MTRA Pro+ ScreenerMTRA Pro+ Screener an analysis tool that provides traders with critical market structure information on up to 10 instruments simultaneously. This indicator consolidates momentum direction, trend analysis, range relationships, and volatility metrics into a single dashboard.

## Key Features

- Customizable display with adjustable positioning, colors, and sizing

**Momentum & Trend Tracking**

- Real-time momentum direction via 5-period SMA slope analysis

- Short-term trend direction using 10-period SMA slope analysis

- Color-coded visual representation for quick interpretation

**Range Relationship Analysis**

- Current bar analysis relative to previous period (Inside, Outside, 2Up, 2Dn)

- Three-period historical view of recent price action patterns

- Immediate identification of breakout and consolidation scenarios

**ATR-Based Volatility Analysis**

- Real-time ATR percentage calculations showing current range vs. average

- Visual distinction between normal (<100% ATR) and extended (>100% ATR) conditions

- Identification of potential exhaustion zones for risk management

**Intraday ATR Levels**

- Dynamic support/resistance levels based on current timeframe ATR

- Real-time upper and lower boundaries for precise entries/exits

- Customizable line styles integrated with price scale

## Practical Applications

- **Context Assessment**: Quickly gauge market conditions across multiple intraday timeframes

- **Exhaustion Detection**: Identify overextended moves when ATR exceeds 100%

- **Confluence Analysis**: Spot potential setups when timeframes align

- **Risk Management**: Some traders will use ATR levels for dynamic stops and position sizing

- **Breakout Confirmation**: Distinguish false breakouts from genuine momentum shifts

## Configuration Options

- Full dashboard positioning and color customization

- Individual timeframe toggles

- Adjustable ATR periods and sensitivity thresholds

- Multiple line styles for level visualization

真实波动幅度均值(ATR)

MTRA Intraday Pro+MTRA Pro Intraday is a multi-timeframe analysis tool that provides traders with critical market structure information across five intraday timeframes: 5m, 15m, 30m, 1h, and 4h. This indicator consolidates momentum direction, trend analysis, range relationships, and volatility metrics into a single dashboard.

***Dashboard Timeframes that are low than chart timeframes can be inaccurate - Because of this always focus attention on the details on higher timeframes for accurate data****

## Key Features

**Multi-Timeframe Analysis**

- Simultaneous analysis across 5m, 15m, 30m, 1h, and 4h timeframes

- Customizable display with adjustable positioning, colors, and sizing

**Momentum & Trend Tracking**

- Real-time momentum direction via 5-period SMA slope analysis

- Short-term trend direction using 10-period SMA slope analysis

- Color-coded visual representation for quick interpretation

**Range Relationship Analysis**

- Current bar analysis relative to previous period (Inside, Outside, 2Up, 2Dn)

- Three-period historical view of recent price action patterns

- Immediate identification of breakout and consolidation scenarios

**ATR-Based Volatility Analysis**

- Real-time ATR percentage calculations showing current range vs. average

- Visual distinction between normal (<100% ATR) and extended (>100% ATR) conditions

- Identification of potential exhaustion zones for risk management

**Intraday ATR Levels**

- Dynamic support/resistance levels based on current timeframe ATR

- Real-time upper and lower boundaries for precise entries/exits

- Customizable line styles integrated with price scale

## Practical Applications

- **Context Assessment**: Quickly gauge market conditions across multiple intraday timeframes

- **Exhaustion Detection**: Identify overextended moves when ATR exceeds 100%

- **Confluence Analysis**: Spot high-probability setups when timeframes align

- **Risk Management**: Use ATR levels for dynamic stops and position sizing

- **Breakout Confirmation**: Distinguish false breakouts from genuine momentum shifts

## Configuration Options

- Full dashboard positioning and color customization

- Individual timeframe toggles

- Adjustable ATR periods and sensitivity thresholds

- Multiple line styles for level visualization

## Who Benefits

- **Scalpers**: 5m/15m alignment for quick entries

- **Day Traders**: Multi-timeframe confluence for swing entries within the day

- **Intraday Swing Traders**: 1h/4h context for position holds

MTRA Pro Intraday transforms complex multi-timeframe analysis into clear, actionable market structure data without switching charts. This tool enhances decision-making by providing objective context across all relevant intraday timeframes in one view.

Pele CandlesPele Candles Indicator

Named after Pele, the Hawaiian goddess of volcanoes, this indicator identifies "explosive" candles with unusually large ranges that exceed a customizable ATR (Average True Range) threshold. These volcanic-like price movements often signal significant market activity where liquidity may have been swept from one side.

Pele candles appear as colored bars (blue for bullish, purple for bearish) when candle ranges surpass the ATR multiplier. While a single Pele candle doesn't guarantee direction, consecutive Pele candles in opposite directions can indicate potential trend reversals - much like volcanic eruptions that reshape the landscape.

The indicator helps traders spot moments of intense market activity and potential turning points, but should be used alongside other analysis tools for confirmation.

Features:

Customizable ATR period and multiplier

Visual highlighting of explosive price moves

Alert notifications for significant candles

No repainting - signals appear in real-time

******Make sure you go to visual order settings and bring to front******

Pua CandlesPua Candles Indicator

Named after "Pua," the Hawaiian word for flower, this indicator identifies small, delicate price movements that often precede significant market expansion. Like tiny flowers that can bloom into something magnificent, Pua candles represent seemingly insignificant moments that frequently mark exhaustion areas in the market.

Pua candles are both inside bars (contained within the previous bar's range) and small relative to the ATR threshold. These quiet, compressed price actions often signal consolidation before major moves. When price eventually expands beyond these delicate formations, it can lead to substantial directional movement.

The indicator highlights bullish Pua candles in teal and bearish ones in pink, making these critical junctures easy to spot. Pay special attention to follow-through action after Pua candles - they often mark the calm before the storm.

Features:

Identifies inside bars with small ATR-relative ranges

Customizable ATR period and smallness threshold

Visual highlighting with Hawaiian-inspired colors

Alert notifications for Pua formations and follow-through

No repainting - confirmed signals only

Perfect for spotting potential breakout setups and market turning points.

******Make sure you go to visual order settings and bring to front******

Trinity Trend Direction ProThe Trinity Trend Pro is a no-nonsense trend filter indicator built around the classic 13 / 48 / 200 EMA stack, but massively upgraded with real intelligence. Instead of just drawing three lines and spamming crossovers like every other EMA script, it only speaks when a genuine, high-reward trend is actually happening. It combines three strict conditions that must all be true at the same time: perfect bullish or bearish EMA alignment, steep slope on all three EMAs (measured in degrees), and wide enough separation between the fast and slow EMA (normalized by ATR). If any of those fail, it stays silent. This eliminates almost all the fakeouts and chop that destroy most traders using regular EMA crossovers.

What makes it truly different is the built-in “trend exhaustion” logic: when the EMAs compress and start braiding (common after a big move), the indicator automatically switches to a neutral “FLAT” state and clears the previous signal instead of stubbornly staying green or red. It also supports an optional higher-timeframe EMA filter (you choose the timeframe and length) so you never fight the bigger trend. One clean arrow appears only when a brand-new strong trend begins, and it stays off the chart until the next real move — no arrow spam.

The background colors the entire chart lightly green or red while the trend is alive, and a compact dashboard in the corner tells you in plain English whether to be long, short, or flat.

How to use it is dead simple: add it to any chart (SPX, BTC, ES, Nasdaq, stocks, anything), look at the dashboard or background color, and only trade when it says “LONG ACTIVE” or “SHORT ACTIVE”. Green arrow + green background = go long (calls, futures, shares). Red arrow + red background = go short (puts or short). Anything else = stay out. Set the two built-in alerts (“NEW BULL TREND” and “NEW BEAR TREND”) and you’ll get notified the exact moment a fresh high-probability move starts. That’s literally all you need to do. No second-guessing, no overthinking, no getting chopped up in sideways markets. In our humble opinion it is one of the cleanest, smartest, most disciplined EMA-based tool on TradingView — designed for traders who are tired of noise and only want the real moves.

Trinity Trend Direction ProThe Trinity Trend Pro is a no-nonsense trend filter indicator built around the classic 13 / 48 / 200 EMA stack, but massively upgraded with real intelligence. Instead of just drawing three lines and spamming crossovers like every other EMA script, it only speaks when a genuine, high-reward trend is actually happening. It combines three strict conditions that must all be true at the same time: perfect bullish or bearish EMA alignment, steep slope on all three EMAs (measured in degrees), and wide enough separation between the fast and slow EMA (normalized by ATR). If any of those fail, it stays silent. This eliminates almost all the fakeouts and chop that destroy most traders using regular EMA crossovers.

What makes it truly different is the built-in “trend exhaustion” logic: when the EMAs compress and start braiding (common after a big move), the indicator automatically switches to a neutral “FLAT” state and clears the previous signal instead of stubbornly staying green or red. It also supports an optional higher-timeframe EMA filter (you choose the timeframe and length) so you never fight the bigger trend. One clean arrow appears only when a brand-new strong trend begins, and it stays off the chart until the next real move — no arrow spam.

The background colors the entire chart lightly green or red while the trend is alive, and a compact dashboard in the corner tells you in plain English whether to be long, short, or flat.

How to use it is dead simple: add it to any chart (SPX, BTC, ES, Nasdaq, stocks, anything), look at the dashboard or background color, and only trade when it says “LONG ACTIVE” or “SHORT ACTIVE”. Green arrow + green background = go long (calls, futures, shares). Red arrow + red background = go short (puts or short). Anything else = stay out. Set the two built-in alerts (“NEW BULL TREND” and “NEW BEAR TREND”) and you’ll get notified the exact moment a fresh high-probability move starts. That’s literally all you need to do. No second-guessing, no overthinking, no getting chopped up in sideways markets. In our humble opinion it is one of the cleanest, smartest, most disciplined EMA-based tool on TradingView — designed for traders who are tired of noise and only want the real moves.

MTRA Pro+Momentum - Trend - Range - ATR Dashboard!

MTRA Pro+ is a comprehensive multi-timeframe analysis tool designed to provide traders with critical market structure information across six different timeframes. This indicator consolidates momentum direction, trend analysis, range relationships, and volatility metrics into a single, customizable dashboard.

Core Features:

Multi-Timeframe Dashboard

Simultaneous analysis across Daily, 24H, Weekly, Monthly, Quarterly, and Yearly timeframes

Customizable display options to focus on relevant timeframes for your trading style

Professional dashboard with adjustable positioning, colors, and sizing

Momentum & Trend Analysis

Real-time momentum direction based on 5-period SMA slope analysis

Short-term trend direction using 10-period SMA slope analysis

Configurable sensitivity settings to filter out market noise

Color-coded visual representation for quick interpretation

Range Relationship Analysis

Current bar analysis relative to previous period (Inside, Outside, 2Up, 2Dn)

Three-period historical view showing recent price action patterns

Immediate identification of breakout and consolidation scenarios

Context for potential continuation or reversal setups

ATR-Based Volatility Analysis

Real-time ATR percentage calculations showing current range relative to average

Visual distinction between normal (<100% ATR) and extended (>100% ATR) conditions

Identification of potential exhaustion zones when price extends beyond typical volatility

Context for position sizing and risk management decisions

Daily ATR Level Visualization

Dynamic support and resistance levels based on current daily ATR

Real-time upper and lower boundaries for intraday trading

Customizable line styles and positioning options

Price scale integration for easy reference

Comprehensive Alert System

Momentum direction changes across all timeframes

Trend direction changes for longer-term position management

Range relationship status changes for breakout/breakdown alerts

ATR percentage threshold crossings for volatility-based signals

Practical Applications:

Market Context Assessment Quickly assess whether the market is trending, consolidating, or experiencing unusual volatility across multiple timeframes. This context helps inform position sizing, entry timing, and exit strategies.

Exhaustion Detection When ATR percentages exceed 100%, price may be overextended relative to typical volatility, potentially signaling pullback opportunities or areas to reduce position size.

Confluence Analysis Identify high-probability setups when multiple timeframes align in momentum and trend direction, or spot potential reversal zones when shorter timeframes diverge from longer-term trends.

Risk Management Enhancement Use ATR-based levels for dynamic stop placement and the dashboard's range analysis to understand current market structure before entering positions.

Breakout Confirmation Range relationship analysis helps distinguish between false breakouts and genuine momentum shifts by providing context about recent price action patterns.

Configuration Options:

Visual Customization

Full dashboard positioning control (9 positions available)

Customizable colors for all elements

Adjustable text size and border styling

Toggle individual timeframes on/off

Technical Parameters

Adjustable ATR periods for each timeframe

Configurable momentum sensitivity thresholds

ATR level display options with margin controls

Multiple line style choices for level visualization

Who Benefits from MTRA Pro+:

Swing Traders: Multi-timeframe trend and momentum alignment for position entries

Day Traders: Real-time ATR levels and range analysis for intraday decision-making

Position Traders: Longer timeframe context for strategic position management

Risk Managers: Volatility-based metrics for dynamic position sizing

Important Notes:

This indicator provides market structure analysis and context - it does not generate specific buy/sell signals. Success depends on combining this information with your trading methodology, proper risk management, and market experience. The tool is designed to enhance decision-making by providing objective market structure data across multiple timeframes.

MTRA Pro+ transforms complex multi-timeframe analysis into an accessible, visual format that helps traders stay informed about market conditions without the need to manually switch between charts and timeframes.

Tripwire Pro+Tripwire – Trail-Based Trend Direction Indicator

OVERVIEW

Tripwire is a powerful, volatility-adaptive trailing indicator designed to keep traders on the right side of momentum while offering signals and alerts based on the users settings and filters.

CONCEPT & INSPIRATION

This indicator is directly inspired from the Zombie9Trail by Frosty (creator of the Zombie Pack and TickHunter for NinjaTrader).

When all filters are turned off, Tripwire replicates the core behavior of Zombie9Trail — delivering the same razor-sharp trailing logic.

Most of Frosty's testing has been done from the 1 minute time frame, while I have personally found for my style of trading the 5 minute time frame works better for me.

WHAT THIS VERSION ADDS — TradingView Enhancements

• Optional multi-layer trend filters (21, 34, 170 EMA) to separate high-probability pullbacks from actual trend changes

• Clean Buy/Sell/Pullback signal labels with alert conditions

• Real-time dashboard showing current trail value, trend state, and filter status

• Fully customizable ATR length, multiplier, source, and visual styling

• All values exported as plots — perfect for CSV download and strategy development

HOW TO USE

Filters ON (recommended for trend-following) → Take signals in the direction of the higher-timeframe trend. Great for staying in strong moves and avoiding fake outs.

Filters OFF (pure Zombie9Trail mode) → Possibly catch early reversals and ride new trends

CREDIT & RESPECT

Core trailing methodology and original genius: Frosty — creator of Zombie9Trail / Zombie Pack / TickHunter (NinjaTrader).

This TradingView adaptation was built in direct homage to his NinjaTrader work and with his encouragement. Everything beyond the base trailing logic (filters, dashboard, alerts, exportable plots, visual polish) is original.

DISCLAIMER

For educational and informational purposes only. Not financial advice. Past performance is no guarantee of future results. Test thoroughly.

US100 AlgoUS100 Algo - Professional Supertrend Strategy with Multi-Filter System

🚀 Professional Algorithmic Trading for US100 (NASDAQ-100)

Battle-tested strategy optimized for 15-minute Heikin Ashi charts with full Tickerly webhook automation.

⚠️ CRITICAL SETUP - READ FIRST

Before using this strategy:

Chart Type: Heikin Ashi (for smooth visuals)

Strategy Settings: Go to Strategy Properties → Set OHLC prices (NOT Heikin Ashi prices)

Timeframe: 15 minutes

Instrument: US100 / NASDAQ-100

This OHLC setting is CRITICAL for accurate signals and live trading. Without it, your backtest and live results will not match!

⚡ Core Strategy

Supertrend Engine - ATR Period 42, Factor 3.0

Heikin Ashi Charts - Filters noise, shows clean trends

Both Directions - LONG and SHORT trades

Multi-Filter System - 5 layers of confirmation

🔧 Smart Filter System

✅ ADX Filter - Only trades strong trends (threshold: 24)

✅ MACD Filter - Confirms momentum direction

✅ Volatility Filter - Requires minimum ATR movement (0.9x)

✅ Volume Filter - Validates with above-average volume (0.7x)

✅ EMA 200 Filter - Optional trend alignment (3 modes available)

All filters can be toggled ON/OFF individually

💰 Risk Management

Take Profit System - Configurable (default: 8.8%)

Visual Labels - Clear LONG/SHORT entry markers

Exit Signals - TP markers on chart

⚠️ Note: TP signals always display on chart for analysis. When TP is disabled in settings, signals show but won't trigger automated exits.

📊 Visual Features

Professional dashboard (movable to 4 corners)

LONG/SHORT entry labels (adjustable size)

Take Profit exit markers

US trading session highlights (optional)

🔔 Tickerly Compatible - Fully Automated

✅ Tested and verified for live trading

✅ Works with Capital.com, OANDA, and other brokers

✅ Instant webhook signal transmission

✅ Zero configuration needed

📈 Quick Optimization Guide

Step 1: Install & Setup

Apply to US100, 15min chart

Enable Heikin Ashi candles

Set strategy to use OHLC prices (in Strategy Properties)

Step 2: Test with Default Settings

Run backtest with all filters enabled

Check profit factor and drawdown

Verify signal quality

Step 3: Fine-Tune Filters

More trades: Lower ADX to 20, disable EMA filter

Higher accuracy: Raise ADX to 28, increase volatility to 1.1

Balanced: Keep defaults (recommended)

Step 4: Optimize Supertrend

Test ATR Period: 35-50 (default 42 works well)

Test Factor: 2.5-3.5 (default 3.0 optimal)

Step 5: Take Profit Testing

Test TP disabled (Supertrend exits only)

Test TP 5%-15% range (default 8.8%)

Compare profit factor vs max drawdown

Step 6: Live Deploy

Paper trade minimum 2 weeks

Verify Tickerly webhook signals

Monitor and adjust as needed

⚙️ Preset Configurations

Conservative (Fewer, high-quality trades)

ADX: 28 | Volatility: 1.1 | Volume: 0.9 | All filters ON

Balanced (Recommended)

ADX: 24 | Volatility: 0.9 | Volume: 0.7 | All filters ON

Aggressive (More trades)

ADX: 20 | Volatility: 0.7 | Volume: 0.5 | EMA filter OFF

✅ What You Get

Complete Pine Script v6 code

Full filter customization

Professional dashboard

Tickerly automation ready

All documentation included

Works on multiple instruments

📈 Best Performance

Strategy performs optimally during:

Active US trading hours

Trending market conditions

With proper filter calibration

On volatile instruments (US100, crypto)

⚠️ Disclaimer

Past performance does not guarantee future results. Always test in demo before live trading. Use proper risk management. Trading involves risk of loss.

Start Trading Smarter Today 🎯

WeeklyDealingRange Pro+ (Fib Edition)Weekly Dealing Range Indicator

Overview

The Weekly Dealing Range indicator identifies range + volatility based pivot levels that form at the close of the first trading session and extend for the entire week. This tool provides key reference points for both trending and range-bound market conditions.

What It Provides

Range High & Low: Weekly session extremes

Median Level: Mid-point of the weekly range

Weekly Open: First session opening price

Fibonacci Extensions: Calculated levels above the high and below the low

Practical Application

These levels serve as:

Reversal zones for mean reversion setups

Support/resistance reference points

Target levels for existing positions

Framework for building trade ideas around high-probability pivot areas

Key Features

Optional function based alerts

Traditional price crosses level alerts

Automatically updates each week

Clean, uncluttered chart display

Works across all timeframes

Suitable for all markets and instruments

BTCUSD Algo🎯 Overview

Advanced algorithmic trading strategy specifically designed for BTCUSD 15-minute Heikin Ashi charts. This algorithm combines the powerful Supertrend indicator with multiple technical filters to identify high-probability entries in the Bitcoin market.

⚠️ CRITICAL SETUP REQUIREMENTS

MUST READ BEFORE USE:

✅ Chart Type: 15-minute Heikin Ashi candles ONLY

✅ Symbol: BTCUSD

✅ Strategy Properties: Enable "Use OHLC Values" to prevent repainting and ensure realistic backtest results

✅ Broker Integration: Tickerly-proven with Capital.com API for automated trading

✅ This Code is for Free, so i would appreciate Comment on this what you think.

🚀 Key Features

📊 Interactive Dashboard

Real-time position tracking (LONG/SHORT/FLAT)

Live P&L display with percentage gains

Entry price monitoring

Take Profit level visualization

Technical indicators overview (Trend, ADX, MACD, ATR, Volume, EMA200)

Fully customizable position (4 corner options)

🏷️ Visual Signal Labels

Clear LONG/SHORT entry markers

TP EXIT labels with profit percentage

Adjustable label sizes (Tiny to Huge)

Optional display toggle

⚡ Core Supertrend Engine

ATR Length: Adjustable period for volatility calculation

Factor: Fine-tunable multiplier for signal sensitivity

Optimized default values for maximum profit factor

🔧 Advanced Filter System (All Optional)

ADX Filter: Trend strength confirmation

MACD Filter: Momentum alignment

Volatility Filter: Minimum ATR requirements

Volume Filter: Above-average volume confirmation

EMA 200 Filter: Directional bias with 3 modes:

Long only above EMA

Short only below EMA

Both directions (filter disabled)

💰 Take Profit System

Percentage-based exits

Adjustable TP levels

Visual TP line on dashboard

Note: Currently in development - shows in strategy but signals not yet active

🌍 US Session Highlighting

Visual background colors for:

US Open (09:30-11:30 ET)

Lunch Session (11:30-13:30 ET)

Afternoon Session (13:30-16:00 ET)

🎓 Optimization Guide - Avoiding Overfitting

IMPORTANT: Follow this sequence to prevent curve-fitting:

Step 1: Disable ALL Filters

Start with pure Supertrend signals - uncheck all filter options

Step 2: Optimize ATR Length

This parameter controls how many candles are used for volatility calculation

Higher values = More candles = Smoother signals = Fewer trades

Lower values = Fewer candles = Faster signals = More trades (overfitting risk!)

Adjust until you find the best Profit Factor

Default optimized value included

Step 3: Optimize Factor

Fine-tune the Supertrend multiplier

Work in small increments (0.1 - 0.5)

Balance between signal frequency and accuracy

Step 4: (Optional) Add Filters

Only after core optimization

Add filters one at a time

Test each addition's impact

Less is more!

💡 "Less is More" Philosophy

This strategy follows the principle of simplicity. The default parameters are optimized for maximum profit, but the power lies in finding the sweet spot for YOUR trading style and market conditions.

✅ Automated Trading Ready

Fully compatible with Tickerly webhook integration

Tested with Capital.com API

Real-time signal generation

No repainting when properly configured

📋 What You Get

Complete Pine Script v6 code

Professional dashboard interface

Multiple customization options

Clear visual signals

Session analysis tools

Optimization framework

⚙️ Technical Specifications

Version: Pine Script v6

Type: Strategy (with overlay)

Default Quantity: Fixed (adjustable)

Indicators Used: Supertrend, ADX, MACD, ATR, EMA, Volume MA

🎨 Customization Options

Dashboard visibility toggle

Dashboard position (4 corners)

Signal labels on/off

Label size adjustment

EMA line display

All filters with checkboxes

Color schemes for sessions

TP percentage adjustment

⚡ Ready to deploy? Remember:

Set to Heikin Ashi 15m

Enable "Use OHLC Values" in properties

Start with all filters OFF

Optimize ATR Length first

Trade smart, not hard! 🚀

Disclaimer: Past performance does not guarantee future results. Always test thoroughly before live trading. Currently under active development - Take Profit automation pending completion.

Session Ranges Pro+Session Range Zones – Professional Edition

OVERVIEW

Professional visualization of the classic opening-range / Initial Balance concept across Asian, London, and Regular (US) sessions.

Displays the high/low of the user-defined opening window as thick, hierarchical filled zones with optional Fibonacci and standard-deviation extensions plus full alerting.

CONCEPT BACKGROUND

Using the high and low of the first 30–60 minutes of a session as key support/resistance is public-domain knowledge that has been standard in institutional trading for decades (Initial Balance, Opening Range, Session Range, etc.).

On TradingView the same principle was popularized under the name “Defining / DealingRange / DR/IDR” by TheMas7er and others.

IMPLEMENTATION & VALUE ADDED

This indicator follows the established, public-domain range-calculation methodology but has been completely rewritten with the following original enhancements:

• Clean, filled High / Mid / Low zones for instant visual hierarchy

• Intuitive Asian / London / Regular session labelling and fully custom timing

• Comprehensive dynamic & static Fibonacci and 50%/100% standard-deviation extensions

• Alert conditions on every zone, midline, opening level, and extension line

• Modern, modular code architecture using arrays and custom drawing functions

• No repainting, lightweight performance on any intraday timeframe

HOW TO USE

Apply to 1–15 min charts. Select desired sessions and formation period (30 or 60 min typical).

Shaded zones serve as primary support/resistance; extensions provide measured-move targets.

CREDIT & TRANSPARENCY

Core methodology: public domain (Initial Balance / Opening Range / Session Range).

Early TradingView popularization of the DR/IDR naming and feature set: TheMas7er **(with thanks to community contributors like bmsitiaan and trading-guide for refinements)**.

**Utilizes PineCoders' VisibleChart library for optimized chart rendering.**

This script uses the same foundational principle and logical input options but is an independent implementation. All visual presentation, zone system, multi-session handling, extension systems, alerting framework, and underlying code structure are original.

DISCLAIMER

For educational and informational purposes only. Not financial advice. Past performance is no guarantee of future results. Test thoroughly on your instruments and timeframes.

PonoTrading WDRWeekly Dealing Range Indicator

Overview

The Weekly Dealing Range indicator identifies range + volatility based pivot levels that form at the close of the first trading session and extend for the entire week. This tool provides key reference points for both trending and range-bound market conditions.

What It Provides

Range High & Low: Weekly session extremes

Median Level: Mid-point of the weekly range

Weekly Open: First session opening price

Standard Deviation Extensions: Calculated levels above the high and below the low

Practical Application

These levels serve as:

Reversal zones for mean reversion setups

Support/resistance reference points

Target levels for existing positions

Framework for building trade ideas around high-probability pivot areas

Key Features

Traditional price crosses level alerts

Automatically updates each week

Clean, uncluttered chart display

Works across all timeframes

Suitable for all markets and instruments

NeuraEdge ORB Professional Opening Range Breakout Indicator-15m🚀 NeuraEdge ORB - Professional Opening Range Breakout Indicator

We're excited to release this clean, effective Opening Range Breakout (ORB) indicator for the trading community. The 15-minute ORB is one of the most time-tested intraday strategies, and we've built this tool to make it simple and actionable.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📖 WHAT IS THE 15-MINUTE ORB STRATEGY?

The Opening Range Breakout strategy captures the initial price range established in the first 15 minutes of market open (9:30-9:45 AM ET). This range often sets the tone for the trading day, as institutional order flow and overnight gap reactions play out during this window.

The concept is simple:

- Mark the HIGH and LOW of the first 15 minutes

- Trade the breakout when price breaks above or below this range

- Use the opposite side of the range as your stop loss

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚙️ HOW TO USE THIS INDICATOR

1️⃣ SETUP

• Apply to SPY, QQQ, IWM, or any liquid stock/ETF

• Recommended timeframes: 1-minute or 5-minute charts

• The indicator automatically detects the 9:30-9:45 AM ET session

2️⃣ WAIT FOR THE RANGE

• A blue box will form showing the Opening Range

• Wait for the 15-minute period to complete (marked "✅ COMPLETE" in dashboard)

• Note the range size - larger ranges often mean stronger moves

3️⃣ TRADE THE BREAKOUT

• 🟢 LONG: When price closes above the Opening Range High

• 🔴 SHORT: When price closes below the Opening Range Low

• Signals appear automatically with entry, stop loss (SL), and take profit (TP) levels

4️⃣ MANAGE YOUR TRADE

• Stop Loss: Placed at opposite side of range (default) or midpoint

• Take Profit: Based on your selected Risk:Reward ratio

• The indicator tracks win rate automatically

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🎯 ENTRY TYPES

BREAKOUT MODE (Default)

- Enters immediately when price breaks the range

- More signals, catches the initial move

- Best for: Trending days, high momentum

RETEST MODE

- Waits for price to break out, then pull back to the range

- Fewer signals, better entry price

- Best for: Choppy days, tighter stops

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📊 SETTINGS EXPLAINED

Display Settings:

- Show Signals - Toggle buy/sell signals

- Show Opening Range Box - Visual box around the 15-min range

- Show Dashboard - Information panel with status and stats

Opening Range Settings:

- Opening Range Minutes - Default 15, adjustable 5-60

- Stop Trading After - Prevents late-day trades (default 3PM ET)

Entry Settings:

- Entry Type - Breakout or Retest

- Require Volume Confirmation - Only signals on above-average volume

- Require FVG Confluence - Adds Fair Value Gap filter for extra confirmation

Risk Management:

- Stop Loss Placement - Opposite Side / Midpoint / ATR Based

- Risk:Reward Ratio - Set your target (1.5 recommended)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💡 TIPS FOR BEST RESULTS

✅ DO:

- Trade liquid instruments (SPY, QQQ, major stocks)

- Use 1-5 minute charts for better entry precision

- Respect the stop loss - the range defines your risk

- Pay attention to range size (0.5-1.5x ATR is ideal)

- Be patient - only 1-2 setups per day

❌ AVOID:

- Trading both directions on the same day

- Taking trades after 2-3 PM ET

- Very small ranges (likely to get chopped out)

- Low volume breakouts (often fail)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📈 DASHBOARD INFORMATION

The dashboard shows:

- OR Status - Forming / Complete / Waiting

- OR High/Low - The range levels

- Range Size - In points and ATR multiples

- Breakout Direction - Long / Short / None

- Volume Status - High or Normal

- Win Rate - Tracked automatically

- W/L Record - Wins and losses count

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🔔 ALERTS INCLUDED

- Opening Range Complete - Notifies when the 15-min range is set

- ORB Long Signal - Buy signal triggered

- ORB Short Signal - Sell signal triggered

- Breakout Up/Down - Range broken (even without signal)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚠️ DISCLAIMER

This indicator is for educational and informational purposes only. Past performance does not guarantee future results. Always use proper risk management and never risk more than you can afford to lose. This is not financial advice.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

We hope you find this indicator valuable in your trading journey!

💬 Questions or feedback? Leave a comment below.

🌐 Check out our full Indicator Suite: www.neura-edge.com

📧 Support: support@neura-edge.com

Happy Trading!

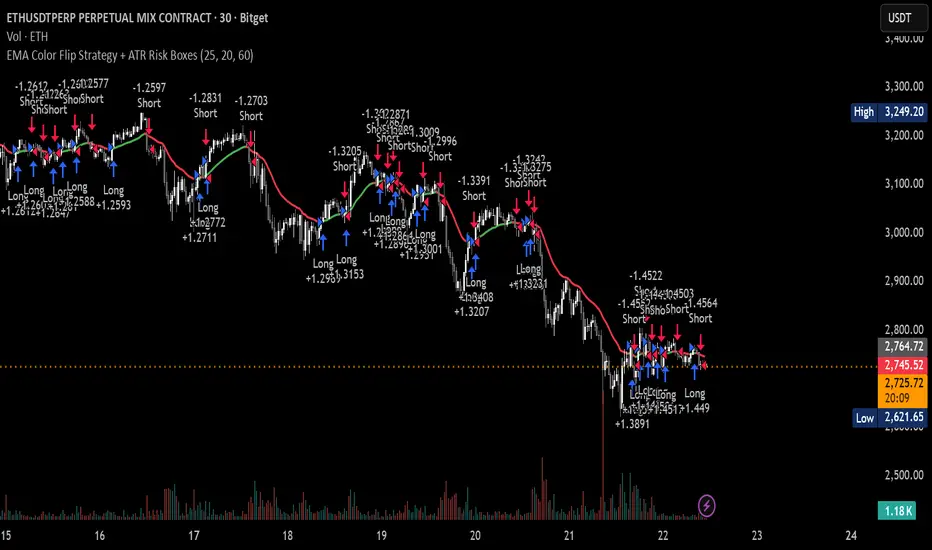

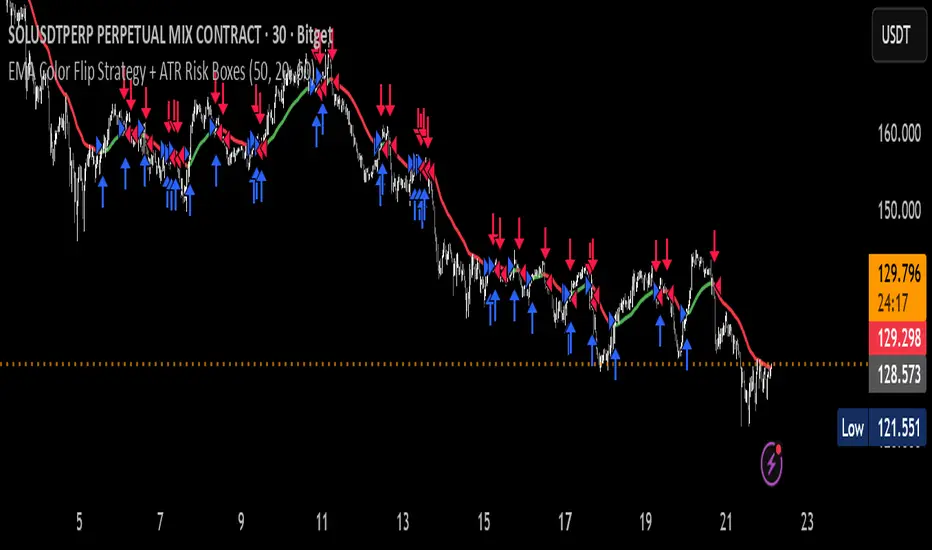

EMA Color Flip Strategy Experimenting on SOL 30 min chart, it seems good!

Let me know what you think!

WeeklyDealingRange Pro+Weekly Dealing Range Indicator

Overview

The Weekly Dealing Range indicator identifies range + volatility based pivot levels that form at the close of the first trading session and extend for the entire week. This tool provides key reference points for both trending and range-bound market conditions.

What It Provides

Range High & Low: Weekly session extremes

Median Level: Mid-point of the weekly range

Weekly Open: First session opening price

Standard Deviation Extensions: Calculated levels above the high and below the low

Practical Application

These levels serve as:

Reversal zones for mean reversion setups

Support/resistance reference points

Target levels for existing positions

Framework for building trade ideas around high-probability pivot areas

Key Features

Optional function based alerts

Traditional price crosses level alerts

Automatically updates each week

Clean, uncluttered chart display

Works across all timeframes

Suitable for all markets and instruments

ATR Volatility AlertsOverview:

This is a dynamic alert tool based on the Average True Range (ATR), designed to help traders detect sudden price movements that exceed normal volatility levels. Whether you are trading breakouts or monitoring for abnormal spikes, this indicator visualizes these events on the chart and triggers system alerts when the price move exceeds your specified ATR multiplier.

Key Features:

Fully Customizable ATR Range:

You can adjust the ATR Length (Default: 14) and the Multiplier (Default: 1.5x).

Tip: Increase the multiplier (e.g., to 2.0 or 3.0) to catch only extreme volatility, or lower it for scalping smaller moves.

Visual Chart Signals:

Visual markers appear instantly when a bar's movement exceeds the ATR threshold.

Green Triangle: Indicates an Upward Spike.

Red Triangle: Indicates a Downward Spike.

Flexible System Alerts:

Designed to integrate seamlessly with TradingView's alert system. You can choose from three specific alert directions based on your strategy:

1.Price Spike Up: Triggers only on sharp upward moves.

2.Price Spike Down: Triggers only on sharp downward moves.

3.Bidirectional Volatility Alert: Triggers on BOTH huge pumps and dumps.

How to Set Alerts:

Click the "Create Alert" button in TradingView.

Select ATR Volatility Alerts in the "Condition" dropdown.

Choose the specific logic you need:

· Select Price Spike Up for bullish monitoring.

· Select Price Spike Down for bearish monitoring.

· Select Bidirectional Volatility Alert to watch for any volatility expansion.

Two Supertrend Crossover SignalThis indicator is designed to visualize trend shifts using two Supertrend lines and a crossover-based signal system.

It also colors the area between the two Supertrend lines based on the current trend direction, making trend changes easy to identify at a glance.

How It Works

The indicator plots:

Fast Supertrend (shorter ATR length, lower factor)

Slow Supertrend (longer ATR length, higher factor)

A crossover between these two Supertrend lines indicates a possible trend shift.

Buy Signal

A BUY signal occurs when: Fast Supertrend crosses ABOVE Slow Supertrend

This suggests bullish momentum strengthening.

Sell Signal

A SELL signal occurs when: Fast Supertrend crosses BELOW Slow Supertrend

This suggests bearish momentum increasing.

Buy/Sell Signal Labels

The chart displays clear BUY (green) and SELL (red) labels at every crossover.

These signals help traders quickly pinpoint potential entries or exits.

This indicator is ideal for:

✓ Trend trading

✓ Swing trading

✓ Identifying momentum shifts

✓ Visual confirmation of market direction

✓ Combining with price action or EMA filters

You may adjust ATR length and multiplier depending on the timeframe:

For Scalping (1–5 min):

Fast ATR: 5–7

Slow ATR: 10–14

For Intraday (5–15 min):

Fast ATR: 7

Slow ATR: 10–14

For Swing Trading (1h–4h):

Fast ATR: 10

Slow ATR: 20

Important Notes

This indicator does not repaint the Supertrend values.

Signals are based on confirmed crossovers.

Use stop-loss and risk management appropriate for your strategy.

Always combine with market context (support/resistance, volume, etc.)

Scalper Pro Pattern Recognition & Price Action📘 Scalper Pro Pattern Recognition & Price Action

Overview

Scalper Pro is a dynamic multi-layer trend recognition and price action strategy that integrates Supertrend, Smart Money Concepts (SMC), and volatility-based risk control.

It adapts to market volatility in real time to enhance entry precision and optimize risk.

⚠️ This script is for educational and research purposes only.

Past performance does not guarantee future results.

🎯 Strategy Objectives

Detect structural market shifts (BOS / CHoCH) automatically.

Identify Order Blocks (OB), Fair Value Gaps (FVG), and key liquidity zones.

Plot dynamic Take-Profit (TP) and Stop-Loss (SL) levels based on ATR.

Avoid low-volatility (sideways) conditions using ADX filtering.

Combine trend-following signals with structural confirmation.

✨ Key Features

Supertrend Entry Signals — Generates precise buy/sell markers based on price crossovers with the Supertrend line.

Order Block Detection — Automatically plots both Internal and Swing Order Blocks for smart money insights.

Fair Value Gap Visualization — Highlights inefficiency zones in bullish or bearish structures.

Market Structure Labels — Marks Break of Structure (BOS) and Change of Character (CHoCH) points for clear trend shifts.

Dynamic Risk Levels — Automatically generates TP/SL lines and price labels using ATR-based distance.

📊 Trading Rules

Long Entry:

• Price crosses above the Supertrend (ta.crossover(close, supertrend))

• ADX above sideways threshold (trend condition confirmed)

• Optional confirmation from a bullish BOS or CHoCH

Short Entry:

• Price crosses below the Supertrend (ta.crossunder(close, supertrend))

• ADX above threshold

• Optional confirmation from a bearish BOS or CHoCH

Exit (or Reverse):

• Opposite Supertrend crossover

• Price hits TP/SL lines

• Trend shift confirmed by internal BOS/CHoCH

💰 Risk Management Parameters

Stop Loss & Take Profit based on ATR × risk multiplier

ATR Length: 14 (default)

Risk %: 3% per trade

Sideways Filter: ADX < 15 → no trade zone

TP1–TP3 = Entry ± (ATR × 1~3)

⚙️ Indicator Settings

Supertrend Module:

ATR Length: 10

Factor: nsensitivity × 7

ADX Module:

ADX Length: 15

Sideways Threshold: 15

EMA Set:

EMA (5, 9, 13, 34, 50) × Volatility Factor (3)

SMA Filter:

SMA(8) & SMA(9) for short-term trend confirmation

Smart Money Concepts Module:

Displays BOS/CHoCH, Order Blocks, FVGs, Equal Highs/Lows, and Premium/Discount zones

🔧 Improvements & Uniqueness

Integrates Supertrend momentum with Smart Money Concepts (SMC) structural analysis.

Dual detection layers: Internal (micro) and Swing (macro) structures.

ATR-driven auto labeling for entry, stop, and profit targets.

Premium/Discount and Equilibrium zones visualized on the chart.

Built-in ADX filter to skip low-trend market conditions.

✅ Summary

Scalper Pro Pattern Recognition & Price Action merges classical trend-following with modern market structure analytics.

It combines momentum detection, volatility control, and smart money mapping into one cohesive framework.

Unified trend, structure, and risk visualization.

Auto-marked BOS/CHoCH, OB, FVG, and liquidity zones.

Usable for scalping, intraday, or swing trading setups.

⚠️ This strategy is based on historical data and designed for educational use only.

Always apply sound risk management and forward testing before live trading.

ICT Sigma Hybrid FVGThis indicator combines three analytical components—statistical volatility modeling, ICT imbalance logic, and higher-timeframe bias filtering—to help traders interpret displacement-driven price inefficiencies. The goal is to reduce noise and highlight only meaningful FVGs that occur with sufficient volatility and directional context.

Sigma Volatility Zones

The script calculates statistically normalized deviation levels using a multi-regime standard deviation blended with ATR.

This produces adaptive volatility zones that:

Expand during trending or high-volatility periods

Contract during consolidation

Highlight extremes more accurately than fixed standard deviations

These zones help users identify where price is operating in premium/discount relative to recent volatility.

Fair Value Gaps With Displacement Scoring

Every potential FVG is evaluated using a displacement score based on candle body expansion, wick displacement, and relative move efficiency. FVGs that do not exceed the minimum score are filtered out. This ensures the script only displays gaps associated with meaningful movement, not minor pricing noise.

Optional Higher-Timeframe Bias Filter

The HTF bias engine evaluates structure using selected higher-timeframe EMAs.

When enabled, the indicator:

Shows bullish FVGs only in bullish higher-timeframe conditions

Shows bearish FVGs only in bearish conditions

Hides counter-trend FVGs that may have lower reliability

Users may disable this to see all qualifying gaps regardless of bias.

ATR-Adaptive Volatility Conditioning

ATR is blended into the model so the displacement score and sigma zones adjust automatically to sudden volatility changes such as:

Major economic releases

Earnings

High-impact market events

Overnight volatility shifts

This helps maintain consistent FVG quality during rapidly changing conditions.

How to Use the Indicator:

Use sigma levels to understand whether price is extended or discounted relative to recent volatility.

Monitor FVGs that appear within or near sigma extremes to identify potential exhaustion or continuation zones.

Combine HTF bias with LTF displacement gaps to align intraday entries with broader directional flow.

ATR-adjusted scoring helps distinguish between meaningful inefficiencies and low-quality gaps.

Example 1 — Intraday Sigma Expansion & Displacement FVG Reaction

Figure 1. Price collapses from a 4.5σ extreme during a volatility expansion event.

Only high-impact FVGs are shown due to the displacement filter, removing low-quality gaps.

Sigma bands expand dynamically as volatility increases, illustrating how the model adapts automatically.

Example 2 — Higher-Timeframe Sigma Compression After a Major Trend Leg

Figure 2. After a large macro move, sigma levels compress tightly, forming a volatility cluster.

These HTF sigma zones later act as reaction levels during continuation.

This demonstrates why the model blends HTF sigma structure with LTF displacement gaps for alignment.

Recommended Settings

Standard deviation lookback: 100

ATR length: 50

ATR blend weight: 0.5

Minimum Z-score: 1.8

Sigma levels: 1.5 / 3 / 4.5

HTF bias: Daily (optional)

FVG displacement filter: On

The Bear & Bull TieWhat it does:

Bear & Bull Tie is a moving average crossover indicator that identifies trend reversals and generates entry/exit signals based on the relationship between price and three simple moving averages (SMA 21, SMA 55, SMA 89). The indicator combines these three MAs into an Average Moving Average (AMA) to confirm directional bias, then uses ATR (Average True Range) volatility measurement for dynamic position sizing and stop-loss placement.

How it works:

The indicator operates on a simple but effective principle: it enters a bullish trend when price closes above all three moving averages simultaneously, and enters a bearish trend when price closes below all three MAs simultaneously. This "three MA alignment" approach filters out noise and confirms genuine trend changes. The indicator then plots:

Entry levels at the highest MA during uptrends or lowest MA during downtrends

Stop-loss zones calculated using 2x ATR distance from entry prices

Trend confirmation fill between price and the Average Moving Average, color-coded blue for bullish and red for bearish

The ATR-based stop-loss sizing adapts to market volatility, making it suitable for different market conditions and timeframes.

How to use it:

Monitor the filled zones to visually confirm your trend bias

Watch for alerts when new long or short setups form; entry prices and ATR-based stops are displayed on the chart

Trade the zones between your entry level and stop-loss zone, adjusting position size based on your risk tolerance

Exit when colors reverse to indicate trend termination

The indicator works best on higher timeframes (1H and above) where trend clarity is stronger and false signals are reduced.

Alerts: FOR AUTOMATION / NOTIFICATION's (create an alert for B/B tie (2, 4) that uses Any Alert / Function Call )

Long Positions:

entries ---> "Bull Tie on NVDA | Entry : 100.5 | ATR Stop : 99.5"

exits ------> "Bull Tie on NVDA | Exit : 110.1"

Short Positions:

entries ---> "Bear Tie on NVDA | Entry : 120.05 | ATR Stop : 85.05"

exits -----> "Bear Tie on NVDA | Exit : 100"

Credits:

This script incorporates concepts and code portions from @LOKEN94 with his explicit permission. Special thanks for the foundational logic that inspired this development.

Disclaimer:

This indicator is for educational and analytical purposes. It is not financial advice. Past performance does not guarantee future results. Always manage risk properly and use stops. Test thoroughly on historical data before live trading.