Magic Equity Trend & PivotsMagic Equity Trend & Pivots is a robust technical analysis engine designed specifically for equity and index traders. It serves as a comprehensive "Trend & Level" companion, combining institutional Pivot Points with a proprietary EMA trend filtering system to identify high-probability setups.

How the Magic Works

This indicator simplifies complex market data into a clear visual workflow:

1. The Magic Equity Trend (Trend Identification) The script uses a weighted system to determine the dominant market direction:

Bullish Trend: Price holds above the primary Trend SMA + a Volatility Buffer (Green Zone).

Bearish Trend: Price is rejected below the Trend SMA - Buffer (Red Zone).

No-Trade Zone: When the price is trapped inside the buffer (Gray Channel), the trend is considered weak or ranging.

2. Institutional Pivot Points Price often reacts at hidden levels. This tool calculates and overlays these levels automatically:

Multi-Type Support: Choose between Traditional, Fibonacci, Woodie, Classic, DM, and Camarilla pivots.

Timeframe Smart-Switching: Use fixed timeframes (e.g., Weekly Pivots on a Daily chart) or let the "Auto" mode decide the best reference period for your current view.

Historical Mode: Unlike standard pivots, these can be back-tested visually to see how prices respected levels in the past.

3. Precision Entry & Exit Logic Trade signals are not random; they are based on a strict confluence of "Magic" factors:

Entry Signal: Requires Trend Alignment + Fast/Slow EMA Crossover + RSI Strength (>60) + Relative Volume Spike.

Top-Up (Add-on): Detects low-risk opportunities to add to a position when price pulls back to the EMA10/20 during a strong trend.

Two-Stage Exit: Secures profits using either an ATR Trailing Stop or an Intraday RSI Breakdown, depending on your settings.

4. Divergence & Momentum

RSI Divergence: Automatically plots Regular Bullish and Bearish divergences to warn of potential reversals at tops or bottoms.

Darvas Boxes: Visualizes consolidation ranges to help identify breakouts.

5. Performance Dashboard A data table provides a snapshot of the asset's health:

Mean Reversion: Measures the % distance from key EMAs (10, 20, 50).

RVOL & ADR: Displays Relative Volume and Average Daily Range to gauge volatility.

Performance Tracker: A theoretical summary table showing how the trend signals have performed over the last 1W, 1M, and 1Y periods.

Settings & Customization

Visuals: Fully customizable colors for the Trend Cloud, Pivots, and Backgrounds.

Filters: Toggle specific filters (Volume, RSI, Trend Buffer) to adapt the sensitivity to different asset classes.

Disclaimer: This tool is for educational purposes and technical analysis assistance only. Past performance displayed in the dashboard does not guarantee future results.

股指

US/SPY- Financial Regime Index Swing Strategy Credits: concept inspired by EdgeTools Bloomberg Financial Conditions Index (Proxy)

Improvements: eight component basket, inverse volatility weights, winsorization option( statistical technique used to limit the influence of outliers in a dataset by replacing extreme values with less extreme ones, rather than removing them entirely), slope and price gates, exit guards, table and gradients.

Summary in one paragraph

A macro regime swing strategy for index ETFs, futures, FX majors, and large cap equities on daily calculation with optional lower time execution. It acts only when a composite Financial Conditions proxy plus slope and an optional price filter align. Originality comes from an eight component macro basket with inverse volatility weights and winsorized return z scores that produce a portable yardstick.

Scope and intent

Markets: SPY and peers, ES futures, ACWI, liquid FX majors, BTC, large cap equities.

Timeframes: calculation daily by default, trade on any chart.

Default demo: SPY on Daily.

Purpose: convert broad financial conditions into clear swing bias and exits.

Originality and usefulness

Unique fusion: return z scores for eight liquid proxies with inverse volatility weighting and optional winsorization, then slope and price gates.

Failure mode addressed: false starts in chop and early shorts during easy liquidity.

Testability: all knobs are inputs and the table shows components and weights.

Portable yardstick: z scores center at zero so thresholds transfer across symbols.

Method overview in plain language

Base measures

Return basis: natural log return over a configurable window, standardized to a z score. Winsorization optional to cap extremes.

Components

EQ US and EQ GLB measure equity tone.

CREDIT uses LQD over HYG. Higher credit quality outperformance is risk off so sign is flipped after z score.

RATES2Y uses two year yield, sign flipped.

SLOPE uses ten minus two year yield spread.

USD uses DXY, sign flipped.

VOL uses VIX, sign flipped.

LIQ uses BIL over SPY, sign flipped.

Each component is smoothed by the composite EMA.

Fusion rule

Weighted sum where weights are equal or inverse volatility with exponent gamma, normalized to percent so they sum to one.

Signal rule

Long when composite crosses up the long threshold and its slope is positive and price is above the SMA filter, or when composite is above the configured always long floor.

Short when composite crosses down the short threshold and its slope is negative and price is below the SMA filter.

Long exit on cross down of the long exit line or on a fresh short signal.

Short exit on cross up of the short exit line or on a fresh long signal, or when composite falls below the force short exit guard.

What you will see on the chart

Markers on suggestion bars: L for long, S for short, LX and SX for exits.

Reference lines at zero and soft regime bands at plus one and minus one.

Optional background gradient by regime intensity.

Compact table with component z, weight percent, and composite readout.

Table fields and quick reading guide

Component: EQ US, EQ GLB, CREDIT, RATES2Y, SLOPE, USD, VOL, LIQ.

Z: current standardized value, green for positive risk tone where applicable.

Weight: contribution percent after normalization.

Composite: current index value.

Reading tip: a broadly green Z column with slope positive often precedes better long context.

Inputs with guidance

Setup

Calc timeframe: default Daily. Leave blank to inherit chart.

Lookback: 50 to 1500. Larger length stabilizes regimes and delays turns.

EMA smoothing: 1 to 200. Higher smooths noise and delays signals.

Normalization

Winsorize z at ±3: caps extremes to reduce one off shocks.

Return window for equities: 5 to 260. Shorter reacts faster.

Weighting

Weight lookback: 20 to 520.

Weight mode: Equal or InvVol.

InvVol exponent gamma: 0.1 to 3. Higher compresses noisy components more.

Signals

Trade side: Long Short or Both.

Entry threshold long and short: portable z thresholds.

Exit line long and short: soft exits that give back less.

Slope lookback bars: 1 to 20.

Always long floor bfci ≥ X: macro easy mode keep long.

Force short exit when bfci < Y: macro stress guard.

Confirm

Use price trend filter and Price SMA length.

View

Glow line and Show component table.

Symbols

SPY ACWI HYG LQD VIX DXY US02Y US10Y BIL are defaults and can be changed.

Realism and responsible publication

No performance claims. Past is not future.

Shapes can move intrabar and settle on close.

Execution is on standard candles only.

Honest limitations and failure modes

Major economic releases and illiquid sessions can break assumptions.

Very quiet regimes reduce contrast. Use longer windows or higher thresholds.

Component proxies are ETFs and indexes and cannot match a proprietary FCI exactly.

Strategy notice

Orders are simulated on standard candles. All security calls use lookahead off. Nonstandard chart types are not supported for strategies.

Entries and exits

Long rule: bfci cross above long threshold with positive slope and optional price filter OR bfci above the always long floor.

Short rule: bfci cross below short threshold with negative slope and optional price filter.

Exit rules: long exit on bfci cross below long exit or on a short signal. Short exit on bfci cross above short exit or on a long signal or on force close guard.

Position sizing

Percent of equity by default. Keep target risk per trade low. One percent is a sensible starting point. For this example we used 3% of the total capital

Commisions

We used a 0.05% comission and 5 tick slippage

Legal

Education and research only. Not investment advice. Test in simulation first. Use realistic costs.

Average Daily Range [Blaz]Version 1.0 – Published October 2025: Initial release

1. Overview & Purpose

The Average Daily Range is an advanced volatility assessment tool designed to give traders a clear, real-time view of the market's expected daily movement. It calculates the average range between daily highs and lows over a user-defined historical period and projects this average onto the current trading session.

By visualising the potential high and low boundaries for the day, this indicator assists in setting realistic profit targets, managing risk effectively, and identifying when price action is becoming overextended relative to its recent volatility profile. It is an essential tool for day traders and swing traders across all markets, including Forex, Stocks, Crypto, Futures, and Commodities.

2. Core Functionality & Key Features

The indicator provides a dynamic, multi-faceted analysis of daily volatility:

Historical ADR Calculation: Automatically computes the Average Daily Range based on the specified number of previous trading days (configurable from 1 to 20).

Real-Time Range Tracking: Monitors and displays the current day's live price range as it develops.

Percentage Used Metric: Shows the percentage of the historical ADR that the current day's range has already consumed, providing an immediate gauge of remaining volatility potential.

Remaining Range Projection: Visually highlights the potential upward and downward movement remaining to meet the average range, displayed as semi-transparent areas on the chart.

Daily Open Reference: Plots customisable vertical separation lines and horizontal price lines at the daily open to clearly anchor the current session's price action.

3. Visual Components & Analytical Insights

A fully configured Average Daily Range setup displays several key analytical components that work together to provide a comprehensive volatility overview.

3.1. Information Table

A highly customizable data table provides a concise summary of all critical metrics at a glance:

Historical Ranges: Displays the individual daily ranges for the selected lookback period.

ADR Value: The calculated average range.

Today's Range: The live, developing range for the current session.

% Used: A colour-coded percentage (turning orange upon exceeding 100% and red upon exceeding 150%) showing how much of the average volatility has been consumed.

3.2. Visual Range Projections

Remaining Range Zones: When the current day's range is below the historical average, semi-transparent zones extend from the current day's extreme high and low, illustrating the additional movement required to reach the ADR. This provides an instant visual cue for potential target zones.

Daily Open Markers: Clean, customisable lines mark the start of each trading day (vertical line) and the daily open price (horizontal line), helping to contextualise intraday price moves.

4. Input Parameters and Settings

4.1. General Settings

Lookback: Set the number of days used to calculate the Average Daily Range (1-20).

Set Alert: Configure alerts to be notified when the current day's range consumes a significant portion (e.g., 100% or more) of the historical ADR.

4.2. Table Customization

Visibility & Style: Toggle the table and historical data on/off. Fully customise the header and body colours, text colours, border style, and font sizes.

Placement & Orientation: Precisely position the table anywhere on the chart (Top/Bottom/Centre, Left/Right) and choose between Horizontal or Vertical layout to best suit your chart layout.

4.3. Visual Style Controls

Remaining Range: Toggle the projection zones on/off and customise their colour and transparency.

Daily Open Markers: Independently control the visibility, colour, style, and width of the daily separation line and the open price line.

5. Protected Logic & Original Design

The Average Daily Range indicator incorporates proprietary logic for efficiently tracking intraday extremes, managing historical data arrays, and dynamically rendering visual elements. The closed-source nature of this tool protects the author's original code structure and optimisation techniques, particularly the real-time area fill projection logic for the remaining daily range and the dynamic table management system. This ensures the indicator remains performant and reliable while being freely accessible to the entire TradingView community.

6. Disclaimer & Terms of Use

This indicator, titled Average Daily Range , has been independently developed by the author. The code and its structural logic are original and were written entirely from scratch to reflect a unique and efficient approach to volatility analysis. The internal mechanics were written from scratch and are not based on any publicly available script or third-party code.

This tool is provided solely for educational and informational purposes. It is not intended as financial advice, investment guidance, or a specific recommendation to buy or sell any financial instrument. The indicator is designed to assist with technical analysis based on volatility but does not guarantee accuracy or profitability.

Trading financial markets involves significant risk, including the possibility of loss of capital. By using this indicator, you acknowledge and accept that you are solely responsible for any decisions you make and for all trading outcomes. No part of this script should be considered a signal or assurance of success in the market.

Implied Volatility RangeThe Implied Volatility Range is a forward-looking tool that transforms option market data into probability ranges for future prices. Based on the lognormal distribution of asset prices assumed in modern option pricing models, it converts the implied volatility curve into a volatility cone with dynamic labels that show the market’s expectations for the price distribution at a specific point in time. At the selected future date, it displays projected price levels and their percentage change from today’s close across 1, 2, and 3 standard deviation (σ) ranges:

1σ range = ~68.2% probability the price will remain within this range.

2σ range = ~95.4% probability the price will remain within this range.

3σ range = ~99.7% probability the price will remain within this range.

What makes this indicator especially useful is its ability to incorporate implied volatility skew. When only ATM IV (%) is entered, the indicator displays the standard Black–Scholes lognormal distribution. By adding High IV (%) and Low IV (%) values tied to strikes above and below the current price, the indicator interpolates between these inputs to approximate the implied volatility skew. This adjustment produces a market-implied probability distribution that indicates whether the option market is leaning bullish or bearish, based on the data entered in the menu:

ATM IV (%) = Implied volatility at the current spot price (at-the-money).

High IV (%) = Implied volatility at a strike above the current spot price.

High Strike = Strike price corresponding to the High IV input (OTM call).

Low IV (%) = Implied volatility at a strike below the current spot price.

Low Strike = Strike price corresponding to the Low IV input (OTM put).

Expiration (Day, Month, Year) = Option expiration date for the projection.

Once these inputs are entered, the indicator calculates implied probability ranges and, if both High IV and Low IV values are provided, adjusts for skew to approximate the option market’s distribution. If no implied volatility data is supplied, the indicator defaults to a lognormal distribution based on historical volatility, using past realized volatility over the same forward horizon. This keeps the tool functional even without implied volatility inputs, though in that case the output represents only an approximation of ATM IV, not the actual market view.

In summary, the Implied Volatility Range is a powerful tool that translates implied volatility inputs into a clear and practical estimate of the market’s expectations for future prices. It allows traders to visualize the probability of price ranges while also highlighting directional bias, a dimension often difficult to interpret from traditional implied volatility charts. It should be emphasized, however, that this tool reflects only the market’s expectations at a specific point in time, which may change as new information and trading activity reshape implied volatility.

Normalized Equity/Bond RatioThis indicator calculates a normalized equity-to-bond ratio over a 252-day lookback (~1 trading year) to assess risk-on vs. risk-off sentiment. It addresses the issue of direct ratios (e.g., SPY/TLT) being visually dominated by high nominal stock prices, which can obscure bond price movements.

A rising ratio indicates equities are outperforming bonds, suggesting risk-on conditions, while a declining ratio signals a shift toward bonds, often associated with risk-off behavior. The normalization ensures better visibility and comparability of the trend over time.

A ratio > 1 means the equity (e.g., SPY) is outperforming the bond (e.g., AGG) since the lookback. A ratio < 1 means bonds are outperforming.

Time-input Lines [MFX]THE LINES

The indicator plots a horizontal price line at a specified hour and minute (default: 9:30 - Equities Open). This line extends for a predefined number of minutes (default: 60 minutes - Opening Range Full Spectrum). Additionally, the indicator can plot two vertical lines: one at the selected start time and another at the end of the horizontal line.

STYLE

Both the horizontal and vertical lines are fully customizable, allowing adjustments to color, style, and width. For a cleaner, minimalist chart, any of these lines can be disabled.

TIMEZONE

By default, the indicator operates in the New York time zone, but this can be modified by unchecking the option and specifying a custom offset relative to UTC/GMT. The default offset is +2, corresponding to CEST (Central European Summer Time, UTC/GMT+2). The offset can be adjusted with up to 15-minute precision, where 0.25 represents a quarter of an hour.

US Market Strength Momentum [LG]This indicator is designed to analyze the relative strength momentum of two US market indices, the Russell 2000 and S&P 500, by calculating their rate of change over a 21-bar period and comparing them. The difference between the average rate of change for IWM and SPY is then plotted as a histogram, with green bars indicating positive momentum and red bars indicating negative momentum.

The indicator also includes a moving average line, calculated over a 200-bar period, which is plotted on top of the histogram. This moving average helps to smooth out the data and provide a clearer picture of the longer-term trend.

In this indicator, the strength of the Russell 2000 compared to S&P 500 is seen as a gauge of market participants' risk tolerance. When Russell outperforms the S&P, market participants are assumed to be taking on greater risk in search of greater beta. When the S&P outperforms Russell, the assumption is that market participants are fleeing to safer assets (in regards to equities indices). The time frame the indicator is viewed on as well as the size of the rate of change delta dictates the strength of the trend.

IOFin F-Score by zdmre🗣The IOFin F-Score is a discrete score between zero and ten that reflects ten criteria used to determine the strength of a firm's financial position.

🗣It is used to determine the best value stocks, with ten being the best and zero being the worst.

The IOFin F-Score broken down into the following categories:

Profitability

Equity, cash flow, liquidity, and source of funds

Operating efficiency

Criteria Include:

Price to book (P/B) lower than 3 (1 point)

Debt to Equity (D/E) lower than 0.5 (1 point)

Price to FreeCashFlow (P/FCF) equal to or lower than 20 (1 point)

Peg Ratio lower than 1 (1 point)

Sustainable Growth Rate higher than 0.3 (1 point)

Return on Assets (ROIC) higher than 0.07 (1 point)

Return on Equity (ROE) higher than 0.3 (1 point)

EnterpriseValue/Ebitda lower than 10 (1 point)

Quick Ratio equal to or higher than 1 (1 point)

Operating Margin higher than 0.15 (1 point)

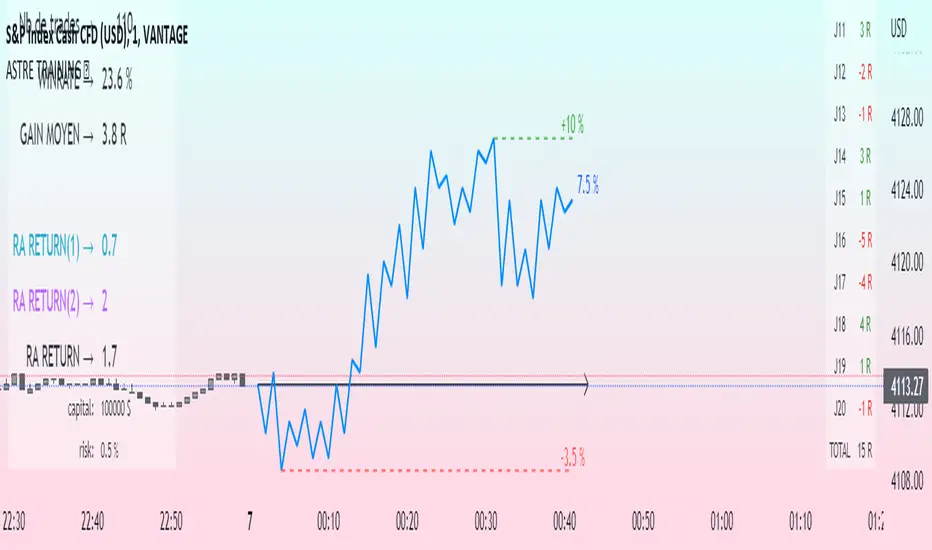

Challenge training (journal)Dynamic trading journal with equity curve display. Detailed results with prop firm objectives, editable, $/month estimation, possibility to compare two strategies.

one line in parameter = one trading day. 20 days max.

For each trading day, specify : The number of trades, the number of SL, the number of total winning RR.

A table at the bottom right summarizes the days and performances during the backtest in order to have an idea of the current performance.

The bottom left table summarizes the overall performance with some key information.

Depending on the number of days traded, a monthly "salary" is deducted, taking into account the prop firm commission.

there is the possibility to define a "Type" for each trading day, 1 or 2. It allows to compare in a binary way, example for type 1: when the high time frame structure is doing well and I am confident for scalping, otherwise type 2.

Again: type 1: SL shorter by 50%, type 2: normal SL etc..

the button "separate 1 and 2" allows to display two additional equity curves : type 1 and type 2. It allows to have a quick visual comparison on the impact of our parameter studied in our backtest on our performance. at the scale of the main equity curve

All the conditions to succeed in the challenge are adjustable in the parameters. The drawdown calculation has been simplified - in order not to have to put 80 trades in the parameters window, I have gathered them by "day", and pessimistically, we consider first the stoplosses and then the take profits, simplifying the performances of the day into "one losing trade" and "one winning trade" (graphically). It is a good compromise between quantity and quality.

Use "A random day trading" indicator to spice up your training.

I hope this will be useful for you to track your performance !

Financial IndicesThis indicator provides simple table at the top of the screen that shows the most important financial indices

1. Dividend Yield (DY), Fiscal quarter.

2. Earning per Share Growth (EG), Fiscal quarter.

3. Price-to=Book (PB) Ratio, Fiscal quarter.

4. Price-to-Earning (PE) Ratio, Twelve trailing Months.

Debt-to-Equity (D/E) Ratio, Fiscal quarter.

You can configure your preferences regarding the minimum and maximum acceptable values. Also, you can configure the table color of positive values or negative values

Equity Bond Currency DashboardDepicts demand-flow between Equities, Bonds and Currencies of 6 countries. Useful in tracking the flow of smart money and checking the dynamics of inter-connected markets.

Principle:

DXY lies at the heart of the diagram with usd-currency pairs of 5 countries connected to it. When demand for a currency increases it strengthens against Dollar. This is depicted by a line from DXY to the currency indicating demand flow from Dollar to the currency (DXY is only an indicative symbol for Dollar, the currency may not be part of the dollar index). Similarly when Dollar strengthens against the currency, demand flow is depicted by a line from the currency to DXY. Currency blocks are connected to Equity and Bond Yields of the respective countries. Equities and Bonds, when bought, takes the demand from the respective currencies and vice versa.

Overall, the demand flows in the direction of arrows. The flow is incomplete without commodities, import/export, interest/inflation rates of countries, however, the diagram most of the times explains why an asset class is performing the way it is.

Left side bar of each block is very similar to OHLC candles except for the following -

Instead of wicks, top and bottom of the bar represents high and low for the selected time-frame

Open and close are normalised for high and low

Bar border is red if close < prev.close, green if close >= prev.close

Other notes:

The diagram requires at least 200 bars in the chart to render. Please select the symbol and time-frame that contain at least 200 bars.

The diagram requires a live market to render the flow. To check flows on historical bars, set the option from settings.

Desired indices could be selected for countries of choice. Default settings point to futures wherever possible to have the markets live simultaneously across the countries.

Yield Curve (2-10yr)Yield curve of the 2-10 year US Treasury Bonds, with over 50 years of history.

The Yield Curve is the interest rate on the 10 year bond minus the 2 year bond.

When it inverts (crosses under 0) a recession usually follows 6-12 months later.

It's a great leading indicator to identify risk in the macroeconomic environment.

Financial MetricsGives a sneak peak into some of the important financial ratios described below:

1. P/E : price to earnings ratio (Green when P/E<15)

2. PEG: Price to earnings growth ratio (Green when PEG<1)

3. P/S: Price to sales ratio (Green when P/S<2)

4. EV/FCF: Enterprise Value to Free Cashflow ratio

5. OPM: Operating Profit Margin % (Green when OPM>15%)

6. D/E: Debt to equity ratio (Green when D/E<1)

7. ROE: Return on equity % (Green when ROE>15%)

8. Div_Yield: Dividend yield

Disclaimer: All the limits defined are based on the widely accepted general values, but are subjective to particular sector or group of stocks. For example IT stocks command higher valuation than cyclical stocks like metal. So Compare with other stocks of the same sector to reach any conclusion.

Morningstar Equity Style Box HeatmapStyle boxes are a classification scheme created by Morningstar. They visually provide a graphical representation of investing categories for equity investments. A style box is a valuable tool for investors to use when determining asset allocation.

There are 9 categories:

Large Value, Large Blend, Large Growth

Medium Value, Medium Blend, Medium Growth

Small Value, Small Blend, Small Growth

The strength of the 9 categories are found by using 9 Vanguard ETF's that follow the respective CRSP index of their category.

Silen's Financials Fair ValueIt is finally here! 🔥 My 3rd and most important script in my Financial series! 🚀

Ever imagined to see all fundamentals (or many that is) combined into one indicator that is right on your chart, showing you how your favorite stock is trading compared to its fundamentals?

Well, here is your answer! 📡

____________________________________________________________________________________________

This script shows you my own personal interpretation of fair value, based solely on the financial fundamentals of a company compared to market averages.

I don't believe that certain sectors of the market should be priced higher than others. If you look at historical data you'll see that favored sectors always rotate - placing insanely high P/E multiples on some sectors. Once they are "out" and people rotate away from those sectors you're left with nothing but the naked fundamentals that matter. So, you'll see many companies, that have been doing well on paper, see their share price decline by 70-90% for no other reasons than people favoring other sectors.

That's why it's even more important to focus on fair value that is solely fundamentals-based. Know when your stock gets to expensive. 🤯

____________________________________________________________________________________________

To give you some examples:

- Most Megacaps trade at historically high valuations, several times my fair value. Those include AAPL, MSFT, NVDA, AMZN, TSLA, JPM, TSM, V and so on. And no, in the past they partially traded below (my) fair value.

- Most Cybersecurity / Cloud companies are trading at truly massive multiples of my fair value. (NET, DDOG, etc)

- Many Smallcaps & Midcaps are trading several multiples (OESX, CODX, QFIN) below my fair value. And no, in the past they partially traded above (my) fair value.

Ok, so much about the market. You ultimately decide how much you want to orientate on fair value. 👨🏫

____________________________________________________________________________________________

This fair value indicator (purple line):

Takes the P/E rate of the company and compares it to the market (50% weight)

Takes the P/S rate of the company and compares it to the market (50% weight)

Then adds boni and mali f or debt/equity rates and debt and equity itself

Also looks at past growth and calculates future P/E and P/S rates which adds , in some cases, value to the fair value (green line)

Also compares how historical valuations have behaved compared to fair value and simulates a fair value guideline (dark blue line)

____________________________________________________________________________________________

This script is part 3️⃣ of a series of indicators that work well together.

Script 1️⃣ of the series is:

P/E & P/S Rates

Script 2️⃣ of the series is:

Debt & Equity

If you use all 3 scripts together it will look like this, giving you truly deep and simple information about the fundamentals of a company:

Example 1 - AMD

Example 2 - HZO

Example 3 - APPS

I hope this script makes your investing and stock picks a lot easier! 🔆💹🕗

Disclaimer: Fair value is always subjective. There are many different approaches to fair value. This one is only my personal interpretation.

Disclaimer 2: This script works only for the Day-Timeframe.

Disclaimer 3: This script uses 17,5 P/E and 3,0 P/S as market averages. The actual average keeps changing but, historically speaking, these seemed to be good numbers.

Feel free to share your thoughts and feedback! 🙃

Auxiliary Equity Configurator (AXE)Auxiliary Equity Configurator (AXE) is a whole new level money management auxiliary that calculates statistically preferable lot based on the Account balance, Winning rate, Risk reward ratio, and Kelly multiplier configured a priori in the input panel.

On the chart, RR visualization bands, Expected balance history matrix in the worst successive trading loss (for displaying how many times you can trade with a given lot at simple/compound interest), and Info-table for the calculation details are shown.

Regarding RR visualization bands, whenever the Tolerable drawback input changes, the proper lot is calculated based on the given data. You can easily access how many lots you should possess and the take-profit/stop-loss price to set. A tolerable drawback can be placed in the quoted currency rate of the displayed chart, except the forex and part of CFD symbols (Gold, Silver, Platinum, WTI oil, Brent oil, Natural gas, and more in the future!) that is valued in Pips. Parameters are configurable in suit with the broker you are using. Also, RR visualization bands are brilliantly interactive, thanks to pine v5 interactive scripts.

The currency for Account balance and Tolerable drawback is automatically converted to USD for internal calculation; therefore, no mess-ups around thinking currency value conversion whatsoever! The design for each tool is highly customizable, too.

Unleash yourself from consuming the colossal amount of time thinking of money management with AXE!

Silen's Financials Debt & EquityThis Script shows Debt (red) & Equity (green), as well as Total Equity and Net Income in a preformatted way for a symbol. Total revenue's and Net income's visibility is turned off by default and can be activated in the indicator settings. 🍳

Disclaimer: Any content in this script can be completely replicated by using Tradingview's Build-In Financial Indicators: Total debt, Total equity, Net income and Total revenue. It requires a lot of formatting work to get them to this state though. 👌

However, you are going to need 4 Financial Indicators clogging 🚽 your screen. With this indicator you have them preformatted as an overlay on your chart so you know exactly what's going on with your ticker's financials. 💰

I recommend only using Debt & Equity OR Total Equity & Net Income together. Although displaying all 4 indicators together is possible, it will make your chart quite messy.

This is how the indicator looks like for Total equity and Net Income:

This Script (2) is part of a Series that will contain 3 scripts to help you easily evaluate if a stock is trading in harmony with its fundamentals or not. ☯

Script 1 already exists:

Script 3 will be a Fair Value Indicator. 📣

Script 1 and 2 combined will look like this: 🌄

If you have any questions, let me know! 🙂

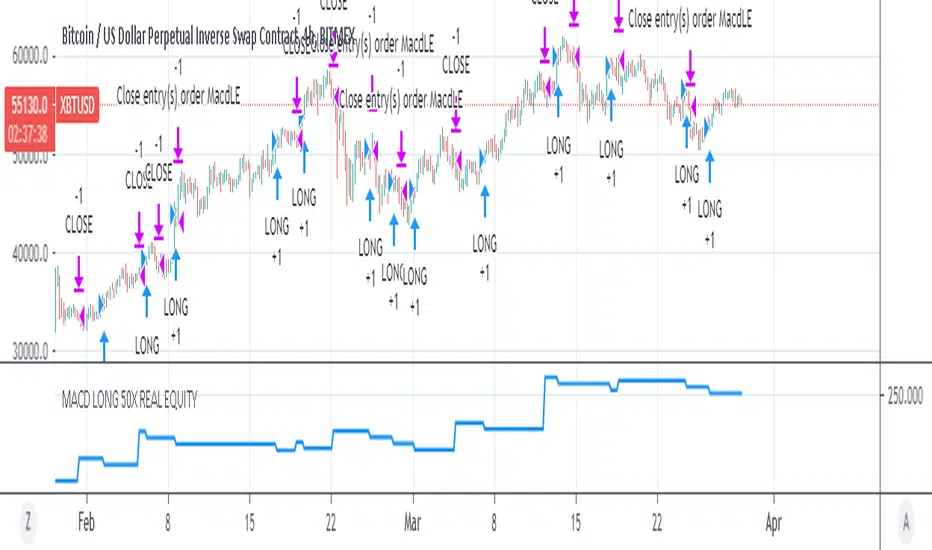

MACD 50x Leveraged Strategy Real Equity Simulation Hello, I wrote this script to merge the two scripts I shared before.

The aim here is to see the real value of the state of the capital as a result of leveraged transactions and to combine both long and short directions.

Scripts :

MACD Long 50x Leverage Strategy :

MACD Short 50x Leverage Strategy :

The parameters have not changed so they are the same as the previous two scripts:

Adding margin: Forbidden or not specified. (Add Margin : No)

Position Size : %1 (0.01) (For each trade)

Stop-Loss : %2 (For each trade)

Long : Crossover(delta,0) (Standard MACD)

Long Exit : Long Stop Level or Short Entry

(In the case of Long Stop, all trades are closed and no positions are opened in short direction.)

Short : Crossunder(delta,0) (Standard MACD)

Short Exit : Short Stop or Long Entry

(In the case of Short Stop, all trades are closed and no positions are opened in the long direction.)

NOTE :

This is a simulation made using standard parameters, showing the state of the balance in very simple rules with leveraged transactions only.

The nice thing here is the direct observation of the results by making modifications on the strategy parameters.

Regards.

P1 FundamentalsP1 is because to me, this is a priority 1 indicator, so I have P1 and P2 indicators ordered on the favorite list.

What can you check on the selection pane?

On “period”, you can show the data related to:

the fiscal quarters

or the fiscal years.

You can select a pack of financial data that I have organized in sections:

Revenue & earnings

EPS & DPS (EPS, EPS estimate, DPS and dividend payout ratio )

Debt (total debt, total equity and cash & equivalents)

Returns (ROE, ROIC, ROA and R&D revenue to ratio)

I recommend to just select one of them, in other case the chart is a mess.

Any feedback on the code is welcome!!

MACD 50x Leveraged Short Strategy with Real Equity

Hello there ,

Short version of the Macd Long strategy.

MACD Long strategy:

Adding margin: Forbidden or not specified. (Add Margin : No)

Position size: (for each trade) 1%

Stop-Loss: (2% Above Entry Level)

Long: macd crossunder

Exit: macd crossover

Or ofc touching the stop-Loss value as predicted.

These strategies are just examples.

The goal is to observe true equity and equity change.

Warning: This strategy simulation is for Short direction only.

Regards.

MACD 50x Leveraged Long Strategy Results with Real Equity Hello there.

I was looking for a way to simulate leveraged transactions in Tradingview and this script came out.

You can examine the equity graph without looking at the strategy results.

Thus, the facts will come to light.

Strategy parameters:

Adding margin: Forbidden or not specified. (Add Margin : No)

Position size: (for each trade) 1%

Stop-Loss: (2%)

Long: macd crossover

Exit: macd crossunder

Or ofc touching the stop-Loss value as predicted.

Warning: This strategy simulation is for Long direction only.

Regards.

Equity chart [LM]Hey Guys,

I have created draft version of chart where you can put your position amount and position price and position date for each entry and it will chart your equity as candle stick chart. There are currently possible to include 4 positions but you can add as many you like by modyfing the code.

It will calculate your average entry based on your input and in date where you add other entry it will create gap. I have already plan to include there also leverage on each position. The idea is that you should trade your equity and with this indicator you will be able to create your custom indicator based on equity chart and not price chart.

!! Unless you will enter position nothing will be rendered

Indicator is under breadth indicator because didn't know where to put it.

I release this script for collaboration and improving the idea with new features

Cheers,

Lukas

Swing Reversal IndicatorSwing Reversal Indicator was meant to help identify pivot points on the chart which indicate momentum to buy and sell. The indicator uses 3 main questions to help plot the points:

Criteria

Did price take out yesterday's high or low?

Is today's range bigger than yesterday? (Indicates activity in price)

Is the close in the upper/lower portion of the candle? Thus, indicating momentum in that direction

This indicator was built to help me find pivot points for directional options trading however can be used for equities and forex swing trading and other strategies. Used in conjunction with a BB extreme can provide good setups.

Alerts are available for both the long and the short positions and the indicator will repaint as price moves.

The character Plotted can be changed in the settings

The size of the candle area can be changed as well if you want to tighten/loosen the trigger points based on the third question above.