DeeptestDeeptest: Quantitative Backtesting Library for Pine Script

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ OVERVIEW

Deeptest is a Pine Script library that provides quantitative analysis tools for strategy backtesting. It calculates over 100 statistical metrics including risk-adjusted return ratios (Sharpe, Sortino, Calmar), drawdown analysis, Value at Risk (VaR), Conditional VaR, and performs Monte Carlo simulation and Walk-Forward Analysis.

█ WHY THIS LIBRARY MATTERS

Pine Script is a simple yet effective coding language for algorithmic and quantitative trading. Its accessibility enables traders to quickly prototype and test ideas directly within TradingView. However, the built-in strategy tester provides only basic metrics (net profit, win rate, drawdown), which is often insufficient for serious strategy evaluation.

Due to this limitation, many traders migrate to alternative backtesting platforms that offer comprehensive analytics. These platforms require other language programming knowledge, environment setup, and significant time investment—often just to test a simple trading idea.

Deeptest bridges this gap by bringing institutional-level quantitative analytics directly to Pine Script. Traders can now perform sophisticated analysis without leaving TradingView or learning complex external platforms. All calculations are derived from strategy.closedtrades.* , ensuring compatibility with any existing Pine Script strategy.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ ORIGINALITY AND USEFULNESS

This library is original work that adds value to the TradingView community in the following ways:

1. Comprehensive Metric Suite: Implements 112+ statistical calculations in a single library, including advanced metrics not available in TradingView's built-in tester (p-value, Z-score, Skewness, Kurtosis, Risk of Ruin).

2. Monte Carlo Simulation: Implements trade-sequence randomization to stress-test strategy robustness by simulating 1000+ alternative equity curves.

3. Walk-Forward Analysis: Divides historical data into rolling in-sample and out-of-sample windows to detect overfitting by comparing training vs. testing performance.

4. Rolling Window Statistics: Calculates time-varying Sharpe, Sortino, and Expectancy to analyze metric consistency throughout the backtest period.

5. Interactive Table Display: Renders professional-grade tables with color-coded thresholds, tooltips explaining each metric, and period analysis cards for drawdowns/trades.

6. Benchmark Comparison: Automatically fetches S&P 500 data to calculate Alpha, Beta, and R-squared, enabling objective assessment of strategy skill vs. passive investing.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ KEY FEATURES

Performance Metrics

Net Profit, CAGR, Monthly Return, Expectancy

Profit Factor, Payoff Ratio, Sample Size

Compounding Effect Analysis

Risk Metrics

Sharpe Ratio, Sortino Ratio, Calmar Ratio (MAR)

Martin Ratio, Ulcer Index

Max Drawdown, Average Drawdown, Drawdown Duration

Risk of Ruin, R-squared (equity curve linearity)

Statistical Distribution

Value at Risk (VaR 95%), Conditional VaR

Skewness (return asymmetry)

Kurtosis (tail fatness)

Z-Score, p-value (statistical significance testing)

Trade Analysis

Win Rate, Breakeven Rate, Loss Rate

Average Trade Duration, Time in Market

Consecutive Win/Loss Streaks with Expected values

Top/Worst Trades with R-multiple tracking

Advanced Analytics

Monte Carlo Simulation (1000+ iterations)

Walk-Forward Analysis (rolling windows)

Rolling Statistics (time-varying metrics)

Out-of-Sample Testing

Benchmark Comparison

Alpha (excess return vs. benchmark)

Beta (systematic risk correlation)

Buy & Hold comparison

R-squared vs. benchmark

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ QUICK START

Basic Usage

//@version=6

strategy("My Strategy", overlay=true)

// Import the library

import Fractalyst/Deeptest/1 as *

// Your strategy logic

fastMA = ta.sma(close, 10)

slowMA = ta.sma(close, 30)

if ta.crossover(fastMA, slowMA)

strategy.entry("Long", strategy.long)

if ta.crossunder(fastMA, slowMA)

strategy.close("Long")

// Run the analysis

DT.runDeeptest()

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ METRIC EXPLANATIONS

The Deeptest table displays 23 metrics across the main row, with 23 additional metrics in the complementary row. Each metric includes detailed tooltips accessible by hovering over the value.

Main Row — Performance Metrics (Columns 0-6)

Net Profit — (Final Equity - Initial Capital) / Initial Capital × 100

— >20%: Excellent, >0%: Profitable, <0%: Loss

— Total return percentage over entire backtest period

Payoff Ratio — Average Win / Average Loss

— >1.5: Excellent, >1.0: Good, <1.0: Losses exceed wins

— Average winning trade size relative to average losing trade. Breakeven win rate = 100% / (1 + Payoff)

Sample Size — Count of closed trades

— >=30: Statistically valid, <30: Insufficient data

— Number of completed trades. Includes 95% confidence interval for win rate in tooltip

Profit Factor — Gross Profit / Gross Loss

— >=1.5: Excellent, >1.0: Profitable, <1.0: Losing

— Ratio of total winnings to total losses. Uses absolute values unlike payoff ratio

CAGR — (Final / Initial)^(365.25 / Days) - 1

— >=10%: Excellent, >0%: Positive growth

— Compound Annual Growth Rate - annualized return accounting for compounding

Expectancy — Sum of all returns / Trade count

— >0.20%: Excellent, >0%: Positive edge

— Average return per trade as percentage. Positive expectancy indicates profitable edge

Monthly Return — Net Profit / (Months in test)

— >0%: Profitable month average

— Average monthly return. Geometric monthly also shown in tooltip

Main Row — Trade Statistics (Columns 7-14)

Avg Duration — Average time in position per trade

— Mean holding period from entry to exit. Influenced by timeframe and trading style

Max CW — Longest consecutive winning streak

— Maximum consecutive wins. Expected value = ln(trades) / ln(1/winRate)

Max CL — Longest consecutive losing streak

— Maximum consecutive losses. Important for psychological risk tolerance

Win Rate — Wins / Total Trades

— Higher is better

— Percentage of profitable trades. Breakeven win rate shown in tooltip

BE Rate — Breakeven Trades / Total Trades

— Lower is better

— Percentage of trades that broke even (neither profit nor loss)

Loss Rate — Losses / Total Trades

— Lower is better

— Percentage of unprofitable trades. Together with win rate and BE rate, sums to 100%

Frequency — Trades per month

— Trading activity level. Displays intelligently (e.g., "12/mo", "1.5/wk", "3/day")

Exposure — Time in market / Total time × 100

— Lower = less risk

— Percentage of time the strategy had open positions

Main Row — Risk Metrics (Columns 15-22)

Sharpe Ratio — (Return - Rf) / StdDev × sqrt(Periods)

— >=3: Excellent, >=2: Good, >=1: Fair, <1: Poor

— Measures risk-adjusted return using total volatility. Annualized using sqrt(252) for daily

Sortino Ratio — (Return - Rf) / DownsideDev × sqrt(Periods)

— >=2: Excellent, >=1: Good, <1: Needs improvement

— Similar to Sharpe but only penalizes downside volatility. Can be higher than Sharpe

Max DD — (Peak - Trough) / Peak × 100

— <5%: Excellent, 5-15%: Moderate, 15-30%: High, >30%: Severe

— Largest peak-to-trough decline in equity. Critical for risk tolerance and position sizing

RoR — Risk of Ruin probability

— <1%: Excellent, 1-5%: Acceptable, 5-10%: Elevated, >10%: Dangerous

— Probability of losing entire trading account based on win rate and payoff ratio

R² — R-squared of equity curve vs. time

— >=0.95: Excellent, 0.90-0.95: Good, 0.80-0.90: Moderate, <0.80: Erratic

— Coefficient of determination measuring linearity of equity growth

MAR — CAGR / |Max Drawdown|

— Higher is better, negative = bad

— Calmar Ratio. Reward relative to worst-case loss. Negative if max DD exceeds CAGR

CVaR — Average of returns below VaR threshold

— Lower absolute is better

— Conditional Value at Risk (Expected Shortfall). Average loss in worst 5% of outcomes

p-value — Binomial test probability

— <0.05: Significant, 0.05-0.10: Marginal, >0.10: Likely random

— Probability that observed results are due to chance. Low p-value means statistically significant edge

Complementary Row — Extended Metrics

Compounding — (Compounded Return / Total Return) × 100

— Percentage of total profit attributable to compounding (position sizing)

Avg Win — Sum of wins / Win count

— Average profitable trade return in percentage

Avg Trade — Sum of all returns / Total trades

— Same as Expectancy (Column 5). Displayed here for convenience

Avg Loss — Sum of losses / Loss count

— Average unprofitable trade return in percentage (negative value)

Martin Ratio — CAGR / Ulcer Index

— Similar to Calmar but uses Ulcer Index instead of Max DD

Rolling Expectancy — Mean of rolling window expectancies

— Average expectancy calculated across rolling windows. Shows consistency of edge

Avg W Dur — Avg duration of winning trades

— Average time from entry to exit for winning trades only

Max Eq — Highest equity value reached

— Peak equity achieved during backtest

Min Eq — Lowest equity value reached

— Trough equity point. Important for understanding worst-case absolute loss

Buy & Hold — (Close_last / Close_first - 1) × 100

— >0%: Passive profit

— Return of simply buying and holding the asset from backtest start to end

Alpha — Strategy CAGR - Benchmark CAGR

— >0: Has skill (beats benchmark)

— Excess return above passive benchmark. Positive alpha indicates genuine value-added skill

Beta — Covariance(Strategy, Benchmark) / Variance(Benchmark)

— <1: Less volatile than market, >1: More volatile

— Systematic risk correlation with benchmark

Avg L Dur — Avg duration of losing trades

— Average time from entry to exit for losing trades only

Rolling Sharpe/Sortino — Dynamic based on win rate

— >2: Good consistency

— Rolling metric across sliding windows. Shows Sharpe if win rate >50%, Sortino if <=50%

Curr DD — Current drawdown from peak

— Lower is better

— Present drawdown percentage. Zero means at new equity high

DAR — CAGR adjusted for target DD

— Higher is better

— Drawdown-Adjusted Return. DAR^5 = CAGR if max DD = 5%

Kurtosis — Fourth moment / StdDev^4 - 3

— ~0: Normal, >0: Fat tails, <0: Thin tails

— Measures "tailedness" of return distribution (excess kurtosis)

Skewness — Third moment / StdDev^3

— >0: Positive skew (big wins), <0: Negative skew (big losses)

— Return distribution asymmetry

VaR — 5th percentile of returns

— Lower absolute is better

— Value at Risk at 95% confidence. Maximum expected loss in worst 5% of outcomes

Ulcer — sqrt(mean(drawdown^2))

— Lower is better

— Ulcer Index - root mean square of drawdowns. Penalizes both depth AND duration

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ MONTE CARLO SIMULATION

Purpose

Monte Carlo simulation tests strategy robustness by randomizing the order of trades while keeping trade returns unchanged. This simulates alternative equity curves to assess outcome variability.

Method

Extract all historical trade returns

Randomly shuffle the sequence (1000+ iterations)

Calculate cumulative equity for each shuffle

Build distribution of final outcomes

Output

The stress test table shows:

Median Outcome: 50th percentile result

5th Percentile: Worst 5% of outcomes

95th Percentile: Best 95% of outcomes

Success Rate: Percentage of simulations that were profitable

Interpretation

If 95% of simulations are profitable: Strategy is robust

If median is far from actual result: High variance/unreliability

If 5th percentile shows large loss: High tail risk

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ WALK-FORWARD ANALYSIS

Purpose

Walk-Forward Analysis (WFA) is the gold standard for detecting strategy overfitting. It simulates real-world trading by dividing historical data into rolling "training" (in-sample) and "validation" (out-of-sample) periods. A strategy that performs well on unseen data is more likely to succeed in live trading.

Method

The implementation uses a non-overlapping window approach following AmiBroker's gold standard methodology:

Segment Calculation: Total trades divided into N windows (default: 12), IS = ~75%, OOS = ~25%, Step = OOS length

Window Structure: Each window has IS (training) followed by OOS (validation). Each OOS becomes the next window's IS (rolling forward)

Metrics Calculated: CAGR, Sharpe, Sortino, MaxDD, Win Rate, Expectancy, Profit Factor, Payoff

Aggregation: IS metrics averaged across all IS periods, OOS metrics averaged across all OOS periods

Output

IS CAGR: In-sample annualized return

OOS CAGR: Out-of-sample annualized return ( THE key metric )

IS/OOS Sharpe: In/out-of-sample risk-adjusted return

Success Rate: % of OOS windows that were profitable

Interpretation

Robust: IS/OOS CAGR gap <20%, OOS Success Rate >80%

Some Overfitting: CAGR gap 20-50%, Success Rate 50-80%

Severe Overfitting: CAGR gap >50%, Success Rate <50%

Key Principles:

OOS is what matters — Only OOS predicts live performance

Consistency > Magnitude — 10% IS / 9% OOS beats 30% IS / 5% OOS

Window count — More windows = more reliable validation

Non-overlapping OOS — Prevents data leakage

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ TABLE DISPLAY

Main Table — Organized into three sections:

Performance Metrics (Cols 0-6): Net Profit, Payoff, Sample Size, Profit Factor, CAGR, Expectancy, Monthly

Trade Statistics (Cols 7-14): Avg Duration, Max CW, Max CL, Win, BE, Loss, Frequency, Exposure

Risk Metrics (Cols 15-22): Sharpe, Sortino, Max DD, RoR, R², MAR, CVaR, p-value

Color Coding

🟢 Green: Excellent performance

🟠 Orange: Acceptable performance

⚪ Gray: Neutral / Fair

🔴 Red: Poor performance

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ IMPLEMENTATION NOTES

Data Source: All metrics calculated from strategy.closedtrades , ensuring compatibility with any Pine Script strategy

Calculation Timing: All calculations occur on barstate.islastconfirmedhistory to optimize performance

Limitations: Requires at least 1 closed trade for basic metrics, 30+ trades for reliable statistical analysis

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ QUICK NOTES

➙ This library has been developed and refined over two years of real-world strategy testing. Every calculation has been validated against industry-standard quantitative finance references.

➙ The entire codebase is thoroughly documented inline. If you are curious about how a metric is calculated or want to understand the implementation details, dive into the source code -- it is written to be read and learned from.

➙ This description focuses on usage and concepts rather than exhaustively listing every exported type and function. The library source code is thoroughly documented inline -- explore it to understand implementation details and internal logic.

➙ All calculations execute on barstate.islastconfirmedhistory to minimize runtime overhead. The library is designed for efficiency without sacrificing accuracy.

➙ Beyond analysis, this library serves as a learning resource. Study the source code to understand quantitative finance concepts, Pine Script advanced techniques, and proper statistical methodology.

➙ Metrics are their own not binary good/bad indicators. A high Sharpe ratio with low sample size is misleading. A deep drawdown during a market crash may be acceptable. Study each function and metric individually -- evaluate your strategy contextually, not by threshold alone.

➙ All strategies face alpha decay over time. Instead of over-optimizing a single strategy on one timeframe and market, build a diversified portfolio across multiple markets and timeframes. Deeptest helps you validate each component so you can combine robust strategies into a trading portfolio.

➙ Screenshots shown in the documentation are solely for visual representation to demonstrate how the tables and metrics will be displayed. Please do not compare your strategy's performance with the metrics shown in these screenshots -- they are illustrative examples only, not performance targets or benchmarks.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ HOW-TO

Using Deeptest is intentionally straightforward. Just import the library and call DT.runDeeptest() at the end of your strategy code in main scope. .

//@version=6

strategy("My Strategy", overlay=true)

// Import the library

import Fractalyst/Deeptest/1 as DT

// Your strategy logic

fastMA = ta.sma(close, 10)

slowMA = ta.sma(close, 30)

if ta.crossover(fastMA, slowMA)

strategy.entry("Long", strategy.long)

if ta.crossunder(fastMA, slowMA)

strategy.close("Long")

// Run the analysis

DT.runDeeptest()

And yes... it's compatible with any TradingView Strategy! 🪄

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ CREDITS

Author: @Fractalyst

Font Library: by @fikira - @kaigouthro - @Duyck

Community: Inspired by the @PineCoders community initiative, encouraging developers to contribute open-source libraries and continuously enhance the Pine Script ecosystem for all traders.

if you find Deeptest valuable in your trading journey, feel free to use it in your strategies and give a shoutout to @Fractalyst -- Your recognition directly supports ongoing development and open-source contributions to Pine Script.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ DISCLAIMER

This library is provided for educational and research purposes. Past performance does not guarantee future results. Always test thoroughly and use proper risk management. The author is not responsible for any trading losses incurred through the use of this code.

指标和策略

Count█ OVERVIEW

A library of functions for counting the number of times (frequency) that elements occur in an array or matrix.

█ USAGE

Import the Count library.

import joebaus/count/1 as c

Create an array or matrix that is a `float`, `int`, `string`, or `bool` type to count elements from, then call the count function on the array or matrix.

id = array.from(1.00, 1.50, 1.25, 1.00, 0.75, 1.25, 1.75, 1.25)

countMap = id.count() // Alternatively: countMap = c.count(id)

The "count map" will return a map with keys for each unique element in the array or matrix, and with respective values representing the number of times the unique element was counted. The keys will be the same type as the array or matrix counted. The values will always be an `int` type.

array mapKeys = countMap.keys() // Returns unique keys

array mapValues = countMap.values() // Returns counts

If an array is in ascending or descending order, then the keys of the map will also generate in the same order.

intArray = array.from(2, 2, 2, 3, 4, 4, 4, 4, 4, 6, 6) // Ascending order

map countMap = intArray.count() // Creates a "count map" of all unique elements

array mapKeys = countMap.keys() // Returns // Ascending order

array mapValues = countMap.values() // Returns count

Include a value to get the count of only that value in an array or matrix.

floatMatrix = matrix.new(3, 3, 0.0)

floatMatrix.set(0, 0, 1.0), floatMatrix.set(1, 0, 1.0), floatMatrix.set(2, 0, 1.0)

floatMatrix.set(0, 1, 1.5), floatMatrix.set(1, 1, 2.0), floatMatrix.set(2, 1, 2.5)

floatMatrix.set(0, 2, 1.0), floatMatrix.set(1, 2, 2.5), floatMatrix.set(2, 2, 1.5)

int countFloatMatrix = floatMatrix.count(1.0) // Counts all 1.0 elements, returns 5

// Alternatively: int countFloatMatrix = c.count(floatMatrix, 1.0)

The string method of count() can use strings or regular expressions like "bull*" to count all matching occurrences in a string array.

stringArray = array.from('bullish', 'bull', 'bullish', 'bear', 'bull', 'bearish', 'bearish')

int countString = stringArray.count('bullish') // Returns 2

int countStringRegex = stringArray.count('bull*') // Returns 4

To count multiple values, use an array of values instead of a single value. Returning a count map only of elements in the array.

countArray = array.from(1.0, 2.5)

map countMap = floatMatrix.count(countArray)

array mapKeys = countMap.keys() // Returns keys

array mapValues = countMap.values() // Returns counts

Multiple regex patterns or strings can be counted as well.

stringMatrix = matrix.new(3, 3, '')

stringMatrix.set(0, 0, 'a'), stringMatrix.set(1, 0, 'a'), stringMatrix.set(2, 0, 'a')

stringMatrix.set(0, 1, 'b'), stringMatrix.set(1, 1, 'c'), stringMatrix.set(2, 1, 'd')

stringMatrix.set(0, 2, 'a'), stringMatrix.set(1, 2, 'd'), stringMatrix.set(2, 2, 'b')

// Count the number of times the regex patterns `'^(a|c)$'` and `'^(b|d)$'` occur

array regexes = array.from('^(a|c)$', '^(b|d)$')

map countMap = stringMatrix.count(regexes)

array mapKeys = countMap.keys() // Returns

array mapValues = countMap.values() // Returns

An optional comparison operator can be specified to count the number of times an equality was satisfied for `float`, `int`, and `bool` methods of `count()`.

intArray = array.from(2, 2, 2, 3, 4, 4, 4, 4, 4, 6, 6)

// Count the number of times an element is greater than 4

countInt = intArray.count(4, '>') // Returns 2

When passing an array of values to count and a comparison operator, the operator will apply to each value.

intArray = array.from(2, 2, 2, 3, 4, 4, 4, 4, 4, 6, 6)

values = array.from(3, 4)

// Count the number of times and element is greater than 3 and 4

map countMap = intArray.count(values, '>')

array mapKeys = countMap.keys() // Returns

array mapValues = countMap.values() // Returns

Multiple comparison operators can be applied when counting multiple values.

intMatrix = matrix.new(3, 3, 0)

intMatrix.set(0, 0, 2), intMatrix.set(1, 0, 3), intMatrix.set(2, 0, 5)

intMatrix.set(0, 1, 2), intMatrix.set(1, 1, 4), intMatrix.set(2, 1, 2)

intMatrix.set(0, 2, 5), intMatrix.set(1, 2, 2), intMatrix.set(2, 2, 3)

values = array.from(3, 4)

comparisons = array.from('<', '>')

// Count the number of times an element is less than 3 and greater than 4

map countMap = intMatrix.count(values, comparisons)

array mapKeys = countMap.keys() // Returns

array mapValues = countMap.values() // Returns

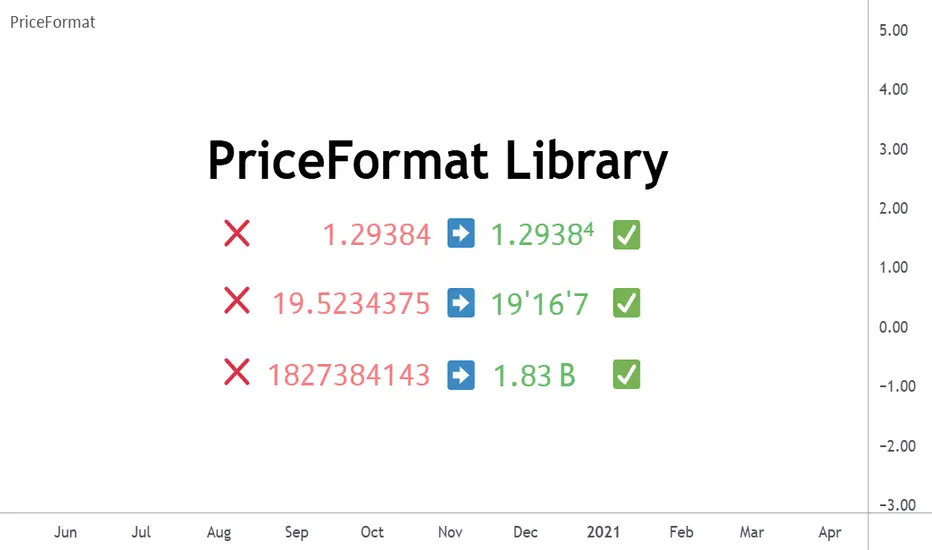

PriceFormatLibrary for automatically converting price values to formatted strings

matching the same format that TradingView uses to display open/high/low/close prices on the chart.

█ OVERVIEW

This library is intended for Pine Coders who are authors of scripts that display numbers onto a user's charts. Typically, 𝚜𝚝𝚛.𝚝𝚘𝚜𝚝𝚛𝚒𝚗𝚐() would be used to convert a number into a string which can be displayed in a label / box / table, but this only works well for values that are formatted as a simple decimal number. The purpose of this library is to provide an easy way to create a formatted string for values which use other types of formats besides the decimal format.

The main functions exported by this library are:

𝚏𝚘𝚛𝚖𝚊𝚝𝙿𝚛𝚒𝚌𝚎() - creates a formatted string from a price value

𝚖𝚎𝚊𝚜𝚞𝚛𝚎𝙿𝚛𝚒𝚌𝚎𝙲𝚑𝚊𝚗𝚐𝚎() - creates a formatted string from the distance between two prices

𝚝𝚘𝚜𝚝𝚛𝚒𝚗𝚐() - an alternative to the built-in 𝚜𝚝𝚛.𝚝𝚘𝚜𝚝𝚛𝚒𝚗𝚐(𝚟𝚊𝚕𝚞𝚎, 𝚏𝚘𝚛𝚖𝚊𝚝)

This library also exports some auxiliary functions which are used under the hood of the previously mentioned functions, but can also be useful to Pine Coders that need fine-tuned control for customized formatting of numeric values:

Functions that determine information about the current chart:

𝚒𝚜𝙵𝚛𝚊𝚌𝚝𝚒𝚘𝚗𝚊𝚕𝙵𝚘𝚛𝚖𝚊𝚝(), 𝚒𝚜𝚅𝚘𝚕𝚞𝚖𝚎𝙵𝚘𝚛𝚖𝚊𝚝(), 𝚒𝚜𝙿𝚎𝚛𝚌𝚎𝚗𝚝𝚊𝚐𝚎𝙵𝚘𝚛𝚖𝚊𝚝(), 𝚒𝚜𝙳𝚎𝚌𝚒𝚖𝚊𝚕𝙵𝚘𝚛𝚖𝚊𝚝(), 𝚒𝚜𝙿𝚒𝚙𝚜𝙵𝚘𝚛𝚖𝚊𝚝()

Functions that convert a 𝚏𝚕𝚘𝚊𝚝 value to a formatted string:

𝚊𝚜𝙳𝚎𝚌𝚒𝚖𝚊𝚕(), 𝚊𝚜𝙿𝚒𝚙𝚜(), 𝚊𝚜𝙵𝚛𝚊𝚌𝚝𝚒𝚘𝚗𝚊𝚕(), 𝚊𝚜𝚅𝚘𝚕𝚞𝚖𝚎()

█ EXAMPLES

• Simple Example

This example shows the simplest way to utilize this library.

//@version=6

indicator("Simple Example")

import n00btraders/PriceFormat/1

var table t = table.new(position.middle_right, 2, 1, bgcolor = color.new(color.blue, 90), force_overlay = true)

if barstate.isfirst

table.cell(t, 0, 0, "Current Price: ", text_color = color.black, text_size = 40)

table.cell(t, 1, 0, text_color = color.blue, text_size = 40)

if barstate.islast

string lastPrice = close.formatPrice() // Simple, easy way to format price

table.cell_set_text(t, 1, 0, lastPrice)

• Complex Example

This example calls all of the main functions and uses their optional arguments.

//@version=6

indicator("Complex Example")

import n00btraders/PriceFormat/1

// Enum values that can be used as optional arguments

precision = input.enum(PriceFormat.Precision.DEFAULT)

language = input.enum(PriceFormat.Language.ENGLISH)

// Main library functions used to create formatted strings

string formattedOpen = open.formatPrice(precision, language, allowPips = true)

string rawOpenPrice = PriceFormat.tostring(open, format.price)

string formattedClose = close.formatPrice(precision, language, allowPips = true)

string rawClosePrice = PriceFormat.tostring(close, format.price)

= PriceFormat.measurePriceChange(open, close, precision, language, allowPips = true)

// Labels to display formatted values on chart

string prices = str.format("Open: {0} ({1}) Close: {2} ({3})", formattedOpen, rawOpenPrice, formattedClose, rawClosePrice)

string change = str.format("Change (close - open): {0} / {1}", distance, ticks)

label.new(chart.point.now(high), prices, yloc = yloc.abovebar, textalign = text.align_left, force_overlay = true)

label.new(chart.point.now(low), change, yloc = yloc.belowbar, style = label.style_label_up, force_overlay = true)

█ NOTES

• Function Descriptions

The library source code uses Markdown for the exported functions. Hover over a function/method call in the Pine Editor to display formatted, detailed information about the function/method.

• Precision Settings

The Precision option in the chart settings can change the format of how prices are displayed on the chart. Since the user's selected choice cannot be known through any Pine built-in variable, this library provides a 𝙿𝚛𝚎𝚌𝚒𝚜𝚒𝚘𝚗 enum that can be used as an optional script input for the user to specify their selected choice.

• Language Settings

The Language option in the user menu can change the decimal/grouping separators in the prices that are displayed on the chart. Since the user's selected choice cannot be known through any Pine built-in variable, this library provides a 𝙻𝚊𝚗𝚐𝚞𝚊𝚐𝚎 enum that can be used as an optional script input for the user to specify their selected choice.

█ EXPORTED FUNCTIONS

method formatPrice(price, precision, language, allowPips)

Formats a price value to match how it would be displayed on the user's current chart.

Namespace types: series float, simple float, input float, const float

Parameters:

price (float) : The value to format.

precision (series Precision) : A Precision.* enum value.

language (series Language) : A Language.* enum value.

allowPips (simple bool) : Whether to allow decimal numbers to display as pips.

Returns: Automatically formatted price string.

measurePriceChange(startPrice, endPrice, precision, language, allowPips)

Measures a change in price in terms of both distance and ticks.

Parameters:

startPrice (float) : The starting price.

endPrice (float) : The ending price.

precision (series Precision) : A Precision.* enum value.

language (series Language) : A Language.* enum value.

allowPips (simple bool) : Whether to allow decimal numbers to display as pips.

Returns: A tuple of formatted strings: .

method tostring(value, format)

Alternative to the Pine `str.tostring(value, format)` built-in function.

Namespace types: series float, simple float, input float, const float

Parameters:

value (float) : (series float) The value to format.

format (string) : (series string) The format string.

Returns: String in the specified format.

isFractionalFormat()

Determines if the default behavior of the chart's price scale is to use a fractional format.

Returns: True if the chart can display prices in fractional format.

isVolumeFormat()

Determines if the default behavior of the chart's price scale is to display prices as volume.

Returns: True if the chart can display prices as volume.

isPercentageFormat()

Determines if the default behavior of the chart's price scale is to display percentages.

Returns: True if the chart can display prices as percentages.

isDecimalFormat()

Determines if the default behavior of the chart's price scale is to use a decimal format.

Returns: True if the chart can display prices in decimal format.

isPipsFormat()

Determines if the current symbol's prices can be displayed as pips.

Returns: True if the chart can display prices as pips.

method asDecimal(value, precision, minTick, decimalSeparator, groupingSeparator, eNotation)

Converts a number to a string in decimal format.

Namespace types: series float, simple float, input float, const float

Parameters:

value (float) : The value to format.

precision (int) : Number of decimal places.

minTick (float) : Minimum tick size.

decimalSeparator (string) : The decimal separator.

groupingSeparator (string) : The thousands separator, aka digit group separator.

eNotation (bool) : Whether the result should use E notation.

Returns: String in decimal format.

method asPips(value, priceScale, minMove, minMove2, decimalSeparator, groupingSeparator)

Converts a number to a string in decimal format with the last digit replaced by a superscript.

Namespace types: series float, simple float, input float, const float

Parameters:

value (float) : The value to format.

priceScale (int) : Price scale.

minMove (int) : Min move.

minMove2 (int) : Min move 2.

decimalSeparator (string) : The decimal separator.

groupingSeparator (string) : The thousands separator, aka digit group separator.

Returns: String in decimal format with an emphasis on the pip value.

method asFractional(value, priceScale, minMove, minMove2, fractionalSeparator1, fractionalSeparator2)

Converts a number to a string in fractional format.

Namespace types: series float, simple float, input float, const float

Parameters:

value (float) : The value to format.

priceScale (int) : Price scale.

minMove (int) : Min move.

minMove2 (int) : Min move 2.

fractionalSeparator1 (string) : The primary fractional separator.

fractionalSeparator2 (string) : The secondary fractional separator.

Returns: String in fractional format.

method asVolume(value, precision, minTick, decimalSeparator, groupingSeparator, spacing)

Converts a number to a string in volume format.

Namespace types: series float, simple float, input float, const float

Parameters:

value (float) : The value to format.

precision (int) : Maximum number of decimal places.

minTick (float) : Minimum tick size.

decimalSeparator (string) : The decimal separator.

groupingSeparator (string) : The thousands separator, aka digit group separator.

spacing (string) : The whitespace separator.

Returns: String in volume format.

LogNormalLibrary "LogNormal"

A collection of functions used to model skewed distributions as log-normal.

Prices are commonly modeled using log-normal distributions (ie. Black-Scholes) because they exhibit multiplicative changes with long tails; skewed exponential growth and high variance. This approach is particularly useful for understanding price behavior and estimating risk, assuming continuously compounding returns are normally distributed.

Because log space analysis is not as direct as using math.log(price) , this library extends the Error Functions library to make working with log-normally distributed data as simple as possible.

- - -

QUICK START

Import library into your project

Initialize model with a mean and standard deviation

Pass model params between methods to compute various properties

var LogNorm model = LN.init(arr.avg(), arr.stdev()) // Assumes the library is imported as LN

var mode = model.mode()

Outputs from the model can be adjusted to better fit the data.

var Quantile data = arr.quantiles()

var more_accurate_mode = mode.fit(model, data) // Fits value from model to data

Inputs to the model can also be adjusted to better fit the data.

datum = 123.45

model_equivalent_datum = datum.fit(data, model) // Fits value from data to the model

area_from_zero_to_datum = model.cdf(model_equivalent_datum)

- - -

TYPES

There are two requisite UDTs: LogNorm and Quantile . They are used to pass parameters between functions and are set automatically (see Type Management ).

LogNorm

Object for log space parameters and linear space quantiles .

Fields:

mu (float) : Log space mu ( µ ).

sigma (float) : Log space sigma ( σ ).

variance (float) : Log space variance ( σ² ).

quantiles (Quantile) : Linear space quantiles.

Quantile

Object for linear quantiles, most similar to a seven-number summary .

Fields:

Q0 (float) : Smallest Value

LW (float) : Lower Whisker Endpoint

LC (float) : Lower Whisker Crosshatch

Q1 (float) : First Quartile

Q2 (float) : Second Quartile

Q3 (float) : Third Quartile

UC (float) : Upper Whisker Crosshatch

UW (float) : Upper Whisker Endpoint

Q4 (float) : Largest Value

IQR (float) : Interquartile Range

MH (float) : Midhinge

TM (float) : Trimean

MR (float) : Mid-Range

- - -

TYPE MANAGEMENT

These functions reliably initialize and update the UDTs. Because parameterization is interdependent, avoid setting the LogNorm and Quantile fields directly .

init(mean, stdev, variance)

Initializes a LogNorm object.

Parameters:

mean (float) : Linearly measured mean.

stdev (float) : Linearly measured standard deviation.

variance (float) : Linearly measured variance.

Returns: LogNorm Object

set(ln, mean, stdev, variance)

Transforms linear measurements into log space parameters for a LogNorm object.

Parameters:

ln (LogNorm) : Object containing log space parameters.

mean (float) : Linearly measured mean.

stdev (float) : Linearly measured standard deviation.

variance (float) : Linearly measured variance.

Returns: LogNorm Object

quantiles(arr)

Gets empirical quantiles from an array of floats.

Parameters:

arr (array) : Float array object.

Returns: Quantile Object

- - -

DESCRIPTIVE STATISTICS

Using only the initialized LogNorm parameters, these functions compute a model's central tendency and standardized moments.

mean(ln)

Computes the linear mean from log space parameters.

Parameters:

ln (LogNorm) : Object containing log space parameters.

Returns: Between 0 and ∞

median(ln)

Computes the linear median from log space parameters.

Parameters:

ln (LogNorm) : Object containing log space parameters.

Returns: Between 0 and ∞

mode(ln)

Computes the linear mode from log space parameters.

Parameters:

ln (LogNorm) : Object containing log space parameters.

Returns: Between 0 and ∞

variance(ln)

Computes the linear variance from log space parameters.

Parameters:

ln (LogNorm) : Object containing log space parameters.

Returns: Between 0 and ∞

skewness(ln)

Computes the linear skewness from log space parameters.

Parameters:

ln (LogNorm) : Object containing log space parameters.

Returns: Between 0 and ∞

kurtosis(ln, excess)

Computes the linear kurtosis from log space parameters.

Parameters:

ln (LogNorm) : Object containing log space parameters.

excess (bool) : Excess Kurtosis (true) or regular Kurtosis (false).

Returns: Between 0 and ∞

hyper_skewness(ln)

Computes the linear hyper skewness from log space parameters.

Parameters:

ln (LogNorm) : Object containing log space parameters.

Returns: Between 0 and ∞

hyper_kurtosis(ln, excess)

Computes the linear hyper kurtosis from log space parameters.

Parameters:

ln (LogNorm) : Object containing log space parameters.

excess (bool) : Excess Hyper Kurtosis (true) or regular Hyper Kurtosis (false).

Returns: Between 0 and ∞

- - -

DISTRIBUTION FUNCTIONS

These wrap Gaussian functions to make working with model space more direct. Because they are contained within a log-normal library, they describe estimations relative to a log-normal curve, even though they fundamentally measure a Gaussian curve.

pdf(ln, x, empirical_quantiles)

A Probability Density Function estimates the probability density . For clarity, density is not a probability .

Parameters:

ln (LogNorm) : Object of log space parameters.

x (float) : Linear X coordinate for which a density will be estimated.

empirical_quantiles (Quantile) : Quantiles as observed in the data (optional).

Returns: Between 0 and ∞

cdf(ln, x, precise)

A Cumulative Distribution Function estimates the area under a Log-Normal curve between Zero and a linear X coordinate.

Parameters:

ln (LogNorm) : Object of log space parameters.

x (float) : Linear X coordinate .

precise (bool) : Double precision (true) or single precision (false).

Returns: Between 0 and 1

ccdf(ln, x, precise)

A Complementary Cumulative Distribution Function estimates the area under a Log-Normal curve between a linear X coordinate and Infinity.

Parameters:

ln (LogNorm) : Object of log space parameters.

x (float) : Linear X coordinate .

precise (bool) : Double precision (true) or single precision (false).

Returns: Between 0 and 1

cdfinv(ln, a, precise)

An Inverse Cumulative Distribution Function reverses the Log-Normal cdf() by estimating the linear X coordinate from an area.

Parameters:

ln (LogNorm) : Object of log space parameters.

a (float) : Normalized area .

precise (bool) : Double precision (true) or single precision (false).

Returns: Between 0 and ∞

ccdfinv(ln, a, precise)

An Inverse Complementary Cumulative Distribution Function reverses the Log-Normal ccdf() by estimating the linear X coordinate from an area.

Parameters:

ln (LogNorm) : Object of log space parameters.

a (float) : Normalized area .

precise (bool) : Double precision (true) or single precision (false).

Returns: Between 0 and ∞

cdfab(ln, x1, x2, precise)

A Cumulative Distribution Function from A to B estimates the area under a Log-Normal curve between two linear X coordinates (A and B).

Parameters:

ln (LogNorm) : Object of log space parameters.

x1 (float) : First linear X coordinate .

x2 (float) : Second linear X coordinate .

precise (bool) : Double precision (true) or single precision (false).

Returns: Between 0 and 1

ott(ln, x, precise)

A One-Tailed Test transforms a linear X coordinate into an absolute Z Score before estimating the area under a Log-Normal curve between Z and Infinity.

Parameters:

ln (LogNorm) : Object of log space parameters.

x (float) : Linear X coordinate .

precise (bool) : Double precision (true) or single precision (false).

Returns: Between 0 and 0.5

ttt(ln, x, precise)

A Two-Tailed Test transforms a linear X coordinate into symmetrical ± Z Scores before estimating the area under a Log-Normal curve from Zero to -Z, and +Z to Infinity.

Parameters:

ln (LogNorm) : Object of log space parameters.

x (float) : Linear X coordinate .

precise (bool) : Double precision (true) or single precision (false).

Returns: Between 0 and 1

ottinv(ln, a, precise)

An Inverse One-Tailed Test reverses the Log-Normal ott() by estimating a linear X coordinate for the right tail from an area.

Parameters:

ln (LogNorm) : Object of log space parameters.

a (float) : Half a normalized area .

precise (bool) : Double precision (true) or single precision (false).

Returns: Between 0 and ∞

tttinv(ln, a, precise)

An Inverse Two-Tailed Test reverses the Log-Normal ttt() by estimating two linear X coordinates from an area.

Parameters:

ln (LogNorm) : Object of log space parameters.

a (float) : Normalized area .

precise (bool) : Double precision (true) or single precision (false).

Returns: Linear space tuple :

- - -

UNCERTAINTY

Model-based measures of uncertainty, information, and risk.

sterr(sample_size, fisher_info)

The standard error of a sample statistic.

Parameters:

sample_size (float) : Number of observations.

fisher_info (float) : Fisher information.

Returns: Between 0 and ∞

surprisal(p, base)

Quantifies the information content of a single event.

Parameters:

p (float) : Probability of the event .

base (float) : Logarithmic base (optional).

Returns: Between 0 and ∞

entropy(ln, base)

Computes the differential entropy (average surprisal).

Parameters:

ln (LogNorm) : Object of log space parameters.

base (float) : Logarithmic base (optional).

Returns: Between 0 and ∞

perplexity(ln, base)

Computes the average number of distinguishable outcomes from the entropy.

Parameters:

ln (LogNorm)

base (float) : Logarithmic base used for Entropy (optional).

Returns: Between 0 and ∞

value_at_risk(ln, p, precise)

Estimates a risk threshold under normal market conditions for a given confidence level.

Parameters:

ln (LogNorm) : Object of log space parameters.

p (float) : Probability threshold, aka. the confidence level .

precise (bool) : Double precision (true) or single precision (false).

Returns: Between 0 and ∞

value_at_risk_inv(ln, value_at_risk, precise)

Reverses the value_at_risk() by estimating the confidence level from the risk threshold.

Parameters:

ln (LogNorm) : Object of log space parameters.

value_at_risk (float) : Value at Risk.

precise (bool) : Double precision (true) or single precision (false).

Returns: Between 0 and 1

conditional_value_at_risk(ln, p, precise)

Estimates the average loss beyond a confidence level, aka. expected shortfall.

Parameters:

ln (LogNorm) : Object of log space parameters.

p (float) : Probability threshold, aka. the confidence level .

precise (bool) : Double precision (true) or single precision (false).

Returns: Between 0 and ∞

conditional_value_at_risk_inv(ln, conditional_value_at_risk, precise)

Reverses the conditional_value_at_risk() by estimating the confidence level of an average loss.

Parameters:

ln (LogNorm) : Object of log space parameters.

conditional_value_at_risk (float) : Conditional Value at Risk.

precise (bool) : Double precision (true) or single precision (false).

Returns: Between 0 and 1

partial_expectation(ln, x, precise)

Estimates the partial expectation of a linear X coordinate.

Parameters:

ln (LogNorm) : Object of log space parameters.

x (float) : Linear X coordinate .

precise (bool) : Double precision (true) or single precision (false).

Returns: Between 0 and µ

partial_expectation_inv(ln, partial_expectation, precise)

Reverses the partial_expectation() by estimating a linear X coordinate.

Parameters:

ln (LogNorm) : Object of log space parameters.

partial_expectation (float) : Partial Expectation .

precise (bool) : Double precision (true) or single precision (false).

Returns: Between 0 and ∞

conditional_expectation(ln, x, precise)

Estimates the conditional expectation of a linear X coordinate.

Parameters:

ln (LogNorm) : Object of log space parameters.

x (float) : Linear X coordinate .

precise (bool) : Double precision (true) or single precision (false).

Returns: Between X and ∞

conditional_expectation_inv(ln, conditional_expectation, precise)

Reverses the conditional_expectation by estimating a linear X coordinate.

Parameters:

ln (LogNorm) : Object of log space parameters.

conditional_expectation (float) : Conditional Expectation .

precise (bool) : Double precision (true) or single precision (false).

Returns: Between 0 and ∞

fisher(ln, log)

Computes the Fisher Information Matrix for the distribution, not a linear X coordinate.

Parameters:

ln (LogNorm) : Object of log space parameters.

log (bool) : Sets if the matrix should be in log (true) or linear (false) space.

Returns: FIM for the distribution

fisher(ln, x, log)

Computes the Fisher Information Matrix for a linear X coordinate, not the distribution itself.

Parameters:

ln (LogNorm) : Object of log space parameters.

x (float) : Linear X coordinate .

log (bool) : Sets if the matrix should be in log (true) or linear (false) space.

Returns: FIM for the linear X coordinate

confidence_interval(ln, x, sample_size, confidence, precise)

Estimates a confidence interval for a linear X coordinate.

Parameters:

ln (LogNorm) : Object of log space parameters.

x (float) : Linear X coordinate .

sample_size (float) : Number of observations.

confidence (float) : Confidence level .

precise (bool) : Double precision (true) or single precision (false).

Returns: CI for the linear X coordinate

- - -

CURVE FITTING

An overloaded function that helps transform values between spaces. The primary function uses quantiles, and the overloads wrap the primary function to make working with LogNorm more direct.

fit(x, a, b)

Transforms X coordinate between spaces A and B.

Parameters:

x (float) : Linear X coordinate from space A .

a (LogNorm | Quantile | array) : LogNorm, Quantile, or float array.

b (LogNorm | Quantile | array) : LogNorm, Quantile, or float array.

Returns: Adjusted X coordinate

- - -

EXPORTED HELPERS

Small utilities to simplify extensibility.

z_score(ln, x)

Converts a linear X coordinate into a Z Score.

Parameters:

ln (LogNorm) : Object of log space parameters.

x (float) : Linear X coordinate.

Returns: Between -∞ and +∞

x_coord(ln, z)

Converts a Z Score into a linear X coordinate.

Parameters:

ln (LogNorm) : Object of log space parameters.

z (float) : Standard normal Z Score.

Returns: Between 0 and ∞

iget(arr, index)

Gets an interpolated value of a pseudo -element (fictional element between real array elements). Useful for quantile mapping.

Parameters:

arr (array) : Float array object.

index (float) : Index of the pseudo element.

Returns: Interpolated value of the arrays pseudo element.

RiskMetrics█ OVERVIEW

This library is a tool for Pine programmers that provides functions for calculating risk-adjusted performance metrics on periodic price returns. The calculations used by this library's functions closely mirror those the Broker Emulator uses to calculate strategy performance metrics (e.g., Sharpe and Sortino ratios) without depending on strategy-specific functionality.

█ CONCEPTS

Returns, risk, and volatility

The return on an investment is the relative gain or loss over a period, often expressed as a percentage. Investment returns can originate from several sources, including capital gains, dividends, and interest income. Many investors seek the highest returns possible in the quest for profit. However, prudent investing and trading entails evaluating such returns against the associated risks (i.e., the uncertainty of returns and the potential for financial losses) for a clearer perspective on overall performance and sustainability.

One way investors and analysts assess the risk of an investment is by analyzing its volatility , i.e., the statistical dispersion of historical returns. Investors often use volatility in risk estimation because it provides a quantifiable way to gauge the expected extent of fluctuation in returns. Elevated volatility implies heightened uncertainty in the market, which suggests higher expected risk. Conversely, low volatility implies relatively stable returns with relatively minimal fluctuations, thus suggesting lower expected risk. Several risk-adjusted performance metrics utilize volatility in their calculations for this reason.

Risk-free rate

The risk-free rate represents the rate of return on a hypothetical investment carrying no risk of financial loss. This theoretical rate provides a benchmark for comparing the returns on a risky investment and evaluating whether its excess returns justify the risks. If an investment's returns are at or below the theoretical risk-free rate or the risk premium is below a desired amount, it may suggest that the returns do not compensate for the extra risk, which might be a call to reassess the investment.

Since the risk-free rate is a theoretical concept, investors often utilize proxies for the rate in practice, such as Treasury bills and other government bonds. Conventionally, analysts consider such instruments "risk-free" for a domestic holder, as they are a form of government obligation with a low perceived likelihood of default.

The average yield on short-term Treasury bills, influenced by economic conditions, monetary policies, and inflation expectations, has historically hovered around 2-3% over the long term. This range also aligns with central banks' inflation targets. As such, one may interpret a value within this range as a minimum proxy for the risk-free rate, as it may correspond to the minimum rate required to maintain purchasing power over time.

The built-in Sharpe and Sortino ratios that strategies calculate and display in the Performance Summary tab use a default risk-free rate of 2%, and the metrics in this library's example code use the same default rate. Users can adjust this value to fit their analysis needs.

Risk-adjusted performance

Risk-adjusted performance metrics gauge the effectiveness of an investment by considering its returns relative to the perceived risk. They aim to provide a more well-rounded picture of performance by factoring in the level of risk taken to achieve returns. Investors can utilize such metrics to help determine whether the returns from an investment justify the risks and make informed decisions.

The two most commonly used risk-adjusted performance metrics are the Sharpe ratio and the Sortino ratio.

1. Sharpe ratio

The Sharpe ratio , developed by Nobel laureate William F. Sharpe, measures the performance of an investment compared to a theoretically risk-free asset, adjusted for the investment risk. The ratio uses the following formula:

Sharpe Ratio = (𝑅𝑎 − 𝑅𝑓) / 𝜎𝑎

Where:

• 𝑅𝑎 = Average return of the investment

• 𝑅𝑓 = Theoretical risk-free rate of return

• 𝜎𝑎 = Standard deviation of the investment's returns (volatility)

A higher Sharpe ratio indicates a more favorable risk-adjusted return, as it signifies that the investment produced higher excess returns per unit of increase in total perceived risk.

2. Sortino ratio

The Sortino ratio is a modified form of the Sharpe ratio that only considers downside volatility , i.e., the volatility of returns below the theoretical risk-free benchmark. Although it shares close similarities with the Sharpe ratio, it can produce very different values, especially when the returns do not have a symmetrical distribution, since it does not penalize upside and downside volatility equally. The ratio uses the following formula:

Sortino Ratio = (𝑅𝑎 − 𝑅𝑓) / 𝜎𝑑

Where:

• 𝑅𝑎 = Average return of the investment

• 𝑅𝑓 = Theoretical risk-free rate of return

• 𝜎𝑑 = Downside deviation (standard deviation of negative excess returns, or downside volatility)

The Sortino ratio offers an alternative perspective on an investment's return-generating efficiency since it does not consider upside volatility in its calculation. A higher Sortino ratio signifies that the investment produced higher excess returns per unit of increase in perceived downside risk.

█ CALCULATIONS

Return period detection

Calculating risk-adjusted performance metrics requires collecting returns across several periods of a given size. Analysts may use different period sizes based on the context and their preferences. However, two widely used standards are monthly or daily periods, depending on the available data and the investment's duration. The built-in ratios displayed in the Strategy Tester utilize returns from either monthly or daily periods in their calculations based on the following logic:

• Use monthly returns if the history of closed trades spans at least two months.

• Use daily returns if the trades span at least two days but less than two months.

• Do not calculate the ratios if the trade data spans fewer than two days.

This library's `detectPeriod()` function applies related logic to available chart data rather than trade data to determine which period is appropriate:

• It returns true if the chart's data spans at least two months, indicating that it's sufficient to use monthly periods.

• It returns false if the chart's data spans at least two days but not two months, suggesting the use of daily periods.

• It returns na if the length of the chart's data covers less than two days, signifying that the data is insufficient for meaningful ratio calculations.

It's important to note that programmers should only call `detectPeriod()` from a script's global scope or within the outermost scope of a function called from the global scope, as it requires the time value from the first bar to accurately measure the amount of time covered by the chart's data.

Collecting periodic returns

This library's `getPeriodicReturns()` function tracks price return data within monthly or daily periods and stores the periodic values in an array . It uses a `detectPeriod()` call as the condition to determine whether each element in the array represents the return over a monthly or daily period.

The `getPeriodicReturns()` function has two overloads. The first overload requires two arguments and outputs an array of monthly or daily returns for use in the `sharpe()` and `sortino()` methods. To calculate these returns:

1. The `percentChange` argument should be a series that represents percentage gains or losses. The values can be bar-to-bar return percentages on the chart timeframe or percentages requested from a higher timeframe.

2. The function compounds all non-na `percentChange` values within each monthly or daily period to calculate the period's total return percentage. When the `percentChange` represents returns from a higher timeframe, ensure the requested data includes gaps to avoid compounding redundant values.

3. After a period ends, the function queues the compounded return into the array , removing the oldest element from the array when its size exceeds the `maxPeriods` argument.

The resulting array represents the sequence of closed returns over up to `maxPeriods` months or days, depending on the available data.

The second overload of the function includes an additional `benchmark` parameter. Unlike the first overload, this version tracks and collects differences between the `percentChange` and the specified `benchmark` values. The resulting array represents the sequence of excess returns over up to `maxPeriods` months or days. Passing this array to the `sharpe()` and `sortino()` methods calculates generalized Information ratios , which represent the risk-adjustment performance of a sequence of returns compared to a risky benchmark instead of a risk-free rate. For consistency, ensure the non-na times of the `benchmark` values align with the times of the `percentChange` values.

Ratio methods

This library's `sharpe()` and `sortino()` methods respectively calculate the Sharpe and Sortino ratios based on an array of returns compared to a specified annual benchmark. Both methods adjust the annual benchmark based on the number of periods per year to suit the frequency of the returns:

• If the method call does not include a `periodsPerYear` argument, it uses `detectPeriod()` to determine whether the returns represent monthly or daily values based on the chart's history. If monthly, the method divides the `annualBenchmark` value by 12. If daily, it divides the value by 365.

• If the method call does specify a `periodsPerYear` argument, the argument's value supersedes the automatic calculation, facilitating custom benchmark adjustments, such as dividing by 252 when analyzing collected daily stock returns.

When the array passed to these methods represents a sequence of excess returns , such as the result from the second overload of `getPeriodicReturns()`, use an `annualBenchmark` value of 0 to avoid comparing those excess returns to a separate rate.

By default, these methods only calculate the ratios on the last available bar to minimize their resource usage. Users can override this behavior with the `forceCalc` parameter. When the value is true , the method calculates the ratio on each call if sufficient data is available, regardless of the bar index.

Look first. Then leap.

█ FUNCTIONS & METHODS

This library contains the following functions:

detectPeriod()

Determines whether the chart data has sufficient coverage to use monthly or daily returns

for risk metric calculations.

Returns: (bool) `true` if the period spans more than two months, `false` if it otherwise spans more

than two days, and `na` if the data is insufficient.

getPeriodicReturns(percentChange, maxPeriods)

(Overload 1 of 2) Tracks periodic return percentages and queues them into an array for ratio

calculations. The span of the chart's historical data determines whether the function uses

daily or monthly periods in its calculations. If the chart spans more than two months,

it uses "1M" periods. Otherwise, if the chart spans more than two days, it uses "1D"

periods. If the chart covers less than two days, it does not store changes.

Parameters:

percentChange (float) : (series float) The change percentage. The function compounds non-na values from each

chart bar within monthly or daily periods to calculate the periodic changes.

maxPeriods (simple int) : (simple int) The maximum number of periodic returns to store in the returned array.

Returns: (array) An array containing the overall percentage changes for each period, limited

to the maximum specified by `maxPeriods`.

getPeriodicReturns(percentChange, benchmark, maxPeriods)

(Overload 2 of 2) Tracks periodic excess return percentages and queues the values into an

array. The span of the chart's historical data determines whether the function uses

daily or monthly periods in its calculations. If the chart spans more than two months,

it uses "1M" periods. Otherwise, if the chart spans more than two days, it uses "1D"

periods. If the chart covers less than two days, it does not store changes.

Parameters:

percentChange (float) : (series float) The change percentage. The function compounds non-na values from each

chart bar within monthly or daily periods to calculate the periodic changes.

benchmark (float) : (series float) The benchmark percentage to compare against `percentChange` values.

The function compounds non-na values from each bar within monthly or

daily periods and subtracts the results from the compounded `percentChange` values to

calculate the excess returns. For consistency, ensure this series has a similar history

length to the `percentChange` with aligned non-na value times.

maxPeriods (simple int) : (simple int) The maximum number of periodic excess returns to store in the returned array.

Returns: (array) An array containing monthly or daily excess returns, limited

to the maximum specified by `maxPeriods`.

method sharpeRatio(returnsArray, annualBenchmark, forceCalc, periodsPerYear)

Calculates the Sharpe ratio for an array of periodic returns.

Callable as a method or a function.

Namespace types: array

Parameters:

returnsArray (array) : (array) An array of periodic return percentages, e.g., returns over monthly or

daily periods.

annualBenchmark (float) : (series float) The annual rate of return to compare against `returnsArray` values. When

`periodsPerYear` is `na`, the function divides this value by 12 to calculate a

monthly benchmark if the chart's data spans at least two months or 365 for a daily

benchmark if the data otherwise spans at least two days. If `periodsPerYear`

has a specified value, the function divides the rate by that value instead.

forceCalc (bool) : (series bool) If `true`, calculates the ratio on every call. Otherwise, ratio calculation

only occurs on the last available bar. Optional. The default is `false`.

periodsPerYear (simple int) : (simple int) If specified, divides the annual rate by this value instead of the value

determined by the time span of the chart's data.

Returns: (float) The Sharpe ratio, which estimates the excess return per unit of total volatility.

method sortinoRatio(returnsArray, annualBenchmark, forceCalc, periodsPerYear)

Calculates the Sortino ratio for an array of periodic returns.

Callable as a method or a function.

Namespace types: array

Parameters:

returnsArray (array) : (array) An array of periodic return percentages, e.g., returns over monthly or

daily periods.

annualBenchmark (float) : (series float) The annual rate of return to compare against `returnsArray` values. When

`periodsPerYear` is `na`, the function divides this value by 12 to calculate a

monthly benchmark if the chart's data spans at least two months or 365 for a daily

benchmark if the data otherwise spans at least two days. If `periodsPerYear`

has a specified value, the function divides the rate by that value instead.

forceCalc (bool) : (series bool) If `true`, calculates the ratio on every call. Otherwise, ratio calculation

only occurs on the last available bar. Optional. The default is `false`.

periodsPerYear (simple int) : (simple int) If specified, divides the annual rate by this value instead of the value

determined by the time span of the chart's data.

Returns: (float) The Sortino ratio, which estimates the excess return per unit of downside

volatility.

analytics_tablesLibrary "analytics_tables"

📝 Description

This library provides the implementation of several performance-related statistics and metrics, presented in the form of tables.

The metrics shown in the afforementioned tables where developed during the past years of my in-depth analalysis of various strategies in an atempt to reason about the performance of each strategy.

The visualization and some statistics where inspired by the existing implementations of the "Seasonality" script, and the performance matrix implementations of @QuantNomad and @ZenAndTheArtOfTrading scripts.

While this library is meant to be used by my strategy framework "Template Trailing Strategy (Backtester)" script, I wrapped it in a library hoping this can be usefull for other community strategy scripts that will be released in the future.

🤔 How to Guide

To use the functionality this library provides in your script you have to import it first!

Copy the import statement of the latest release by pressing the copy button below and then paste it into your script. Give a short name to this library so you can refer to it later on. The import statement should look like this:

import jason5480/analytics_tables/1 as ant

There are three types of tables provided by this library in the initial release. The stats table the metrics table and the seasonality table.

Each one shows different kinds of performance statistics.

The table UDT shall be initialized once using the `init()` method.

They can be updated using the `update()` method where the updated data UDT object shall be passed.

The data UDT can also initialized and get updated on demend depending on the use case

A code example for the StatsTable is the following:

var ant.StatsData statsData = ant.StatsData.new()

statsData.update(SideStats.new(), SideStats.new(), 0)

if (barstate.islastconfirmedhistory or (barstate.isrealtime and barstate.isconfirmed))

var statsTable = ant.StatsTable.new().init(ant.getTablePos('TOP', 'RIGHT'))

statsTable.update(statsData)

A code example for the MetricsTable is the following:

var ant.StatsData statsData = ant.StatsData.new()

statsData.update(ant.SideStats.new(), ant.SideStats.new(), 0)

if (barstate.islastconfirmedhistory or (barstate.isrealtime and barstate.isconfirmed))

var metricsTable = ant.MetricsTable.new().init(ant.getTablePos('BOTTOM', 'RIGHT'))

metricsTable.update(statsData, 10)

A code example for the SeasonalityTable is the following:

var ant.SeasonalData seasonalData = ant.SeasonalData.new().init(Seasonality.monthOfYear)

seasonalData.update()

if (barstate.islastconfirmedhistory or (barstate.isrealtime and barstate.isconfirmed))

var seasonalTable = ant.SeasonalTable.new().init(seasonalData, ant.getTablePos('BOTTOM', 'LEFT'))

seasonalTable.update(seasonalData)

🏋️♂️ Please refer to the "EXAMPLE" regions of the script for more advanced and up to date code examples!

Special thanks to @Mrcrbw for the proposal to develop this library and @DCNeu for the constructive feedback 🏆.

getTablePos(ypos, xpos)

Get table position compatible string

Parameters:

ypos (simple string) : The position on y axise

xpos (simple string) : The position on x axise

Returns: The position to be passed to the table

method init(this, pos, height, width, positiveTxtColor, negativeTxtColor, neutralTxtColor, positiveBgColor, negativeBgColor, neutralBgColor)

Initialize the stats table object with the given colors in the given position

Namespace types: StatsTable

Parameters:

this (StatsTable) : The stats table object

pos (simple string) : The table position string

height (simple float) : The height of the table as a percentage of the charts height. By default, 0 auto-adjusts the height based on the text inside the cells

width (simple float) : The width of the table as a percentage of the charts height. By default, 0 auto-adjusts the width based on the text inside the cells

positiveTxtColor (simple color) : The text color when positive

negativeTxtColor (simple color) : The text color when negative

neutralTxtColor (simple color) : The text color when neutral

positiveBgColor (simple color) : The background color with transparency when positive

negativeBgColor (simple color) : The background color with transparency when negative

neutralBgColor (simple color) : The background color with transparency when neutral

method init(this, pos, height, width, neutralBgColor)

Initialize the metrics table object with the given colors in the given position

Namespace types: MetricsTable

Parameters:

this (MetricsTable) : The metrics table object

pos (simple string) : The table position string

height (simple float) : The height of the table as a percentage of the charts height. By default, 0 auto-adjusts the height based on the text inside the cells

width (simple float) : The width of the table as a percentage of the charts width. By default, 0 auto-adjusts the width based on the text inside the cells

neutralBgColor (simple color) : The background color with transparency when neutral

method init(this, seas)

Initialize the seasonal data

Namespace types: SeasonalData

Parameters:

this (SeasonalData) : The seasonal data object

seas (simple Seasonality) : The seasonality of the matrix data

method init(this, data, pos, maxNumOfYears, height, width, extended, neutralTxtColor, neutralBgColor)

Initialize the seasonal table object with the given colors in the given position

Namespace types: SeasonalTable

Parameters:

this (SeasonalTable) : The seasonal table object

data (SeasonalData) : The seasonality data of the table

pos (simple string) : The table position string

maxNumOfYears (simple int) : The maximum number of years that fit into the table

height (simple float) : The height of the table as a percentage of the charts height. By default, 0 auto-adjusts the height based on the text inside the cells

width (simple float) : The width of the table as a percentage of the charts width. By default, 0 auto-adjusts the width based on the text inside the cells

extended (simple bool) : The seasonal table with extended columns for performance

neutralTxtColor (simple color) : The text color when neutral

neutralBgColor (simple color) : The background color with transparency when neutral

method update(this, wins, losses, numOfInconclusiveExits)

Update the strategy info data of the strategy

Namespace types: StatsData

Parameters:

this (StatsData) : The strategy statistics object

wins (SideStats)

losses (SideStats)

numOfInconclusiveExits (int) : The number of inconclusive trades

method update(this, stats, positiveTxtColor, negativeTxtColor, negativeBgColor, neutralBgColor)

Update the stats table object with the given data

Namespace types: StatsTable

Parameters:

this (StatsTable) : The stats table object

stats (StatsData) : The stats data to update the table

positiveTxtColor (simple color) : The text color when positive

negativeTxtColor (simple color) : The text color when negative

negativeBgColor (simple color) : The background color with transparency when negative

neutralBgColor (simple color) : The background color with transparency when neutral

method update(this, stats, buyAndHoldPerc, positiveTxtColor, negativeTxtColor, positiveBgColor, negativeBgColor)

Update the metrics table object with the given data

Namespace types: MetricsTable

Parameters:

this (MetricsTable) : The metrics table object

stats (StatsData) : The stats data to update the table

buyAndHoldPerc (float) : The buy and hold percetage

positiveTxtColor (simple color) : The text color when positive

negativeTxtColor (simple color) : The text color when negative

positiveBgColor (simple color) : The background color with transparency when positive

negativeBgColor (simple color) : The background color with transparency when negative

method update(this)

Update the seasonal data based on the season and eon timeframe

Namespace types: SeasonalData

Parameters:

this (SeasonalData) : The seasonal data object

method update(this, data, positiveTxtColor, negativeTxtColor, neutralTxtColor, positiveBgColor, negativeBgColor, neutralBgColor, timeBgColor)

Update the seasonal table object with the given data

Namespace types: SeasonalTable

Parameters:

this (SeasonalTable) : The seasonal table object

data (SeasonalData) : The seasonal cell data to update the table

positiveTxtColor (simple color) : The text color when positive

negativeTxtColor (simple color) : The text color when negative

neutralTxtColor (simple color) : The text color when neutral

positiveBgColor (simple color) : The background color with transparency when positive

negativeBgColor (simple color) : The background color with transparency when negative

neutralBgColor (simple color) : The background color with transparency when neutral

timeBgColor (simple color) : The background color of the time gradient

SideStats

Object that represents the strategy statistics data of one side win or lose

Fields:

numOf (series int)

sumFreeProfit (series float)

freeProfitStDev (series float)

sumProfit (series float)

profitStDev (series float)

sumGain (series float)

gainStDev (series float)

avgQuantityPerc (series float)

avgCapitalRiskPerc (series float)

avgTPExecutedCount (series float)

avgRiskRewardRatio (series float)

maxStreak (series int)

StatsTable

Object that represents the stats table

Fields:

table (series table) : The actual table

rows (series int) : The number of rows of the table

columns (series int) : The number of columns of the table

StatsData

Object that represents the statistics data of the strategy

Fields:

wins (SideStats)

losses (SideStats)

numOfInconclusiveExits (series int)

avgFreeProfitStr (series string)

freeProfitStDevStr (series string)

lossFreeProfitStDevStr (series string)

avgProfitStr (series string)

profitStDevStr (series string)

lossProfitStDevStr (series string)

avgQuantityStr (series string)

MetricsTable

Object that represents the metrics table

Fields:

table (series table) : The actual table

rows (series int) : The number of rows of the table

columns (series int) : The number of columns of the table

SeasonalData

Object that represents the seasonal table dynamic data

Fields:

seasonality (series Seasonality)

eonToMatrixRow (map)

numOfEons (series int)

mostRecentMatrixRow (series int)

balances (matrix)

returnPercs (matrix)

maxDDs (matrix)

eonReturnPercs (array)

eonCAGRs (array)

eonMaxDDs (array)

SeasonalTable

Object that represents the seasonal table

Fields:

table (series table) : The actual table

headRows (series int) : The number of head rows of the table

headColumns (series int) : The number of head columns of the table

eonRows (series int) : The number of eon rows of the table

seasonColumns (series int) : The number of season columns of the table

statsRows (series int)

statsColumns (series int) : The number of stats columns of the table

rows (series int) : The number of rows of the table

columns (series int) : The number of columns of the table

extended (series bool) : Whether the table has additional performance statistics

FiniteStateMachine🟩 OVERVIEW

A flexible framework for creating, testing and implementing a Finite State Machine (FSM) in your script. FSMs use rules to control how states change in response to events.

This is the first Finite State Machine library on TradingView and it's quite a different way to think about your script's logic. Advantages of using this vs hardcoding all your logic include:

• Explicit logic : You can see all rules easily side-by-side.

• Validation : Tables show your rules and validation results right on the chart.

• Dual approach : Simple matrix for straightforward transitions; map implementation for concurrent scenarios. You can combine them for complex needs.

• Type safety : Shows how to use enums for robustness while maintaining string compatibility.

• Real-world examples : Includes both conceptual (traffic lights) and practical (trading strategy) demonstrations.

• Priority control : Explicit control over which rules take precedence when multiple conditions are met.

• Wildcard system : Flexible pattern matching for states and events.

The library seems complex, but it's not really. Your conditions, events, and their potential interactions are complex. The FSM makes them all explicit, which is some work. However, like all "good" pain in life, this is front-loaded, and *saves* pain later, in the form of unintended interactions and bugs that are very hard to find and fix.

🟩 SIMPLE FSM (MATRIX-BASED)

The simple FSM uses a matrix to define transition rules with the structure: state > event > state. We look up the current state, check if the event in that row matches, and if it does, output the resulting state.

Each row in the matrix defines one rule, and the first matching row, counting from the top down, is applied.

A limitation of this method is that you can supply only ONE event.

You can design layered rules using widlcards. Use an empty string "" or the special string "ANY" for any state or event wildcard.

The matrix FSM is foruse where you have clear, sequential state transitions triggered by single events. Think traffic lights, or any logic where only one thing can happen at a time.

The demo for this FSM is of traffic lights.

🟩 CONCURRENT FSM (MAP-BASED)