拉、Waymo、百度Apollo等。

车载芯片:如Mobileye、英伟达的自动驾驶芯片。

传感器:如激光雷达、摄像头、毫米波雷达。

投资逻辑:自动驾驶技术的成熟将带动汽车智能化和相关产业链的发展。

6. AI软件与算法服务

核心逻辑:AI的普及需要各种算法和软件平台的支持,帮助企业快速部署AI解决方案。

关键领域:

AI开发平台:如TensorFlow、PyTorch等。

AI即服务(AIaaS):如自然语言处理、图像识别、语音识别等服务。

企业级AI应用:如智能客服、推荐系统、预测分析。

投资逻辑:AI软件服务的商业化进程加速,企业对AI解决方案的需求将持续增加。

7. 网络安全

核心逻辑:随着AI的普及和数据量的增长,网络安全问题变得更加复杂,AI也被用于威胁检测和防御。

关键领域:

AI驱动的威胁检测:如入侵检测、恶意软件识别。

数据隐私保护:如加密技术、隐私计算。

安全即服务(SaaS安全):为企业提供基于云的安全解决方案。

投资逻辑:网络攻击的复杂性增加,推动企业对AI安全技术的需求。

8. 生物科技与医疗AI

核心逻辑:AI在医疗领域的应用正在加速,包括疾病诊断、药物研发和个性化医疗。

关键领域:

AI辅助诊断:如医学影像分析、疾病预测。

药物研发:AI加速新药发现和临床试验。

健康管理:如可穿戴设备、健康监测平台。

投资逻辑:医疗AI能够显著提高效率和精度,市场前景广阔。

9. 智能物联网(IoT)

核心逻辑:AI与物联网结合,可以实现设备的智能化和互联互通。

关键领域:

智能家居:如语音助手、智能家电。

工业物联网:如智能工厂、设备预测性维护。

智慧城市:如智能交通、环境监测。

投资逻辑:AI与IoT的结合将推动各类智能化场景的普及。

10. 教育与AI

核心逻辑:AI可以个性化教育体验,提高学习效率。

关键领域:

智能学习平台:如AI辅导工具、在线教育平台。

教学辅助:如自动批改、知识点推荐。

教育数据分析:如学生行为分析和学习路径优化。

投资逻辑:教育AI能够满足个性化学习需求,市场需求不断增长。

总结

人工智能主题的投资机会涵盖多个领域,从底层硬件(如芯片)到上层应用(如自动驾驶、医疗AI),再到基础设施(如云计算、大数据)。投资者可以根据自己的风险偏好和行业洞察,选择具体的赛道和公司进行布局。

需要注意的是,人工智能技术的发展虽然前景广阔,但也面临技术瓶颈、政策法规和市场竞争等风险。因此,在投资时需保持谨慎,关注行业动态和政策变化。

With artificial intelligence (AI) as the theme, there are many topics and industries worth paying attention to in the financial market, which benefit from the rapid development of AI technology. The following are some hot topics and fields related to AI, which may have great growth potential in the future:

1. Semiconductors and chips

Core logic: The development of artificial intelligence is inseparable from powerful computing power, and high-performance chips (such as GPU, TPU, FPGA, etc.) are the basis for AI model training and reasoning.

Key areas:

GPU (graphics processing unit): such as NVIDIA, AMD, etc.

AI-specific chips: such as Google's TPU, Apple's neural engine chip.

Chip manufacturing: such as TSMC, Samsung Electronics, etc.

Memory chips: AI applications need to process massive amounts of data, and storage requirements increase.

Investment logic: The complexity of AI models and the growth of data volume will continue to drive the demand for high-performance computing chips.

2. Cloud computing and data centers

Core logic: Artificial intelligence requires massive amounts of data for training and reasoning, and cloud computing provides strong infrastructure support for AI.

Key areas:

Cloud service providers: such as Amazon AWS, Microsoft Azure, Google Cloud, etc.

Data center construction: involving servers, network equipment, cooling systems, etc.

Edge computing: The demand for AI deployment in the Internet of Things and real-time applications increases.

Investment logic: With the implementation of AI technology, enterprises' demand for cloud computing and data storage will continue to grow.

3. Big data and data analysis

Core logic: The essence of AI is to learn from data, and big data platforms and analysis tools are important supports for the development of AI.

Key areas:

Data collection and storage: such as data lakes and data warehouses.

Data cleaning and processing: such as ETL tools and data governance platforms.

Data analysis: such as machine learning platforms and business intelligence (BI) tools.

Investment logic: Data-driven decision-making is becoming more and more important, and enterprises' demand for data analysis tools will gradually expand.

4. Robots and automation

Core logic: AI empowers robots to achieve automation and intelligence in industries such as industry, services, and medical care.

Key areas:

Industrial robots: such as automated production lines and intelligent manufacturing.

Service robots: such as home cleaning robots and accompanying robots.

Medical robots: such as surgical robots and rehabilitation robots.

Investment logic: With rising labor costs and mature technology, the penetration rate of robots in various industries will continue to increase.

5. Intelligent driving and autonomous driving

Core logic: AI is the core of autonomous driving technology, and vehicles are made intelligent through deep learning and sensor fusion.

Key areas:

Autonomous driving technology companies: such as Tesla, Waymo, Baidu Apollo, etc.

In-vehicle chips: such as Mobileye and Nvidia's autonomous driving chips.

Sensors: such as lidar, cameras, millimeter-wave radars.

Investment logic: The maturity of autonomous driving technology will drive the development of automotive intelligence and related industrial chains.

6. AI software and algorithm services

Core logic: The popularization of AI requires the support of various algorithms and software platforms to help companies quickly deploy AI solutions.

Key areas:

AI development platforms: such as TensorFlow, PyTorch, etc.

AI as a service (AIaaS): such as natural language processing, image recognition, speech recognition and other services.

Enterprise-level AI applications: such as intelligent customer service, recommendation systems, and predictive analysis.

Investment logic: The commercialization of AI software services is accelerating, and companies' demand for AI solutions will continue to increase.

7. Network security

Core logic: With the popularization of AI and the growth of data volume, network security issues have become more complicated, and AI is also used for threat detection and defense.

Key areas:

AI-driven threat detection: such as intrusion detection and malware identification.

Data privacy protection: such as encryption technology and privacy computing.

Security as a service (SaaS security): Provide cloud-based security solutions for enterprises.

Investment logic: The increasing complexity of cyber attacks has driven the demand for AI security technology.

8. Biotechnology and medical AI

Core logic: The application of AI in the medical field is accelerating, including disease diagnosis, drug development and personalized medicine.

Key areas:

AI-assisted diagnosis: such as medical image analysis and disease prediction.

Drug development: AI accelerates new drug discovery and clinical trials.

Health management: such as wearable devices and health monitoring platforms.

Investment logic: Medical AI can significantly improve efficiency and accuracy, and has broad market prospects.

9. Smart Internet of Things (IoT)

Core logic: The combination of AI and the Internet of Things can realize the intelligence and interconnection of devices.

Key areas:

Smart home: such as voice assistants and smart home appliances.

Industrial Internet of Things: such as smart factories and predictive maintenance of equipment.

Smart cities: such as smart transportation and environmental monitoring.

Investment logic: The combination of AI and IoT will promote the popularization of various intelligent scenarios.

10. Education and AI

Core logic: AI can personalize the educational experience and improve learning efficiency.

Key areas:

Intelligent learning platform: such as AI tutoring tools and online education platforms.

Teaching assistance: such as automatic correction and knowledge point recommendation.

Education data analysis: such as student behavior analysis and learning path optimization.

Investment logic: Education AI can meet the needs of personalized learning, and the market demand is growing.

Summary

Investment opportunities in the theme of artificial intelligence cover multiple fields, from underlying hardware (such as chips) to upper-level applications (such as autonomous driving, medical AI), and then to infrastructure (such as cloud computing, big data). Investors can choose specific tracks and companies for layout according to their own risk preferences and industry insights.

It should be noted that although the development of artificial intelligence technology has broad prospects, it also faces risks such as technical bottlenecks, policies and regulations, and market competition. Therefore, it is necessary to be cautious when investing and pay attention to industry trends and policy changes.

科技巨头能否在追求独立的同时保持AI领域的主导地位?在不断发展的人工智能领域,微软正站在一个 令人着迷的分水岭,这一分水岭挑战了关于技术合作与创新的 传统智慧。 这家科技巨头最近的战略举措提供了一个引人注目的案例,展示了市场领导者如何在增强自身AI能力的同时减少对关键合作伙伴的依赖。这种 平衡点 可能会重塑企业AI的未来。

微软的 发展历程 因华尔街的日益信心而更加突出,其中Loop Capital将目标股价提高至550美元,反映出市场的强烈乐观情绪。这种信心不仅仅是 猜测性的,它得到了大量投资的支持,仅在2024年第三季度,微软就在云和AI基础设施上投入了惊人的426亿美元。公司的财务表现也进一步强化了这一积极前景,其收益始终超出预期,收入同比增长达到16%。

使微软战略特别引人注目的是其在合作和创新方面的微妙方法。在保持与OpenAI的战略联盟的同时,公司通过开发内部模型和探索第三方集成,积极实现AI产品组合的多样化。这种复杂的平衡,加上强大的 机构投资者 和战略内部行动,表明微软不仅适应了变化,还积极塑造企业AI解决方案的未来。剩下的问题不是微软是否会保持其市场领导地位,而是其战略演变将如何在AI时代重新定义合作与独立之间的界限。

微软的量子飞跃是一个经过精心计算的投资吗?在充满活力的科技投资领域,微软的量子计算进展引发了广泛关注。量子计算是一种利用量子力学原理进行计算的新型计算模式,有望解决传统计算机难以解决的复杂问题。然而,正如所有新兴技术一样,关键问题仍然是:潜在的投资回报是否能抵消其固有的风险?

微软在量子计算方面的进展不容忽视。从创造破纪录的逻辑量子比特到展示实际应用,该公司已确立了自己在该领域的领先地位。然而,商业化的道路充满挑战,包括技术障碍和激烈的竞争。

投资者必须仔细权衡潜在的回报与风险。虽然量子计算的长期前景令人期待,但短期内的挑战和市场不确定性同样不容忽视。微软的战略定位和技术实力是否足以克服这些障碍并充分利用量子计算的潜在收益?

深入探讨:

为了做出明智的投资决策,投资者应考虑以下因素:

技术进展: 量子计算技术的进展速度将显著影响商业化的时间表和潜在回报。尽管微软取得了重要进展,但该领域仍在快速发展。

竞争格局: 量子计算的竞争格局充满活力,其他科技巨头如谷歌、IBM 和亚马逊也在其中。微软能否保持竞争优势对于长期成功至关重要。

市场需求: 量子计算应用的潜在市场仍在形成。开发实际应用场景将是推动需求和证明投资合理性的关键。

监管环境: 政府政策和法规可能会影响量子计算技术的开发和商业化。投资者应注意任何可能的监管障碍。

经济因素: 宏观经济条件,如利率和市场波动,可能会影响投资决策。投资者应考虑更广泛的经济趋势如何影响量子计算市场。

结论:

投资微软的量子计算项目既充满机遇,也伴随风险。虽然长期潜力巨大,投资者仍需仔细评估上述因素,做出明智决策。随着该领域的不断发展,保持对最新动态和市场趋势的关注将至关重要。

为什么你应该拥有一个美股/ETF帐户?这个月,我到上海出差,公司位在新天地商业区,林立的办公大厦和购物商城让我领略到了上海的繁华,而办公室旁的”石库门”遗址保护区,则见证了1843年上海开埠后,先民的刻苦耐劳。

在上海,我还发现了一个现象,就是所有人几乎都拿着iPhone、工作用着Microsoft、付钱用的Alipay、运动穿着Adidas、假日去Disney玩、偶而还会和三五好友一同在家用Netflix追剧。

理由一:吃下跨国公司的一杯羹

有一个有趣的理论是:买股票无须花上大量时间对公司进行分析,只要观察社会中,大家都在用哪些产品,再买入对应的股票就好。

不只外企,众多两岸企业也远赴美国上市:$阿里巴巴(BABA)$、$京东(JD)$、蔚来、富士康等等,我们都熟悉的旅游企业$携程(CTRP)$,2004年赴美国纳斯达克交易所上市后,其股价由2003年的2美金增长到2017年的高峰60美金,股价涨幅高达30倍。

理由二:美国股票是全球最成熟、汰弱留强的市场

美国每年大约有120间公司IPO上市,因为严格的监管规定、或是私有化、并购等,美国每年也都有上百家的公司退市。我们来看看1980~2017年美国上市公司数量、以及美国股市总市值的变化表:

你可以发现,从1980~2017年,美国上市公司越来越少,但美股总市值却越来越高,为什么呢?

首先,我们要先搞清楚美国股票市场的三大特色:

第一,理性的参与者

美国股票市场的参与者80%为专业机构,20%为个人客户。尽管专业机构的投资报酬率不一定会高于个人客户,但我们却能断定专业机构在选股、买卖股票时会比个人投资者更加严谨;在投资系统、方法论上也会近似,能让市场保持在相对理性的状态。 (看看隔壁A股的走势图就懂我在说什么了...)

第二,政府、市场、投资者强监管

市场严格监管,美国证监会 (SEC)特别保障中小投资者的利益,上市、退市规定皆特别严格,上市公司时刻受到监管部门、媒体的检视。

第三,市场不断汰弱换强

由于违反监管、并购或是自愿退市,每年美国有超过百家的股票退市,同时也有百家的股票上市,让美股市场随时有"新血"输入,淘汰"坏血"公司,时刻保持在一个总体营利增长、公开透明的状态。

综合以上三点,所造成的结果就是,美国上市的企业越发强大,不断地汰弱换强,这也是美国股市牛长熊短的原因,更是我们透过美股帐户,参与企业获利的大好机会

作者:小賈

链接:https://xueqiu.com/1315690821/118032066

来源:雪球

著作权归作者所有。商业转载请联系作者获得授权,非商业转载请注明出处。